Content Intelligence Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.59 Billion |

| Market Size (2031) | USD 9.15 Billion |

| Growth Rate (2026 - 2031) | 28.74% CAGR |

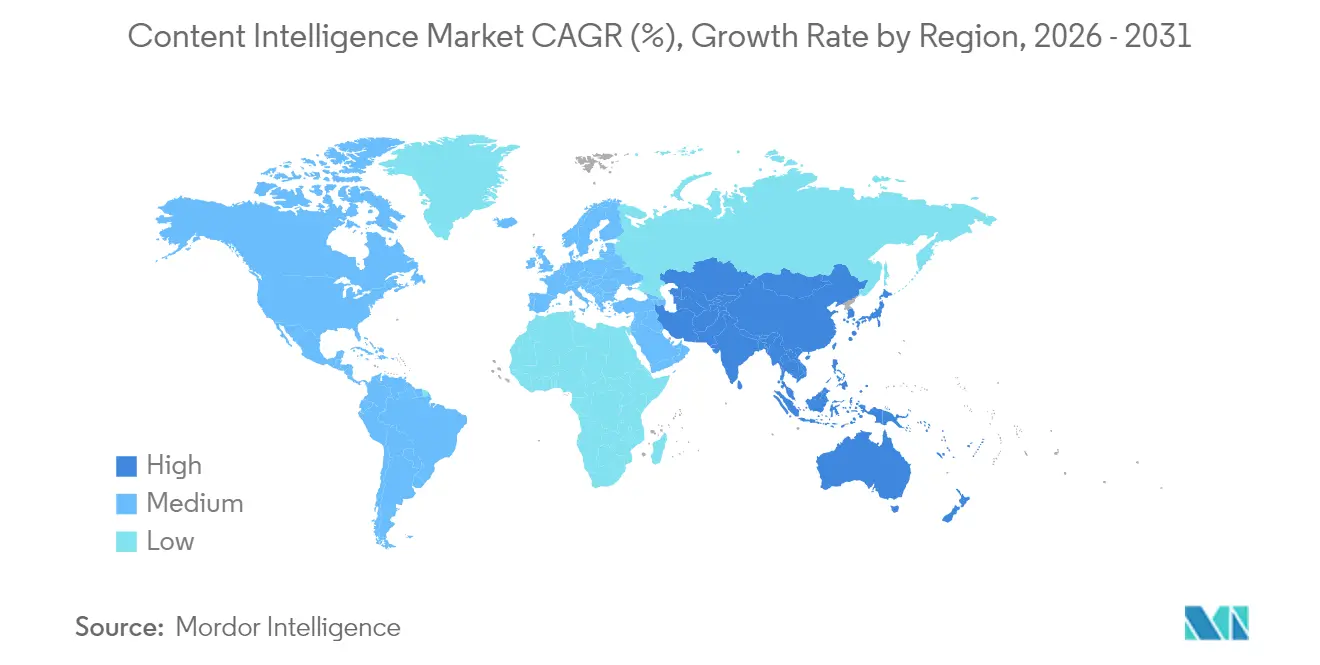

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

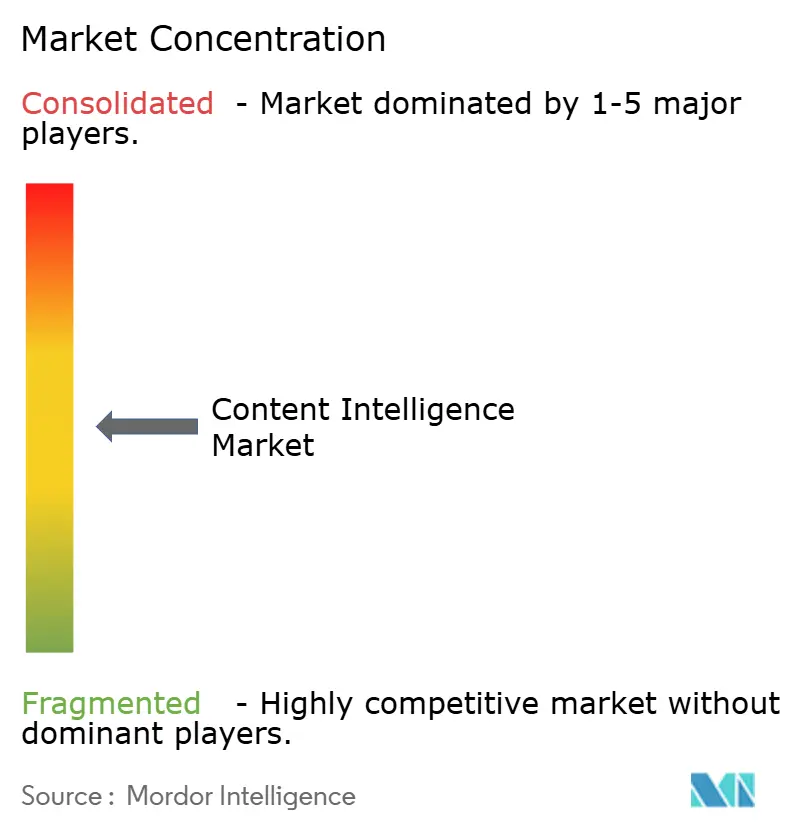

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Content Intelligence Market Analysis by Mordor Intelligence

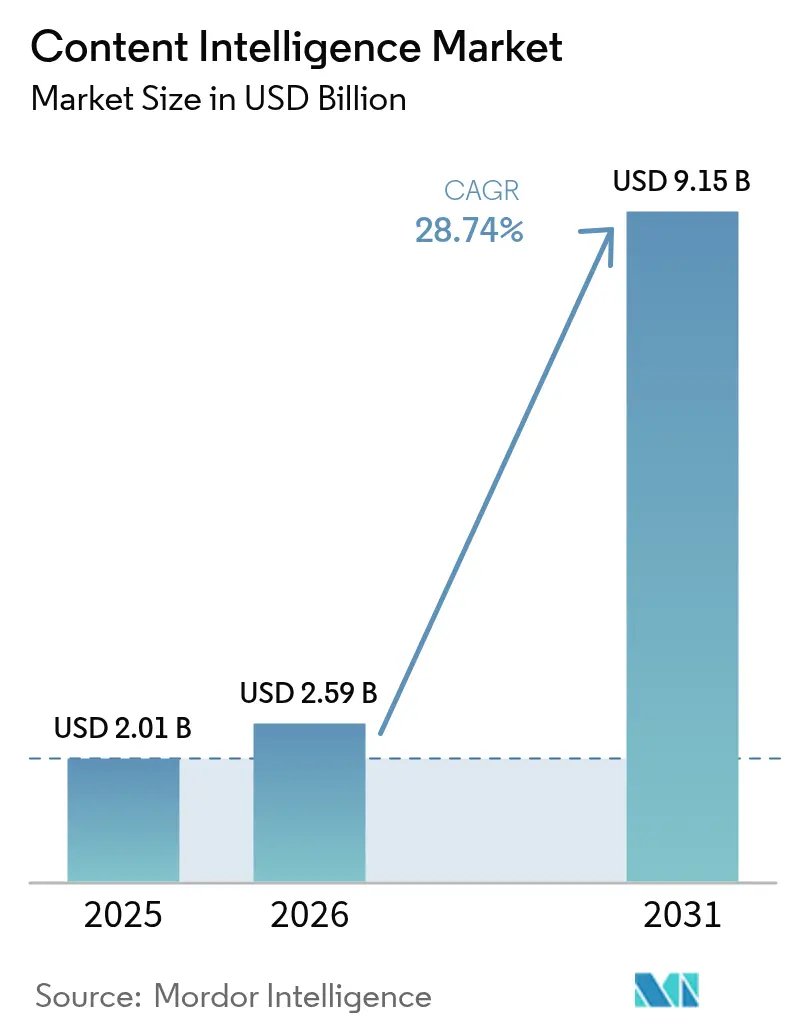

The Content intelligence market size is expected to grow from USD 2.01 billion in 2025 to USD 2.59 billion in 2026 and is forecast to reach USD 9.15 billion by 2031 at 28.74% CAGR over 2026-2031. This growth trajectory mirrors enterprises’ need to apply AI-driven content optimization to rising data volumes and heightened customer expectations. Mandatory WCAG 3.0 accessibility rules, the rapid shift to video-first engagement, and the availability of cost-efficient small language models are reinforcing near-term adoption. Vendors that deliver cloud scalability, hybrid data-sovereignty options, and outcome-based pricing gain an edge as organizations focus on measurable returns. Competitive dynamics intensify as synthetic audience data and zero-party targeting unlock granular personalization, prompting traditional content management providers to integrate generative AI to keep pace.

Key Report Takeaways

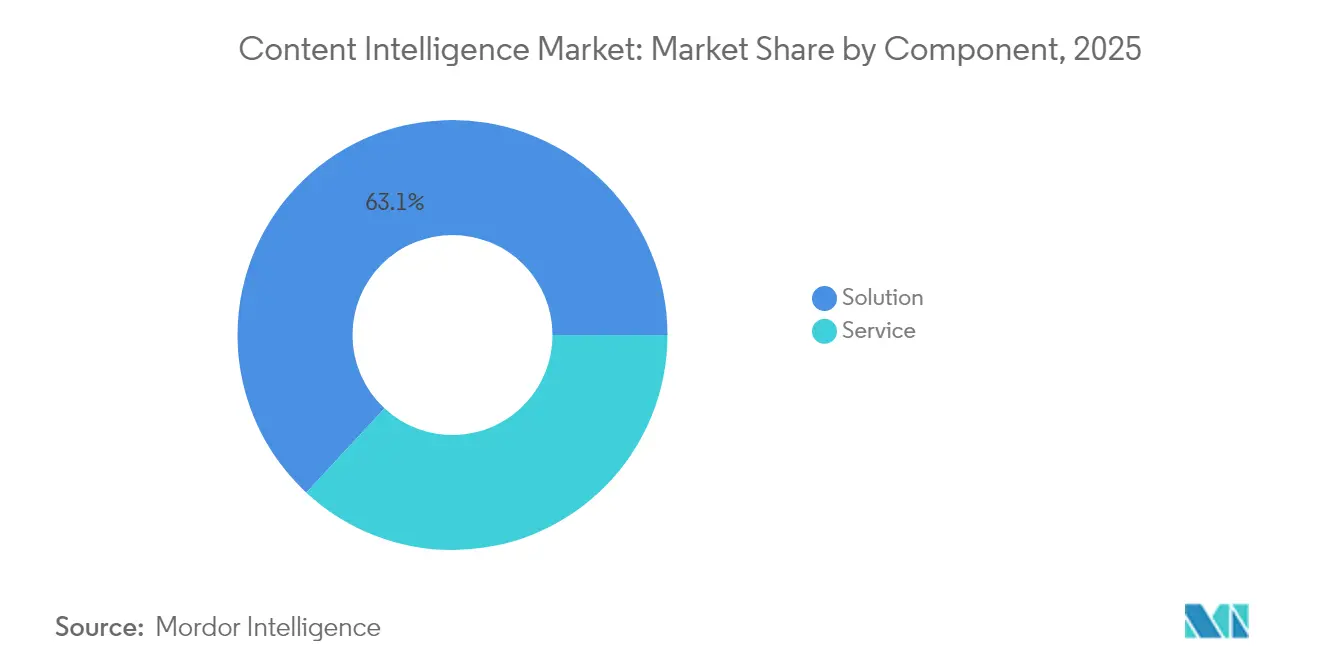

- By component, Solutions retained 63.10% of the Content intelligence market share in 2025, while Services is forecast to rise at a 33.02% CAGR through 2031.

- By deployment, cloud led with 76.20% share in 2025; the hybrid segment is expanding at a 35.95% CAGR to 2031.

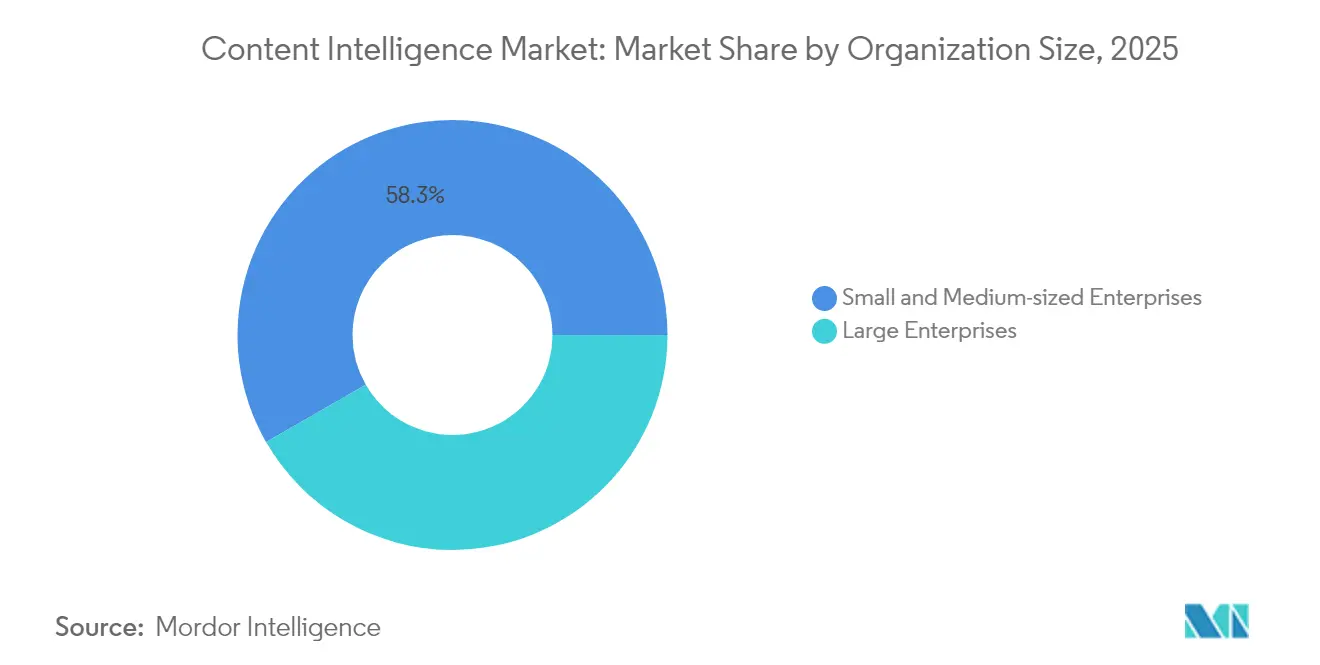

- By organization size, SMEs held 58.30% of the market in 2025 and are advancing at a 34.22% CAGR to 2031.

- By end-user vertical, Media and Entertainment accounted for 25.60% revenue in 2025, whereas Healthcare and Life-sciences is growing fastest at a 32.02% CAGR to 2031.

- By geography, North America contributed 37.40% of 2025 revenue, while Asia-Pacific is forecast to grow at a 33.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Content Intelligence Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Demand for personalised, data-driven content at scale | +8.2% | Global, with early gains in North America and EU | Medium term (2-4 years) |

| AI/ML integration across martech stacks | +7.8% | Global, spill-over from APAC to MEA | Short term (≤ 2 years) |

| Omnichannel content explosion on video and social platforms | +6.4% | APAC core, expanding to North America | Medium term (2-4 years) |

| Accessibility regulations (WCAG 3.0) accelerating adoption | +4.1% | North America and EU, with compliance spillover globally | Long term (≥ 4 years) |

| Deployment of in-house small language models lowering TCO | +5.7% | Global, with enterprise concentration in developed markets | Short term (≤ 2 years) |

| Synthetic audience data unlocking zero-party targeting | +3.9% | North America and EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for personalised, data-driven content at scale

Enterprises now recognize that generic messaging struggles to cut through sophisticated consumer filters. Adobe’s Customer Experience Orchestration platform demonstrated engagement gains of up to 30% for banner variants in 2024.[1]: Adobe, “Introducing New Generative AI Capabilities in Adobe Experience Manager Sites,” business.adobe.com The move toward first-party data strategies gives firms proprietary fuel for ever-more-accurate personalization models. Organizations using content intelligence market platforms report 40-70% faster creation cycles and higher relevance scores, confirming that scale and quality are no longer trade-offs. Financial services, healthcare, and retail all cite similar benefits as AI tailors content to regulatory or customer nuances. The emphasis on performance measurement accelerates spending on analytics modules that quantify engagement lifts. These dynamics strengthen the content intelligence market outlook for mid-term growth.

AI/ML integration across martech stacks

Generative AI has shifted from bolt-on feature to core infrastructure. Adobe’s GenStudio unifies creation, brand governance, and analytics in one workflow, showing how AI removes hand-offs that slowed production.[2]Adobe, “Adobe Expands GenStudio Content Supply Chain Offering for Marketing and Creative Teams,” news.adobe.com OpenText’s Titanium X combines 15 AI aviators and more than 100 agents, promising USD 1 billion in savings over a decade for process-heavy clients. Consolidation pressures legacy vendors to upgrade or risk displacement by AI-native entrants. Firms now budget for continuous model tuning, agent orchestration, and data-ops rather than one-time licenses. Early adopters of integrated stacks credit AI orchestration for real-time A/B testing and fully automated campaign iteration. This integration drives a sustained uplift across the content intelligence market through 2030.

Omnichannel content explosion on video and social platforms

Short-form video, live commerce, and interactive media multiply content variants per campaign. Adobe Premiere Pro’s Generative Extend now automates editing and localization across formats and languages, trimming adaptation times by up to 80%.[3]Adobe, “Adobe Expands GenStudio Content Supply Chain Offering for Marketing and Creative Teams,” news.adobe.com Asia-Pacific’s creator economy, valued at USD 135.2 billion in 2023 with 207 million contributors, signals the scale of assets that require AI assistance. Brands leveraging the content intelligence market achieve faster platform compliance, timely reactions to algorithm shifts, and consistent brand voice. Social commerce growth drives demand for clip-level optimization, thumbnail generation, and noise-reduction algorithms. Together these factors sustain high growth momentum, especially in APAC, over the medium term.

Accessibility regulations (WCAG 3.0) accelerating adoption

WCAG 3.0 moves from rule-based criteria to outcome-based testing, making manual inspection insufficient. Acquia’s early analysis underscores the need for AI engines that score color contrast, alt-text quality, and navigation patterns in real time. US rules effective June 28, 2025, mandate WCAG 2.1 Level AA today, with WCAG 3.0 on the horizon, pushing firms to embed accessibility checks into every asset. Integrated accessibility modules inside content intelligence market platforms cut remediation costs by 60-80% and lower legal risk. Vendors combine automated audits with natural-language suggestions so editors can correct issues inside their workflow. Long-term compliance pressure ensures steady uptake even after initial deadlines pass.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data-privacy and GDPR / DMA compliance costs | -4.3% | EU core, expanding globally through regulatory spillover | Long term (≥ 4 years) |

| Shortage of content-AI talent and change-management gaps | -3.7% | Global, with acute shortages in developed markets | Medium term (2-4 years) |

| GPU/ASIC supply-chain bottlenecks inflating inference costs | -2.8% | Global, with manufacturing concentration in APAC | Short term (≤ 2 years) |

| Hallucination-driven brand-liability risks | -2.1% | Global, with regulatory focus in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and GDPR / DMA compliance costs

OpenAI’s EUR 15 million fine in 2025 illustrates the financial exposure tied to data misuse. New European Data Protection Board guidance obliges firms to justify every personal-data use in training, monitoring, and inference. Enterprises adopting the content intelligence market must therefore invest in privacy-preserving architectures, on-premise deployments, and synthetic data pipelines. Compliance audits add 25-40% to total cost of ownership, slowing buying cycles in heavily regulated sectors. Despite the drag, firms accept higher costs to retain EU market access.

Shortage of content-AI talent and change-management gaps

A limited pool of professionals who combine AI, content strategy, and governance extends project timelines by 6-12 months in many organizations. Resistance from creative teams that perceive automation as a threat adds further friction. Successful rollouts pair upskilling programs with phased automation to build trust. Vendors supplement software with managed services to close skill gaps, yet scarcity remains a medium-term brake on the content intelligence industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Implementation Excellence

Services captured rapid growth with a 33.02% CAGR through 2031 even though Solutions retained 63.10% of 2025 revenue. The Content intelligence market size for services is projected to climb sharply as companies need consulting, workflow redesign, and change management alongside tooling. Larger regulated enterprises turn to specialized integrators that align AI output with compliance obligations. Case in point, Adobe’s collaboration with PwC targets heavily regulated verticals to bundle platform, data governance, and domain expertise. Solutions revenue remains sizable, yet commoditization of basic AI features tempers its pace. Vendors differentiate by embedding industry-specific models and low-code orchestration, yet buyers still lean on service partners to translate capability into business value. That dependence underpins sustained Services acceleration across the content intelligence market.

Implementation success metrics underscore the shift: organizations pairing software and managed services report 20-30% higher adoption rates and quicker time-to-value than tool-only deployments. Subscription-based services now account for 76% of Veritone’s customer contracts, signaling a pivot toward outcome-centric engagements. Over the forecast horizon, mature enterprises will rebalance budgets toward advisory, model fine-tuning, and continuous optimization as AI moves from pilot to production.

By Deployment: Hybrid Architectures Balance Performance and Sovereignty

Cloud remained dominant at a 76.20% share in 2025, but hybrid configurations now post the fastest trajectory at 35.95% CAGR. The Content intelligence market share for hybrid setups rises as firms split sensitive data onto local clusters while keeping burst workloads in public clouds. Hybrid rollouts lower latency for real-time personalization and meet jurisdictional data mandates without forgoing elastic scaling. Early adopters have measured 30-50% operating-expense savings compared with all-cloud when processing heavy multimedia assets. Vendors respond with containerized micro-services that slide easily between environments, shielding users from infrastructure complexity.

On-premise instances hold niche value for defense and highly regulated healthcare customers. The release of small, domain-tuned language models that perform well on CPU cores further reduces reliance on GPU-rich data centers, making local inference practical. Over time, multi-cloud control planes that abstract policy, model versioning, and usage metering will become standard. This flexibility cements hybrid as a mainstream choice across the content intelligence market.

By Organization Size: SMEs Lead Adoption and Growth

SMEs controlled 58.30% of 2025 revenue and generate the steepest growth at a 34.22% CAGR. Consumption-based SaaS levels entry barriers, enabling smaller firms to match enterprise-grade personalization with lean teams. The content intelligence market size for SME solutions is expanding as vendors introduce intuitive dashboards, pre-set workflows, and template libraries that cut configuration overhead. For many SMEs, AI automation is not optional but a requirement to compete against larger budgets. Automated captioning, image generation, and basic editorial checks free staff to focus on strategic content.

Large enterprises retain significant spending power, yet intricate compliance demands and cross-department coordination slow their rollouts. Consequently, SME volumes help vendors amortize R&D and sharpen ease-of-use features that later benefit all tiers. Competitive pressures will keep vendors pursuing price-transparent plans favored by small businesses, thereby sustaining the dual leadership of SMEs in adoption and growth.

By End-User Vertical: Healthcare Accelerates Beyond Media Leadership

Media and Entertainment held the most revenue at 25.60% in 2025, exploiting AI for audience analytics, automated editing, and multi-language localization. Healthcare-and Life-sciences leads in pace with a 32.02% CAGR. Clinics and pharmaceutical firms need automated patient education, clinical documentation, and compliance filings. Integrated language models that translate medical jargon into lay summaries shorten turnaround and reduce staff workload. Early pilots show 40% faster discharge-summary preparation and improved patient satisfaction scores.

In financial services, banks use AI-curated content to streamline compliance reports and customer onboarding. Government bodies, such as Singapore’s Ministry of Manpower, employ conversational agents for dispute resolution, achieving a 500% jump in self-service outcomes. Manufacturing, IT, and telecommunications sectors adopt AI for product documentation and support chat, while retail leans on automated catalog descriptions and localized offers. Diversifying use cases reinforce steady vertical expansion within the content intelligence market.

Geography Analysis

North America generated 37.40% of 2025 revenue thanks to early enterprise AI rollouts and deep cloud infrastructure. The region maintains clear leadership, yet growth stabilizes as large enterprises shift from experimentation to optimization. The Content intelligence market size in North America climbs steadily, supported by regulatory pushes for accessibility and rising zero-party data strategies. Vendor ecosystems cluster around established tech hubs, securing venture funding and fostering partnerships with system integrators.

Asia-Pacific exhibits the fastest pace at 33.84% CAGR, driven by national AI programs and a flourishing creator economy that fuels demand for multilingual, multi-platform content. Local start-ups launch lightweight models fine-tuned for regional languages, helping brands localize at scale. Hybrid cloud adoption also rises where data-residency rules coexist with cost pressures. These forces gradually chip away at North American dominance, although the two regions together still command most of the content intelligence market.

Europe shows resilient expansion as GDPR and the forthcoming EU AI Act compel enterprises to adopt content governance and explainability tooling. Many firms choose hybrid or on-premise deployments to align with stringent data-sovereignty mandates. South America and the Middle East and Africa remain nascent but attractive; improved broadband and government digitization plans create green-field opportunities for SaaS providers. Global penetration confirms that AI-enabled content intelligence is trending from early adopter privilege toward mainstream necessity.

Competitive Landscape

Competition is moderately fragmented, with no single vendor holding overwhelming sway. Adobe, Microsoft, and OpenText marshal large-scale R&D budgets and broad suites that combine creative tools, experience platforms, and enterprise agents. Their integrated ecosystems, exemplified by Adobe’s GenStudio and Firefly, appeal to buyers seeking one-stop solutions. Mid-tier specialists such as Acrolinx and Veritone counter by focusing on linguistic quality, domain-specific models, or media-centric pipelines. Start-ups highlight automation depth and rapid iteration to capture unmet niches.

M&A activity remains brisk as traditional content management vendors absorb AI start-ups to close feature gaps. Partnerships with global consultancies position platform providers to deliver full-stack solutions that join software with advisory. Competitive advantage increasingly rests on model governance, fine-tuning ease, and certification for regulated industries rather than core content management functions, which are now table stakes. Buyers scrutinize proof-of-value pilots, reference architectures, and vendor roadmaps before committing to multi-year deals. This market structure supports innovation, yet consistent performance and compliance credentials determine long-term share gains across the content intelligence market.

Content Intelligence Industry Leaders

Adobe Inc.

OpenText Corporation

Semrush Holdings Inc

Acrolinx GmbH

Veritone Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Perplexity AI proposed a USD 50 billion merger with TikTok US operations.

- May 2025: IgniteTech acquired Khoros, adding AI-powered social engagement for 2,000 corporate clients.

- March 2025: Adobe released Experience Platform Agent Orchestrator for AI-driven customer experience agents.

- March 2025: GSPANN acquired Zorang ContentHubGPT to bolster retail and manufacturing e-commerce content.

Global Content Intelligence Market Report Scope

Content intelligence refers to systems and software solutions that leverage technological advances such as Big Data, natural language processing, and AI to transform raw content data into actionable insights for content makers to drive content strategy.

Thecontent intelligence market is segmented by component (solution, services), deployment (cloud, on-premise, hybrid), organization size (smes, large enterprises), end-user vertical (media and entertainment, government and public sector, bfsi, it and telecom, manufacturing, healthcare and lifesciences, retail, other end-user verticals), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solution |

| Service |

| Cloud |

| On-premise |

| Hybrid |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Media and Entertainment |

| Government and Public Sector |

| Banking, Financial Services and Insurance (BFSI) |

| IT and Telecommunications |

| Manufacturing |

| Healthcare and Life-sciences |

| Retail and e-Commerce |

| Others |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Component | Solution | |

| Service | ||

| By Deployment | Cloud | |

| On-premise | ||

| Hybrid | ||

| By Organisation Size | Small and Medium-sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-user Vertical | Media and Entertainment | |

| Government and Public Sector | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| IT and Telecommunications | ||

| Manufacturing | ||

| Healthcare and Life-sciences | ||

| Retail and e-Commerce | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the content intelligence market?

The market is valued at USD 2.59 billion in 2026 and is projected to hit USD 9.15 billion by 2031 at a 28.74% CAGR.

Which region shows the fastest growth in content intelligence adoption?

Asia-Pacific leads with a 33.84% CAGR through 2031, propelled by national AI strategies and a booming creator economy.

Why are services outpacing solutions in growth?

Enterprises realize ROI depends on implementation expertise, driving the services segment to a 33.02% CAGR versus commoditizing software tools.

How do WCAG 3.0 regulations influence market demand?

Outcome-based accessibility rules require automated monitoring, prompting firms to embed AI-powered compliance checks and accelerating platform adoption.

What deployment model is gaining traction alongside cloud?

Hybrid architectures are rising at a 35.95% CAGR as organizations blend cloud scalability with on-premise data sovereignty.

Which vertical is expanding fastest beyond media and entertainment?

Healthcare & Life-sciences is growing at a 32.02% CAGR due to patient-centric content needs and stringent documentation requirements.

Page last updated on: