Content Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

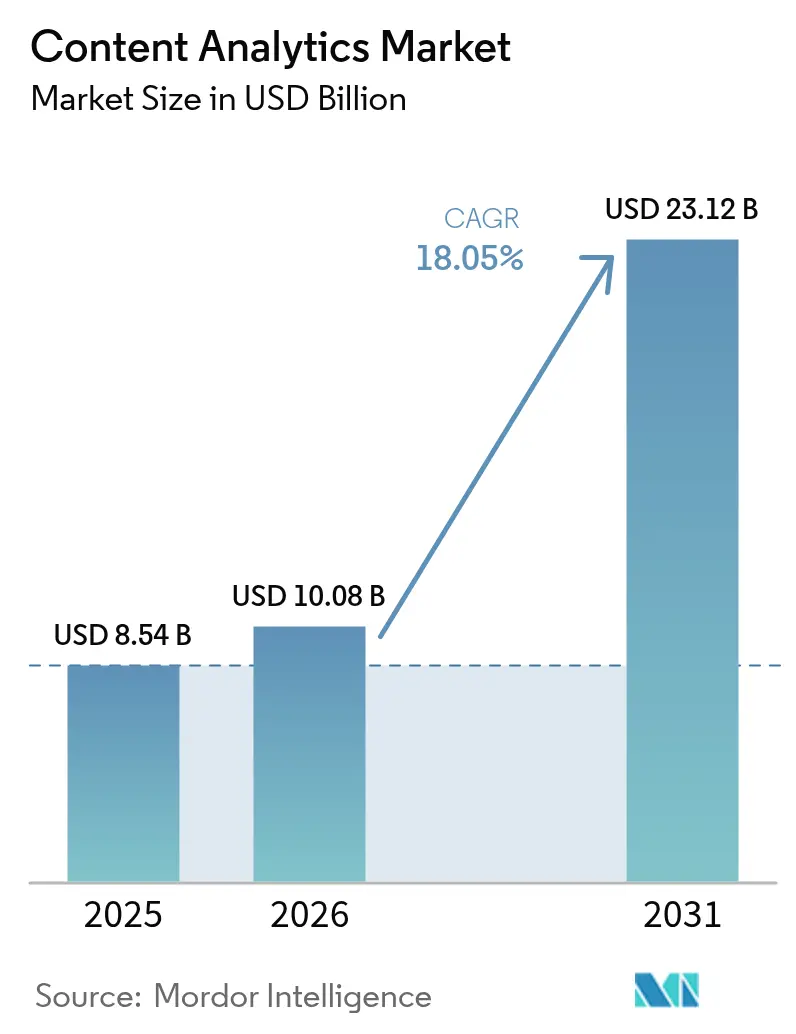

| Market Size (2026) | USD 10.08 Billion |

| Market Size (2031) | USD 23.12 Billion |

| Growth Rate (2026 - 2031) | 18.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Content Analytics Market Analysis by Mordor Intelligence

The Content Analytics Market size was valued at USD 8.54 billion in 2025 and estimated to grow from USD 10.08 billion in 2026 to reach USD 23.12 billion by 2031, at a CAGR of 18.05% during the forecast period (2026-2031). Accelerating cloud migration, rapid adoption of multimodal AI, and the convergence of vector search with semantic embedding technologies are reshaping how enterprises extract value from unstructured information. Public cloud deployments, real-time social listening, and large-language-model-powered “knowledge mining” pipelines are lowering entry barriers and encouraging experimentation. At the same time, demand is rising for hybrid architectures that balance data-sovereignty mandates with the scale advantages of hyperscale AI platforms. Intensifying competition among retail, media, and BFSI incumbents is pushing vendors toward verticalized solutions that promise faster time-to-value and measurable productivity gains. Together, these factors suggest that the content analytics market will keep outpacing broader enterprise-software spending through the forecast window.

Key Report Takeaways

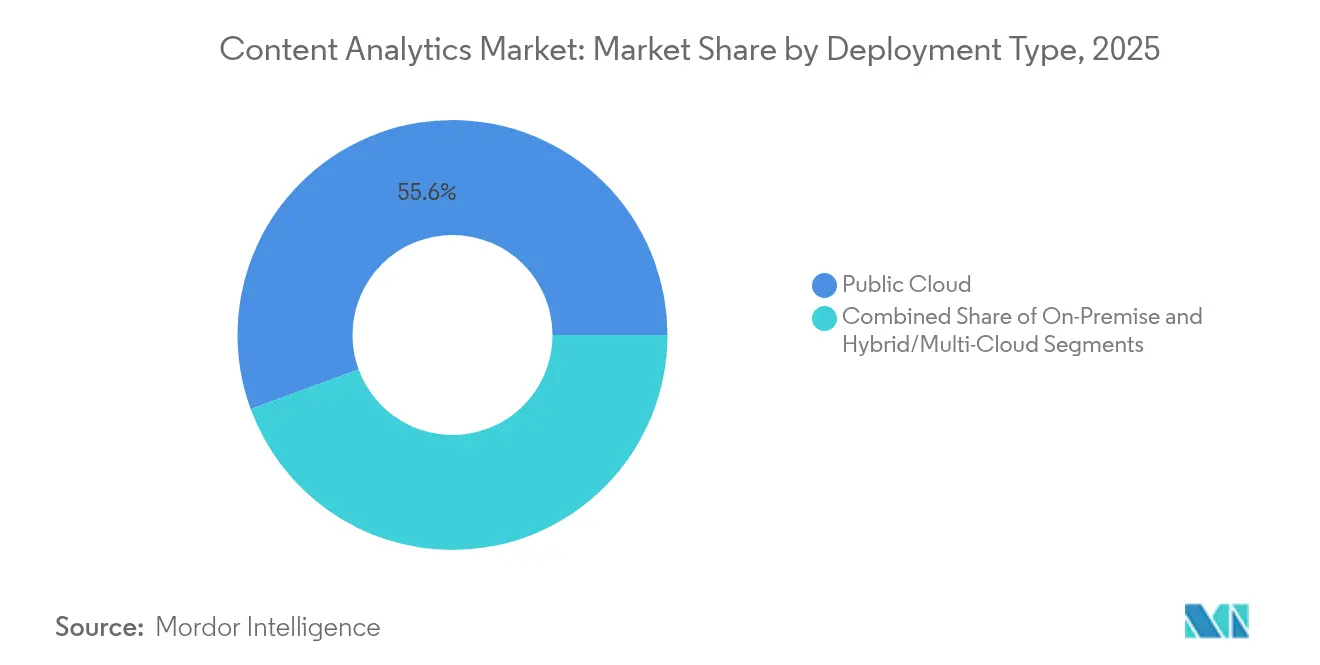

- By deployment type, public cloud led with 55.60% revenue share in 2025, while hybrid and multi-cloud posted the highest projected CAGR at 20.7% through 2031.

- By application, social media analytics accounted for 33.10% of the content analytics market share in 2025, whereas speech and audio analytics are set to expand at a 19.9% CAGR to 2031.

- By end-user industry, retail and consumer goods held 26.00% of 2025 revenue, while media and entertainment is on track for the fastest 19.8% CAGR.

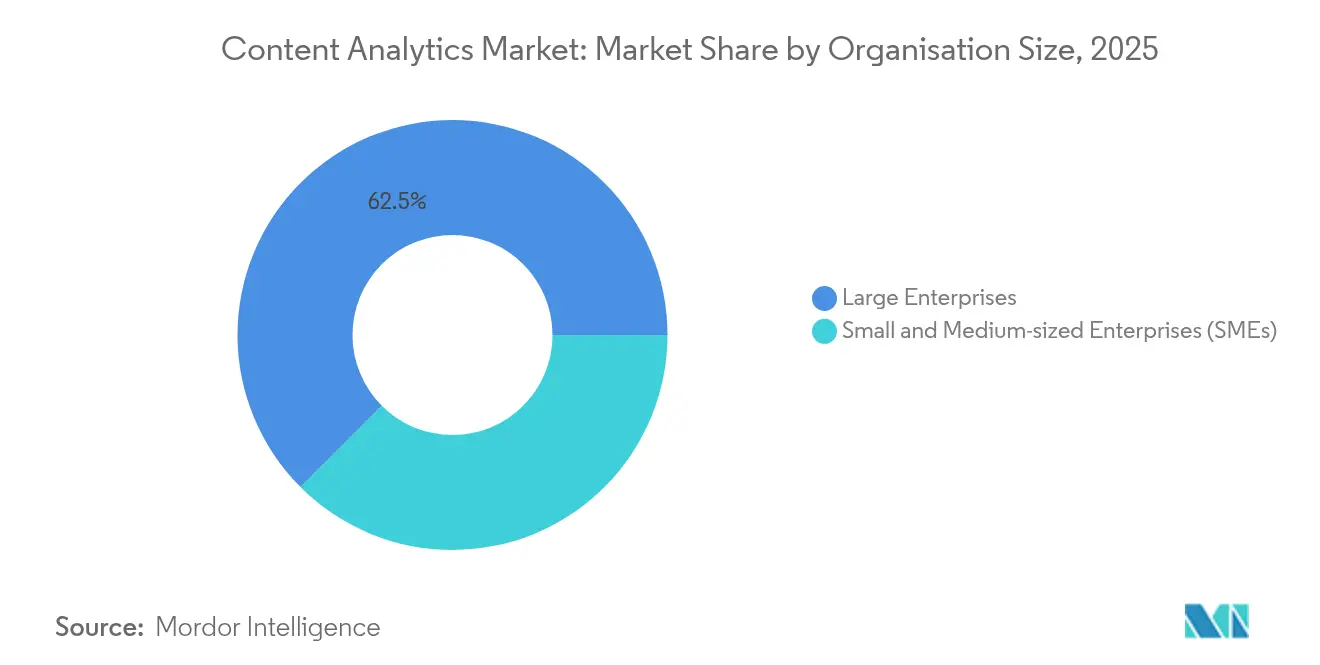

- By organisation size, large enterprises commanded 62.50% of 2025 spending, yet small and medium enterprises are forecast to grow at 21.6% CAGR as cloud-native offerings mature.

- By content type, text maintained 40.70% processing volume in 2025, but multimodal analytics is accelerating at 20.1% CAGR.

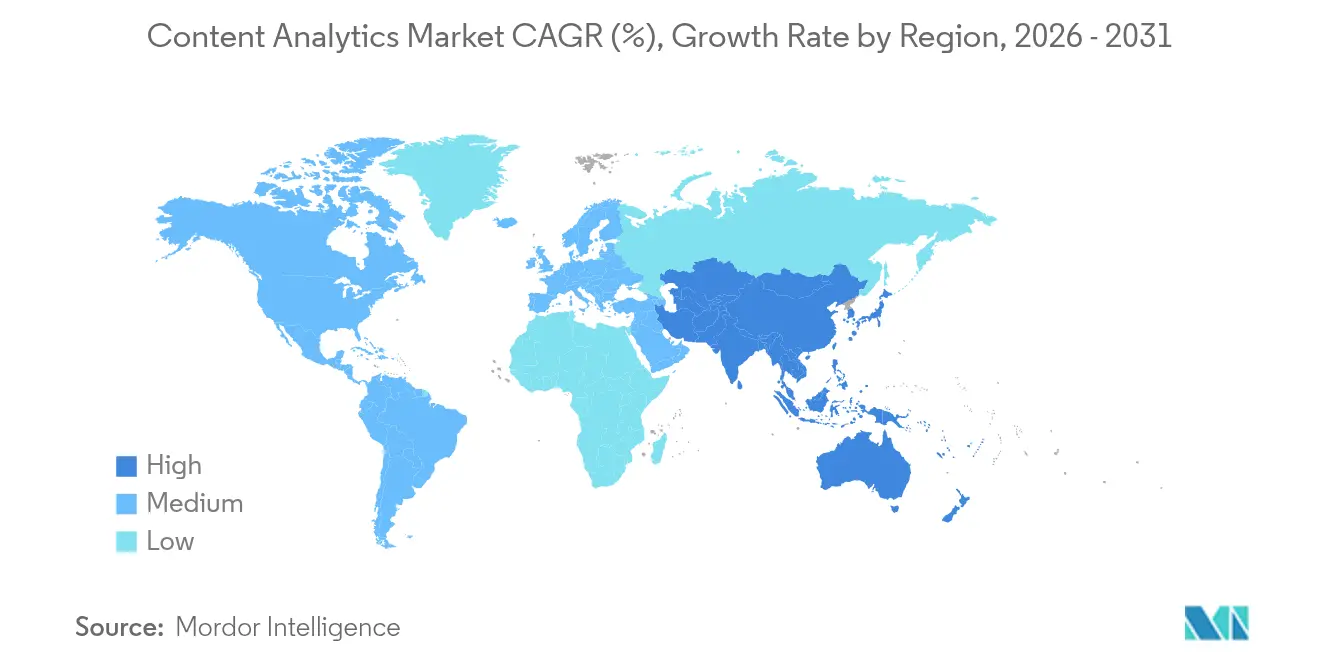

- By geography, North America retained a 37.70% share in 2025; Asia-Pacific is the fastest-growing region with a 21.0% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Content Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential growth of unstructured enterprise data | +3.2% | Global, APAC leading volume growth | Medium term (2-4 years) |

| Surging adoption of cloud-based analytics platforms | +2.8% | North America and EU early adoption, APAC rapid scaling | Short term (≤ 2 years) |

| Real-time social media listening for brand reputation | +2.1% | Global, concentrated in consumer-facing industries | Short term (≤ 2 years) |

| Vector search and semantic embedding unlock deeper insights | +1.9% | Technology hubs in US, China, EU | Medium term (2-4 years) |

| Multimodal (text-image-video) analytics in GenAI workflows | +1.7% | Global, led by media and retail sectors | Long term (≥ 4 years) |

| e-Discovery compliance pressures in regulated industries | +1.5% | North America, EU, with regulatory spillover globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exponential Growth of Unstructured Enterprise Data

Unstructured information already represents the majority of corporate memory, with 80% of the 175 zettabytes expected in 2025 originating outside relational systems. [1]Ran Zhou, “Vector Search in the Lakehouse: Unlocking Unstructured Data,” e6data, e6data.com Health-care providers, for example, digitized millions of images and charts to unlock real-time clinical insight while eliminating physical storage costs. [2]Iron Mountain Case Study Team, “Digitization Cures Medical Records to Optimize Patient Care,” Iron Mountain, ironmountain.com These volumes are pushing enterprises toward lakehouse architectures that embed vector functions inside familiar SQL engines, allowing knowledge workers to ask semantic questions against documents, chat logs, and medical scans in the same query.

Surging Adoption of Cloud-Based Analytics Platforms

Public-cloud AI services let enterprises rent transformer-scale models on demand, avoiding capital expenditure on specialized hardware. Amazon Web Services recorded USD 33.5 billion in Q1 2025 sales, up 17% year on year, driven largely by analytics workloads. Hybrid patterns are now mainstream as firms split workloads across providers to optimize for latency, cost, and jurisdictional compliance. Google BigQuery and Microsoft Knowledge Mining pipelines are anchoring this shift by abstracting infrastructure while exposing vector search APIs.

Real-Time Social Media Listening for Brand Reputation

Sixty percent of global social-media users reside in Asia-Pacific, creating vast, fast-moving data streams. Enterprises pipe live posts, images, and short-form videos into sentiment models that trigger granular ad bidding or product-availability updates within minutes. Retailers integrating social signals with transaction data saw 6.2% conversion-rate lifts in grocery segments.

Vector Search and Semantic Embedding Unlock Deeper Insights

Embedding-based retrieval replaces brittle keyword matching with context-aware similarity reasoning. Google’s Gemini family demonstrates near-expert performance across text, image, and audio tasks, catalyzing demand for cross-modal knowledge graphs. Financial services, life sciences, and regulated industries rely on these graphs to surface hidden relationships among contracts, medical imagery, and emailed directives, shortening disclosure cycles and enhancing compliance monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of data-literate workforce and change management gaps | -2.3% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Escalating data-privacy and data-sovereignty regulations | -1.8% | EU leading, North America following, APAC showing fragmented rules | Medium term (2-4 years) |

| High energy and carbon footprint of large-scale AI pipelines | -1.4% | Global, concentrated in data center regions | Medium term (2-4 years) |

| Fragmentation of content formats and lack of standardisation | -1.1% | Global, varying by industry vertical | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Data-Literate Workforce and Change Management Gaps

Only 37% of technology leaders judge generative AI as valuable today, largely because firms struggle to translate prototypes into scaled workflows. [3]Katie Tarasov, “Companies Are Bullish on AI but Skeptical of Payoff,” CNBC, cnbc.com Federal Reserve research shows AI uptake ranging from 5% to 40% across companies, highlighting the skills dispersion in data engineering, model governance, and domain-specific prompt design. Without targeted reskilling programs, analytics value realisation risks stalling despite abundant vendor offerings.

Escalating Data-Privacy and Sovereignty Regulations

Seventy-five percent of professionals identify privacy compliance as the top AI deployment concern. The European Corporate Sustainability Reporting Directive alone brings 3,200 US firms under new disclosure mandates from fiscal 2026, forcing architecture redesigns that partition data by jurisdiction. China’s strategy of shipping training data offshore for model refinement, then repatriating the resulting weights, illustrates the operational complexity now baked into expansion planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Strategies Balance Control and Scale

Public-cloud services captured 55.60% revenue in 2025 as enterprises sought frictionless access to transformer-class models. This share underscores the cost-efficiency and elasticity advantages that cloud hyperscalers continue to refine. The content analytics market size for public-cloud workloads is projected to climb steeply on the back of managed feature stores, model hubs, and enterprise prompts libraries. Hybrid and multi-cloud deployments are on a 20.7% CAGR trajectory because firms must reconcile latency-sensitive use cases with data-residency statutes. In regulated sectors, on-premise appliances remain indispensable for workloads requiring deterministic throughput or sovereign control.

Enterprises increasingly position vector indexes at the edge while offloading heavy embedding generation to cloud GPUs, achieving policy compliance without sacrificing insight depth. Vendors now bundle observability dashboards that score pipeline health across private and public endpoints, a trend that strengthens the content analytics market’s resilience to single-provider outages.

By Application: Speech Analytics Accelerates

Social media monitoring retained a 33.10% share in 2025, reflecting mature adoption of brand-listening suites and influencer tracking modules. Yet contact-center automation, real-time transcription, and voice biometrics are pushing speech and audio analytics toward a 19.9% CAGR, the fastest among tracked segments. The content analytics market size for speech-centric tools is scaling as voice assistants proliferate across banking, travel, and healthcare kiosks. High-quality automatic speech recognition feeds multi-modal dashboards where tone, sentiment, and intent scores guide agent coaching or trigger escalation workflows.

Text analytics remains essential for contractual review and compliance flagging, while video-centric pipelines serve loss-prevention and streaming-content optimisation. Convergence is gaining speed as social-video clips, call-center transcriptions, and user-posted images are routed into the same model garden. The industry narrative, therefore, shifts away from siloed products toward cohesive experience engines, reinforcing long-term growth prospects for the content analytics market.

By End-user Industry: Media and Entertainment Narrows the Gap

Retail and consumer goods accounted for 26.00% of expenditure in 2025 because personalization engines and shelf-level monitoring deliver measurable revenue uplift. However, automated storyboarding, talent-matching, and trailer optimisation set the stage for media and entertainment to advance at a 19.8% CAGR. Competitive pressures to reduce production cycles have sparked aggressive experimentation with script-to-screen AI workflows, positioning studios and streamers as major downstream consumers in the content analytics market.

Other sectors remain active adopters. BFSI institutions employ graph-based fraud alerting that builds on transactional embeddings, while healthcare pairs diagnostic imaging with clinical notes to enhance evidence-based care. Oil and gas firms deploy generative AI for well-integrity documentation, proving that domain-trained models can unlock niche operational efficiency. These patterns validate cross-industry breadth within the content analytics industry, even though spend concentration still skews toward sectors with direct consumer engagement.

By Organisation Size: SMEs Adopt Cloud-Native Suites

Large enterprises held 62.50% market revenue in 2025 because they can fund multi-year roadmaps that integrate analytics with ERP and CRM backbones. They also command the data volume that lucrative insight engines require. Small and medium enterprises, however, are forecast to grow usage at 21.6% CAGR as turnkey SaaS packages abstract model orchestration, governance, and continuous-integration complexity. This democratisation ensures that competitive advantage no longer depends on owning clusters of GPUs, a change that broadens the addressable base for vendors across the content analytics market.

Vendors cater to SMEs with vertical starter kits—out-of-box sentiment analysis for hospitality, micro-influencer scouting for consumer brands, or case-law summarisation for boutique legal practices. Subscription pricing, pay-per-document tiers, and low-code integration blueprints reduce initial commitment. The resulting ecosystem effect funnels fresh data back into shared embeddings stores, enriching the benchmarks that power next-generation releases.

By Content Type: Multimodal Workflows Reshape Foundations

Text accounted for 40.70% processing throughput in 2025, benefiting from mature NLP toolchains and enterprise familiarity. Multimodal and composite analysis, however, is surging at a 20.1% CAGR as users expect coherent answers spanning chat transcripts, product images, and support videos. Inside the content analytics market, teams now route heterogeneous payloads to unified embedding layers that preserve cross-modal context.

Image pipelines leverage CLIP-style encoders for visual similarity, while audio segments feed diarisation models that stitch speaker changes to event metadata. Video frames undergo object detection, then are linked to sentiment tags extracted from concurrent comments. This context blending produces richer downstream dashboards and creates new IP in prompt-template libraries. Forward-leaning adopters thus position multimodal capacity as a prerequisite for AI maturity assessments, amplifying growth across the content analytics market.

Geography Analysis

North America held 37.70% revenue share in 2025 because early cloud adoption produced mature data-science talent pools and extensive third-party marketplace ecosystems. Major providers like AWS drove double-digit percentage growth by bundling advanced vector search primitives into serverless databases, raising the entry barrier for regional challengers. Technology buyers benefit from a stable regulatory backdrop, although impending European ESG-reporting mandates already affect thousands of US multinationals that must align disclosure pipelines accordingly. The region’s spend mix spans financial services, health-tech, and direct-to-consumer retail, ensuring diversified momentum for the content analytics market.

Asia-Pacific is the fastest-growing territory, expected to clock a 21.0% CAGR through 2031. Government-backed infrastructure projects, including Hong Kong’s 3,000-petaflops supercomputing centre and India’s USD 1.3 billion compute strategy, provision the GPU density required for multimodal and large-language model workloads. Social-media penetration across WeChat, LINE, and Douyin ensures abundant vernacular data that accelerates fine-tuning cycles. Regional cloud providers are racing to deliver sovereign AI zones to meet localisation rules, a move likely to preserve high services revenue inside domestic value chains.

Europe advances steadily despite fragmented privacy regimes. Seventy-five percent of professionals cite regulation as their biggest AI hurdle, yet the region leads in privacy-preserving analytics such as federated learning. Automotive, industrial, and energy sectors align with academic labs to commercialise lightweight multimodal models that run on embedded hardware, reinforcing manufacturing competitiveness. Private investment still trails North American and Chinese levels, motivating policy debate on strategic AI autonomy.

Middle East and Africa show emerging momentum in public-sector digitalisation and fintech. Limited local GPU availability has spurred interest in edge accelerators that minimise data egress. Latin America mirrors this trend, with retail payment disruptors and urban-safety agencies embracing SaaS voice analytics. Although smaller in absolute terms, these regions contribute incremental demand that diversifies vendor revenue streams and mitigates geographic concentration risk in the global content analytics market.

Regulatory Landscape

Regulation affecting content analytics is tightening around platform accountability and AI transparency, which is pushing vendors to operationalize governance for unstructured content pipelines. In the European Union, the Digital Services Act (Regulation (EU) 2022/2065) requires online platforms to maintain clear terms and conditions and document content moderation policies, including the use of algorithmic decision-making and human review. This is raising demand for explainable classification, monitoring, and reporting features built into analytics stacks.

Value Chain Analysis

The content analytics value chain starts with content generation and ingestion across enterprise repositories and external channels (web, social, contact-center audio, video, and images). It then moves through data preparation (ETL, labeling, metadata enrichment) and the model and retrieval layers (embeddings, vector search, multimodal models), before being packaged into applications such as social listening, document and web analytics, speech analytics, e-discovery, and industry-specific dashboards. These outputs are delivered via SaaS, managed services, or hybrid deployments. Hyperscalers (AWS, Microsoft, Google) and open-source ecosystems (for example, OpenSearch under the Apache Software Foundation) provide foundational compute, storage, and search primitives. Specialist vendors differentiate with domain ontologies, workflow integrations, and governance controls that sit around these primitives.

Competitive Landscape

Market concentration remains moderate as platform hyperscalers, established enterprise-software vendors, and specialist boutiques jostle for share. AWS, Microsoft, and Google embed multimodal embedding layers into storage, workflow, and BI products, leveraging scale to bundle data residency, billing, and compliance into single contracts. Anthropic’s collaboration with Amazon Q Connect illustrates how tightly integrated LLMs reduce agent handling time by 10-15%. Such efficiency gains widen the moat for cloud incumbents.

Specialist vendors differentiate on vertical depth. SLB developed generative AI blueprints for well-integrity documentation, reducing investigation duration for oilfield engineers. Palantir pushes configurable ontology layers that appeal to defence and health agencies that need granular access controls. Smaller players focus on focal use-cases such as toxic-speech detection or AI code review, then partner with hyperscalers for distribution. Intellectual-property filings in vector compression and bias mitigation signal that patents will play a larger role in safeguarding margins as commoditisation accelerates.

Channel alliances matter because buyers prefer integrated stacks. Applied Industrial Technologies’ acquisition of IRIS Factory Automation strengthens process-automation portfolios that feed analytics engines with shop-floor images. Retail brands Oh Polly and AllSaints selected Algolia and Dixa, respectively, to modernise digital experiences, showcasing demand for composable front-end intelligence that plugs into existing ERP foundations.

Future competition will intensify around edge deployments, regulatory tech, and carbon-efficient inference. The influx of open-source multimodal models lowers barriers for challengers, while capital-intensive inference clusters sustain entry hurdles. As a result, incumbents with strong channel reach and proprietary usage telemetry possess a defensible advantage, though niche innovators will continue to disrupt single-function categories within the content analytics market.

Content Analytics Industry Leaders

Adobe Inc.

Alphabet Inc. (Google Cloud)

Amazon Web Services, Inc.

Apache Software Foundation (OpenSearch)

Apple Inc. (Apple Analytics)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-grade content analytics is a clear monetization path as AI transparency and platform accountability requirements move from policy design into operational enforcement. The EU AI Act includes obligations such as AI literacy requirements in force since February 2, 2025 (Article 4) and a major transparency milestone on August 2, 2026 (including Article 50 disclosure obligations for AI-generated content). That sequencing is increasing buyer demand for audit-ready capabilities such as tamper-evident logging, model and version tracking, content provenance, and automated monitoring across text, audio, and multimodal workflows.

Recent Industry Developments

- July 2026: The initiative to deploy agentic AI powered advertising technology on AWS associated with Warner Bros. Discovery was announced. The project links large-scale content signals to automated workflows and strengthens real-time content analytics and orchestration capabilities in media monetization stacks.

- May 2026: Snowflake expanded its collaboration with AWS through a multi-year USD 6 billion commitment to accelerate enterprise agentic AI adoption on AWS infrastructure. The agreement aligns data platforms, infrastructure capacity, and joint go-to-market motions, expanding cloud-based analytics reach.

- April 2026: The acquisition of Semrush Holdings, Inc. by Adobe was completed, adding brand visibility capabilities that connect content performance signals with customer experience workflows. The deal strengthens integrated content analytics across creation, optimization, and measurement, increasing competitive pressure on standalone analytics vendors to deepen CX integrations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the content analytics market is the revenue earned from software and related services that analyze digital content like text, images, audio, and video to produce insights used for actions such as marketing, risk control, and customer experience improvement.

Scope exclusions: we exclude generic business intelligence tools, pure storage or data-warehouse products, manual tagging work, and stand-alone transcription services.

Segmentation Overview

- By Deployment Type

- On-Premise

- Public Cloud

- Hybrid/Multi-Cloud

- By Application

- Text Analytics

- Video Analytics

- Social Media Analytics

- Speech/Audio Analytics

- Web and Document Analytics

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Retail and Consumer Goods

- IT and Telecom

- Manufacturing

- Government and Public Sector

- Media and Entertainment

- Other End-user Industries

- By Organisation Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By Content Type

- Text

- Image

- Audio

- Video

- Multimodal/Composite

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set guardrails for what should be counted and what should not be counted, especially where content analytics features get bundled into broader platform suites. We rely on public sources such as US SEC filings, US Bureau of Labor Statistics data on tech employment, US Census trade and services statistics, and OECD digital economy indicators to understand demand direction and spending ability. We also review standards and regulatory guidance that shape adoption, including NIST publications and privacy regulator materials, since compliance-driven monitoring use cases often affect budget timing.

In parallel, we review company annual reports, earnings call transcripts, product documentation on public websites, and reputable press coverage to map how content analytics is packaged and sold. For cross-checking financial context, we use paid subscriptions that provide company financials and intelligence, patent databases, and news and financials coverage to confirm product focus and launch timing. These desk sources are illustrative only, and many other public references were used during the research process for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys are used to stress-test the scope and convert desk assumptions into workable inputs, including typical pricing motions, buyer adoption patterns, and how frequently analytics modules are purchased as add-ons. We spoke with a mix of solution providers, channel partners, and enterprise users across APAC, EMEA, and the Americas so regional buying cycles and cloud adoption differences were reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 46% |

| Mid tier: 49% | Functional/Unit leaders: 43% | EMEA: 29% |

| Smaller Players: 20% | Managers: 45% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where we reconstruct the addressable spend by combining enterprise software and IT services spending signals, then filtering it to the share directed toward analyzing unstructured and multimedia content for business outcomes. Once that demand pool is formed, totals are reconciled with selective bottom-up checks, such as sampled vendor revenue disclosures, channel feedback on attach rates, and a sanity check using typical average selling price bands multiplied by adoption volumes.

The model is guided by market fingerprints that shift year to year, including cloud versus on-premise mix, usage growth in text and video content, compliance-driven monitoring needs, improvements in NLP and computer-vision accuracy, and the share of deployments purchased as discrete analytics modules rather than as a bundled feature. When a bottom-up view cannot be completed for smaller providers due to limited disclosures, we bridge the gap using peer group ratios and interview-led penetration assumptions, then re-check reasonableness at the regional level.

For forecasting, we use scenario analysis because budgets can shift quickly based on regulation updates and enterprise AI investment cycles. Scenarios are anchored to interview consensus on near-term adoption, then adjusted using indicators like digital content growth, IT spend trends, and cloud migration pace so the trajectory remains explainable and repeatable.

Data Validation & Update Cycle

Validation is done in layers so obvious errors do not pass through to the final output. We compare market totals against independent signals like enterprise software spending direction, cloud adoption indicators, and disclosed performance of relevant product lines, and then we check for large jumps that do not fit the adoption story. If a variance looks abnormal, the assumptions behind pricing, module attach rates, or regional splits are revisited and, when needed, the team re-contacts interviewees to confirm what changed.

Before sign-off, the model and the written logic go through a multi-step review so inputs, units, and currency conversions are consistent across regions. Reports are refreshed annually, and interim updates are made when a material market event changes demand or packaging. Right before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Content Analytics Market Size Measured Against Other Published Estimates

Published market sizes for content analytics rarely match exactly because companies can count different revenue boundaries, pick different base years, and apply different pricing and adoption assumptions. Even when the topic name looks similar, the number can move depending on whether only discrete analytics modules are counted or if wider adjacent tools are included.

Product packaging checks and module-level revenue cues, supported by interview confirmations on attach rates, are the evidence that ties Mordor Intelligence's 2026 estimate to what is actually paid for content analytics capability rather than bundled features that are hard to separate. Differences also come from forecast posture, where some publishers lean on faster cloud migration or aggressive AI adoption without re-checking if budgets and compliance timelines line up across regions. Currency timing and update cadence matter as well, especially when enterprise software spend trends shift within a year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.08 B (2026) | |

| Industry Research Publisher A | USD 11.16 B (2025) | Uses an earlier base year and appears to apply a broader content analytics umbrella without clearly separating discrete analytics modules from wider software capabilities, which can inflate counted revenues. |

| Industry Research Publisher B | USD 11.56 B (2025) | Runs a longer forecast window and starts from a 2025 base that may embed more optimistic adoption and pricing progression, with limited clarity on exclusions like generic BI or stand-alone data infrastructure. |

Looking across the three figures, the spread is mainly explained by scope boundaries and base-year choices, and then amplified by how pricing and adoption are carried forward in the forecast. Our approach keeps the market tied to discrete, paid content analytics functionality and uses interview-backed checks so the final value can be traced back to clear, repeatable inputs.

Key Questions Answered in the Report

What is the current size of the content analytics market?

The market stands at USD 10.08 billion in 2026 and is projected to reach USD 23.12 billion by 2031, reflecting an 18.05% CAGR.

Which deployment model is expanding fastest?

Hybrid and multi-cloud configurations are advancing at a 20.7% CAGR as firms balance data-sovereignty mandates with hyperscale AI capacity.

Which application shows the highest growth momentum?

Speech and audio analytics lead with a 19.9% CAGR, fueled by contact-center automation and voice-enabled customer service.

Which region is poised for the quickest expansion?

Asia-Pacific is projected to grow at a 21.0% CAGR through 2031, supported by large-scale AI infrastructure investments.

What is the main driver behind enterprise adoption of content analytics?

The explosive rise of unstructured data—estimated to hit 80% of 175 zettabytes in 2025—demands vector-based semantic processing for actionable insight.

How are small and medium enterprises benefiting from content analytics?

SMEs are adopting cloud-native suites at a 21.6% CAGR, gaining enterprise-grade AI capabilities without heavy capital outlays.

Page last updated on: