Enterprise Content Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

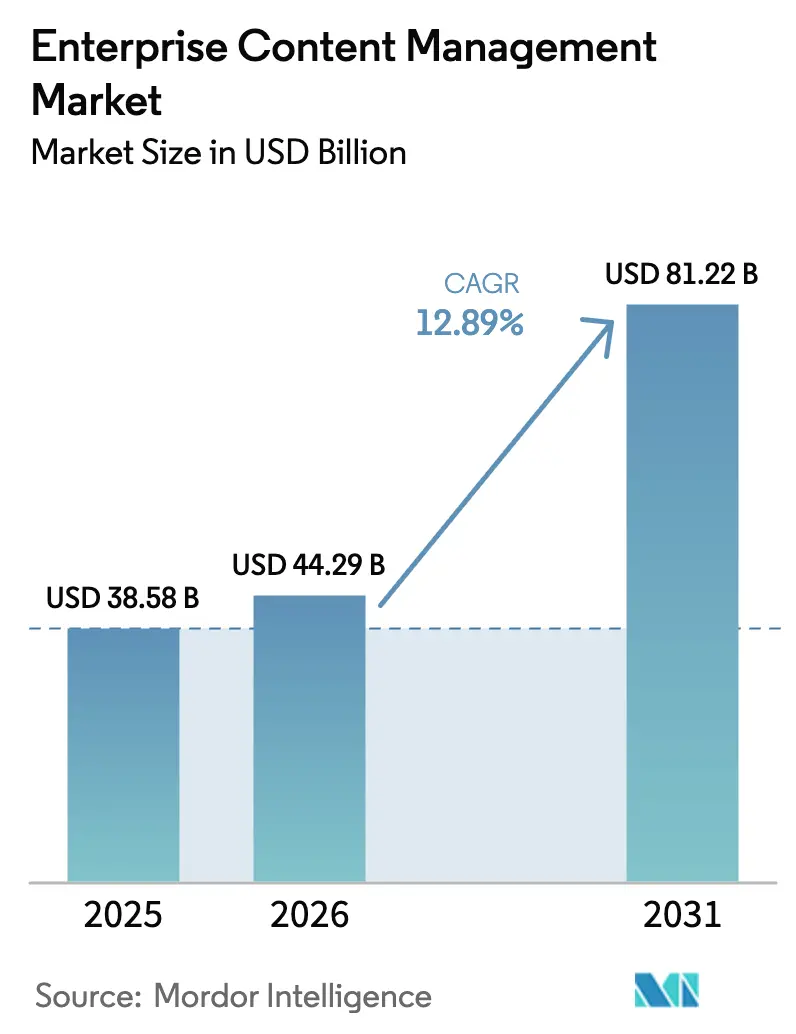

| Market Size (2026) | USD 44.29 Billion |

| Market Size (2031) | USD 81.22 Billion |

| Growth Rate (2026 - 2031) | 12.89% CAGR |

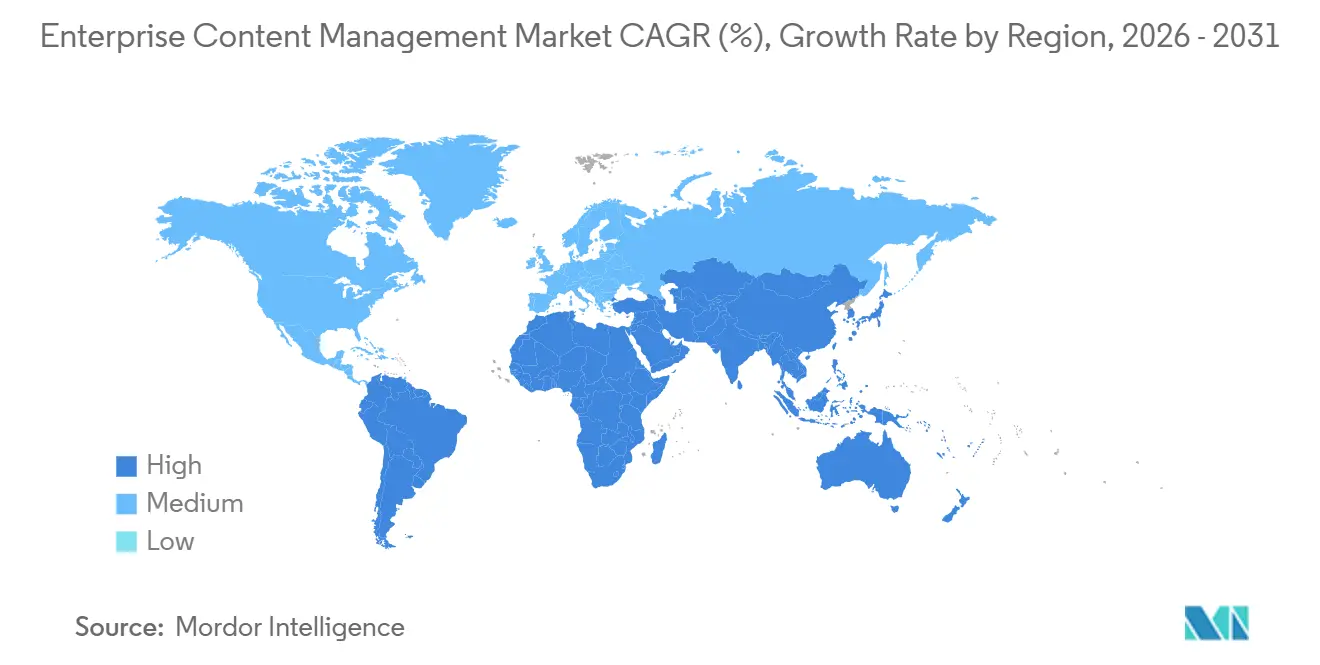

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

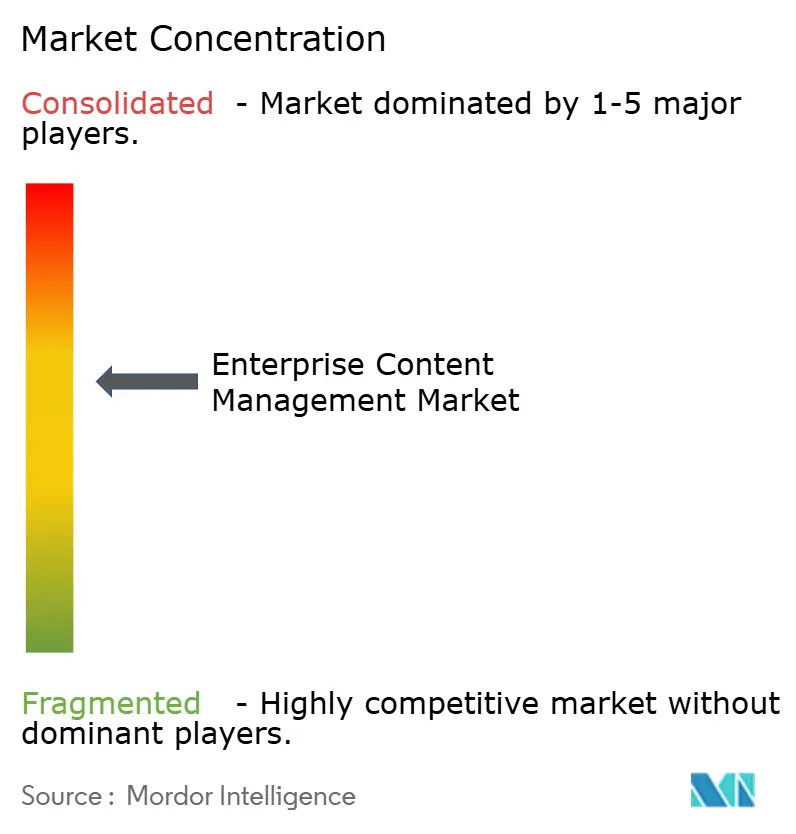

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Content Management Market Analysis by Mordor Intelligence

The Enterprise Content Management Market size is expected to grow from USD 38.58 billion in 2025 to USD 44.29 billion in 2026 and is forecast to reach USD 81.22 billion by 2031 at 12.89% CAGR over 2026-2031.

Key growth drivers include unstructured data growth that overwhelms legacy repositories, intensifying regulatory enforcement that demands auditable retention controls, and the rollout of AI toolsets that automate document classification and case workflows. Token-based pricing is widening access for mid-market buyers, while multi-cloud architectures that respect regional data-residency rules are redefining competitive differentiation. Vendors that intersect hyper-automation with sovereign-cloud compliance continue to outpace peers, even as breach headlines and API cost inflation reshape procurement criteria.

Key Report Takeaways

- By solution type, Document Management led with a 28.19% revenue share in 2025, whereas Digital Asset Management is expected to advance at a 13.36% CAGR through 2031.

- By deployment mode, On-Premises captured 53.48% of 2025 revenue, while Cloud is forecast to grow at a 13.91% CAGR to 2031.

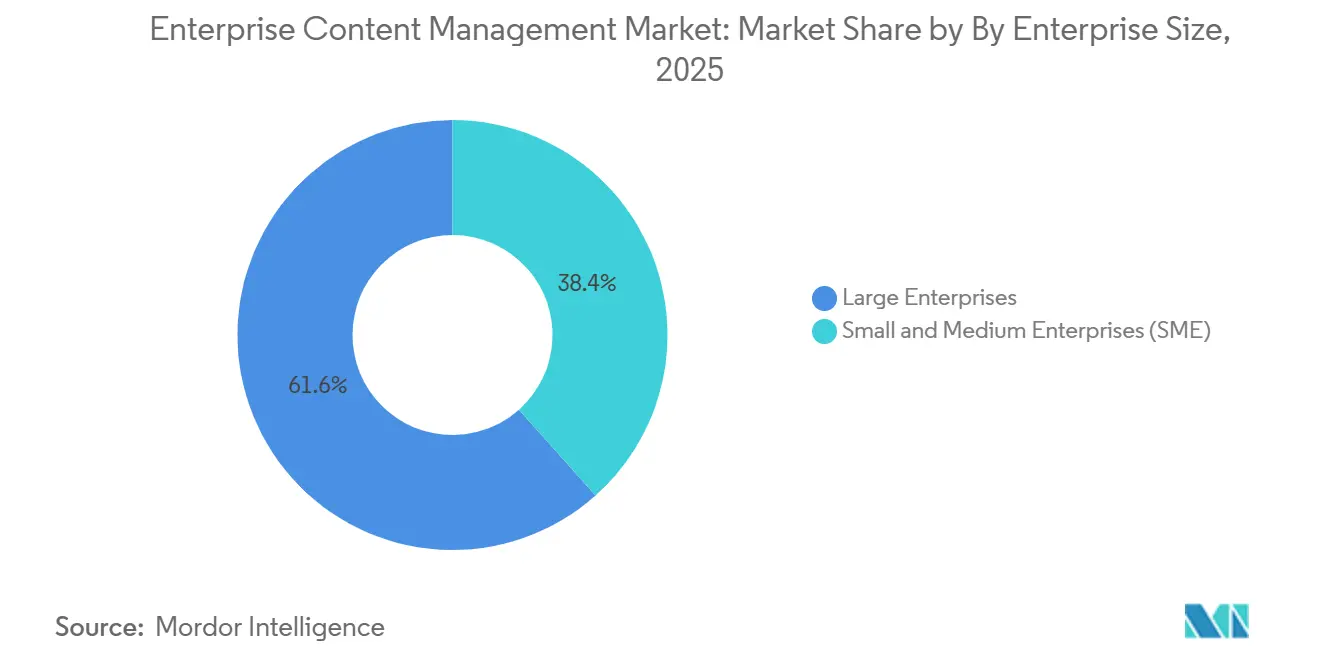

- By enterprise size, Large Enterprises held 61.59% of the Enterprise Content Management market share in 2025; Small and Medium Enterprises are poised for a 13.27% CAGR through 2031.

- By end-user industry, BFSI accounted for 22.54% of spending in 2025, while Healthcare is projected to record a 13.66% CAGR to 2031.

- By geography, North America commanded a 38.73% share in 2025, yet Asia Pacific is set for a 13.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Enterprise Content Management Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Compliance Mandates for Content Lifecycle Governance | +2.80% | Global, with heightened enforcement in EU and India | Medium term (2-4 years) |

| Explosion of Enterprise Unstructured Data Volumes | +3.20% | Global, APAC core with spill-over to MEA | Long term (≥ 4 years) |

| Accelerated Shift to Cloud-Native ECM Deployments | +2.50% | North America and EU, early adoption in APAC urban centers | Short term (≤ 2 years) |

| AI-Driven Content Intelligence and Hyper-Automation | +2.10% | North America and EU, pilot deployments in APAC | Medium term (2-4 years) |

| Rising Adoption of Industry-Specific Pretrained Language Models for Domain Document Automation | +1.40% | North America and EU, niche verticals in APAC | Long term (≥ 4 years) |

| Token-Based Consumption Pricing Reshaping Mid-Market Adoption | +1.70% | Global, strongest uptake in North America and EU SME segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance Mandates for Content Lifecycle Governance

Stringent rules such as GDPR, the UK Data Protection Act 2018, and India’s Digital Personal Data Protection Act 2023 impose retention schedules, right-to-erasure protocols, and immutable audit-trail requirements. The May 2024 EUR 251 million (USD 283 million) penalty on Meta highlighted regulators’ willingness to levy material fines, driving enterprises toward geo-fenced repositories and auto-classification engines. Financial institutions face overlapping Basel III and MiFID II mandates, while healthcare providers juggle HIPAA with state privacy statutes, reinforcing the need for integrated governance within the Enterprise Content Management market. Solution roadmaps now embed policy templates that map regional statutes to metadata fields, enabling defensible deletion and automated litigation holds. Boards increasingly view non-compliant content workflows as financial and reputational liabilities, elevating ECM adoption to a core risk-mitigation strategy.

Explosion of Enterprise Unstructured Data Volumes

Unstructured documents, emails, CAD files, and sensor logs account for more than 80% of corporate data, growing by double digits annually. Manual tagging cannot scale, so enterprises turn to NLP-infused platforms that surface relevant information in milliseconds. Microsoft’s Copilot for SharePoint Premium cuts search time by up to 70%, while Adobe’s AI Agents autogenerate summaries for marketing assets, signaling a pivot from passive storage to proactive knowledge discovery.[1]Microsoft Corporation, “Microsoft SharePoint Premium with Copilot,” microsoft.com The productivity gains justify investment even during budget tightening, especially as legal teams leverage auto-redaction to streamline e-discovery. In Asia Pacific, data-growth velocity is amplified by IoT rollouts, positioning next-generation ECM as an operational necessity rather than a discretionary upgrade.

Accelerated Shift to Cloud-Native ECM Deployments

Cloud deployments are advancing at a 13.91% CAGR to 2031, outstripping on-premises installations as hybrid architectures alleviate latency and data-sovereignty worries. OpenText’s tiered Documentum packages illustrate how consumption pricing can lower first-year costs for mid-market buyers.[2]OpenText Corporation, “Documentum Pricing Tier Announcement,” opentext.com Yet the June 2024 Snowflake breach, which exposed 165 organizations, underscored that shared-responsibility models need vendor-managed keys, multi-region failover, and zero-trust network access. As a result, procurement scorecards now weight SOC 2 Type II and ISO 27001 equally with AI features. In regulated sectors, hybrid models keep master records on-premises while offloading analytics to the cloud, balancing compliance and innovation.

AI-Driven Content Intelligence and Hyper-Automation

Generative AI transforms ECM from static vaults into dynamic orchestration hubs. M-Files’ Aino suggests metadata tags and drafts responses by mining historical correspondence, while Box’s AI summarization reduces discovery cycles from weeks to hours.[3]M-Files Corporation, “Aino AI Assistant Overview,” m-files.com Adobe’s December 2025 ChatGPT integration brings natural-language search to 800 million weekly users, blurring lines between creation and management. Industry-tuned models for legal contract review, radiology report summarization, and manufacturing drawing control serve as competitive moats. Reported workflow cycle-time reductions of 40%–60% translate into accelerated revenue recognition and faster claims adjudication, fortifying the Enterprise Content Management market growth narrative.

Restraints Impact Analysis of Enterprise Content Management Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security and Privacy Concerns in Cloud and Mobile ECM | -1.90% | Global, acute in regulated industries (BFSI, Healthcare, Government) | Short term (≤ 2 years) |

| Complexity of Merging Legacy Repositories Post-M&A | -1.20% | North America and EU, high M&A activity regions | Medium term (2-4 years) |

| Cross-Border Data-Transfer Restrictions (GDPR, DPDPA, etc.) | -1.50% | EU, India, with ripple effects in APAC and MEA | Long term (≥ 4 years) |

| Escalating API Rate-Limit Costs in Content Collaboration Platforms | -0.80% | Global, concentrated in high-volume enterprise deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Security and Privacy Concerns in Cloud and Mobile ECM

The February 2024 Change Healthcare ransomware attack affecting over 100 million individuals and costing USD 22 million in ransom brought cloud-repository vulnerabilities to the forefront. Snowflake’s breach four months later fuelled deeper scepticism toward shared-credential models. Chief information security officers now mandate immutability, real-time anomaly detection, and device-level encryption for mobile access before green-lighting cloud migration. Liability frameworks increasingly hold data controllers accountable for third-party incidents, raising insurance costs and elongating procurement cycles in risk-averse industries such as banking and defense. While vendors race to certify zero-trust architectures, security fears will continue to dilute near-term Enterprise Content Management market expansion.

Cross-Border Data-Transfer Restrictions (GDPR, DPDPA, etc.)

The invalidation of the EU-US Privacy Shield and India’s localization mandates compel multinationals to maintain region-specific ECM instances, inflating infrastructure budgets. Meta’s EUR 251 million penalty underscored the financial stakes of non-compliance. Fragmentation complicates disaster recovery and introduces latency when global teams collaborate, especially on cross-functional projects such as drug-development dossiers. Vendors respond with federated architectures and centralized policy engines, yet legal uncertainty persists as new adequacy negotiations unfold. Compliance overhead diverts funds that could otherwise fuel innovative AI add-ons, moderating long-term Enterprise Content Management market momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Enterprise Content Management Market Segment Analysis

By Solution Type:

Digital Asset Management Outpaces Traditional Document WorkflowsDocument Management retained a 28.19% revenue lead in 2025 because regulated verticals rely on version control for contracts, policies, and filings. However, Digital Asset Management is scaling at a 13.36% CAGR as retailers and media houses orchestrate thousands of omnichannel images and videos. The Enterprise Content Management market size for Digital Asset Management is projected to double by 2031 as AI-driven auto-cropping, format conversion, and rights management become table stakes. Adobe’s fiscal 2025 revenue of USD 23.8 billion illustrates monetization potential as generative models simplify asset reuse. Increasingly, vendors bundle document, asset, and workflow capabilities, dissolving traditional category boundaries and nudging buyers toward platform commitments that minimize point-solution sprawl.

Content creators now demand real-time collaboration, intuitive search, and embedded analytics that surface asset performance metrics. Microsoft’s Copilot integration allows marketers to locate “blue-background images” without manual tagging, while Oracle streamlines brand-kit governance across dispersed agencies. Case Management and Workflow engines, once sold separately, are now embedded into Digital Asset modules, routing creative approvals and enforcing brand-consistency checkpoints. This convergence elevates lock-in risk, prompting procurement teams to prioritize open APIs and metadata-interoperability standards. As solution boundaries blur, platform extensibility and ecosystem depth will dictate wallet share within the Enterprise Content Management market.

By Deployment Mode:

Cloud Gains Momentum Despite On-Premises IncumbencyOn-Premises deployments held 53.48% of 2025 revenue because banks, defense contractors, and hospitals still favour air-gapped environments for sensitive records. Yet the cloud sub-segment is advancing at a 13.91% CAGR, underscoring a decisive shift toward elastic compute and pay-as-you-go economics. The Enterprise Content Management market size associated with cloud offerings is set to eclipse on-premises spend by 2029 if current momentum persists. Usage-based pricing, highlighted by L.E.K. Consulting research, aligns vendor revenue with customer consumption, driving higher renewal rates and stickier net-retention metrics.

OpenText’s Express, Premium, and Ultimate Documentum tiers demonstrate granular metering that lowers pilot costs while preserving upsell pathways. Hybrid architectures keep master data on-site but use cloud analytics for anomaly detection and full-text indexing, mitigating compliance hurdles without sacrificing AI functionality. Nevertheless, the Snowflake breach reminded enterprises that encryption-key ownership and zero-trust segmentation are non-negotiable. As cyber-underwriting criteria tighten, buyers will favour vendors that furnish audit-ready SOC 2 Type II reports and native cyber-insurance endorsements.

By Enterprise Size:

SME Adoption Accelerates on Consumption PricingLarge Enterprises commanded 61.59% of spending in 2025, leveraging multi-year enterprise license agreements and deep integrations with ERP and CRM systems. Small and Medium Enterprises, however, are expanding adoption at a 13.27% CAGR, a trajectory fuelled by SaaS models that replace hefty capex with monthly operational outlays. The average SME deploys core document and workflow functions first, then layers record-management or digital-asset modules as headcount and content volumes grow.

Token-based schemes de-risk initial rollouts by letting teams pay only for active users or gigabytes stored. Microsoft, Oracle, and Egnyte offer tiered storage and API bundles that scale linearly, enabling SMEs to test AI features without a wholesale platform commitment. Implementation time shrinks from months to weeks thanks to industry-specific templates, empowering smaller firms to meet the compliance benchmarks once reserved for blue-chip incumbents. As labour-constrained organizations prioritize automation, SME penetration will remain a powerful tailwind for the Enterprise Content Management market.

By End-User Industry:

Healthcare Surges on EHR Integration MandatesBFSI sustained a 22.54% spending lead in 2025 on the back of stringent record-retention rules under Basel III, MiFID II, and anti-money-laundering frameworks. Yet Healthcare is charting a 13.66% CAGR through 2031, energized by electronic health record integration, patient-consent management, and FDA 21 CFR Part 11 electronic-signature compliance. The Enterprise Content Management market share for radiology image and clinical-trial repositories is poised to expand as hospitals digitize diagnostics and pharma sponsors automate regulatory submissions.

Change Healthcare’s ransomware incident propelled zero-trust architectures and immutable audit trails to the top of procurement checklists. Meanwhile, telecom operators use ECM to streamline service-order documentation, and manufacturers integrate it with PLM systems to accelerate engineering change orders. Education, government, and energy sectors represent growing niches as digital-public-service and smart-grid initiatives mature. Verticalized language models and prebuilt process connectors will be decisive in vendor shortlists, reinforcing specialization as a lever for margin expansion.

Geography Analysis

North America Enterprise Content Management Market

North America retained 38.73% of 2025 revenue, reflecting early cloud adoption, vendor density, and strict sectoral regulations that favour enterprise-grade platforms. Mature ECM installations in banking and federal agencies emphasize integration with compliance analytics, while Mexico’s automotive suppliers deploy content workflows to satisfy IATF 16949 traceability. Meta’s EUR 251 million fine, imposed by Ireland’s regulator yet impacting U.S. operations, illustrates how extraterritorial enforcement shapes the Enterprise Content Management market even within home jurisdictions.

APAC Enterprise Content Management Market

Asia Pacific is projected to grow at a 13.51% CAGR through 2031, propelled by China’s software-localization edicts, India’s public-service digitization drives, and Japan’s demographic-led automation push. China’s Data Security Law compels multinationals to operate in-country ECM stacks, spurring demand for modular designs that synchronize metadata globally while localizing personal data. India’s Digital Personal Data Protection Act enforces similar localization, prompting hybrid cloud builds that isolate sensitive datasets inside national borders. South Korea’s 5G ubiquity accelerates mobile ECM uptake, while Australia’s anti-money-laundering reforms sustain financial-sector investment.

EMEA and South America Enterprise Content Management Market

Europe, South America, Middle East and Africa collectively comprise the remaining share, with Europe anchored by GDPR-induced platform refreshes in Germany, France, and the United Kingdom. Brazil’s open-banking regulations encourage banks to standardize content pipelines, whereas Saudi Arabia’s smart-city ambitions necessitate centralized citizen-service repositories. Divergent retention schedules and consent frameworks across these regions elevate the importance of configurable policy engines. Enterprises that deploy federated architectures as regional instances governed by a unified control plane can reconcile local compliance with global collaboration, carving a defensible path in the Enterprise Content Management market.

Regulatory Landscape

Enterprise content management (ECM) procurement and deployments are increasingly shaped by electronic-recordkeeping mandates and cybersecurity control baselines, particularly for government and other heavily regulated environments. In the United States, OMB and NARA policy direction, including OMB M-23-07, reinforces the requirement for federal agencies to manage permanent records electronically, while 36 CFR Part 1236 establishes federal electronic records management controls and associated metadata expectations for electronic records. NARA also continues to operationalize reporting and oversight, including its AC 04.2026 memorandum, which set the 2025 federal agency records management reporting window from March 9, 2026 to May 15, 2026.

Security-by-design and auditable governance requirements are being built into buying criteria through standards and agency-specific solicitations. NIST SP 800-53 Revision 5, including updates published in 2026, provides the cybersecurity and privacy control baseline that influences how ECM systems are secured, monitored, and assessed in public-sector environments. At the state level, New York Attorney General RFP-25-007 (January 2026) shows how agencies are specifying cloud-based ECM capabilities to improve records management, compliance, and retrieval, reinforcing demand for platforms that can meet lifecycle governance, metadata capture, and retention requirements aligned with NARA guidance such as Universal ERM Requirements.

Competitive Landscape

The market exhibits moderate concentration. Microsoft, OpenText, IBM, and Oracle leverage embedded ties to productivity, database, and ERP suites, capturing outsized wallet share. Hyland, Box, M-Files, and Laserfiche differentiate through vertical-specific workflows in healthcare, legal, and municipal segments. Consumption-based pricing and API-first architecture enable newcomers to undercut legacy maintenance contracts, enticing cost-sensitive SMEs.

Strategic activity centers on AI infusion. Microsoft’s Copilot conversational search, Adobe’s generative image tagging, and Box’s sentiment analysis slash knowledge-worker friction. OpenText adopted tiered Documentum bundles in November 2025, aligning revenue with usage and boosting renewals. Niche players exploit domain models. M-Files automates legal brief routing, while SER Group targets pharmaceutical regulatory dossiers. Vendors prioritizing SOC 2 and ISO 27001 attestations win contracts in BFSI and Healthcare, where breach risk eclipses speed-to-market.

Partner ecosystems serve as force multipliers. Microsoft’s integration with ServiceNow streamlines incident-response documentation, whereas Adobe’s alliance with Shopify links digital-asset libraries to commerce storefronts. OEM agreements, such as IBM embedding Hyland workflows into its consulting stack, broaden reach without diluting R and D focus. As compliance complexity scales, buyers gravitate toward platforms that marry feature breadth with verifiable security, setting the direction for future Enterprise Content Management market consolidation.

Enterprise Content Management Industry Leaders

Microsoft Corporation

OpenText Corporation

IBM Corporation

Oracle Corporation

Hyland Software Inc.

- *Disclaimer: Major Players sorted in no particular order

Enterprise Content Management Market Companies Covered in this Report

- Microsoft Corporation

- OpenText Corporation

- IBM Corporation

- Hyland Software Inc.

- Oracle Corporation

- Box Inc.

- Adobe Inc.

- Xerox Holdings Corporation

- M-Files Corporation

- Alfresco Software Inc. (Hyland)

- DocuWare GmbH

- Datamatics Global Services Ltd.

- Hewlett Packard Enterprise Company

- Capgemini SE

- Newgen Software Technologies Ltd.

- Laserfiche Inc.

- SER Group

- Fabasoft AG

- Everteam Global Services

- KnowledgeLake Inc.

- iManage LLC

- Egnyte Inc.

Market Opportunities and Future Outlook

Agentic automation and AI-native content services are emerging as a clear whitespace area as ECM platforms shift from user-driven document handling toward autonomous task execution across classification, extraction, routing, and discovery. Vendor roadmaps in 2026 indicate a move from add-on copilots to agentic capabilities embedded into repositories and workflow layers, including OpenText advancing Content Aviator features in its 26.2 releases and Hyland publicizing agentic automation enhancements within Content Innovation Cloud. This shift raises the bar for governed, metadata-rich content foundations, both for knowledge work and for compliance operations such as defensible deletion, litigation holds, and audit-ready retention.

Data residency, sovereign-cloud options, and API-first architectures are also expanding addressable use cases for multinationals that must keep content inside specific jurisdictions while still enabling enterprise-wide search and automation. Hyland collaboration with Microsoft to deploy Content Innovation Cloud on Microsoft Azure is positioned around geographic data residency needs, and OpenText made ECM-related enterprise data and AI solutions available on AWS European Sovereign Cloud (April 2026), supporting more compliant landing zones for regulated buyers. API-driven content services, including Microsoft SharePoint Embedded, are being positioned as a modernization path for legacy ECM, allowing organizations to keep existing repositories while exposing content and governance controls to broader application and AI ecosystems, which supports incremental adoption rather than disruptive replacement programs.

Recent Industry Developments in Enterprise Content Management Market

- June 2026: IBM announced the general availability of IBM Content Cortex Essentials Edition, positioned as an AI-native content services evolution path from FileNet Content Manager. The launch highlights how incumbent ECM stacks are being extended with AI-first services to reduce the need for full platform replacement while modernizing automation and discovery capabilities.

- April 2026: OpenText announced its enterprise data and AI solutions, including OpenText Content Management and Documentum, would be available on AWS European Sovereign Cloud. This move broadens sovereign-cloud deployment options for regulated European workloads and strengthens vendor positioning around data residency and compliance-driven cloud modernization.

- September 2024: OpenText introduced next-generation Aviator AI capabilities to enrich content workflows. The update reinforced the competitive push to embed AI directly into core ECM use cases such as search, summarization, and workflow assistance, accelerating platform differentiation beyond traditional repository features.

Enterprise Content Management Market Report Scope and Research Methodology

Market Definition and Coverage

For this report, the market covers enterprise content management (ECM) platforms and related services that help organizations capture, organize, store, secure, govern, and retrieve business content through its lifecycle across cloud and on-premises setups.

Scope exclusions: We do not count stand-alone web content tools that do not include core ECM functions such as workflow, records retention, or information governance.

Segments Covered in This Report

- By Solution Type

- Content Management

- Document Management

- Case Management

- Workflow Management

- Record Management

- Digital Asset Management

- Other Solution Types

- By Deployment Mode

- On-Premises

- Cloud

- By Enterprise Size

- Small and Medium Enterprises (SME)

- Large Enterprises

- By End-User Industry

- Telecom and IT

- BFSI

- Retail and E-Commerce

- Education

- Manufacturing

- Media and Entertainment

- Government and Public Sector

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We started by building a clean fact base on demand, supply, and adoption patterns tied to enterprise software spend and content governance. Public sources were used to anchor definitions and directional trends, such as guidance and data from the US Securities and Exchange Commission, the US Bureau of Labor Statistics, the National Institute of Standards and Technology, the European Union Agency for Cybersecurity, and the OECD.

After that, we reviewed company filings, investor decks, product documentation, association websites, and reputable press coverage to map typical ECM deployment patterns and buying triggers. A paid subscription focused on company financials and news was used to sanity check revenue exposure and regional mix for relevant suppliers, and a paid patent database was used to spot where workflow, records, and content security features were evolving. These desk sources are illustrative only, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the desk assumptions and to fill gaps around pricing ranges, cloud migration timing, and how buyers bundle software with services. We spoke with a mix of solution providers, channel partners, system integrators, and enterprise users across major regions so adoption differences by regulation, industry, and IT maturity could be reflected in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 18% | APAC: 42% |

| Mid tier: 43% | Functional/Unit leaders: 39% | EMEA: 35% |

| Smaller Players: 18% | Managers: 43% | Americas: 23% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs the addressable ECM spend pool from enterprise software and IT services spending signals, and then applies adoption and attach-rate logic for content capture, workflow, and governance use cases by region. Once those totals were formed, they were corroborated with selective bottom-up approximations, such as sampled vendor revenue exposure checks, channel feedback on deal sizes, and modeled volume times ASP for common user and repository scale bands.

A few inputs that mattered in practice included the pace of cloud migration for content workloads, compliance pressure tied to retention and audit needs, growth in unstructured data volumes, the split between subscription and maintenance contracts, and typical implementation effort for regulated industries. Where direct bottom-up visibility was limited, gaps were handled through conservative penetration ranges that were validated in interviews, and then adjusted only when multiple independent responses aligned.

For forecasting, we used scenario analysis supported by expert inputs on macro IT budgets, security and privacy requirements, and expected changes in cloud pricing and bundling. The scenarios were then converted into a single base case by weighting them against the most common buyer plans and vendor pipeline signals reported in primary discussions.

Data Validation & Update Cycle

Outputs were checked against independent signals such as enterprise software spending direction, cloud adoption indicators, and supplier revenue commentary, and then reviewed for outliers at the region and component level. When a variance looked large, the assumption behind it was traced back to its input and re-tested through extra desk checks or a follow-up primary touchpoint.

Before sign-off, the model and write-up go through multi-step analyst review so the math, definitions, and assumptions remain consistent across sections. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or sharp shifts in enterprise IT spending. Right before delivery, a final pass is done to make sure clients receive the most current view available.

Mordor Intelligence's Enterprise Content Management Market Size Compared Against Other Published Estimates

Published market values for ECM often do not match because firms count different solution buckets, use different base years, and convert currencies using different timing and assumptions. In addition, some models lean heavily on supplier narratives, while others rely more on demand-side indicators, and both choices can move the final total.

A common driver in this market is whether stand-alone web content tools, adjacent collaboration layers, and broader digital experience spend are folded into the number. Some external figures also assume faster subscription ASP expansion or treat implementation services as fully incremental each year, which can lift the total quickly. In Mordor Intelligence's estimate, stand-alone web content tools without workflow, retention, or governance modules are not counted, and services are included only when they are directly tied to ECM deployment and ongoing support.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 44.29 B (2026) | |

| Trade Publisher A | USD 49.57 B (2025) | Uses a different base year and mixes solution definitions that can include broader web content management and adjacent use cases, and it also applies a higher near-term growth path that expands the 2025 starting point. |

| Industry Research Group B | USD 43.94 B (2024) | Anchors the series on a 2023 estimation base and reports a 2024 value, so year alignment alone creates a visible gap, and component treatment can differ depending on how services and applications are grouped. |

The spread in the table is largely explained by scope choices around what counts as ECM and by base-year alignment, which then flows into different growth paths. By keeping the inputs tied to observable adoption signals and by keeping inclusions and exclusions explicit, the final market value stays traceable to repeatable steps that can be rechecked as new information comes in.

Key Questions Answered in the Report

What is the current value of the Enterprise Content Management market?

The Enterprise Content Management market is valued at USD 44.29 billion in 2026.

How fast is cloud deployment growing within this space?

Cloud deployment revenue is forecast to rise at a 13.91% CAGR through 2031.

Which region will expand the quickest by 2031?

Asia Pacific is projected to record a 13.51% CAGR, the fastest of any region.

Why is Healthcare investing heavily in ECM?

Electronic health record integration and HIPAA-driven audit demands are pushing Healthcare spending at a 13.66% CAGR through 2031.

What pricing trend is reshaping SME adoption?

Token-based consumption pricing lets SMEs pay only for actual usage, cutting upfront costs.

Which driver has the greatest influence on future growth?

The explosion of unstructured data, with a +3.2% impact on the forecast CAGR, is the most influential driver.

Page last updated on: