360-Degree Feedback Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

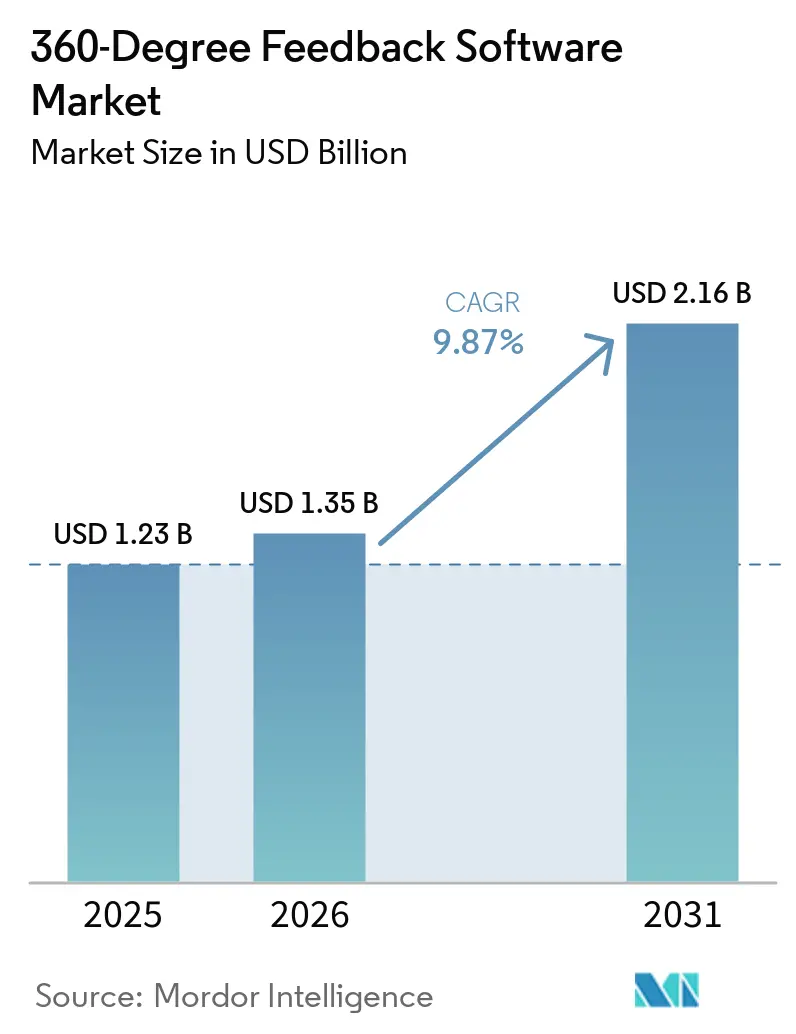

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 2.16 Billion |

| Growth Rate (2026 - 2031) | 9.87% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

360-Degree Feedback Software Market Analysis by Mordor Intelligence

The 360-degree feedback software market size is expected to grow from USD 1.23 billion in 2025 to USD 1.35 billion in 2026 and is forecast to reach USD 2.16 billion by 2031 at 9.87% CAGR over 2026-2031. Strong enterprise demand for multi-rater tools that plug into continuous performance suites, the widespread adoption of hybrid work, and rapid advances in AI-driven coaching engines are reinforcing a multi-year expansion path. Vendors that embed real-time personalization, sentiment analytics, and bias detection into their platforms enjoy a clear pricing premium, while those that rely on static survey workflows face commoditization pressures. Mergers such as Paychex-Paycor and Workday-Sana reveal how incumbents use acquisitions to secure AI talent intelligence capabilities and broaden upmarket reach. At the same time, freemium models aimed at small and medium enterprises (SMEs) are widening the funnel in South America and Asia-Pacific, signaling that the 360-degree feedback software market will remain one of the most dynamic segments of the broader human capital management stack.

Key Report Takeaways

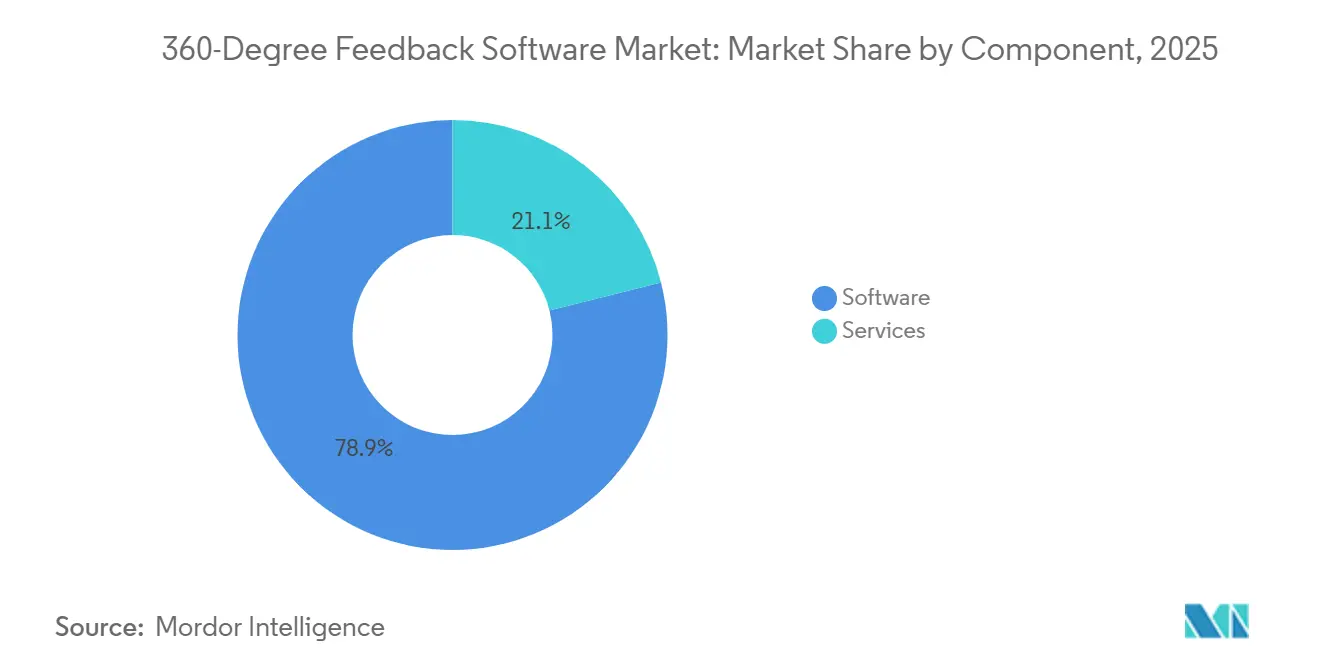

- By component, software accounted for 78.92% of the 360-degree feedback software market revenue in 2025, while services are projected to expand at a 10.96% CAGR through 2031.

- By deployment, cloud held 69.14% of the 360-degree feedback software market share in 2025, yet hybrid configurations are advancing at an 11.42% CAGR to 2031.

- By organization size, large enterprises led with 60.83% revenue share in 2025, whereas SMEs are pacing the market at an 11.88% CAGR through 2031.

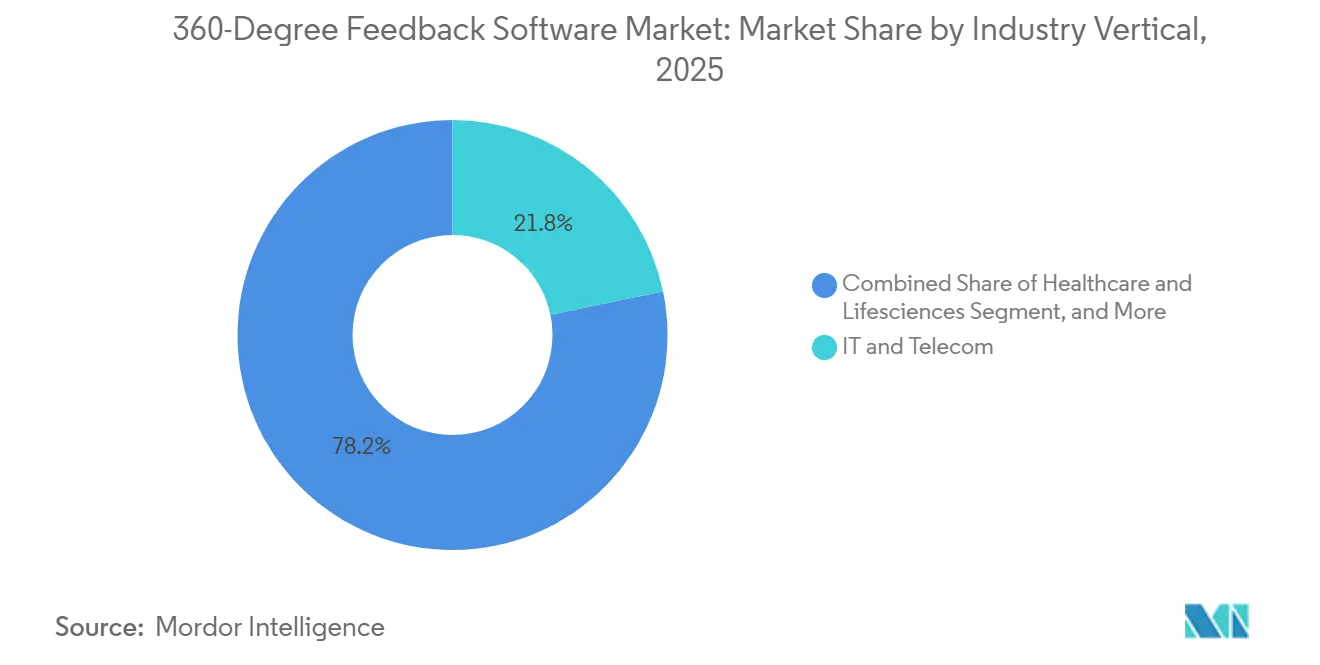

- By industry vertical, IT and telecom contributed 21.76% of the 360-degree feedback software market, 2025 revenue, while healthcare and lifesciences post the fastest 11.21% CAGR to 2031.

- By pricing model, subscription accounted for 73.41% of 2025 spending, while freemium is growing at a 12.74% CAGR during 2026-2031.

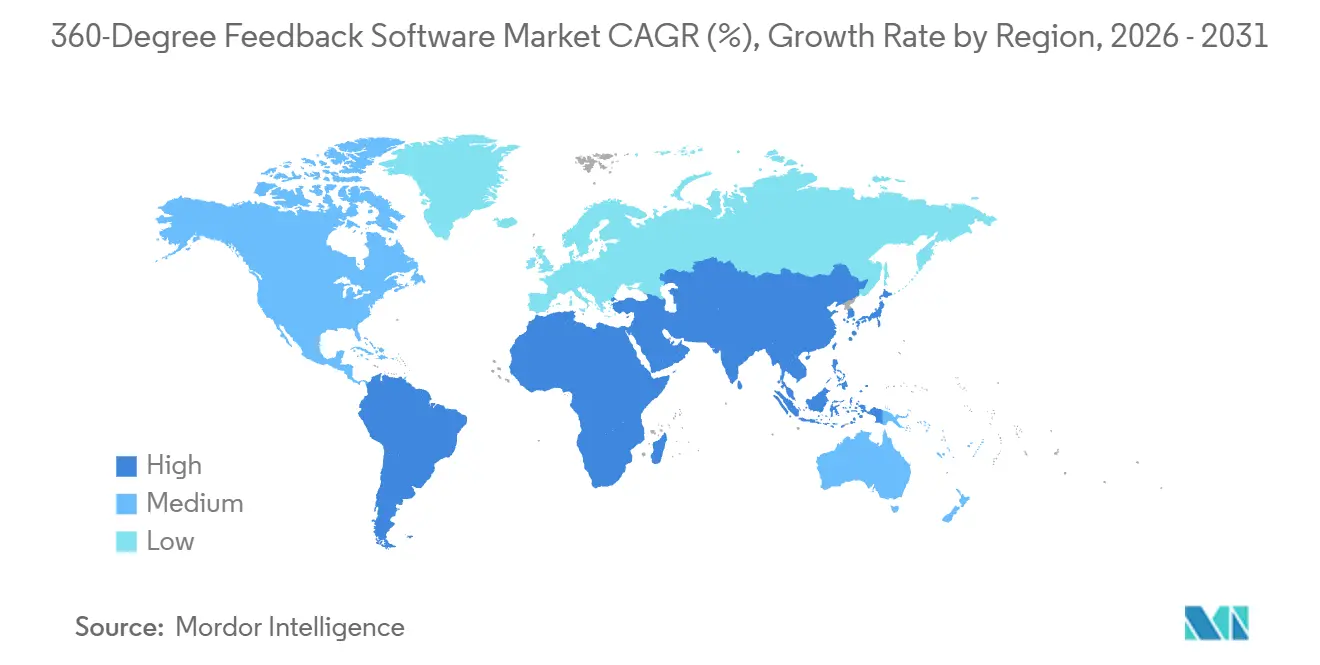

- By geography, North America dominated with 39.28% revenue share in 2025; Asia-Pacific is the fastest growing geography at a 12.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 360-Degree Feedback Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Personalized Feedback Workflows | +1.8% | Global, early lift in North America and Western Europe | Medium term (2-4 years) |

| Integration of 360-Degree Feedback Into Continuous Performance Management Suites | +1.6% | Global, strongest in North America and Asia-Pacific enterprise cohorts | Short term (≤ 2 years) |

| Expansion of Hybrid and Remote Work Operating Models | +1.4% | Global, notably in North America, Europe, and urban Asia-Pacific hubs | Short term (≤ 2 years) |

| Rising Demand for Data-Driven Leadership Development Programs | +1.2% | North America, Europe, and executive education markets in Asia-Pacific | Medium term (2-4 years) |

| Growing Adoption Across Emerging-Market SMBs via Freemium Strategies | +0.9% | Asia-Pacific, South America, Middle East and Africa | Long term (≥ 4 years) |

| Increasing Regulatory Emphasis on Objective Employee Evaluations | +0.7% | Europe, North America, Middle East public sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Personalized Feedback Workflows

Generative AI now tailors question sets to individual competency gaps and rapidly converts raw multi-rater data into coaching prompts, slashing insight lead time from weeks to hours. Microsoft Viva Glint, SAP SuccessFactors, and Oracle HCM Cloud have all released agentic AI features that surface sentiment patterns and flag rating discrepancies, prompting 48% of European HR teams to pilot specialized AI performance tools in 2025.[1]Rosanna Campbell, “How European HR Teams Are Leading in 2026,” Lattice, lattice.com Vendors unable to embed real-time personalization or bias screening risk price erosion as buyers increasingly view those capabilities as table stakes.

Integration of 360-Degree Feedback into Continuous Performance Management Suites

Quarterly reviews are replacing annual appraisals, pushing organizations to converge feedback, goal tracking, and peer recognition into unified workflows. Workday’s 2025 acquisition of Sana for USD 1.1 billion was framed as a move to weave AI-driven talent intelligence across its HCM suite, underscoring how tightly integrated analytics now shape succession planning and skill development. Stand-alone vendors, therefore, face a build-or-partner decision as cross-suite integration has become a primary buying criterion in the 360-degree feedback software market.

Expansion of Hybrid and Remote Work Operating Models

Distributed teams need asynchronous, mobile-friendly feedback mechanisms that respect multiple time zones and preserve psychological safety. A 2025 SHRM study reported that 45% of European employers already rely on digital performance tools, while 62% are consolidating HR technology stacks, confirming that hybrid work is accelerating platform adoption.[2]Society for Human Resource Management, “2025 Digital HR Adoption Study,” shrm.org Encryption, anonymous channels, and third-party administration options have emerged as must-have features to sustain rater candor in fully virtual environments.

Rising Demand for Data-Driven Leadership Development Programs

Executive education providers and corporate academies increasingly anchor curricula in measurable 360-degree data. Health systems such as Norton Healthcare linked multi-rater assessments to patient safety outcomes, while Stanford and Columbia business schools embed the surveys into leadership courses, illustrating how feedback data bolsters program ROI claims. Procurement teams now ask for outcome-based case studies rather than generic satisfaction metrics, elevating data transparency as a competitive lever.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns Over Data Privacy and Psychometric Bias | -1.1% | Global, acute in Europe and California | Short term (≤ 2 years) |

| Change-Management Challenges in Traditional Hierarchical Cultures | -0.9% | East Asia, Middle East, legacy manufacturing worldwide | Medium term (2-4 years) |

| Limited HR Tech Budgets in Micro-Enterprises | -0.6% | South America, Africa, rural Asia-Pacific | Long term (≥ 4 years) |

| Interoperability Gaps with Legacy HCM or ERP Stacks | -0.5% | Global, especially large enterprises with pre-2020 deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Concerns Over Data Privacy and Psychometric Bias

Strict statutes like GDPR and California ADMT now require transparency on algorithmic decision-making, elevating vendor compliance costs and amplifying litigation risk. A 2025 Journal of Applied Psychology article revealed that 30% of responses in large firms were skewed by rater bias, prompting buyers to demand encryption, audit logs, and statistical bias checks. Vendors lagging on these safeguards face procurement delays and potential reputational damage.

Change-Management Challenges in Traditional Hierarchical Cultures

High power-distance workplaces resist upward or peer critique, stretching roll-out timelines and depressing participation rates in the 360-degree feedback software market. Boston Consulting Group’s 2025 modeling found that mandates alone rarely shift feedback norms without local champions and extensive education. Vendors thus expend extra advisory hours to localize question tone, group feedback sessions, and post-survey coaching, inflating the total cost of ownership in East Asian and Middle Eastern deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Share as Integration Complexity Rises

Software captured 78.92% of market revenue of the 360-degree feedback software market in 2025, reflecting the dominance of license and subscription fees, yet services are projected to expand at 10.96% CAGR through 2031, outpacing the overall market rate. SurveyConnect observed that 40% of HR teams in firms above 5,000 employees failed to create actionable dashboards within a month, catalyzing demand for advisory projects.[3]Audrey Hogan, “Challenges of 360-Degree Feedback in Large Organizations,” surveyconnect.com As a result, vendors now bundle quarterly calibration workshops into premium tiers, blending software and services in one subscription.

The 360-degree feedback software market benefits as service partners monetize rater-training, psychometric validation, and culture-change roadmaps, especially in regulated verticals where GDPR or healthcare accreditation demands third-party attestation. Paychex's January 2025 announcement of its USD 4.1 billion acquisition of Paycor highlighted expected run-rate cost synergies exceeding USD 80 million, with substantial revenue synergy opportunities tied to cross-selling implementation and advisory services across a combined customer base of approximately 745,000 clients.

By Deployment: Hybrid Configurations Accelerate in Regulated Industries

Cloud deployment commanded 69.14% of the 360-degree feedback software market share in 2025, driven by scalability, automatic updates, and lower upfront capital expenditure, yet hybrid configurations are growing at 11.42% CAGR through 2031, the fastest rate among deployment models. UAE regulations that require federal employee records to stay on national soil have spurred interest in private cloud nodes hosted in domestic data centers. SAP’s 2026 SuccessFactors release leverages cloud infrastructure for real-time AI while supporting customer-controlled storage for compensation files, illustrating how large vendors balance sovereignty and agility.

Hybrid architectures appeal to financial services, healthcare, and government entities that must balance data sovereignty mandates with the agility and AI capabilities of cloud-native platforms. On-premises deployments persist in legacy manufacturing firms and defense contractors where air-gapped networks and stringent cybersecurity protocols prohibit cloud connectivity, though this segment is contracting as vendors phase out on-premises support in favor of private cloud instances hosted in customer-controlled data centers.

By Organization Size: SMBs Adopt Freemium Models to Bypass Budget Constraints

Large enterprises held 60.83% of market share in 2025, reflecting their ability to negotiate enterprise licensing agreements and absorb implementation costs, yet small and medium-sized enterprises are adopting at 11.88% CAGR through 2031, the fastest growth rate by organization size. This acceleration is driven by freemium go-to-market strategies that eliminate upfront licensing fees and allow SMBs to pilot 360-degree feedback with limited user cohorts before committing to paid tiers. HR Cloud's freemium model, which offers basic feedback functionality at no cost and monetizes through advanced analytics and integrations, exemplifies this approach, as do regional specialists in South America such as Gupy, Smartleader, and Mandü, which provide Portuguese and Spanish-language platforms tailored to local labor regulations and SMB budgets.

Talent Strategy Group reported that 88% of store managers engaging with TruRating’s TruCoaching consume insights on mobile, underscoring how lightweight, phone-first designs resonate with smaller firms.[4]Talent Strategy Group, “Mobile Consumption of HR Analytics,” talentstrategygroup.com Yet micro-enterprises still struggle to allocate staff to design competency libraries, which remains a barrier until AI-assisted setup wizards become mainstream. As SMEs graduate to paid tiers, upsell levers center on advanced analytics, integrations, and security certifications, reinforcing recurring revenue durability inside the 360-degree feedback software market.

By Industry Vertical: Healthcare Accelerates Amid Accreditation Pressures

IT and telecom accounted for 21.76% of market share in 2025, reflecting early adoption of digital HR tools and a cultural affinity for data-driven performance management, yet healthcare and lifesciences are expanding at 11.21% CAGR through 2031, the fastest rate among industry verticals. This surge is propelled by Joint Commission accreditation requirements that mandate objective competency assessments for clinical staff, the need to link 360-degree feedback to patient safety metrics, and the proliferation of value-based care models that tie reimbursement to team performance. Norton Healthcare used Perceptyx assessments to tie leadership behavior to safety metrics, providing a data trail that meets auditor and board governance requirements.

BFSI captured the second-largest share after IT and telecom, driven by regulatory scrutiny of risk management practices and the need for transparent succession planning in client-facing roles. Conversely, IT and telecom, already digital-savvy, continue to invest for iterative coaching but at a slower clip because penetration rates are high. Retail uptake is buoyed by TruCoaching, which distills customer transaction feedback into weekly action plans and demonstrates rapid revenue lift for frontline teams.

By Pricing Model: Freemium Surges as Vendors Target Emerging Markets

Subscription-based pricing accounted for 73.41% of revenue in 2025, reflecting the dominance of per-user-per-month SaaS models that align vendor revenue with customer growth. Yet freemium models are expanding at a 12.74% CAGR through 2031, the fastest rate among pricing structures. Freemium strategies lower the barrier to entry for SMBs and emerging-market enterprises that lack upfront capital for perpetual licenses or multi-year subscriptions, enabling vendors to capture land-and-expand opportunities by monetizing advanced features such as AI-driven coaching, custom competency libraries, and API integrations once users demonstrate engagement.

HR Cloud's tiered pricing, which offers basic feedback functionality at no cost and charges for analytics and integrations, exemplifies this model, as do South American vendors such as Gupy and Smartleader, which provide free trials and pay-per-use options tailored to cash-constrained SMBs. Perpetual or one-time license models are contracting as vendors phase out on-premises support and migrate customers to cloud subscriptions, though they persist in government and defense sectors where multi-year procurement cycles and budget approval processes favor upfront capital expenditure over recurring operational costs.

Geography Analysis

North America generated 39.28% of 2025 revenue, sustained by Fortune 500 cross-suite expansions and a compliance environment that rewards transparent talent processes. Federal contractors moving to hybrid deployments have lengthened deal cycles but lifted average contract value as buyers layer advisory and security modules. The region also benefits from early adoption of AI-enabled HR tools, which enhances analytics-driven decision-making and accelerates platform upgrades. Additionally, strong vendor ecosystems and high HR tech spending capacity continue to reinforce North America’s leadership position.

Europe posts slower topline growth yet enjoys sticky renewal rates because GDPR heightens vendor switching costs. Lattice data show 51% of European firms run quarterly reviews, cementing demand for continuous feedback loops. High legal scrutiny means buyers favor platforms that provide clear audit trails and automated deletion workflows, adding complexity that protects incumbent penetration. This regulatory environment encourages long-term vendor relationships and increases demand for compliant, enterprise-grade solutions. Moreover, multilingual workforce requirements further drive the need for customizable and localized platforms.

Asia-Pacific is the clear volume driver with a 12.36% CAGR. Indian vendors such as Darwinbox localize labor codes and offer vernacular interfaces while Chinese state-owned enterprises modernize talent oversight under national digitalization programs. Cultural hesitancy toward upward feedback persists in Japan and South Korea, so vendors invest in anonymity guarantees and group discourse formats that sustain user confidence without violating face-saving norms. Rapid SME digitization and cost-sensitive SaaS adoption are also expanding the addressable market across the region. In addition, increasing government-led digital transformation initiatives are accelerating enterprise adoption of structured feedback systems.

Competitive Landscape

Competition remains high and stands moderately fragmented, with no vendor exceeding a 15% share and strategies split between horizontal HCM providers and experience-focused specialists. SAP’s 2025 buyout of SmartRecruiters and Workday’s Sana acquisition highlight efforts to unify sourcing, performance, and learning into AI-driven suites. Oracle responded with AI Agents in the same period to defend its position and maintain competitiveness. This consolidation trend reflects a broader push toward integrated, end-to-end HR ecosystems.

Niche players such as Lattice, 15Five, and Culture Amp continue to win mid-market deals by focusing on ease of use, strong integrations with tools like Slack, and intuitive, consumer-grade interfaces. They compensate for relatively smaller R&D budgets through partnerships for localization and by leveraging freemium, community-driven adoption strategies. Their ability to deliver quick deployment and user-friendly experiences makes them attractive for growing organizations.

Emerging disruptors such as Darwinbox, Zoho, and Gupy are gaining traction in Asia-Pacific and South America by offering competitive pricing and region-specific content capabilities. TruRating is carving out a niche with transaction-linked 360 feedback tailored for retail environments, demonstrating how specialized use cases can create distinct opportunities within the market. This highlights the increasing importance of vertical-focused solutions in driving differentiation.

360-Degree Feedback Software Industry Leaders

Culture Amp Pty Ltd

Qualtrics LLC

Momentive Global Inc.

Cornerstone OnDemand Inc.

Workday Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: UKG retired UKG Pro Backoffice, migrating clients to UKG One View to tighten links between payroll and 360-degree feedback modules.

- January 2026: TruRating launched TruCoaching, an AI module that turns point-of-sale feedback from 88% of in-store shoppers into weekly coaching prompts for retail staff.

- September 2025: SAP completed the acquisition of SmartRecruiters to embed recruiting analytics into SuccessFactors and cross-sell 360-degree feedback modules.

- September 2025: Workday finalized its USD 1.1 billion Sana purchase, adding talent intelligence that unifies feedback, skills, and learning.

Global 360-Degree Feedback Software Market Report Scope

The 360-degree feedback software market refers to the revenue generated from digital platforms that collect, manage, and analyze multi-source employee feedback, including peer, manager, and subordinate feedback, as well as self-assessments. These solutions enable organizations to evaluate employee performance, leadership effectiveness, and behavioral competencies through structured and continuous feedback processes.

The 360-Degree Feedback Software Market Report is Segmented by Component (Software, and Services), Deployment (Cloud, On-premises, and Hybrid), Organization Size (Small and Medium-sized Enterprises, and Large Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Lifesciences, Retail and E-commerce, Manufacturing, Government and Public Sector, and Other Industry Verticals), Pricing Model (Subscription-Based, Perpetual/One-Time License, Usage-Based/Pay-Per-Use, and Freemium), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-premises |

| Hybrid |

| Small and Medium-sized Enterprises |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Manufacturing |

| Government and Public Sector |

| Other Industry Verticals |

| Subscription-Based |

| Perpetual / One-Time License |

| Usage-Based / Pay-Per-Use |

| Freemium |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment | Cloud | |

| On-premises | ||

| Hybrid | ||

| By Organization Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | IT and Telecom | |

| BFSI | ||

| Healthcare and Lifesciences | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Other Industry Verticals | ||

| By Pricing Model | Subscription-Based | |

| Perpetual / One-Time License | ||

| Usage-Based / Pay-Per-Use | ||

| Freemium | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the 360-degree feedback software market be by 2031?

The 360-degree feedback software market size is forecast to reach USD 2.16 billion by 2031, expanding at a 9.87% CAGR, according to Mordor Intelligence.

Which deployment model is growing the fastest?

Hybrid deployments post the highest 11.42% CAGR to 2031 as regulated industries balance data sovereignty with cloud analytics.

Why are services gaining share in the 360-degree feedback software industry?

Organizations need integration, change-management, and analytics consulting, pushing services revenue to a 10.96% CAGR through 2031.

Which region will outpace others in growth?

Asia-Pacific is projected to grow at a 12.36% CAGR as India and China digitize HR processes and local vendors offer freemium entry points.

What is driving healthcare adoption of 360-degree feedback?

Joint Commission accreditation and ties between competency reviews and patient safety metrics propel healthcare and lifesciences at an 11.21% CAGR.

Page last updated on: