Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

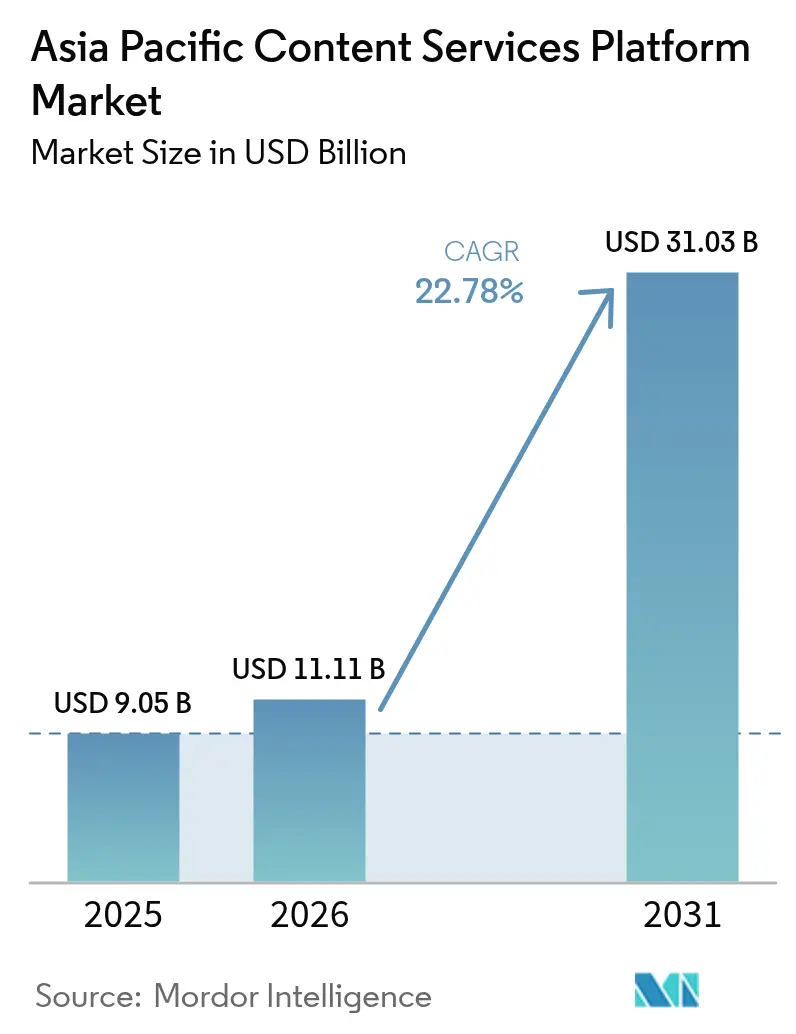

| Base Year Market Size (2025) | USD 9.05 Billion |

| Market Size (2026) | USD 11.11 Billion |

| Market Size (2031) | USD 31.03 Billion |

| Growth Rate (2026 - 2031) | 22.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Content Services Platform Market Analysis by Mordor Intelligence

The content services platform market size in Asia-Pacific in 2026 is estimated at USD 11.11 billion, growing from 2025 value of USD 9.05 billion with 2031 projections showing USD 31.03 billion, growing at 22.78% CAGR over 2026-2031. Momentum stems from accelerating cloud-first mandates, mounting volumes of unstructured data, and rapid progress in AI-driven document intelligence across enterprises. China’s data-residency rules and India’s Digital India program are reshaping vendor strategies, while ASEAN subsidies keep adoption barriers low for small businesses. Edge-ready architectures that exploit 5G, growth in compliant cloud regions, and sustainability-linked storage criteria are emerging as the next battlegrounds. Competitive intensity remains moderate as global suites vie with regional specialists that offer localization, regulatory assurance, and vertical depth.

Key Report Takeaways

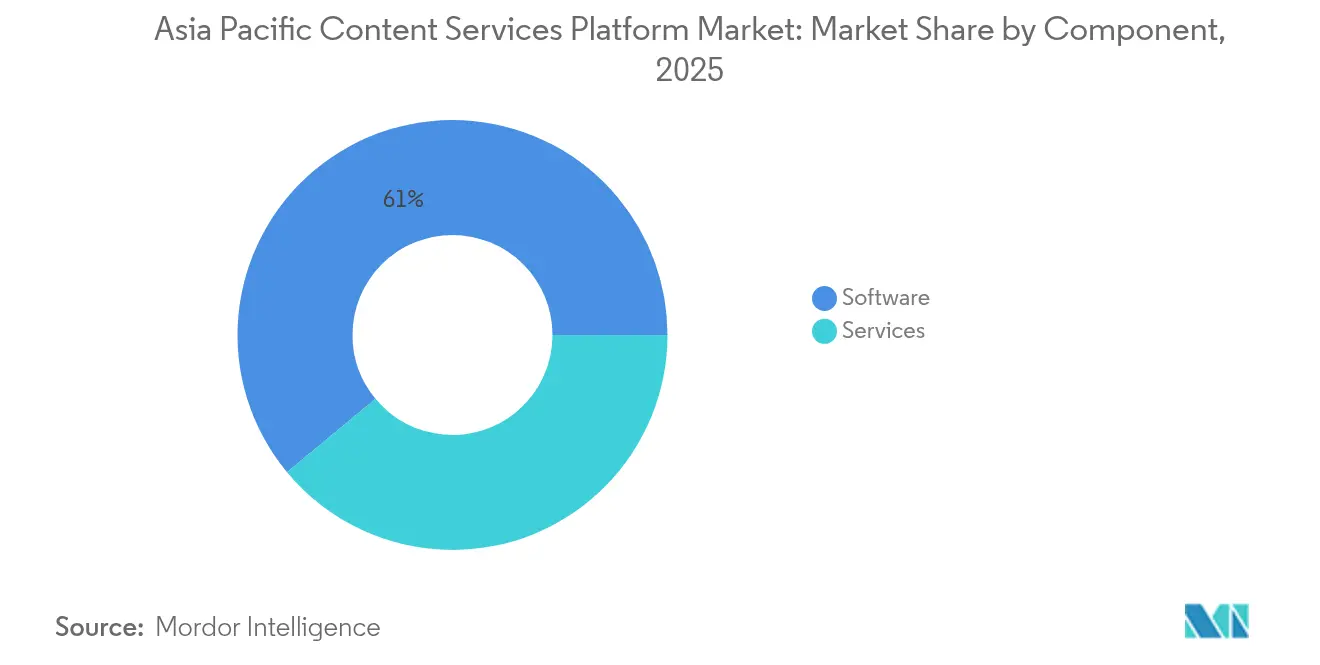

- By component, software retained 61.02% of the content services platform market share in 2025; services are expanding at a 23.95% CAGR to 2031.

- By deployment model, the cloud segment commanded 69.78% of the content services platform market size in 2025 and is set to advance at 24.99% CAGR.

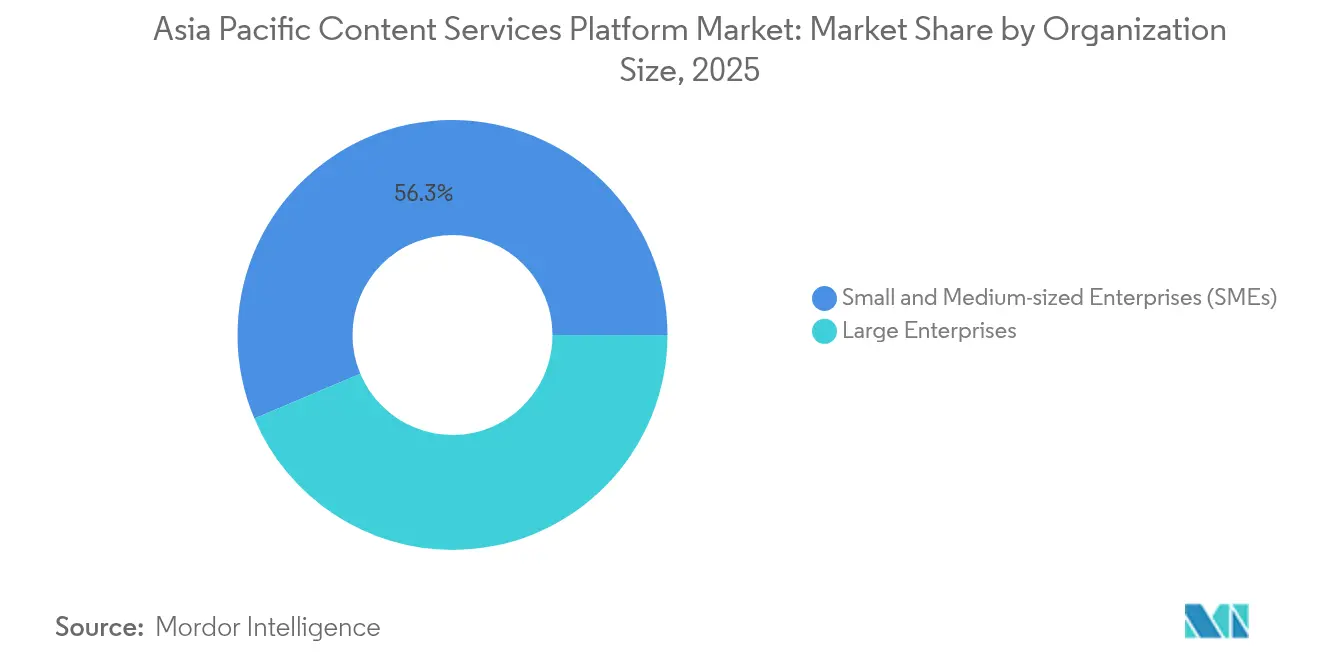

- By organization size, large enterprises captured 43.66% of 2025 revenue, whereas SMEs are scaling at 23.62% CAGR.

- By end-user industry, BFSI led with 25.02% share of the content services platform market size in 2025; retail and e-commerce are rising at 23.18% CAGR.

- By geography, China dominated with 27.52% share in 2025; India is registering the fastest 23.42% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Content Services Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first spending boom across ASEAN and India | +4.2% | ASEAN core markets, India primary | Medium term (2-4 years) |

| Generative-AI infused content intelligence add-ons | +3.8% | Global, with China and Japan leading | Short term (≤ 2 years) |

| SME digital-workflow subsidies (e.g., Singapore DSG grants) | +2.1% | Singapore, Malaysia, Thailand | Medium term (2-4 years) |

| 5G-enabled edge content processing for field operations | +1.9% | South Korea, Japan, Australia | Long term (≥ 4 years) |

| Mandatory e-invoicing regulations in Japan and Korea | +1.7% | Japan, South Korea | Short term (≤ 2 years) |

| Carbon-accounted content storage buying criteria | +1.4% | Australia, Singapore, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-first spending boom across ASEAN and India

Regional cloud infrastructure investment surged 117% between 2019 and 2024, lifting the content services platform market as businesses traded legacy repositories for scalable SaaS suites.[1]GSMA Intelligence, “The Mobile Economy Asia Pacific 2024,” gsma.comMicrosoft’s USD 1.7 billion Indonesian cloud buildout and double-digit Office 365 APAC growth illustrate vendor commitment. Financial services institutions are front-loading projects to satisfy cloud-adoption mandates, widening demand for compliant document workflows. Singapore’s Advanced Digital Solutions grants that cover 50% of project costs have guided more than 450 solutions into production, driving replication across Malaysia and Thailand. The compounding influence of public-sector funding, hyperscaler expansion, and peer success stories positions cloud as the default architecture for the content services platform market over the next three years.

Generative-AI infused content intelligence add-ons

Enterprises are tripling Gen-AI budgets to USD 3.4 billion in 2024, steering platforms from passive storage toward insight engines.[2]IBM Corporation, “IBM Q1 2025 Earnings,” ibm.com IBM exceeded USD 6 billion in Gen-AI revenue on the strength of APAC deployments that automate classification, redaction, and summary creation. Adobe’s Document Cloud integrated AI features that extract structured data, supporting record Q3 2024 revenue of USD 5.41 billion, with APAC at 14.1% of turnover. ServiceNow supplemented search precision through the Raytion acquisition, confirming that AI enrichment is table-stakes for leadership. Early adopters report 70% decreases in manual processing time, validating positive ROI. The shift is not merely feature-led—it reshapes buyer criteria, repositioning the content services platform market as an intelligent knowledge fabric.

SME digital-workflow subsidies

Government grants across ASEAN counter the twin hurdles of budget and skills for small firms. Singapore’s Productivity Solutions Grant and CTO-as-a-Service fund up to half of project costs and advisory fees.[3]Infocomm Media Development Authority, “SMEs Go Digital Programme,” imda.gov.sg Malaysia’s Digital Economy Blueprint earmarks resources so SMEs can embed workflow automation into core operations. AvePoint’s 29% APAC revenue growth, with SMEs contributing a rising share, underscores how subsidies convert latent interest into tangible deals. Catalogues of pre-approved solutions reduce procurement cycles while ensuring local compliance. The multiplier effect shows in vendor channel expansion, as partners replicate templates from Singapore to Vietnam and the Philippines. Subsidy continuity through 2027 is expected to keep SME uptake on a steep trajectory.

5G-enabled edge content processing for field operations

Full-scale 5G rollouts enable real-time ingestion and synchronization of high-resolution files in manufacturing, healthcare, and logistics. Factories in South Korea cite 15-20% efficiency gains from instant QC documentation that syncs with centralized repositories. Hospitals stream HD video and imaging to remote surgeons, prompting demand for low-latency content pipelines. Logistics providers report 25% faster picking through 5G-ready document viewers. Construction firms use edge-capable platforms to fetch blueprints and safety protocols onsite, trimming delays. Japan and Australia lead the pilot wave while ASEAN operators invest in stand-alone 5G cores. As coverage widens, vendors are re-architecting for distributed processing while maintaining centralized governance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-residency splinter-net (China CSL, India DPDP) | -2.8% | China, India primary, spillover to ASEAN | Short term (≤ 2 years) |

| Scarcity of in-region hyperscale datacenter capacity outside tier-1 cities | -1.9% | Southeast Asia, India tier-2/3 cities | Medium term (2-4 years) |

| Skills gap in low-code workflow design | -1.4% | Global, acute in emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Rising subscription fatigue among mid-market buyers | -1.1% | Global, pronounced in mature Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-residency splinter-net

China’s Network Data Security Management Regulations effective January 2025 force cross-border disclosure reviews and local processing for “important data,” raising compliance cost for multinational suites. India’s Digital Personal Data Protection Act demands explicit consent layers and localization that reshape software architecture. Vendors now maintain variant builds per jurisdiction, eroding economies of scale. Mid-market firms lack budgets for multiregional governance, slowing adoption. Vietnam is drafting similar rules, signaling more fragmentation. While the content services platform market continues to grow, these policies clip near-term velocity and favor local incumbents.

Scarcity of hyperscale datacenter capacity outside tier-1 cities

The APAC colocation footprint reached 10,233 MW in 2023 yet remains concentrated in Singapore, Tokyo, and Sydney. Secondary cities endure long lead times and higher network latency. Alibaba Cloud’s retreat from Australia and India highlights margin pressure when volumes are thin . Southeast Asia is still 55–70% under-penetrated relative to the US and China, constraining edge performance for document-heavy workloads. AI builds will add 14.7 GW but mostly in mature hubs, widening the gap. For the content services platform market, limited regional redundancy increases outage risk and tempers expansion plans in high-potential interiors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services acceleration amid software maturity

Software continued to anchor 61.02% of 2025 revenue, led by document and records management modules essential for compliance in the content services platform market. However, services posted the fastest 23.95% CAGR as enterprises sought expert integration and change-management support. The shift elevates implementation partners in vendor ecosystems. Hyland’s Hyderabad hub and rollout of DDMS 2.0 to 35 000 Malaysian users illustrate how consultative delivery unlocks large public-sector deals. AI-driven data-capture innovations are compressing onboarding cycles while workflow suites converge with process-automation platforms. Security and governance upgrades remain non-negotiable as regional privacy laws tighten.

The services pivot translates into higher attach rates and recurring revenue, favoring vendors that embed domain expertise. Engagement models are migrating from license plus maintenance toward outcome-based managed services. As a result, the content services platform market size tied to services is projected to widen its contribution through 2031. Vendors that deliver continuous optimization and regulatory updates are expected to consolidate accounts, raising switching costs and supporting premium pricing.

By Deployment Model: Cloud dominance accelerates

Cloud options secured 69.78% of the 2025 content services platform market share and are forecast for 24.99% CAGR. Enterprises appreciate consumption-based pricing and seamless API integrations that align with broader digital roadmaps. Microsoft’s 400 million paid Office 365 seats demonstrate platform pull for content-centric collaboration. Hybrid and on-premise models persist within heavily regulated verticals, yet even these users adopt cloud connectors for external collaboration. Vendors now emphasize regional PoPs and sovereign-cloud offsets to satisfy data-locality clauses.

The economic case deepens as hyperscaler nodes proliferate and marketplace billing streamlines procurement. Adobe’s Document Cloud thrives on cross-suite coherence, mirroring buyer preference for unified, cloud-native ecosystems. Consequently, the content services platform market size linked to cloud deployments is expected to eclipse 80.54% by 2031 as SME adoption surges and large enterprises migrate phased workloads.

By Organization Size: SME momentum builds

Large enterprises still generated 43.66% of 2025 spend through complex, multi-repository estates that demand enterprise-grade governance. Yet SMEs delivered the fastest 23.62% CAGR, empowered by grants and low-code interfaces. Singapore’s subsidies led to an influx of first-time buyers, while Malaysia’s blueprint channels funds to regional resellers. Cloud delivery removes upfront capex, making enterprise-grade tools accessible. AvePoint captured this wave, reporting APAC revenue gains that outpaced global averages.

The trajectory signals a democratization of functionality. Vendors craft tiered packages with pre-built workflows and chatbot help desks tailored to SMEs. Community enablement and learning portals keep support overhead low. As these firms scale, account expansion becomes a key driver, reinforcing lifetime value within the content services platform market.

By End-user Industry: BFSI leadership with retail acceleration

Financial institutions controlled 25.02% of 2025 revenue because of strict reporting, KYC, and risk-audit obligations. Document lifecycles in banking remain mission-critical, spurring early adoption of AI tagging and consent-management modules. Retail and e-commerce now exhibit the highest 23.18% CAGR, mirroring APAC’s 61% share of global online retail by 2025. Omnichannel merchants require synchronized product details, marketing media, and localized compliance wrappers across storefronts.

Government, healthcare, and telecom sectors maintain steady demand as each confronts data-sovereignty rules and customer-centric digital experiences. Transportation and logistics firms digitize shipping paperwork to manage supply-chain volatility. Diversification reduces vendor concentration risk and expands the use-case repertoire that underpins the content services platform industry.

Geography Analysis

China retained 27.52% of 2025 spend, supported by stringent residency laws that privilege domestic processing and by a vast enterprise pool seeking AI-ready governance tools. Tencent Cloud’s TCI ECM platform wins traction under these conditions, while foreign suites juggle licensing and compliance workarounds. Demand growth remains resilient as new security norms compel continuous upgrades within the content services platform market.

India delivered a 23.42% CAGR, the fastest in the region, propelled by Digital India, rapid SME cloud uptake, and plentiful IT-services talent. Tier-2 and tier-3 clusters follow metros in embracing workflow automation. Tata Consultancy Services’ BaNCS Content Suite secures domestic banks, while Microsoft and Adobe scale local zones to navigate the DPDP Act. Regulatory clarity and subsidy continuity underpin forward momentum.

Japan, South Korea, and Australia/New Zealand exhibit mature yet evolving dynamics. Japan pushes e-invoicing and lean processing. South Korea accelerates manufacturing digitization through 5G. Australia prioritizes carbon-accounted storage in procurement. Emerging economies such as Thailand, Vietnam, and the Philippines form the Rest of APAC, posting double-digit growth via public-sector master plans, thus broadening the addressable content services platform market.

Competitive Landscape

The content services platform market features moderate fragmentation, with global suites such as Microsoft, Adobe, and IBM dovetailing content modules into larger productivity and AI clouds. Regional contenders like Tencent Cloud and Tata Consultancy Services secure share through localized hosting and compliance assurance. The battlefield centers on cloud, AI enrichment, and verticalized templates.

MandA activity reflects consolidation. Hyland bought Nuxeo and Alfresco to embed modern asset services, then unveiled the Content Innovation Cloud that fuses analytics across repositories. ServiceNow’s Raytion deal sharpened federated search while Salesforce scooped Zoomin to deepen unstructured data management. Private-equity entry, exemplified by TA’s stake in SER, injects capital for geographic push.

White-space exists in healthcare imaging, government records, and manufacturing quality compliance, domains where specialized workflows offer entry barriers. Vendors with sovereign-cloud alignment and AI explainability stand to differentiate. Price discipline is emerging as buyers confront subscription fatigue, pushing suppliers toward bundled tiers and value-based metrics within the content services platform market.

Asia Pacific Content Services Platform Industry Leaders

IBM Corporation

Microsoft Corporation

OpenText corporation

Oracle Corporation

Box Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SER welcomed a strategic growth investment from TA Associates to accelerate international expansion and AI innovation.

- January 2025: OPEXUS and Casepoint merged with majority investment from Thoma Bravo to build a unified platform with broader APAC reach.

- December 2024: M-Files completed a majority recapitalization led by Haveli Investments and Bregal Milestone to boost AI automation.

- September 2024: Hyland introduced The Content Innovation Cloud for AI-driven insights across repositories.

Asia Pacific Content Services Platform Market Report Scope

The term "content service platform" primarily refers to software created on SaaS that enables users to exchange, collaborate, and produce audio & video content. The content service platform involves features such as data capture, document and record management, workflow management, and indexing. Due to the existence of features like information management, contact management, and vendor invoice management, content service platforms are now vastly employed in businesses.

The Asia Pacific Content Services Platform Market is segregated By Component (Solution/Software, Services ), Deployment Type (On-premise, cloud), By Organization Size (Small and Medium-sized Enterprises, Large Enterprises), End-user Industry (BFSI, Government and Public Sector, Healthcare and Life Sciences, IT, Telecom, Retail, E-commerce, Transportation and Logistics), and Geography.

By Component

| Solution / Software | Document and Records Management |

| Data Capture | |

| Workflow / Case Management | |

| Information Security and Governance | |

| Other Solutions | |

| Services |

By Deployment Model

| Cloud |

| On-premise / Hybrid |

By Organization Size

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

By End-user Industry

| BFSI |

| Government and Public Sector |

| Healthcare and Life Sciences |

| IT and Telecom |

| Retail and E-commerce |

| Transportation and Logistics |

| Other Industries |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Component | Solution / Software | Document and Records Management |

| Data Capture | ||

| Workflow / Case Management | ||

| Information Security and Governance | ||

| Other Solutions | ||

| Services | ||

| By Deployment Model | Cloud | |

| On-premise / Hybrid | ||

| By Organization Size | Small and Medium-sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-user Industry | BFSI | |

| Government and Public Sector | ||

| Healthcare and Life Sciences | ||

| IT and Telecom | ||

| Retail and E-commerce | ||

| Transportation and Logistics | ||

| Other Industries | ||

| By Country | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the APAC content services platform market?

The market is valued at USD 11.11 billion in 2026 and is projected to grow at a 22.78% CAGR to USD 31.03 billion by 2031.

Which deployment model is growing fastest?

Cloud deployment leads with 69.78% share in 2025 and is forecast for 24.99% CAGR as enterprises favor scalable, compliant SaaS platforms.

Why is India the fastest-growing geography?

Digital India incentives, rising SME cloud adoption, and strong domestic IT services capabilities underpin a 23.42% CAGR through 2031.

How are government subsidies affecting SME adoption?

Programs like Singapore’s Productivity Solutions Grant cover up to 50% of project costs, triggering rapid SME uptake of content workflows.

Page last updated on: