Cloud Enterprise Content Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

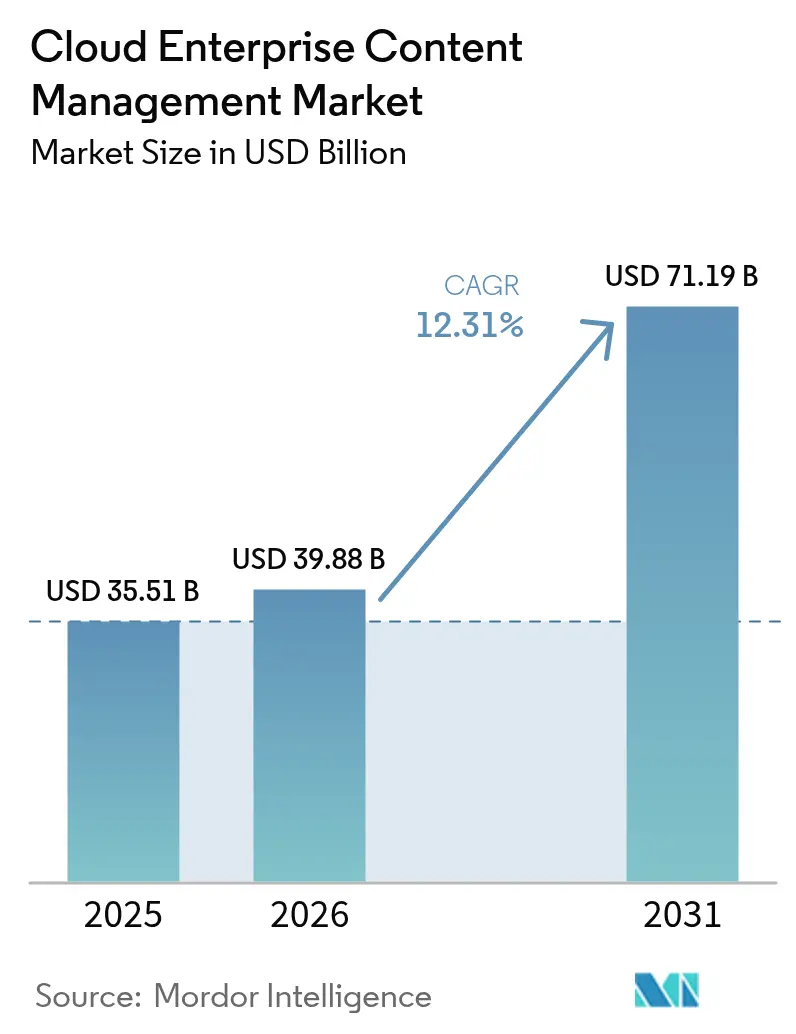

| Market Size (2026) | USD 39.88 Billion |

| Market Size (2031) | USD 71.19 Billion |

| Growth Rate (2026 - 2031) | 12.31% CAGR |

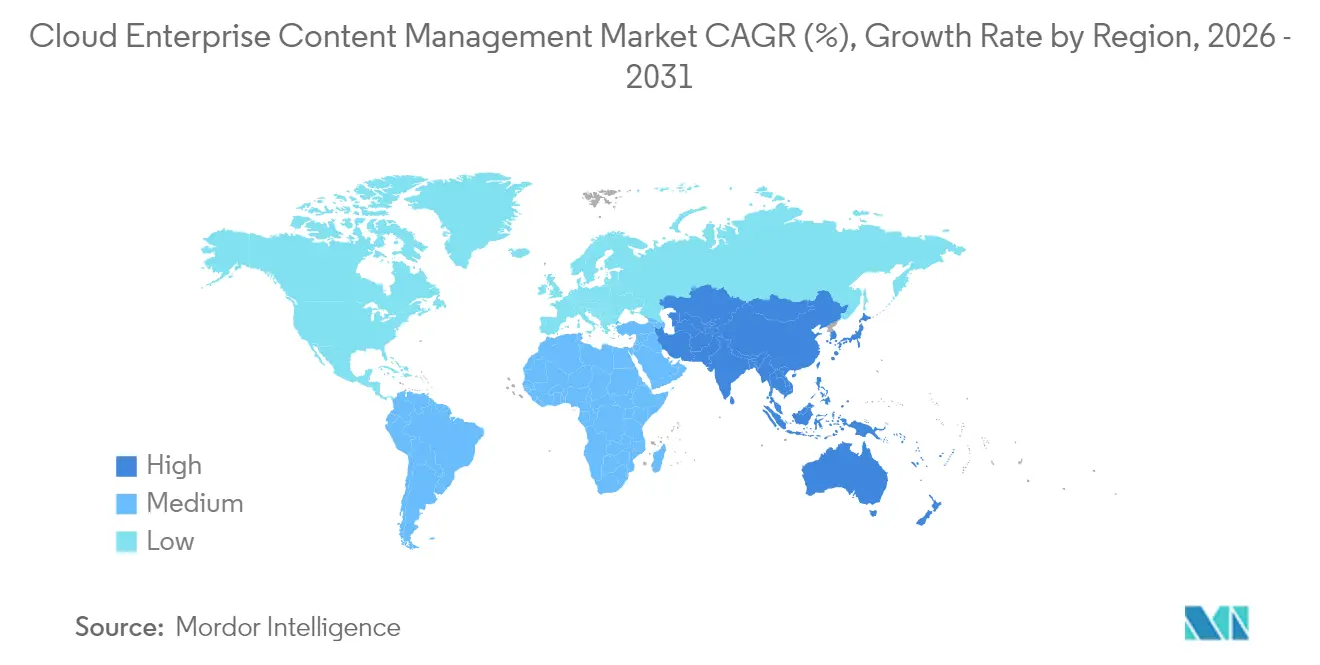

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Enterprise Content Management Market Analysis by Mordor Intelligence

The cloud enterprise content management market size was valued at USD 35.51 billion in 2025 and estimated to grow from USD 39.88 billion in 2026 to reach USD 71.19 billion by 2031, at a CAGR of 12.31% during the forecast period (2026-2031). Heightened board-level concern over unstructured-data risk, stricter global privacy statutes, and rapid advances in generative artificial intelligence are reshaping buyer priorities. Organizations now treat content governance as a strategic control surface, channeling budgets toward SaaS platforms that automate classification, retention, and audit logging. Public-cloud deployments dominate initial rollouts, yet hybrid architectures are accelerating as firms reconcile sovereignty mandates with elastic scaling. Vendors are embedding confidential computing and tokenization to unlock workloads previously restricted to on-premise vaults, while managed-service specialists absorb day-to-day administration for overstretched IT teams. Collectively, these trends position the cloud enterprise content management market for double-digit expansion even as macroeconomic pressures temper discretionary spending in other software categories.[1]U.S. Department of Health and Human Services, “21st Century Cures Act Interoperability Final Rule,” hhs.gov

Key Report Takeaways

- By deployment model, public cloud led the cloud enterprise content management market with 63.54% in 2025, whereas hybrid cloud is expected to pace the field at a 16.52% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance captured 26.72% of 2025 revenue, while healthcare is forecast to advance at a 13.78% CAGR as interoperability rules tighten.

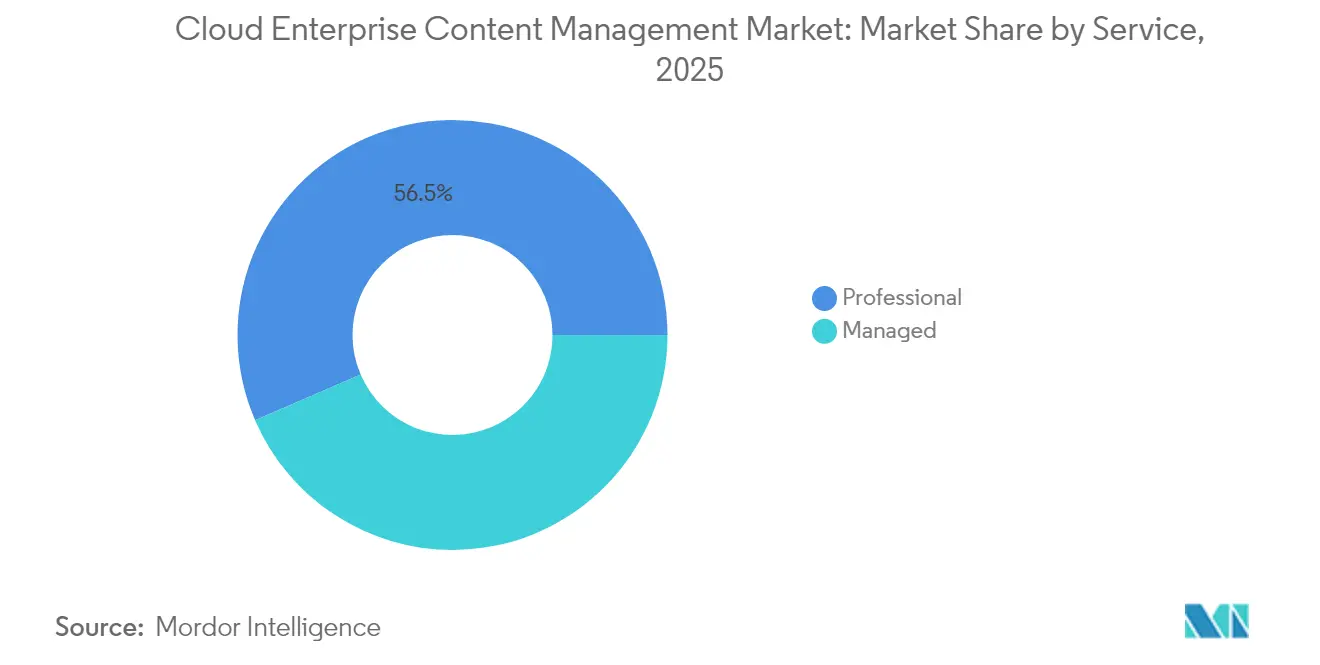

- By service, professional services commanded a 56.48% share in 2025, yet managed services are expanding at a 15.04% CAGR as firms outsource compliance monitoring.

- By organization size, large enterprises accounted for 64.42% of installations in 2025; however, the small and medium enterprise segment is scaling fastest at an 17.35% CAGR, driven by subscription pricing.

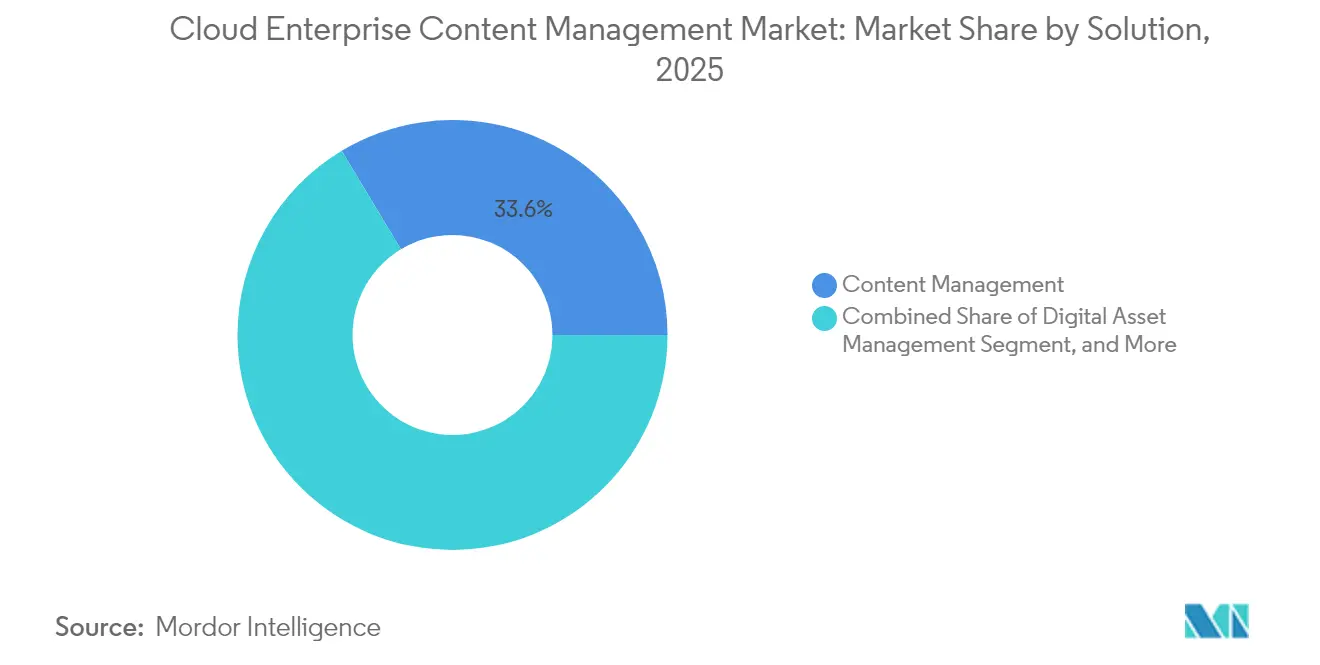

- By solution, content management remained the largest module, accounting for a 33.62% share in 2025, whereas digital asset management exhibited the fastest growth at a 15.18% CAGR driven by video-first demand.

- By geography, North America contributed 37.56% of global revenue in 2025, while the Asia Pacific is projected to track a robust 16.05% CAGR to 2031, driven by state-backed digitization mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Enterprise Content Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Powered Content Automation for Governance and Compliance | +2.8% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Growing Digital Transformation in Regulated Industries | +2.5% | Global, concentrated in BFSI and healthcare | Long term (≥4 years) |

| Increasing Adoption of Cloud Computing | +2.2% | Global, stronger uptake in the Asia Pacific and the Middle East | Medium term (2-4 years) |

| Shift Toward Remote and Hybrid Work Models | +1.8% | Global, especially North America and Europe | Short term (≤2 years) |

| Rising Enterprise Mobility and BYOD Policies | +1.5% | Global, notable in North America and the Asia Pacific | Medium term (2-4 years) |

| Confidential Computing and Tokenization Enabling Highly Secure Cloud ECM | +1.2% | North America and Europe, expanding in the Asia Pacific finance | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

AI-Powered Content Automation for Governance and Compliance

Generative AI is trimming weeks from content-governance cycles by automating classification, metadata tagging, and retention enforcement. Microsoft Copilot in SharePoint Premium now automatically drafts summaries, extracts clauses, and applies sensitivity labels, accelerating audit readiness. Early adopters, particularly in regulated verticals, report steep reductions in review backlogs and lower remediation costs after supervisory exams. OpenText Aviator enables natural-language search across legacy archives, allowing legal teams to surface non-compliant records before regulators do. Beyond efficiency, automated policy application lowers breach exposure under penalties that can reach 4% of global turnover. As tooling matures, AI-driven governance is expected to permeate mid-market deployments, solidifying its influence on the cloud enterprise content management market.[2]Microsoft Corporation, “Announcing SharePoint Premium,” microsoft.com

Growing Digital Transformation in Regulated Industries

New statutes are forcing BFSI and healthcare operators to modernize content workflows or risk sanctions. Europe’s Digital Operational Resilience Act obliges banks to store immutable vendor-interaction logs, while the U.S. 21st Century Cures Act blocks information hoarding by providers. India’s Digital Personal Data Protection Act mandates granular logs of data-access and erasure events. Unable to retrofit decades-old repositories in time, institutions are fast-tracking cloud migrations that include pre-configured retention schedules and tamper-evident logging. Vendors now ship sector templates that cut implementation cycles in half, making compliance readiness a key purchase trigger for the cloud enterprise content management market.

Increasing Adoption of Cloud Computing

Lower infrastructure costs and near-instant scalability are pulling content workloads into the broader cloud-first wave. Regional public-sector clouds in the Asia Pacific and sovereign-cloud regions in the Middle East have reduced geopolitical risk for multinationals. Meanwhile, hyperscalers bundle encryption, key management, and compliance attestations that smaller on-premise setups cannot match. As connectivity improves and platform ecosystems expand, pure on-premise installations become increasingly difficult to justify economically, sustaining baseline demand in the cloud-based enterprise content management market.

Shift Toward Remote and Hybrid Work Models

Distributed teams need universal, policy-controlled access to contracts, SOPs, and design files. Remote work surged in 2024 and remained sticky, driving firms to replace file shares and email attachments with browser-based content hubs. Seamless versioning, e-signature integration, and mobile SDKs now shape RFP criteria. Organizations that delay upgrades face fragmented compliance footprints and user frustration, which can keep conversion pipelines active for vendors over the next two years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Migration From Legacy ECM to Cloud-Native Platforms | -1.5% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Multi-Tenant Security and Compliance Concerns | -1.2% | Global, heightened in defense, pharmaceuticals, and legal | Long term (≥4 years) |

| Bandwidth Limitations in Developing Regions | -0.8% | Asia Pacific, Middle East, Africa, South America | Short term (≤2 years) |

| Vendor Lock-In Risks Limiting Strategic Flexibility | -0.7% | Global, affecting multi-cloud adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Migration From Legacy ECM to Cloud-Native Platforms

Decades of bespoke metadata, custom workflows, and proprietary file formats complicate cloud rollouts. Broken document links, missing audit trails, and incompatible retention codes stall projects, inflate budgets, and force parallel system upkeep. Financial institutions face additional hurdles because securities rules require original-format access for seven years, which slows down decommissioning plans. Skilled integrators who can navigate both legacy and cloud stacks are scarce, which pushes costs higher and dampens near-term momentum in the cloud enterprise content management market.[3]AIIM International, “State of Intelligent Information Management,” aiim.org

Multi-Tenant Security and Compliance Concerns

Highly regulated sectors fear cross-tenant leakage and inadequate role segregation. Documented misconfigurations have already exposed sensitive data, reinforcing perceptions that shared-infrastructure models conflict with zero-trust mandates. Confidential computing chips offer encrypted processing but incur double-digit performance overhead, which limits their uptake for latency-sensitive use cases. Where stakes include export-control violations or fines for protected health information, many buyers still default to private or hybrid clouds, tempering the full adoption of SaaS.[4]Cloud Security Alliance, “Top Threats to Cloud Computing 2024,”

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Digital Asset Management Rises on Rich-Media Momentum

Content management accounted for 33.62% of 2025 revenue, reflecting its stature as the repository of record for policies, SOPs, and contractual evidence. Digital asset management is growing at a 15.18% CAGR as marketing and training teams generate terabytes of video and high-resolution imagery. Enterprises running more than 1 million assets report campaign launch times 40% faster once automated tagging and version control replace ad-hoc file shares. Case management and workflow engines are popular in insurance claims and permitting offices, where multistep approvals must reconcile statutory clocks with customer SLAs. Record management retains strategic relevance for industries subject to ISO 15489 retention mandates, ensuring defensible deletion and effective management of legal holds. Collectively, these modules anchor cross-sell opportunities that raise account revenue and deepen vendor lock-in within the cloud enterprise content management market.

Workflow orchestration is reclaiming attention as no-code tooling empowers business users to automate common approvals without developer intervention. Microsoft Power Automate and OpenText AppWorks now offer drag-and-drop design canvases, reducing IT backlog and accelerating ROI. Case-management suites, such as Hyland OnBase, support government agencies in tracking citizen petitions and triggering alerts when statutory deadlines approach. Record-management features have expanded to encompass collaboration transcripts and social posts, which are now considered business records by several regulators. The convergence of these capabilities is nudging vendors toward content-services platforms that bundle capture, management, storage, preservation, and delivery functions under a single license, reinforcing a one-stop-shop positioning.

By Deployment Model: Hybrid Designs Balance Sovereignty and Scale

Hybrid architectures are expanding at 16.52% CAGR, eclipsing both pure public and private segments. Enterprises routinely retain customer financial records and IP on private cloud nodes while funneling lower-risk assets to public SaaS for elastic search and AI-based analytics. In the European Union, 73% of surveyed banks adopted hybrid frameworks to comply with GDPR localization rules, a pattern also reflected in China’s PIPL-driven mainland hosting policies. Although the public cloud held a 63.54% share of the cloud enterprise content management market in 2025, egress fees and shared-tenant concerns are steering larger buyers toward mixed estates that hedge regulatory exposure.

Private-cloud offerings remain vital for defense contractors and pharmaceutical labs that stipulate physical isolation, yet their growth is constrained by high capex and the need for specialized staff. Appliances such as AWS Outposts and Microsoft Azure Stack blur boundaries by delivering SaaS APIs on customer premises. Disaster-recovery design is another hybrid driver: immutable off-site backups harden ransomware resilience without breaching residency rules. The resulting architectural flexibility keeps platform selection fluid, sustaining multi-vendor competition and innovation cadence across the cloud enterprise content management market.

By End-User Industry: Healthcare Leads Growth Amid Interoperability Mandates

The banking, financial services, and insurance sector accounted for 26.72% of sector revenue in 2025, primarily due to record-keeping mandates under the Basel III and MiFID II regulations. However, healthcare is advancing at a 13.78% CAGR as the 21st Century Cures Act penalizes information blocking and forces EHR interoperability. Hospitals pairing Epic or Cerner with native content management plug-ins are reducing release-of-information cycle times and curbing malpractice exposure. Manufacturing and retail are digitizing supplier contracts and product specifications, feeding ERP systems with version-controlled documents that enable faster and more informed supply-chain decisions. Meanwhile, telecom operators centralize network diagrams and SLAs to shorten onboarding for new field engineers.

Energy utilities deploy content platforms to preserve maintenance logs and incident reports, integrating SCADA outputs for predictive-maintenance scheduling. Education and government users leverage shared repositories for digital learning and citizen services, embedding metadata taxonomies that speed search and retrieval. Each vertical pushes vendors to ship domain templates with preconfigured retention schedules, thereby shrinking deployment cycles and boosting win rates in the cloud enterprise content management market.

By Service: Managed Services Accelerate Under Compliance Burden

Professional services dominated 2025 revenue, accounting for a 56.48% share, due to complex legacy migrations that require bespoke data mapping and change management. Yet managed services are growing at 15.04% CAGR as enterprises hand off platform upkeep, patching, and policy audits to specialists. Outcome-based contracts guarantee uptime and compliance, converting unpredictable internal labor costs into fixed fees. System integrators, such as Accenture and Cognizant, bundle advisory, implementation, and run-state operations, allowing clients to avoid multi-vendor coordination. Vendors, including Hyland, OpenText, and IBM, now embed 24/7 monitoring and quarterly governance reviews into premium tiers, addressing talent shortages in content-security roles.

Small and medium-sized enterprises are particularly keen on managed offerings that combine hardware, software, and labor into a single subscription, aligning spending with usage. Meanwhile, large enterprises still commission bespoke professional-service engagements when consolidating dozens of legacy silos, ensuring data lineage continuity and regulatory sign-off. The convergence of both models under a unified commercial framework underscores the strategic importance of service revenue in the cloud-based enterprise content management market.

By Organization Size: SMEs Tap SaaS to Level the Playing Field

Large enterprises constituted 64.42% of deployments in 2025, as their complex governance needs favor advanced legal-hold and e-discovery modules. Nonetheless, small and medium-sized enterprises are the fastest-growing cohort, with a 17.35% CAGR, buoyed by pay-as-you-go pricing of below USD 10 per user per month. Microsoft 365, Box Business, and Dropbox Advanced integrate sensitivity labels and retention tagging, previously reserved for high-tier contracts, thereby lowering the barrier to enterprise-grade controls. No-code workflow builders and pre-configured templates shave implementation windows from months to weeks, freeing scarce IT staff for strategic projects.

Adoption hurdles persist: nearly 54% of SME projects fail to meet productivity targets due to limited training budgets and cultural resistance to new workflows. Vendors address this gap with guided onboarding, community forums, and AI-driven help bots that cut support tickets. As subscription models mature, SME usage patterns feed telemetry back to providers, informing iterative UI improvements that further democratize sophisticated capabilities across the cloud enterprise content management market.

Geography Analysis

North America generated 37.56% of 2025 revenue as the Securities and Exchange Commission, the Food and Drug Administration, and state privacy acts enforced stiff penalties for lapses in record retention. Multinationals headquartered in the region utilize granular content-classification engines to distinguish between personal data subject to California Consumer Privacy Act rules and general corporate documents, thereby reducing litigation exposure. U.S.-based tech giants also set architectural blueprints that ripple worldwide, accelerating innovation cycles across the cloud enterprise content management market.

Europe follows a compliance-first trajectory shaped by GDPR and the Digital Operational Resilience Act. Financial institutions invest in immutable archival layers that withstand supervisory scrutiny, while public administrations fund e-governance portals that demand robust version control. Vendor data residency commitments and Schrems-II-compliant contractual clauses are now standard requirements in RFPs. In the Middle East and Africa, sovereign digitization strategies, such as the Dubai Paperless Initiative, stimulate adoption; however, sporadic connectivity in Sub-Saharan regions hinders real-time collaboration and tempers immediate market size gains.

Asia Pacific, forecast to grow at 16.05% CAGR, benefits from high-priority government programs in India, China, and Japan that mandate electronic procurement, tax, and licensing records. Domestic cloud champions partner with global vendors to launch localized SaaS offerings that satisfy residency rules while offering global-class features. South America exhibits a cautious uptake as bandwidth prices decline and tax authorities transition to digital reporting, yet currency volatility can hinder purchase decisions. Overall, regulatory clarity and infrastructure upgrades are expected to expand regional adoption channels through 2031, supporting sustained growth for the cloud-based enterprise content management market.

Regulatory Landscape

Cloud enterprise content management (ECM) purchasing and deployment are shaped by compliance regimes that mandate provable controls over access, retention, auditability, and cross-border transfers of regulated content. In the United States, FedRAMP is a key gatekeeper for cloud use by federal agencies, and its transition to FedRAMP 20x is shifting authorization programs toward continuous, automation-friendly assurance for cloud services that store and process sensitive records.

In 2026, two formalization steps increased the compliance bar for cloud ECM platforms and their cloud-hosting partners. FedRAMP issued consolidated rules dated June 24, 2026 that codify requirements such as machine-readable compliance artifacts for agency authorization decisions, pushing vendors and managed-service providers to operationalize control evidence within their governance tooling. In parallel, ISO/IEC 27017 was published as an updated cloud security controls standard in April 2026, reinforcing the need for demonstrable cloud-specific security practices that align with enterprise audit programs and regulated-sector procurement requirements.

Value Chain Analysis

The cloud ECM value chain spans content ingestion (capture, scanning, connectors), core platform software (repositories, search, records and retention, workflow), security and governance layers (identity, encryption, key management, audit logging, DLP), hyperscale or sovereign cloud infrastructure (compute, storage, networking, KMS), and delivery channels such as direct SaaS sales plus system integrators and managed-service providers that handle migrations and run-state compliance. Large buyers, especially in BFSI and healthcare, commonly source a bundled stack that includes vendor templates, policy configuration, and ongoing monitoring, which keeps professional and managed services tightly coupled to software subscription revenue.

Partnerships with hyperscalers are increasingly a primary route to capability upgrades and distribution, as vendors embed agentic and Copilot-style experiences while relying on Azure, AWS, or Google Cloud for scalable AI services and compliance attestations. Examples include M-Files deepening collaboration with Microsoft (March 2026) to integrate content context into Microsoft 365 Copilot experiences, and Hyland partnering with Microsoft (June 2026) to bring Hyland Content Innovation Cloud to Azure with joint go-to-market motions. A parallel compliance-driven branch of the value chain is emerging around sovereign cloud, highlighted by OpenText partnering with S3NS (Thales and Google Cloud) in April 2026 to address sensitive-data workloads in France, reinforcing sovereignty, residency, and certification constraints as a decisive channel and architecture determinant.

Competitive Landscape

The top five suppliers, Microsoft, OpenText, IBM, Oracle, and Hyland, controlled a significant share of 2024 revenue, leaving more than half the cloud enterprise content management market in the hands of regional specialists and open-source challengers. Incumbents leverage AI differentiation, notably Microsoft’s Copilot for auto-classification and OpenText Aviator for natural language compliance queries. IBM’s blockchain-backed audit trail patents point to cryptographic mitigations against multi-tenant skepticism. Niche vendors such as Box, M-Files, and Laserfiche appeal to small and medium-sized enterprises with streamlined user experiences and per-user billing, forgoing advanced e-discovery capabilities to keep costs low.

Vertical specialization offers a springboard for disruptors. Veeva Systems dominates life sciences by delivering FDA-ready templates that compress submission timelines. Kiteworks targets zero-trust mandates through private-cloud appliances that bundle secure file transfer with content management.

Managed-service packaging blurs the line between software vendor and systems integrator, as Hyland and OpenText open offshore delivery centers to rival Accenture and Cognizant for run-state deals. Competitive intensity is expected to rise as generative AI commoditizes baseline features, shifting the focus of differentiation to domain knowledge and partner ecosystems.

Cloud Enterprise Content Management Industry Leaders

Alfresco Software Inc.

Box Inc.

Adobe Inc.

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace area is the shift from repository-centric ECM to agentic content operations, where platforms embed AI agents that can extract, classify, and trigger downstream actions while preserving retention and audit trails. Microsoft moving SharePoint Copilot Apps into public preview in July 2026 provides a concrete adoption pathway for buyers standardizing on Microsoft 365 and looking to turn governed content into task execution within existing productivity workflows. This creates room for ECM vendors and integrators to differentiate on policy-aware agent orchestration, higher-fidelity metadata extraction, and regulated-workflow templates that reduce manual review burdens.

A second opportunity is compliance-aligned deployment choice, especially for sovereignty-constrained workloads that cannot fully utilize general public cloud regions. The European Commission work on sovereign cloud frameworks in 2026, alongside vendor moves such as OpenText partnering with S3NS (Thales and Google Cloud) for sovereign cloud solutions in France, underlines demand for localized control planes, residency assurances, and audit-ready operations that still integrate with hyperscaler AI ecosystems. For media- and rich-content-heavy enterprises, partnerships like Avid and Google Cloud (April 2026) that integrate Gemini and Vertex AI into content production pipelines also reinforce demand for cloud ECM and digital asset management that supports large-scale search, rights management, and governed reuse across distributed teams.

Recent Industry Developments

- June 2026: IBM completed the acquisition of Confluent, expanding its real-time data integration capabilities for enterprise AI and agent-driven use cases. The addition of high-scale event streaming strengthens IBM's ability to feed current context into content and workflow automation stacks that depend on timely signals across applications. This move also raises competitive pressure on ECM ecosystems that are positioning around agentic automation and continuous compliance monitoring.

- February 2025: IBM announced its intent to acquire DataStax to deepen watsonx capabilities and address enterprise generative AI data needs. The planned combination targets stronger governance and retrieval across data estates, which influences how ECM repositories are connected to AI applications and knowledge workflows. It also reinforces the role of interoperable data and content layers as a procurement criterion for regulated enterprises.

- July 2024: IBM completed the acquisition of StreamSets and webMethods, bolstering its automation, data, and AI portfolios. The deal expanded IBM's integration and data pipeline tooling, which is central to migrating legacy repositories and orchestrating cross-system content workflows. Stronger integration coverage helps shorten implementation cycles in complex ECM modernization programs that span multiple line-of-business systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers cloud-delivered enterprise content management solutions and related services that help organizations capture, store, govern, search, and manage business content and records across departments, delivered through public, private, or hybrid cloud.

Scope exclusions: We exclude on-premises only ECM deployments and general IT outsourcing that is not directly tied to cloud ECM implementation, migration, or ongoing management.

Segmentation Overview

- By Solution

- Content Management

- Case Management

- Workflow Management

- Record Management

- Digital Asset Management

- Other Solutions

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By End-User Industry

- Banking, Financial Services and Insurance (BFSI)

- Energy and Power

- Medical and Healthcare

- Manufacturing

- Retail

- Information Technology and Telecom

- Other End-User Industries

- By Service

- Professional

- Managed

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base around cloud adoption, content governance, and regulated record-keeping needs that shape buying for cloud ECM. We relied on public and official sources such as the National Institute of Standards and Technology guidance for cloud and security, US Securities and Exchange Commission filings for risk and revenue commentary, the US Bureau of Labor Statistics for employment trends linked to IT services demand, and the US Census Bureau for basic enterprise and industry structure indicators.

To keep assumptions grounded, we also referred to sources such as standards and frameworks from the International Organization for Standardization, regulator and privacy authority publications that influence retention and compliance programs, customs and trade statistics where relevant for IT services proxies, and peer-reviewed journals covering information governance and content lifecycle management. General secondary sources like company annual reports, investor presentations, product documentation, association websites, and reputable press were reviewed for directional checks. A paid subscription for company financials and intelligence was used selectively to normalize revenue splits when disclosures were grouped across content platforms and workflow tools. These desk research sources are illustrative only, and many other public references were used to collect, validate, and clarify inputs during the work.

Primary Interviews and Surveys

Primary interviews and surveys were conducted with a spread of cloud ECM solution providers, implementation and managed service teams, and enterprise buyers who own content, records, and workflow programs across major regions. These conversations helped us validate deployment model mix, typical service attach rates, and renewal and expansion patterns, which then filled gaps left by mixed or bundled public disclosures.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 52% |

| Mid tier: 48% | Functional/Unit leaders: 33% | EMEA: 29% |

| Smaller Players: 21% | Managers: 53% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where enterprise software and IT services spending is narrowed into the cloud ECM demand pool using adoption indicators by region and end-user industry, and then allocated across solutions and services. Once the first cut is formed, it is corroborated with selective bottom-up approximations, such as sampled supplier exposure to cloud ECM, channel checks on deal sizes, and ASP x volume style estimates for subscriptions and service delivery, followed by adjustments when mismatches show up.

Key inputs in the model include the split across public, private, and hybrid cloud deployments, the pace of content digitization and workflow automation programs, compliance-driven records retention requirements, managed services penetration, and the organization size mix between SMEs and large enterprises. Where disclosures are blended, revenue lines are separated using interview-led allocation keys, and coverage gaps for smaller suppliers are handled through calibrated uplift factors tied to enterprise counts and typical contract values.

For forecasting, scenario analysis is used and then anchored to expected cloud migration pace, regulatory pressure, and enterprise budget sentiment, with primary feedback used to refine renewal cycles and pricing progression. When leading indicators diverge, assumptions are re-tested and smoothed so the forecast remains explainable and repeatable.

Data Validation & Update Cycle

Outputs are triangulated against independent signals like cloud software spending direction, enterprise digital transformation priorities, and service backlog and pipeline commentary, and then checked for regional and industry-level outliers. When variance is material, we revisit the driver inputs, re-check allocation keys, and re-contact selected respondents to confirm whether pricing, bundling, or deployment mix shifted.

A multi-step review is completed before sign-off so arithmetic integrity, scope alignment, and assumption logic are verified. Reports are refreshed annually, with interim updates when major product, regulatory, or macro events can change adoption or pricing, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Cloud Enterprise Content Management Market Size Compared Against Other Published Estimates

Published market sizes for cloud enterprise content management can differ even when the topic label looks similar, because included revenue lines and service treatment are not consistent across sources. Differences also come from base year choice, currency timing, and how frequently deployment model mix and pricing assumptions are refreshed.

The main gap comes from how services are counted, where Mordor Intelligence includes professional and managed services only when they are directly tied to cloud ECM implementation, migration, or ongoing operation, rather than broad IT services that merely touch content workflows.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 39.88 B (2026) | |

| Global Consultancy A | USD 35.51 B (2025) | Uses an earlier year and can diverge when public versus hybrid deployment mix and service attach rates are not re-weighted using recent enterprise buying patterns. |

| Industry Publisher B | USD 37.48 B (2025) | Component-based sizing can shift totals depending on whether services are counted broadly and whether solution revenue includes adjacent content tools beyond ECM workflows and records use cases. |

Overall, the table shows that scope around service revenue and timing of core assumptions explain most of the spread, rather than a single demand driver. By keeping deployment mix, service attach, and regulated industry adoption checks explicit, the final size remains traceable to clear inputs that can be repeated during updates.

Key Questions Answered in the Report

What is the current value of the cloud enterprise content management market?

The market stood at USD 39.88 billion in 2026 and is projected to reach USD 71.19 billion by 2031.

Which deployment model is growing fastest?

The hybrid cloud is expanding at a 16.52% CAGR as organizations balance data sovereignty with scalability.

Why is healthcare adoption accelerating?

Hospital systems face interoperability mandates under the 21st Century Cures Act, driving a 13.78% CAGR for healthcare use cases.

How are vendors addressing security concerns?

Providers embed confidential computing enclaves and tokenization to safeguard sensitive data in multi-tenant environments, thereby ensuring the confidentiality, integrity, and security of sensitive data.

What role does artificial intelligence play?

Generative AI automates classification, metadata tagging, and policy enforcement, cutting audit preparation from weeks to days.

Are small and medium enterprises investing in these platforms?

Yes, SME adoption is climbing at 17.35% CAGR due to low per-user subscription pricing and no-code workflow tools.

Page last updated on: