Europe Consumer Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 175.71 Billion |

| Market Size (2026) | USD 182.79 Billion |

| Market Size (2031) | USD 222.69 Billion |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Consumer Packaging Market Analysis by Mordor Intelligence

The Europe consumer packaging market size was valued at USD 175.71 billion in 2025 and estimated to grow from USD 182.79 billion in 2026 to reach USD 222.69 billion by 2031, at a CAGR of 4.03% during the forecast period (2026-2031). Growth is steered by the EU Packaging and Packaging Waste Regulation, accelerating brand commitments to closed-loop systems, and sustained momentum in e-commerce fulfillment.[1]European Chemicals Agency, “Understanding the Packaging and Packaging Waste Regulation,” echa.europa.eu Material substitution toward fiber, mono-PET, and lightweight metal formats is reshaping capital allocation, while energy-price shocks force converters to reassess operating footprints. The competitive field is further altered by digital printing, which shortens design-to-launch cycles and supports SKU fragmentation, and by deposit-return infrastructure that channels recycled feedstock into high-value beverage applications.

Key Report Takeaways

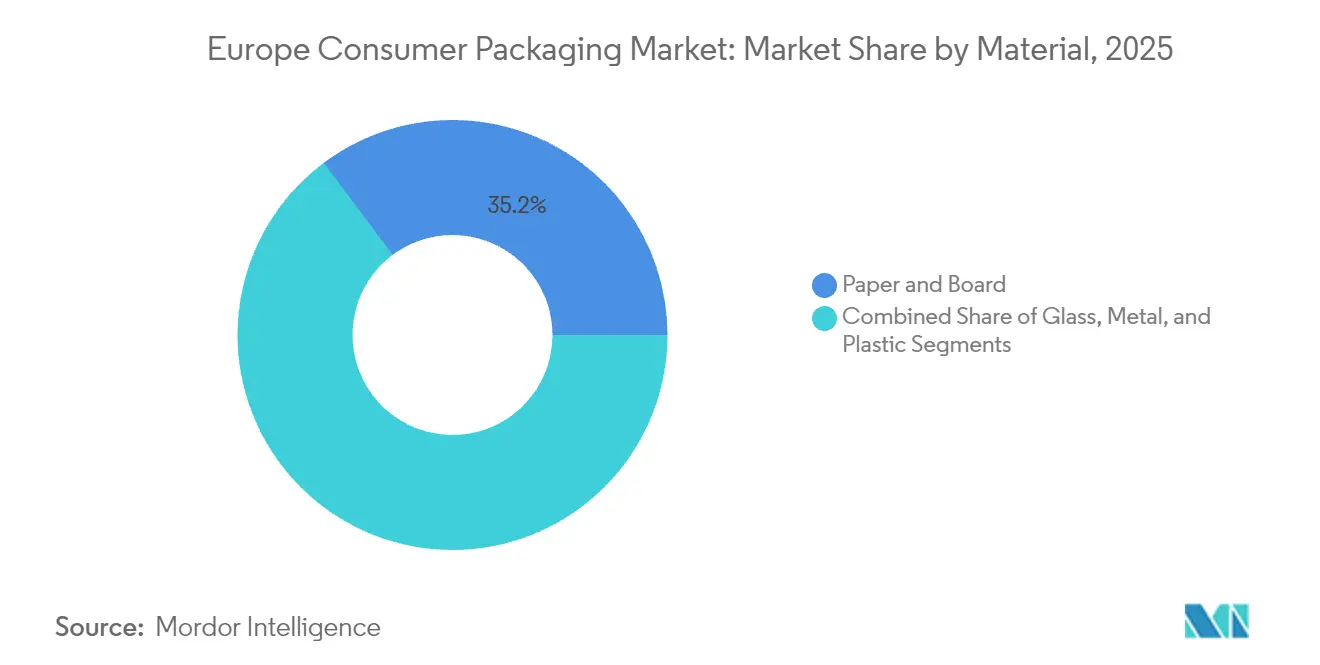

- By material, paper and board captured 35.22% the europe consumer packaging market share in 2025.

- By packaging format, the europe consumer packaging market for rigid solutions is projected to grow at a 5.62% CAGR between 2026-2031.

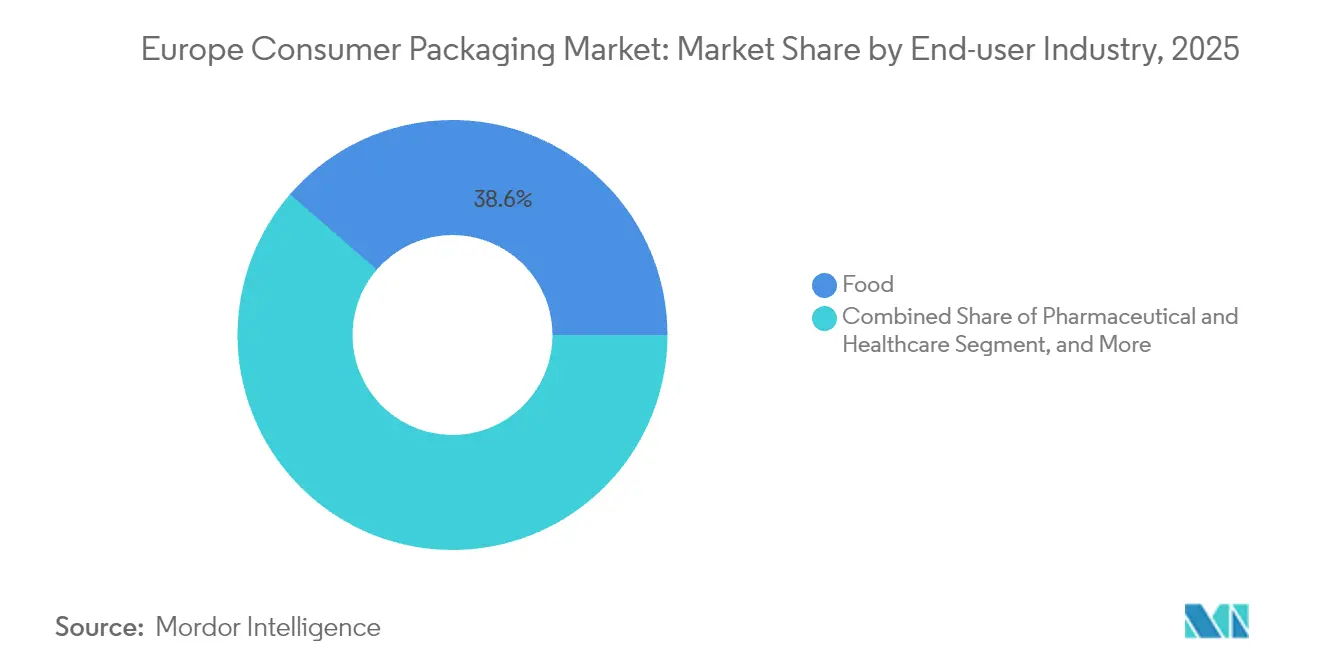

- By end-user industry, food applications captured 38.64% of the europe consumer packaging market share in 2025.

- By country, the europe consumer packaging market for Poland is projected to grow at a 5.15% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on consumer packaging market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Consumer Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-driven demand for flexible plastic packs | +3.3% | Germany, France, United Kingdom | Medium term (2-4 years) |

| E-commerce boom creating last-mile packaging needs | +2.4% | Poland, Spain, core EMEA | Short term (≤ 2 years) |

| Shift toward lightweighting and easy-open formats | +2.0% | Germany, Netherlands, Nordics | Medium term (2-4 years) |

| EU Single-Use Plastics Directive spurring mono-material R&D | +2.8% | EU-27 | Long term (≥ 4 years) |

| Deposit-return schemes scaling rPET demand | +1.6% | Germany, France, Italy | Medium term (2-4 years) |

| Digital printing enabling SKU proliferation and short runs | +1.2% | Western Europe premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience-driven demand for flexible plastic packs

Flexible formats continue to migrate volume from glass and metal as on-the-go consumption rebounds across urban corridors. Portion-controlled pouches with easy-open reclosable features meet the mobile lifestyle of 25- to 45-year-olds who prize portability and freshness. Price movements remain modest. 7-micron aluminum foil rose 4% in late 2024, but converters offset cost upticks through barrier-coated lightweight films that extend shelf life without adding bulk. Functionality now outweighs format loyalty, drawing liquid applications such as sauces and baby food toward spouted pouches and away from heavier rigid alternatives. The result is sustained share capture for flexibles in both food and personal-care aisles.

E-commerce boom creating last-mile packaging needs

Direct-to-consumer fulfillment adds multiple touchpoints where packs must survive conveyor drops, temperature shifts, and doorstep scrutiny. The PPWR mandates 40% reusable transport and sales packaging by 2030, pressuring retailers to harmonize automation with sustainability. Demand is surging for molded-fiber inserts and precision-engineered corrugated boxes that balance cushioning with dimensional efficiency. Poland and Spain show the steepest e-commerce penetration curves, widening the regional growth gap within the European consumer packaging market. Brand owners also leverage digital print to transform each parcel into a marketing canvas, elevating unboxing to a revenue lever rather than a cost center.

Shift toward lightweighting and easy-open formats

Pack owners cut material content by 10-15% while retaining barrier integrity through high-stretch alloys and multilayer polymer optimization. Ball’s 36 billion-unit 2024 EMEA can output demonstrates weight-down success without compromising performance. Ergonomic tabs and peel-off ends lighten cognitive and physical loads for aging consumers, satisfying regulatory accessibility objectives.[2]Ball Corporation, “Ball Reports Fourth Quarter 2024 Results,” ball.comFreight savings multiply the cost benefit as retailers chase lower scope-3 emissions. Thin-wall PET bottles and ultra-light steel cans are reinforcing rigid packaging’s renaissance across beverages and household chemicals.

EU Single-Use Plastics Directive spurring mono-material R&D

Mono-PE and mono-PP films move from laboratory trials to commercial scale as converters replace traditional multilayer laminates that hinder recycling streams. Surface plasma coatings and vapor-deposited barriers deliver oxygen and moisture protection without foil or PET tie layers, aligning with the EU mandate that all packaging be recyclable by 2030. Copier-grade adhesives and de-inkable inks emerge as critical enablers for curbside compatibility. Capital inflows gravitate toward tech vendors offering integrated recyclable substrate systems, stimulating consolidation among specialty chemical suppliers.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polymer and paper pulp prices | -2.4% | All EU markets | Short term (≤ 2 years) |

| Expanding EU bans on difficult-to-recycle formats | -1.6% | EU-27 | Medium term (2-4 years) |

| Recycling gaps for multilayer flexibles | -1.2% | Western Europe | Long term (≥ 4 years) |

| Energy-price shocks inflating glass and metal costs | -2.0% | Energy-intensive regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile polymer and paper pulp prices

Feedstock swings erode converter margins and disrupt pricing contracts fixed on quarterly indices. Polyethylene values softened in early 2024 amid weak downstream demand, yet PET tightened when Asian supply lines faltered, demonstrating the difficulty of forecasting input trajectories. On the fiber side, coated paper spiked nearly 10% in Q2 2024 before easing, driven by mill maintenance outages and logistics bottlenecks. Vertical integration into recycling or pulp assets is gaining favor, but it locks capital that could fund innovation or geographic expansion.

Expanding EU bans on difficult-to-recycle formats

National add-ons to EU rules generate a mosaic of compliance deadlines that strain design and inventory systems. Italy’s labeling statute requires granular disposal instructions, complicating shared artwork for pan-EU launches. Small converters frequently lack the engineering bandwidth to reformulate multi-layer pouches on tight timelines, which may accelerate market exits or mergers. Brands juggle dual inventories, legacy packs for exempt channels, and next-gen formats for regulated geographies, raising warehousing costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Paper Dominance Faces PET Challenge

Paper and board defended 35.22% of 2025 revenue on the strength of e-commerce shippers and foodservice disposables. The Europe consumer packaging market size for paper-based solutions is projected to expand modestly as regulatory goodwill and consumer perception remain supportive. However, PET’s 5.74% CAGR underscores a decisive momentum swing driven by deposit-return economics and brand pledges for food-grade recycled content. Europe consumer packaging market share gains accrue to mono-PET beverage bottles that averaged 24% recycled resin in 2024, validating closed-loop viability. In contrast, PE and PP navigate headwinds from single-use caps, cutlery, and thin grocery bags disappearing under new bans.

The PET narrative is reinforced by mechanical recycling yields that reach 75% in optimized plants, narrowing the carbon delta versus fiber-based cartons. Meanwhile, glass lobbies are campaigning for EUR 20 billion in furnace electrification, but elevated electricity tariffs cloud competitiveness. Aluminum retains a strong circularity story, yet the liquidity of post-consumer can sheet fluctuates with regional redemption rates. Specialty polymers hold pockets of growth in pharma blister packs and personal-care pump components, where performance trumps uniform recyclability mandates.

By Packaging Format: Rigid Growth Surprises Market

Rigid formats counterintuitively post the fastest 5.62% CAGR through 2031 as mono-material clarity simplifies sortation and recapture. Brands leverage thinner gauges and alternative alloys to mitigate weight penalties, while consumer acceptance of lightweight cans and recycled-content PET jars improves shelf appeal. Flexible packs still own 47.58% of 2025 spending due to film thrift and logistical efficiency, but recyclability scoring under PPWR threatens complex laminates. Semi-rigid thermoforms emerge as a hybrid, coupling form stability with higher recycling rates than multilayer sachets.

Digital embossing and tactile coatings elevate rigid pack shelf presence, bolstering premium categories from nutraceutical gummies to single-origin coffees. Crown Holdings’ 5% European can volume uptick in Q3 2024 affirms beverage category resilience. Flexible converters respond with solvent-free lamination lines and mono-PE high-barrier films to safeguard their share. Format competition pushes R&D spending toward compatibility solutions, including detachable layers and water-soluble tie resins.

By End-user Industry: E-commerce Disrupts Traditional Hierarchies

Food products contributed 38.64% of 2025 turnover thanks to established supply chains and mandatory shelf-life standards. Europe consumer packaging market size increments will keep food the anchor segment, yet e-commerce retail packs clock the fastest 6.11% CAGR as door-step fulfillment demands rugged, brandable formats. Beverages benefit from aluminum’s infinite recyclability and higher consumer recovery rates, though gas volatility adds margin risk.

E-commerce’s rise compels cosmetic and home-care brands to rethink secondary packaging, leading to corrugated inserts designed for social-media-friendly unboxing. Pharmaceuticals maintain stable growth on serialization and anti-counterfeit imperatives that require high-quality substrates and security inks. Niche industrial uses from EV battery components to precision electronics-drive uptake of molded pulp cushioning, showcasing the breadth of demand vectors inside the Europe consumer packaging market.

Geography Analysis

Germany anchors the Europe consumer packaging market with a 26.41% stake in 2025, supported by the continent’s most mature deposit-return logistics and an integrated recycling framework that hits 98% collection on aluminum beverage cans. Packaging producers cluster near automotive and FMCG corridors, leveraging automation to drive cost per thousand units lower than regional averages. Regulatory certainty and consumer eco-literacy justify ongoing investment in refillable glass and high-grade rPET infrastructure. Domestic growth tails off in volume, but value mix tilts upscale as brands deploy smart features such as NFC tags for provenance tracking.

Poland leads continental growth at 5.15% CAGR, spurred by rising household incomes and relocation of light-manufacturing plants from Western Europe and China. Government incentives coupled with EU cohesion funds modernize logistics corridors, trimming lead times for cross-border exports. E-commerce parcel density in Warsaw and Kraków surpasses 150 orders per 1,000 people weekly, amplifying corrugated and mailer demand. The forthcoming national deposit scheme primes PET and aluminum flows for closed-loop manufacturing, attracting extruder and flake-washing investment. Western converters enter joint ventures with Polish partners to hedge against labor cost inflation in core EU economies.

Southern and Western European markets France, Italy, Spain contribute scale but diverge in policy nuance. France fast-tracks a beverage deposit system, expanding reverse-vending machine fleets across retail chains. Italy mandates granular disposal labeling, compelling localized graphics lines, whereas Spain’s eco-modulation fees penalize virgin-plastic intensity, nudging brands toward fiber and compostables. The United Kingdom, while outside EU law, mirrors most PPWR goals and imposes a GBP 200 per tonne plastics tax on sub-30% recycled content, influencing cross-Channel pack decisions. Nordic economies carve a premium niche for bio-composites and fiber-based caps rooted in forestry supply chains, while the Benelux region pilots digital watermarking for high-speed sorting at MRFs, a technology expected to ripple across the Europe consumer packaging market over the forecast horizon.

Competitive Landscape

Competition skews material-specific: Ball Corporation controls 39% of EMEA aluminum beverage can output, reflecting high capital barriers and entrenched brand contracts. Conversely, flexible packaging is fragmented, with more than 400 regional converters whose proximity advantages serve just-in-time delivery to food processors. M&A momentum leans toward scale and circularity; Mondi’s acquisition of Schumacher’s Western European assets expands Kraft-Liner's reach for e-commerce shippers.

Strategic levers center on vertical integration into recycled-material supply, automation that shrinks unit labor, and deployment of digital print fronts to capture premium runs. White-space innovation focuses on mono-material barrier flexibles, where converters pioneer plasma-coated PE films matched with de-inkable adhesives. Chemical suppliers partner upstream to deliver functional coatings that unlock recyclability credits under PPWR scoring.

Cost shocks from energy and feedstock volatility compress margins for glass and metal players, accelerating electrification pilots and renewable PPA contracts. Extended Producer Responsibility fees re-allocate end-of-life costs to producers, advantaging incumbents with closed-loop alliances. Certification under ISO 14001 and alignment to the European Sustainability Reporting Standards becomes a qualifier in tender bids, tightening procurement for suppliers lacking ESG credentials. Competitive intensity thus hinges less on price and more on regulatory fluency and proven circularity pathways within the Europe consumer packaging market.

Europe Consumer Packaging Industry Leaders

International Paper Company

Constantia Flexibles Group GmbH

Huhtamäki Oyj

Tetra Pak International SA

Amcor PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mondi closed FY 2024 with EUR 1,049 million EBITDA and announced five capacity expansions, including a Czech paper machine, while buying Canada’s Hinton pulp mill to secure a renewable-fiber supply.

- February 2025: Ball’s EMEA beverage segment earned USD 416 million on USD 3.47 billion sales in Q4 2024 as it pivots into pure-play aluminum packaging after divesting aerospace.

- February 2025: Berry Global posted USD 2.4 billion Q1 2025 revenue and advanced its merger with Amcor while exiting tapes to sharpen focus on consumer packaging.

- January 2025: The PPWR entered force, obliging all packaging sold in the EU to be recyclable by 2030 and setting material-specific recycled-content quotas.

Europe Consumer Packaging Market Report Scope

The consumer packaging market refers to the industry that produces packaging materials and solutions for consumer goods. This market is crucial in protecting, preserving, and promoting products for sale and use. Consumer packaging encompasses a wide range of materials, including paper, cardboard, plastic, glass, and metal, which are used to create various types of packaging, such as boxes, bottles, cans, pouches, and more.

The consumer packaging market is segmented by material (plastic [material type {polyethylene, polypropylene, polyvinyl chloride, polyethylene terephthalate, other material types}], [type {rigid plastic packaging, flexible plastic packaging}], paper [type {carton board, containerboard, linerboard, and other types}], glass, and metal [type {cans, caps, and closures, other types}]), end-user industry (food, beverage, pharmaceutical and healthcare, and cosmetics, personal care, and household care), and country (United Kingdom, Germany, France, Italy, Poland, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Plastic | PE (Polyethylene) |

| PP (Polypropylene) | |

| PET (Polyethylene Terephthalate) | |

| PVC (Polyvinyl Chloride) | |

| Other Plastics | |

| Paper and Board | Cartonboard |

| Containerboard and Linerboard | |

| Molded Fiber | |

| Glass | |

| Metal | Cans |

| Caps and Closures | |

| Tubes | |

| Other Metals |

| Rigid |

| Flexible |

| Semi-rigid |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Cosmetics, Personal and Home Care |

| Other End-user Industry |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Poland |

| Rest of Europe |

| By Material | Plastic | PE (Polyethylene) |

| PP (Polypropylene) | ||

| PET (Polyethylene Terephthalate) | ||

| PVC (Polyvinyl Chloride) | ||

| Other Plastics | ||

| Paper and Board | Cartonboard | |

| Containerboard and Linerboard | ||

| Molded Fiber | ||

| Glass | ||

| Metal | Cans | |

| Caps and Closures | ||

| Tubes | ||

| Other Metals | ||

| By Packaging Format | Rigid | |

| Flexible | ||

| Semi-rigid | ||

| By End-user Industry | Food | |

| Beverage | ||

| Pharmaceutical and Healthcare | ||

| Cosmetics, Personal and Home Care | ||

| Other End-user Industry | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Poland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe consumer packaging market?

It is valued at USD 182.79 billion in 2026 and is projected to reach USD 222.69 billion by 2031.

How fast is the market expected to grow?

The forecast CAGR stands at 4.03% between 2026 and 2031.

Which material segment is expanding the quickest?

PET posts the fastest 5.74% CAGR, buoyed by deposit-return systems and recycled-content mandates.

Why is Poland the fastest-growing national market?

Manufacturing capacity shifts, low labor costs, and surging e-commerce adoption deliver Poland a 5.15% CAGR through 2031.

How are EU regulations influencing packaging design?

The PPWR requires all packs be recyclable by 2030, driving a pivot toward mono-material structures and higher recycled-content ratios.

Which end-user category is gaining the most momentum?

E-commerce retail packs are advancing at a 6.11% CAGR amid rising direct-to-consumer shipments.

Page last updated on: