Agricultural Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

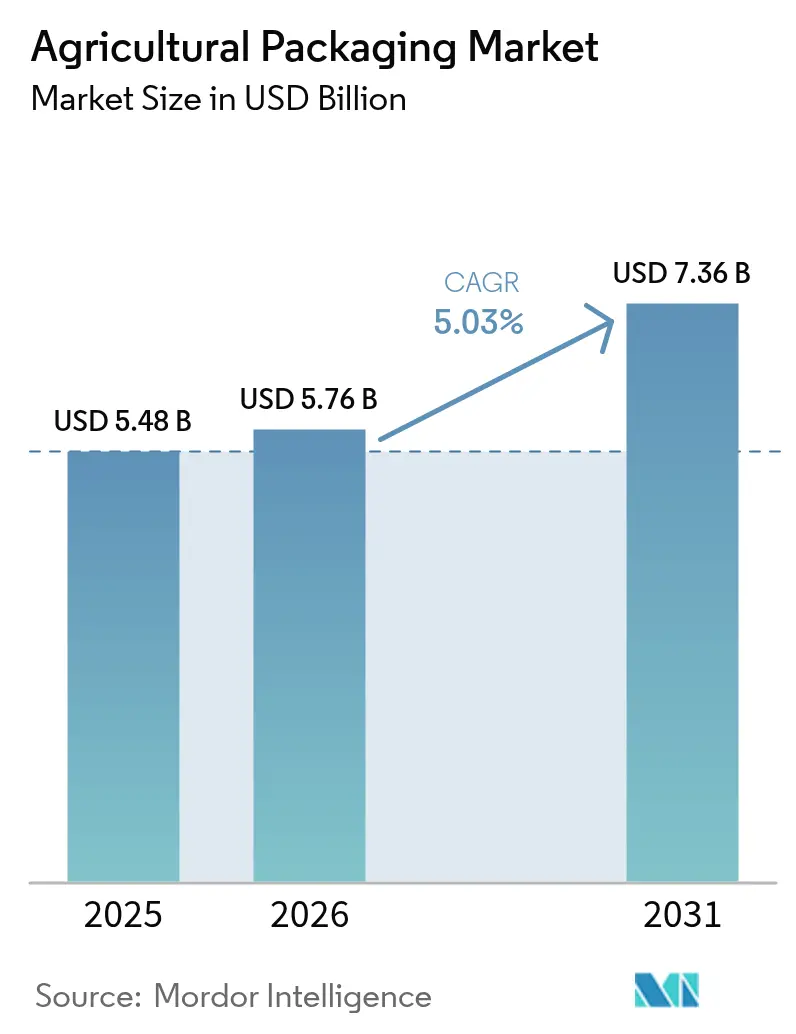

| Market Size (2026) | USD 5.76 Billion |

| Market Size (2031) | USD 7.36 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Packaging Market Analysis by Mordor Intelligence

The agricultural packaging market size in 2026 is estimated at USD 5.76 billion, growing from 2025 value of USD 5.48 billion with 2031 projections showing USD 7.36 billion, growing at 5.03% CAGR over 2026-2031. This steady climb demonstrates the sector’s resilience as regulators demand recyclability, recycled-content thresholds, and lower carbon footprints. Asia-Pacific’s export-oriented agribusiness, Europe’s aggressive sustainability targets, and North America’s traceability mandates jointly stimulate material innovation and format redesign across the agricultural packaging market. Plastic continues to dominate volumes, yet biodegradable films and molded-fiber formats accelerate on the back of the European Union’s Packaging and Packaging Waste Regulation (PPWR) and California’s compostable-labeling law. Meanwhile, bulk-handling mechanisation in China, India, and Brazil propels mid- to large-capacity flexible intermediate bulk containers (FIBC), whereas precision farming in the United States and Western Europe lifts demand for smaller, application-specific packs. Raw-material cost swings and extended-producer-responsibility (EPR) fees temper profitability, but consolidation among converters and resin suppliers is creating scale economies that offset part of the inflationary pressure.

Key Report Takeaways

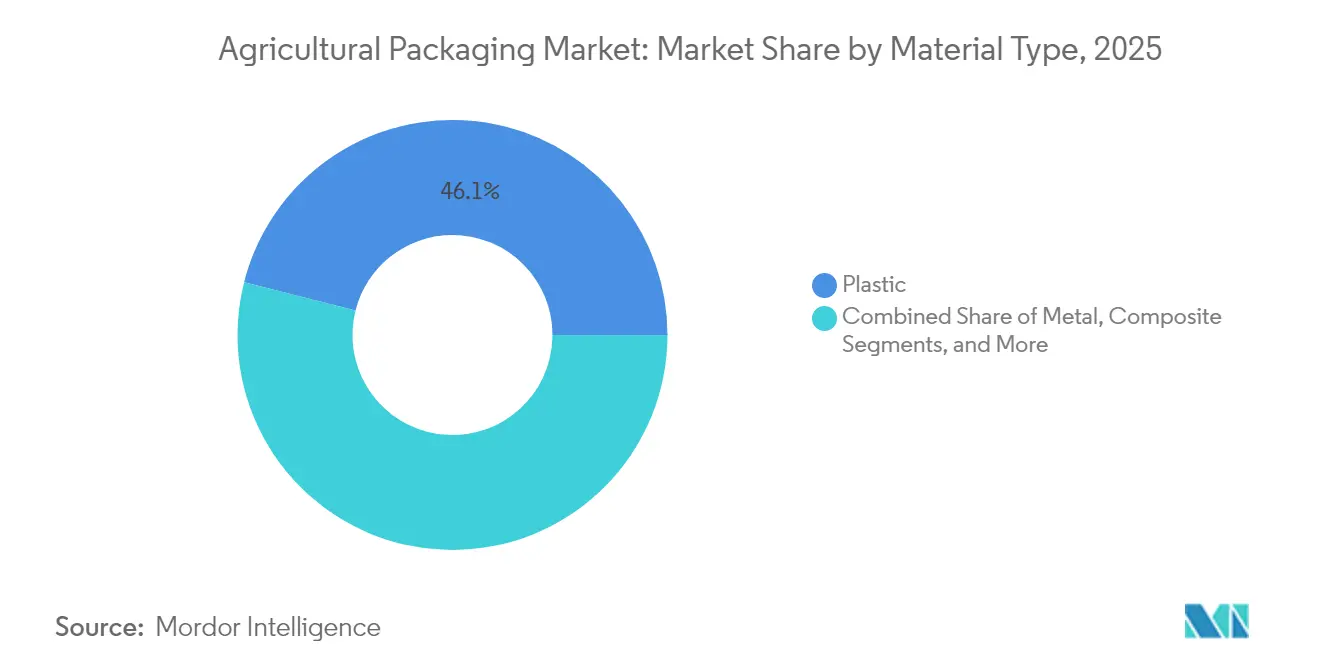

- By material type, plastic held 46.05% of agricultural packaging market share in 2025, while biodegradable films are projected to expand at an 8.01% CAGR through 2031.

- By application, fertilizers led with 38.02% revenue share in 2025; crop protection biologics are set to grow at a 7.45% CAGR to 2031.

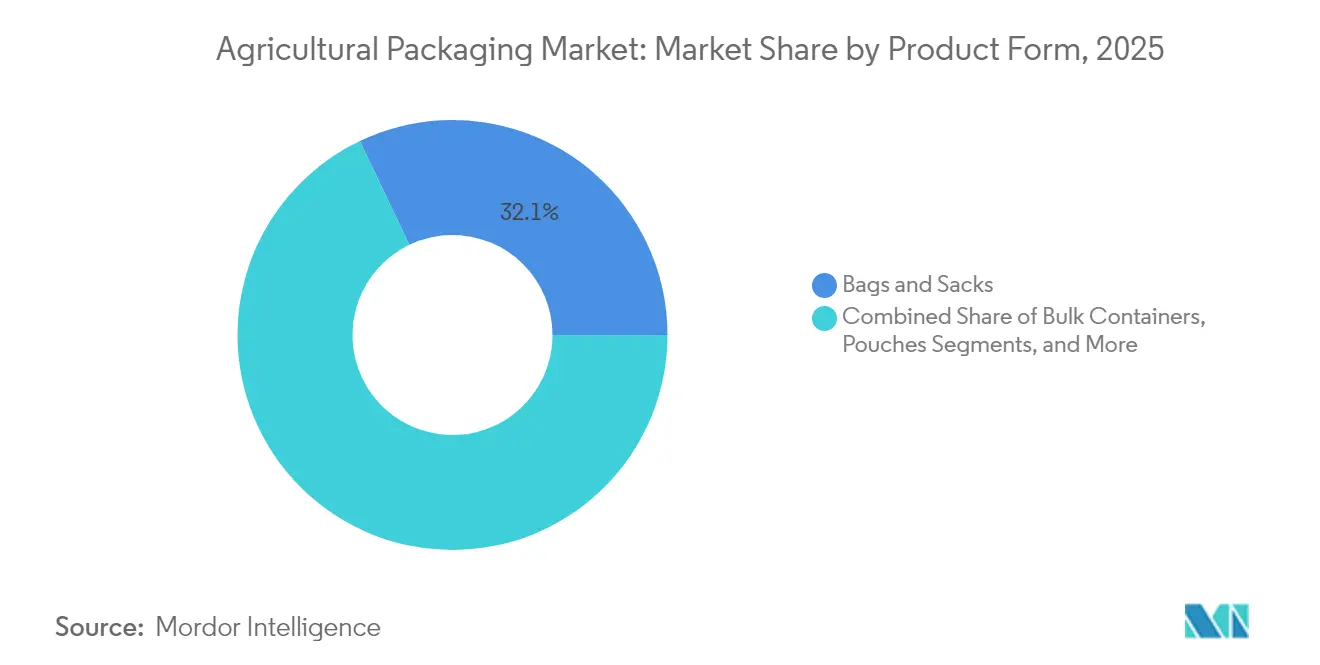

- By product form, bags and sacks captured 32.10% of the agricultural packaging market size in 2025, whereas pouches exhibit the fastest 8.55% CAGR.

- By capacity range, 26-100 kg / 21-200 L packs controlled 43.80% share in 2025; ≤25 kg / ≤20 L formats are forecast to register a 8.62% CAGR.

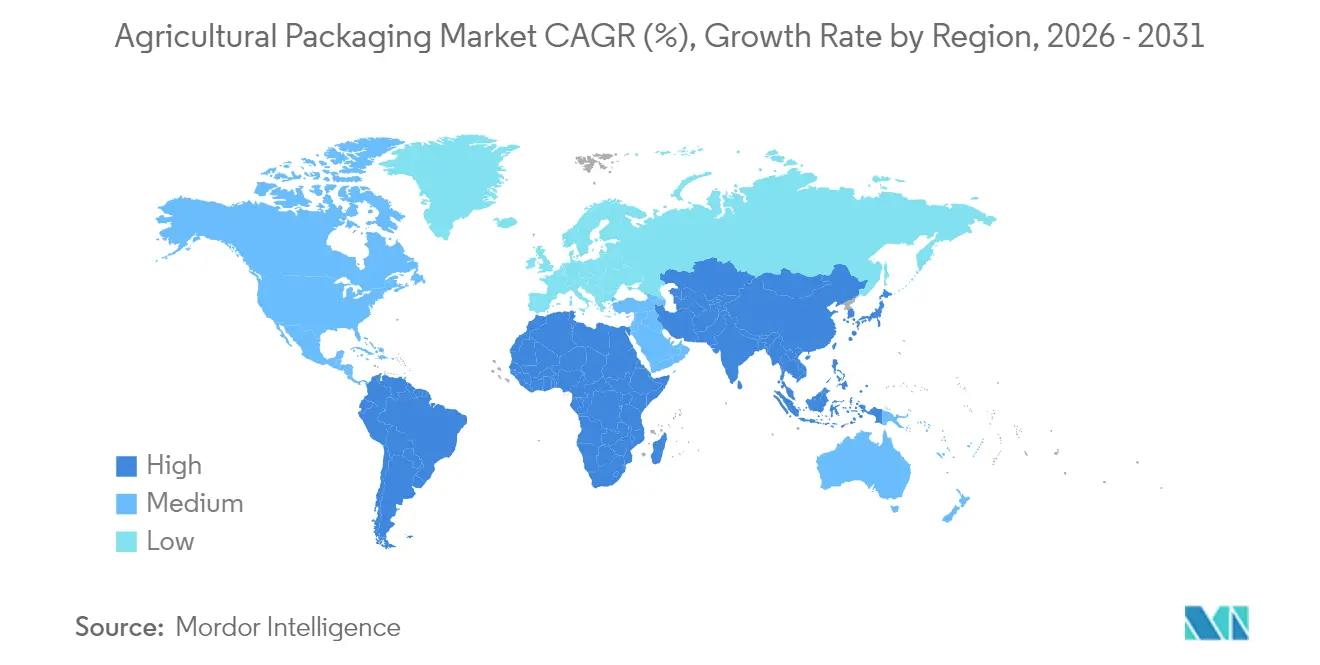

- By geography, Asia-Pacific dominated with a 39.85% agricultural packaging market share in 2025, while Europe is predicted to post the strongest 7.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for agro-chemicals | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Sustainability-driven material innovations | +0.9% | Europe and North America leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of cross-border agri-produce trade | +0.8% | Global, particularly US-China-EU trade corridors | Medium term (2-4 years) |

| Mechanisation and bulk handling adoption | +0.7% | Asia-Pacific core, spill-over to Latin America and Africa | Long term (≥ 4 years) |

| Smart / QR-enabled traceability packaging | +0.5% | North America & EU, early adoption in developed Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Agro-Chemicals

Global pesticide and fertilizer consumption keeps rising as nations pursue higher yields. India’s regulators cleared 416 new crop-protection products in H1 2024, spanning legacy insecticides and novel actives, thereby boosting packaging volumes. China’s four-decade transition into the world’s largest pesticide exporter demands standardized pack formats that comply with multiple destination-market rules. In the United States, anti-dumping probes on 2,4-D imports from Asia reshape domestic filling plans, while Philippine authorities’ seizure of counterfeit chemicals underscores the role of tamper-evident packaging in brand protection pna.gov.ph. Driven by food-security programs and precision-application equipment, the agricultural packaging market welcomes higher-barrier laminates and smaller dose-specific pouches that reduce spillage and worker exposure.

Sustainability-Driven Material Innovations

The EU’s PPWR obliges all packs to be recyclable by 2030 and fixes recycled-content quotas of 30% for PET by that date, rising to 50% by 2040. Mondi’s paper-based Advantage Kraft Mulch replaces black PE mulch film, signalling material substitution momentum in field applications. Academic work on hemp-hurd molded fiber and lignin-based nanocomposites shows that bio-derived substrates can deliver moisture resistance and UV shielding comparable to petroleum-based films. Greif’s EnviroRAP paperboard and Lactips’ edible-film patents add further evidence that sustainable materials are moving from pilot to commercial scale. As EPR fees penalise unrecyclable formats, converters accelerate R&D spend on bio-resins, mono-material laminates, and water-based barriers.

Expansion of Cross-Border Agri-Produce Trade

USDA foresees United States agricultural exports touching USD 169.5 billion in FY 2025, with horticulture alone contributing USD 41.5 billion.[1]USDA, “Outlook for U.S. Agricultural Trade,” downloads.usda.library.cornell.edu Pallet and bag suppliers must now satisfy ISPM-15 fumigation rules for over 100 destination markets. China’s new customs declaration regulation, effective May 2025, tightens paperwork accuracy, raising demand for QR-coded labels that expedite clearance. Australia is similarly integrating food-safety data into its Biosecurity Import Conditions platform from June 2025 onward. These measures collectively lift requirements for rugged packs, extended shelf-life linings, and multi-language regulatory markings across the agricultural packaging market.

Mechanisation and Bulk-Handling Adoption

Asia-Pacific growers are adopting FIBC and silage tubes to match the scale of automated seeding and fertilizing machinery. The region’s returnable transport packaging value is projected to swell by USD 1.40 billion between 2023 and 2028, clocking an 8.87% CAGR. Brazil’s Packem SA recently ordered USD 1.29 million of FIBC from India, illustrating cross-continental sourcing opportunities. RKW’s seven-layer Hytibag silage film extends forage shelf life, while screw-conveyor separators under development support dust-free bulk loading. As mechanised fleets spread from China to sub-Saharan Africa, farmers demand lighter, more ergonomic sacks and spouts that dovetail with automated dispensing rigs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory pressure on plastics and VOCs | -0.8% | Europe and North America leading, expanding globally | Medium term (2-4 years) |

| Raw-material price volatility | -1.1% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Counterfeit ag-inputs raising compliance cost | -0.4% | Asia-Pacific and developing markets, spill-over to global trade | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure on Plastics and VOCs

The PPWR bans per- and polyfluoroalkyl substances above threshold limits in food-contact packs, eliminating numerous fluoropolymer coatings used on fertilizer bags. California’s SB 343 will prohibit “chasing-arrows” symbols on packs that fail recyclability tests after October 2026, while SB 54 compels a 25% plastic reduction by 2032. Oregon’s EPR law demands granular reporting of packaging weights from April 2025, raising administrative overhead for small converters. Studies reveal that current composting facilities cannot separate bio-bags from conventional plastics effectively, complicating claims of commercial compostability. Collectively, these statutes force design changes that may elevate costs and slow material changeovers in the agricultural packaging market.

Raw-Material Price Volatility

World Bank data point to a 4% decline in agricultural commodity indices for 2025, but gas-linked nitrogen fertilizer prices remain high, squeezing farm input budgets and influencing order volumes for bulk sacks. Mondi’s first-half 2024 EBITDA slipped 17% year on year as pulp and resin prices gyrated. Adverse weather lifted cocoa, olive, and coffee prices in 2024, altering crop-mix forecasts and hence related packaging demand patterns. Possible tariff hikes on fertilizer imports threaten additional cost pass-through, prompting growers to delay replenishment or switch to cheaper inputs, which depresses packaging sales volumes. The premium that still attaches to certified compostable films widens the affordability gap versus polyethylene during inflationary spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastic Dominance Faces Biodegradable Disruption

Plastic accounted for 46.05% of the agricultural packaging market share in 2025, thanks to its durability, lightweight, and ingrained supply chains. High-density polyethylene drums and polypropylene woven sacks dominate fertilizer and pesticide applications because they resist puncture and chemicals. Yet the agricultural packaging market is experiencing a rapid pivot toward biodegradable films, the fastest-growing sub-segment at an 8.01% CAGR through 2031. European regulations imposing 30% recycled content on PET by 2030 push converters to blend post-consumer resin or switch materials entirely.Producers such as Mondi and Greif commercialize paper-based mulch and 100% recycled paperboard liners, respectively, offering comparable performance while easing EPR liabilities.

The competitive intensity is rising as academic breakthroughs in hemp-fiber molded substrates and lignin-bionanocomposites promise moisture, oxygen, and UV performance formerly exclusive to polymer laminates. Composite multilayers maintain a niche in high-value seeds and micro-nutrient sachets, although recyclability concerns and layer-separation costs keep their growth modest. Metal pails serve ultra-volatile herbicides, but volumes are stable rather than expanding. Overall, sustainability imperatives are redefining raw-material procurement, tooling investments, and brand-owner messaging across the agricultural packaging market.

By Application: Fertilizers Lead While Biologics Accelerate

Fertilizers generated 38.02% of 2025 revenue, securing the largest slice of the agricultural packaging market size through their essential role in maximizing yields. Bags, FIBC, and laminated sacks dominate because granulated nutrients require abrasion-resistant structures. Conversely, crop-protection biologics, while starting from a smaller base, hold the highest 7.45% CAGR as growers adopt microbial inoculants and biostimulants to meet residue-limit regulations. These live organisms demand chilled, oxygen-barrier pouches or rigid bottles that preserve viability, driving innovation in cold-chain compatible formats.

Traditional synthetic pesticides continue to command large tonnage, yet their growth moderates under stricter toxicity norms. Seed-trait packaging seeks improved dust retention and precise dispensing holes to safeguard genetic performance. Governments are investing directly in packaging R&D; USDA earmarked USD 10 million for a Sustainable Packaging Innovation Lab focused on produce exporters, reflecting growing recognition of packaging as a trade enabler. Authenticity safeguards such as color-shift inks and tamper rings are proliferating to combat counterfeit agricultural inputs in developing markets.

By Product Form: Traditional Bags Compete with Innovative Pouches

Bags and sacks held 32.10% of agricultural packaging market share in 2025 owing to proven cost, fill speeds, and global manufacturing footprints. Woven PP sacks with BOPP laminations remain the default for fertilizers and livestock feed. However, stand-up and spouted pouches are the fastest-rising form at an 8.55% CAGR, capturing volumes from smallholder-oriented crop-protection packs and specialty nutrient concentrates. FLtècnics’ AutoSplicer technology lifts pouch-line efficiency by 10%, narrowing the cost gap to bags.

Rigid HDPE and PET containers target high-value liquids where precise dosing reduces waste; Pactiv Evergreen’s SmartPour rigid eliminates inner liners while adding resealability. Bulk drums and IBCs continue to support industrial-scale fertilizer dissolving stations, benefitting from mechanisation trends. Caps, closures, and liners are evolving toward tethered designs to meet forthcoming EU loose-cap bans, adding another compliance layer for fillers and molders within the agricultural packaging market.

By Capacity Range: Mid-Range Dominance with Small-Package Growth

Packs in the 26-100 kg / 21-200 L bracket commanded 43.80% of 2025 revenue, mirroring the operational sweet-spot of medium-scale farms and cooperatives. These formats fit manual handling limits yet deliver freight efficiencies on pallets and in containers. Smaller packs (≤25 kg / ≤20 L) are projected to post a 8.62% CAGR, the highest within the segmentation, as precision sprayers, drone delivery systems, and micro-dosing protocols demand exact quantities and easier lifting. The agricultural packaging market size for these small formats is rising fastest in North America and Europe where labour regulations and ageing farm workforces favor reduced-weight sacks.

Large bulk (>100 kg) FIBC and silage tubes cater to mechanised mega-farms in Brazil, Australia, and parts of China. RKW’s seven-layer silobag supports controlled-atmosphere grain storage, illustrating technology transfer from food to agri-input packaging. Academic prototypes such as screw-conveyor integrated packs indicate future convergence between packaging and dispensing hardware. Legislated weight caps in Europe may further nudge the market toward lighter, ergonomically friendly formats over the forecast horizon.

Geography Analysis

Asia-Pacific anchored 39.85% of agricultural packaging market share in 2025, propelled by China’s transformation into the world’s largest pesticide exporter and India’s fertilizer-intensification drive. Rapid mechanisation, expanding e-commerce channels for seeds and garden products, and governmental food-security priorities keep the regional outlook robust. Vietnam’s paper-packaging sales illustrate the spill-over effect, forecast to reach USD 3.5 billion by 2026 on a 9.73% yearly climb. As Asia’s share of global agri-chemicals balloons, converters increase local resin recycling and invest in solvent-free lamination lines to meet downstream brand requirements.

Europe is on track to log the fastest 7.86% CAGR through 2031, buoyed by stringent circular-economy legislation and affluent consumers willing to pay for certified-sustainable agricultural produce. The PPWR alone compels systematic redesign of pack structures, opening space for molded-fiber trays, mono-material films, and smart labels that capture provenance data. Additionally, EU Green Deal subsidies encourage on-farm biomass conversion into packaging feedstock, shortening supply chains.

North America maintains healthy demand on the back of export-oriented grain and horticulture segments. USDA forecasts highlight record outbound shipments that rely on moisture-barrier liners and QR-coded pallet tags to comply with ISPM-15 wood-treatment and traceability rules. The Middle East and Africa, while smaller today, show accelerating import-substitution programs and aquaculture expansion that will require both flexible and rigid packs suited to arid climates. Latin America benefits from Brazilian mechanisation and bio-fertilizer adoption, issuing new opportunities for producers specialising in high-barrier multilayer bags.

Competitive Landscape

The agricultural packaging market is moderately fragmented, with a mix of global conglomerates and specialist regional firms. Mondi, Amcor, Sonoco, Berry Global, and Greif leverage global resin procurement, multi-continent plant networks, and in-house design centres to lock in long-term contracts with crop-chem majors. Regional contenders such as LC Packaging, NNZ Group, and Bulkcorp International defend market share via quick turnaround times and tailored FIBC specifications.

Strategic consolidation intensified in 2024. Sonoco acquired Eviosys for EUR 2.41 billion and divested its Thermoformed and Flexibles Packaging unit to TOPPAN for USD 1.8 billion, sharpening its consumer-packaging focus.[3]Sonoco Products Company, “Sonoco Completes Acquisition of Eviosys,” investor.sonoco.comIn January 2025, Amcor and Berry Global unveiled an all-stock merger that will create a USD 24 billion revenue entity, pledging USD 180 million annually to R&D in recyclable and compostable formats. Such combinations aim to pool intellectual property, harmonise extrusion assets, and strengthen bargaining power with petrochemical suppliers.

Technology is a key competitive lever. Kwik Lok’s QR-code closures and Trustwell’s blockchain tie-ups illustrate how digital traceability adds value beyond the physical pack. Patent filings around edible, starch-based films and cellulose-nanocrystal coatings reflect an arms race to secure defensible niches in eco-friendly substrates. Meanwhile, capital expenditure on automation—such as robotic palletizers and inline auto-splicing—reduces unit costs and enhances consistency, allowing mid-sized converters to compete on both price and sustainability credentials. Supply-chain resilience, especially around recycled resin sourcing, now factors as highly into customer tenders as historical pricing.

Agricultural Packaging Industry Leaders

Sonoco Products Company

Mondi Group

Greif Inc.

Pactiv LLC

Amcor PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Amcor and Berry Global announced an all-stock merger creating a USD 24 billion packaging leader with USD 180 million annual R&D spend focused on sustainable solutions.

- January 2025: Amcor signed an MoU with NOVA Chemicals to source mechanically recycled polyethylene for flexible films.

- December 2024: TOPPAN Holdings agreed to buy Sonoco’s Thermoformed & Flexible Packaging business for USD 1.8 billion.

- December 2024: Sonoco completed its EUR 2.41 billion acquisition of Eviosys, strengthening its metal-can offering.

Global Agricultural Packaging Market Report Scope

Agricultural packaging plays a significant role. It helps farmers and manufacturers deliver food in the best possible way and avoid wastage during post-harvest treatment procedures, production processes, storage, and transportation. Moreover, it ensures short and long-term stability between the farmers and the consumers. The scope of the study is currently focused on critical countries in regions such as North America, Europe, Asia-Pacific, and the Rest of the World. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the market that supports the market estimations and growth rates over the forecast period.

The Agricultural Packaging Market is segmented by Material Type (Plastic, Metal, Paper and Paperboard, Composite Materials), Application Type (Pesticides, Fertilizers, Seeds), Product Type (Bags & Sacks (Plastic & Paper), Bulk Containers (Drums & IBC), Pouches, Containers (Metal & Plastic)) and Geography (North America, Europe, Asia Pacific, Rest of the World). The report offers market forecasts and size in value (USD) for all the above segments.d.

| Plastic |

| Paper and Paperboard |

| Metal |

| Composite |

| Biodegradable Films |

| Pesticides |

| Fertilizers |

| Seeds and Traits |

| Crop Protection Biologics |

| Bags and Sacks |

| Bulk Containers (FIBC, Drums, IBC) |

| Pouches |

| Rigid Containers (Cans, Bottles) |

| Caps, Lids and Liners |

| ≤25 kg / ≤20 L |

| 26 – 100 kg/ 21 – 200 L |

| More than 100 kg/ 200 L (Bulk) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Plastic | ||

| Paper and Paperboard | |||

| Metal | |||

| Composite | |||

| Biodegradable Films | |||

| By Application | Pesticides | ||

| Fertilizers | |||

| Seeds and Traits | |||

| Crop Protection Biologics | |||

| By Product Form | Bags and Sacks | ||

| Bulk Containers (FIBC, Drums, IBC) | |||

| Pouches | |||

| Rigid Containers (Cans, Bottles) | |||

| Caps, Lids and Liners | |||

| By Capacity Range | ≤25 kg / ≤20 L | ||

| 26 – 100 kg/ 21 – 200 L | |||

| More than 100 kg/ 200 L (Bulk) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current agricultural packaging market size?

The agricultural packaging market size stood at USD 5.76 billion in 2026 and is forecast to hit USD 7.36 billion by 2031.

Which region leads the agricultural packaging market?

Asia-Pacific held 39.85% of 2025 revenue, driven by China’s pesticide exports and India’s fertilizer growth.

Which material segment is expanding fastest?

Biodegradable films post the quickest 8.01% CAGR as regulations favour recyclable and compostable formats.

How are sustainability regulations affecting packaging choices?

EU and US laws mandate recyclability and recycled content, pushing converters toward paper-based, mono-material, and bio-resin solutions.

Which application shows the strongest growth?

Crop-protection biologics packaging will grow at 7.45% CAGR, reflecting farmers’ shift toward eco-friendly pest management.

What impact will the Amcor-Berry Global merger have?

The combined entity’s USD 180 million annual R&D budget is expected to accelerate innovation in recyclable and compostable agricultural packs.

Page last updated on: