Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 400.08 Billion |

| Market Size (2031) | USD 515.06 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Packaging Market Analysis by Mordor Intelligence

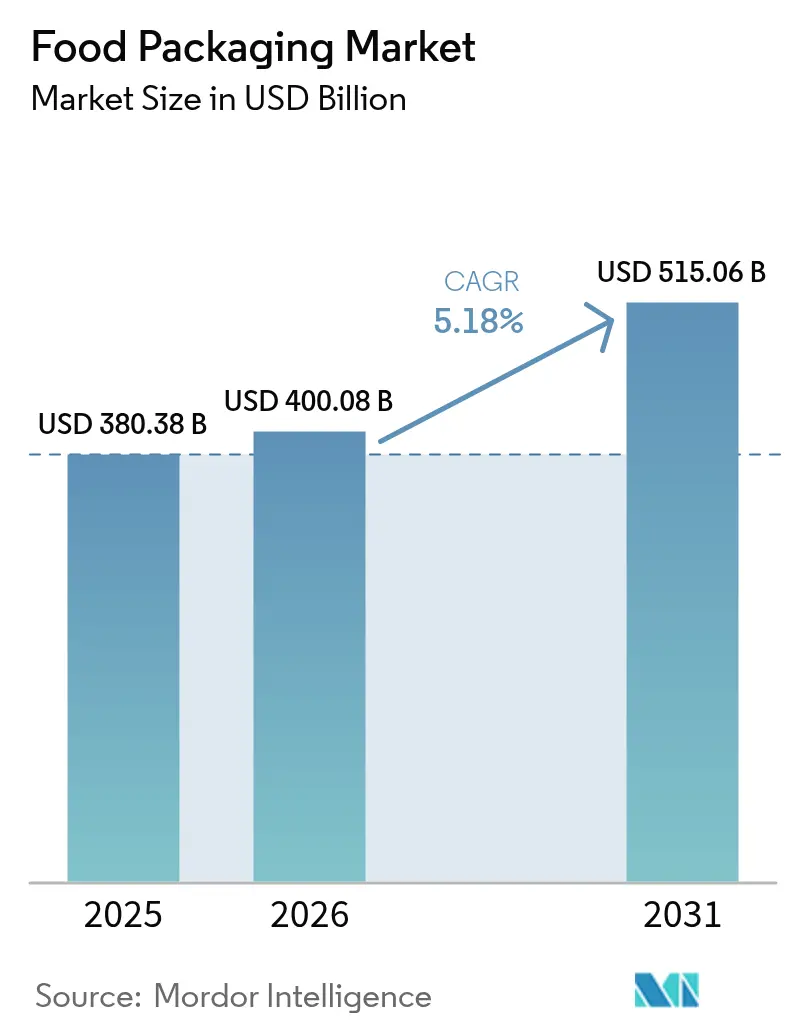

The food packaging market size in 2026 is estimated at USD 400.08 billion, growing from 2025 value of USD 380.38 billion with 2031 projections showing USD 515.06 billion, growing at 5.18% CAGR over 2026-2031. Expansion rests on rapid urbanisation in Asia-Pacific, stronger regulatory attention to recycled content across North America and Europe, and the steady shift among global brand owners toward material-efficient flexible formats. Manufacturers also benefit from investments in cold-chain infrastructure that widen retail reach for chilled and frozen foods, while premiumisation trends revitalise glass demand and encourage adoption of high-barrier technologies able to support clean-label claims. On the supply side, direct customer relationships remain the dominant route to market; however, e-commerce logistics specialists are accelerating uptake of indirect channels that serve small and mid-size food processors. Merger activity among the leading converters is reshaping competitive boundaries by pooling R&D, recycling assets and global distribution footprints.

Key Report Takeaways

- By material, plastics accounted for 58.55% revenue in 2025; glass is set to record the fastest 7.12% CAGR through 2031.

- By packaging format, flexible solutions held 56.10% share in 2025 and are expanding at a 6.18% CAGR.

- By product type, pouches captured 35.25% share in 2025 and will climb at an 8.32% CAGR to 2031.

- By technology, Modified Atmosphere Packaging led with 32.10% share in 2025, whereas aseptic systems are projected to post the highest 8.55% CAGR.

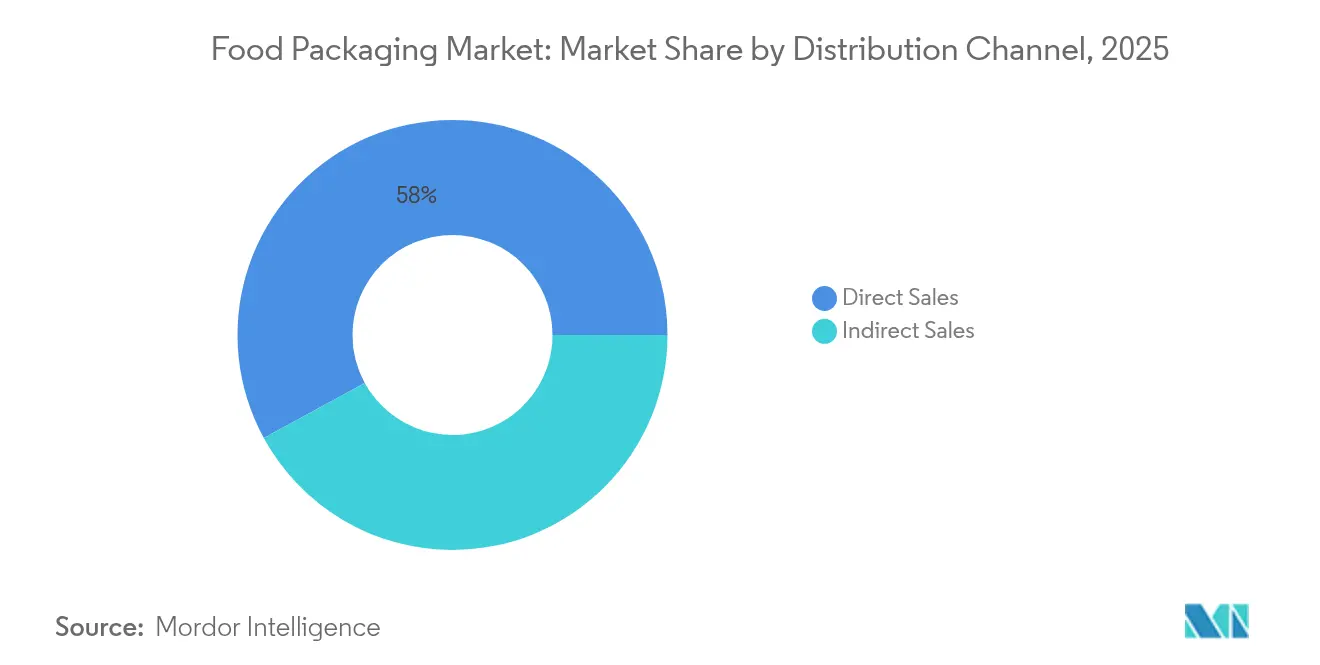

- By distribution channel, direct sales represented 57.95% share in 2025; indirect routes are advancing at a 6.53% CAGR as e-commerce broadens reach.

- By application, poultry and meat products held 28.05% share in 2025, while ready meals are predicted to log the swiftest 7.46% CAGR.

- By region, Asia-Pacific led with 40.85% of food packaging market share in 2025, while the same region is projected to rise at an 8.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated urban convenience retail growth across Asia | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Legislative push for post-consumer recycled content in North America | +0.8% | North America & EU | Short term (≤ 2 years) |

| Expansion of direct-to-consumer meal-kit services in Europe | +0.6% | Europe, expanding to North America | Medium term (2-4 years) |

| Rising demand for ready-to-eat seafood in Japan | +0.4% | Japan, expanding to APAC | Short term (≤ 2 years) |

| Cold-chain build-out in Sub-Saharan Africa | +0.3% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Digital printing for short-run SKUs in Latin America | +0.2% | Latin America, global expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Urban Convenience Retail Growth Across Asia Driving Demand for Single-Serve Packs

Rapid migration to metropolitan areas in China, India and Southeast Asia is shortening shopping cycles and increasing demand for portion-controlled food packs. Convenience stores now reach dense inner-city districts where refrigeration space is limited, rewarding brands that supply lightweight single-serve options able to deliver freshness and curb food waste. Younger working consumers also prize portability, prompting processors to redesign legacy SKUs into resealable pouches or thermoformed cups that command premium price points. The push for on-the-go formats reinforces the food packaging market’s shift toward barrier-enhanced flexibles and thin-gauge rigid plastics that meet shelf-life targets. Investments in small-footprint filling lines have fallen by as much as 18% per unit since 2024, lowering barriers for regional co-packers and accelerating format diversification.

Legislative Push for Post-Consumer Recycled Content in North American Food Packaging

State-level mandates such as California’s SB 54 and Maine’s recycled-content quota are tightening supply of food-grade PCR, raising resin premiums to 15-20% above virgin PET in peak quarters. Brand owners are therefore signing multiyear offtake agreements with recyclers and co-investing in sorting capacity to lock in feedstock security. Equipment suppliers report a 26% rise in orders for extrusion and filtration systems that can process higher PCR ratios without compromising clarity. The legislation also spurs label redesigns that highlight recycled content, resonating with consumers who increasingly equate PCR usage with brand responsibility. EPR fees ranging from USD 192 per ton for glass to USD 423 per ton for plastics are being internalised into long-term cost models, accelerating adoption of mono-material flexible laminates compatible with curbside recycling. [1]Association of Plastic Recyclers, “Recycled Plastic Content Requirements Are Here and More Are Coming Soon. Here Is What You Need to Know,” plasticsrecycling.org

Rapid Expansion of Direct-to-Consumer Meal-Kit Services in Europe Requiring Customisable Temperature-Stable Packaging

Subscription meal-kit operators in Germany, France and the Nordics are leapfrogging traditional chilled distribution by deploying high-insulation shippers integrating phase-change packs suited to seasonal extremes. Lead times of 24-48 hours from assembly to doorstep compel structurally rigid solutions that withstand parcel handling while offering branding real estate for personalised menus. Digital printing facilitates lot-size-one graphics that reinforce customer loyalty, and predictable subscription volumes justify investments in automation tailored to meal-kit dimensions. Material suppliers are refining foam-free pads using cellulose and mineral composites that curb landfill disposal and meet compostability standards. Overall, the segment channels incremental 0.6% CAGR uplift to the broader food packaging market by creating demand for bespoke secondary packs that were marginal only five years ago.

Surge in Demand for Ready-to-Eat Seafood in Japan Fuelling Adoption of High-Barrier Retort Pouches

An ageing population and a rising share of single-person households have catalysed a shift from chilled seafood toward shelf-stable meals. Retortable pouches, equipped with aluminium oxide-coated films, deliver ambient storage for up to 12 months while preserving umami and texture valued by Japanese consumers. Processors are upgrading rotary sterilisation lines to run variable-thickness laminates that cut cycle times by 9%. Brands leverage the pouch facings for recipe storytelling, supporting premium price positioning amid stagnant overall seafood volumes. Government promotion of catch-to-table traceability is further driving coding solutions embedded within pouch materials, linking shoppers to harvest data via QR scans. [2]U.S. Department of Agriculture, “Food Processing Ingredients Annual,” usda.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Single-Use Plastic Directive raises costs for multilayer flexibles | -0.9% | Europe, expanding globally | Short term (≤ 2 years) |

| Volatility in recycled resin pricing | -0.7% | Global, acute in North America & EU | Medium term (2-4 years) |

| Limited industrial composting infrastructure in APAC | -0.5% | APAC core | Long term (≥ 4 years) |

| Migration-safety concerns for recycled paperboard in high-fat foods | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Single-Use Plastic Directive Raising Compliance Costs for Multilayer Flexible Structures

The European Packaging and Packaging Waste Regulation mandates all consumer packs sold after 2028 achieve demonstrable recyclability, imposing steep redesign expenses on converters that rely on PET-PE or PA-PE laminates. Transitioning to mono-material polypropylene or polyethylene structures raises raw-material cost by up to 14% because of barrier-coating upgrades and compatibility tests with existing seal jaws. Sorting facilities must also integrate near-infra-red sensors capable of distinguishing new laminates, an investment smaller municipalities struggle to justify. Manufacturers that cannot amortise the redesign across global volumes are at risk of ceding EU shelf space to larger peers with deeper R&D pipelines.[3]European Parliament, “Packaging and packaging waste,” europarl.europa.eu

Volatility in Recycled Resin Pricing Undermining Cost Competitiveness of Sustainable Formats

Food-grade R-PET and R-PE prices spiked 30-40% within single quarters in 2024, driven by beverage demand fluctuations and export restrictions. Such swings erode profit margins for converters committed to mandatory PCR thresholds, prompting some to hedge through inventory build-ups that tie up working capital. Global brand owners counteract volatility by investing in vertically integrated washing lines, yet capacity additions lag demand by 18-24 months. The uncertainty delays rollout of recyclable pouch platforms and hampers progress toward publicly stated sustainability goals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastics Hold Scale While Glass Accelerates

Plastics generated the highest revenue, holding 58.55% of food packaging market share in 2025 owing to versatility and cost advantages. In value terms, the food packaging market size for plastics is projected to advance at 4.92% CAGR beyond 2026 as bio-circular polypropylene and chemically recycled PET enter commercial scale. Glass, although occupying a smaller base, will grow 7.12% annually, propelled by premium beverages and sauces that leverage infinite recyclability claims.

Growth in paperboard aligns with e-commerce and corrugated shipping demand, while metals sustain niche roles in canned meals through lightweighting innovation. Across all materials, regulatory incentives for recyclability and the emergence of deposit-return systems are influencing brand selections. Material substitution decisions increasingly weigh carbon footprints alongside cost, nudging processors toward mono-material architectures compatible with region-specific recycling streams.

By Packaging Format: Flexible Dominance Built on Efficiency

Flexible solutions captured 56.10% of the overall market in 2025 and will progress at a 6.18% CAGR through 2031. Stand-up pouches, flow wraps and pillow bags reduce shipping weight by up to 70% versus comparable rigid options, supporting retailer sustainability targets. As a result, the food packaging market size for flexible formats is expected to reach USD 307.2 billion within the forecast window.

Rigid plastics, glass jars and metal cans remain indispensable where product integrity and tamper evidence are paramount. Converters are stretching rigid relevance by deploying in-mould label technologies that supply 360-degree graphics without post-application steps. Future format selection will pivot on mechanical recyclability, infrastructure readiness and brand-specific storytelling goals.

By Product Type: Pouches Set the Pace

In 2025 pouches held 35.25% of category revenue and are forecast to rise 8.32% annually, reflecting elevated household acceptance across dry snacks, sauces and baby foods. Multi-layer stand-up pouches accommodate reclose sliders, facilitating portion control and repeat usage. Bottles and jars retain share in ambient beverages and spreads, aided by ergonomic handling features.

Cans secure strong footholds in pet food and seafood owing to robustness and 100% recyclability rates above 70% in Europe. Corrugated boxes continue as secondary and tertiary packaging for growing online grocery shipments. Pouch development now centres on high-barrier mono-PE laminates that target curbside recycling without compromising water-vapour protection.

By Technology: Aseptic Systems Close the Gap on MAP

Modified Atmosphere Packaging contributed 32.10% revenue in 2025 through application in fresh produce, meats and bakery. Aseptic processing, however, is expected to deliver the highest 8.55% CAGR, narrowing the share gap by 2031 as dairy, plant-based milks and sauces capitalise on ambient logistics.The food packaging market share held by aseptic lines is improving due to reductions in sterilant-chemical usage and energy consumption.

High-pressure processing remains confined to premium juices and ready meals but benefits from growing clean-label preferences. Retort remains vital in regional diets favouring shelf-stable proteins, with pouch flexibility allowing faster heat penetration and reduced cook times versus cans.

By Distribution Channel: Indirect Routes Gain Momentum

Direct sales accounted for 57.95% revenue in 2025, reflecting integrated supply agreements between global converters and multinational food groups. Indirect channels, including specialist distributors and online marketplaces, will grow faster at 6.53% CAGR as small brands seek low-volume order flexibility. Procurement digitalisation reduces search costs, encouraging regional converters to display catalogues on B2B platforms that match buyers with nearby stock.

For converters, indirect expansion offers an avenue to smooth capacity utilisation and introduce sustainable portfolios to niche organic food producers. Yet technical service provision remains decisive, meaning full transition away from direct sales is unlikely in the medium term.

By Application: Meat Rules but Ready Meals Surge

Poultry and red-meat packaging held 28.05% revenue in 2025 thanks to stringent shelf-life requirements and consumer safety standards. Vacuum skin packs and MAP trays dominate, underpinned by adoption of easy-peel lidding films that aid product visibility. The food packaging market share commanded by meat is expected to remain above 25% through 2031 despite plant-protein substitution.

Ready meals and convenience foods are forecast to clock a 7.46% CAGR, driven by urban lifestyles and demand for microwave-ready portions. Reusable paperboard sleeves combined with CPET trays illustrate hybrid material strategies that enhance brand sustainability profiles. Other growing uses span dairy fortified drinks, produce snack-packs and high-barrier solutions for seafood, each shaping future R&D priorities.

Geography Analysis

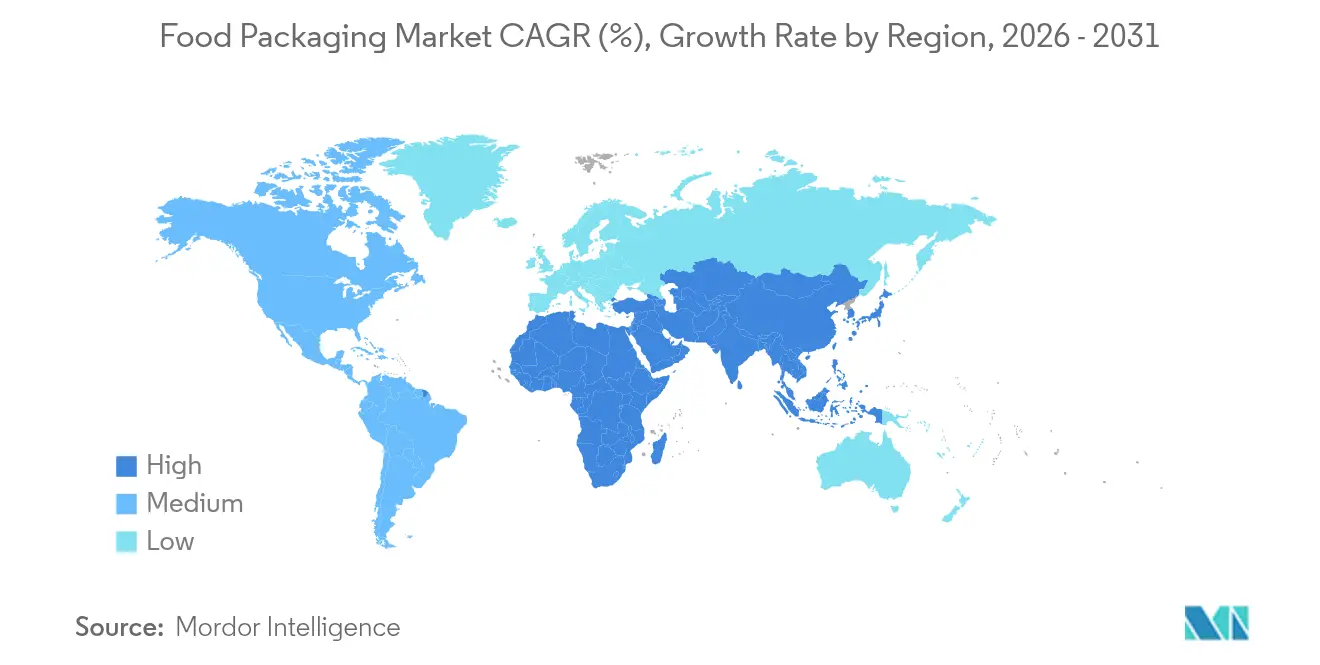

Asia-Pacific generated 40.85% of global revenue in 2025 and is expected to expand at an 8.22% CAGR through 2031, propelled by rising incomes, cold-chain expansion and a surge in organised retail. China’s scale provides significant pull for polymer suppliers, while India’s government incentives for food parks are spurring domestic demand for carton, pouch and rigid PET formats. Japan and South Korea focus on premiumisation and recyclable glass, whereas Southeast Asian nations rapidly adopt lightweight flexibles to counter rising freight costs. Region-wide, the food packaging market size is forecast to surpass USD 245.8 billion by 2031, reflecting both export-oriented agri-food growth and domestic consumption upgrades.

North America ranks second in value, sustained by mature packaged food categories and leadership in PCR regulation. The United States is at the forefront of plant-based material trials and chemical recycling pilots that promise scalable circularity. Canada supports sector development with tax credits for recycling infrastructure, and Mexico capitalises on proximity to US retailers by attracting joint-venture converters along the border. EPR schemes, live in four states and pending in several others, incentivise mono-material design and recyclability labelling. Collectively, these policies underpin a steady mid-single-digit CAGR despite high base consumption.

Europe’s market is shaped by stringent ecological rules under the PPWR. Germany, the United Kingdom and France dominate volume; Italy leads in design innovation for compostable trays. Eastern European production clusters are attracting investments from Western converters seeking cost efficiencies. Despite regulatory burdens, Europe remains a knowledge hub for deposit-return systems, influencing policy in Latin America and Africa. While growth lags Asia, the continent secures value through premium sustainable packs and high adoption of digital watermarking for waste-sorting.

Competitive Landscape

The industry demonstrates fragmented following a wave of mergers and acquisitions that bolstered incumbent scale and innovation budgets. Amcor’s USD 8.4 billion purchase of Berry Global combined complementary flexibles portfolios, yielding an entity with USD 24 billion annual sales and a global footprint across 45 countries. Sonoco’s USD 3.9 billion addition of Eviosys produced a leading metal-can specialist with synergies in aerosol and seafood end-markets, while Smurfit WestRock emerged from a USD 11.2 billion paper giant tie-up that positions the firm to leverage containerboard integration.

Strategic focus now tilts toward developing barrier-coated paper, compostable films and PCR-rich rigid containers that satisfy future regulatory curves. Patents such as Amcor’s AmFiber Performance Paper underscore the race for proprietary solutions that deliver both high oxygen resistance and curbside recyclability. Simultaneously, converters are investing in closed-loop recycling, including vertically integrated wash plants near urban centres to secure feedstock for high-purity PCR.

New entrants concentrate on niche technologies: start-ups harnessing mycelium-based foams for insulation, IoT-enabled smart labels that track cold-chain compliance, and refill-ready rigid systems for zero-waste grocery concepts. Although their market shares remain small, alliance deals with retailers and CPGs provide pathways to scale. Overall, competitive intensity centres on speed to sustainable innovation, cost leadership in PCR sourcing and the ability to deliver personalised graphics at commercial speed.

Food Packaging Industry Leaders

Amcor Plc.

Mondi Group

Sealed Air Corporation

Smurfit WestRock

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tetra Pak and Cayuga Milk Ingredients completed a USD 270 million New York dairy-plant upgrade adding UHT/aseptic lines

- May 2025: ProMach acquired DJS Systems, broadening automation capabilities for disposable food packs.

- March 2025: Faerch Group bought MCP Performance Plastic to expand in the USD 55 billion US food packaging market.

- February 2025: Metsä Group partnered with Amcor to co-develop moulded-fibre food packaging.

Global Food Packaging Market Report Scope

Food packaging encompasses the materials and containers used to wrap, protect, preserve, transport, and display food products. It is essential in the food supply chain to ensure food safety and hygiene, extend shelf life, and maintain food quality, convenience, and consumer information.

The food packaging market is segmented by type of material (plastic, metal, glass, and paper & paperboard), packaging type (rigid, semi-rigid, flexible), product type (cans, converted roll stock, gusseted box, corrugated box, and boxboard), application (dairy products, poultry & meat products, fruits & vegetables, and bakery & confectionery) and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material Type

| Plastics | PET |

| PE (HDPE and LDPE) | |

| PP | |

| Other Plastics | |

| Paper and Paperboard | |

| Metal | |

| Glass |

By Packaging Format

| Rigid |

| Flexible |

By Product Type

| Cans |

| Bottles and Jars |

| Pouches |

| Corrugated Boxes |

| Other Product Type |

By Technology

| Modified Atmosphere Packaging (MAP) |

| Vacuum Packaging |

| Hot-Fill |

| High-Pressure Processing (HPP) |

| Aseptic |

| Retort |

By Distribution Channel

| Direct Sales |

| Indirect Sales |

By Application

| Dairy Products |

| Poultry and Meat Products |

| Fruits and Vegetables |

| Bakery and Confectionery |

| Seafood |

| Ready Meals and Convenience Food |

| Frozen Food |

| Other Application |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Plastics | PET | |

| PE (HDPE and LDPE) | |||

| PP | |||

| Other Plastics | |||

| Paper and Paperboard | |||

| Metal | |||

| Glass | |||

| By Packaging Format | Rigid | ||

| Flexible | |||

| By Product Type | Cans | ||

| Bottles and Jars | |||

| Pouches | |||

| Corrugated Boxes | |||

| Other Product Type | |||

| By Technology | Modified Atmosphere Packaging (MAP) | ||

| Vacuum Packaging | |||

| Hot-Fill | |||

| High-Pressure Processing (HPP) | |||

| Aseptic | |||

| Retort | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Application | Dairy Products | ||

| Poultry and Meat Products | |||

| Fruits and Vegetables | |||

| Bakery and Confectionery | |||

| Seafood | |||

| Ready Meals and Convenience Food | |||

| Frozen Food | |||

| Other Application | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the food packaging market and how fast is it growing?

The market stands at USD 400.08 billion in 2026 and is on track to reach USD 515.06 billion by 2031, advancing at a 5.18% CAGR.

Which region generates the highest revenue in food packaging?

Asia-Pacific leads with 40.85% of global revenue in 2025 and is also the fastest-growing region at an 8.22% CAGR through 2031.

Why are flexible packaging formats gaining share?

Flexible packs use less material, cut freight weight by up to 70%, and meet brand sustainability goals, helping them secure 56.10% market share in 2025 and a 6.18% growth rate.

Which packaging technology is projected to grow the fastest?

Aseptic processing shows the highest momentum with an expected 8.55% CAGR, driven by demand for shelf-stable dairy, beverages and sauces.

How do North American regulations influence recycled content usage?

Mandates such as California’s SB 54 require minimum PCR levels, pushing resin premiums up by 15-20% versus virgin PET and prompting long-term supply contracts.

What challenge does the EU Single-Use Plastic Directive pose to multilayer flexibles?

The regulation forces a redesign to recyclable mono-material structures, raising production costs by as much as 14% and tightening compliance timelines to 2028.

Page last updated on: