Food And Beverage Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

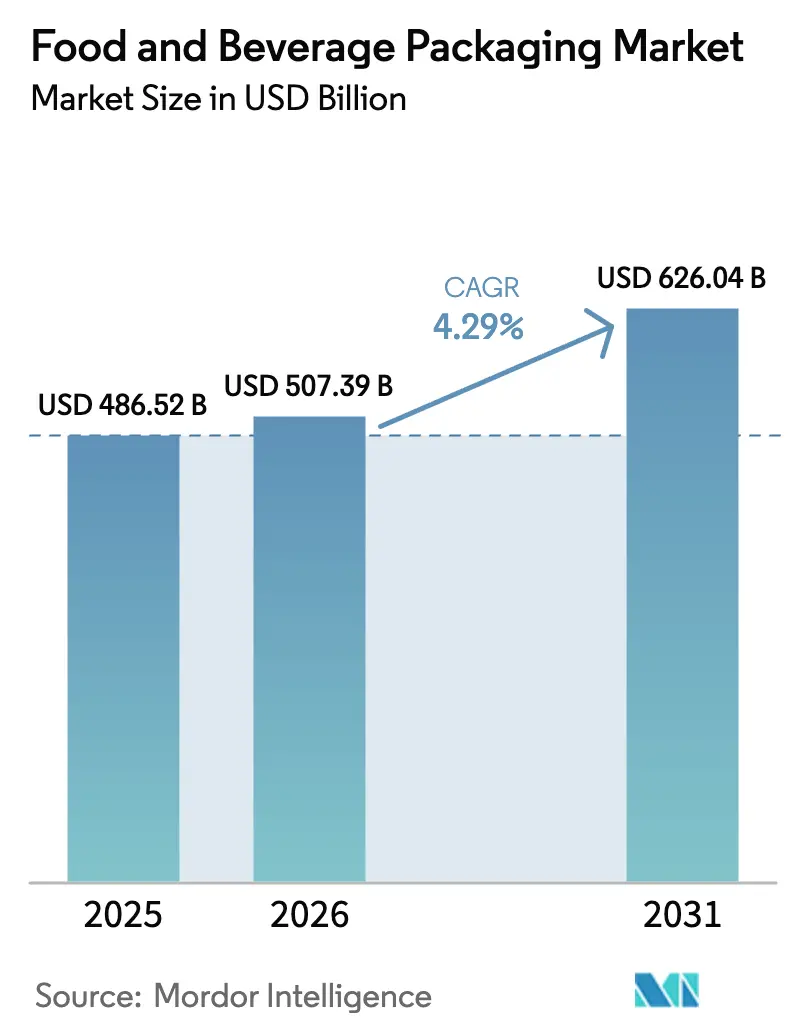

| Market Size (2026) | USD 507.39 Billion |

| Market Size (2031) | USD 626.04 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

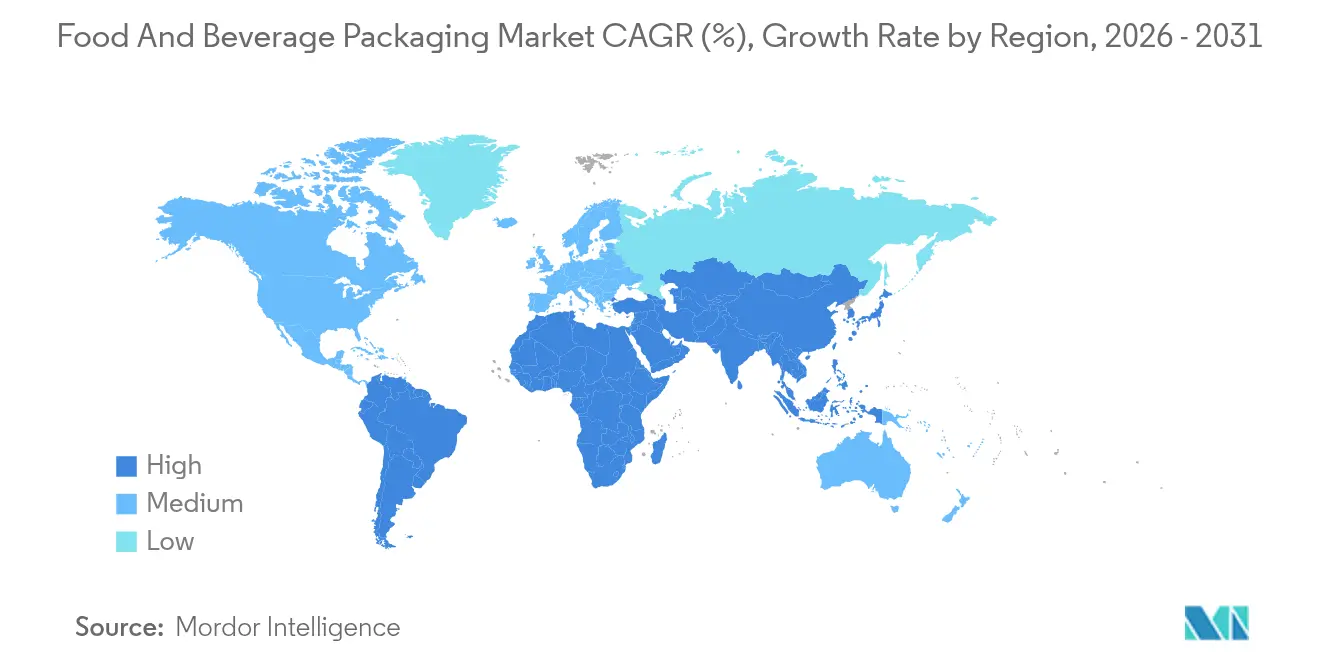

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

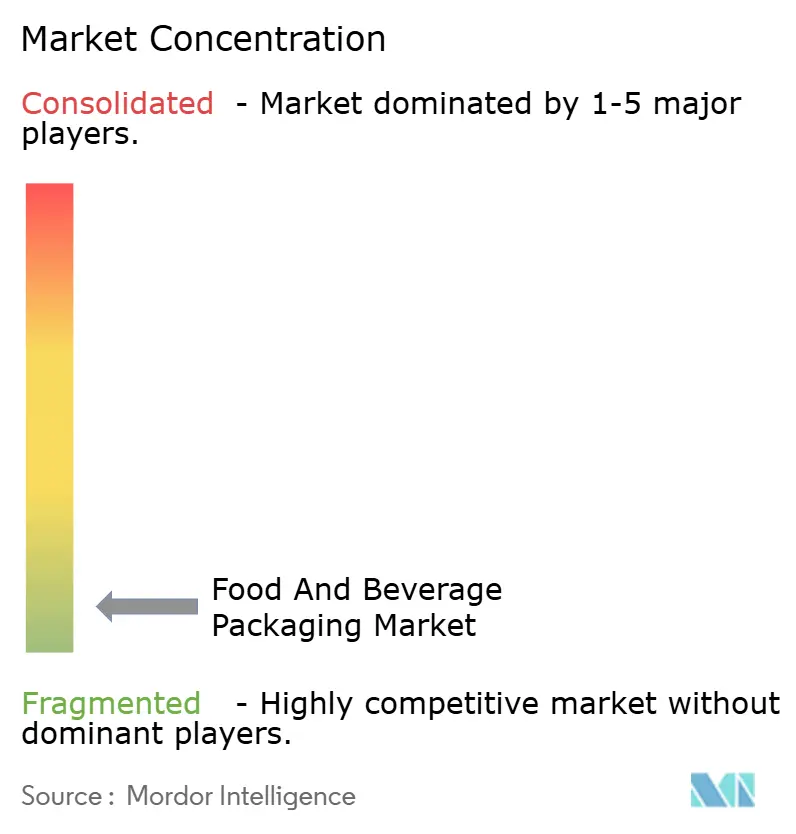

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food And Beverage Packaging Market Analysis by Mordor Intelligence

The food and beverage packaging market size is expected to grow from USD 486.52 billion in 2025 to USD 507.39 billion in 2026 and is forecast to reach USD 626.04 billion by 2031 at 4.29% CAGR over 2026-2031. The ability to meet sustainability mandates while containing material inflation keeps demand steady across core substrates. Consumer preference for single-serve packs, regulatory pushes for recycled content, and investments in high-barrier mono-material films jointly underpin revenue growth. Established converters rely on scale to fund R&D in compostable polymers, whereas mid-tier players focus on regional quick-commerce contracts. Heightened cost volatility for aluminum and glass is spurring substitution toward flexible laminates, yet premium beverage brands continue to favor metal and glass for differentiation. Across geographies, policy harmonization—particularly around extended producer responsibility (EPR) fees—shapes long-term capital allocation decisions for the global food and beverage packaging market.

Key Report Takeaways

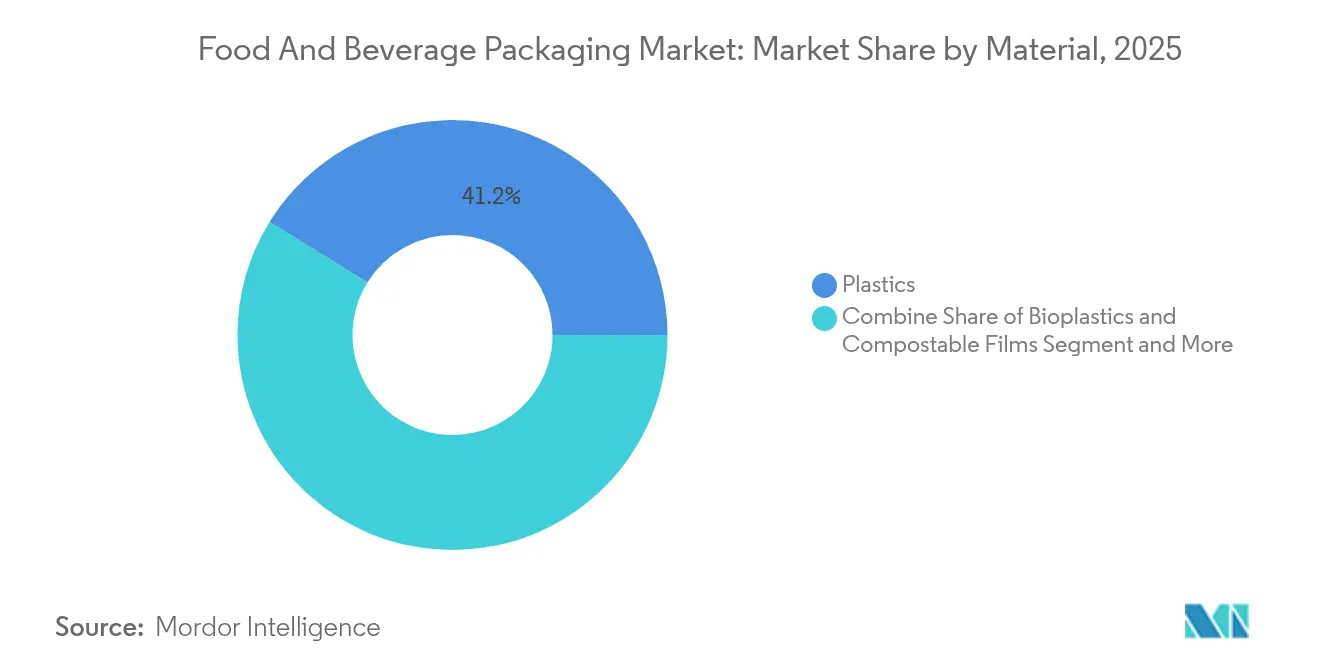

- By material, plastics led with 41.20% of the food and beverage packaging market share in 2025; bioplastics and compostable films are forecast to post the fastest 7.52% CAGR through 2031.

- By product format, flexible packaging accounted for 54.10% of 2025 revenue, while rigid formats are projected to trail at a 2.67% CAGR.

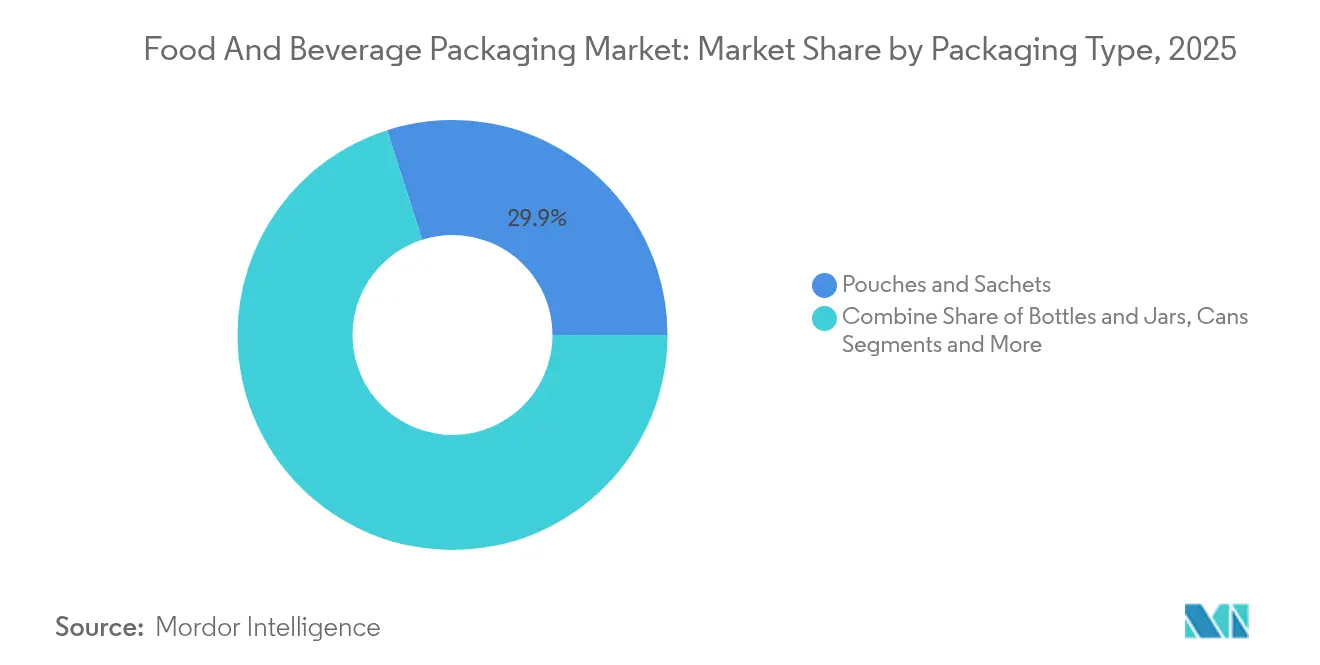

- By packaging type, pouches and sachets captured 29.92% share of the food and beverage packaging market size in 2025 and are set to grow at 7.55% CAGR to 2031.

- By application, food retained 56.20% revenue share in 2025; beverages are expected to register the highest 5.61% CAGR through 2031.

- By geography, Asia-Pacific commanded 41.40% of 2025 revenue and is projected to lead with a 7.18% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food And Beverage Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for single-serve ready-to-eat meals among Asian millennials | +1.2% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Brewery shift to lightweight recyclable aluminum bottles in N. America | +0.8% | North America & Europe | Short term (≤ 2 years) |

| EU "Green Deal" targets drive paper-based barrier innovations | +0.9% | Europe core, spill-over to Global | Long term (≥ 4 years) |

| Quick-commerce boom needs tamper-evident secondary packs | +0.7% | Global, with early gains in urban centers | Short term (≤ 2 years) |

| Craft-spirit premiumization in LatAm boosts embossed glass with NFC closures | +0.4% | South America & North America | Medium term (2-4 years) |

| Rise of dairy-alternative drinks drives aseptic cartons | +0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Single-Serve Ready-to-Eat Meals Among Asian Millennials

Single-serve pack formats are proliferating across Asia-Pacific as urban millennials trade traditional cooking for convenience-centric eating occasions. Portion-controlled SKUs enable premium per-unit pricing, reduce household food waste, and align with regulations that incentivize smaller pack sizes through favorable tax treatment. The food and beverage packaging market benefits as co-packers invest in high-throughput form-fill-seal lines capable of running multiple SKU sizes with rapid changeovers. Digital grocery platforms reinforce the trend because compact portions fit the tight delivery windows and limited refrigeration space common in dense cities. Regional converters that secure recyclable mono-material structures gain a first-mover cost advantage once EPR fees escalate. Amid this shift, multinational brands localize flavor profiles in 100 g–250 g pouches to capture weekday lunch-box demand, underpinning volume growth for the food and beverage packaging market. [1]Roland Foods, “March 2025 Regional Market Report News,” rolandfoods.com

Brewery Shift to Lightweight Recyclable Aluminum Bottles in North America

Craft and premium breweries are accelerating the transition from glass to lightweight aluminum bottles to curb freight costs, improve shelf stability, and elevate sustainability credentials. The switch cuts outbound logistics weight by roughly 60%, which offsets volatility in can-sheet premiums tied to constrained smelting capacity. Aluminum’s near-infinite recyclability resonates with advocacy groups that publish brand-scorecards on circularity, nudging purchasing managers to favor metal over non-recyclable laminates. The investment case strengthened when Ball Corporation integrated Florida Can Manufacturing in 2025 to secure incremental supply for short-run specialty SKUs. [2] Ball Corporation, “Further Optimizes North American Network with Florida Can Manufacturing Acquisition,” ball.com With hop-forward styles sensitive to photodegradation, breweries adopt matte sleeves and internal varnishes to preserve flavor. These performance advantages sustain high-single-digit tonnage growth for aluminum bottles across the food and beverage packaging market.

EU “Green Deal” Targets Drive Paper-Based Barrier Innovations

Europe’s Packaging and Packaging Waste Regulation mandates that all packs be reusable or recyclable by 2030, compelling converters to retrofit paper substrates with bio-based coatings that rival multilayer plastics. Early adopters deploy dispersion-coated fiber that maintains grease-resistance without PFAS, thereby avoiding looming per- and polyfluoroalkyl substance bans. Capital expenditure is rising for pilot coaters that test chitosan or PVOH layers capable of withstanding humid distribution channels. Retailers attach “recycle-ready” iconography to spur consumer sorting compliance, reinforcing volume upside for barrier-enhanced paperboard. Scale advantages accrue to mills that vertically integrate pulp, coating chemistry, and lamination, consolidating share within the European region of the food and beverage packaging market.

Quick-Commerce Boom Needs Tamper-Evident Secondary Packs

The promise of 30-minute grocery delivery reshapes upstream packaging design. Primary packs engineered for retail shelves often lack the seal integrity needed for couriers who handle totes multiple times before hand-off. Brands now specify polymer-based over-wraps with frangible tear-strips, or paperboard sleeves embedded with VOID-if-tampered inks. Liability frameworks widen to encompass last-mile platforms, making tamper evidence a legal necessity. Pack solutions integrate QR codes that log seal status at dispatch and arrival, enhancing traceability. Converters supplying the food and beverage packaging market invest in digital presses for serialized graphics, enabling small-batch city-specific runs that marry security and marketing in a single component.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-tax surcharges on virgin-content packs in UK and Canada | -0.6% | North America & Europe | Short term (≤ 2 years) |

| US PFAS limits force costly paperboard reformulation | -0.8% | North America core, spill-over to Global | Medium term (2-4 years) |

| Aluminum can-sheet shortages restrict supply for craft brewers | -0.5% | Global | Short term (≤ 2 years) |

| Energy-intensive glass melting raises costs in EU | -0.4% | Europe core, spill-over to Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-Tax Surcharges on Virgin-Content Packs in UK and Canada

Taxes levied on packaging with less than 30% recycled content add 15–20% to resin-based input costs in early-adopter markets. Small converters lacking reclaim capacity face margin compression or customer attrition, accelerating merger pipelines as regional players seek scale to amortize pelletizing and washing investments. Brand owners hedge by redesigning SKUs in mono-PP films that incorporate post-consumer resin, though clarity and odor challenges persist. Cross-border arbitrage emerges, with extruders in low-tax jurisdictions exporting rollstock to brand owners in taxed markets, slightly muting policy effectiveness. Over the forecast horizon, such fiscal drag trims the baseline growth rate of the food and beverage packaging market amid compliance learning curves.

US PFAS Limits Force Costly Paperboard Reformulation

From 2024, the US FDA restricts PFAS in food-contact coatings, prompting redesign across roughly 40% of grease-resistant paperboard volumes. Alternative water-based coatings can raise board basis weight by 10%, eroding run speeds and inflating transport emissions. Mills invest in pilot coaters to qualify alginate or carnauba systems, but downstream printers must recalibrate ovens to cure at lower temperatures. Foodservice chains negotiate surcharges while seeking co-branding that highlights safer chemistry, positioning compliance as a consumer-trust asset. Nonetheless, prolonged certification timelines squeeze cash flows for independent converters, applying a moderate negative pressure to the food and beverage packaging market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bioplastics Drive Sustainability Transformation

Demand patterns underscore plastics’ versatility, with conventional resins retaining 41.20% share in 2025. Yet regulatory ceilings on virgin polymer use and landfill restrictions unlock 7.52% CAGR for bioplastics, positioning them as the clear volumetric outlier through 2031 within the food and beverage packaging market. Early adopters blend PLA with PBAT to achieve home-compostable certification, thereby qualifying for municipal collection pilots in Europe and China. Brand-owner RFPs now weight carbon footprint reduction ahead of resin cost, tilting scorecards toward biopolymer bids. As capacity expands in Thailand and the United States, unit costs are forecast to converge with LDPE by 2027, accelerating substitution in dry snack pouches. Paper and paperboard sustain mid-single-digit growth, buoyed by corrugated e-commerce shippers that require no food-contact compliance. Meanwhile, aluminum’s share inches upward in premium RTD coffee cans because of its impeccable oxygen barrier and infinite recyclability. Glass volumes stay flat, but average selling price escalates as spirits brands premiumize bottle design with UV-cured metallic inks.

The economic case for bioplastics strengthens once EPR fee differentials widen. Producers of PLA and PHA now integrate fermentation residues into biomass boilers, achieving cradle-to-gate emissions cuts that attract ESG-linked financing. Processors in the food and beverage packaging industry retrofit blown-film lines with lower-shear screws to maintain throughput when running PLA blends. Material suppliers bundle technical support packages, reducing qualification lead times for co-packers. These ecosystem gains reinforce the structural pivot toward bio-derived substrates across the breadth of the food and beverage packaging market.

By Product Format: Flexible Packaging Leads Innovation

Flexible laminates commanded 54.10% revenue in 2025 and are projected to advance at a 5.72% CAGR, solidifying their role as the core substrate family for the food and beverage packaging market. Weight-to-product ratios up to 80% lower than rigid packs translate into freight savings and carbon-label advantages that resonate with net-zero roadmaps. Retort pouches for shelf-stable soups swap aluminum foil for ultra-thin oxide-coated PET, slashing pack weight while retaining 121 °C sterilization resilience. Converter R&D funnels capital into solvent-free adhesive systems that speed curing and trim VOC emissions. In chilled dairy, thermoformable mono-PET webs replace multi-material structures, enabling closed-loop bottle-to-tray recycling. Rigid packaging retains critical niches, especially where in-use ergonomics or on-shelf blocking factor matter—glass jars for gourmet condiments, composite cans for powdered beverages, and multilayer PET bottles for hot-fill juice.

As corporate climate pledges tighten, investment shifts to flexible mono-material platforms. Amcor’s recycle-ready portfolio exemplifies the trend, delivering drop-in rollstock that achieves up to 35% PCR incorporation without compromising barrier or seal performance. Digital watermark initiatives financed by European brand coalitions promise to streamline near-infrared sorting, preparing infrastructure for high-grade film reclaim. Together, these developments cement flexible formats as the most dynamic battleground within the food and beverage packaging market.

By Packaging Type: Pouches and Sachets Capture Growth

Pouches and sachets held 29.92% share of the food and beverage packaging market size in 2025 and are on track for 7.55% CAGR. Value stems from efficient cube utilization and reduced headspace, which lower transport emissions and warehouse footprints. Reclosable spouts make stand-up pouches viable for family-sized condiments, while three-side-seal sachets enable micronutrient fortification in low-income regions. Brand marketers exploit high printable surface area to differentiate SKUs in congested digital storefronts. Aluminum cans sustain relevance in carbonated categories, yet can-sheet scarcity forces price escalations that marginally erode volume intent among independent craft brewers. Bottles—both glass and PET—maintain shelf-impact advantages but undergo lightweighting to stay cost-competitive.

Emergence of e-commerce-ready pouch structures with drop-test ratings up to 1 m widens application scope into fragile fillings such as whipped dairy and cold-brew coffee concentrates. Smart-label integrations deliver batch-level authenticity checks, supporting cross-border compliance for infant nutrition brands. Tetra Pak’s carton-based innovations further blur format boundaries by accommodating granular particulates without clogging aseptic fillers. Collectively, these trajectories affirm pouches and sachets as the fastest-moving node in the evolving architecture of the food and beverage packaging market.

By Application: Beverages Drive Premium Innovation

While food accounted for 56.20% of 2025 revenue, beverages are forecast to rise at a 5.61% CAGR, reflecting a pivot toward premium experiential consumption. Craft breweries escalate aluminum packaging demand, leveraging full-body shrink sleeves for seasonal limited editions. Functional drinks fortified with collagen or adaptogens pursue amber glass to protect light-sensitive actives, sustaining furnace utilization in Europe and North America. Spirits houses integrate NFC neck tags to combat counterfeiting, validating purchases via blockchain ledgers maintained by consortiums of distillers. Dairy-alternative beverages rely on aseptic carton lines to ship non-refrigerated SKUs, freeing retailers from cold-chain overheads and widening geographic reach. Within the food and beverage packaging market, these beverage-centric innovations command higher price realization than bulk food staples, cushioning converters against raw-material inflation.

Forward-looking portfolios feature hybrid packs—PET bottles with molded-in handles housed in paperboard multipacks—designed to meet plastic-reduction pledges without sacrificing consumer convenience. Diageo’s research shows millennial consumers are willing to pay a 12% premium for spirits in low-carbon packs, driving R&D into glass cullet substitution with recycled feldspar. This willingness to reward sustainable design fuels continuous iteration among converters serving beverage clients, ensuring a robust growth corridor for the broader food and beverage packaging market.

Geography Analysis

Asia-Pacific dominates the food and beverage packaging market with 41.40% revenue in 2025 and projects a 7.18% CAGR through 2031. China’s ban on non-recyclable multilayer films catalyzes investment in PE-based mono-material plants, while India’s mandatory extended producer responsibility fees stimulate collection network upgrades. Urban middle-class households in Indonesia and Vietnam shift away from wet-market bulk buying toward bar-coded packaged staples, boosting demand for sachet and pouch lines. Government subsidies for biopolymer compounding in Thailand accelerate regional capacity, reducing reliance on imported PLA pellets. Multinationals localize production to buffer foreign-exchange risk, reinforcing Asia-Pacific’s outsized contribution to the food and beverage packaging market.

North America combines innovation depth with raw-material self-sufficiency, anchoring premiumization. U.S. can-sheet mills expand capacity to serve hard-seltzer and ready-to-drink coffee launches, offsetting slight declines in carbonated soft drinks. Canadian regulators implement a graduated recycled-content tax credit, encouraging investment in mechanical PET recycling. Mexico leverages its proximity to the U.S. to attract greenfield pouch-making operations targeting convenience-store chains across the border. Collectively, these dynamics secure North America’s position as the second-largest contributor to the food and beverage packaging market.

Europe operates as the global regulatory bellwether. The PPWR’s 2030 recyclability mandate compels end-market redesigns and drives uptake of paper-based barrier packs. Germany’s deposit-return expansion to include dairy drinks lifts PET collection rates above 90%. Southern European glassworks integrate bio-fuel furnaces to mitigate carbon levies, sustaining competitive export pricing. Eastern Europe emerges as a cost-effective hub for flexo-printed corrugated displays destined for Western retailers. Such intra-regional specialization underpins Europe’s mature yet steadily growing share of the food and beverage packaging market.

Mordor Intelligence provides coverage of the food and beverage packaging market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

Market structure remains fragmented. Amcor channels USD 200 million annually into next-generation recycle-ready films, positioning itself as the preferred partner for FMCG sustainability roadmaps. Tetra Pak’s service contracts bundle preventive maintenance with line-optimization analytics, deepening customer lock-in across 9,000 aseptic fillers worldwide. Mondi leverages cradle-to-cradle certified kraft paper assets to secure long-term supply agreements with European retailers transitioning away from plastic carriers.

Transaction activity has accelerated. Sonoco’s USD 3.9 billion acquisition of Eviosys—completed in December 2024—creates the world’s largest metal food-can platform and broadens its aerosol footprint. Ball’s purchase of Florida Can Manufacturing removes a regional bottleneck, ensuring stable supply for Southeastern breweries Meanwhile, niche innovators pursue white-space: U-flex in India scales digital-printed pouches for D2C brands; Pulpex develops molded-fiber bottles for non-carbonated drinks. Competitive intensity will heighten as EPR fees and decarbonization targets favor vertically integrated players within the food and beverage packaging market.

Digitalization forms the new frontier. Converters embed RFID in cases to monitor cold-chain compliance, while blockchain pilots trace aluminum from smelter to shelf. Early successes secure customer loyalty and enable premium pricing structures that offset capex. Nevertheless, rising energy costs threaten margins for glassmakers and extrusion blow-molders, spurring joint procurement of renewable power. The interplay of sustainability, consolidation, and smart-packaging adoption will keep strategic maneuvering brisk throughout the forecast horizon of the food and beverage packaging market.

Food And Beverage Packaging Industry Leaders

Mondi plc

Amcor Plc

Sealed Air Corporation

Sonoco Products Company

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ball Corporation acquired Florida Can Manufacturing to optimize its North American aluminum beverage packaging network, enhancing regional supply resilience.

- January 2025: Packaging Corporation of America instituted a USD 70 per-ton corrugated price increase effective January 1 to counter higher fiber costs.

- December 2024: Sonoco Products Company completed the EUR 3.6 billion (USD 3.9 billion) acquisition of Eviosys, forming the world’s largest metal food-can and aerosol producer.

- July 2024: O-I Glass commenced a USD 150 million technology and sustainability upgrade at its Alloa, UK plant, including low-NOx furnace rebuilds.

Global Food And Beverage Packaging Market Report Scope

Food and beverage packaging protects products from external resistance, tampering, breakage, and damage. Proper packaging of food and beverages can also preserve the product for longer use. Packaging is an important part of the food and beverage industry and helps maintain product hygiene.

The food and beverage packaging market is segmented for food packaging market by material (plastic, paperboard, metal, glass), type of product (pouches and bags, bottles and jars, trays and containers, films and wraps, other types of products), application (dairy products, meat, poultry, and seafood, bakery and confectionary, fruits and vegetables, other applications) and beverage packaging market by material (plastic, paperboard, metal, glass), type of product (bottles, cans, pouches and cartons, caps and closures, other types of products), application (carbonated soft drinks and fruit beverages, beer, wine and distilled spirits, bottled water, milk, energy and sports drinks, other applications) and by geography (North America [United States and Canada], Europe [United Kingdom, Germany, France and Rest of Europe], Asia-Pacific [China, Japan, India and Rest of Asia-Pacific], Latin America [Brazil, Mexico and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa and Rest of Middle East and Africa]. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Plastics |

| Paper and Paperboard |

| Metal |

| Glass |

| Bioplastics and Compostable Films |

| Flexible Packaging |

| Rigid Packaging |

| Bottles and Jars |

| Cans |

| Pouches and Sachets |

| Caps and Closures |

| Trays and Containers |

| Films and Wraps |

| Other Packaging Types |

| Food | Dairy Products |

| Meat, Poultry and Seafood | |

| Bakery and Confectionery | |

| Fruits and Vegetables | |

| Other Food Product | |

| Beverages | Carbonated Soft Drinks |

| Beer | |

| Spirits | |

| Dairy-based Beverages | |

| Other Beverages |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material | Plastics | ||

| Paper and Paperboard | |||

| Metal | |||

| Glass | |||

| Bioplastics and Compostable Films | |||

| By Product Format | Flexible Packaging | ||

| Rigid Packaging | |||

| By Packaging Type | Bottles and Jars | ||

| Cans | |||

| Pouches and Sachets | |||

| Caps and Closures | |||

| Trays and Containers | |||

| Films and Wraps | |||

| Other Packaging Types | |||

| By Application | Food | Dairy Products | |

| Meat, Poultry and Seafood | |||

| Bakery and Confectionery | |||

| Fruits and Vegetables | |||

| Other Food Product | |||

| Beverages | Carbonated Soft Drinks | ||

| Beer | |||

| Spirits | |||

| Dairy-based Beverages | |||

| Other Beverages | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the food and beverage packaging market?

The food and beverage packaging market size is valued at USD 507.39 billion in 2026, with a forecast to reach USD 626.04 billion by 2031.

Which region is growing fastest in the food and beverage packaging market?

Asia-Pacific is projected to expand at a 7.18% CAGR through 2031, the highest among all regions due to rapid urbanization and regulatory support for sustainable packs.

Why are pouches and sachets gaining popularity?

They optimize cube utilization, cut logistics emissions, and meet portion-control demand, enabling a 7.55% CAGR and 29.92% revenue share in 2025.

How are sustainability regulations influencing material choices?

Plastic-tax surcharges and PFAS bans drive adoption of recycled resins, bioplastics, and PFAS-free paperboard, prompting converters to retool for compliant substrates.

What role does digitalization play in packaging innovation?

RFID-enabled traceability, blockchain authentication, and QR-based consumer engagement are gaining traction, allowing brands to ensure security and collect usage data.

Page last updated on: