Cosmetics Refill And Reusable System Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

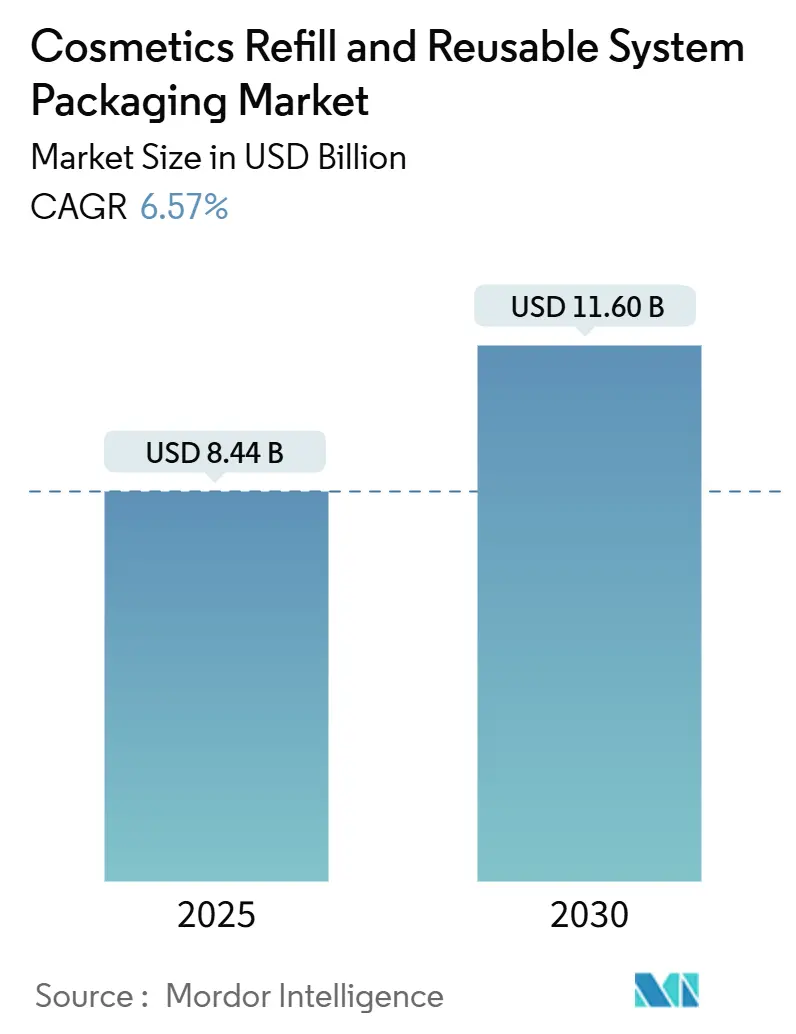

| Market Size (2025) | USD 8.44 Billion |

| Market Size (2030) | USD 11.60 Billion |

| Growth Rate (2025 - 2030) | 6.57% CAGR |

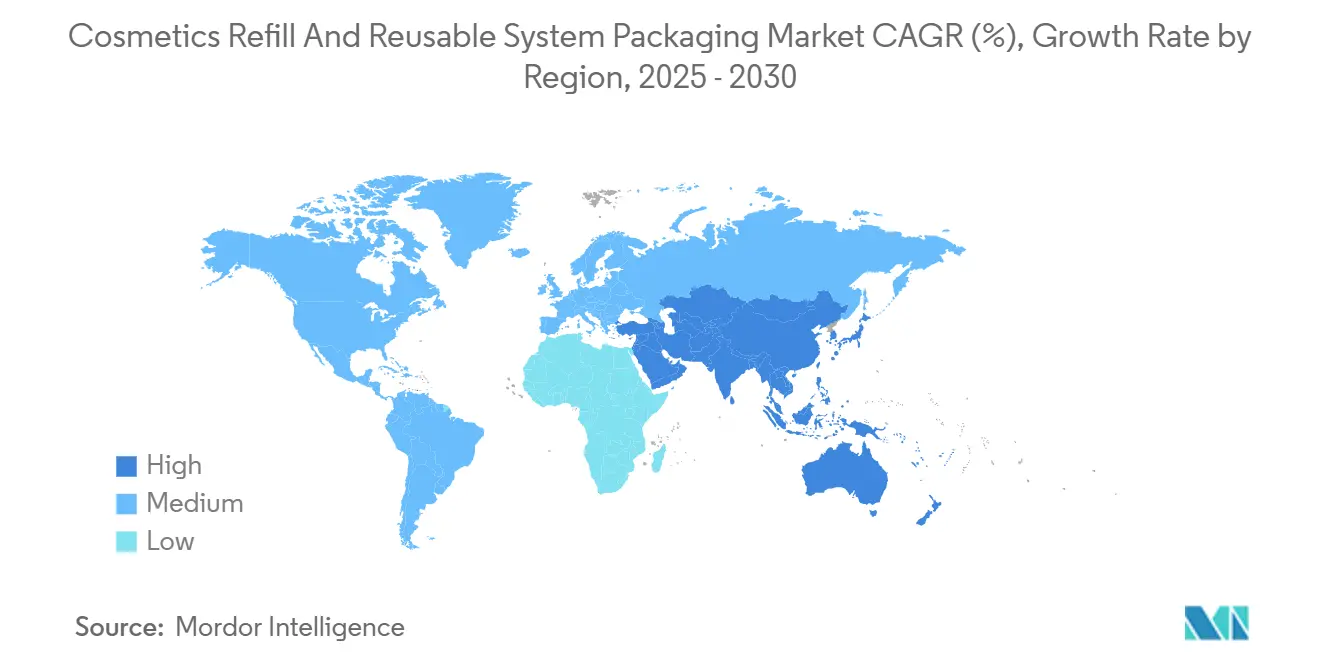

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetics Refill And Reusable System Packaging Market Analysis by Mordor Intelligence

The cosmetics refill and reusable system packaging market size is estimated at USD 8.44 billion in 2025 and is projected to reach USD 11.6 billion by 2030, growing at a 6.57% CAGR. This trajectory reflects the tightening of global rules on single-use plastics, most notably the European Union's restriction on microplastics, which entered into force in January 2024. Retail collaborations, such as Loop’s expansion with major chains, deliver up to 40% packaging cost savings for partner brands and encourage rapid consumer adoption. Regional progress remains uneven: Europe holds the leading 32.71% share, backed by stringent waste directives, while the Asia-Pacific region posts the fastest 8.49% CAGR, thanks to urban digital consumers who equate reusable formats with status and convenience. Although the arena is fragmented, large multinationals are now competing with smaller specialists for the first-mover advantage, and technology-enabled reverse logistics programs report container return rates as high as 85%.

Key Report Takeaways

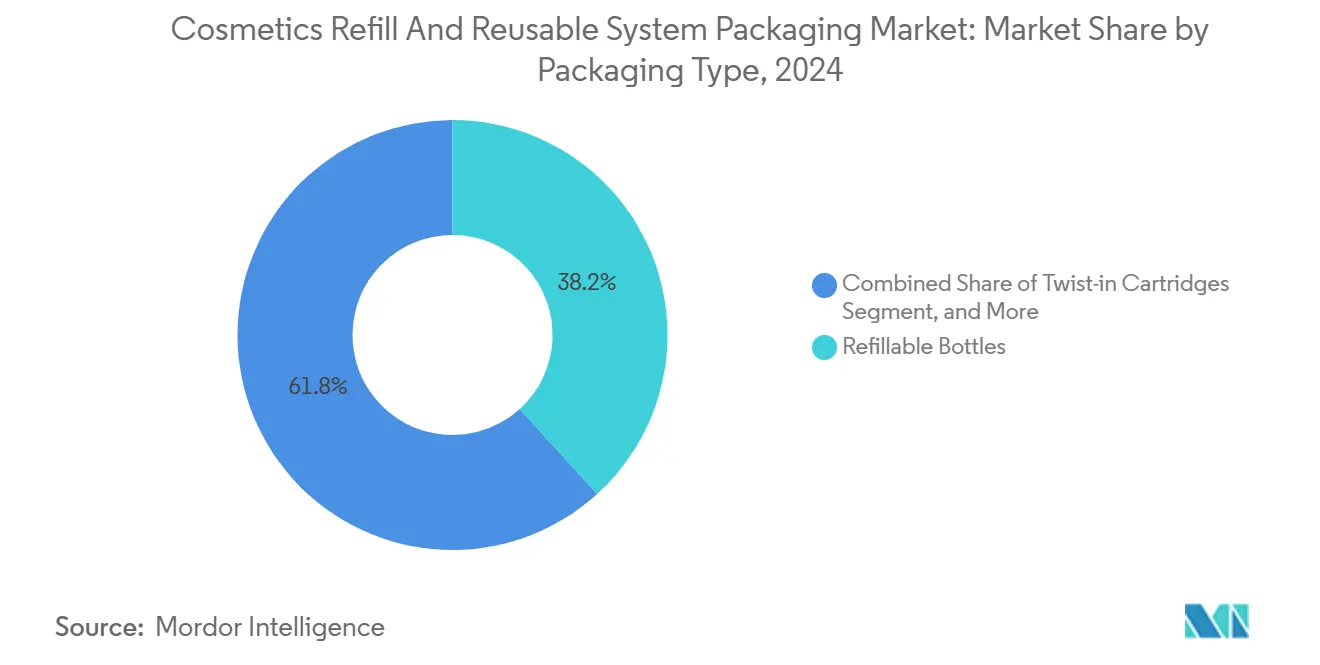

- By packaging type, refillable bottles commanded 38.24% of the cosmetics refill and reusable system packaging market share in 2024.

- By material, the cosmetics refill and reusable system packaging market size for biopolymers is expected to expand at an 8.81% CAGR.

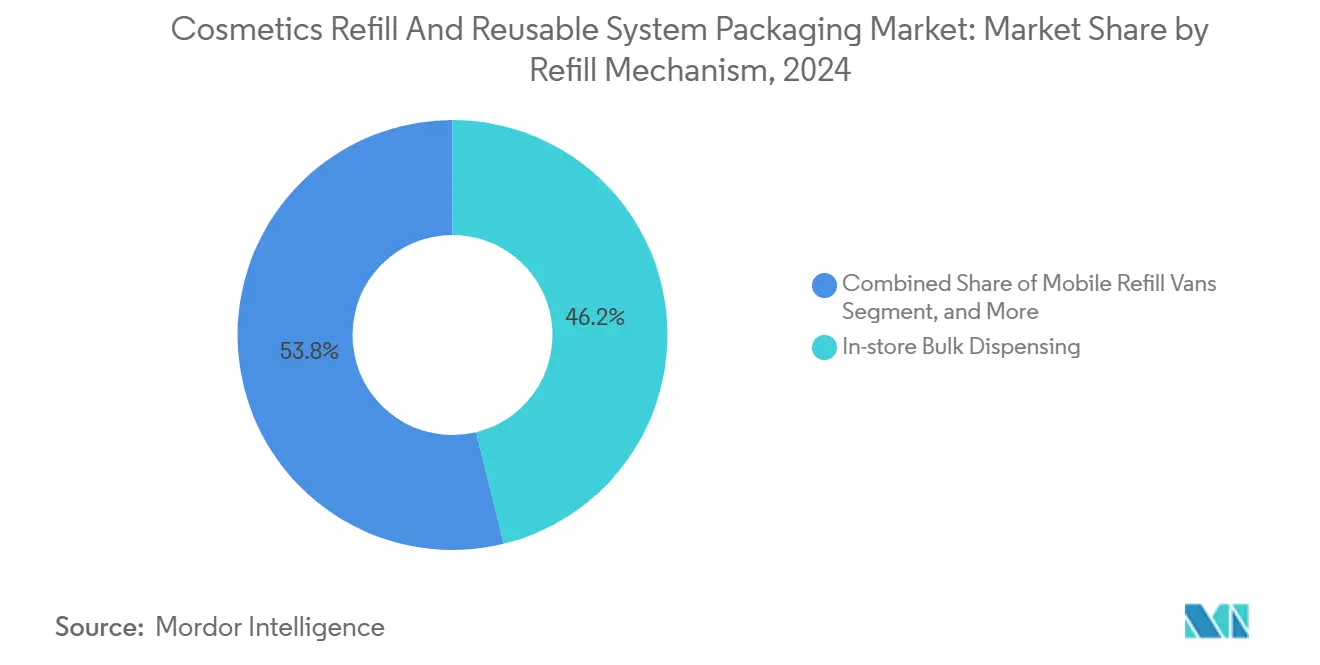

- By refill mechanism, in-store bulk dispensing accounted for 46.19% of the cosmetics refill and reusable system packaging market size in 2024.

- By distribution channel, the cosmetics refill and reusable system packaging market size for direct-to-consumer e-commerce is anticipated to grow at an 8.91% CAGR.

- By geography, Europe held 32.71% of the cosmetics refill and reusable system packaging market share in 2024.

Global Cosmetics Refill And Reusable System Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of loop retail partnerships | +1.2% | North America and Europe | Medium term (2-4 years) |

| Brand commitments to zero-waste targets | +1.1% | Europe and North America | Long term (≥ 4 years) |

| Consumer demand for sustainable luxury | +0.9% | Europe and North America expanding to Asia-Pacific | Medium term (2-4 years) |

| Regulatory bans on single-use plastics | +1.3% | Europe leading, global follow-on | Short term (≤ 2 years) |

| Refill station cost efficiencies | +0.8% | Developed markets then emerging markets | Long term (≥ 4 years) |

| Digital tracking enabling reverse logistics | +0.7% | Technology-advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of Loop Retail Partnerships

The Loop-Ulta Beauty alliance, launched in March 2024, demonstrates how embedding refill services inside mainstream beauty stores removes behavioral friction. Shoppers pick refill-ready versions of premium brands, earn points through existing loyalty programs, and return empties during routine visits, lifting customer lifetime value by 23% compared with disposable formats.[1]Ulta Beauty, “Ulta Beauty Partners with Loop to Expand Sustainable Beauty Options,” ultabeauty.com Retailers benefit from incremental foot traffic, while brands cut landfill fees and logistics costs, underscoring why retail partnerships now rank among the strongest growth catalysts for the cosmetics refill and reusable system packaging market.

Brand Commitments to Zero-Waste Targets

Global beauty majors have moved beyond pilot projects to formal pledges that hardwire reuse into supply chains. Unilever’s 2024 decision to invest USD 50 million in 500 European refill stations aligns with its earlier goal to halve virgin plastic use by 2025. Similar initiatives at L’Oréal introduced refillable lipstick cartridges that cut material use by 75% while preserving luxury aesthetics.[2]L’Oréal, “L’Oréal Launches Refillable Lipstick Program Across Europe,” loreal.com Such mandates ensure a steady order pipeline for dispensing equipment suppliers and incentivize contract manufacturers to redesign molds for modular components, magnifying long-term growth.

Consumer Demand for Sustainable Luxury

Reusable jars and aluminum compacts increasingly signal exclusivity. High-income shoppers value craftsmanship and durability, purchasing limited-edition cases from niche labels like Kjaer Weis that become collectibles. Emotional attachment extends product life and drives refill sales without the need for discounting. As premium beauty shifts from embellishment toward responsible indulgence, willingness to pay surcharges offsets earlier concerns that sustainability would erode margins, further propelling the cosmetics refill and reusable system packaging market.

Regulatory Bans on Single-Use Plastics

Policy remains the most decisive growth engine. The EU Single-Use Plastics Directive obliges producers to finance waste management, effectively penalizing disposable designs. France mandates 20% reusable packaging by 2030, and California sets similar thresholds by 2032, prompting companies to harmonize global portfolios. The cost of non-compliance sharpens board-level focus, making refill systems a financial imperative rather than an ethical choice.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hygiene and contamination concerns | -0.6% | Global, heightened in Asia-Pacific | Short term (≤ 2 years) |

| High upfront dispenser infrastructure cost | -0.8% | Emerging markets and small retailers | Medium term (2-4 years) |

| Limited compatibility across brand formats | -0.5% | Global fragmented retail | Medium term (2-4 years) |

| Complex reverse logistics in emerging markets | -0.4% | Latin America, Africa and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hygiene and Contamination Concerns

Post-pandemic shoppers remain wary of shared surfaces. Acceptance of bulk cosmetic dispensers lags in markets such as Japan, where cultural norms favor sealed units. Beauty Kitchen mitigates the issue with antimicrobial finishes, UV sterilization, and single-use applicators inside its U.K. refill stations.[3]Beauty Kitchen, “Refill Stations Hygiene Standards and Safety Protocols,” beautykitchen.co.uk These engineering upgrades enhance trust, but they also increase unit costs, restraining growth until standardized hygiene protocols are adopted globally.

High Upfront Dispenser Infrastructure Cost

A complete multi-SKU dispensing island can cost USD 25,000-75,000 per store when factoring in installation, staff training, and inventory software. Independent retailers and operators in emerging economies often lack that capital. Algramo’s franchise model shifts the burden to monthly leasing fees, proving especially successful across 200 Latin American sites scaled in 2024. While financing innovations are easing pain points, budget barriers continue to trim near-term adoption curves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Bottles Retain Scale as Cartridges Rapidly Advance

Refillable bottles generated 38.24% of 2024 revenues, maintaining consumer familiarity across cleansers, shampoos, and body washes. Their entrenched production lines and versatile pump or squeeze closures enable brands to retrofit existing SKUs quickly, reinforcing their dominance within the cosmetics refill and reusable system packaging market. Adoption also benefits retailers, as bottle refills integrate seamlessly with current shelf layouts and scanning systems.

Twist-in cartridges, however, post the category-leading 8.21% CAGR through 2030. Precise dosage, mess-free application, and compact shipping volumes align cartridges with premium serums, foundations, and travel assortments. Modular cartridge frames further unlock cross-category merchandising: a single aluminum case can host refills for fragrance, lip color, or sunscreen, broadening consumer lifetime value. Brand storytelling centered on engineered precision and waste reduction continues to propel cartridge momentum, reshaping the competitive playbooks of product design teams.

By Material: Glass Sets the High-End Standard as Biopolymers Surge

Glass captured a 34.52% share in 2024, prized for its intrinsic inertness, infinite recyclability, and luxurious hand feel. The prestige skincare and fine fragrance segments rely on the material to signal efficacy and purity, and European return-deposit schemes make glass circulation economically viable. The cosmetics refill and reusable system packaging market size for glass is projected to increase steadily; however, weight and breakage risks constrain scale beyond upmarket tiers.

Biopolymers, derived from sugarcane or corn starch, outpace all rivals at an 8.81% CAGR. They address microplastic leakage concerns and meet compostability standards, expanding appeal to mass and masstige brands that face tighter packaging taxes. Early mechanical issues, such as brittleness, are being alleviated as resin suppliers refine their formulations. Cost parity with virgin PET is approaching, setting the stage for biopolymer breakthroughs throughout personal care aisles.

By Refill Mechanism: Store Dispensing Commands Today, Mobile Vans Gain Ground

In-store bulk dispensing accounted for 46.19% of global revenue in 2024, relying on staff oversight to reassure first-time users about hygiene and correct fill levels. Specialty retailers and natural product chains leverage refill bars as foot-traffic magnets, turning eco-friendly practices into experiential shopping. Their layouts prominently display avoided-waste metrics, strengthening brand equity within the cosmetics refill and reusable system packaging market.

Mobile refill vans, advancing at 7.61% CAGR, extend service reach to dense urban neighborhoods and corporate campuses. Loop launched pilot fleets in 2024 that let consumers schedule doorstep top-ups using an app-based route planner. The model sidesteps retail build-out costs, provides real-time inventory feedback, and aligns with an on-demand culture. Municipal climate grants and shared-mobility partnerships are expected to widen geographic coverage over the next five years.

By Distribution Channel: Physical Stores Still Rule as Direct-to-Consumer Accelerates

Brick-and-mortar outlets retained a 41.35% revenue edge in 2024 because tactile testing and immediate gratification remain pivotal for cosmetic purchases. Retail assistants demonstrate refill techniques, easing shopper learning curves and driving sales of attachment items like reusable pumps or branded tote bags. Their omnichannel investments, from QR code scanners to digital refill passports, blend online data capture with in-store theater, cementing loyalty in the cosmetics refill and reusable system packaging industry.

Direct-to-consumer e-commerce enjoys the highest 8.91% CAGR, driven by subscription models that automate replenishment and minimize the occurrence of forgotten containers. Brands such as Plaine Products bundle refills with video tutorials and impact dashboards that tally carbon savings, enhancing perceived value. Lower overhead and direct feedback loops enable continuous package tweaks, allowing digital-native challengers to out-innovate traditional incumbents in terms of speed and personalization.

Geography Analysis

Europe maintained its leadership with a 32.71% share in 2024, driven by comprehensive directives such as the ban on single-use plastics and national levies on virgin plastic. Nordic countries, Germany, and France exhibit the highest per-capita purchase of refill SKUs, and retailers, including The Body Shop, have introduced multi-aisle refill hubs across their flagship stores. Government grants for circular economy pilots and consumer loyalty to homegrown sustainable brands reinforce expansion.

The Asia-Pacific region delivers the fastest growth, with an 8.49% CAGR through 2030, reflecting rising disposable incomes and digital sophistication. In China, refill subscription bundles seamlessly integrate into super-app ecosystems, transforming sustainability into a lifestyle signal for Gen Z and millennial shoppers. Japanese retailers adopt compact cartridge kiosks that match cultural preferences for cleanliness and efficiency, while Korean ODM manufacturers scale turnkey refill modules that blend K-beauty aesthetics with rigorous hygiene assurance.

North America exhibits solid mid-single-digit growth, supported by state targets, such as California’s SB 54, and venture funding for circular startups. Major chains are piloting refill islands in high-traffic metropolitan stores; Sephora’s 2024 program integrates UV sterilization and contactless valves to address lingering safety concerns. Canada’s federal plastic pact complements provincial actions, encouraging harmonized label guidelines and return-reward incentives that ease cross-border brand rollouts.

Competitive Landscape

The field remains moderately fragmented, with no single player exceeding a 10% revenue share. Legacy multinationals, such as Unilever and L’Oréal, retrofit hero SKUs for reuse, while specialty platforms, including Loop Global Holdings, Returnity Innovation, and TerraCycle, build dedicated logistics and tracking infrastructure. Competitive differentiation hinges on mastering three variables: consumer convenience, verifiable hygiene, and total delivered cost.

Technology investment has accelerated. Returnity secured a blockchain patent that logs every container cycle, driving 85% return rates and curbing fraud. Equipment suppliers race to file IP on self-cleaning dispensers and modular cartridge docks. Vertical integration strategies emerge: TerraCycle leverages its waste-processing expertise to offer turnkey circular packaging services that span collection through resin regranulation.

White-space opportunities persist in emerging markets where domestic labels can secure early distribution rights and shape consumer norms. Professional salons and spa chains also represent fertile ground; their service-centric model dovetails with closed-loop container programs that ensure controlled reuse cycles and premium upsell potential. As certification schemes like ISO 14001 gain traction, transparent lifecycle accounting will further separate leaders from laggards.

Cosmetics Refill And Reusable System Packaging Industry Leaders

Loop Global Holdings LLC

Algramo SpA

Kjaer Weis Inc.

Izzy Zero Waste Beauty Inc.

TerraCycle US LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TerraCycle introduced an AI-driven refill kiosk that automates container inspection before dispensing, slated for pilot in 30 German drugstores.

- October 2024: Unilever announced a USD 50 million program to install 500 refill stations across European retailers.

- September 2024: Loop Global Holdings raised USD 25 million in Series B funding to expand mobile refill vans in North America.

- August 2024: L’Oréal unveiled aluminum refillable lipstick cartridges across 12 European nations, reducing pack materials 75%.

Global Cosmetics Refill And Reusable System Packaging Market Report Scope

| Refillable Jars |

| Refillable Bottles |

| Reusable Pouches |

| Twist-in Cartridges |

| Other Packaging Types |

| Glass |

| Aluminum |

| Post-consumer Recycled Plastic (PCR) |

| Biopolymers |

| Stainless Steel |

| In-store Bulk Dispensing |

| Return and Refill Subscription |

| Cartridge Replacement |

| Mobile Refill Vans |

| Offline Retail |

| Direct-to-Consumer E-commerce |

| Third-party Marketplaces |

| Professional Salons |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Refillable Jars | ||

| Refillable Bottles | |||

| Reusable Pouches | |||

| Twist-in Cartridges | |||

| Other Packaging Types | |||

| By Material | Glass | ||

| Aluminum | |||

| Post-consumer Recycled Plastic (PCR) | |||

| Biopolymers | |||

| Stainless Steel | |||

| By Refill Mechanism | In-store Bulk Dispensing | ||

| Return and Refill Subscription | |||

| Cartridge Replacement | |||

| Mobile Refill Vans | |||

| By Distribution Channel | Offline Retail | ||

| Direct-to-Consumer E-commerce | |||

| Third-party Marketplaces | |||

| Professional Salons | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the cosmetics refill and reusable system packaging market in 2025?

The market reaches USD 8.44 billion in 2025 and is set to keep expanding at a 6.57% CAGR.

Which region grows the fastest in cosmetics refill and reuse solutions?

Asia-Pacific records the quickest pace, with an expected 8.49% CAGR through 2030.

Which packaging format currently dominates reuse programs?

Refillable bottles hold the top position, capturing 38.24% revenue share in 2024.

What is the biggest obstacle to wider refill adoption for small retailers?

High upfront dispenser investments of USD 25,000-75,000 per location remain the main barrier.

Which company recently committed the most capital to refill infrastructure?

Unilever earmarked USD 50 million in 2024 to deploy 500 refill stations across Europe.

How do mobile refill vans fit into the competitive landscape?

They deliver convenient doorstep service and are projected to grow at 7.61% CAGR, expanding access without heavy retail build-out costs.

Page last updated on: