Consumer Genomics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

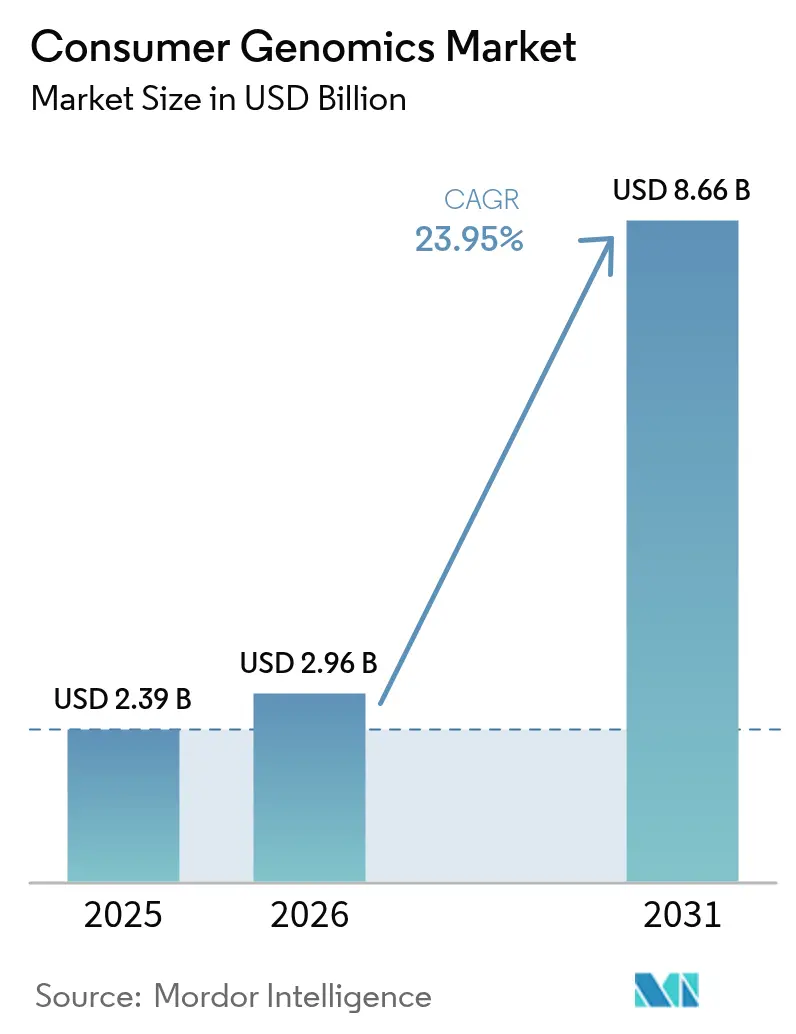

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 8.66 Billion |

| Growth Rate (2026 - 2031) | 23.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

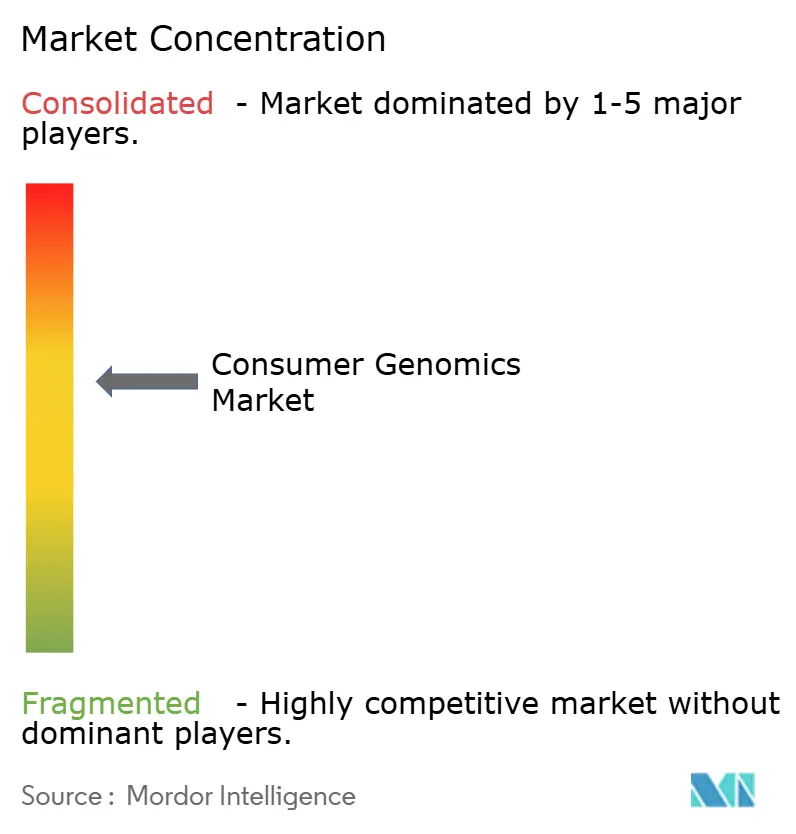

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Genomics Market Analysis by Mordor Intelligence

The consumer genomics market size was valued at USD 2.39 billion in 2025 and estimated to grow from USD 2.96 billion in 2026 to reach USD 8.66 billion by 2031, at a CAGR of 23.95% during the forecast period (2026-2031). A rising share of digitally engaged consumers now bypasses traditional medical routes to secure genomic insights, reflecting broader healthcare digitization trends. Roughly 35 million Americans had already purchased at-home kits by 2021, underscoring a mainstream shift toward proactive health management.[1]Onero Institute, “Genetic Testing and Public Health Behavior,” Onero Institute, oneroinstitute.org Ancestry services currently account for 38.4% of revenues, yet fast-growing health, wellness, and sports nutrition tests are unlocking new avenues for personalized disease prevention. Single-nucleotide polymorphism (SNP) genotyping remains the dominant technology with a 44.6% share, while polygenic risk-scoring analytics is scaling quickly through insurer alliances that link genomic risk to preventive programs. Online channels capture 82.1% of kit shipments, but newly formed insurance partnerships are expanding fastest, aided by regulatory corridors that recognize consumer ownership of health data.

Key Report Takeaways

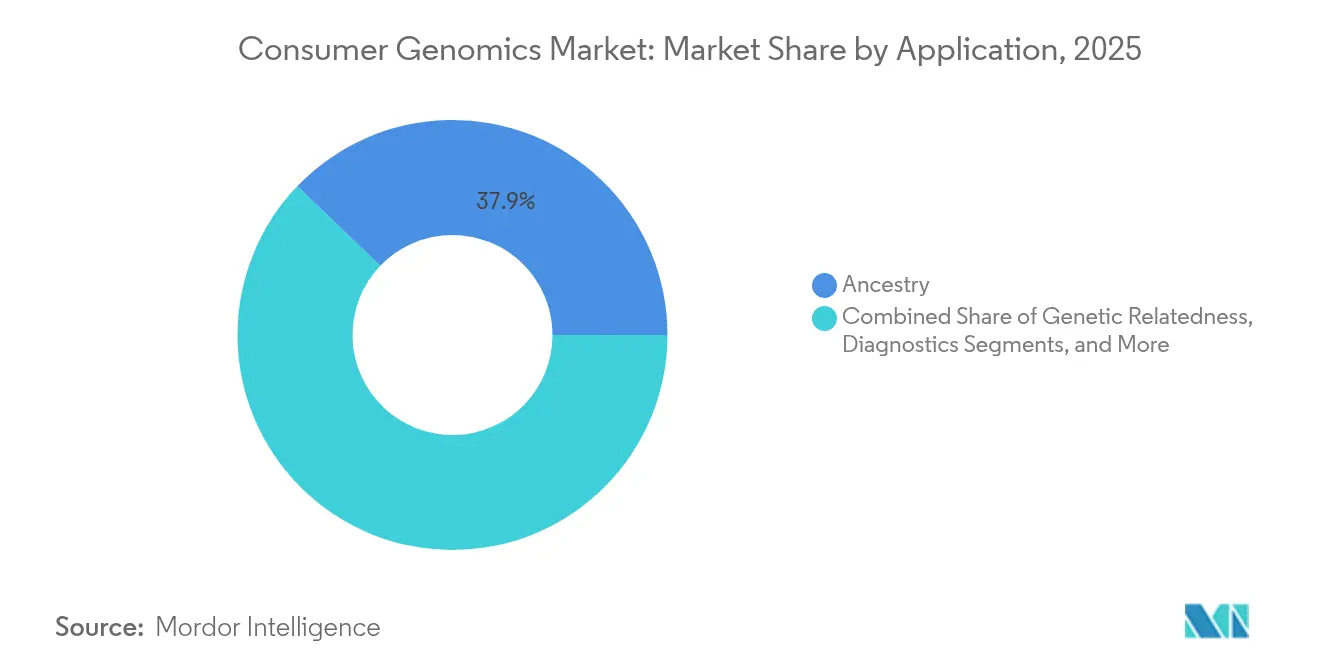

- By application, ancestry maintained 37.85% of the consumer genomics market share in 2025, while sports nutrition and health tests are projected to grow at a 28.1% CAGR through 2031.

- By sample type, Saliva-based collection kits account for the most significant share of consumer genomics sampling, representing 41.55% in 2025. Buccal (cheek) swab collection is expected to post the highest growth rate at 17.9% through 2031.

- By technology, SNP genotyping held 44.12% of the consumer genomics market size in 2025; polygenic risk-scoring analytics is advancing at a 31.1% CAGR to 2031.

- By distribution channel, online direct sales had an 81.35% revenue share in 2025, whereas insurance partnerships are set to expand at a 33.8% CAGR between 2026 and 2031.

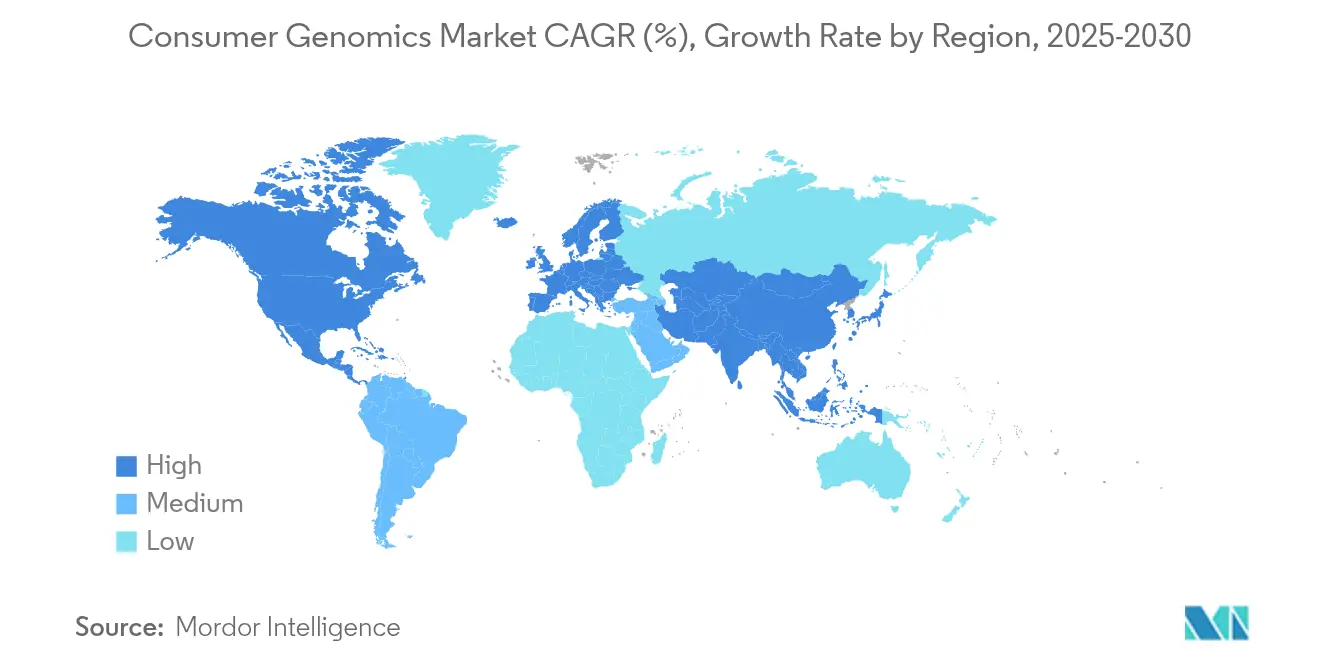

- By geography, North America accounted for 41.12% revenue share in 2025, but Asia-Pacific is forecast to post a 26.3% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Consumer Genomics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer & physician interest in DTC kits | +4.20% | Global, strongest in North America & APAC | Short term (≤ 2 years) |

| Continuous fall in sequencing costs & tech advances | +6.80% | Global, accelerated in developed markets | Medium term (2-4 years) |

| Expansion of supportive DTC regulatory corridors | +3.10% | North America, selective EU markets | Long term (≥ 4 years) |

| Integration of polygenic risk scores within insurance plans | +5.40% | North America, emerging in APAC | Medium term (2-4 years) |

| Retail-pharmacy genomic kiosks & partnerships | +2.70% | North America, pilot programs in Europe | Short term (≤ 2 years) |

| Blockchain-enabled genomic data monetization ecosystems | +1.80% | Global, early adoption in tech-forward markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer & Physician Interest in DTC Kits

More than 33 million tests were performed in 2023, illustrating how genomic literacy now influences everyday health decisions.[2]American Heart Association, “Consumer Genomics and Cardiovascular Risk,” American Heart Association, heart.org Physicians increasingly view home-based results as a conversation starter for preventive care, especially when genetic counseling supports interpretation. Consumer empowerment is evident in demand for combined ancestry, pharmacogenetic, and disease-predisposition offerings that translate data into precise diet, exercise, and medication choices. Clinics complement this trend by integrating secure portals that import DTC files into electronic health records for longitudinal monitoring. The shift confirms a behavioral move from episodic testing toward continuous genomic engagement.

Continuous Fall in Sequencing Costs & Tech Advances

The first human genome cost USD 3 billion. Today, whole genome sequencing services are regularly priced below USD 1,000, shrinking the economic barrier that once limited mainstream adoption. Next-generation sequencers deliver higher accuracy and shorter run times, enabling week-long turnarounds that align with consumer expectations for rapid insights. GeneDx recently paid USD 51 million for Fabric Genomics to integrate AI-based variant interpretation, a deal that highlights market demand for automated analytics at scale. These advances feed directly into richer polygenic scores covering cardiovascular, metabolic, and oncologic conditions.

Expansion Of Supportive DTC Regulatory Corridors

Policy makers increasingly favor consumer access models that balance innovation with safety oversight. The U.S. Senate’s Genomic Data Protection Act, tabled in March 2025, signals bipartisan commitment to stricter privacy norms while endorsing at-home genetic services Thirteen states have already codified DTC guidelines, creating a mosaic of requirements companies must navigate. The FDA’s evolving stance on laboratory-developed tests offers clearer validation pathways without undermining product speed to market. Internationally, selective European Union markets now pilot exemptions for low-risk wellness assays, paving the way for cross-border kit distribution when firms meet GDPR obligations.

Integration Of Polygenic Risk Scores Within Insurance Plans

Insurers are repositioning genetic data as a lever for personalized prevention rather than underwriting exclusion. MassMutual’s collaboration with Genomics plc led 70% of covered policyholders to adopt targeted lifestyle interventions after receiving polygenic insights, validating a behavior-change thesis. UK-based Bupa recently introduced a predictive test for adults over 40-45 years to flag cardiovascular and cancer risks, integrating machine-learning algorithms into routine screenings. Reinsurer SCOR offers genomic cancer panels to life clients, underscoring how risk scores can cut claims cost trajectories through earlier detection. These partnerships collectively deepen the consumer genomics market by shifting payment responsibility from individuals to benefit managers.

Restraints Impact Analysis of Consumer Genomics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cybersecurity breaches | –3.9% | Global, heightened in EU under GDPR | Short term (≤ 2 years) |

| Patchy, evolving multi-country regulations | –2.6% | Europe primary, emerging in APAC | Medium term (2-4 years) |

| Insolvency-driven liquidation of genetic databases | –1.8% | Global, concentrated in venture-backed startups | Short term (≤ 2 years) |

| AI-driven bias from over-indexed ethnicity datasets | –1.4% | Global, particularly affecting non-European populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Cybersecurity Breaches

The 2023 breach that exposed 7 million 23andMe profiles demonstrated how quickly trust can erode when genomic vaults are compromised. The U.S. Federal Trade Commission has since tightened oversight, fining firms that misrepresent security practices or fail to purge raw DNA files when customers withdraw consent. Public anxiety remains acute around genetic discrimination in insurance, despite protections such as the Genetic Information Nondiscrimination Act. Industry leaders now anchor marketing around bank-grade encryption, zero-knowledge proof architectures, and regular third-party audits to reassure skeptical buyers.

Patchy, Evolving Multi-Country Regulations

Europe embodies the most fragmented playing field. France bans most direct sales, Germany mandates physician mediation, while the UK permits self-ordering provided counseling options are available.[3European Journal of Human Genetics, “Regulating Direct-to-Consumer Tests,” EJHG, ejhg.org] Compliance teams juggle local consent forms, sample shipping restrictions, and data localization laws that inflate operating costs. Startups must often choose between targeted market entry or expensive multi-region compliance frameworks, slowing the pace at which the consumer genomics market scales globally.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Consumer Genomics Market Segment Analysis

By Application:

Ancestry Dominance Yields to Health-Focused InnovationAncestry services commanded 37.85% of 2025 revenue, illustrating their early mover appeal among first-time kit buyers. Growing penetration of health, nutrition, and sports performance assays is reshaping the consumer genomics market size for premium products that integrate dietary guidance, sleep coaching, and personalized supplements. Sports nutrition tests alone are charting a 28.1% CAGR through 2031 as elite and amateur athletes seek genotype-matched macronutrient ratios. Diagnostic panels for monogenic disorders also gain ground by pairing carrier screening with actionable reproductive counseling. Consumers increasingly prefer bundled offerings that fold ancestry, traits, and wellness into one subscription, suggesting a gradual fade of single-purpose genealogy kits. Stakeholders that position tests within broader digital health ecosystems, including mobile coaching apps, strengthen customer lifetime value as they evolve from one-off sales to recurring insights.

Second-generation platforms now embed pharmacogenomic modules that translate metabolizer status into practical medication adjustments covering anticoagulants, antidepressants, and statins. Clinics report reduced adverse drug events when such data appears in electronic health records ahead of prescribing decisions. Regulatory clarity around wellness versus diagnostic claims continues to influence feature design, yet early evidence indicates multi-category kits secure higher average selling prices without prolonging turnaround times.

By Technology:

SNP Genotyping Leadership Challenged by Advanced AnalyticsSNP genotyping underpins 44.12% of 2025 kit volumes, favored for cost efficiency and a decade-long legacy of accuracy. Even so, insurance-backed programs are accelerating the shift toward polygenic risk-scoring engines that integrate hundreds of thousands of variants to deliver continuous risk curves for complex diseases. This subsegment is expected to expand at a 31.1% CAGR, outpacing any other technology stack inside the consumer genomics market. Whole-genome sequencing enjoys a price inflection point below USD 1,000, prompting Bupa to pilot genomic wellness packages for select enrollees seeking comprehensive coverage across 300 genes. Microarrays remain relevant for ancestry work because historical reference libraries map seamlessly to their variant selection, whereas targeted sequencing panels carve niches in cardiovascular or oncology-focused kits where depth of coverage matters.

Cloud pipelines have matured to the point where raw read alignment, variant calling, and annotation complete in hours rather than days, giving vendors the agility to promise single-digit-day delivery windows. The maturation of containerized bioinformatics also enables smaller upstarts to rent capacity from hyperscaler marketplaces without building expensive on-premise infrastructure, democratizing entrance into data-rich segments.

By Sample Type:

Saliva Convenience Drives Consumer PreferenceSaliva-based collection kits account for the most significant share of consumer genomics sampling, representing 41.55% in 2025. As per the survey, saliva tubes dominate market adoption with 72% response rates, offering users a painless, mail-friendly workflow that fits the direct-to-consumer brand promise. Buccal swabs post the industry’s highest 80% response rates among pediatric and geriatric demographics who struggle with saliva generation, positioning swabs as a strategic expansion channel for family-oriented kits. Blood spot cards, though invasive, retain traction in newborn and rare-disease contexts where depth of coverage or biomarker co-testing enhances diagnostic value. Suppliers develop novel stabilization buffers that protect nucleic acids at ambient temperatures for up to 28 days, extending geographic reach into tropical regions without refrigeration. The next innovation wave targets micro-collection devices integrating barcodes and time-stamped tamper seals to mitigate sample mix-up and bolster chain-of-custody records.

By Distribution Channel:

Online DTC Dominance with Emerging Partnership ModelsPure-play e-commerce captured 81.35% of 2025 kit shipments, validating the convenience of doorstep delivery and user-initiated sample return. The channel’s conversion funnel benefits from influencer marketing, referral discounts, and bundled ancestry-plus-health packages. Still, insurance partnerships register the fastest growth at 33.8% CAGR as carriers co-finance kits to drive preventive interventions that can trim claim outlays within three years. Corporate wellness portals represent a third pillar, with employers such as SAP uncovering actionable variants in hundreds of staff members and integrating findings into company-sponsored coaching programs. Pharmacies advance omnichannel reach by stocking select kits on shelf and by offering phlebotomy services when deeper sequencing is ordered, signaling a hybrid model where brick-and-mortar enhances accessibility for populations uncomfortable with online payments.

Geography Analysis

North America Consumer Genomics Market

North America retained 41.12% revenue in 2025 due to high consumer awareness, mature digital payment infrastructure, and clinician familiarity with genomic decision-support tools. The consumer genomics market size in the region will keep expanding as state-by-state legislative clarity tempers earlier litigation risks surrounding privacy and data ownership. Leading universities frequently partner with kit vendors to crowd-source research cohorts, offering free or discounted tests that funnel additional volume into reference databases.

APAC Consumer Genomics Market

Asia-Pacific, advancing at a 26.3% CAGR, stands out as the prime expansion frontier. Rising disposable incomes in China, India, and Southeast Asia intersect with escalating lifestyle diseases, making preventive genomic risk assessment an attractive household expenditure. Local governments are investing in national genome projects that stimulate consumer curiosity while suppliers localize content in Mandarin, Hindi, and Bahasa to overcome linguistic hurdles. At-home saliva collection bypasses hospital queues in megacities, a convenience valued by middle-class families balancing busy schedules.

Broader European Markets

Europe presents a dichotomy of progressive data rights and heterogeneous testing rules. The General Data Protection Regulation forces explicit consent practices, multi-factor authentication, and encrypted transfer, elevating compliance costs but building consumer confidence. Countries like the Netherlands and the UK permit direct ordering, yet France insists on medical oversight. Vendors deploy modular platforms that activate or deactivate features to fit local laws, indicating a tailored rather than blanket expansion strategy. Consumers show a growing appetite for health-oriented packages, especially those integrating cardiovascular and metabolic traits that align with regional public-health priorities.

Regulatory Landscape

Consumer genomics sits across medical-device oversight, consumer-protection enforcement, and data-privacy law, and requirements change materially by geography, including whether a kit is positioned with health or diagnostic claims. In the United States, the FDA framework for direct-to-consumer tests focuses on products that present medical claims (for example, genetic health risk and carrier screening), while the Federal Trade Commission (FTC) oversees deceptive marketing and privacy-related practices; the 2023 breach involving approximately 7 million 23andMe profiles has kept scrutiny high. A notable U.S. regulatory anchor is the September 2024 Federal Register action that classified whole exome sequencing as a Class II device with special controls under 21 CFR 866.6000, reinforcing expectations around validation and controls for higher-complexity genomic offerings.

In Europe, the In Vitro Diagnostic Regulation (IVDR, Regulation (EU) 2017/746) uses a risk-based approach and, for most consumer genetic tests, pushes companies away from self-certification and toward Notified Body conformity assessment backed by clinical performance evidence. This raises the compliance bar for cross-border kit distribution under GDPR constraints. Standards are also tightening at the analytics layer: PD ISO/TS 20738:2026, published in March 2026, sets requirements for data analysis in direct-to-consumer genomics, signaling more explicit expectations for bioinformatics pipeline governance (including version control and reference dataset justification) as automated interpretation becomes more common.

Competitive Landscape

The consumer genomics market currently displays moderate concentration. Regeneron’s USD 256 million acquisition of 23andMe brought one of the sector’s largest datasets under pharmaceutical stewardship, raising debate on vertical integration between test providers and drug developers. AncestryDNA continues to harness its 25 million-sample biobank to enhance ethnicity breakouts, while MyHeritage leverages European regulatory familiarity to consolidate niche genealogy segments. GeneDx’s purchase of Fabric Genomics underscores a pivot toward AI-first interpretation engines that can scan millions of variant-phenotype links in seconds.

Tempus strengthened oncology coverage with Ambry Genetics, adding germline capabilities to its somatic cancer portfolio. Labcorp absorbed select Invitae assets to reinforce clinical workflows that blend diagnostic confirmation and patient counseling at scale. On the blockchain side, Nebula Genomics and GenoBank.io market data-share royalties as a differentiator, aiming to lure privacy-conscious users away from centralized warehouses. White-space opportunities persist in under-represented ethnic groups, with startups forming community governance boards to guide data sharing and benefit distribution.

Regulated laboratories are also courting the consumer genomics industry by offering hybrid services where consumers self-order basic panels online and receive physician follow-up if medically significant variants emerge. This model mitigates the compliance risk of purely unmediated reporting while preserving user autonomy.

Consumer Genomics Industry Leaders

23andMe, Inc.

Ancestry

Positive Biosciences, Ltd.

Futura Genetics

Helix OpCo LLC

- *Disclaimer: Major Players sorted in no particular order

Consumer Genomics Market Companies Covered in this Report

- 23andMe

- AncestryDNA

- MyHeritage

- Helix

- Illumina

- Color Genomics

- Veritas Genetics

- Nebula Genomics

- Futura Genetics

- Gene by Gene

- Pathway genomics

- Xcode Life

- Toolbox Genomics

- CircleDNA

- Dante Labs

- LifeDNA

- Living DNA

- Invitae

Market Opportunities and Future Outlook

One commercialization opportunity is expanding consumer genomics from one-off DTC reports into preventive-care workflows that connect genomic risk with longitudinal clinical data and payer-sponsored interventions. In March 2026, Illumina and Veritas Genetics (Powered by Fuze Health) formed a strategic consortium to integrate whole-genome sequencing into proactive healthcare and insurance plans, indicating continued effort to operationalize WGS alongside standardized analysis pipelines in benefit design rather than selling kits only through online channels.

The market also has whitespace around trust, privacy engineering, and data stewardship models as consumer and regulator attention converges on breach risk and secondary data use. In July 2026, a multistate settlement tied to 23andMe bankruptcy claims added governance and security requirements, including an advisory board and adherence to comprehensive privacy laws for the 23andMe Research Institute, which lifts the baseline for consent, deletion, and security practices vendors can use to differentiate. On the investment side, funding is also targeting AI-enabled health platforms adjacent to consumer genomics, illustrated by Prenetics securing USD 1 billion in growth financing for its IM8 platform in July 2026; this capital supports broader clinical evidence generation, product diversification, and integration partnerships that translate genomics into recurring, programmatic use cases, including insurer-linked preventive programs.

Recent Industry Developments in Consumer Genomics Market

- May 2026: 23andMe announced a partnership with HealthEx to connect personal genetic data with medical records as part of building pathways toward personalized medicine. The linkage of consumer-generated genomic results with EHR data supports a hybrid model where insights can be used alongside clinical history, aligning with the market shift toward longitudinal, actionable reporting.

- March 2025: 23andMe launched a new genetic report covering MTHFR variants related to homocysteine levels and paired it with an optional clinical lab test. The portfolio expansion broadened its health-reporting options while reinforcing a tighter bridge between consumer education and confirmatory clinical testing when biomarker context is needed.

- November 2024: 23andMe entered a strategic research collaboration with Mirador Therapeutics to use aggregated genetic data in precision medicine research. Such collaborations highlight the value of scaled consumer datasets as a research asset, while also increasing the emphasis on transparent consent and data-governance practices.

Consumer Genomics Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the consumer genomics market is defined as revenues earned from direct-to-consumer genetic testing services where individuals buy a kit, provide a sample, and receive DNA-based results for ancestry and personal health and wellness insights.

Scope exclusions: Clinical physician-ordered genetic tests, tests conducted in clinical care settings, forensic DNA work for law enforcement, and enterprise bulk sequencing contracts are excluded.

Segments Covered in This Report

- By Application

- Genetic Relatedness

- Diagnostics

- Lifestyle, Wellness & Nutrition

- Ancestry

- Personalized Medicine & Pharmacogenetics

- Sports Nutrition & Health

- Recreational Traits

- Other Application Types

- By Technology

- Microarray Genotyping

- SNP Genotyping

- Targeted Sequencing Panels

- Whole Exome Sequencing (WES)

- Whole Genome Sequencing (WGS)

- Polygenic Risk Scoring Analytics

- Other Technologies

- By Sample Type

- Saliva

- Buccal Swab

- Blood Spot

- Other Samples

- By Distribution Channel

- Direct-to-Consumer

- Physician-mediated & Clinics

- Pharmacies & Retail

- Health & Wellness Partnerships

- Insurance Partnerships

- Corporate Wellness Programs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped set the guardrails for what counts as consumer-focused testing. It also provided base indicators that we carried into the model. We referenced public health and science sources such as the US FDA, the US National Institutes of Health, the World Health Organization, and OECD health statistics to understand test oversight and regional adoption context. For test reporting practices and the types of results that typically get included in consumer offerings, we also used reputable scientific literature, including peer-reviewed journals in genetics and public health.

On the commercial side, we reviewed company filings, investor presentations, and product disclosures to map typical revenue streams, pricing practices, and channel patterns. We then checked those mappings against widely read press coverage and genetics and laboratory quality association websites. Where a paid subscription was available, it was used only for company financials and news context, and a patent database was used to cross-check which testing technologies companies were emphasizing over time. The sources listed are illustrative only, since we also used additional public references to collect inputs, cross-check figures, and clarify edge cases.

Primary Interviews and Surveys

Primary work centered on interviews and surveys with DTC testing service teams, lab operations leaders, channel partners, and downstream stakeholders who track consumer uptake, pricing moves, and repeat purchase behavior. We also spoke with subject experts across major regions to tighten assumptions on test volumes, average selling prices, and the split in reporting between ancestry and health and wellness when desk signals were incomplete or inconsistent.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 16% | APAC: 46% |

| Mid tier: 58% | Functional/Unit leaders: 28% | EMEA: 35% |

| Smaller Players: 16% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach where consumer testing revenues are reconstructed from adoption signals, average pricing levels, and the share of results delivered through direct-to-consumer channels. The model uses region level build-ups based on variables such as estimated test kit volumes shipped or processed, the split between ancestry and health and wellness focused reports, the mix of genotyping versus sequencing oriented offerings, and average selling price ranges by channel (online-only versus clinic-mediated consumer services where applicable). These inputs were then adjusted for refund rates, repeat testing behavior, and the share of revenue coming from value-added digital reporting, which can be meaningful in this market.

To keep totals realistic, we corroborated outputs with selective bottom-up approximations. These included supplier and lab capacity sense-checks, and sampled price times volume checks using publicly visible product and service structures. Where company disclosures were not detailed, gaps were handled by using conservative revenue bands and triangulating them with interview feedback, rather than forcing a full roll-up. Forecasts were developed using scenario analysis supported by simple time series smoothing on the key variables, and the final trajectory was aligned to expert views on adoption pace, pricing pressure, and regulatory attention.

Data Validation & Update Cycle

Validation was done through multiple passes of variance checks so that outliers in any one region or year did not drive the full market. Analysts compared model outputs against independent signals such as reported testing activity trends, consumer adoption indicators, and observable pricing moves, and then reviewed any large deviations before sign-off.

If a mismatch persisted, we revisited the key assumption and, when needed, respondents were re-contacted to confirm what changed in the market. The report is refreshed annually, and interim updates are triggered when there are material events that can shift volumes, pricing, or channel access. Before delivery, a final review pass is completed so clients receive the most current view available.

Mordor Intelligence's Consumer Genomics Market Growth Trends and Forecast Market Size Compared Against Other Published Estimates

Published market values for consumer genomics often vary because the scope lines are drawn differently and because each publisher makes separate calls on what revenue streams count as part of consumer testing. The year used as a starting point, the way currency conversion is timed, and how quickly pricing is assumed to decline can also move the final number.

The biggest gaps usually come from whether physician-ordered clinical testing is blended into the total, and whether instruments and other lab infrastructure sales are treated as part of the market even when the end customer is not a consumer. Some estimates also treat data licensing and research access revenue as a core part of the market, while others keep the focus on kit sales, lab processing, and consumer-facing reporting only, which is the approach used here and applied consistently by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.96 B (2026) | |

| Trade Journal A | USD 4.17 B (2025) | Uses an earlier base year and a broader revenue scope that can include more product categories and service lines beyond direct consumer kit plus lab processing economics, which inflates the near-term total. |

| Global Consultancy B | USD 2.85 B (2024) | Anchors on a different base year and applies a wider product lens (for example, instruments and consumables) that can pull in lab-side revenues not always tied to direct consumer testing volumes. |

The table shows that most of the spread is explained by scope and base-year choices, not by a disagreement that demand is rising. By keeping the counted revenues tied to identifiable consumer purchase and processing flows, and then cross-checking them with adoption and pricing signals, the final number stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the consumer genomics market in 2031?

The consumer genomics market is estimated to reach USD 8.66 billion by 2031, expanding at 23.95% CAGR during the forecast period (2026-2031).

Which application segment is growing the fastest?

Sports nutrition and health-focused tests are registering the highest momentum, with a projected 28.1% CAGR through 2031.

How are insurers influencing market growth?

Insurance partnerships now grow at a 33.8% CAGR as carriers subsidize kits to encourage preventive health actions, boosting long-term adoption.

Why is polygenic risk scoring gaining traction?

Polygenic analytics integrate millions of genomic variants to produce nuanced disease predictions, helping physicians and insurers tailor early interventions.

What role do blockchain platforms play in consumer genomics?

Blockchain solutions let users monetize their anonymized DNA files by selling limited research access, reinforcing data ownership while creating new revenue streams.

Which region presents the largest near-term growth opportunity?

Asia-Pacific leads in growth potential, with a 26.3% CAGR driven by rising incomes, urbanization, and increased lifestyle disease prevalence.

Page last updated on: