Global Transcriptomics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

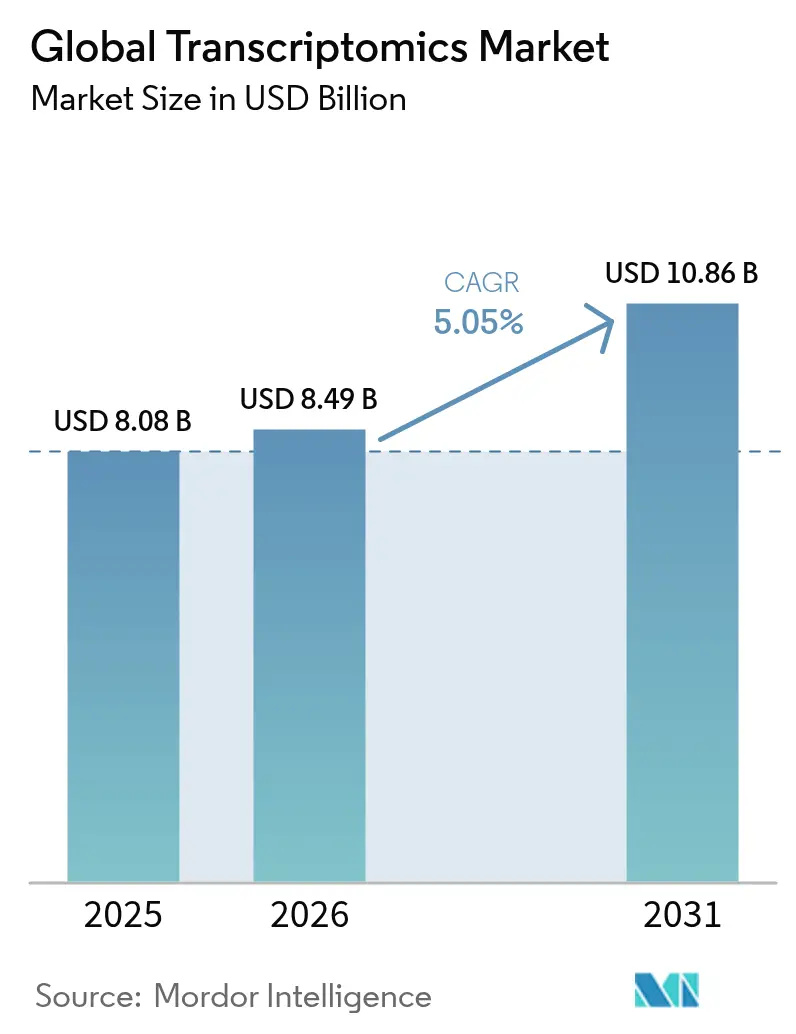

| Market Size (2026) | USD 8.49 Billion |

| Market Size (2031) | USD 10.86 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

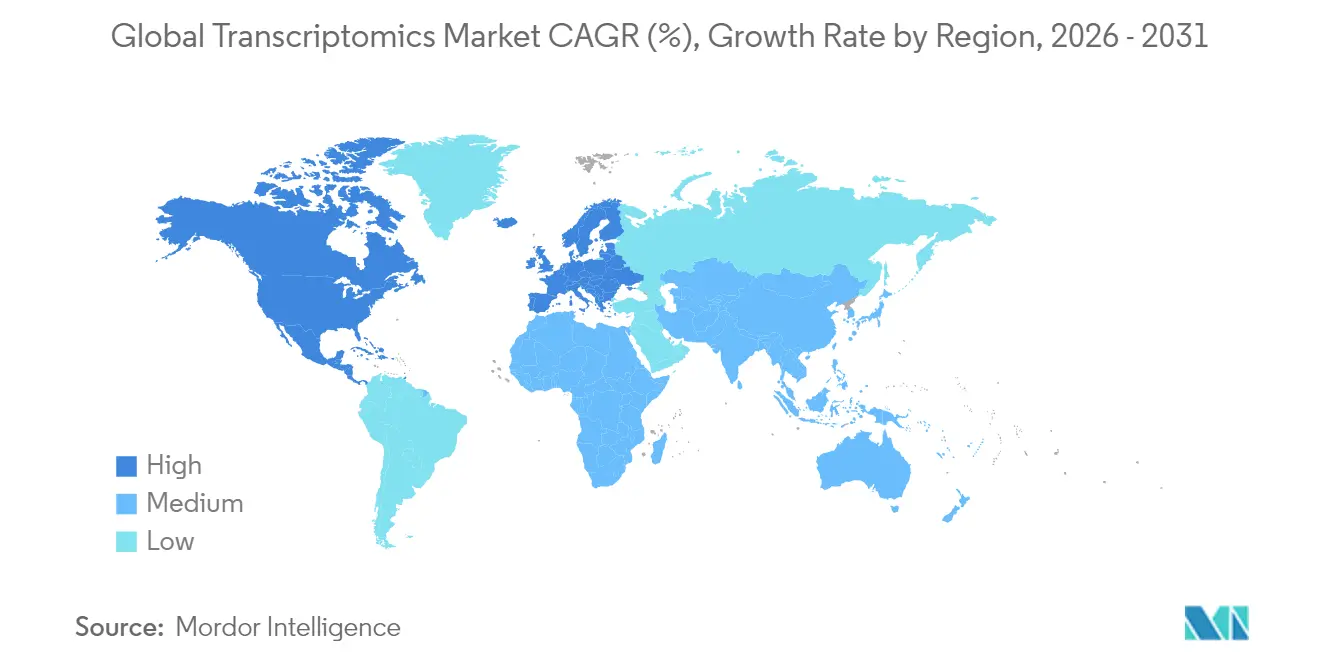

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Transcriptomics Market Analysis by Mordor Intelligence

The transcriptomics market size is expected to grow from USD 8.08 billion in 2025 to USD 8.49 billion in 2026 and is forecast to reach USD 10.86 billion by 2031 at 5.05% CAGR over 2026-2031. Near-term growth stems from rising clinical demand for gene-expression profiling across oncology, immunology, and rare-disease applications, while longer-term expansion will be driven by artificial-intelligence (AI) integration, spatial sequencing advances, and broad reimbursement adoption. Single-cell RNA sequencing (scRNA-seq) underpins almost half of current revenues, yet spatial transcriptomics is outpacing all other technologies as laboratories seek tissue-architecture context. North America’s mature reimbursement pathways sustain its leadership, whereas Asia-Pacific benefits from state-backed genomics initiatives and lower clinical-trial costs. Strategic acquisitions that bundle transcriptomics with proteomics and metabolomics signal a market pivot toward end-to-end precision-medicine solutions rather than stand-alone expression platforms.

Key Report Takeaways

- By technology, single-cell RNA sequencing captured 46.78% of transcriptomics market share in 2025, while spatial transcriptomics is forecast to expand at a 6.32% CAGR through 2031.

- By product, consumables and reagents accounted for 53.74% of the transcriptomics market size in 2025; instruments are advancing at a 6.55% CAGR.

- By application, drug discovery held 41.02% revenue share in 2025, whereas biomarker identification is set to grow at 6.89% CAGR to 2031.

- By end user, academic and research institutes commanded 43.32% share of the transcriptomics market size in 2025, while pharmaceutical-biotechnology companies post the fastest 6.82% CAGR.

- By geography, North America led with 44.96% transcriptomics market share in 2025; Asia-Pacific is projected to grow at 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transcriptomics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption Of RNA-Seq Platforms | +1.2% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Expansion Of Transcriptomics-Based Drug Discovery | +1.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Cloud-Native AI Pipelines Are Democratizing Large-Scale Transcriptomic Data Analysis | +1.0% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Rising Chronic Disease Burden & Precision Diagnostics Demand | +1.5% | Global, with highest impact in aging populations | Long term (≥ 4 years) |

| Emergence Of Spatial & Single-Cell Transcriptomics | +0.9% | North America, EU, Japan, South Korea | Medium term (2-4 years) |

| Agri-Genomics Programs In Food-Insecure Regions | +0.4% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption Of RNA-Seq Platforms

Clinical laboratories increasingly integrate RNA-sequencing workflows following 2024 FDA approvals of assays such as TruSight Oncology Comprehensive, creating reimbursement certainty and accelerating platform uptake [1]U.S. Food & Drug Administration, “TruSight Oncology Comprehensive Approval,” fda.gov. Long-read technologies from Oxford Nanopore and Pacific Biosciences have solved splice-variant detection, reporting median 98.8% read accuracy for direct RNA sequencing. Clinical sequencing revenues exceeded research use for the first time in 2023, pushing manufacturers to emphasize automation and interpretation software rather than throughput. The shift raises quality-control expectations but simultaneously unlocks premium pricing, reinforcing a recurring consumables model that underpins sustained transcriptomics market growth.

Expansion Of Transcriptomics-Based Drug Discovery

Pharmaceutical companies deploy multi-omics AI to mine scRNA-seq data for drug targets, cutting development timelines; Recursion Pharmaceuticals’ approach exemplifies this trend. Spatial transcriptomics adds micro-environment context critical for oncology research, and FDA guidance from its 2024 Omics Days conference clarified biomarker-validation pathways, spurring investment. Resulting translational studies move expression biomarkers from discovery to pivotal trials faster, lifting demand for high-throughput sequencing reagents.

Rising Chronic Disease Burden & Precision Diagnostics Demand

Liquid-biopsy platforms now combine circulating tumor RNA with DNA mutation panels for real-time disease monitoring; Foundation Medicine’s Liquid CDx secured expanded approval in 2024. COVID-19’s molecular-testing infrastructure remains in place, easing hospital adoption of transcriptomic assays across oncology and cardiology. Point-of-care nanopore devices deliver gene-expression results in remote settings, helping health systems manage chronic conditions proactively and lowering downstream treatment costs.

Emergence Of Spatial & Single-Cell Transcriptomics

Spatial methods moved from research to clinical validation as Illumina introduced a high-density platform in 2025 that profiles millions of cells per slide. AI-driven pattern recognition maps cellular interaction networks, revealing disease pathways unseen in bulk analysis. Falling per-cell costs democratize access for smaller centers, deepening the user base and reinforcing the consumables revenue stream vital to the transcriptomics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Platform & Consumable Costs | -1.1% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Bioinformatics Skill Gap & Data-Handling Complexity | -0.8% | Global, particularly acute in APAC and Latin America | Medium term (2-4 years) |

| Stringent Data-Privacy / Clinical-Validation Regulations | -0.6% | EU, North America, with spillover to global markets | Medium term (2-4 years) |

| Supply Bottlenecks For Single-Cell Reagents | -0.4% | Global, with manufacturing concentrated in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Platform & Consumable Costs

A scRNA-seq run ranges from USD 3,170 to USD 25,540, straining research grants and discouraging small clinical labs. Consumables outpace instrument costs over a platform’s life, yet limited supplier competition slows price declines. Emerging entrants Element Biosciences and Ultima Genomics promise lower-cost chemistries, but widespread adoption remains two years away. Leasing and service models help offset capital expenditure, though they raise lifecycle costs and reduce workflow flexibility.

Bioinformatics Skill Gap & Data-Handling Complexity

Multi-layer expression datasets demand expertise spanning biology, statistics, and computer science, skills scarce outside top centers [2]National Center for Biotechnology Information, “Single-Cell Transcriptomics Databases,” ncbi.nlm.nih.gov . Automated cloud pipelines lower entry barriers, yet many clinicians distrust opaque algorithms for diagnostic decisions. Universities struggle to update curricula to pace evolving methods, inflating salaries and giving large urban centers a talent monopoly that slows broader transcriptomics market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Single-Cell Dominance Faces Spatial Challenge

Single-cell RNA sequencing held 46.78% transcriptomics market share in 2025, underscoring its role in resolving cellular heterogeneity that bulk methods overlook . The segment’s maturity redirects innovation toward workflow throughput and cost reduction, while spatial platforms record a 6.32% CAGR as laboratories seek tissue-structure context.

The transcriptomics market continues to tilt toward multimodal solutions that merge scRNA-seq with spatial barcoding, enhancing insight without sacrificing resolution. Long-read chemistries capture complex isoforms, broadening oncologic and neurologic study scope. Although microarrays fade, quantitative PCR maintains a foothold for rapid, low-plex assays. Vendors therefore balance portfolios between high-content discovery tools and targeted clinical panels to secure diverse revenue streams.

By Product: Consumables Revenue Model Drives Recurring Growth

Consumables generated 53.74% of the transcriptomics market size in 2025, emphasizing the power of a razor-razorblade model that assures recurrent cash flow. Instrument sales slowed as core features converged across vendors, yielding only 6.55% growth.

Software and analytical-service revenues accelerate as data complexity grows, allowing specialized providers to capture value beyond wet-lab reagents. Cloud-native pipelines democratize advanced bioinformatics, yet premium prices for clinical-grade kits keep margins high. As the installed instrument base saturates top research centers, consumable vendors pivot to emerging markets and mid-tier hospitals, tailoring kit sizes and price points to local budgets.

By Application: Drug Discovery Leadership Yields to Diagnostics Growth

Drug discovery commanded 41.02% revenue in 2025, but biomarker identification’s 6.89% CAGR through 2031 signals a shift toward diagnostic deployment. Early-stage RNA signatures now guide patient-selection criteria, lowering trial failure rates.

High regulatory clarity encourages commercial labs to launch expression panels for minimal residual disease and immune-checkpoint response. Agriculture-focused transcriptomics gains momentum through CRISPR-enabled crop improvement projects led by USDA, diversifying the transcriptomics market beyond biomedical confines. Environmental monitoring and forensics emerge as niche uses that extend the technology’s reach.

By End User: Academic Institutions Lead Despite Pharma Acceleration

Academic and research institutes held 43.32% of the transcriptomics market size in 2025, reflecting sustained public-grant funding. Growth, however, moderates as budgets plateau, while pharmaceutical-biotechnology firms post a 6.82% CAGR by linking transcriptomics to pipeline productivity.

Clinical laboratories expand rapidly once reimbursement pathways stabilize, reshaping test-volume distribution toward patient-centric assays. Contract research organizations offer turnkey sequencing and analysis, enabling smaller biotechs to compete without capital-intensive infrastructure. Government agencies also scale transcriptomic surveillance for public-health monitoring, broadening the end-user base.

Geography Analysis

North America accounted for 44.96% transcriptomics market share in 2025, anchored by abundant venture capital, dense biopharma clusters, and FDA companion-diagnostic pathways that encourage clinical validation. Public–private partnerships such as the Cancer Moonshot sustain large-scale expression-atlas projects, keeping domestic consumables demand high. Canada leverages a single-payer system to run population-level gene-expression studies, while Mexico lures contract-manufacturing investment through lower costs and rising clinical-trial activity.

Asia-Pacific posts a 7.05% CAGR, propelled by China’s multi-billion-dollar precision-medicine grants and Japan’s early adoption of spatial-omic diagnostics. India’s contract-research ecosystem couples vast patient pools with cost-efficient trials that increasingly include transcriptomic endpoints. Australia’s government-funded Genomics Australia program encourages translational-omics collaborations, funneling academic breakthroughs into commercial assays. Diverse regulatory regimes remain both opportunity and obstacle, with some markets offering accelerated approvals and others demanding prolonged local validation.

Europe maintains strong basic-research output through projects like Genome of Europe, yet stringent General Data Protection Regulation (GDPR) rules lengthen time-to-clinic for novel diagnostics. Germany, the United Kingdom, and France dominate test volumes, supported by established reimbursement codes. Smaller nations such as Switzerland and the Netherlands specialize in high-content single-cell analytics and platform integration consulting. Post-Brexit collaboration frameworks ensure continued data exchange, preserving the region’s cohesive R&D landscape.

Regulatory Landscape

Regulation of transcriptomics spans clinical diagnostic oversight, nonclinical submission standards, and growing multi-omics quality expectations. In the United States, the FDA maintains device oversight for gene-expression profiling tests through Class II Special Controls guidance for breast cancer prognosis systems, which shapes analytical validation, labeling, and performance requirements for transcriptomic IVDs used in clinical decision-making. In Europe, clinical transcriptomic assays sit alongside stringent privacy and evidence requirements, including GDPR, as well as centralized medicines evaluation expectations when transcriptomic biomarkers appear in development programs and companion diagnostic discussions.

In 2026, standards activity tightened validation-ready expectations for workflows used alongside drug development and biologics quality control. The European Pharmacopoeia Commission published Issue 12.1, General Chapter 2.6.41 on NGS-based adventitious viral detection, reinforcing method controls that can influence sequencing-enabled QC environments relying on RNA workflows. ISO also advanced multi-omics standardization by registering DIS 24934 for multi-omics quality control and data integration and progressing ISO/CD 25379-2 for NGS workflows in human RNA examination, pushing vendors and service labs toward more harmonized pre-analytical handling, library preparation, and reporting practices.

Value Chain Analysis

The transcriptomics value chain starts with specialized upstream inputs (enzymes, nucleotides, barcoded oligonucleotides, magnetic beads, and plastics) provided to kit developers and reagent formulators, then moves to midstream manufacturing of sample-prep and library-prep consumables that underpin recurring revenue. Downstream, platform providers combine instruments (sequencers, single-cell and spatial systems, and automation), software, and bioinformatics pipelines, selling through direct channels to large biopharma and academic centers or via distributor and channel-partner models for smaller laboratories. For clinical-grade service delivery, gating steps such as CLIA certification and ISO 15189 accreditation affect purchasing decisions for regulated testing and validation-grade analyses.

Supply risk concentrates around high-barrier enzyme manufacturing and temperature-sensitive reagents, where lead times for library-prep kits can extend to 4-8 weeks and cold-chain performance can constrain single-cell workflows. Value capture continues shifting toward integrated analysis as the bioinformatics skill gap slows clinical commercialization, increasing demand for validated pipelines and automated interpretation layers. Platform ecosystems also keep expanding through spatial capability upgrades, including Brukers February 2026 updates around CosMx whole-transcriptome content and AI-based segmentation additions to its AtoMx SIP environment, reinforcing the move toward bundled wet-lab plus analytics offerings rather than stand-alone kits.

Competitive Landscape

The transcriptomics market shows moderate consolidation as sequencing incumbents extend portfolios via mergers and vertical integration. Illumina’s USD 350 million SomaLogic deal and Thermo Fisher’s USD 3.1 billion Olink acquisition illustrate the pivot toward multi-omic ecosystems that bundle RNA, protein, and spatial data. These moves elevate switching costs for customers, who increasingly favor one-stop solutions covering sample prep through AI reporting.

Emergent challengers such as Element Biosciences and Ultima Genomics attract attention with lower-cost chemistries and innovative sequencing-by-synthesis variants, forcing incumbents to revisit pricing and reagent formats. Roche’s Sequencing-by-Expansion technology enters pilot deployment in 2025, promising higher read accuracy on clinical FFPE tissue. Competitive focus shifts from maximum throughput to usability, automation, and integrated analytics that eliminate bioinformatics bottlenecks.

Intellectual-property positioning remains decisive; Illumina continues to defend core bridge-amplification patents while newcomers design around them. White-space opportunities lie in point-of-care devices, cGMP-compliant automation for cell-therapy QC, and real-time AI interpretation dashboards. Vendors able to manage data security under global privacy frameworks hold an advantage as cross-border genomic collaborations expand.

Global Transcriptomics Industry Leaders

F. Hoffmann-La Roche Ltd

Thermo Fisher Scientific

Merck KGaA

GE Healthcare

Bio-Rad Laboratories

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standardization and clinical validation infrastructure create clear whitespace for vendors that can package transcriptomics into audit-ready workflows. CEN/TS 17981-2:2024 sets technical specifications for NGS workflows focused on human RNA across pre-examination through bioinformatics, supporting opportunities for kit makers, software suppliers, and service providers to align products with a shared workflow specification instead of bespoke lab-by-lab methods. In parallel, ISO activity in 2026, including DIS 24934 for multi-omics quality control and the development track for ISO/CD 25379-2 on human RNA examination, increases demand for referenceable QC, documentation, and data-integration capabilities that support multi-site deployments.

Clinical translation and large-cohort programs are expanding use cases where transcriptomics competes on reproducibility, turnaround time, and secure analytics. U.S. FDA oversight frameworks for gene-expression profiling tests and EU pathways under IVDR push investment toward validated bioinformatics, traceable data handling, and controlled sample-to-report automation, areas that favor suppliers combining consumables with software and services. Population-scale biobank and precision-medicine initiatives also underpin procurement for multi-omics measurement and analytics stacks, as indicated by Thermo Fishers April 2026 collaboration with Singapores PRECISE-SG100K program using integrated proteomics platforms alongside broader omics research infrastructure, which supports demand for interoperable, multi-omics-aligned workflows that include transcriptomic components.

Recent Industry Developments

- June 2026: Merck KGaA entered into a definitive agreement to acquire Bio-Techne Corporation for USD 11.3 billion. The deal targets expanded capabilities in life science tools across multi-omics, spatial biology, and precision diagnostics. Consolidation at this scale can reshape supplier selection for transcriptomics workflows through broader bundled portfolios and manufacturing reach.

- April 2026: Roche announced a definitive merger agreement to acquire SAGA Diagnostics and integrate its tumor-informed molecular residual disease platform into Foundation Medicine. The merger strengthens Roches position in liquid biopsy and oncology testing where gene-expression and RNA-derived signals complement DNA-based readouts. Integration into an established clinical diagnostics franchise supports broader adoption of transcriptomics-adjacent assays in regulated settings.

- May 2024: Bruker acquired NanoString Technologies for USD 392.6 million, adding AtoMx, nCounter, GeoMx, and CosMx product lines. The acquisition expanded Brukers installed base and menu depth in spatial and expression profiling, creating a more vertically integrated offering from instruments through assays. The enlarged portfolio increased competitive pressure on other spatial transcriptomics and digital pathology-adjacent platform providers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the transcriptomics market is counted as the revenue generated from tools and services used to measure and interpret RNA expression, including sequencing and array workflows, related reagents, instruments, software, and analysis services used in research and clinical oriented settings.

Scope exclusions: We exclude general lab plastics, pure data storage with no analytics function, and adjacent omics kits such as proteomics or metabolomics.

Segmentation Overview

- By Technology

- Microarray

- Real-time Quantitative PCR (qPCR)

- Next-Generation Sequencing (RNA-Seq)

- Single-cell RNA-Seq

- Spatial Transcriptomics

- In-situ Hybridization & Other Methods

- By Product

- Consumables & Reagents

- Instruments

- Software & Services

- By Application

- Drug Discovery & Development

- Diagnostics & Disease Profiling

- Biomarker & Target Identification

- Agriculture & Plant Science

- Others

- By End User

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Clinical & Diagnostic Laboratories

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building the real world demand context for transcriptomics, and then mapping how that demand translates into spend across instruments, consumables, software, and services. We referred to public sources such as the National Institutes of Health funding databases, the National Center for Biotechnology Information (NCBI) resources for sequencing and expression repositories, and the World Health Organization for disease burden signals that shape research priorities.

To avoid relying on one data stream, we also checked sources such as the US Food and Drug Administration for diagnostic and testing related signals, the OECD and World Bank for macro indicators tied to R&D intensity, and peer reviewed journals that report adoption trends in RNA sequencing, microarrays, and single cell workflows. Company filings, investor presentations, and reputable science press were used to confirm product mix and pricing direction. Where needed, paid subscriptions supporting company financials and patent databases were used to cross check revenue exposure and innovation activity. These sources are illustrative only, and many other public references were used for clarification and validation during the work.

Primary Interviews and Surveys

Primary work was used to stress test the desk assumptions on usage, pricing, and buying behavior across the transcriptomics workflow, especially where public data is not consistent. We spoke with a mix of product and commercial leaders, lab managers, and procurement facing roles across APAC, EMEA, and the Americas, so our model reflects differences in funding cycles, platform mix, and service outsourcing patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | APAC: 41% |

| Mid tier: 49% | Functional/Unit leaders: 38% | EMEA: 34% |

| Smaller Players: 17% | Managers: 47% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic, where the top-down view reconstructs spend by linking RNA sequencing and gene expression workflow volumes to typical reagent pull-through, instrument placements, and service outsourcing levels by region. Those totals are then corroborated using selective bottom-up approximations, such as sampling average selling price ranges for key consumables and instruments, cross checking service price bands, and rolling up a set of supplier and channel indicators to see if the implied revenue pool is realistic.

Key inputs that shape the model include sequencing run volumes and installed base trends, the mix shift between NGS, microarrays, and qPCR based expression, average consumables per sample, service share for data analysis, and price progression as throughput improves. When a country level split is hard to observe, we use proxy indicators like research funding direction, clinical testing uptake signals, and academic lab intensity, and then normalize to regional totals.

For the forecast, scenario analysis is applied and then anchored to an exponential smoothing trend on the core demand indicators. Adoption is assumed to progress steadily, with step ups possible after major platform cycles. Assumptions are reviewed with interview feedback on budget outlook, procurement timing, and expected pricing moves so the growth path stays practical and explainable.

Data Validation & Update Cycle

Outputs are checked through multiple steps so obvious errors do not get carried into the final totals. We compare the resulting market values against independent signals such as R&D funding direction, instrument shipment momentum, and changes in service outsourcing, and then investigate any large variances before sign-off.

If anomalies show up, the inputs are revisited and selected experts are re-contacted to confirm whether the change is real or model-driven. Reports are refreshed annually, with interim updates when material events can shift pricing, adoption, or regional demand. Before delivery, the latest pass is completed so clients receive an updated view based on the most recent inputs available.

Mordor Intelligence's Transcriptomics Market Estimate Compared With Other Published Estimates

Published market sizes for transcriptomics can differ even when they seem to describe the same topic, because the counted scope, the timing of currency conversion, and the way pricing is trended over time are not handled uniformly. Differences also come from how strictly services are included, how single cell or clinical use cases are treated, and whether the estimate is refreshed after major funding or instrument cycle changes.

In this study, the refresh cadence is tied to new pricing checks and re-validation of the split between consumables pull-through, instrument demand, and outsourced analysis, which also reduces drift from one year to the next when exchange rates move. Currency timing is kept consistent for the base year, and ASP logic is constrained by observed workflow mix shifts, a set of controls applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.49 B (2026) | |

| Global Consultancy A | USD 9.17 B (2026) | Uses a different base-year framing (2025 as base) and often applies faster price progression for high-throughput sequencing, which can lift the 2026 value when blended across regions. |

| Industry Publisher B | USD 7.74 B (2024) | Anchors on an earlier year and may include a broader services bucket without re-checking the instrument versus consumables split for later workflow mix changes, which can shift the starting value. |

The table shows that most of the spread can be explained by timing and how pricing and services are treated, rather than by a totally different view of demand. When the base year, currency conversion point, and workflow level checks are kept consistent, the resulting market size becomes easier to trace back to clear drivers and to update in a repeatable way.

Key Questions Answered in the Report

What is the current Global Transcriptomics Market size?

The transcriptomics market size reached USD 8.49 billion in 2026 and is forecast to hit USD 10.86 billion by 2031.

Who are the key players in Global Transcriptomics Market?

F. Hoffmann-La Roche Ltd, Thermo Fisher Scientific, Merck KGaA, GE Healthcare and Bio-Rad Laboratories are the major companies operating in the Global Transcriptomics Market.

Which is the fastest growing region in Global Transcriptomics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which technology leads the transcriptomics market?

Single-cell RNA sequencing leads with 46.78% market share, though spatial transcriptomics is growing faster at a 6.32% CAGR.

Page last updated on: