Metabolomics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.77 Billion |

| Market Size (2031) | USD 4.57 Billion |

| Growth Rate (2026 - 2031) | 10.47% CAGR |

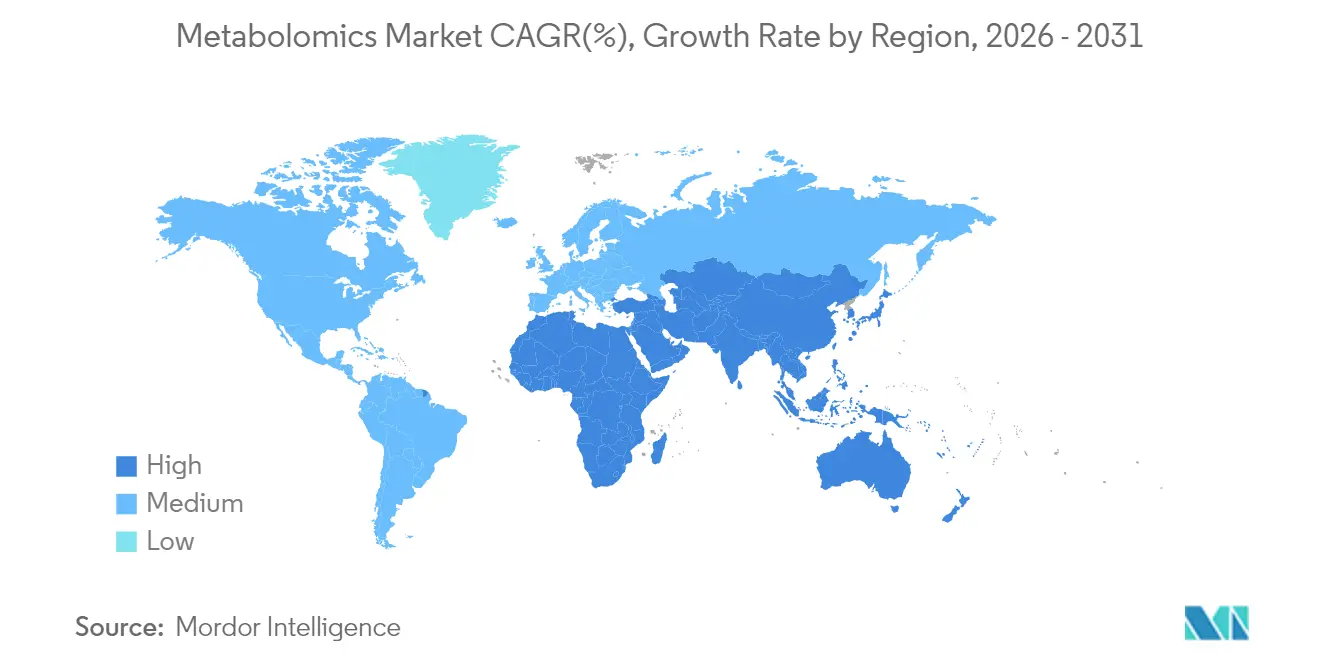

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

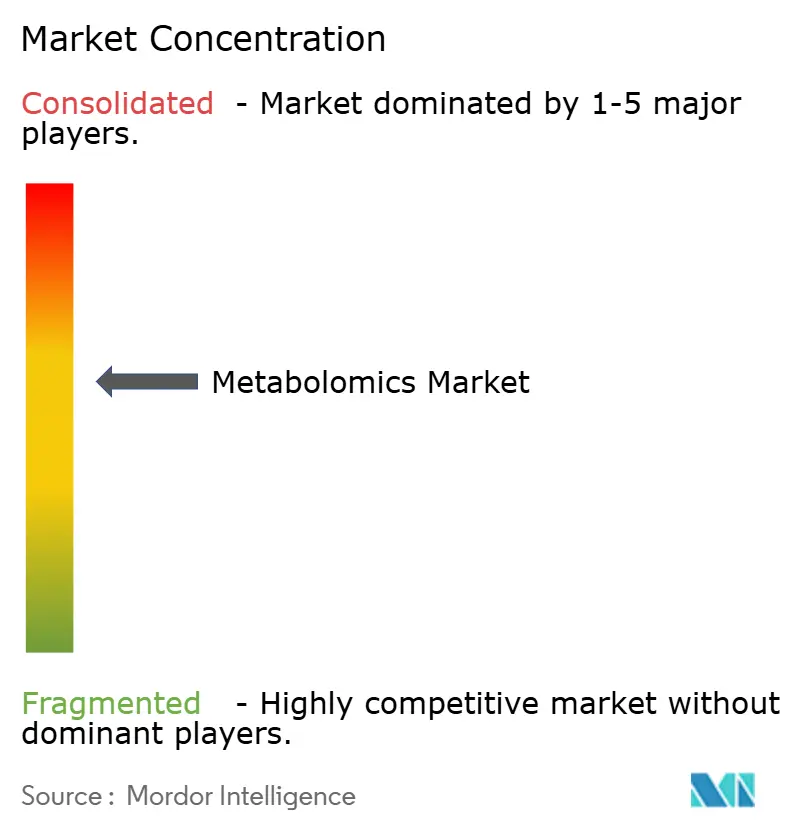

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metabolomics Market Analysis by Mordor Intelligence

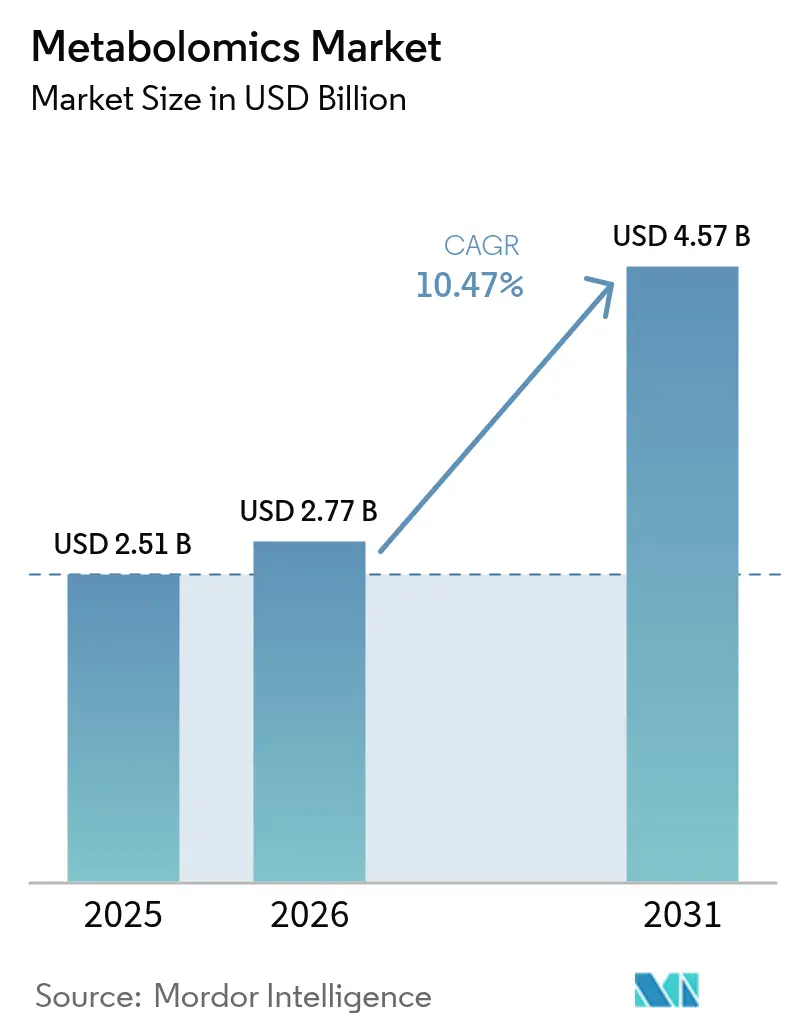

The Metabolomics Market size was valued at USD 2.51 billion in 2025 and estimated to grow from USD 2.77 billion in 2026 to reach USD 4.57 billion by 2031, at a CAGR of 10.47% during the forecast period (2026-2031).

Sustained demand for precision-medicine solutions, rapid improvements in high-resolution mass-spectrometry platforms, and widespread deployment of artificial-intelligence pipelines are the primary forces widening the metabolomics market opportunity set. Pharmaceutical companies are embedding metabolomic readouts in early-stage screening to shorten development timelines, while hospitals are beginning to adopt targeted metabolite panels for routine diagnostics. Regulatory harmonization—most notably the FDA’s Q2(R2) analytical-procedure validation framework gives laboratory directors greater confidence to integrate these assays into clinical workflows. Intensifying competition, manifested in multi-billion-dollar acquisitions of complementary “omics” assets, further highlights the strategic importance of metabolomics within end-to-end life-science toolkits. Collectively, these dynamics underpin robust capital inflows, reinforce the long-term growth trajectory, and solidify the metabolomics market as a cornerstone of next-generation healthcare innovation.

Key Report Takeaways

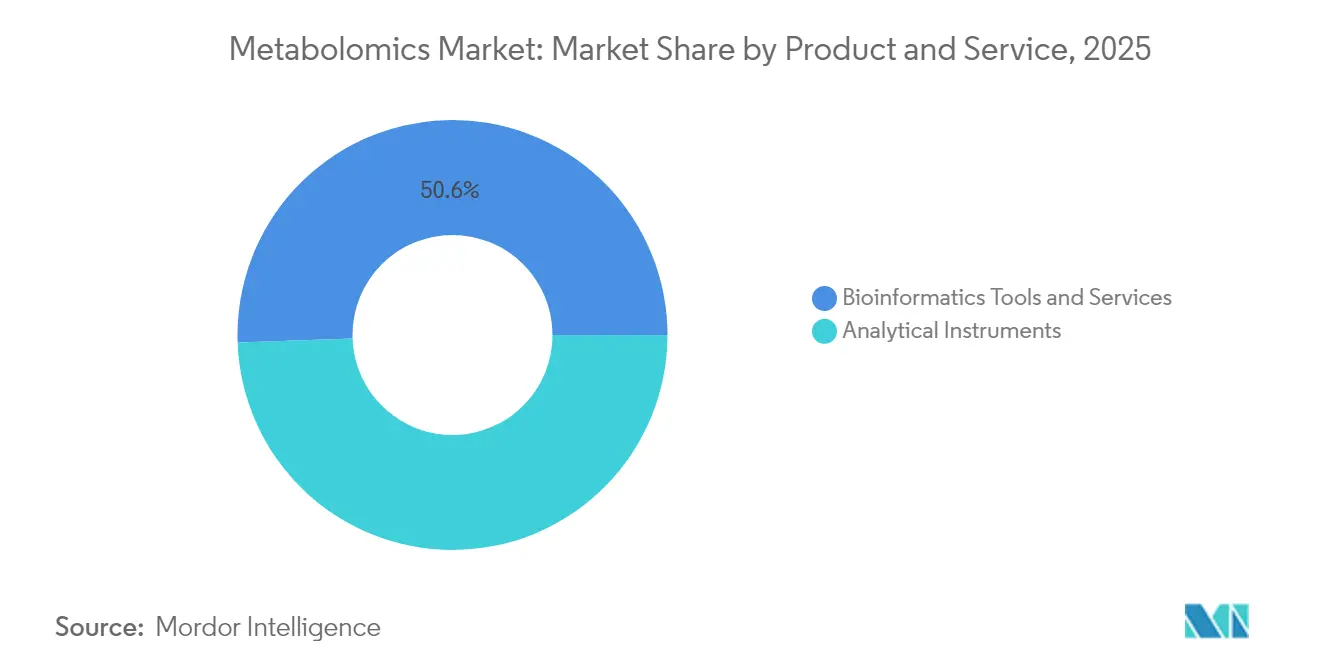

- By product & service, bioinformatics tools and services held 50.55% of 2025 revenue, while the same segment is projected to expand at an 11.21% CAGR through 2031.

- By application, biomarker and drug discovery accounted for 31.05% of the metabolomics market share in 2025; personalized medicine is set to register the fastest 14.68% CAGR to 2031.

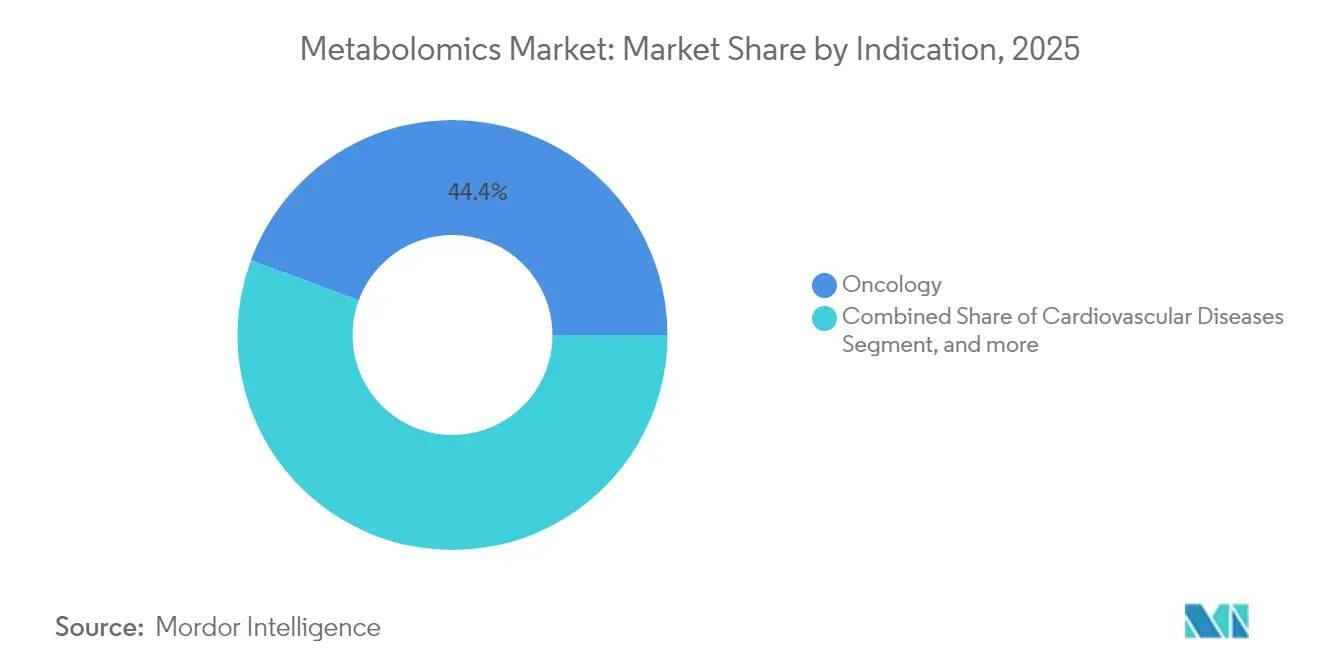

- By indication, oncology dominated with 44.35% revenue share in 2025, whereas neurological disorders lead future growth at a 15.45% CAGR.

- By end user, academic and research institutes led with 36.95% revenue share in 2025; hospitals and diagnostic laboratories deliver the highest 11.08% adoption CAGR to 2031.

- By geography, North America contributed 41.10% of 2025 revenue, while Asia-Pacific is forecast to grow at a 13.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metabolomics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Personalized/Precision Medicine | +2.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Escalating Public & Private R&D Funding for Omics-Based Drug Discovery | +2.1% | North America, EU, Asia-Pacific core markets | Long term (≥ 4 years) |

| Technological Advances in High-Resolution MS And LC Platforms | +1.9% | Global, manufacturing concentrated in US, Germany, Japan | Short term (≤ 2 years) |

| Growing Adoption of Multi-Omics Workflow Integration in Pharma Pipelines | +1.6% | Global pharmaceutical hubs, spill-over to emerging markets | Medium term (2-4 years) |

| AI-Driven Metabolite-Annotation Platforms Shortening Analysis Time | +1.4% | Technology centers in North America, EU, China | Short term (≤ 2 years) |

| Expansion of Single-Cell & Spatial Metabolomics for Rare-Cell Profiling | +1.2% | Research-intensive regions: North America, EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Personalized/Precision Medicine

Precision-nutrition and individualized-therapy initiatives are firmly embedding metabolomic readouts into clinical-decision pathways. The NIH has earmarked USD 156 million over five years to study diet-gene-metabolome interactions, underscoring policy-level commitment to patient-specific interventions. Basket and umbrella clinical-trial designs routinely stratify patients by circulating metabolite profiles, which accelerates enrollment and enhances statistical power. Molecular portraits that integrate metabolomics with genomic and proteomic layers improve diagnostic specificity, reduce adverse-event rates, and direct evaluated therapies toward responsive sub-populations. Pharmaceutical sponsors value metabolomic data because it delivers real-time pharmacodynamic feedback that complements static genetic biomarkers. Point-of-care devices, currently undergoing validation, promise to extend these capabilities to primary-care settings, broadening the total accessible patient pool and reinforcing positive uptake momentum across the metabolomics market.

Escalating Public & Private R&D Funding for Omics-Based Drug Discovery

Long-cycle research budgets increasingly allocate dedicated lines to multi-omics infrastructure, with metabolomics frequently cited as a critical short-list priority. Large pharmaceutical enterprises now integrate AI-driven annotation engines, such as PandaOmics, to converge metabolomic, transcriptomic, and proteomic datasets, thereby illuminating novel druggable targets. Competitive grant programs in Europe and Asia-Pacific also fund translational metabolomics for rare-disease research, boosting cross-border collaboration and NGS-linked compound‐screening throughput. Venture and growth-equity investors continue to fund specialist platform companies that convert metabolite libraries into actionable therapeutic insights, bringing fresh capital and commercial discipline to the metabolomics market. These cumulative injections of funding absorb development risk and accelerate time-to-market for data-rich services.

Technological Advances in High-Resolution MS and LC Platforms

Next-generation instrumentation, highlighted by the Stellar platform’s 10-fold sensitivity gain and 5-fold compound-throughput expansion, has markedly enlarged the metabolite dynamic range that researchers can interrogate. SCIEX’s ZT Scan DIA upgrade extends data-independent acquisition to near comprehensive coverage while preserving quantitative linearity. Pairing these hardware improvements with self-supervised learning models trained on millions of spectra drastically slashes manual-curation time, moves discovery workflows upstream, and trims per-sample processing cost. Miniaturized, cartridge-based sample-handling modules further reduce instrument downtime, making high-end platforms viable for regional hospitals rather than only Tier-1 academic centers. Collectively, these innovations widen the installed-base footprint and support double-digit expansion within the metabolomics market.

Growing Adoption of Multi-Omics Workflow Integration in Pharma Pipelines

Spatial multi-omics now overlays metabolomic, genomic, and transcriptomic data at sub-cellular resolution, enabling researchers to map drug-induced metabolic rewiring inside tissue microenvironments. Web-based software suites eliminate coding barriers, allowing bench scientists to run cross-platform analytics through drag-and-drop interfaces.[1]“Metabolomics: Towards Comprehensive Metabolic Profiling,” Nature Biotechnology, nature.com Single-cell metabolomics reveals intra-tumoral heterogeneity and metabolic niche dependencies that bulk assays systematically miss, directing more precise combination-therapy design. Regulatory bodies are codifying guidelines exemplified by the FDA’s Q14 protocol-development framework that legitimize multi-omics methods inside formal submission dossiers.[2]Food and Drug Administration, “Q2(R2) Validation of Analytical Procedures,” fda.gov Standard-setting drives platform vendor alignment and underpins solid commercial value propositions throughout the metabolomics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Nature of Advanced Analytical Instruments | -1.8% | Global, particularly affecting emerging markets and smaller institutions | Short term (≤ 2 years) |

| Shortage Of Bioinformaticians with Metabolome Expertise | -1.2% | Global, most acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Lack of Globally Harmonised Metabolite Reference Standards | -0.9% | Global, with regulatory fragmentation between US, EU, and Asia-Pacific | Long term (≥ 4 years) |

| Data-Privacy Hurdles in Federated Clinical Metabolomics Networks | -0.7% | EU and North America primarily, expanding to global markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Nature of Advanced Analytical Instruments

State-of-the-art high-resolution mass spectrometers often sell for USD 500,000–2 million, with recurrent service contracts adding 10-15% of purchase cost annually. Smaller institutions struggle to justify such capital outlays, constraining broader diffusion and keeping usage concentrated among well-funded centers. Vendor-hosted leasing models and collaborative core-facility networks provide interim relief, yet budgetary headwinds remain a formidable drag. The metabolomics market nevertheless benefits from gradual cost compression as modular, 3D-printed components reduce manufacturing expense. Cloud-connected platforms that enable remote operation and data processing further alleviate on-site infrastructure requirements, slightly easing this restraint’s severity over time.

Shortage of Bioinformaticians with Metabolome Expertise

Comprehensive metabolomic analysis demands cross-disciplinary skill sets that meld analytical chemistry, machine learning, and systems biology talent that remains in short supply.[3]“Urinary Metabolite Signatures for Early Alzheimer’s Detection,” Frontiers in Aging Neuroscience, frontiersin.org Emerging markets face heightened scarcity as competitive salaries in established regions siphon specialized professionals. Universities have begun rolling out tailored curricula, but graduate output is still below growing laboratory demand. Automated annotation pipelines and low-code visualization modules partially bridge the expertise gap, permitting non-specialists to generate publication-quality insights. Even so, talent acquisition challenges temper the pace at which newly equipped facilities can scale, marginally dampening near-term expansion within the metabolomics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Bioinformatics Dominance Drives Market Evolution

The bioinformatics tools and services segment captured 50.55% of the metabolomics market size in 2025 and is projected to sustain an 11.21% CAGR through 2031, reflecting the data-centric orientation of modern metabolomics workflows. This leadership is anchored in the recognition that fewer than 2% of recorded spectra can be matched to curated libraries, turning algorithmic annotation into the field’s primary bottleneck. Emerging cloud-native engines automatically cross-reference spectral data against ever-larger repositories while ranking putative compound identities with probabilistic confidence scores. Multi-tenant deployment models distribute computational overhead and lower entry barriers for resource-constrained laboratories, further expanding total addressable users inside the metabolomics market.

Sophisticated pipelines such as microbeMASST now integrate taxonomic metadata, unlocking previously invisible microbial-metabolite linkages and fuelling downstream functional-omics investigations. As user interfaces simplify, bench scientists without advanced coding experience can execute high-dimensional pathway mapping, which in turn accelerates hypothesis generation. Hardware vendors reinforce symbiotic demand by offering end-to-end instrument-to-cloud data capture and automated upload utilities. This virtuous cycle elevates bioinformatics from a back-office support role to a primary revenue engine, ensuring the segment’s continued prominence within the broader metabolomics market.

By Application: Personalized Medicine Reshapes Clinical Metabolomics

Biomarker and drug discovery maintained 31.05% revenue share in 2025; however, personalized-medicine workflows will lead expansion at a 14.68% CAGR, confirming the strategic importance of patient-specific interventions. Consumer interest in nutrition-based disease prevention, alongside clinical adoption of treatment-tailoring assays, is realigning investment priorities toward comprehensive profile-matching services. Toxicology programs leverage untargeted metabolomic screens to uncover off-pathway liabilities earlier in the pipeline, saving late-stage attrition cost and guiding revision cycles. Nutrigenomics applications assess bioactive-compound bioavailability and metabolic adaptation, delivering actionable dietary recommendations that resonate with wellness-oriented stakeholders across the metabolomics market.

Clinical laboratories implement validated panels for metabolic disorders, chronic kidney disease, and oncology recurrence monitoring, demonstrating real-world utility and reimbursement readiness. The rise of multiplex assays capable of quantifying hundreds of analytes simultaneously enhances diagnostic yield per sample, lowering per-target cost and increasing clinician adoption. Integration with electronic health-record systems further embeds metabolomic data into routine care, reinforcing personalized medicine’s status as the high-growth frontier of the metabolomics market.

By Indication: Neurological Disorders Drive Innovation Beyond Oncology

Oncology retained a 44.35% revenue lead in 2025, yet neurological applications will outpace all others with a 15.45% CAGR to 2031 as researchers discover early-stage metabolic fingerprints for neurodegeneration. Urine-based markers such as theophylline show promise for non-invasive Alzheimer’s screening, offering alternatives to spinal-fluid taps and complex imaging studies. Similarly, metabolomic interrogation of Parkinson’s disease reveals folate and tetrahydrobiopterin pathway disruption, inviting targeted supplementation trials. Spatial metabolomics applied to brain-tumor tissues uncovers microenvironment-specific nutrient dependencies, guiding local-delivery therapeutic concepts within the metabolomics market.

Cardiovascular and infectious-disease research maintains solid footing, but the distinct unmet need in early neurodegenerative diagnosis positions neurological-disorder assays at the innovation forefront. Pharma pipelines increasingly reference cerebrospinal-fluid metabolic profiles for patient stratification in adaptive-design trials, accelerating evidence generation. Public-funded consortia pool large-scale biobank samples to expand statistical power, propelling biomarker validation forwards and highlighting this indication’s strategic significance for the metabolomics market.

By End User: Clinical Translation Accelerates Hospital Adoption

Academic and research institutes held 36.95% of 2025 revenue; nonetheless, hospital and diagnostic-laboratory contracts are forecast to grow at an 11.08% CAGR as certified assays transition from bench to bedside. Clearer regulatory pathways, combined with evidence of clinical utility, are pushing procurement committees to allocate capital toward mass-spectrometry-based platforms. Point-of-care devices that deploy cartridge-miniaturized NMR or ambient-ionization MS remove logistical delays inherent in centralized testing and open new channels across the metabolomics market.

Contract research organizations (CROs) enhance adoption velocity by offering turnkey multi-omics trial-support packages, de-risking complex analytical requirements for sponsors. Pharmaceutical companies outsource high-volume profiling to specialized CROs while reserving core-capability investments for strategic discovery workflows. This flexible capacity model smooths demand spikes and ensures that new entrants can access best-in-class technical infrastructure without heavy upfront costs. Consequently, hospital adoption of validated panels is set to scale rapidly, further embedding clinical metabolomics in routine care pathways.

Geography Analysis

North America preserved 41.10% revenue leadership in 2025, fortified by robust NIH and enterprise-level R&D spending, mature regulatory frameworks, and local manufacturing reinvestment exemplified by Thermo Fisher Scientific’s USD 2.0 billion capacity expansion plan. The metabolomics market size for the United States reflects widespread deployment of multi-omics oncology tests, fast catch-up of metabolic-panel reimbursement, and extensive academic-industry partnerships. Canada’s precision-health initiatives and Mexico’s growing pharmaceutical export capacity provide incremental lift, sustaining the region’s aggregate revenue share. Data-privacy legislation such as the California Consumer Privacy Act drives early adoption of privacy-enhancing computation, reinforcing North American leadership in secure, interoperable metabolomics data platforms.

Asia-Pacific represents the fastest-growing territory at a 13.22% CAGR through 2031, driven by China’s localization of high-end mass-spectrometer assembly and India’s scaling clinical-trial infrastructure. Government stimulus packages covering precision medicine, coupled with inward foreign-direct investment, underpin capacity build-out across Tier-1 hospitals. Japan’s Foods with Function Claims framework enables metabolomics-supported functional-food labels that command premium shelf pricing, extending commercial relevance beyond pharma into consumer-health sectors. Australia and South Korea leverage strong academic ecosystems to attract multinational-sponsored trials, further enlarging the regional metabolomics market footprint.

Europe maintains a substantial portion of global revenue through coordinated Horizon-funded research networks, established biopharmaceutical clusters, and accelerated adoption of privacy-preserving data federations. Germany’s engineering prowess undergirds continued instrumentation innovation, while the United Kingdom pushes translational medicine programs that embed metabolomics into National Health Service pilot pathways. France streamlines reimbursement for multi-omics oncology tests, stimulating domestic laboratory demand. Italy and Spain add volume via growing clinical-research outsourcing assignments. The European Commission’s emphasis on green and sustainable agrifood supply chains triggers additional metabolomics market applications in food authenticity and environmental surveillance, providing diversified revenue channels across the continent.

Competitive Landscape

The metabolomics market features moderate concentration, with legacy analytical-instrument giants expanding through inorganic moves while specialist software firms carve out high-growth niches. Thermo Fisher Scientific, Agilent Technologies, and Waters Corporation command outsized installed bases, leveraging life-cycle service contracts and consumables bundles to lock in customers. Thermo Fisher’s USD 3.1 billion Olink acquisition and forthcoming USD 4.1 billion Solventum purchase demonstrate aggressive portfolio broadening aimed at vertical integration from sample prep to data analytics. Agilent pairs cutting-edge hardware with proprietary ChemStation software upgrades that streamline study design, hoping to counter software-driven challengers.

Emerging players differentiate through AI-first product strategies. Metabolon secured USD 60 million of credit, allocating funds to scale its metabolite-library expansion and automated-analysis engine. Olaris, now backed by Bruker equity, launched an NMR-based kidney-transplant monitoring assay, illustrating how focused disease-area solutions can achieve rapid market entry. SCIEX deepened its computational stack by partnering with Bioinformatics Solutions Inc., fusing ZenoTOF hardware with cloud-delivered peptide-search algorithms that enhance proteomics depth and feed metabolomics pathway-cross-talk analysis.

Competitive intensity is expected to heighten as point-of-care vendors enter the field. Companies developing cartridge-style ambient-ionization modules seek to bypass traditional bench‐top hardware, disrupting incumbent revenue streams. Privacy-preserving federated-learning platforms promise compliant cross-institutional data sharing, opening white-space for SaaS vendors unattached to instrument chains. Finally, sustained pharma demand for spatial metabolomics and 3-dimensional tissue mapping will reward firms that combine hardware, reagents, and AI analytics into seamless turnkey offerings, reshaping competitive dynamics across the metabolomics market.

Metabolomics Industry Leaders

Thermo Fisher Scientific Inc.

Bio-Rad Laboratories

Agilent Technologies Inc.

Bruker

Danaher Corporation (SCIEX)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Olaris received an undisclosed investment from Bruker Corporation to advance its metabolomics platform and launched myOLARIS-KTdx, a non-invasive urine-based test for kidney graft injury surveillance utilizing NMR technology.

- April 2025: Thermo Fisher Scientific announced a USD 2 billion investment in US innovation and manufacturing over four years, including USD 1.5 billion for capital expenditures and USD 500 million for R&D focused on high-impact innovation in life sciences.

- April 2025: Bruker Corporation made a majority investment in Ridom GmbH to expand its microbiology solutions into NGS applications, enhancing capabilities in genomic bacterial strain differentiation and phylogenetic analysis.

- February 2025: Thermo Fisher Scientific announced the acquisition of Solventum's Purification & Filtration business for approximately USD 4.1 billion to enhance bioproduction capabilities, with expected closure by end of 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the metabolomics market captures every product, software module, and fee-for-service activity that enables the comprehensive identification and quantification of small-molecule metabolites within biological samples. In scope are separation platforms (LC, GC, CE), high-resolution detection systems (MS, NMR), bundled consumables, and licensed bioinformatics environments that convert raw spectra into biological insight for academic, clinical, and industrial users.

Scope exclusion: Standalone multi-omics instruments or analytics sold for proteomics or genomics only are not counted.

Segmentation Overview

- By Product & Service

- Analytical Instruments

- Separation Techniques

- Liquid Chromatography

- Gas Chromatography

- Capillary Electrophoresis

- Detection Techniques

- Mass Spectrometry

- Nuclear Magnetic Resonance

- Other Detection Techniques

- Separation Techniques

- Bioinformatics Tools & Services

- Analytical Instruments

- By Application

- Biomarker & Drug Discovery

- Toxicology

- Nutrigenomics

- Personalized Medicine

- Clinical Diagnostics

- Environmental & Agricultural Research

- By Indication

- Oncology

- Cardiovascular Diseases

- Neurological Disorders

- Infectious Diseases

- Metabolic Disorders

- By End User

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

- Hospitals & Diagnostic Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed principal investigators at metabolomics core facilities across North America, Europe, and Asia-Pacific, senior product managers from instrument makers, and business development leads at specialist CROs. Conversations tested volume assumptions, average selling prices, and platform replacement cycles, while surveys of end-user labs clarified unmet needs in untargeted workflows and bioinformatics capacity.

Desk Research

We begin with publicly available macro and industry datapoints that frame demand for metabolomics workflows, such as NIH RePORTER grant logs, World Bank R&D intensity tables, OECD health-tech trade data, and FDA biomarker qualification dossiers. Technical uptake is tracked through patent families retrieved via Questel, import-export records on Volza, and company 10-Ks parsed through Dow Jones Factiva. Academic citation trends, peer-reviewed studies, and association white papers (e.g., Metabolomics Society) further confirm emerging use cases and regional adoption. These sources illustrate funding shifts, instrument shipments, and pricing norms. The list is illustrative, not exhaustive, and many additional references supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down model reconstructs global spending by mapping installed LC-MS and NMR bases to annual utilization, grant funding pipelines, and instrument replacement frequency. Selective bottom-up roll-ups of sampled ASP x units from vendor disclosures and channel checks temper each geographic total. Key variables like NIH metabolomics program awards, price erosion on triple-quadrupole MS, number of new oncology clinical trials applying metabolomic endpoints, and average core-lab sample throughput drive a multivariate regression that projects revenue through 2030. Where primary data gaps persist, conservative benchmarks from adjacent omics tools are imputed and later adjusted once corroborated by fresh interviews.

Data Validation & Update Cycle

Outputs undergo variance checks against external shipment tallies and academic publication counts, followed by a two-stage peer review within Mordor. Reports refresh each year, with interim revisions triggered by material events such as a disruptive platform launch or major funding surge. A final analyst sweep ensures the client receives the latest calibrated view.

Why Mordor's Metabolomics Baseline Commands Reliability

Published estimates differ because firms pick dissimilar scopes, inflation factors, and refresh cadences. By anchoring totals to verifiable instrument deployments and cross-checking with real spending proxies, Mordor delivers a balanced midpoint rather than an optimistic or exceedingly conservative extreme.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.51 Bn (2025) | Mordor Intelligence | - |

| USD 3.72 Bn (2024) | Global Consultancy A | Aggregates broader multi-omics services and software, inflating addressable spend |

| USD 3.77 Bn (2024) | Industry Insights Firm B | Adds downstream CRO contract revenues and applies aggressive ASP escalation |

The comparison shows that divergent scopes, rather than calculation errors, drive the spread. By selecting only metabolomics-specific revenue streams and refreshing assumptions annually, Mordor provides decision-makers with a transparent, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current size of the metabolomics market?

The metabolomics market is valued at USD 2.77 billion in 2026 and is projected to reach USD 4.57 billion by 2031.

Which product segment leads the metabolomics market?

Bioinformatics tools and services lead with 50.55% revenue share in 2025 and exhibit an 11.21% CAGR outlook.

Why is Asia-Pacific considered the fastest-growing region?

Localized instrument manufacturing in China and expanding clinical-research capacity in India push Asia-Pacific to a 13.22% CAGR through 2031.

How are hospitals adopting metabolomics?

Hospitals and diagnostic labs are integrating validated metabolite panels for disease monitoring, growing at an 11.08% CAGR due to clearer regulatory guidance.

What technological advances are accelerating the field?

Next-generation mass spectrometry platforms offering 10-fold sensitivity gains and AI-powered annotation tools drastically reduce analysis time and broaden application scope.

Which indications show the highest growth potential?

Neurological disorders lead future growth with a 15.45% CAGR, driven by advances in early-stage Alzheimer’s and Parkinson’s biomarkers.

Page last updated on: