Market Overview

| Study Period | 2020 - 2031 |

|---|---|

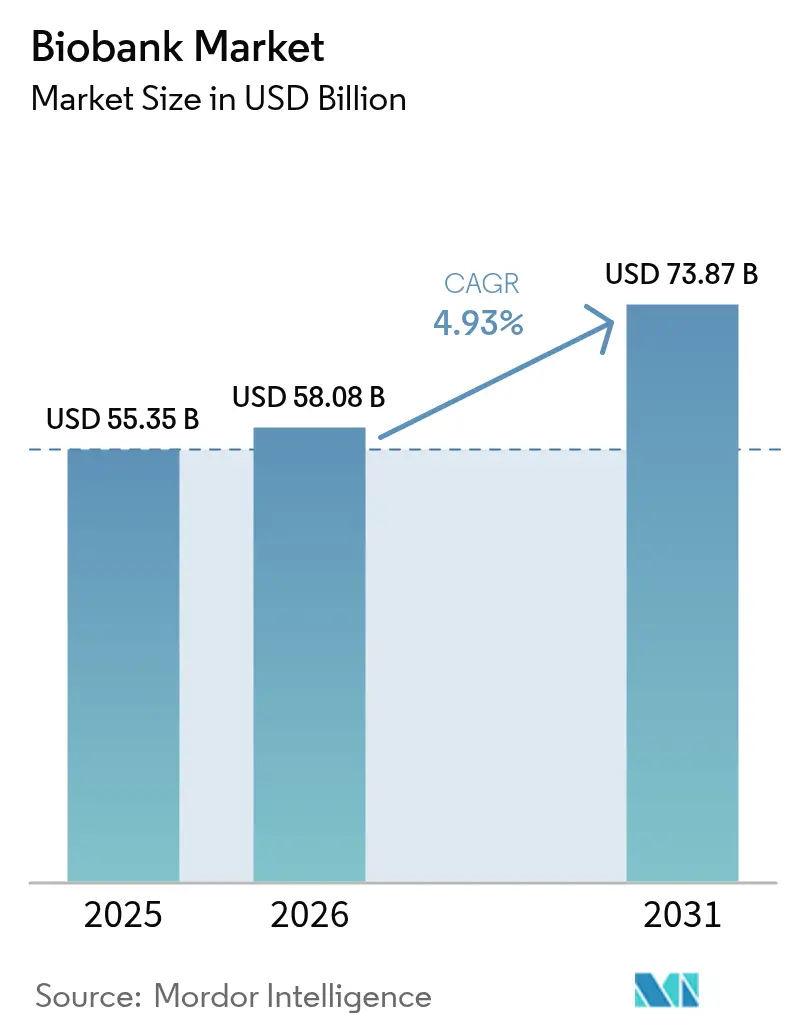

| Market Size (2026) | USD 58.08 Billion |

| Market Size (2031) | USD 73.87 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biobank Market Analysis by Mordor Intelligence

Biobank market size in 2026 is estimated at USD 58.08 billion, growing from 2025 value of USD 55.35 billion with 2031 projections showing USD 73.87 billion, growing at 4.93% CAGR over 2026-2031.

Expansion reflects the move from building sample repositories to supporting precision-medicine pipelines that merge stem-cell therapies, proteomics, and multi-omics workflows. Clearer regulations, such as the FDA’s January 2025 draft guidance on donor eligibility, are reducing clinical uncertainty and accelerating adoption in hospital and pharmaceutical settings. Demand is further lifted by hospital uptake of cord-blood services, public and private funding for pandemic preparedness, and the rise of AI-based quality analytics. Competitive intensity is moderate, with large suppliers acquiring niche innovators to offer integrated cold-chain, automation, and analytic platforms.

Key Report Takeaways

- By application, regenerative medicine led with 36.12% revenue share in 2025; it is also projected to record the fastest 7.02% CAGR to 2031.

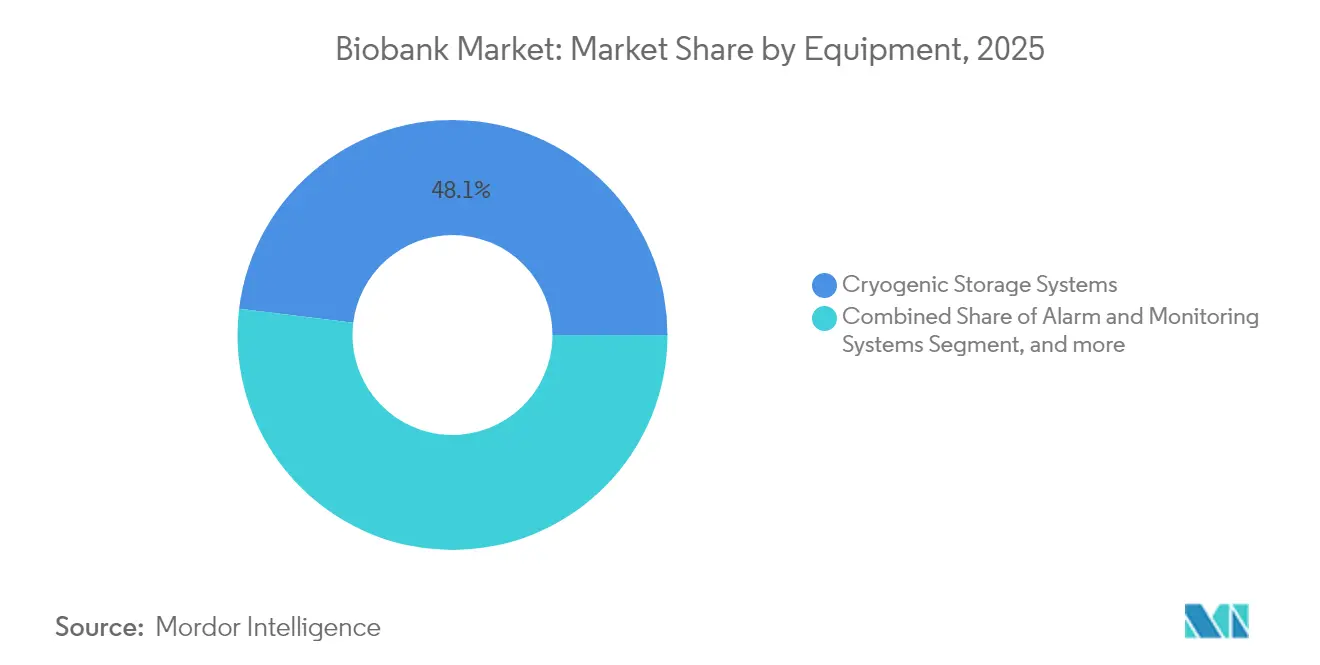

- By equipment, cryogenic storage systems held 48.05% of the biobank market size in 2025; freezers are on track for a 7.78% CAGR during the forecast period.

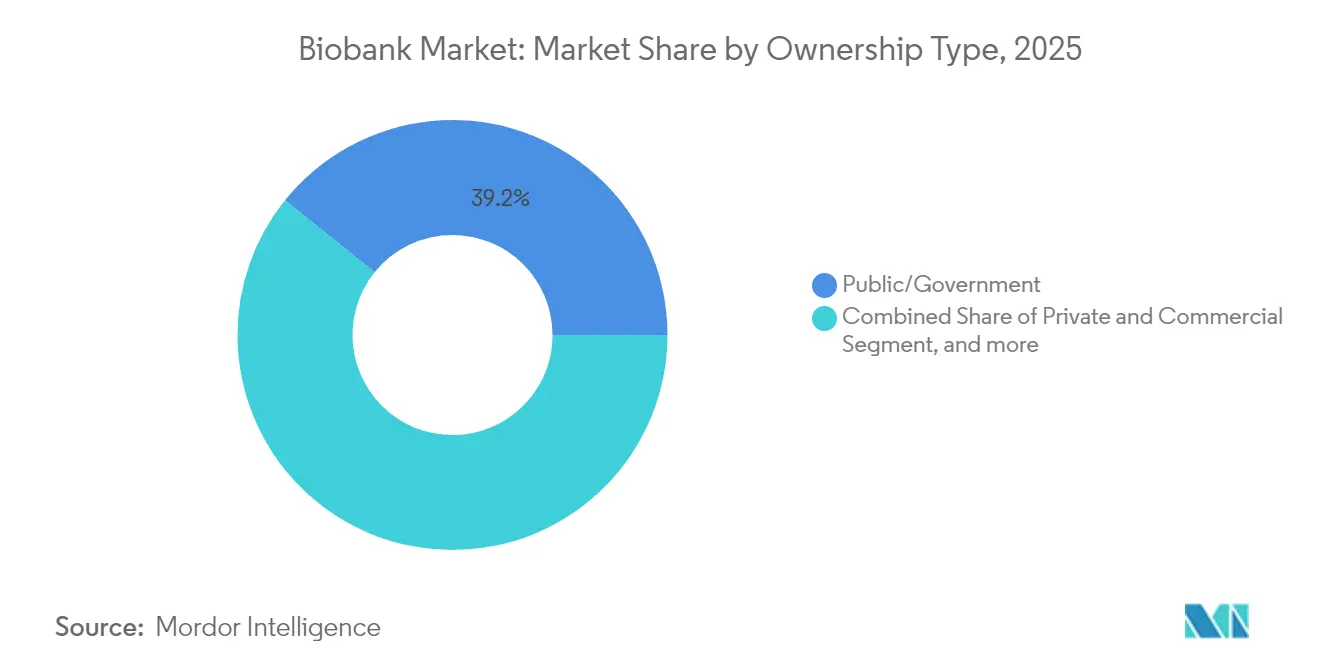

- By ownership model, public and government entities commanded 39.22% share of the biobank market in 2025; academic and non-profit biobanks are the fastest-growing group at 9.28% CAGR.

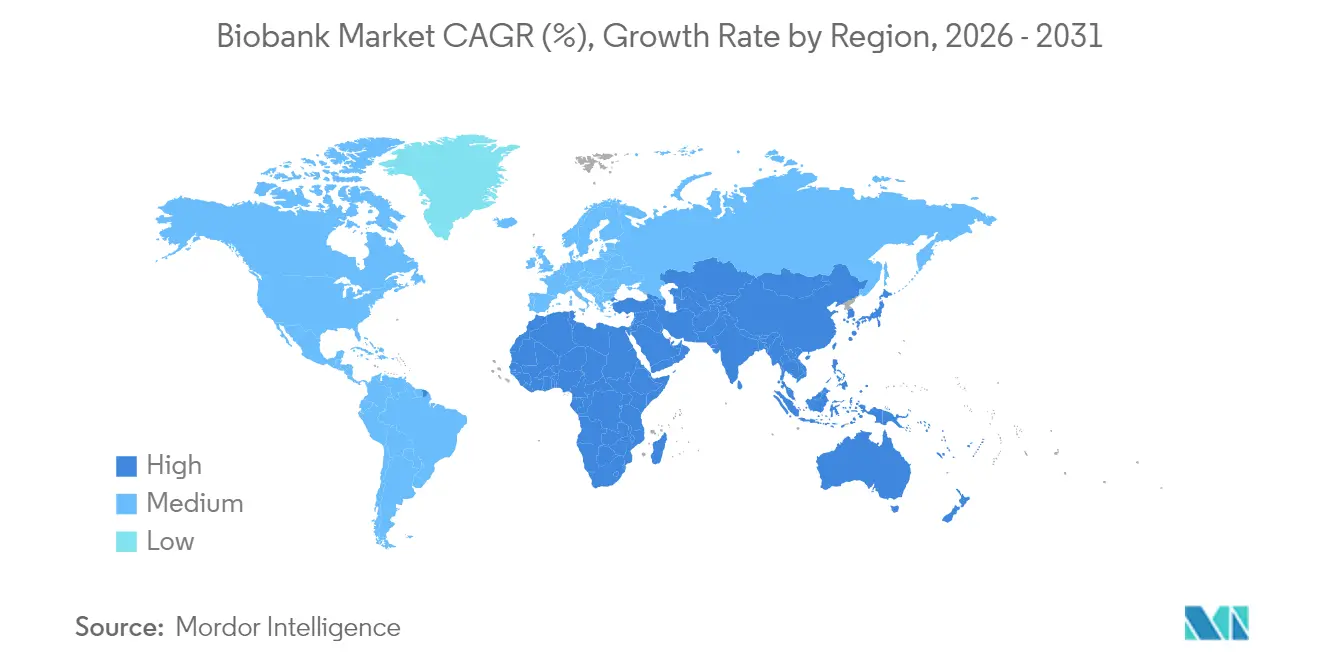

- By geography, North America dominated with a 35.90% share in 2025, yet Asia-Pacific is the fastest-growing region at a 9.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biobank Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovations in Regenerative Medicine | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing Incidences of Chronic Diseases | +0.8% | Global, with higher impact in aging populations of developed markets | Long term (≥ 4 years) |

| Advances in Drug Discovery & Development | +1.0% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Government & NGO Funding Inflows | +0.7% | Global, with emphasis on public health initiatives | Short term (≤ 2 years) |

| AI-Driven Sample-Quality Analytics Adoption | +0.5% | Technology-advanced markets: North America, Europe, select APAC | Medium term (2-4 years) |

| Decentralized Blockchain-Enabled Consent Networks | +0.3% | Early adoption in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Innovations in Regenerative Medicine

Breakthroughs such as Cedars-Sinai’s cardiosphere-derived cells for Duchenne muscular dystrophy show how a single cell type can serve multiple therapeutic paths.[1]Cedars-Sinai, “Cardiosphere-Derived Cells Show Promise for Duchenne Muscular Dystrophy,” nature.com Gene-edited progenitor cells for ALS require biobanks to guarantee both cellular integrity and genomic stability. ARPA-H’s EMBODY program demands infrastructure that is able to support complex immune-cell reprogramming.[2]Advanced Research Projects Agency for Health, “EMBODY Program Announcement,” arpa-h.gov Research on microgravity-grown stem cells suggests that orbital production techniques will soon influence ground-based processing. Collectively, these shifts push the biobank market toward facilities that resemble small-scale manufacturing plants rather than passive warehouses.

Growing Incidences of Chronic Diseases

The UCLA team showed that linking biobank genetics to electronic health records predicts patient responses to standard drugs.[3]UCLA Health Sciences, “Biobank Genomics Predict Drug Response,” ucla.edu In China, cord-blood transplants for Thalassemia Major climbed from 30,000 to nearly 40,000 cases in 2024, demonstrating clinical reliance on banked materials. Tianjin’s 19-year-old autologous cord-blood success underscores the long-term utility of well-preserved samples. Haplocord protocols that combine cord blood with haploidentical donors maximise sample use, raising demand on existing repositories. As chronic conditions proliferate, the biobank market is shifting from research-centric to therapy-centric operations.

Advances in Drug Discovery & Development

Thermo Fisher’s involvement in the UK Biobank Pharma Proteomics Project, analysing 5,400 proteins across 600,000 samples, exemplifies the scale modern drug pipelines require. BioAge Labs and Novartis structured a deal worth up to USD 530 million based on proprietary longevity datasets. BD’s FACSDiscover A8 analyser captures 50 cellular traits in real time, enabling richer biobank datasets. AstraZeneca’s Open Innovation platform requests integrated imaging and multi-omics packages, illustrating that pharmaceutical partners now expect data-rich assets rather than isolated vials. This integration cements the biobank market as a strategic pillar of drug discovery.

Government & NGO Funding Inflows

ATCC secured USD 87 million from BARDA to build Project NextGen, a centralised repository for pandemic-relevant materials. The EU committed EUR 45 million (USD 49 million) to the Genome of Europe reference sequencing project, leveraging national biobank assets. ARPA-H’s OCULAB initiative explores tear-based biomarkers, pushing collection beyond blood and tissue samples. Brazil’s Fiocruz established a biodiversity bank during COVID-19, proving that rapid government action can stand up compliant infrastructure. These programmes standardise protocols and inject capital, lifting the biobank market across multiple regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex & Evolving Regulatory Regimes | -0.9% | Global, with varying intensity by jurisdiction | Medium term (2-4 years) |

| High Total Ownership Cost of Cryogenic Infrastructure | -0.6% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Litigation Over Donor Privacy & Data Ownership | -0.4% | Primarily North America & Europe | Long term (≥ 4 years) |

| Liquid-Nitrogen Price Volatility | -0.3% | Global, with supply chain dependencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex & Evolving Regulatory Regimes

The EU’s Regulation 2024/1938 on substances of human origin will demand major workflow upgrades by 2027. Florida’s 2025 stem-cell statute permits non-FDA-approved therapies if stored in FDA-registered facilities, creating cross-state compliance puzzles. China’s planned relaxation of genetic-resource controls offers growth but brings interim uncertainty. Such divergent rules force biobanks to fund parallel quality systems, adding cost while lengthening approval timelines. Well-capitalised operators gain an advantage, potentially tilting the biobank market toward larger, multinational institutions.

High Total Ownership Cost of Cryogenic Infrastructure

Capital outlays span cryogenic freezers, alarm systems and back-up power, while liquid-nitrogen sourcing remains volatile. Mechanical systems save up to 70% in running costs yet still need specialised maintenance. Failures such as the Cordlife temperature incident required extensive remediation and new staff. In the UAE, regulatory demands pushed banks to build local laboratories, raising entry barriers. These pressures slow footprint expansion in resource-constrained regions, unevenly shaping global biobank market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Automation Drives Infrastructure Evolution

Cryogenic storage systems generated the most significant portion of 48.05% in the biobank market size for equipment in 2025. End users are migrating towards freezers that achieve tighter temperature uniformity and lower energy draw, sustaining a robust 7.78% CAGR. Vendors such as Haier Biomedical introduced wide-neck models with dual-coolant redundancy and touchscreen diagnostics. Alarm and monitoring platforms represent the quickest-moving subsegment because regulators now expect continuous data logging. The arrival of SPT Labtech’s pneumatic arktic XC system reduces manual handling, raising throughput without compromising traceability.

Storage accessories are also evolving. Densely stacked racking and laser-etched barcodes help academic centres squeeze capacity from existing footprints. Mechanical ultra-low freezers offering ±5 °C uniformity are gaining favor as facilities attempt to lower nitrogen usage. Collectively, these shifts point to an equipment landscape where hardware, software and analytics converge, elevating entry requirements for new suppliers and reshaping competition inside the biobank market.

By Application: Regenerative Medicine Leads Dual Growth

Regenerative medicine controlled 36.12% of 2025 revenue and matches that dominance with the fastest 7.02% CAGR through 2031. Drug-discovery applications follow, boosted by collaborations like Thermo Fisher’s proteomics work with the UK Biobank. Disease-surveillance programmes are adopting large-scale sample libraries to map outbreak dynamics, anchoring steady growth. The Tianjin Cord Blood Bank’s cure for aplastic anaemia after 19 years of storage shows that older archives retain high therapeutic value.

Future-oriented programmes, including ARPA-H’s PRINT for 3D-printed organs, create fresh sample requirements. Biobanks hence pivot toward integrated pipelines serving lab-bench discovery and bedside therapy alike. This convergence raises average revenue per sample and extends value chains inside the biobank market.

By Ownership Type: Academic Sector Accelerates Innovation

Public and government operators generated 39.22% of revenue in 2025, owing to long-established repositories and stable funding. Academic and non-profit centres show the quickest 9.28% CAGR on the back of university-industry alliances. Harvard’s Longevity Study banks multifaceted ageing biomarkers, and Germany’s Biobank Alliance links 16 institutions to field 900,000 biosample queries. Private players continue to carve niches in newborn screening, personalised medicine, and logistics services.

Hybrid models are spreading, with public entities hosting base infrastructure while private partners scale analytical platforms. This collaborative fabric diversifies revenue sources, cushions funding cycles and stimulates healthy competition in the biobank market ecosystem.

Geography Analysis

North America generated 35.90% of global revenue in 2025, anchored by FDA guidelines that provide a clear compliance path and by multi-billion-dollar capital commitments from major suppliers. Thermo Fisher is investing USD 2 billion to reinforce domestic cold-chain and analytical production. ATCC’s USD 87 million BARDA contract underscores federal support for pandemic-ready repositories.Continued precision-medicine roll-outs in Canada and heightened clinical-trial activity in Mexico sustain regional sample demand, bolstering revenues for the biobank market.

Europe’s harmonised regulatory approach under Regulation 2024/1938 is stimulating cross-border projects such as the EUR 45 (USD 52) million Genome of Europe initiative. The UK Biobank’s 200,000-genome release cements its status as a flagship data resource. Germany’s federated network processes thousands of requests against 900,000 stored biospecimens, setting a benchmark for operational transparency. Southern European countries leverage EU funding to upgrade freezer capacity and digital-consent tools, broadening sample accessibility across the broader biobank market.

Asia-Pacific is advancing at a 9.72% CAGR, the fastest worldwide. China plans to relax genetic-resource export rules, encouraging multinational R&D partnerships. National cord-blood treatments escalated to nearly 40,000 cases in 2024, proving clinical readiness for banked therapies. Japan remains a leader in allogeneic cord-blood transplants, and SK pharmteco’s USD 260 million Korean facility will expand GMP-grade storage capacity. Australia and South Korea strengthen regional momentum through strong ethics frameworks and translational-research programmes, collectively propelling the biobank market.

Regulatory Landscape

Biobanking regulation is jurisdiction-led, combining specimen safety requirements with privacy and research-ethics obligations. In the United States, FDA activity related to biospecimen handling in clinical research continues to shape operating practices, including the January 2025 draft guidance addressing considerations for tissue biopsies in clinical trials. Institutions also align with the Common Rule framework, including the option of broad consent for future research use of identifiable biospecimens.

In Europe, biobanks process personal data under GDPR alongside national tissue safety legislation, and upcoming compliance changes are being absorbed through quality-system upgrades. ISO 20387:2018 remains a widely used global benchmark for biobanking competence and operational processes, and its ongoing revision work (noted as active in 2025) strengthens the role of standards and accreditation as de facto harmonizers where a single biobank law does not apply across regions.

Competitive Landscape

The biobank market is moderately competitive. A few major players dominate some segments, while others are distributed among multiple players. Large technology vendors are consolidating capabilities to offer end-to-end workflows. Thermo Fisher’s USD 3.1 billion acquisition of Olink enhances proteomics, while the USD 4.1 billion Solventum filtration deal extends upstream bioprocessing. BD partners with Hamilton to integrate automated single-cell sorting into multi-omics pipelines. Cryoport’s takeover of TEC4MED and Bluebird Express gives it 675 active clinical-trial logistics contracts across 17 countries.

Specialists create value by focusing on diversity and decentralisation. Galatea Bio raised USD 25 million to chart genetic diversity in 10 million participants, offering prized datasets for pharma alliances. Johns Hopkins advocates a hybrid model where regional repositories feed into centralised analytics, mitigating diversity gaps seen during COVID-19. Technology differentiation now hinges on AI-driven integrity scoring and blockchain consent networks that optimise chain-of-custody while reducing data silos. These innovations intensify competition yet expand overall capabilities, reinforcing sustainable growth for the biobank market.

Biobank Industry Leaders

Hamilton Company

Thermo Fisher Scientific Inc.

Avantor Inc. (VWR)

BioLife Solutions Inc.

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A niche is forming for high-capacity, automation-heavy facilities that can support both biospecimen custody and data-rich services for multi-omics and precision-medicine workflows. In March 2026, Heidelberg Cell and Liquid Biobank (CLB) inaugurated a large-scale biobank warehouse in Heidelberg with capacity for more than 5 million samples and automated cryopreservation at -196 degrees C, which reflects continued demand for industrialized storage and retrieval. UK Biobank has also advanced its new Manchester Science Park headquarters program, with completion and relocation scheduled for summer 2026 and design capacity that includes advanced robotic freezer systems for up to 20 million samples, which raises expectations for throughput, traceability, and integrated informatics.

A second opportunity centers on publicly backed upgrades to cryogenic infrastructure and compliance tooling, particularly in Europe where funding and harmonization pressures are converging. In March 2026, University Medical Center Halle announced an expansion of its cryogenic warehouse on the Steintor Medical Campus supported by EUR 9.3 million in EU and Saxony-Anhalt funding, with construction slated to start in autumn 2026. These projects create near-term demand for automation platforms, monitoring and audit trails, and sample-quality analytics that help biobanks meet evolving consent and secondary-use governance requirements while servicing pharma and academic users at larger scale.

Recent Industry Developments

- April 2026: Thermo Fisher Scientific initiated a strategic collaboration with Precision Health Research, Singapore (PRECISE) to advance the PRECISE-SG100K population-scale biobank effort involving more than 100,000 participants. The program links biobanking with proteomics at scale, reinforcing demand for standardized sample processing and data integration across large cohorts.

- May 2025: BD launched the FACSDiscover A8 cell analyzer featuring spectral and real-time cell imaging technologies that enable analysis of up to 50 characteristics of a single cell. The release supports higher-content biobank datasets and increases pull-through for downstream multi-omics workflows and biomarker discovery services.

- May 2024: Hamilton Company announced that four high-capacity Hamilton BiOS automated storage systems would be installed in UK Biobank’s new Manchester Science Park headquarters. The installation decision reflects a shift toward robotics-driven cold storage at flagship repositories and accelerates procurement cycles for automated storage and tracking systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the biobank market is defined as revenues linked to setting up and running biorepositories that collect, process, store, and distribute human biospecimens for research and clinical use, including related equipment, consumables, and services.

Scope exclusions: Veterinary, forensic, fertility-clinic, and human-tissue transplant banking activities are excluded from this market sizing.

Segmentation Overview

- By Product

- Cryogenic Storage Systems

- Refrigerators

- Freezers

- Ice Machines

- Alarm & Monitoring Systems

- Media & Consumables

- Cryogenic Storage Systems

- By Application

- Regenerative Medicine

- Drug Discovery

- Disease & Epidemiology Research

- Life-Science & Genomic Research

- By Ownership Type

- Public/Government

- Academic/Non-profit

- Private & Commercial

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic structure of the market and to set realistic input ranges before we spoke to industry participants. We relied on public sources such as the World Health Organization, OECD health statistics, the US National Institutes of Health, the US Centers for Disease Control and Prevention, and the European Commission and related public health portals for background indicators connected to sample collection, research intensity, and healthcare capacity.

To translate that context into sizing inputs, we also reviewed company filings, investor presentations, press releases, peer reviewed journals on biorepository operations, and biobank network and association websites that publish participation and program updates. In a few places, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used to cross-check revenue splits, ownership structures, and technology adoption signals. These examples are not exhaustive, and many other public and subscription sources were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to confirm what is counted as a biobank revenue stream in practice, and to test assumptions on utilization and pricing that are not visible in public data. We spoke with operators of public and private repositories, lab managers, procurement teams, and service providers across the Americas, EMEA, and APAC so the model could be checked against real workflows, funding patterns, and shipment and storage behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 18% | APAC: 48% |

| Mid tier: 49% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 18% | Managers: 53% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach. The top-down view starts from the demand pool for stored and processed human biospecimens and then reconstructs revenue using observable activity signals. In practice, the model is anchored on indicators such as clinical research activity, life science R&D funding direction, biobank participation footprints, sample inflow and retrieval patterns, and cold storage capacity additions.

Once that structure is in place, selective bottom-up checks are used to keep totals realistic, including supplier revenues tied to biobank equipment and consumables, service pricing ranges for processing and storage, and channel checks on typical contracts by end-user type. Where bottom-up visibility is uneven, gaps are handled by applying conservative penetration and utilization rates by region and by correcting for double counting between equipment sales and service bundles.

For the forecast, scenario analysis is used because growth depends on a small set of high-impact drivers that can move together. Inputs such as changes in research funding cycles, expansion of precision medicine programs, regulatory and consent practices affecting sample availability, and the pace of automation in repositories were stress tested with interview feedback, and then applied to regional trajectories before rolling up to the global total.

Data Validation & Update Cycle

Validation is done in layers so that no single data point overly steers the final number. Model outputs are compared against independent signals such as funding trends, repository expansion announcements, and directionally consistent regional adoption patterns. Large variances are then reviewed for input errors or scope mismatches.

Before sign-off, a second analyst review is completed, and follow-up outreach is triggered if a key assumption (like utilization or average service pricing) appears out of line with multiple interview statements. Reports are refreshed annually, with interim updates when material events occur that can shift demand or pricing. Right before delivery, a fresh check is performed so the client receives the latest updated view.

Mordor Intelligence's Global Biobank Market Sizing Compared With Other Published Estimates

Published biobank market sizes often do not match because authors are not always counting the same revenue streams, and they can also use different base years and currency timing. Differences also show up when some studies mix adjacent banking activities into one total, while others keep them separate and only count human biospecimen repository operations.

The main gap drivers here are scope and how activity is converted into dollars. Some estimates fold in areas like fertility or transplant banking and then apply broad growth rates to a wider pool. Another driver is refresh cadence and scenario choice, because aggressive adoption assumptions for automation, storage expansion, or clinical research growth can lift a 2024 base more quickly than a steadier case.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 58.08 B (2026) | |

| Industry Publisher A | USD 75.40 B (2024) | Uses a broader scope that explicitly includes software along with products and services, and it anchors sizing to a 2024 base year, which shifts the level versus a later-year estimate and may capture adjacent revenue categories. |

| Research Publisher B | USD 83.05 B (2024) | Reports a higher 2024 value that likely reflects wider inclusions across biobanking types, ownership models, and storage categories, and it can also be influenced by faster assumed uptake of services and pricing progression without the same exclusion filters. |

The table shows that the spread is largely explained by what gets counted and the year used for the stated value. By keeping exclusions explicit and tying revenue back to repository operations and human biospecimen handling activities, the estimate stays easier to reproduce and audit, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the biobank market?

The market is valued at USD 58.08 billion in 2026 and is set to reach USD 73.87 billion by 2031.

Which segment shows both the largest share and the fastest growth?

Regenerative medicine accounts for 36.12% of revenue and leads growth with a 7.02% CAGR through 2031.

Why is Asia-Pacific considered the growth engine for biobanking?

Regional reforms that relax genetic-resource rules, rising cord-blood utilisation and major infrastructure projects together underpin a 9.72% CAGR for Asia-Pacific.

How are regulatory changes affecting global biobanking operations?

New standards in the EU, policy shifts in the United States and evolving rules in China require biobanks to update quality systems and invest in compliance, raising operating costs but improving safety.

What technologies are shaping the next phase of the biobank market?

Automation, AI-driven sample-quality analytics, blockchain consent management and room-temperature DNA storage are the main technologies redefining workflows and lowering long-term costs.

Page last updated on: