Consumer Credit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.1 Billion |

| Market Size (2031) | USD 18.28 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

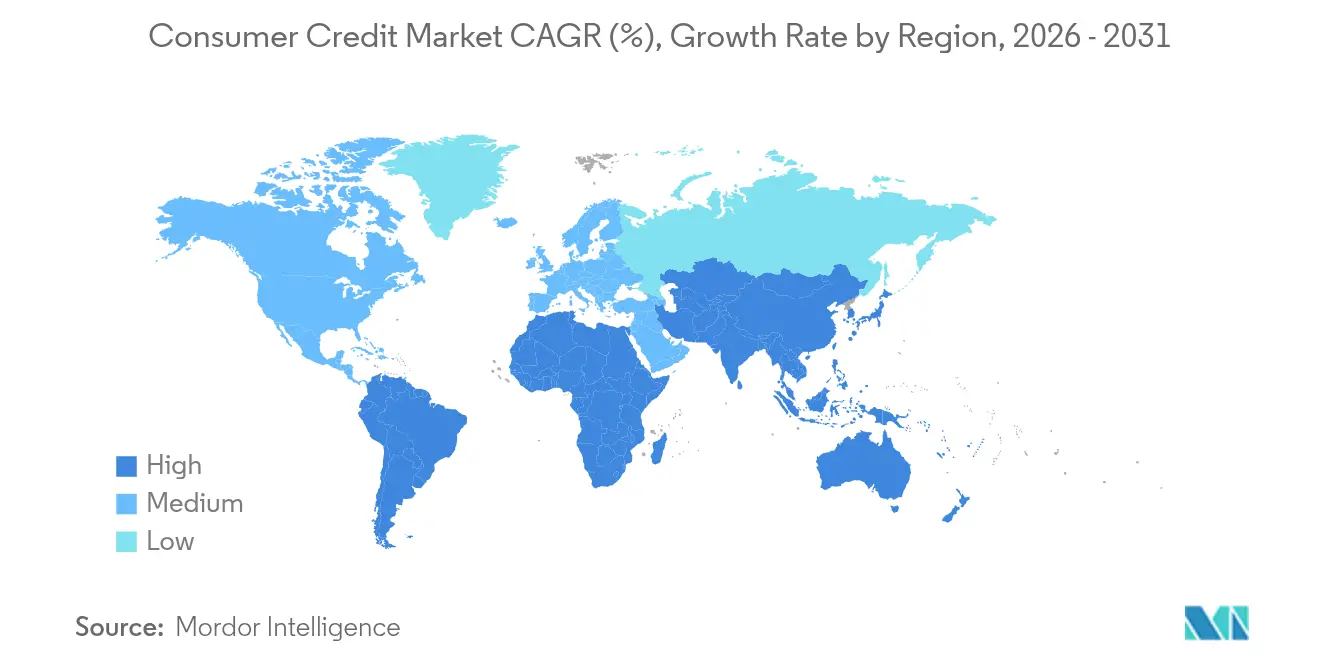

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Credit Market Analysis by Mordor Intelligence

Consumer Credit Market size in 2026 is estimated at USD 14.1 billion, growing from 2025 value of USD 13.39 billion with 2031 projections showing USD 18.28 billion, growing at 5.32% CAGR over 2026-2031.

This steady expansion signals the mainstreaming of fintech-enabled lending models that rely on alternative data and real-time payment rails, eroding the historical dominance of branch-centric banks and card networks. Competition now pivots on the relative speed at which issuers integrate buy-now-pay-later (BNPL) features, real-time payment settlement, and API-based underwriting while satisfying tightening regulatory expectations on data privacy and algorithmic fairness. Rising global policy rates compress net interest margins, yet the revenue outlook remains favorable because new risk-management tools based on tokenized collateral and machine-learning analytics lower credit-loss volatility. At the same time, regional growth differentials widen as Asia-Pacific’s smartphone-centric consumers adopt digital wallets and embedded credit at a pace that outstrips North America’s maturing card market.

Key Report Takeaways

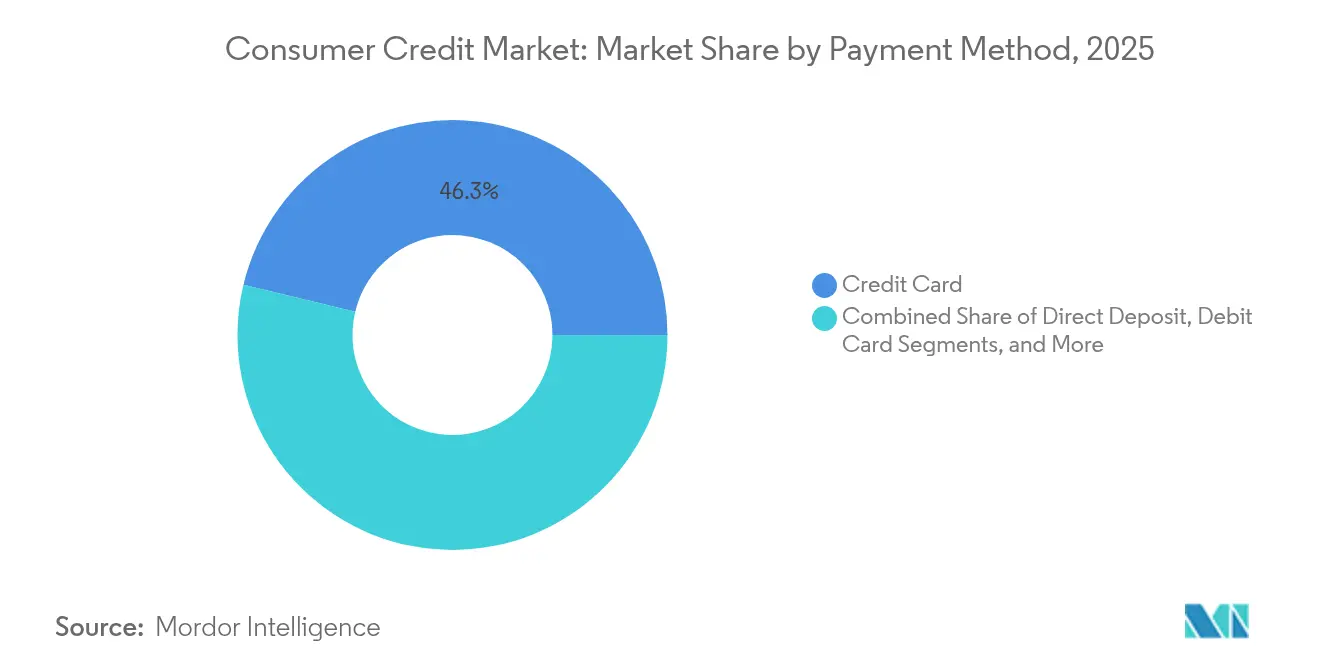

- By payment method: Credit cards led with 46.25% of consumer credit market share in 2025, while BNPL platforms are projected to grow at a 9.24% CAGR through 2031.

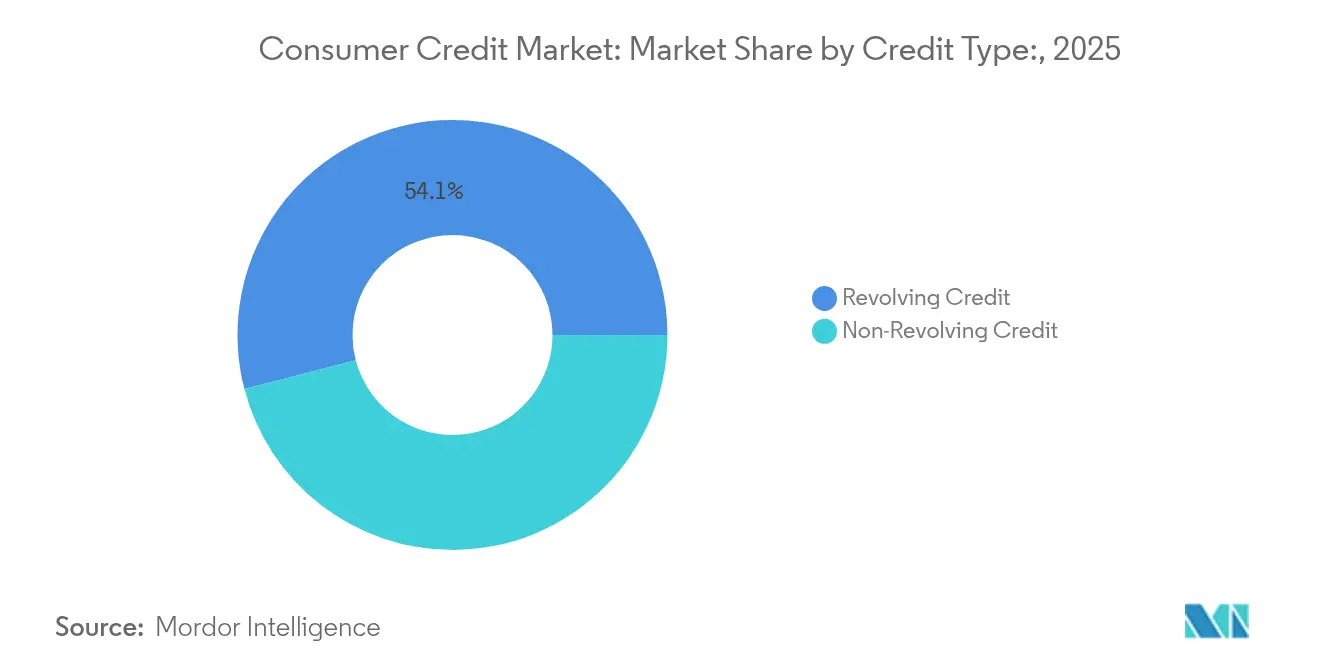

- By credit type: Revolving products accounted for 54.05% share of the consumer credit market size in 2025; fintech-originated installment loans are on track to expand at an 7.78% CAGR to 2031.

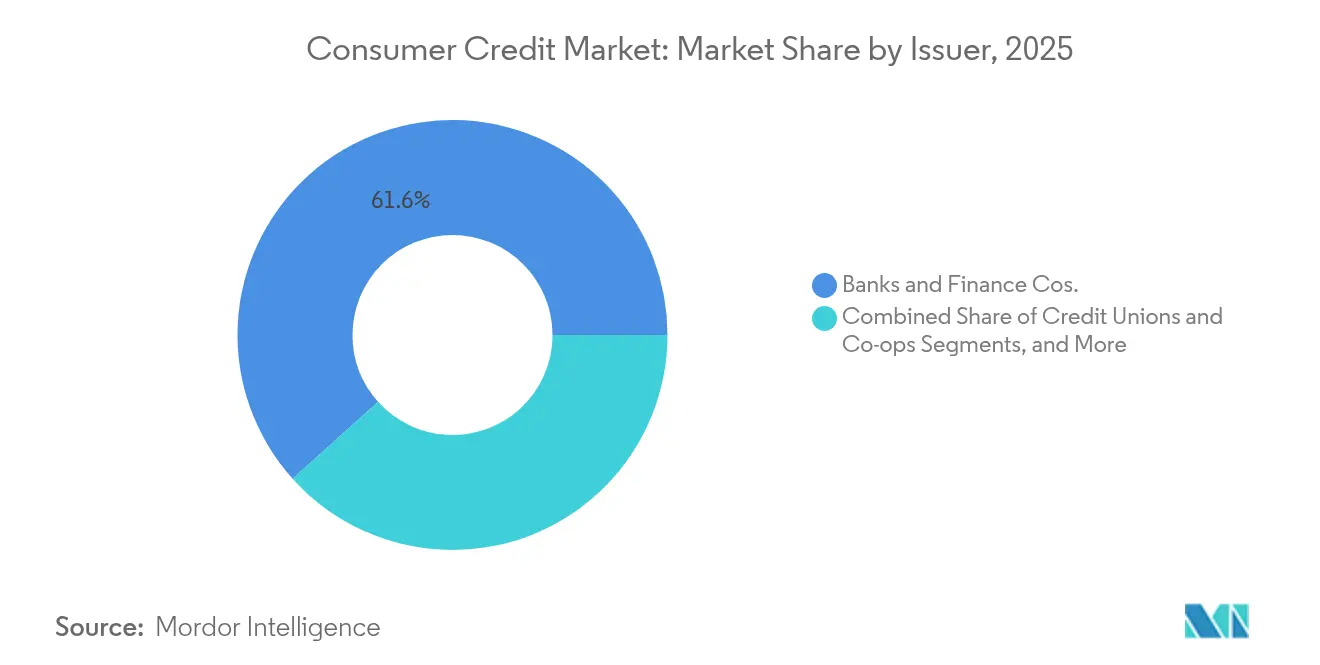

- By issuer: Banks and finance companies retained 61.65% of the consumer credit market share in 2025, yet fintech and neo-lenders post the highest issuer-level CAGR at 10.05%.

- By geography: North America held a 38.45% share of the consumer credit market size in 2025, but Asia-Pacific is the fastest-growing region at a 12.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Consumer Credit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fintech-enabled digital lending boom | +1.2% | Global, with Asia-Pacific leadership | Medium term (2-4 years) |

| Explosive e-commerce and BNPL adoption | +0.9% | North America and EU core, Asia-Pacific acceleration | Short term (≤ 2 years) |

| Real-time payments integration | +0.7% | Global, advanced in Asia-Pacific and EU | Medium term (2-4 years) |

| Financial-inclusion regulation push | +0.6% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Alternative-data credit scoring models | +0.5% | Global, early adoption in North America | Medium term (2-4 years) |

| Tokenized-asset collateralization | +0.3% | North America and EU, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fintech-enabled Digital Lending Boom

Automated underwriting, cloud-native loan-servicing stacks, and institutional marketplace funding have allowed digital lenders to originate loans in minutes rather than days. LendingClub originated USD 1.85 billion of consumer loans in Q4 2024, a 13% year-over-year increase, after shifting from peer-to-peer deposits to bank-chartered funding that supports scale and compliance. Many platforms replicate that model, using machine-learning algorithms to evaluate cash-flow data and social signals so they can serve thin-file or no-file borrowers at competitive yields. Traditional banks respond by opening API gateways and partnering with fintechs to retain customers who now expect near‐instant credit decisions. Regulatory attention, however, intensifies as the Consumer Financial Protection Bureau (CFPB) probes algorithmic bias, forcing lenders to hard-wire explainability into models without diluting speed advantages.[1]Consumer Financial Protection Bureau, “CFPB Takes Action Against Lenders for Algorithmic Bias,” consumerfinance.gov

Explosive E-commerce and BNPL Adoption

Point-of-sale installment plans are reshaping checkout flows and shifting volume away from revolving cards. Klarna reported SEK 216 million in net income for Q3 2024 and readied a USD 15 billion IPO, demonstrating that the BNPL model can reach profitability even under stricter capital rules.[2]Klarna, “Financial Results Q3 2024,” kla.rna.com (via pymnts.com)Because the CFPB now classifies BNPL plans as credit cards, providers must deliver billing statements, dispute resolution, and Reg Z disclosures, raising cost but also creating clearer operating rules. Merchant adoption grows because conversion lifts offset the interchange fees associated with cards, and younger shoppers favor zero-interest installments over high-APR revolvers. Card networks counter by embedding installment options within existing credentials, but the consumer credit market continues to fragment as retailers seek multi-rail flexibility at checkout.

Real-Time Payments Integration

Instant settlement underpins on-demand credit products such as earned-wage access, micro-loans, and dynamic credit-line adjustments. PayPal’s tie-up with Synchrony Financial routes approved credit into real-time payments pipes, letting consumers fund purchases without waiting for batch clearing. In Asia-Pacific, FPS in Hong Kong and UPI in India set usage benchmarks that push global lenders toward 24/7 infrastructure. Real-time risk scoring cuts fraud losses by matching identity verification with tokenized payment credentials, improving margins even as network costs fall. Smaller lenders face formidable barriers because always-on ledgers, redundant cloud zones, and zero-downtime security monitoring require capex that only scaled players or deep-pocketed tech partners can afford.

Financial-Inclusion Regulation Push

Governments are mandating easier credit access for “credit invisibles” through open-banking frameworks, cross-border data portability, and calibrated interest-rate caps. Equifax Canada launched a global consumer credit file that lets newcomers port overseas histories into the domestic scoring ecosystem, tackling the prime-thin diaspora segment that lacked formal credit options.[3]Equifax Canada, “Global Consumer Credit File Launch,” consumer.equifax.ca In emerging Asia-Pacific, regulators embed financial-inclusion targets within digital-bank licensing, spurring mobile-first lenders to incorporate utility bills, rent, and super-app wallet flows into underwriting. Developed jurisdictions focus on algorithmic fairness and robust opt-in disclosures, but the policy thrust remains additive: more data points can qualify more borrowers without degrading portfolio risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global policy rates and cost-of-funds | -1.1% | Global, most acute in developed markets | Short term (≤ 2 years) |

| Household debt over-extension and delinquencies | -0.8% | North America and EU core, emerging in Asia-Pacific | Medium term (2-4 years) |

| Data-privacy curbs on alternative data | -0.4% | EU leadership, spreading to North America | Medium term (2-4 years) |

| Regulatory scrutiny of algorithmic bias | -0.3% | North America and EU, pilot enforcement in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Policy Rates and Cost-of-Funds

Successive hikes by the Federal Reserve and other major central banks transfer directly into higher credit-card APRs, constricting demand for fresh balances and nudging borrowers toward payoff or refinancing. OECD analysis shows that wholesale funding spreads widened more quickly for non-deposit fintech lenders than for universal banks in 2024, eroding the cost advantage that marketplace platforms once enjoyed.[4]Organisation for Economic Co-operation and Development, “Interest-Rate Risk in Consumer Lending,” oecd.org Scale becomes critical: Capital One’s USD 35.3 billion acquisition of Discover grants the combined entity deeper funding pools and integrated payment rails that insulate margins in a high-rate regime. Smaller players with monoline revenue streams must either securitize at less favorable coupons or exit the market, accelerating consolidation.

Household Debt Over-Extension and Delinquencies

Credit-card charge-off rates have trended upward every quarter since mid-2024 as pandemic-era savings buffers dissipated and inflation squeezed discretionary budgets, forcing issuers to raise loss reserves. Delinquency risk is magnified in BNPL, where multiple short-tenor plans create hidden leverage not always captured in traditional bureau files. Younger borrowers facing variable gig-economy incomes are most vulnerable, and lenders that rely heavily on synthetic identity scores see higher fraud write-offs. Rising loss provisioning pushes ROA lower, prompting underwriters to tighten credit boxes, limit promotional offers, and prune credit-line extensions, which in turn tempers expansion across the consumer credit market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Method: BNPL Disrupts Traditional Card Dominance

The consumer credit market size for payment methods skewed toward credit cards in 2025, when those instruments still held a 46.25% share alongside decades-old merchant acceptance networks. Card issuers exploit loyalty ecosystems, co-branded partnerships, and pervasive contactless standards to lock in revolving balances and fee revenue. Yet BNPL entities expand at a 9.24% CAGR by embedding no-interest installments directly into e-commerce carts, appealing to Gen Z shoppers wary of long-term debt. Klarna, Afterpay, and Affirm broaden merchant reach through plug-in SDKs that reduce integration friction and offer real-time underwriting at checkout. The card giants counter with post-purchase installments that repackage existing balances into fixed-tenor plans, blurring categorical lines but preserving interchange flows.

BNPL’s advance forces merchants to juggle multiple rails, leading enterprise gateways to aggregate card, wallet, BNPL, and bank-transfer options inside unified APIs. That shift fragments transaction data, but providers leveraging artificial intelligence reconcile cross-channel purchase histories into single-view credit profiles. Meanwhile, direct-deposit and debit products attract rate-sensitive consumers who prefer immediate settlement amid rising APRs, although their growth pace remains subdued relative to installment offers. Cryptocurrency and peer-to-peer payment methods are still niche, but they outstrip overall market growth in regions where capital controls or under-banked populations create demand for alternative rails. Card networks now invest in BNPL white-label programs and tokenized wallet connectors to defend relevance, illustrating the payment sphere’s fast-evolving dynamics within the wider consumer credit market.

By Credit Type: Installment Products Challenge Revolving Supremacy

Revolving balances represented 54.05% of the consumer credit market share in 2025 as credit cards continued to finance everyday spending and discretionary purchases that benefit from flexible repayment. The interest-bearing nature of cards and their minimum-payment structure yield lucrative net interest margins that underpin bank profitability. Fintech-originated installment loans, however, compound at an 7.78% CAGR through 2031 by addressing large-ticket purchases, debt-consolidation needs, and borrowers who value predictable fixed payments. LendingClub’s USD 1.85 billion fourth-quarter 2024 originations underscore soaring institutional appetite for installment receivables that exhibit shorter duration and granular performance data.

Product boundaries blur further because major card issuers now pre-approve installment plans on existing card limits, seamlessly converting revolvers into structured pay-offs when interest rates surge. Regulators have responded by extending Truth in Lending Act protections to BNPL-styled installment credit, creating a compliance parity that may narrow cost advantages but legitimizes the format inside mainstream lending. Fintech originators differentiate through proprietary risk models that ingest cash-flow telemetry and real-time banking feeds, thus expanding the consumer credit market to millions of sub-prime or near-prime households previously priced out by FICO-centric rules. The confluence of predictable repayment structures and expanded scoring inputs suggests continued momentum for installment credit even as macro headwinds rise.

By Issuer: Fintech Platforms Gain Ground on Banking Giants

The incumbent banking sector still controlled 61.65% of the consumer credit market size in 2025, thanks to regulatory charters, insured deposit funding, and legacy customer trust. Yet fintech and neo-lenders outpace traditional peers with 10.05% CAGR growth by leveraging mobile-first onboarding, frictionless UX, and embedded finance distribution. Capital One’s strategy to fold Discover’s network into its card franchise illustrates how banks use M&A to acquire scale, close technology gaps, and negotiate network fees. Conversely, fintech platforms pursue limited bank charters or partner-bank models to gain direct deposit access, thereby lowering their cost of funds and enabling competitive APRs.

Peer-to-peer lenders largely ceded retail funding after liquidity tightened in 2024’s rate environment, aligning instead with insurance companies, pension funds, and asset managers seeking granular exposure to consumer receivables. As the line between bank and fintech blurs, the consumer credit industry sees joint ventures where incumbents supply balance-sheet heft while technology partners deliver algorithmic underwriting and customer experience design. Credit unions and co-operatives maintain stable, if slower, growth through member-first service and rate-capped products, but even they deploy open banking APIs to stay relevant among digital-native members. The resulting issuer ecosystem is multilateral, with cooperative, bank, fintech, and big-tech players co-existing and often collaborating to capture value across the consumer credit market.

Geography Analysis

North America’s 38.45% share of the consumer credit market in 2025 stems from its extensive card penetration, deep revolving products, and mature credit-bureau infrastructure. Regulatory scrutiny has intensified since the CFPB fined Equifax USD 15 million in January 2025 for persistent file inaccuracies, prompting industry-wide investment in dispute resolution automation and algorithm explainability. The Capital One-Discover merger further resets competitive benchmarks, combining a large issuing base with an in-house payment network that could shift interchange economics. Canada follows a more inclusive path by importing international bureau data, an initiative that smooths immigration-driven population growth and supports incremental loan demand. Mexico, meanwhile, offers expansion prospects through rising formal-sector employment and cross-border e-commerce, yet must navigate interest-rate volatility linked to U.S. monetary policy.

Asia-Pacific delivers the fastest regional expansion, clocking a 12.15% CAGR as smartphone adoption and super-app ecosystems converge to remove frictions in credit origination. China exemplifies scale: QR-code wallets from Alipay and WeChat create embedded credit loops that auto-populate loan applications with real-time purchase data. India’s Unified Payments Interface, coupled with Aadhaar-enabled KYC, propels thin-file borrowers into formal credit channels, spurring explosive growth in micro-credit and BNPL. High-income markets such as Japan and South Korea emphasize robo-advisory features and near-zero-second approvals, while Southeast Asian nations adopt regulatory sandboxes that allow start-ups to test alternative-data models under supervisory observation. Australia and New Zealand, though smaller in population, prioritize consumer-protection enhancements within open-banking schemas, balancing innovation with prudential safeguards.

Europe’s consumer credit landscape centers on the Payment Services Directive and sweeping GDPR rules that shape data use. Open-banking APIs enable third-party aggregators to access transaction data, fostering competitive loan offers that can quickly transfer balances between lenders. The United Kingdom’s post-Brexit regime retains passport-like recognition of EU data flows but adds domestic sandboxes to encourage AI-driven scoring that meets fairness metrics. Germany and France, with conservative lending cultures, see slower volume growth but higher asset quality as borrowers favor installment products over revolvers. Southern European markets such as Spain and Italy lean on fintech-bank partnerships to revive credit growth amid lingering macro uncertainty. Across the continent, geopolitical risks—from energy supply shocks to war-related sanctions—add prudence to underwriting, but the structural shift toward digitization continues to pull share from paper-centric processes in the wider consumer credit market.

Competitive Landscape

The consumer credit industry presents a moderately concentrated profile with traditional banks, card networks, and pure-play fintechs locked in continual competitive realignment. Banks rely on charter advantages, low-cost deposits, and diversified earnings, yet must overhaul legacy cores to replicate real-time experiences offered by digital natives. Card networks Visa and Mastercard feel the dual squeeze of alternative rails—BNPL, RTP, account-to-account transfers—and the emergence of the Capital One–Discover integrated issuer-network model. Fintechs differentiate on speed, personalization, and access for credit-invisible consumers, but higher funding costs push smaller players toward either niche specialization or acquisition.

Strategic moves center on technology adoption and data house-keeping. Lenders integrate machine-learning fraud filters and cloud micro-services, allowing them to update credit policies in hours rather than weeks. Alternative-data usage—utility payments, mobile top-ups, gig-economy earnings—opens new risk pools but triggers privacy audits in GDPR jurisdictions. M&A activity reflects a hunt for scale-driven unit-economics: banks buy fintech platforms to obtain underwriting IP; fintechs seek bank charters to capture cheap deposits. Simultaneously, point-of-sale platforms embed credit within retailer ecosystems, giving them bargaining power over interchange fees and steering high-margin traffic away from traditional issuers.

Competitive intensity is reinforced by policy tightening. Regulators demand transparent explainability for AI credit decisions, M&Ating robust model governance that increases compliance costs. Larger institutions amortize this spend across vast portfolios, whereas start-ups form consortia for shared audit tooling. The proliferation of tokenized collateral pilots—secured by blockchain smart contracts—signals future differentiation in asset-backed segments. Players capable of pairing API-driven distribution with fortress-level compliance stand to consolidate share as capital markets reward durable, transparent growth inside the consumer credit market.

Consumer Credit Industry Leaders

American Express Company

JPMorgan Chase

Capital One

Visa

Mastercard

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Capital One completed its USD 35.3 billion acquisition of Discover Financial Services, creating the largest credit-card issuer by outstanding balances and integrating Discover’s payments network to challenge Visa-Mastercard dominance.

- May 2025: VantageScore launched version 4.0+ that integrates open-banking data, promising a 10% uplift in predictive power and broader inclusion.

- February 2025: Equifax Canada rolled out a global consumer credit file to help newcomers import overseas histories into domestic scoring.

- January 2025: The CFPB fined Equifax USD 15 million over credit-report inaccuracies, underscoring regulatory focus on data quality in consumer reporting.

Global Consumer Credit Market Report Scope

Consumer credit is the term used to define an unsecured debt that was taken to purchase goods and services. It is used to finance the purchase of commodities or services for personal consumption or to refinance debts incurred for such purposes.

The consumer credit market is segmented by payment method (direct deposit, debit card, other payment method), by credit type (revolving credits, non-revolving credits), by issuer (banks and finance companies, credit unions, other issuers), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Direct Deposit |

| Debit Card |

| Credit Card |

| Digital Wallets |

| Buy-Now-Pay-Later (BNPL) |

| Other Payment Methods |

| Revolving Credit |

| Non-Revolving Credit |

| Banks and Finance Companies |

| Credit Unions and Co-ops |

| Fintech and Neo-lenders |

| Peer-to-Peer Platforms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Payment Method | Direct Deposit | ||

| Debit Card | |||

| Credit Card | |||

| Digital Wallets | |||

| Buy-Now-Pay-Later (BNPL) | |||

| Other Payment Methods | |||

| By Credit Type | Revolving Credit | ||

| Non-Revolving Credit | |||

| By Issuer | Banks and Finance Companies | ||

| Credit Unions and Co-ops | |||

| Fintech and Neo-lenders | |||

| Peer-to-Peer Platforms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the consumer credit market in 2026?

The consumer credit market size is USD 14.1 billion in 2026 and is projected to grow at a 5.32% CAGR to USD 18.28 billion by 2031.

Which payment method is growing fastest?

BNPL platforms are the fastest-growing payment method segment, expanding at a 9.24% CAGR through 2031 on the back of e-commerce integration and zero-interest installments.

What region offers the strongest growth outlook?

Asia-Pacific leads with a 12.15% CAGR, driven by mobile-first platforms, government inclusion initiatives, and widespread smartphone adoption.

How are rising interest rates affecting lenders?

Higher policy rates elevate funding costs, squeeze net interest margins, and prompt lenders to tighten underwriting standards, especially among non-deposit fintechs.

Why is the Capital One-Discover deal significant?

The USD 35.3 billion merger fuses a major issuer with its own payment network, potentially altering interchange economics and competitive dynamics with Visa and Mastercard.

Page last updated on: