Financial Services Application Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

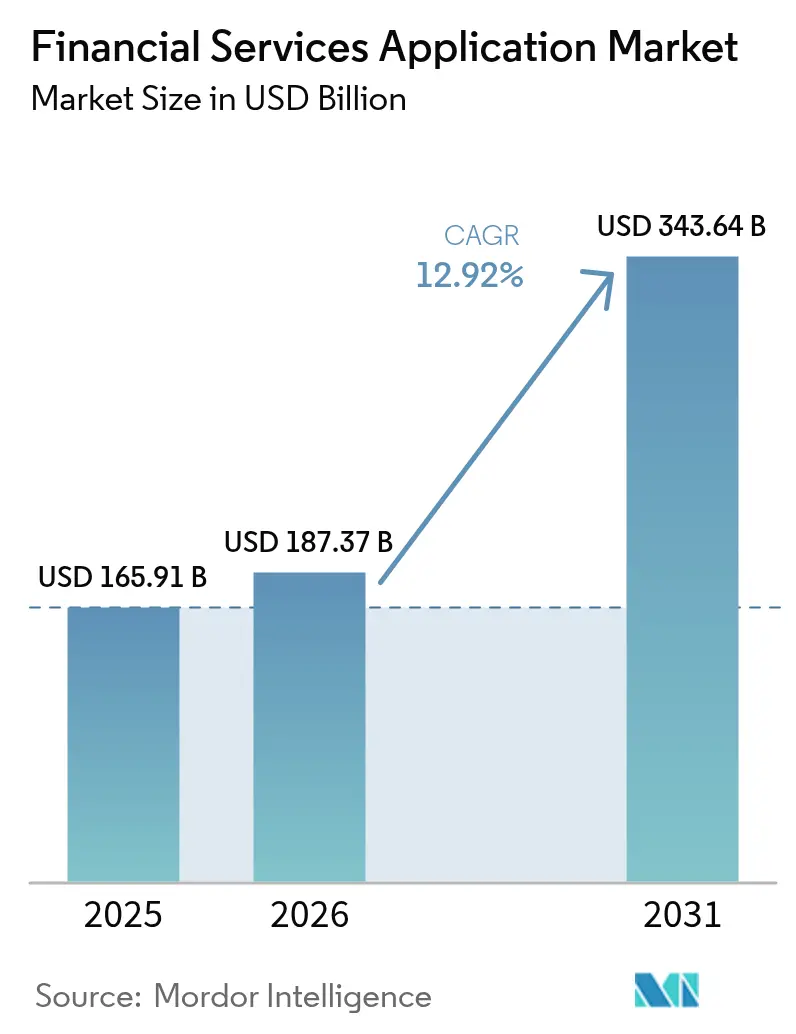

| Market Size (2026) | USD 187.37 Billion |

| Market Size (2031) | USD 343.64 Billion |

| Growth Rate (2026 - 2031) | 12.92% CAGR |

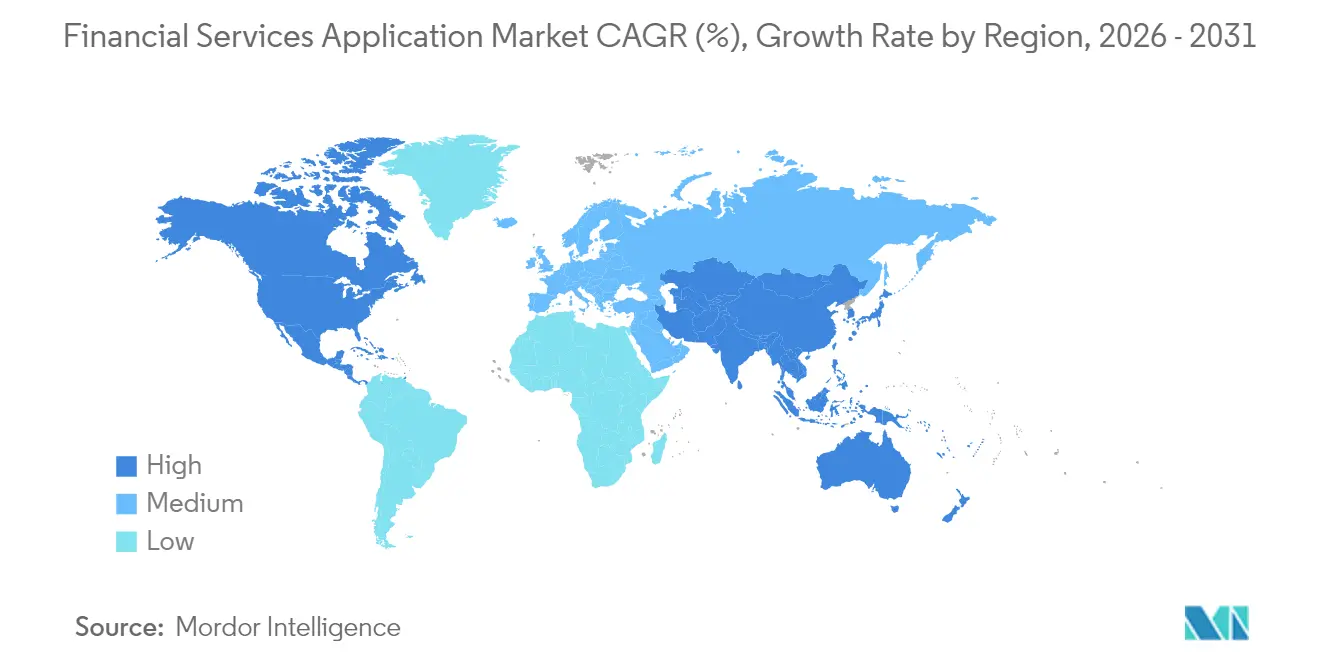

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Financial Services Application Market Analysis by Mordor Intelligence

The financial services applications market size was valued at USD 165.91 billion in 2025 and estimated to grow from USD 187.37 billion in 2026 to reach USD 343.64 billion by 2031, at a CAGR of 12.92% during the forecast period (2026-2031). Strong demand stems from regulatory deadlines, cloud-native architectures and AI-enabled customer experience tools that together redefine how institutions build and operate their technology stacks. Software-defined banking, real-time payment rails and open-banking mandates are pushing buyers toward platform ecosystems that replace fragmented point solutions. Vendors that blend AI, analytics and low-code workflow engines into a single environment are capturing share as banks, insurers and capital-markets firms prioritize speed, compliance and personalization. Meanwhile, robust venture funding and large-scale partnerships have reduced barriers to entry, enabling specialist fintech providers to introduce niche capabilities that plug easily into core platforms.

Key Report Takeaways

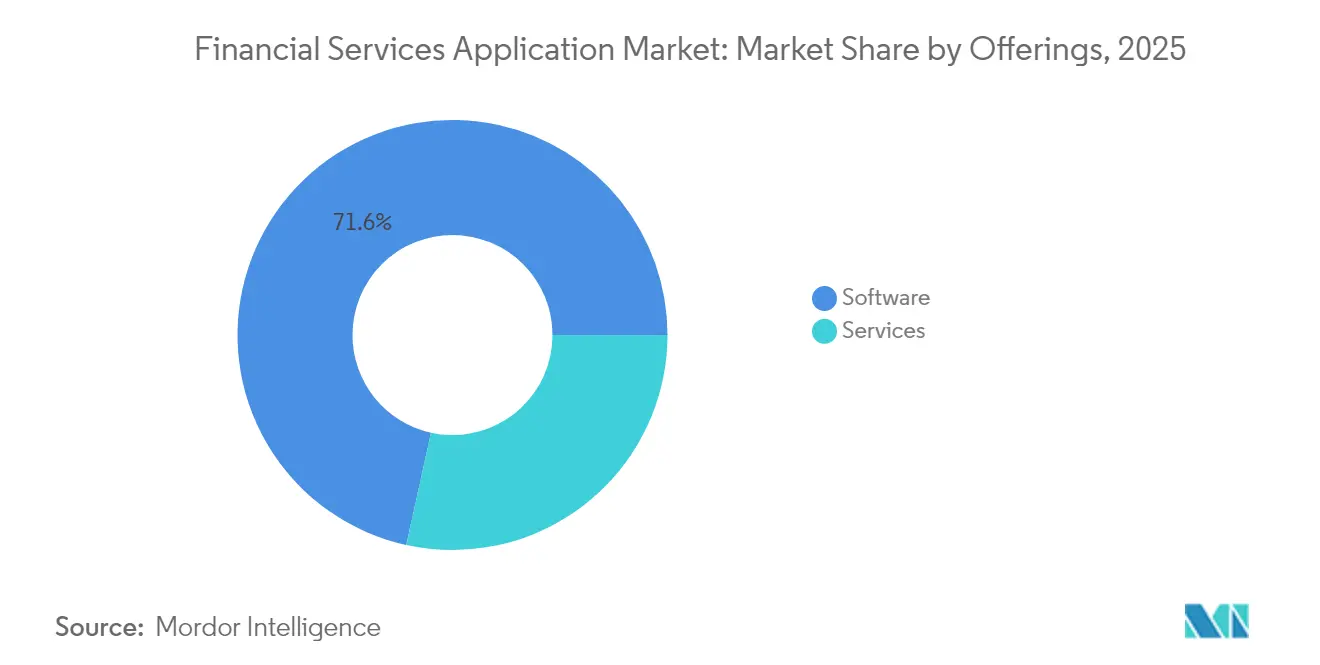

- By offering, software accounted for 71.55% revenue in 2025; BI, analytics & AI suites are expanding at a 14.32% CAGR through 2031.

- By deployment, cloud models captured 63.05% share in 2025, while public-cloud usage is rising at 17.55% CAGR to 2031.

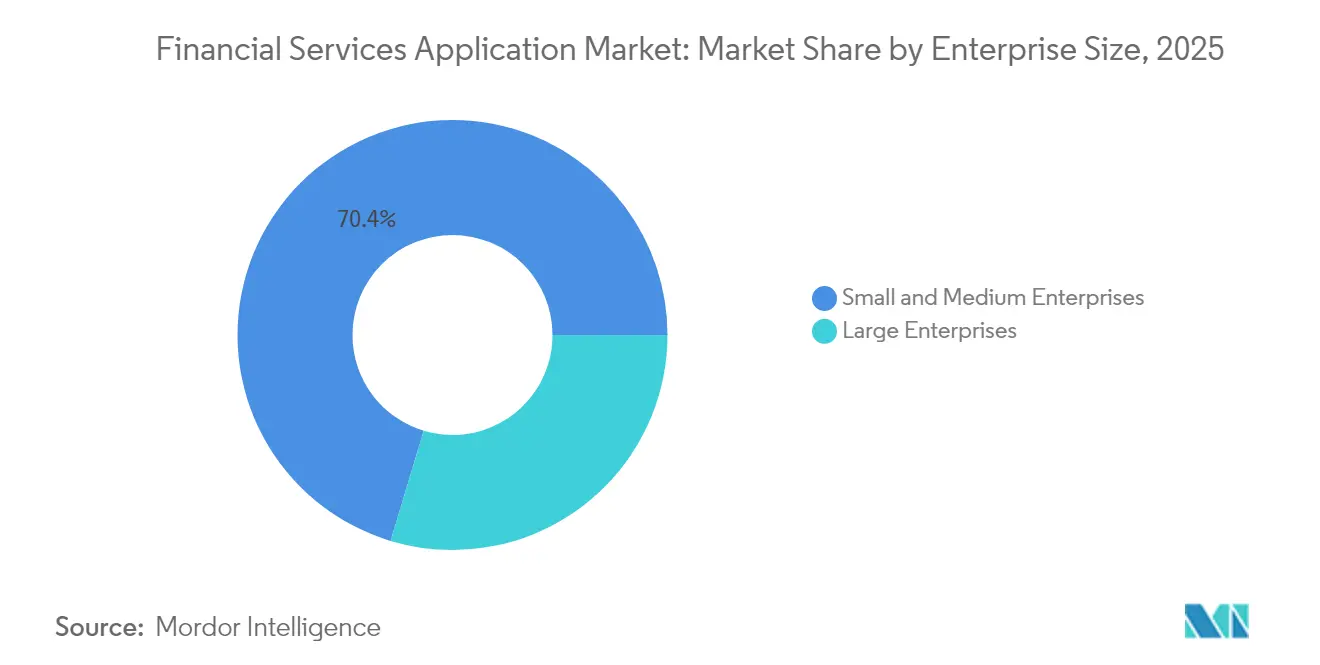

- By enterprise size, large institutions commanded 29.65% revenue in 2025;SMEs show the fastest 15.05% CAGR to 2031.

- By end-user, banks held 70.62% of demand in 2025, whereas fintech and neo-banks are advancing at 14.92% CAGR through 2031.

- By geography, North America led with 37.85% share in 2025; Asia-Pacific is projected to grow the quickest at 12.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Financial Services Application Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cloud-first core modernisation | +3.2% | North America, Europe | Medium term (2-4 years) |

| AI-driven hyper-personalisation | +2.8% | Global, strongest in Asia-Pacific | Long term (≥ 4 years) |

| Open-banking APIs | +2.1% | Europe expanding to North America and Asia-Pacific | Short term (≤ 2 years) |

| Regulatory push for real-time payments | +1.9% | Global, staggered by market | Medium term (2-4 years) |

| Alternative data monetisation | +1.4% | North America, Europe emerging in Asia-Pacific | Long term (≥ 4 years) |

| Quantum-secure cryptography pilots | +0.8% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Cloud-First Core Modernisation Among Tier-1 Banks

Legacy cores restrict scalability, so leading banks are shifting workloads to cloud-native engines that support embedded finance, real-time analytics and continuous deployment. Commerce Bank’s go-live on a Temenos platform cut product launch cycles from months to weeks and illustrated how elastic infrastructure improves customer experience [1]Temenos, “Commerce Bank Goes Live on Temenos Banking Platform,” temenos.com. European and North American institutions are renegotiating outsourcing contracts to accelerate decommissioning of on-premise stacks, freeing capital for innovation. Regulators have clarified that public-cloud usage is acceptable if operational-resilience rules are met, further unlocking budgets. As migration templates mature, mid-tier lenders can reuse proven blueprints, widening the addressable financial services applications market[2]Temenos, “Commerce Bank Goes Live on Temenos Banking Platform,” temenos.com.

AI-Driven Hyper-Personalisation to Lift Share-of-Wallet

Banks now embed generative AI directly inside their core workflow to craft context-aware offers, nudge savings behaviour and price risk dynamically. Temenos’ secured AI module runs inference in real time and meets banking-grade privacy rules, helping lenders tailor messages that raise product adoption. Asia-Pacific institutions are pairing alternative data—such as gig-economy income feeds—with AI scoring to reach first-time borrowers. Early adopters report double-digit gains in cross-sell ratios, proving that algorithmic personalisation lifts revenues faster than rate promotions. Continual model-monitoring remains essential, yet institutions that link AI to clean data pipelines are widening the service gap with slower peers.

Open-Banking APIs Catalysing Fintech–Bank Collaboration

EU payment-service directives forced banks to open customer data through standard APIs, transforming data from proprietary asset to collaboration currency. Third-party developers now weave account-aggregation, instant lending and budgeting tools straight into consumer apps, broadening engagement while lowering acquisition cost for incumbents [ECB.EUROPA.EU]. North American regulators are drafting similar rules, and sandbox pilots across Asia-Pacific indicate broad global uptake. Banks that pivot to API-first architectures tap fee income from ecosystem partners rather than compete head-on, making open-banking a durable growth lever for the financial services applications market.

Regulatory Push for Real-Time Payment Rails

Mandates such as the EU Instant Payments Regulation oblige every bank to process euro transfers in seconds by 2025, triggering platform overhauls well beyond the payment module. Commerce Bank’s launch of FedNow through its Temenos stack showed that risk analytics, fraud controls and liquidity tools must all run in real time. Tight implementation windows accelerate procurement decisions, and vendors offering pre-integrated modules gain a decisive edge. Markets that already completed roll-outs, like India and Brazil, demonstrate sustained transaction-volume growth that justifies the upgrade spend, locking in multi-year software contracts.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating core-banking migration costs | -2.4% | Global, higher in developed markets | Medium term (2-4 years) |

| Vendor lock-in and multi-cloud complexity | -1.8% | Global, impacts large enterprises | Long term (≥ 4 years) |

| Scarcity of domain-ready Gen-AI data | -1.3% | Varies by privacy regime | Short term (≤ 2 years) |

| Post-quantum compliance uncertainty | -0.9% | Security-sensitive sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Core-Banking Migration Costs

Banks budgeting only for licence fees often discover that data cleansing, parallel runs and staff retraining multiply total spend three- to five-fold. IBS Intelligence reported that 55% of institutions see legacy complexity as the primary transformation hurdle. Mid-size lenders face the brunt because they lack dedicated change-management teams, leading to schedule slips that erode projected ROI. Each delay postpones downstream projects such as AI analytics and open-API roll-outs, dampening near-term demand growth for the financial services applications market.

Vendor Lock-In and Multi-Cloud Complexity

Reliance on a single hyperscaler or platform narrows bargaining power and raises exit barriers as interfaces, security policies and staff skills become proprietary. Attempts to hedge risk via multi-cloud introduce new toolchains for observability, encryption and networking that inflate operating expense. The Bank of England flagged cloud concentration as a systemic threat, signalling tougher scrutiny of outsourcing contracts. Large enterprises must weigh resiliency gains against governance overhead, slowing some procurement cycles and tempering growth expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offerings: Software Dominance Drives AI Innovation

Software solutions held 71.55% of financial services applications market share in 2025 as institutions gravitated toward unified suites that reduce integration effort. BI, analytics and AI modules are projected to post a 14.32% CAGR to 2031, powered by demand for predictive risk scoring and hyper-personalisation.

Services such as consulting, migration and managed operations fill capability gaps for banks without deep IT teams. As cloud adoption scales, vendors are bundling implementation accelerators and low-code tooling to shrink go-live timelines, keeping service revenue on a steady upward path.

By Deployment: Public Cloud Accelerates Digital Transformation

Cloud deployments represented 63.05% of the financial services applications market size in 2025, with public cloud usage climbing 17.55% CAGR through 2031. High-availability zones, sovereign-cloud options and regulator-approved blueprints have eased prior security concerns.

Private-cloud and on-premise models persist in jurisdictions with strict data-residency rules, yet cost-benefit analyses increasingly favor refactoring workloads into cloud-native micro-services. Vendors are responding with containerized editions that run identically across environments, giving banks a phased exit route from legacy data centers.

By Enterprise Size: Micro-Enterprises Drive Democratization

Large institutions still generated 29.65% of revenue in 2025 thanks to complex multi-country operations that require broad functionality. However, SMEs are expanding at 15.05% CAGR as subscription pricing and low-code configuration lower entry barriers.

These smaller players often target niche communities or underserved segments and rely on cloud platforms to deliver full-service banking without heavy capital spend. Their success validates the view that competitive advantage comes from customer intimacy rather than owning costly infrastructure, widening the customer base for the financial services applications market.

By End-User: FinTech Innovation Challenges Traditional Banking

Banks accounted for 70.62% demand in 2025, reflecting regulatory obligations and large balance sheets that necessitate end-to-end platforms. Fintech and neo-banks, though smaller in absolute terms, are growing at 14.92% CAGR to 2031 as they embed finance into everyday digital experiences.

Insurers and capital-markets firms adopt specialized modules for risk, portfolio and treasury management, but increasingly tap shared SaaS infrastructure to cut unit costs. Cross-sector convergence—such as insurers offering payment wallets—creates new licensing opportunities for modular vendors.

Geography Analysis

North America led with 37.85% revenue in 2025, underpinned by early cloud adoption, robust venture funding and regulatory clarity around open banking. United States banks pilot AI-driven credit models and instant-payment engines, while Canadian and Mexican lenders prioritise modern savings platforms and card-issuing services.

Asia-Pacific is set to deliver the highest 12.58% CAGR, fuelled by smartphone-first consumer behaviour, government incentives for digital payments and rapid neo-bank launches. Markets such as India benefit from nationwide real-time payment rails, whereas Australia and Singapore focus on open-data frameworks that spur account-switching and product innovation.

Europe remains a sizeable, regulation-led buyer segment. PSD2 and the impending instant-payments mandate oblige every credit institution to upgrade API security, fraud analytics and liquidity tools simultaneously. Coupled with post-Brexit competition among UK, German and French fintech hubs, the region keeps vendor pipelines active despite macroeconomic headwinds.

Competitive Landscape

The field is moderately fragmented: global platform vendors coexist with deep-focus fintech specialists. Leaders like Temenos, Fiserv and FIS bundle core processing, analytics and channel apps, positioning themselves as one-stop shops for digital transformation. Their scale enables multi-year investment in generative AI, quantum-secure encryption and low-code tooling.

Specialists differentiate through speed or function—examples include AI-only credit-risk engines and cross-border payment orchestrators. Partnerships and MandA remain common; Temenos’ divestment of Multifonds and Fiserv’s pending Payfare deal illustrate portfolio pruning to double-down on cloud and embedded finance.

Institutions increasingly shortlist vendors that demonstrate open APIs, regulator-approved reference architectures and a roadmap for zero-downtime upgrades. This platform preference accelerates consolidation, yet sustained fintech entry keeps pricing and innovation pressure high, balancing the landscape.

Financial Services Application Industry Leaders

Accenture Plc

FIS Corporation

Fiserv, Inc.

IBM Corporation

Infosys Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Temenos sold its Multifonds business for USD 400 million to sharpen its focus on cloud-native banking platforms.

- February 2025: Aldermore Bank chose Temenos to modernise small-business savings, unifying multiple legacy systems.

- January 2025: CEC Bank adopted Temenos for retail and corporate banking to improve service agility .

- January 2025: Temenos reported FY-24 ARR and software licensing at the top end of guidance, signalling strong demand.

Global Financial Services Application Market Report Scope

Financial services application is the products and services institutions offer for various financial transactions and other related financial services, like consulting services, integration services, audit, risk, and compliance management.

The Financial Services Application Market is segmented by offering (software (audit, risk, and compliance management, BI and analytics applications, business transaction processing, customer experience, and enterprise IT) and service (consulting, integration, training and support, and operations and maintenance)), deployment (cloud and on-premises), size of enterprise (small and medium enterprises and large enterprises), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The market sizes and forecasts are in terms of value (USD) for all the above segments.

| Software | Core Banking Platforms |

| Audit, Risk and Compliance | |

| Business Transaction Processing | |

| BI, Analytics and AI Suites | |

| Customer Experience and CRM | |

| Enterprise IT (ERP, HR, Finance) | |

| Services | Consulting |

| Integration and Migration | |

| Training and Support | |

| Operations and Managed Services |

| Cloud |

| On-premise |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking |

| Insurance |

| Capital Markets |

| FinTech / Neo-banks |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Offerings | Software | Core Banking Platforms | |

| Audit, Risk and Compliance | |||

| Business Transaction Processing | |||

| BI, Analytics and AI Suites | |||

| Customer Experience and CRM | |||

| Enterprise IT (ERP, HR, Finance) | |||

| Services | Consulting | ||

| Integration and Migration | |||

| Training and Support | |||

| Operations and Managed Services | |||

| By Deployment | Cloud | ||

| On-premise | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-User | Banking | ||

| Insurance | |||

| Capital Markets | |||

| FinTech / Neo-banks | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected growth of the financial services applications market to 2031?

The market is expected to rise from USD 165.91 billion in 2025 to USD 343.64 billion by 2031 at a 12.92% CAGR.

Which offering captures the largest share of spending today?

Software suites hold 71.55% of 2025 revenue, led by BI, analytics and AI modules growing at 14.32% CAGR.

Why is public cloud adoption accelerating among banks?

Regulator-approved security frameworks and lower total cost of ownership pushed cloud deployments to 63.05% share in 2025, with public-cloud workloads advancing at 17.55% CAGR.

Which region is expanding the fastest?

Asia-Pacific leads with a forecast 12.58% CAGR as mobile-first consumers and supportive regulations drive digital-banking uptake.

Page last updated on: