Concierge Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

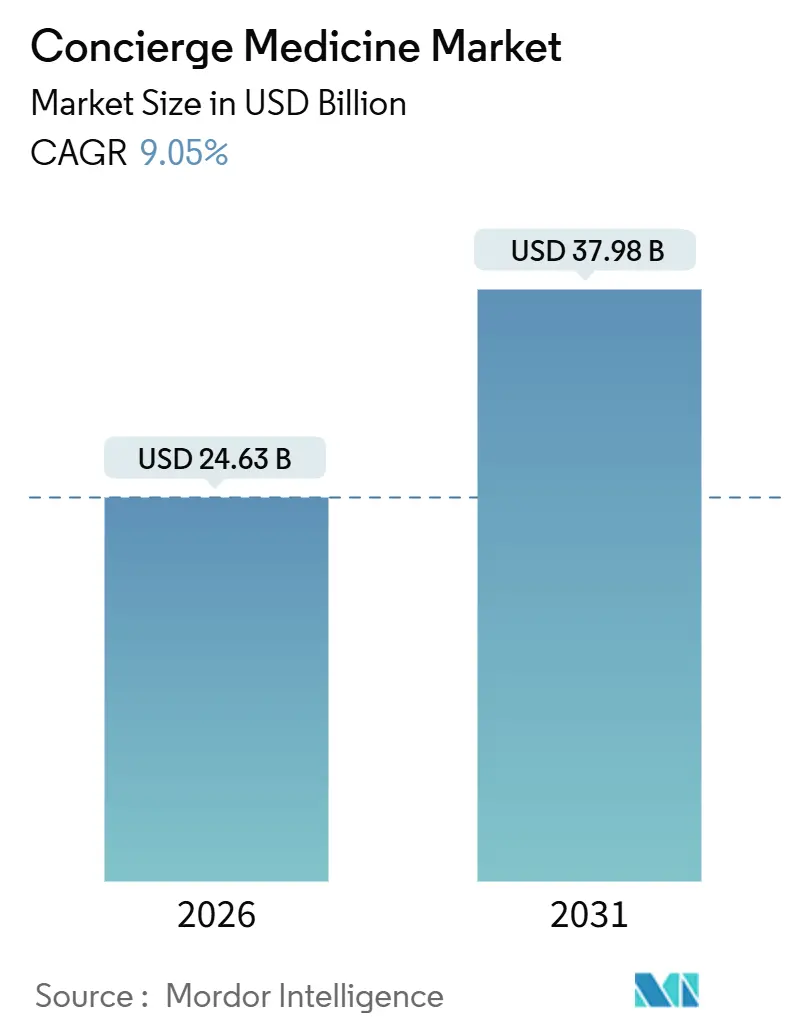

| Market Size (2026) | USD 24.63 Billion |

| Market Size (2031) | USD 37.98 Billion |

| Growth Rate (2026 - 2031) | 9.05% CAGR |

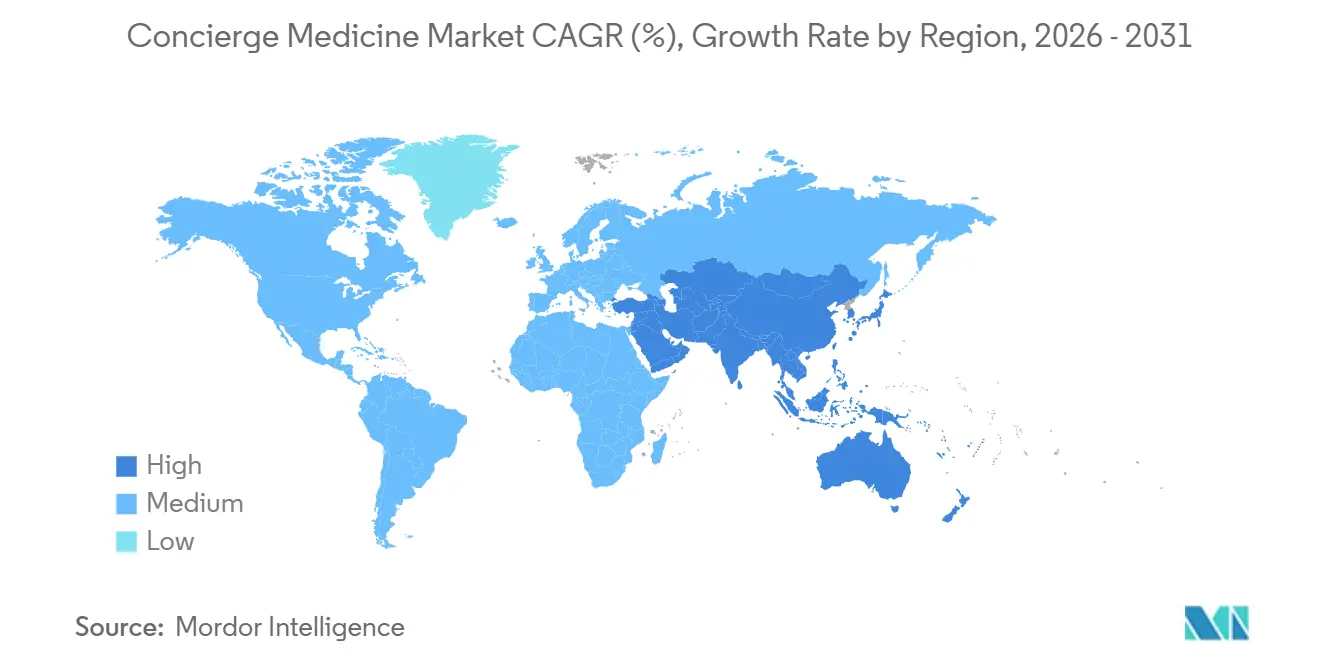

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Concierge Medicine Market Analysis by Mordor Intelligence

The Concierge Medicine Market size is estimated at USD 24.63 billion in 2026, and is expected to reach USD 37.98 billion by 2031, at a CAGR of 9.05% during the forecast period (2026-2031).

Physician burnout, stronger corporate demand for high-touch benefits, and rapid telehealth adoption are reshaping the concierge medicine market, prompting a swift conversion of traditional primary-care offices to membership models. Between 2018 and 2023 the number of U.S. concierge practices jumped 83.1%, while affiliated clinicians climbed 78.4%, pointing to an accelerating supply-side response to patient willingness to pay for personalized care. Corporate benefits groups such as the Health Transformation Alliance now embed concierge memberships for roughly 5 million covered employees to curb absenteeism and avoid unnecessary emergency-department visits. North America remains the largest regional market, but Asia-Pacific is on track for the fastest growth, supported by surging consumer interest in holistic health services and relaxed telehealth rules.

Key Report Takeaways

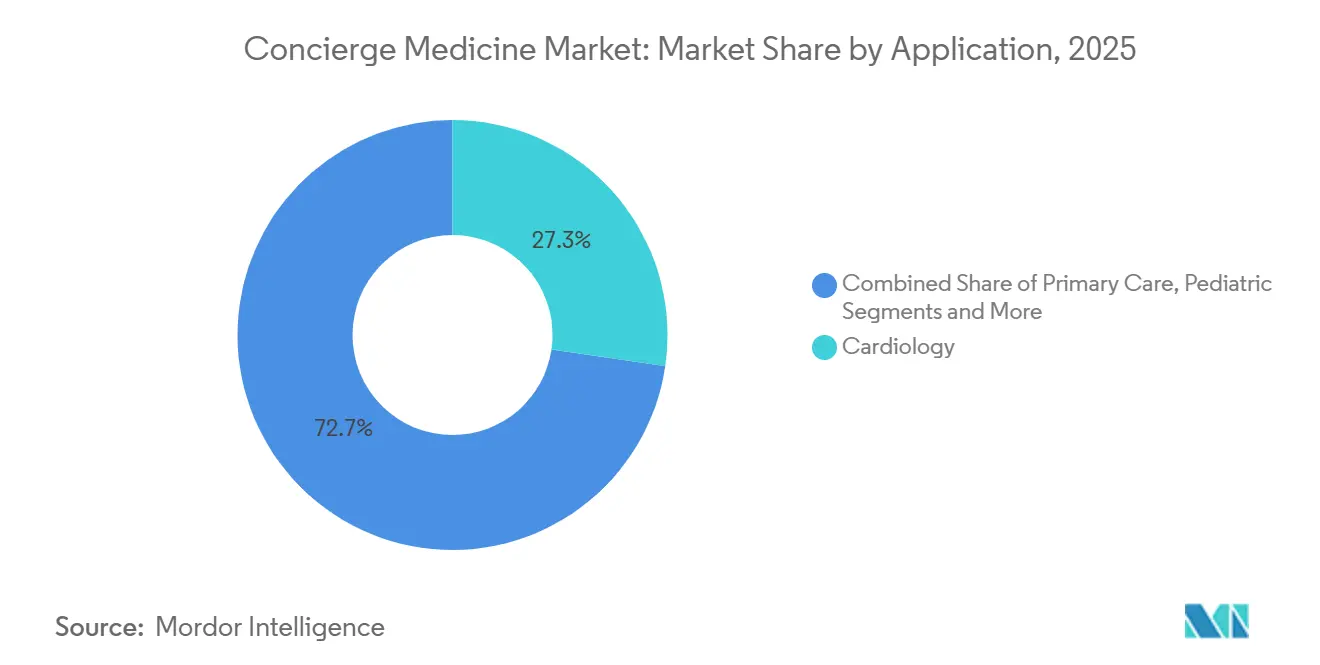

- By application, cardiology held 27.31% of the concierge medicine market share in 2025, while pediatrics is expected to post the highest CAGR of 11.62% from 2026 to 2031.

- By ownership model, physician-led group practices captured 59.83% revenue share in 2025, whereas virtual-only concierge platforms are expanding at a 12.38% CAGR to 2031.

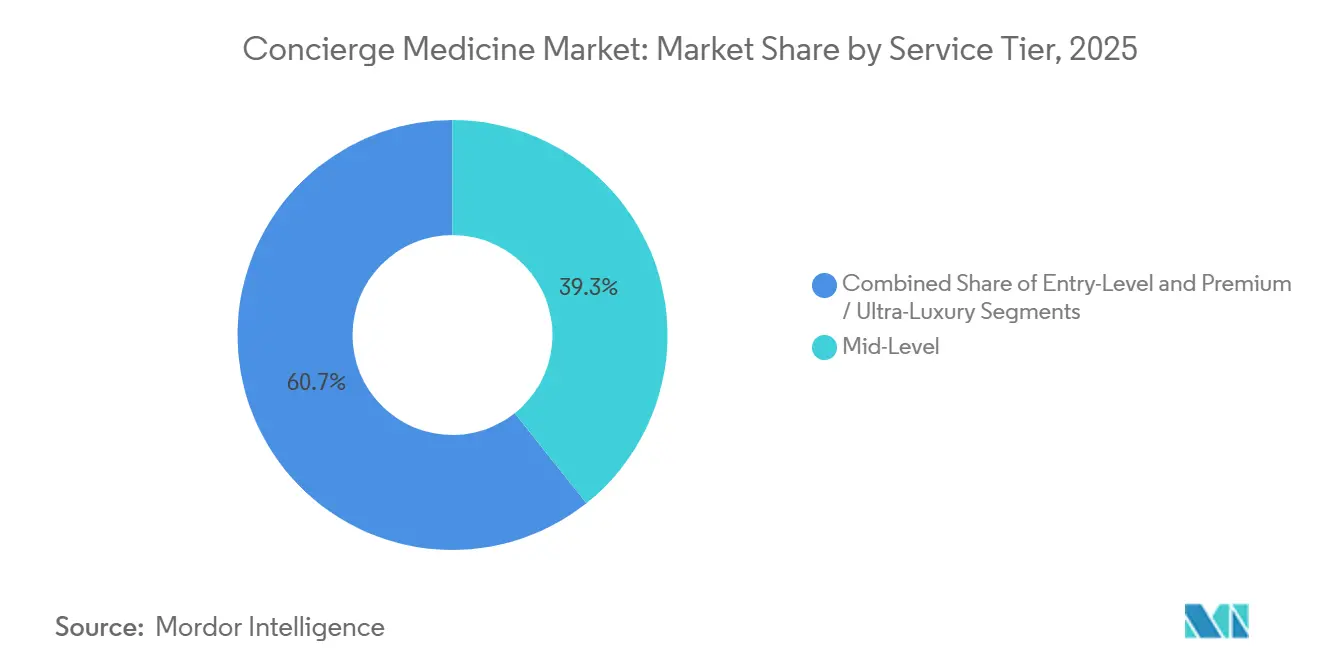

- By service tier, mid-level memberships, priced at USD 3,000–USD 10,000 per year, accounted for 39.28% of the concierge medicine market size in 2025, while premium tiers above USD 10,000 are growing at a 10.16% CAGR.

- By delivery mode, in-person care accounted for 62.86% of the concierge medicine market size in 2025; however, virtual-only models are forecasted to grow at a 13.32% CAGR through 2031.

- By geography, North America retained a 38.36% revenue share in 2025, while the Asia-Pacific region is projected to lead growth with a 12.38% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Concierge Medicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Personalized, time-rich primary care | +2.1% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Physician burnout encouraging conversions | +1.8% | North America, Australia, United Kingdom | Short term (≤ 2 years) |

| Telehealth and remote monitoring integration | +1.5% | Global, fastest in Asia-Pacific | Medium term (2-4 years) |

| Aging, high-net-worth population expansion | +1.3% | North America, Europe, GCC | Long term (≥ 4 years) |

| Employers adding concierge benefits | +1.0% | North America, emerging in Europe & Asia-Pacific | Medium term (2-4 years) |

| AI-enabled continuous care | +0.9% | Global, early in North America & select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Personalized, Time-Rich Primary Care

Patients increasingly pay direct annual fees ranging from USD 1,000 to USD 50,000 to secure same-day appointments, extended visits, and seamless coordination, which are often absent in fee-for-service settings.[1]Concierge Medicine Today, “Concierge Medicine Statistics,” conciergemedicinetoday.com In a 2024 analysis of 18,432 on-demand house-call visits, 52% were self-funded, and 94.2% of users indicated they would rebook, underscoring a durable willingness to spend for convenience. High-net-worth households grew by 562,000 in North America during 2024, broadening the premium customer base. Chronic-disease patients also opt for memberships to hedge against hospital readmissions, translating lifestyle demand into steady subscription revenue. The shift signals a structural shift toward patient-financed, value-driven primary care, supporting the expansion of the concierge medicine market.

Physician Burnout Pushing Practice Conversions

Burnout affected 43% of U.S. physicians in 2024, and 35% considered leaving their current roles within two years.[2]American Medical Association, “Physician Burnout 2024 Survey Results,” ama-assn.org Concierge models typically cap panels at 300-600 patients, compared to 2,000-2,500 in traditional practices, which eases the administrative load. MDVIP, with over 1,300 affiliated doctors, reported 96% physician satisfaction and 90% patient retention in December 2024. A JAMA Health Forum study showed that hospital-employed physicians charge 10.7% more than independent physicians, intensifying pressure for independent conversion. With just 42.2% of doctors remaining in physician-owned settings in 2024, scarcity enables concierge providers to command higher fees, reinforcing momentum toward membership practice models.

Telehealth & Remote Monitoring Integration

CMS extended pandemic-era telehealth flexibilities into 2025, removing rural restrictions and covering audio-only visits.[3]Centers for Medicare & Medicaid Services, “CY 2025 Medicare Physician Fee Schedule Final Rule,” cms.gov Amazon has integrated Amazon Clinic into One Medical's pay-per-visit services, offering video consultations for USD 49, illustrating how hybrid virtual care can lower acquisition costs. Wearable integration enables real-time monitoring of glucose levels and cardiac rhythm, facilitating earlier interventions. An Asia-Pacific consumer survey indicated telehealth adoption doubled from 2020 to 2024, with 90% preferring a single care touchpoint. Asynchronous messaging reduces the time physicians spend per encounter, helping concierge platforms scale profitably and expand the concierge medicine market.

Aging, High-Net-Worth Population Expansion

North America’s high-net-worth cohort increased by 7.3% in 2024 and continues to age, thereby elevating demand for proactive, multi-specialty coordination. Ultra-luxury memberships above USD 10,000, bundling 24/7 physician access, genomic screening, and house calls, are gaining traction. A White House 2025 brief reported that more than 40% of U.S. children now live with chronic conditions, catalyzing pediatric concierge enrollment among affluent parents. Wealth hubs in the GCC and Asia produce pockets of demand for executive and geriatric concierge models. Because health preservation is price-inelastic for these segments, spending supports resilient revenue growth through economic cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited insurance reimbursement | -1.4% | Global, strongest in price-sensitive markets | Short term (≤ 2 years) |

| Shrinking pool of independent physicians | -0.8% | North America, Australia, United Kingdom | Medium term (2-4 years) |

| Regulatory ambiguity on billing | -0.7% | North America, spillover globally | Medium term (2-4 years) |

| Equity and access policy push-back | -0.5% | North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Insurance Reimbursement / High Out-of-Pocket Fees

Membership fees are generally ineligible for reimbursement under Medicare or commercial plans, as they are viewed as non-medical amenities. CMS guidance permits billing only for incremental covered services, leaving annual fees entirely patient-funded. Affordability barriers narrow the eligible population in lower-income markets. Hospital-affiliated physicians already charge 10.7% more than independents, heightening cost concerns that make concierge access appear exclusive. Entry-level direct-primary care tiers priced below USD 3,000 aim to broaden their reach, yet these stripped-down offerings often lack diagnostic breadth, which limits their competitiveness.

Shrinking Pool of Independent Primary-Care Physicians

Hospital contracts often bar departing physicians from practicing locally for several years, blocking concierge startups. Private-equity acquisitions likewise favor volume-based models, diverting potential converts. AMA survey data show that while 35% of doctors consider leaving their current roles, many retire or transition into non-clinical jobs rather than launching concierge ventures. Intensifying recruitment competition elevates physician acquisition costs and slows geographic rollout.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Cardiovascular Dominance Meets Pediatric Acceleration

Cardiology controlled 27.31% of the concierge medicine market share in 2025 on the back of executive demand for ongoing risk surveillance and immediate cath-lab access. The concierge medicine market size for cardiovascular offerings is expected to expand steadily alongside aging demographics that elevate disease burden. Pediatrics, though smaller today, is forecast to grow at 11.62% CAGR through 2031, fueled by rising childhood obesity, diabetes, and behavioral disorders documented by the White House in May 2025.

Specialty diversification continues. Psychiatry concierge demand is escalating as employers link mental health access to productivity, while primary care remains foundational for broad patient panels. Dermatology, orthopedics, and women’s health emerge in pockets where patients value aesthetic outcomes or fertility monitoring, but still account for modest proportions of the overall concierge medicine market size. Providers are increasingly bundling primary care with specialty access to differentiate themselves, creating composite programs that deepen loyalty and lengthen membership tenure.

By Ownership Model: Group Practices Lead, Virtual Platforms Disrupt

Physician-led group practices held 59.83% of the concierge medicine market size in 2025, leveraging shared infrastructure and cross-referral dynamics to keep per-member costs in check. Group economics also support investments in electronic records and remote monitoring, which solo offices often struggle to fund. Virtual-only concierge platforms, however, are projected to record a 12.38% CAGR to 2031, drawing strength from minimal real-estate overhead and AI-enhanced triage that enables clinicians to manage larger panels without compromising visit quality.

Corporate-owned networks such as One Medical, now part of Amazon, operate more than 200 clinics serving roughly 815,000 members, demonstrating how scale amplifies bargaining power with payers and suppliers. Franchise formats provide turnkey platforms for doctors lacking capital to develop proprietary technology, while hospital-affiliated programs integrate inpatient pathways but often fall short in terms of concierge-level responsiveness. Overall, competitive positioning pivots on a provider’s capacity to balance the intimacy of care with operational efficiency, a tension central to the future trajectory of the concierge medicine market.

By Service Tier: Mid-Level Balances Access, Luxury Captures Wealth

Mid-level memberships priced between USD 3,000 and USD 10,000 secured 39.28% of the concierge medicine market size in 2025, offering attractive trade-offs for upper-middle-income households seeking faster access without premium frills. Premium and ultra-luxury tiers are climbing at a 10.16% CAGR, powered by high-net-worth individuals who value global medical navigation, advanced diagnostics, and dedicated care teams. Sollis Health cites a 99% avoidance of emergency department utilization among its members, underlining perceived ROI at the upper end.

Entry-level tiers under USD 3,000 per year aim to democratize concierge access but often rely on larger patient panels and slimmer service menus. Mid-level programs face squeeze pressures from both ends—forced to justify incremental fees versus entry-level, while lacking the white-glove features of luxury competitors. Providers refine tier differentiators to manage churn, highlighting bespoke exam protocols, specialist coordination, and personalized lifestyle planning as value anchors.

By Delivery Mode: In-Person Anchors Trust, Virtual Scales Reach

In-person care accounted for 62.86% of the concierge medicine market size in 2025, as patients continue to prefer physical examinations, on-site labs, and the rapport that comes with face-to-face visits. A 2024 review of house-call services found 94.2% repeat-booking intent, signaling a persistent appetite for direct interaction. Virtual-only platforms are expanding at the fastest rate, with a 13.32% CAGR, aided by remote monitoring devices that deliver continuous biometric data streams to clinicians.

Hybrid models, combining annual physicals with telehealth follow-ups, strike an efficiency balance. CMS rules effective through 2026 continue to reimburse telehealth across geographic locations, alleviating regulatory friction. Virtual modalities nonetheless face limitations for complex diagnostics, prompting many operators to adopt blended offerings. Younger digital-native patients favor messaging consults, making virtual capacity a strategic necessity even for brick-and-mortar practices within the concierge medicine market.

Geography Analysis

North America commanded 38.36% revenue share in 2025, upheld by the largest pool of independent physicians and the densest high-net-worth population. The concierge medicine market size in the United States expanded, with practice counts increasing from 1,658 in 2018 to 3,036 in 2023, and the number of clinicians rising from 3,935 to 7,021 over the same period. U.S. employers further accelerate penetration, bundling memberships to curb absenteeism and emergency department spending. Canada and Mexico exhibit fledgling adoption, centered in major metropolitan areas, where cross-border medical tourists seek continuity of care.

The Asia-Pacific region is projected to grow at a 12.38% CAGR through 2031, driven by rapidly expanding disposable incomes, particularly in China and India. Eighty percent of Asia-Pacific consumers voice interest in health maintenance services, with half ready to pay premiums and ninety percent preferring single-point coordination. Telemedicine use doubled from 2020 to 2024, laying infrastructure that concierge platforms can leverage. AXA Hong Kong’s 2025 upgrade of its Greater Bay Area Medical Concierge Service Network exemplifies the growth of cross-border care. Japan’s aging cohort and Australia’s private insurance norms add further runway for regional expansion.

Europe experiences a moderate uptake, with Germany, the United Kingdom, and France at the forefront, each benefiting from private spending upticks and permissive direct contracting regulations. GCC economies in the Middle East welcome ultra-luxury providers catering to expatriate executives who seek continuity across their global postings. South America remains emergent; affluent segments in Brazil and Argentina adopt concierge services, but broader diffusion is slowed by affordability and fragmented insurance frameworks. Diverse regulatory regimes necessitate localized models, encouraging large operators to form regional partnerships to mitigate the risk of entry.

Competitive Landscape

The concierge medicine market remains moderately fragmented. Amazon’s USD 3.9 billion acquisition of One Medical in 2023 spotlighted intensifying competition as technology giants seek footholds in clinical delivery. One Medical now operates over 200 offices and serves approximately 815,000 members, leveraging scale to negotiate payer contracts and invest in AI tools that reduce documentation times by 40%. Privia Health, supporting 4,642 providers across 1,170 care centers, reported 98% gross provider retention and more than 100 value-based contracts, illustrating a quality-metric-aligned model.

Smaller entities pursue white-space niches such as pediatric care, executive health, and cosmetic dermatology. Virtual-only disruptors avoid real estate costs, allowing for lower membership prices and a broader geographic reach, yet still face hurdles in performing physical exams. Physician recruitment remains the fiercest battleground, given shrinking independent supply. Platforms offering reduced paperwork, higher per-patient revenue, and flexible scheduling gain an advantage in attracting talent.

Regulatory mastery also differentiates winners. Providers who are fluent in Medicare billing stipulations, state insurance disclosure rules, and telehealth licensure requirements scale more effectively across markets. Equity debates spark reputational scrutiny, pushing operators to showcase measurable outcome improvements and stress that higher physician satisfaction ultimately keeps more clinicians in practice. Consolidation is likely to continue as capital-rich entrants acquire established practices to accelerate regional growth, thereby compressing margins for smaller, standalone clinics.

Concierge Medicine Industry Leaders

MDVIP

SignatureMD

Crossover Health

Castle Connolly Private Health Partners

Concierge Choice Physicians

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: NeueHealth was acquired by NEA and an investor consortium at a USD 1.465 billion enterprise value, with shares ceasing trading on the New York Stock Exchange on October 2, 2025. The transaction provided stockholders with USD 7.33 per share in cash and marked a strategic shift toward private ownership for the value-based primary care platform

- March 2025: Amazon-owned One Medical confirmed CEO Trent Green’s departure, prompting interim leadership amid broader Amazon Health Services restructuring.

- July 2024: KFF Health News highlighted rising access disparities linked to annual concierge growth of 10% or more, fueling a policy debate on equity.

- July 2024: K Health raised USD 50 million in an equity financing round led by Claure Group, bringing total funding to date above USD 270 million. The AI-driven primary care platform announced plans to expand partnerships with health systems, including Cedars-Sinai, to increase primary care access by 15%

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the concierge medicine market as membership-based primary or specialty care in which individuals pay a periodic retainer for priority appointments, direct physician access, basic diagnostics, and coordinated referrals.

Scope Exclusions: Procedures delivered solely through one-off executive physical programs or employer on-site clinics are excluded.

Segmentation Overview

- By Application

- Primary Care

- Pediatrics

- Cardiology

- Psychiatry & Mental Health

- Other Applications

- By Ownership Model

- Physician-Owned Solo Practices

- Physician-Led Group Practices

- Corporate-Owned Clinics

- Hospital/Health-System Affiliated Programs

- Franchise Models

- Virtual-Only Concierge Platforms

- By Service Tier

- Entry-Level (USD < 3 k p.a.)

- Mid-Level (USD 3–10 k p.a.)

- Premium / Ultra-Luxury (USD > 10 k p.a.)

- By Delivery Mode

- In-Person

- Hybrid

- Virtual-Only

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed physicians, administrators, payers, and benefit consultants in six regions to validate average panel sizes, fee bands, and churn. A short patient survey refined willingness-to-pay curves. These conversations closed information gaps found during secondary work.

Desk Research

We began with open datasets from OECD, WHO, and the U.S. Centers for Medicare & Medicaid Services to map physician density, out-of-pocket spending, and chronic-disease burdens across 30 economies. Our team next reviewed SEC filings and investor decks of large concierge networks, plus releases from Concierge Medicine Today and the American Academy of Private Physicians. Customs logs of point-of-care devices, patent alerts via Questel, and news feeds from Dow Jones Factiva flagged technology uptake and price shifts. D&B Hoovers supplied revenue snapshots for sample practices. The sources named here illustrate, not exhaust, the wider desk research pool.

Market-Sizing & Forecasting

Our model starts with a top-down rebuild of the paying patient pool, insured adults earning above a specified income level, adjusted for physician adoption and typical panel capacity. Results are cross-checked through selective bottom-up roll-ups of practice revenues derived from sampled average selling price multiplied by member counts. Multivariate regression on concierge physician headcount, median fee trajectory, population aged 55-plus, high-net-worth households, and telehealth adoption drives the forecast period. Regional data gaps are bridged through analog markets and expert judgment before both approaches are averaged into the baseline.

Data Validation & Update Cycle

Outputs undergo peer review, variance checks against hospital admission trends, and currency reconciliations before sign-off. Our analysts refresh models annually, with interim updates whenever regulation, funding, or pandemics materially shift fundamentals.

Why Our Concierge Medicine Baseline Earns Trust

Published estimates often diverge because firms apply different service definitions, fee assumptions, and refresh cadences.

Mordor Intelligence includes hybrid clinics and emerging Asia-Pacific roll-outs, whereas some publishers omit these or freeze exchange rates, creating visible gaps. Other public studies quote 2024 values of about USD 20.40 billion and USD 18.30 billion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.03 B (2025) | Mordor Intelligence | |

| USD 20.40 B (2024) | Global Consultancy A | Excludes Asia-Pacific and hybrid clinics |

| USD 18.30 B (2024) | Trade Journal B | Uses straight-line physician adoption, no primary checks |

Taken together, the comparison shows our figure sits between optimistic fee-driven builds and conservative headcount extrapolations, giving decision-makers a balanced, transparent baseline.

Key Questions Answered in the Report

What CAGR is projected for the concierge medicine market through 2031?

The concierge medicine market is forecast to grow at 9.05% CAGR from 2026 to 2031.

Which application currently holds the largest share?

Cardiology leads, capturing 27.31% of 2025 revenue.

Which region is expected to grow fastest?

Asia-Pacific is projected to post a 12.38% CAGR through 2031.

How big is the mid-level membership segment?

Mid-level tiers priced USD 3,000–USD 10,000 captured 39.28% of 2025 revenue.

What drives physician migration to concierge models?

High burnout rates, with 43% of doctors reporting symptoms in 2024, motivate conversions for smaller panels and improved work-life balance.

Page last updated on: