Desalting And Buffer Exchange Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

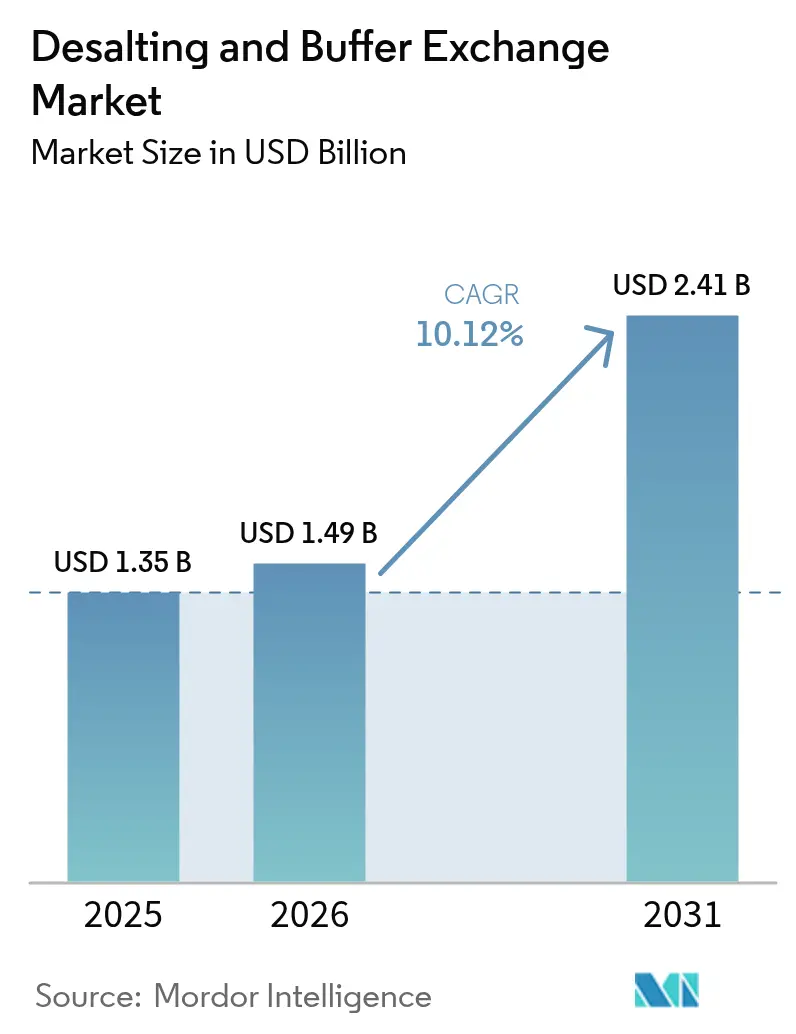

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

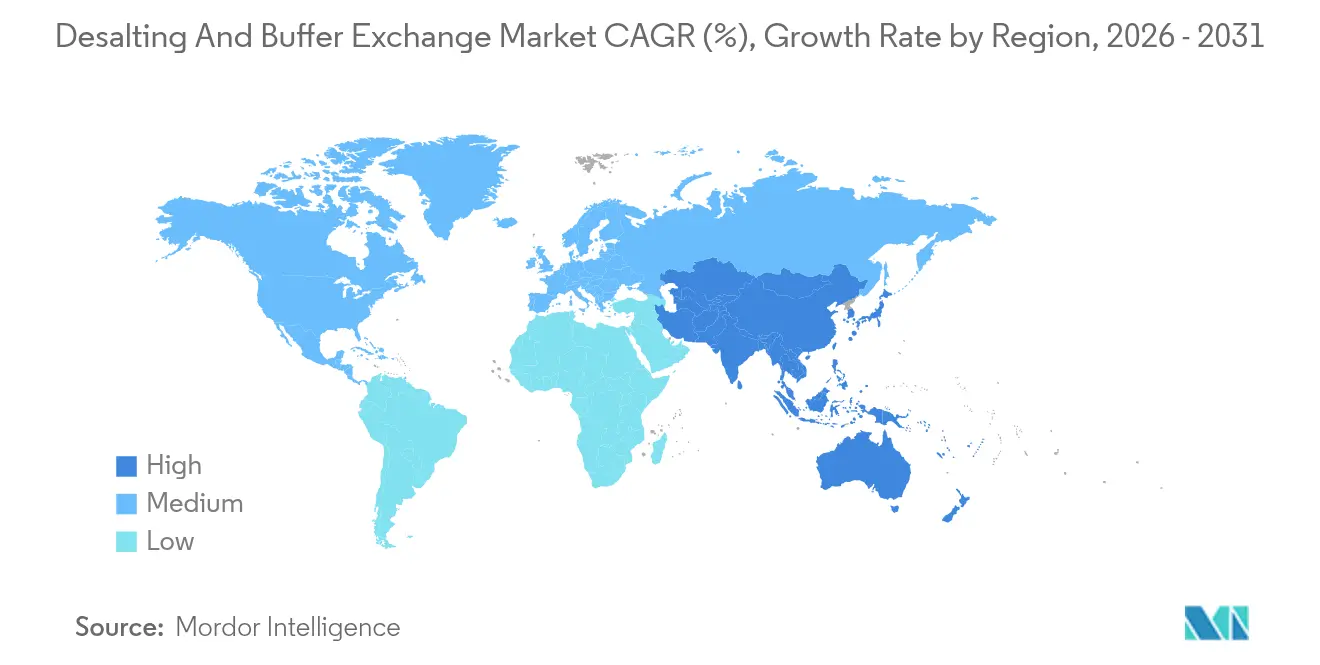

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Desalting And Buffer Exchange Market Analysis by Mordor Intelligence

The desalting and buffer exchange market size was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.49 billion in 2026 to reach USD 2.41 billion by 2031, at a CAGR of 10.12% during the forecast period (2026-2031). Demand momentum is shaped by the rapid scale-up of global biologics production, heightened vaccine manufacturing capacity, and tightening regulatory expectations for downstream purity. Contract development and manufacturing organizations (CDMOs) channel substantial capital toward large-scale facilities, which expands the installed base for purification equipment and lifts recurring consumables sales. Spin columns remain the workhorse of research laboratories, yet centrifugal filter devices and single-use membranes see accelerating uptake as facilities seek higher throughput and reduced validation burden. Geographically, North America retains a technology leadership position, but sustained green-field expansion and policy support in Asia-Pacific give that region the steepest growth runway. Competitive dynamics favor suppliers able to bundle hardware, consumables, and analytics into integrated platforms that shorten tech-transfer timelines and improve regulatory compliance.

Key Report Takeaways

- By product, spin columns held 37.62% of the Desalting And Buffer Exchange market share in 2025, while centrifugal filter devices are forecast to advance at a 12.18% CAGR through 2031.

- By technique, chromatography captured 43.75% revenue share in 2025; filtration methods are expanding at a 12.41% CAGR to 2031.

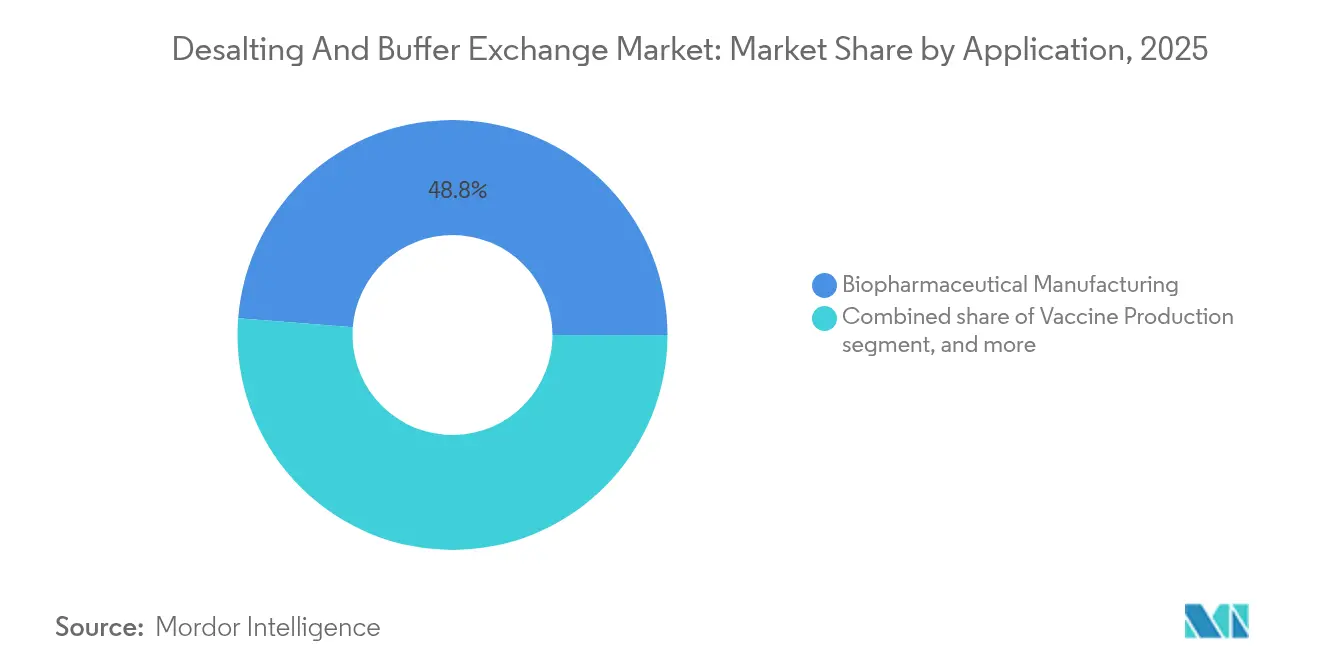

- By application, biopharmaceutical manufacturing accounted for 48.76% of the Desalting And Buffer Exchange market size in 2025, whereas vaccine production is projected to grow at a 13.47% CAGR through 2031.

- By scale, laboratory-level operations commanded 57.84% share in 2025, yet commercial manufacturing scale is rising at a 13.29% CAGR over the outlook period.

- By geography, North America led with 41.88% share in 2025, and Asia-Pacific registers the highest regional CAGR of 11.22% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Desalting And Buffer Exchange Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of global biologics manufacturing capacity | +2.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Increasing investments in genomic and proteomic research | +2.1% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Technological advancements in downstream purification platforms | +1.9% | Global | Medium term (2-4 years) |

| Growth of contract development and manufacturing organizations (CDMOs) | +2.3% | Global with Asia-Pacific surge | Short term (≤ 2 years) |

| Shift toward continuous bioprocessing and automation | +1.7% | North America and Europe | Long term (≥ 4 years) |

| Rising demand for high-throughput diagnostic sample preparation | +1.4% | Global with Asia-Pacific focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Global Biologics Manufacturing Capacity

Large-scale capacity announcements continue to reshape procurement patterns across the desalting and buffer exchange market. Samsung Biologics secured USD 3.3 billion worth of contracts in 2024, while Lonza purchased Roche’s Vacaville plant, adding 330,000 liters of bioreactor capacity to the global network[1]Staff Reporter, “Samsung Biologics lands record contract,” Fierce Pharma, fiercepharma.com. Every incremental bioreactor demands proportional downstream infrastructure, including desalting columns, filter cartridges, and buffer preparation modules. CDMOs such as Fujifilm Diosynth have earmarked more than USD 8 billion for site expansions that come online mid-2025, signaling a multi-year uplift in consumables demand. The economic stakes are significant because purification yields directly influence cost of goods. Consequently, biomanufacturers gravitate toward high-throughput devices that minimize hold times, reduce buffer consumption, and elevate batch consistency.

Increasing Investments in Genomic and Proteomic Research

Next-generation sequencing growth drives stringent requirements for ultra-pure nucleic acid and protein samples. Academic consortia and pharmaceutical discovery units invest in desalting kits that can process hundreds of micro-scale samples in parallel without cross-contamination[2]Editorial Team, “Continuous chromatography gains ground,” BioProcess International, bioprocessintl.com. China and India push toward good manufacturing practice (GMP) compliance, broadening the global footprint of advanced analytical laboratories. Artificial intelligence-enabled assay development further tightens buffer specifications, pressing operators to deploy automated buffer exchange systems that assure reproducibility over extended runs. The resulting rise in throughput requirements reinforces demand for scalable platforms that can migrate from discovery to pilot production with minimal protocol changes.

Technological Advancements In Downstream Purification Platforms

Continuous chromatography, single-pass tangential-flow filtration, and 3D-printed single-use chambers exemplify the technology leap underway in downstream operations. Modern multimodal resins show greater salt tolerance, which reduces the number of buffer exchange steps and shortens cycle time. Real-time sensors now track conductivity and product concentration, enabling feedback control that drives higher yields. Single-use assemblies cut cleaning validation and support multi-product flexibility, though they exacerbate waste-management challenges. Suppliers differentiate through resin chemistries that resist fouling and membranes that sustain high flux under continuous conditions, improving cost-per-gram metrics for high-volume biologics.

Growth Of Contract Development and Manufacturing Organizations (CDMOs)

The CPHI Annual Report anticipates CMOs and hybrids will control 54% of worldwide biologics capacity by 2028, magnifying the gate-keeping role of large-scale outsourcing partners. CDMOs standardize equipment across networks to leverage global validation packages and to negotiate bulk pricing on consumables. Flexible skid-mounted systems allow rapid line reconfiguration between antibodies, cell therapies, and nucleic acid vaccines. Smaller biotech firms, under capital pressure, rely on CDMOs’ turnkey downstream suites to compress development timelines, which reinforces demand for validated purification kits and ready-to-run columns.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled downstream processing workforce | -1.8% | North America and Europe | Short term (≤ 2 years) |

| High capital and operating costs of advanced filtration systems | -2.1% | Emerging markets most affected | Medium term (2-4 years) |

| Sustainability and waste-disposal concerns for single-use consumables | -1.3% | Europe and North America | Long term (≥ 4 years) |

| Supply-chain vulnerabilities for specialty membranes and resins | -1.6% | Asia-Pacific sourcing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Downstream Processing Workforce

Industry surveys underline a widening talent gap in membrane science, process analytics, and automation. Leading clusters such as Boston and Basel attract the limited pool of experienced engineers, leaving newer hubs short-staffed. Project delays and rising labor costs add friction to technology adoption in the desalting and buffer exchange market. Training programs struggle to keep curricula current with rapid equipment upgrades. To mitigate risk, facilities invest in highly automated platforms that reduce operator dependency, yet such systems command higher upfront capital.

Supply Chain Vulnerabilities for Specialty Membranes and Resins

Fluoropolymer films and high-capacity ion-exchange resins originate from a limited set of specialty chemical suppliers concentrated in Asia. Pandemic-era logistics disruptions spotlighted lead-time risk, prompting Western buyers to stockpile inventory[3]Policy Brief, “Supply-chain re-alignment post-Biosecure Act,” Carnegie Endowment, carnegieendowment.org. The US Biosecure Act discourages sourcing from certain Chinese entities, redirecting orders to alternate suppliers in Korea and India. Although diversification improves resilience, interim shortages elevate costs and extend qualification timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Spin Columns Lead Traditional Applications

In 2025 spin columns contributed 37.62% to the desalting and buffer exchange market share, underscoring their entrenched value in routine lab protocols. Researchers prize the plug-and-play format, rapid processing times, and compatibility with a range of biomolecule sizes. The segment continues to innovate through higher-capacity resins and low-binding plastics that improve recovery rates. Conversely, centrifugal filter devices headline the growth narrative with a 12.18% CAGR through 2031, benefiting from escalating high-volume screening and micro-bioreactor usage. Suppliers such as Sartorius enhance membrane geometry to maintain flux at lower centrifugal forces, which protects fragile biologics.

The desalting and buffer exchange market size allocation for spin columns is expected to contract slightly in relative terms as labs migrate to higher-throughput cartridge and plate formats. Dialysis cassettes hold niche appeal where ultra-gentle conditions safeguard conformational integrity of complex proteins. Filter plates penetrate combinatorial chemistry and antibody engineering workflows that demand parallel processing. Bundled kits simplify procurement and validation, encouraging procurement managers to favor single-vendor solutions over piecemeal sourcing.

By Technique: Chromatography Dominance Faces Filtration Challenge

Chromatography retained 43.75% share of the desalting and buffer exchange market in 2025, anchored by size-exclusion and ion-exchange columns that deliver high selectivity for therapeutic proteins. Resin innovations with wider operational pH and salt ranges reduce the number of conditioning steps and drive cost-of-goods efficiency. Filtration methods, however, post a 12.41% CAGR to 2031 as continuous bioprocessing demands inline buffer exchange with minimal hold volumes. Ultrafiltration membranes capable of low protein binding and high flux rates bridge the gap between lab and manufacturing scale.

Precipitation techniques attract renewed attention in cost-sensitive vaccine installations, where polyethylene glycol (PEG) and ammonium sulfate achieve acceptable purity at a fraction of chromatographic consumable expense. Dialysis remains relevant for small-batch production where time penalties are tolerable. Hybrid workflows, combining a single-pass TFF step with polishing chromatography, illustrate how facilities optimize selectivity and throughput without extensive capital upgrades.

By Application: Vaccine Production Accelerates Beyond Traditional Biologics

Biopharmaceutical manufacturing represented 48.76% of the desalting and buffer exchange market size in 2025, spanning monoclonal antibodies, fusion proteins, and recombinant enzymes. The pipeline shift toward antibody-drug conjugates and bispecific antibodies introduces higher molecular complexity, reinforcing purification stringency. Vaccine production, propelled by pandemic preparedness agendas, outpaces all segments at a 13.47% CAGR through 2031. mRNA vaccines require removal of template DNA, enzymes, and residual solvents, intensifying reliance on multimodal chromatography and inline diafiltration.

Diagnostic sample preparation gains momentum as decentralized testing and personalized medicine expand. Automated liquid-handling systems integrate plug-and-play desalting plates to maintain analytical throughput. Emerging applications, including food safety and environmental monitoring, diversify revenue streams, making the desalting and buffer exchange industry less dependent on monoclonal antibody cycles.

By Scale: Commercial Manufacturing Gains Momentum

Laboratory-level operations retained 57.84% share in 2025, reflecting academia’s pervasive role in early-stage discovery. Yet commercial manufacturing scale posts a 13.29% CAGR through 2031 as late-stage biologics secure regulatory approvals. Transitioning from gram-level runs to kilogram-level campaigns imposes new constraints on buffer supply, waste handling, and process analytics. The desalting and buffer exchange market size allocated to pilot-scale serves as a crucial bridge, allowing engineers to stress-test membrane lifetimes and resin capacities before multi-shift manufacturing begins.

Process intensification, characterized by continuous culture feeding directly into downstream skids, compels plants to adopt fully closed buffer exchange loops. Flexible single-use flow-paths promote rapid changeover between products, maximizing facility utilization. Vendors respond with filter cassettes rated for multi-use cycles without performance decay, trimming consumables cost per batch.

Geography Analysis

North America preserved its 41.88% revenue leadership in 2025, thanks to mature GMP frameworks, a dense cluster of CDMOs, and ready access to venture funding that accelerates technology refresh cycles. Regional demand also benefits from federal incentives aimed at reshoring critical bioprocessing components, which favor domestic suppliers of membranes and chromatography resins. The desalting and buffer exchange market size for North America will still expand at mid-single-digit rates as contract manufacturers add capacity to serve global clients.

Europe follows with steady uptake rooted in stringent environmental and quality regulations. The bloc’s Green Deal nudges plants toward lower buffer consumption and recycling programs, stimulating interest in high-yield resins and membranes with extended lifetimes. Brexit-driven supply-chain adjustments redirect some procurement from UK-based distributors to continental hubs, but the overall technology adoption curve remains intact. Collaborative projects under the EU Horizon program support development of recyclable single-use plastics, which could alter consumables preferences over the long term.

Asia-Pacific delivers the most dynamic outlook at an 11.22% CAGR through 2031. China’s pivot to Southeast Asian satellite facilities, combined with India’s bid to capture production displaced by the US Biosecure Act, fuels import demand for purification skids. Governments in Singapore and South Korea subsidize pilot-scale parks that bundle upstream and downstream assets, lowering barriers for domestic start-ups. The desalting and buffer exchange market share held by Asia-Pacific is therefore expected to rise steadily as new green-field plants come online and local reagent suppliers scale production.

Competitive Landscape

Thermo Fisher Scientific’s USD 4.1 billion acquisition of Solventum’s Purification & Filtration unit marks a strategic push to own more of the downstream toolkit and cross-sell consumables with existing bioproduction hardware. Danaher’s merger of Cytiva and Pall forged a USD 7.5 billion entity boasting the industry’s broadest portfolio, enabling single-contract coverage from cell culture to final fill-finish. Such vertical integration pressures mid-tier players to find defensible niches in membrane coatings, specialty resins, or automation software.

Repligen’s purchase of chromatography innovator Tantti illustrates the scramble for differentiated intellectual property that can enhance flow-path performance or lower solvent use. Meanwhile, Sartorius focuses on modular single-use systems, launching TFF cassettes that promise 30% higher flux without compromising selectivity. Competitive advantage increasingly hinges on the ability to offer harmonized hardware-software ecosystems that collapse tech-transfer timelines for CDMO clients.

Environmental scrutiny prompts suppliers to invest in recyclable polymers and to quantify cradle-to-grave carbon footprints. Early-adopter firms position these metrics as value propositions during GMP audits. The expanding market pie also attracts newcomers specializing in 3D-printed flow-cells or AI-driven process control, adding incremental rivalry to incumbent portfolios. Overall, competition gravitates toward platform breadth, proven regulatory track records, and supply-chain resilience.

Desalting And Buffer Exchange Industry Leaders

Sartorius AG

Merck KGaA

Agilient Technologies, Inc.

Thermo Fisher Scientific Inc.

Danaher Corp. (Pall & Cytiva)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific acquired Solventum’s Purification & Filtration business for roughly USD 4.1 billion, expanding its downstream processing footprint.

- February 2025: SK pharmteco committed USD 260 million to a new Sejong facility housing CGMP peptide and small-molecule suites.

- January 2025: Fujifilm Diosynth outlined USD 8 billion of global expansions, including a doubling of its Hillerød plant.

- December 2024: Lonza unveiled its “One Lonza” structure, exiting capsules to sharpen its CDMO focus.

- October 2024: Samsung Biologics closed a USD 1.2 billion production deal with an unnamed Asian partner, its largest single-client contract.

- July 2024: Repligen agreed to acquire Tantti, gaining novel chromatography technology.

Global Desalting And Buffer Exchange Market Report Scope

As per the report's scope, desalting occurs when buffer salts and other molecules are removed from a sample in exchange for water. Buffer exchange occurs when the buffer salts in a sample are exchanged for those in another buffer. The Desalting and Buffer Exchange market is segmented by Product (Cassettes and Cartridges, Kits, Filter Plates, and Other Products), Technique (Filtration, Chromatography, and Precipitation), Application ( Bioprocess Application, Diagnostic Application, Pharmaceutical and Biotechnology Industries, and Other Applications) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Spin Columns |

| Dialysis Cassettes & Cartridges |

| Centrifugal Filter Devices |

| Kits |

| Filter Plates |

| Other Products |

| Filtration | Ultrafiltration / Diafiltration |

| Dialysis | |

| Chromatography | Size-Exclusion (Desalting) |

| Ion-Exchange | |

| Precipitation | PEG Precipitation |

| Ammonium-Sulfate Precipitation |

| Biopharmaceutical Manufacturing |

| Vaccine Production |

| Diagnostic Sample Preparation |

| Other Applications |

| Laboratory-Scale |

| Pilot-Scale |

| Commercial Manufacturing-Scale |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Spin Columns | |

| Dialysis Cassettes & Cartridges | ||

| Centrifugal Filter Devices | ||

| Kits | ||

| Filter Plates | ||

| Other Products | ||

| By Technique | Filtration | Ultrafiltration / Diafiltration |

| Dialysis | ||

| Chromatography | Size-Exclusion (Desalting) | |

| Ion-Exchange | ||

| Precipitation | PEG Precipitation | |

| Ammonium-Sulfate Precipitation | ||

| By Application | Biopharmaceutical Manufacturing | |

| Vaccine Production | ||

| Diagnostic Sample Preparation | ||

| Other Applications | ||

| By Scale | Laboratory-Scale | |

| Pilot-Scale | ||

| Commercial Manufacturing-Scale | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Desalting And Buffer Exchange market in 2031?

The market is forecast to reach USD 2.41 billion by 2031, reflecting a 10.12% CAGR.

Which product type currently dominates sales?

Spin columns lead with 37.62% revenue share in 2025 due to their ease of use in laboratory workflows.

Which region is expanding the fastest?

Asia-Pacific posts the highest growth rate at 11.22% CAGR as China and India scale biopharmaceutical capacity.

Why are centrifugal filter devices growing rapidly?

They support high-throughput screening and deliver higher recovery rates, driving a 12.18% CAGR through 2031.

What factor most constrains adoption of advanced filtration systems?

High capital outlays and operating costs reduce affordability, especially for emerging-market manufacturers.

How has industry consolidation altered supplier dynamics?

Large acquisitions such as Thermo Fisher–Solventum and Danaher’s Cytiva-Pall merger create integrated platforms that bundle hardware, consumables, and analytics.

Page last updated on: