Slimming Aids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

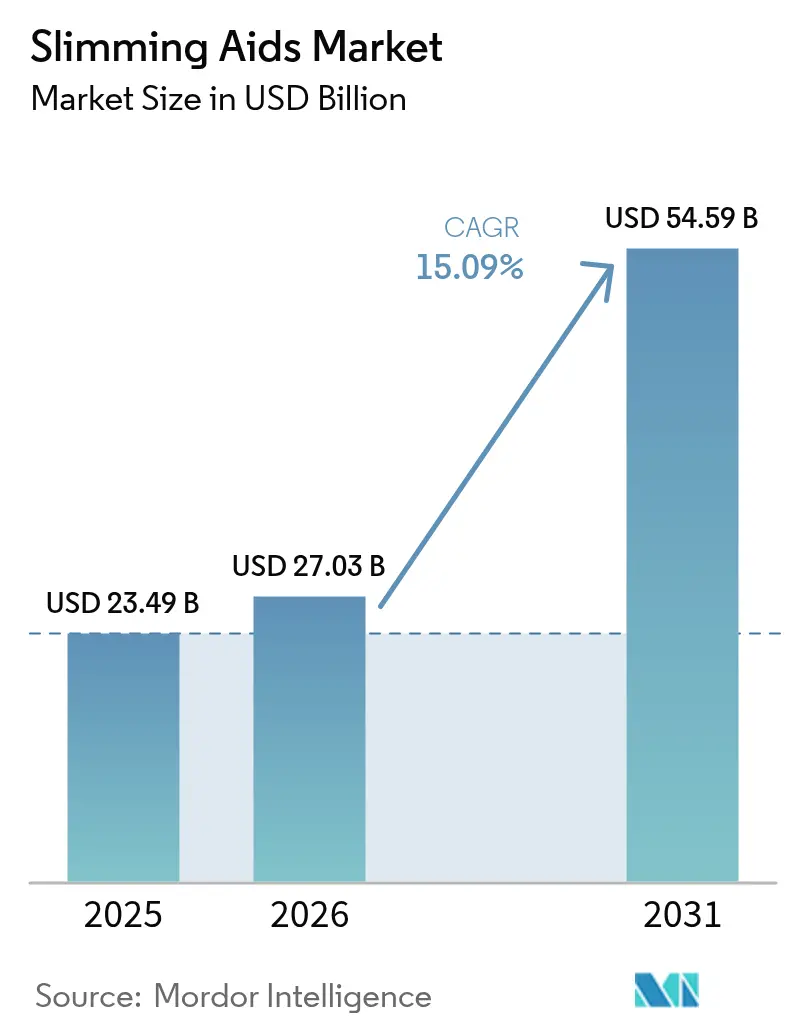

| Market Size (2026) | USD 27.03 Billion |

| Market Size (2031) | USD 54.59 Billion |

| Growth Rate (2026 - 2031) | 15.09% CAGR |

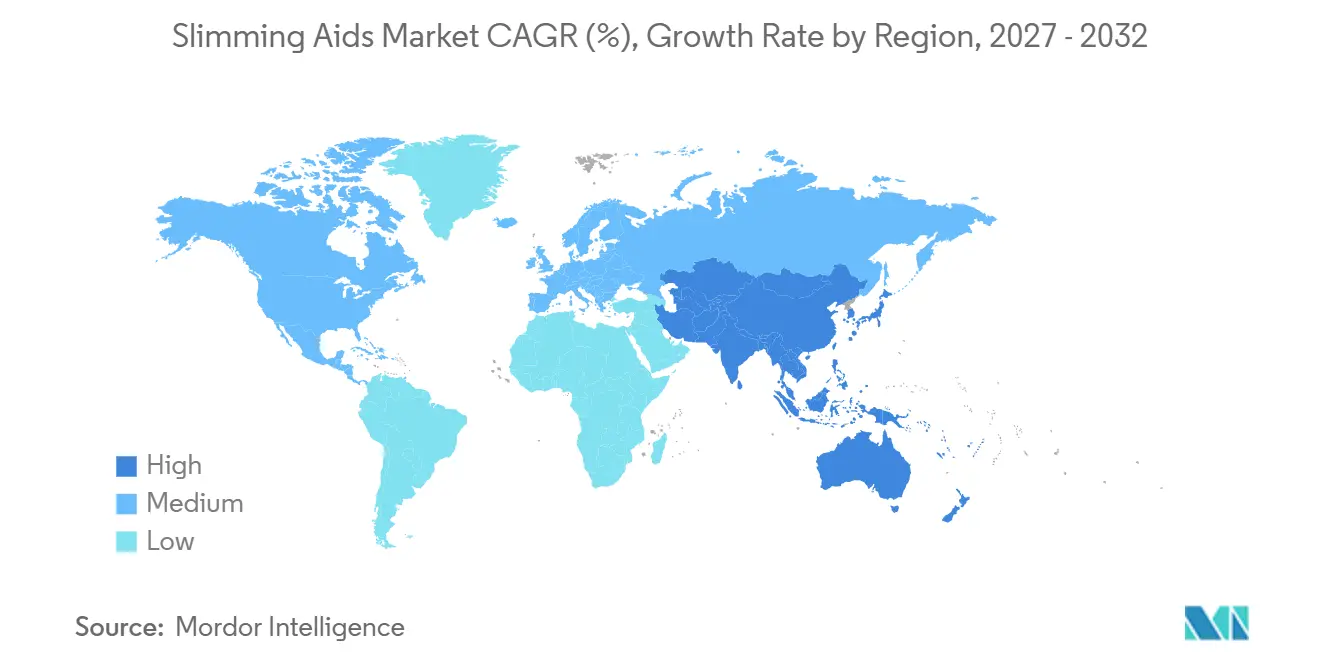

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

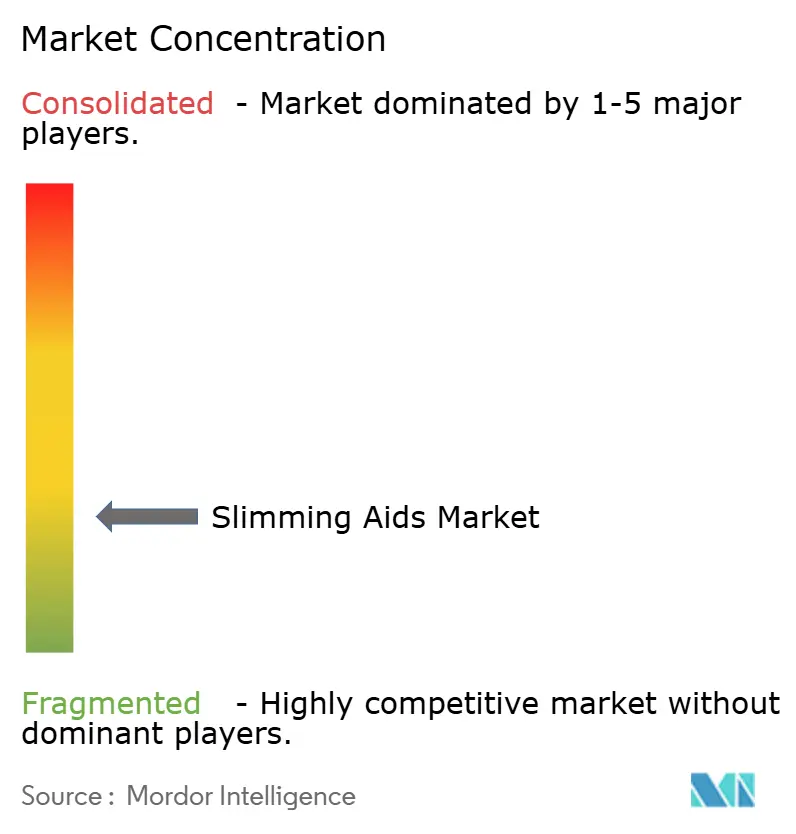

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slimming Aids Market Analysis by Mordor Intelligence

The Slimming Aids Market size is expected to grow from USD 23.49 billion in 2025 to USD 27.03 billion in 2026 and is forecast to reach USD 54.59 billion by 2031 at 15.09% CAGR over 2026-2031.

Consistent double-digit growth reflects the repositioning of obesity from a cosmetic issue to a chronic disease, the rapid approval cycle for next-generation GLP-1 drugs, and rising disposable incomes in emerging economies. Strong cardiovascular outcome data for semaglutide and tirzepatide are broadening payer coverage, while telehealth platforms shorten the prescription pathway and lift adherence rates. At the same time, the fitness ecosystem is integrating wearables and connected equipment that complement pharmacotherapy rather than compete with it. Competitive pressure is intense as meal-plan and supplement incumbents overhaul their portfolios to counter the clinical efficacy of injectable therapies.

Key Report Takeaways

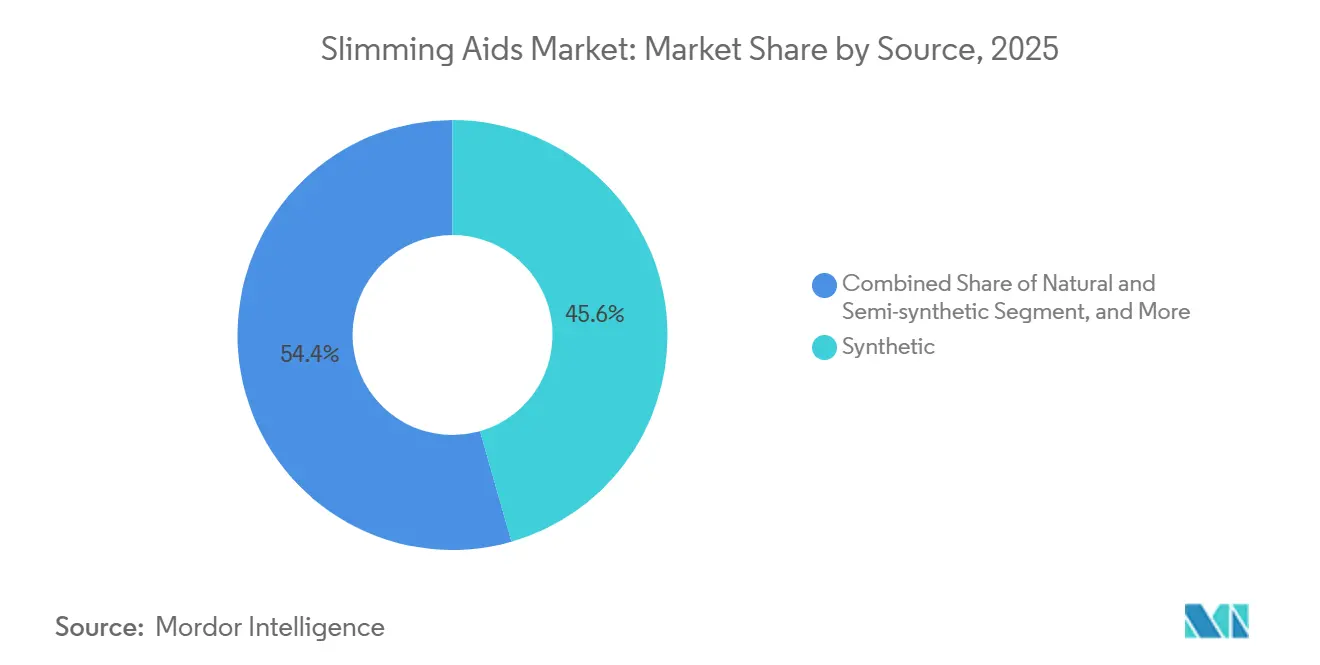

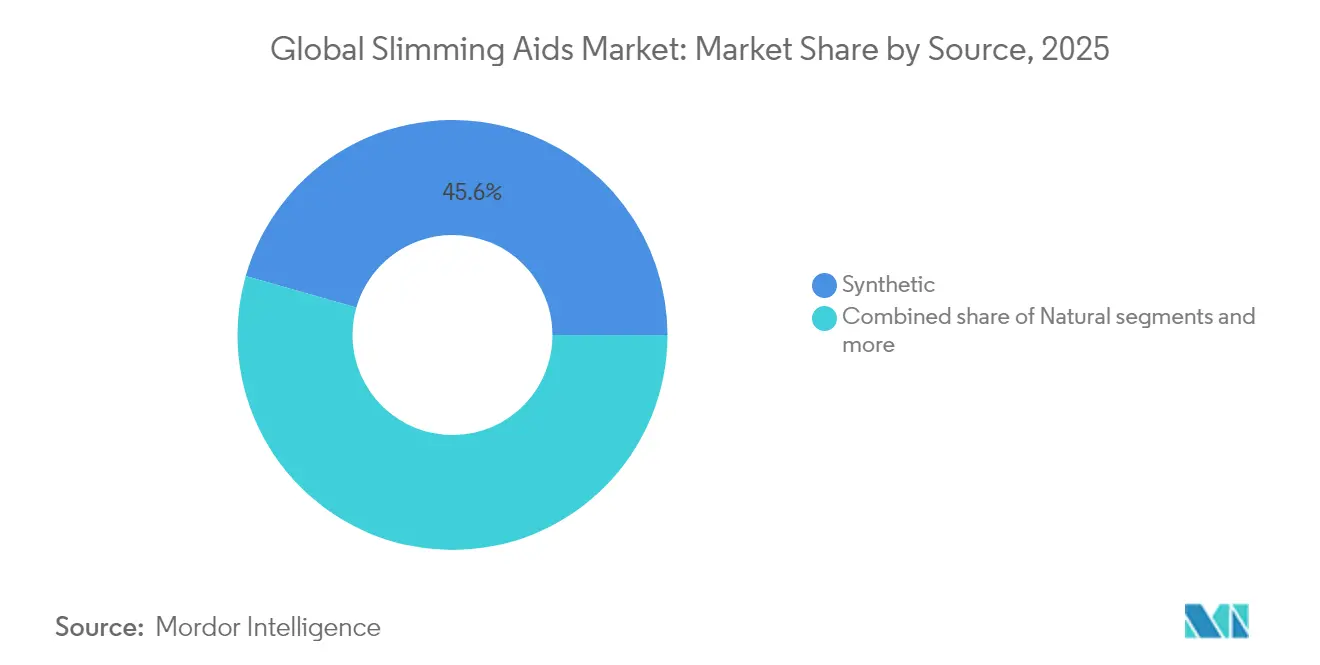

- By source, synthetic products accounted for 45.58% of the slimming aids market share in 2025, while natural formulations are projected to expand at a 16.02% CAGR through 2031.

- By product type, dietary supplements led with 36.74% revenue share in 2025; fitness equipment is forecast to post the fastest growth at 15.48% CAGR between 2026 and 2031.

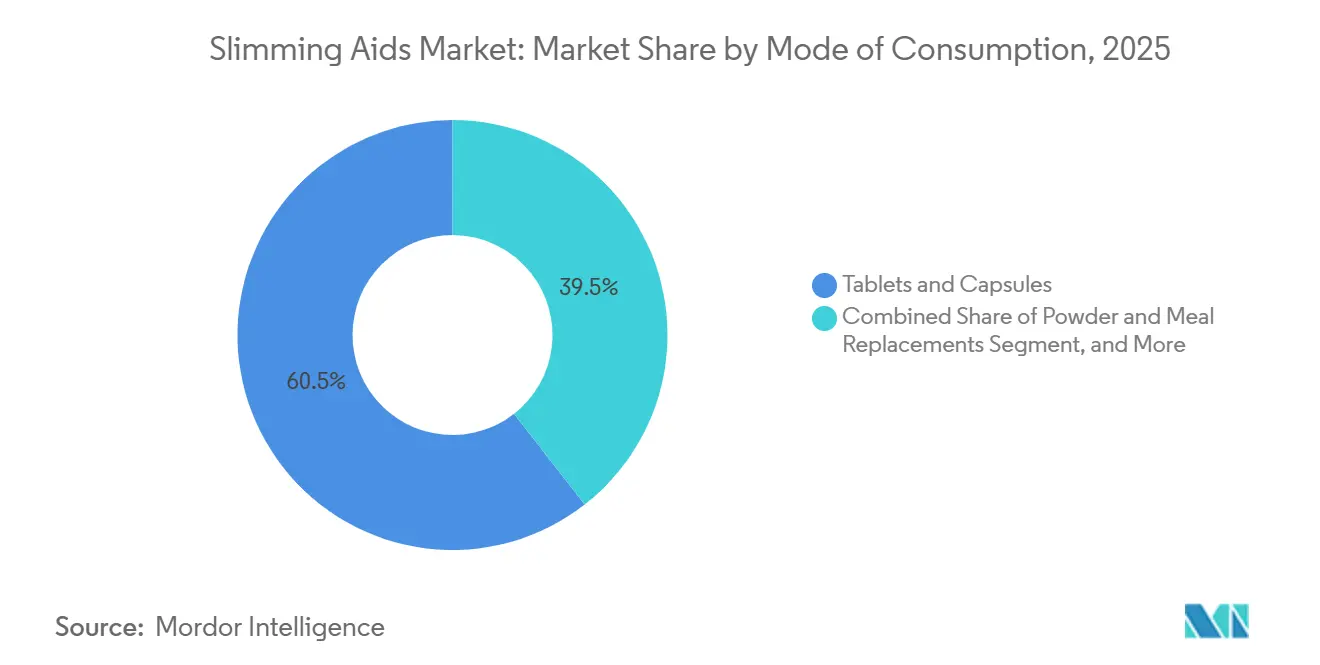

- By Mode of consumption, tablets and capsules accounted for 60.55% of consumption in 2025, whereas powder and meal-replacement formats are advancing at a 16.02% CAGR to 2031.

- By distribution channel, over-the-counter pharmacies accounted for 46.21% of distribution in 2025, while online and e-commerce channels are growing at a 16.45% CAGR through 2031.

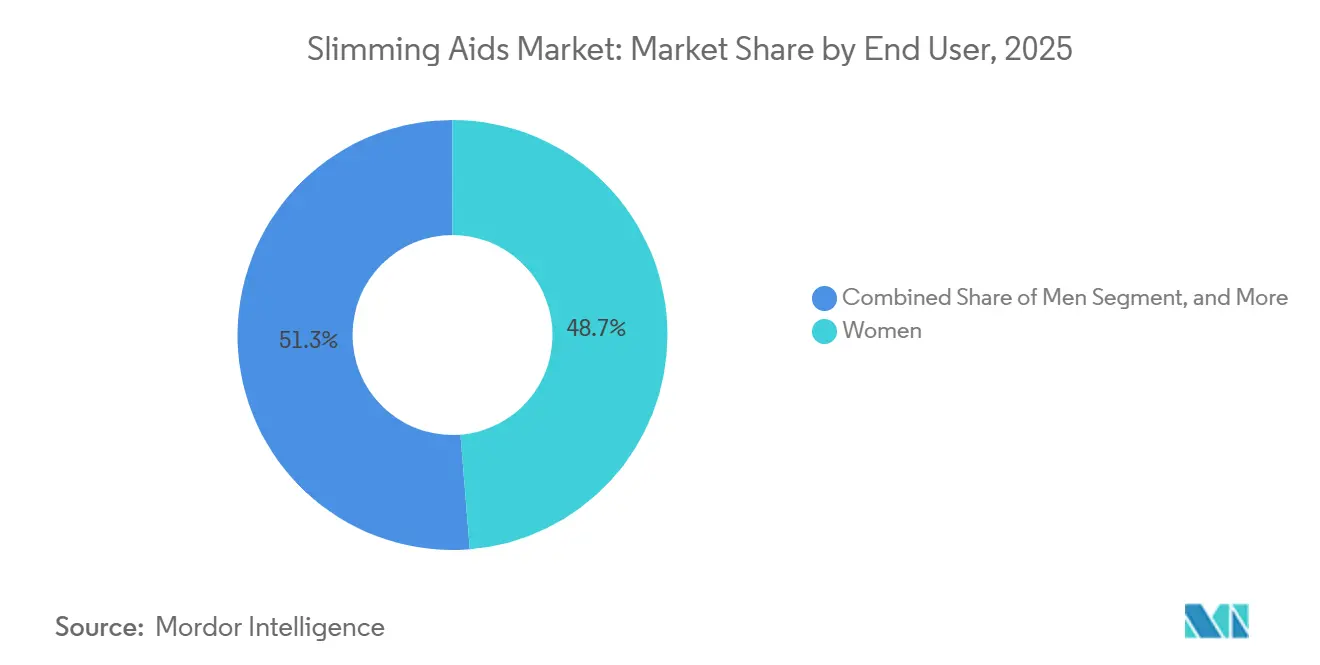

- By end user, women accounted for 48.72% of end users in 2025, but the male segment is projected to grow at a 15.79% CAGR, narrowing the historical gender gap.

- By geography, North America captured 41.87% of revenue in 2025, while Asia-Pacific is set to record the highest regional CAGR at 16.63% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Slimming Aids Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising global obesity prevalence | +3.5% | Global hot spots in North America, China, India, GCC | Long term (≥ 4 years) |

| Launches of GLP-1 & other novel pharmacological aids | +4.2% | North America, EU core, expanding to APAC & Latin America | Medium term (2-4 years) |

| Growing preference for natural & plant-based supplements | +2.8% | North America, EU, urban APAC | Medium term (2-4 years) |

| Subscription-based personalized digital ecosystems | +1.9% | North America lead, EU & APAC catching up | Short term (≤ 2 years) |

| Payer reimbursement pilots for anti-obesity drugs (EU) | +1.2% | Germany, UK, France, Nordics | Medium term (2-4 years) |

| APAC regulatory fast-tracks for microbiome products | +0.8% | Japan, South Korea, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Obesity Prevalence

The World Obesity Atlas 2025 projects that 1.13 billion adults will live with obesity by 2030, translating into an 18% prevalence in men and 21% in women.[1]World Obesity Federation, “World Obesity Day 2024: 1 Billion People Now Living with Obesity,” worldobesity.org China alone is forecast to register 41% of adults with an elevated body-mass index by 2025, straining public-health budgets and magnifying demand for reimbursable therapies. This epidemiological surge moves weight management from discretionary spending to medical necessity, expanding the slimming aids market across both premium pharmaceutical and value-priced supplement segments. Governments are beginning to fund preventive programs, yet eligibility hurdles and co-payments continue to bifurcate access. Manufacturers must therefore tailor their portfolios to vastly different willingness-to-pay thresholds across developed and emerging economies.

Launches of GLP-1 & Other Novel Pharmacological Aids

Semaglutide and tirzepatide deliver 15%-22% body-weight reductions in late-stage trials, eclipsing the 5%-10% efficacy of legacy therapies. Novo Nordisk has pledged USD 4.1 billion to scale U.S. manufacturing, while Eli Lilly is spending USD 9 billion globally, signaling long-term confidence in the prescription segment. Insurers are pivoting from exclusion to pilot reimbursement, especially for patients with diabetes or cardiovascular risks, shrinking the payback window on drug R&D. Subcutaneous delivery, however, deters needle-averse consumers and creates logistical headaches that oral analogs now in Phase III could resolve. Success hinges on balancing clinical superiority with convenience and cost.

Growing Preference for Natural & Plant-Based Supplements

Consumer distrust of synthetic stimulants intensified after multiple FDA recalls, pushing natural-source sales to a forecast 16.02% CAGR through 2031. Formulations leveraging green tea catechins, garcinia cambogia, and konjac root now emphasize satiety and microbiome modulation, positioning them as lifestyle adjuncts rather than cures. Kemin Industries’ potato-derived Slendesta highlights ingredient-level branding that reassures shoppers about provenance and third-party testing. Regulatory bodies are demanding randomized controlled trials for structure-function claims, weeding out opportunistic labels and raising R&D hurdles. Established nutraceutical houses with in-house labs are therefore seizing shelf space as smaller brands exit.

Subscription-Based Personalized Digital Ecosystems

Telehealth operators such as Noom and Hims & Hers combine prescribing, coaching, and fulfillment into monthly bundles that cost USD 120-180 per subscriber.[2]Robert Langreth, “Weight-Loss Drugs Ozempic, Wegovy, Mounjaro Face Supply Shortages,” Bloomberg, bloomberg.com Compounded semaglutide sold at a 30% discount widens access but invites FDA scrutiny over quality variance. User acquisition costs exceed USD 200, making long-term retention pivotal to breakeven. Cross-state medical licensing rules enable national reach, yet any tightening of compounding exemptions would erode the pricing edge and force renegotiation with brand-name manufacturers. Data-driven behavioral nudges are the moat: platforms that hold longitudinal biometric records can personalize dosage and content, boosting adherence and lifetime value.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Counterfeit & sub-standard slimming products | −1.5% | Global e-commerce, notably North America, EU, APAC | Short term (≤ 2 years) |

| Regulatory scrutiny over false marketing claims | −1.3% | North America & EU, rising in APAC | Medium term (2-4 years) |

| GLP-1 drug supply-chain capacity constraints | −1.8% | North America & EU shortages | Short term (≤ 2 years) |

| Consumer backlash to long-term pharmacotherapy side-effects | −1.1% | Early-adopter markets in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit & Sub-Standard Slimming Products

FDA lab tests uncovered hidden stimulants such as sibutramine in online supplements during 2024 sweeps, triggering public alerts and product seizures. In December 2025, customs agents intercepted fake Ozempic pens across Europe that contained no active ingredient. Marketplaces are tightening seller vetting, elevating listing costs, and slowing new-product onboarding. The reputational spillover depresses legitimate sales, particularly in natural categories that lack mandatory third-party assays. While blockchain batch-tracking and QR code verification are emerging countermeasures, their adoption remains patchy among smaller labels.

Regulatory Scrutiny Over False Marketing Claims

Seventeen U.S. companies received warning letters in 2024 for touting “rapid weight loss without diet or exercise,” a claim regulators deemed deceptive. The EU is enforcing pre-market approval under its Nutrition and Health Claims Regulation, pushing smaller entrants out due to the cost of randomized trials. Compliant firms can differentiate through certified claims, yet conservative messaging risks invisibility amid digital ad noise. Finding the sweet spot between evidence-based promotion and engaging storytelling is now a core marketing competency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Natural Formulations Gain Momentum

Natural products accounted for a minority of revenue in 2025, yet their 16.02% forecast CAGR far exceeds that of synthetic counterparts, indicating a structural pivot rather than a passing fad. In monetary terms, the slimming aids market size for natural formulations is on track to double by 2031 as consumers trade up to clean-label alternatives that promise gentler modes of action. Synthetic compounds, which still account for 45.58% of 2025 revenue, continue to dominate the slimming aids market share, driven by predictable pharmacokinetics and lower unit costs. However, synthetic-only portfolios face margin compression as retailers allocate more shelf space to branded botanicals backed by clinical dossiers. Premium natural blends priced 30%-50% above generic synthetics are gaining acceptance among urban millennials who equate plant-based products with safety and sustainability. Regional differentiation is pronounced: North America and Western Europe show the highest willingness to pay, whereas price-sensitive ASEAN markets remain synthetic-heavy. Over the next five years, co-formulations that pair plant extracts with low-dose synthetic enhancers could emerge as the compromise product, offering both efficacy and clean-label cues.

By Product Type: Fitness Equipment Disrupts Traditional Categories

In 2025, dietary supplements generated 36.74% of category revenue, but connected fitness equipment is projected to outpace every other product group with a 15.48% CAGR through 2031. Hardware makers are bundling resistance bands, smart scales, and AI-guided mirrors into subscription ecosystems that capture both upfront and recurring spend. The slimming aids market size attributable to fitness equipment is poised to rival supplements by the end of the decade if churn rates remain below 20%. Supplements remain essential for convenience-oriented consumers, yet are being commoditized as private-label penetration rises. Hardware-linked coaching not only improves workout compliance but also funnels personalized nutrition recommendations, encroaching on supplement territory.

By Mode of Consumption: Injectable Pens Reshape Delivery Preferences

Tablets and capsules comprised 60.55% of units sold in 2025, reflecting entrenched consumer habits and efficient manufacturing economics. Yet injectables, though a smaller volume category, are driving outsized dollar growth because a single pen of semaglutide can cost USD 1,000 per month in the United States. That pricing dynamic uplifts the slimming aids market share of injectable formats despite limited patient penetration. Powder and meal-replacement shakes are gaining popularity at a 16.02% CAGR as reformulations improve taste and mixability, catering to mobile lifestyles. Manufacturers are experimenting with stick sachets that dissolve instantly, sidestepping shaker-bottle inconvenience.

By Distribution Channel: E-Commerce Erodes Pharmacy Dominance

OTC pharmacies & drug stores captured 46.21% of 2025 sales, yet their dominance is eroding as the slimming aids market migrates online, driven by a 16.45% CAGR in e-commerce growth. Telehealth scripts paired with doorstep delivery eliminate the need for physical pickups, allowing platforms to capture dispensing margins. The slimming aids market is expected to surpass retail-pharmacy turnover before 2030 if current growth differentials persist. Amazon and regional marketplaces have introduced seller-verification programs to combat counterfeit risk, increasing compliance overhead but also elevating consumer trust once badges are earned. Hospital pharmacies retain relevance for patients with multiple comorbidities but are constrained by inpatient reimbursement limits.

By End User: Male Segment Narrows Gender Gap

Women accounted for 48.72% of end users in 2025, reflecting historical marketing and social pressures. However, male uptake is accelerating at 15.79% CAGR as campaigns reposition weight loss around cardiometabolic health rather than aesthetics. Digital clinics now feature male-centric landing pages highlighting reductions in myocardial infarction risk, resonating with an audience previously skeptical of “diet pills.” This shift enlarges the total slimming aids market, generating incremental revenue without cannibalizing female demand.

Geography Analysis

North America accounted for 41.87% of the Slimming aids market revenue in 2025, driven by high obesity prevalence and early adoption of GLP-1. U.S. payers increasingly reimburse anti-obesity drugs following strong cardiovascular data, while Canadian single-payer systems integrate GLP-1s into chronic-disease pathways. Direct-to-consumer models, such as LillyDirect, streamline distribution and bolster adherence through two-day delivery.

Asia-Pacific is the fastest-growing region, with a 16.63% CAGR, driven by expanding middle-class populations and proactive government policies. India exemplifies the convergence of rising income and high unmet medical need, with the Slimming aids market size projected to more than double by 2028. Chinese biosimilar entrants will likely compress prices and catalyze volume expansion.

Europe maintains a premium positioning with rigorous EMA oversight that validates therapeutic safety. German sickness funds pilot outcome-based reimbursements, while the U.K. navigates post-Brexit supply logistics. South America and the Middle East & Africa contribute smaller shares but hold long-run optionality as healthcare access improves and pricing pressure eases.

Competitive Landscape

The slimming aids market is moderately fragmented. Pharmaceutical leaders Novo Nordisk and Eli Lilly monopolize the prescription segment with vertically integrated peptide manufacturing and multibillion-dollar capacity expansions, yet their reliance on injectables leaves room for oral analog disruptors. Digital-native challengers Hims & Hers and Noom combine telehealth prescribing, logistics, and behavioral coaching, siphoning margin from pharmacies and benefits managers. The legacy supplement field comprises hundreds of regional players competing on price, many of whom lack the clinical validation now demanded by regulators.

Strategic moves underscore technology’s rising importance. Eli Lilly’s 2024 direct-to-consumer portal bypasses pharmacy benefit managers and could presage broader channel disintermediation. Novo Nordisk’s big-game advertising of once-daily Wegovy tablets illustrates a pivot toward mass-market positioning that normalizes pharmacotherapy. Nutrition companies are deploying continuous glucose monitors and AI-driven meal plans to maintain relevance amid pharmaceutical encroachment. Microbiome startups leverage APAC fast-tracks to pilot novel synbiotics, while formulation innovators explore transdermal patches to eliminate injections.

Competitive intensity is highest in North America and Western Europe, where reimbursement and digital infrastructure support premium pricing. Asia-Pacific is witnessing price disruption as domestic generic manufacturers reverse-engineer peptide synthesis, undercutting multinationals by up to 40%. Margin compression will likely spark consolidation among second-tier supplement labels that cannot fund robust clinical trials or digital upgrades. Over the forecast horizon, the ability to guarantee uninterrupted drug supply, demonstrate real-world effectiveness, and maintain high engagement through digital ecosystems will determine share capture.

Slimming Aids Industry Leaders

Glanbia Plc.

Amway Corp.

Novo Nordisk A/S

Nestlé Health Science

Herbalife Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Telehealth company Hims & Hers announced the launch of a lower-priced compounded alternative to Wegovy, positioning it as an affordable entry point for GLP-1 therapy.

- February 2026: Eli Lilly disclosed USD 1.5 billion in pre-launch inventory for its oral weight-loss candidate orforglipron, underscoring preparation for large-scale rollout.

- February 2026: The FDA unveiled plans to intensify inspections of active pharmaceutical ingredients used by compounders producing GLP-1 drugs, aiming to curb quality variation.

- February 2026: Novo Nordisk aired its first Super-Bowl-style commercial promoting once-daily Wegovy tablets, signaling mainstream targeting of oral formulations.

- December 2025: Novo Nordisk introduced Ozempic in India at a weekly cost of USD 24.35, targeting a rapidly expanding diabetes and obesity market.

Global Slimming Aids Market Report Scope

As per the scope of the report, slimming aids are dietary supplements that are intended to help an individual lose weight and manage weight. Slimming aids are of various types based on their ingredients and consumption methods, such as dietary pills, special teas, weight-loss powders, etc. The slimming aids market is segmented by product type, mode of consumption, and geography. By product type, it is segmented into natural, synthetic, and semi-synthetic. The mode of consumption is segmented into tables and capsules, powder, syrups, and injection. By geography, it is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above-mentioned segments.

| Natural |

| Synthetic |

| Semi-Synthetic |

| Dietary Supplements |

| Meal Replacements |

| Pharmeuticals (RX and OTC) |

| Fitness Equipment |

| Tablets & Capsules |

| Powder & Meal Replacements |

| Syrups & Liquids |

| Injectable Pens |

| Transdermal & Novel Delivery Systems |

| Hospital & Prescribed Retail Pharmacies |

| OTC Pharmacies & Drug Stores |

| Online / E-commerce |

| Specialist Weight-loss Clinics |

| Women |

| Men |

| Children & Adolescents |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Natural | |

| Synthetic | ||

| Semi-Synthetic | ||

| By Product Type | Dietary Supplements | |

| Meal Replacements | ||

| Pharmeuticals (RX and OTC) | ||

| Fitness Equipment | ||

| By Mode of Consumption | Tablets & Capsules | |

| Powder & Meal Replacements | ||

| Syrups & Liquids | ||

| Injectable Pens | ||

| Transdermal & Novel Delivery Systems | ||

| By Distribution Channel | Hospital & Prescribed Retail Pharmacies | |

| OTC Pharmacies & Drug Stores | ||

| Online / E-commerce | ||

| Specialist Weight-loss Clinics | ||

| By End User | Women | |

| Men | ||

| Children & Adolescents | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Global Slimming Aids Market?

The Global Slimming Aids Market size is expected to reach USD 27.03 billion in 2026 and grow at a CAGR of 15.09% to reach USD 54.59 billion by 2031.

What is the current Global Slimming Aids Market size?

In 2026, the Global Slimming Aids Market size is expected to reach USD 27.03 billion.

Who are the key players in Global Slimming Aids Market?

Amway, Nestle SA, Glanbia Plc., Herballife Nutrition Ltd. and Novo Nordisk are the major companies operating in the Global Slimming Aids Market.

Which is the fastest growing region in Global Slimming Aids Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Slimming Aids Market?

In 2025, the North America accounts for the largest market share in Global Slimming Aids Market.

Page last updated on: