Paper Padded And Cushioned Mailers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

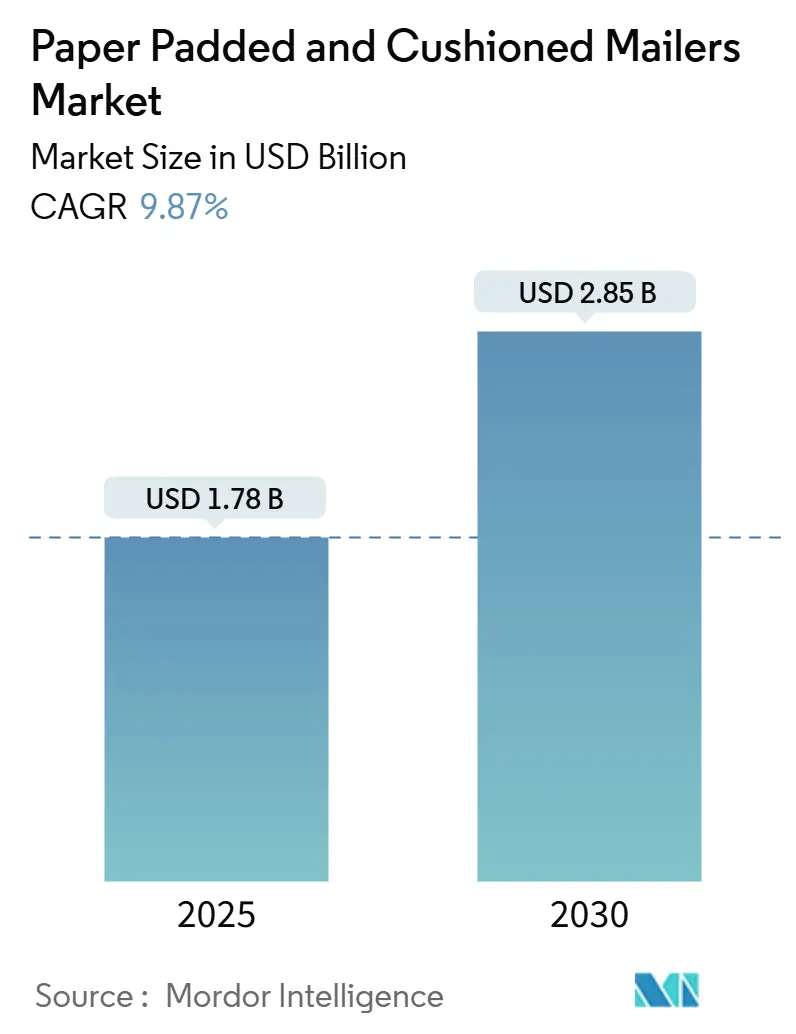

| Market Size (2025) | USD 1.78 Billion |

| Market Size (2030) | USD 2.85 Billion |

| Growth Rate (2025 - 2030) | 9.87% CAGR |

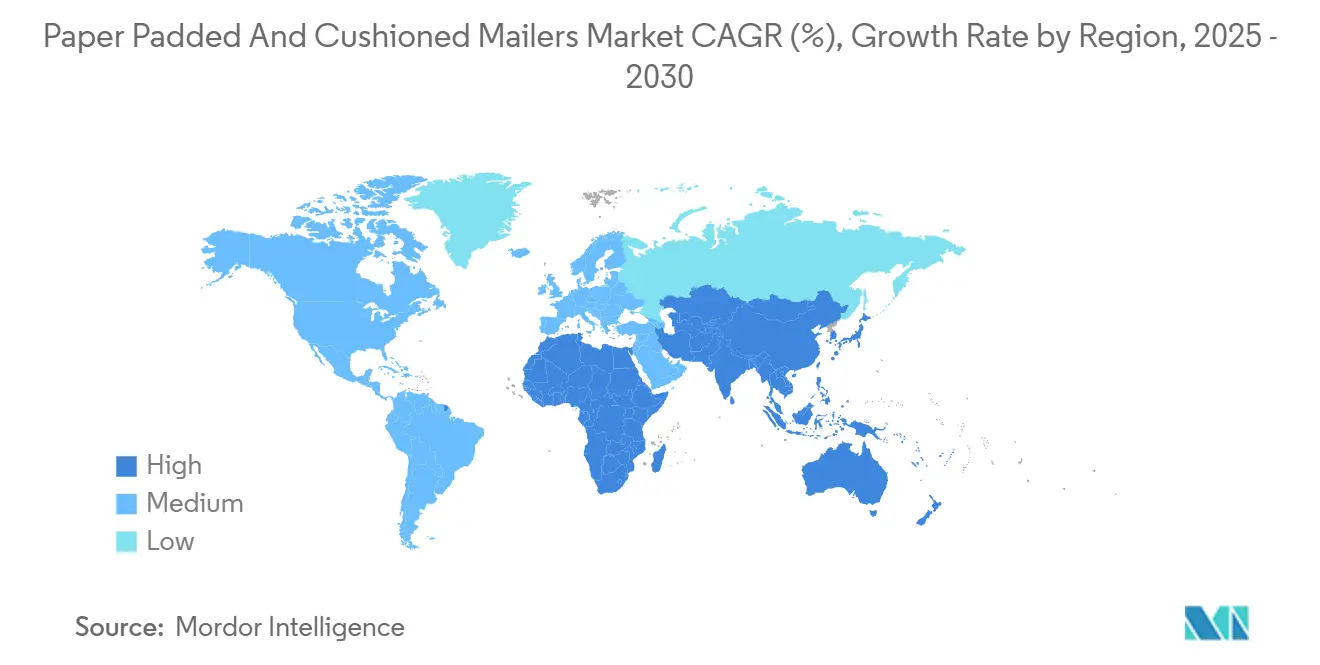

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

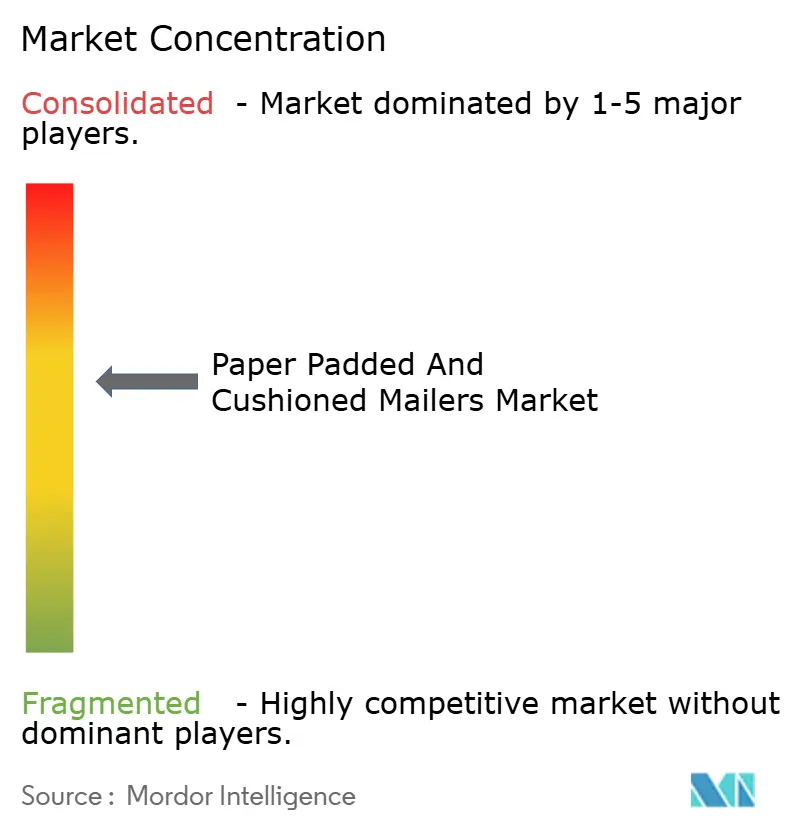

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper Padded And Cushioned Mailers Market Analysis by Mordor Intelligence

The paper padded and cushioned mailers market size is valued at USD 1.78 billion in 2025 and is projected to reach USD 2.85 billion by 2030, growing at a 9.87% CAGR over the forecast period. Rising e-commerce parcel volumes, regulatory pressure to curb plastic use, and cost advantages tied to dimensional-weight rules are collectively accelerating the shift toward lightweight, curbside-recyclable mailers. North America maintains its leadership due to a mature fulfillment infrastructure, while the Asia-Pacific region supplies most of the incremental volume as national online marketplaces penetrate smaller cities. Material innovation, such as honeycomb cores and on-site right-sizing automation, enables manufacturers to deliver performance with less fiber. Industry consolidation, exemplified by the merger of Smurfit and WestRock, amplifies the bargaining power of global suppliers that can combine scale with sustainability credentials.

Key Report Takeaways

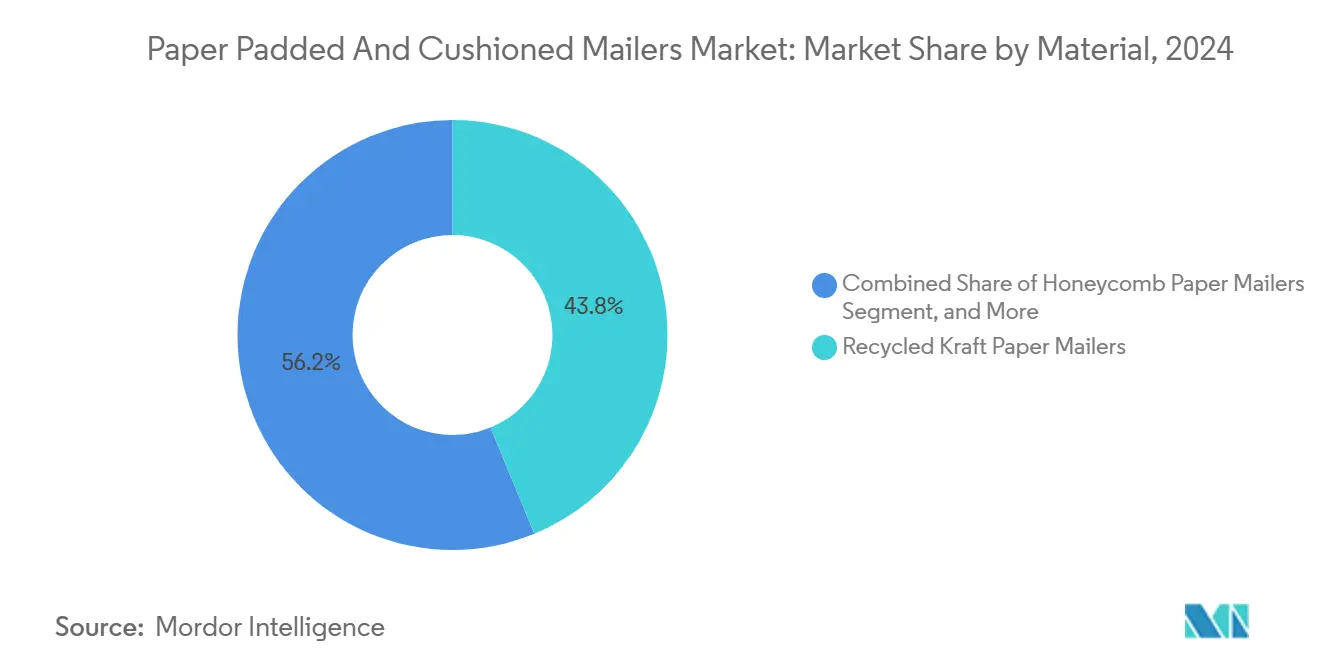

- By material, recycled kraft paper mailers captured 43.78% of the paper padded and cushioned mailers market share in 2024.

- By cushioning technology, paper padded and cushioned mailers market size for honeycomb cores is projected to grow at 12.19% CAGR between 2025–2030.

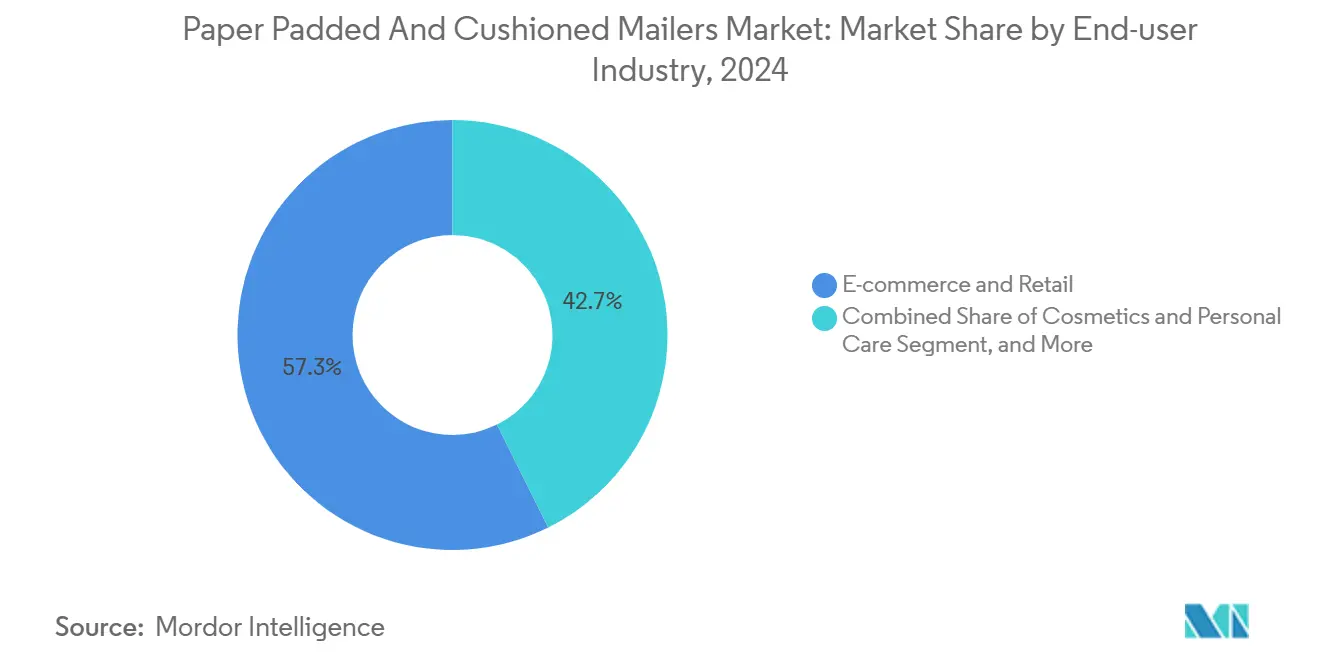

- By end-user industry, e-commerce and retail captured 57.34% of the paper padded and cushioned mailers market share in 2024.

- By closure type, paper padded and cushioned mailers market size for dual peel-and-seal systems is projected to grow at 11.38% CAGR between 2025–2030.

- By geography, North America captured 36.45% of the paper padded and cushioned mailers market share in 2024.

Global Paper Padded And Cushioned Mailers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce parcel volumes | +2.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Shift toward curbside-recyclable packaging | +2.1% | North America and European Union, expanding to Asia-Pacific | Long term (≥4 years) |

| Dim-weight postal cost savings | +1.4% | Global, particularly North America and Europe | Short term (≤2 years) |

| Plastic-reduction regulations and mandates | +1.9% | European Union core, spill-over to North America and Asia-Pacific | Medium term (2-4 years) |

| On-site automated right-size production | +1.2% | North America and Europe, early adoption | Long term (≥4 years) |

| Honeycomb cushioning innovations | +0.6% | Global, manufacturing hubs in Europe and Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Parcel Volumes

Rapid parcel growth increases packaging demand, prompting shippers to adopt lighter formats that minimize freight costs and reduce handling damage. China and India together generated more than half of the Asia-Pacific’s incremental online orders in 2024, forcing brands to ship directly to smaller cities with longer transit chains. Flexible mailers withstand multiple sortation cycles better than rigid cartons, enabling cost-effective cross-border shipping within airline volumetric limits. Platforms refine packaging algorithms to automatically select the lightest compliant mailer, reinforcing a systematic preference for paper-padded and cushioned mailer market solutions.

Shift toward Curbside-Recyclable Packaging

Brands publicize zero-plastic commitments to meet consumer demand for effortless recycling. Amazon’s European operations are phasing out non-recyclable mailers by 2030, prompting suppliers to migrate to mono-material paper formats.[1]Source: Amazon Sustainability Team, “Sustainable Packaging,” amazon.com Extended producer responsibility fees add direct cost pressure, whereas readily recyclable paper avoids penalties. Surveys show that 73% of shoppers are willing to pay a premium for eco-friendly packaging, aligning financial gain with environmental goals. Consequently, the paper-padded and cushioned mailers market gains durable demand across premium and mass retail segments.

Dim-Weight Postal Cost Savings

Carriers charge by whichever is greater, actual weight or volumetric weight, raising costs for bulky boxes. Paper mailers typically weigh 30-40% less than corrugated cartons yet provide equivalent protection, especially in the 1-3 pound category favored by online retailers. The United States Postal Service’s 2024 dimensional-weight threshold revision magnified these savings for shippers using the paper-padded and cushioned mailers market formats. International express lanes, where every gram counts, further reinforce the adoption of logistics algorithms that auto-populate paper as the default container.

Plastic-Reduction Regulations and Retailer Mandates

Binding rules, such as California SB 54 and the European Union Packaging and Packaging Waste Regulation, increase the cost of plastic mailers through fees and recycled-content quotas. Retailers pre-empt penalties by switching to paper. Multi-national campaigns publicizing plastic exit roadmaps place additional reputational pressure on laggards. These combined push-and-pull forces sustain momentum for the paper-padded and cushioned mailers market across regulated and soon-to-be-regulated jurisdictions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled paper feedstock price volatility | -1.8% | Global, acute in North America and Europe | Short term (≤2 years) |

| Moisture-resistance limitations vs poly mailers | -1.2% | Global, particularly humid Asia-Pacific climates | Medium term (2-4 years) |

| Price competition from poly-bubble mailers | -0.9% | Global, cost-sensitive segments | Short term (≤2 years) |

| Postal-sorting jams and surcharge risks | -0.7% | North America and Europe postal systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycled Paper Feedstock Price Volatility

Old corrugated cardboard spot prices fluctuated between USD 85 and USD 165 per ton in 2024, as Asian import demand softened and logistical bottlenecks persisted. Such fluctuations squeeze recycled kraft mailer margins, prompting periodic shifts toward virgin fiber that dilute sustainability narratives. Mills hedge pulp exposures yet still face weekly adjustments that complicate contract pricing in the paper-padded and cushioned mailers market.

Moisture-Resistance Limitations versus Poly Mailers

Paper loses cushioning integrity under sustained 80% relative humidity, with tests showing a drop of up to 15% in compression strength after four days. Poly mailers outperform in tropical or extended-transit lanes, thereby narrowing the addressable share for paper within pharmaceuticals and electronics that require stringent barrier properties. Although specialty coatings mitigate absorption, most compromise recyclability, forcing trade-offs that temper the universal replacement of materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Content Drives Market Leadership

Recycled kraft substrates captured the largest 43.78% share of the paper-padded and cushioned mailers market in 2024, driven by widespread collection networks and cost competitiveness. Volumes remain resilient despite feedstock volatility because corporate buyers secure supply under multi-year take-or-pay contracts. Honeycomb-lined paper mailers are projected to grow at a 11.27% CAGR, driven by their 25% lower carbon footprint and superior shock absorption, which meets electronics drop-test limits. Virgin Kraft continues to serve premium SKUs where surface finish and color uniformity underpin brand positioning.

Macerated newsprint padding appeals to cost-sensitive sellers; however, its availability is eroding due to the global decline in newsprint production. Hybrid paper-poly constructions retain a niche use where partial barrier properties justify the use of mixed materials, although looming recyclability mandates limit their future scope. Investment signals underline the trajectory. International Paper allocated USD 1.2 billion to expand its recycled containerboard operations, ensuring a long-term fiber supply for protective mailers.[2]Source: International Paper Communications, “Major Investment in Recycled Containerboard,” internationalpaper.com In parallel, start-ups commercialize ASTM-certified compostable grades aimed at organic food delivery, demonstrating that the paper-padded and cushioned mailers market can meet both circularity and performance demands.

By Cushioning Technology: Honeycomb Innovation Leads Growth

Macerated padding held a 39.56% market share in 2024, driven by low machine conversion costs and broad machinery availability. Yet honeycomb cores race ahead at a 12.19% CAGR by fusing aerospace-grade hexagonal design into lightweight parcel protection. Shock absorption improves by up to 40% with 30% less fiber compared to traditional pads, which aligns with consumer electronics shippers seeking lower return rates. Corrugated flute inserts are suitable for mid-tier applications, while bubble-paper laminates struggle to scale due to the mixed materials that hinder single-stream recycling.

Expanded molded fiber proves promising for custom shapes; however, tooling costs restrict its uptake to high-margin segments. Automation cements honeycomb advantage. Packsize’s on-demand lines cut and glue cells in under ten seconds, synchronizing with fulfillment systems that feed real-time SKU dimensions. Patent activity at the United States Patent and Trademark Office increased by 34% in 2024, signaling an intensifying rivalry to secure intellectual property around structural geometry.

By End-user Industry: E-commerce Dominance with Electronics Growth

E-commerce and retail channels accounted for 57.34% of revenue in 2024, reflecting the extensive parcel networks established by marketplaces and direct-to-consumer labels. Consistent sizing, high parcel density, and algorithm-driven selection reinforce their heavy reliance on the paper-padded and cushioned mailers market. Consumer electronics grow at the fastest rate, with a 11.16% CAGR, as brands ship premium phones and accessories directly to households, valuing both drop protection and unboxing aesthetics. Cosmetics leverage the printable surface to reinforce sustainability messaging that aligns with brand identity. Books and media maintain a stable customer base anchored in publisher preferences for low-cost yet protective mailers, even as digital formats expand.

Pharmaceuticals, automotive spares, and industrial components round out smaller segments where regulatory or technical parameters dictate specialized formats. Apple’s shift to fiber-based packaging showcases how flagship electronics brands validate paper as a luxury-compatible solution, reinforcing uptake by mid-tier competitors. Similarly, FDA guidelines for tamper evidence incentivize drug makers to adopt reinforced closures, blending compliance and environmental credibility within the paper-padded and cushioned mailers industry.

By Closure Type: Self-Seal Convenience Drives Adoption

Self-seal adhesives controlled 67.53% of the paper-padded and cushioned mailers market size in 2024, as they streamline packing lines and reduce labor time per order. Dual peel-and-seal variations are projected to grow at an 11.38% CAGR, enabling hassle-free returns and tapping into circular economy narratives. Heat-seal formats serve niches that require tamper-evident packaging, particularly within pharmaceuticals shipped through cold-chain corridors. Resealable zip or hook-and-loop closures cater to premium retail where user experience differentiates offerings. Tamper-evident tape remains an economical retrofit option yet lags in automation compatibility.

Fulfillment centers favor solutions that integrate with robotics. CMC’s Genesys Compact line finishes a right-sized adhesive mailer in 12 seconds, underscoring operational efficiencies that tie directly to closure selection. Amazon’s frustration-free packaging scorecard awards points for easy-open and recyclable seals, influencing thousands of sellers to adopt advanced adhesive formats.

Geography Analysis

North America held 36.45% revenue share in 2024, powered by a mature parcel ecosystem, sophisticated automation, and state-level plastic reduction statutes. The U.S. market benefits from the United States Postal Service's dimensional-weight thresholds that inherently reward lightweight packaging. Canada’s Federal Plastics Registry adds administrative pressure, which speeds retailer migration to paper formats, while Mexico’s double-digit e-commerce expansion offers adjacent growth opportunities for cross-border suppliers within the paper-padded and cushioned mailers market. Supply chains leverage abundant recycled fiber from domestic recovery programs, thereby reducing raw material cost volatility compared to their overseas peers. Automation costs are offset by high labor rates, making robotic right-sizing financially compelling across large fulfillment hubs.

The Asia-Pacific region is expected to deliver the fastest growth, with a 10.68% CAGR through 2030, driven by significant increases in parcel volume and government initiatives to curb plastic waste. China and India jointly contribute over half the incremental demand, driven by marketplace penetration into tier-3 and rural geographies that lengthen delivery chains. Japan’s engineering base contributes machine design advances that shorten line changeovers and improve honeycomb production yields. South Korea’s electronics exporters demand shock-resistant mailers capable of direct international shipping without outer cartons, further elevating technical specifications in the region. Cost advantage accrues from densely clustered mills that can scale sustainable substrates at attractive price points, although quality variability and humidity pose ongoing challenges.

Europe advances steadily under stringent regulatory guidance. The European Union Packaging and Packaging Waste Regulation imposes mandatory recycled-content targets that systematically favor the paper padded and cushioned mailers market. Germany’s closed-loop infrastructure underpins high collection rates that enhance fiber security. The United Kingdom, operating separate trade protocols after Brexit, stimulates domestic paper packaging plants seeking to offset rising import checks. Stora Enso’s EUR 500 million (USD 565 million) capacity investment emphasizes supplier commitment to the region’s growth vector.[3]Source: Stora Enso Investor Relations, “Investment in Sustainable Packaging Solutions,” storaenso.comExtended producer responsibility fees applied on non-recyclable mailers tighten economic calculus in favor of paper across sectors.

Competitive Landscape

Moderate consolidation defines the paper-padded and cushioned mailers market. The July 2024 Smurfit WestRock tie-up formed a USD 20 billion entity with integrated mills and converting sites spanning North America and Europe, enabling synchronized raw material sourcing and R&D scale. International Paper’s USD 1.2 billion acquisition of DS Smith diversified its European recycled containerboard footprint, underscoring a strategic pivot toward circular substrates. These headline moves elevate entry barriers for regional converters that lack automated plants or vertically integrated fiber.

Technology leadership, rather than price, dictates share gains. Packsize, Sealed Air, and CMC commercialize robotic lines that customize mailers to SKU dimensions, often reducing fiber use by 30% and enabling savings to be passed on to shippers. Patent filings related to honeycomb architecture surged in 2024, as incumbents secured structural innovations that enhance compression performance at lower grammages. Sustainability credentials serve as a gating criterion for platform partnerships; Amazon and other marketplaces issue scorecards that expressly weight recyclability, disadvantaging vendors with mixed-material portfolios.

White-space niches remain. Moisture-resistant coatings, biodegradable barriers, and molded-fiber inserts tailored to fragile electronics constitute areas where start-ups can out-innovate giants. Huhtamaki’s ISO 14855 certification for compostable coatings illustrates first-mover advantage in regulatory pathfinding. Mid-market converters collaborate with material science ventures to leapfrog older poly laminated lines, thereby preserving relevance in the evolving paper padded and cushioned mailers industry.

Paper Padded And Cushioned Mailers Industry Leaders

Sealed Air Corporation

Pregis LLC

Mondi plc

Intertape Polymer Group Inc.

Supremex Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SIG Group partnered with PulPac to launch dry molded fiber-based closures, aiming to replace plastic components in mailers and cartons with recyclable paper-based alternatives.

- April 2025: Novolex completed a major acquisition of Pactiv Evergreen, strengthening its position in sustainable mailers and expanding its fiber-based packaging portfolio.

- April 2025: IPL and Schoeller Allibert have formed a new entity in the reusable plastic packaging sector. The merger boasts a combined annual revenue exceeding USD 1.4 billion, marking a notable surge from their standalone earnings.

- June 2024: Pregis unveiled Renew Honeycomb Mailers, which combine kraft paper with honeycomb cushioning for enhanced protection and sustainability, targeting the electronics and cosmetics sectors.

Global Paper Padded And Cushioned Mailers Market Report Scope

| Virgin Kraft Paper Mailers |

| Recycled Kraft Paper Mailers |

| Honeycomb-Lined Paper Mailers |

| Macerated Newsprint Padded Mailers |

| Hybrid Paper-Poly Mailers |

| Macerated Paper Padding |

| Honeycomb Paper Core |

| Corrugated Flute Padding |

| Bubble-Paper Laminate |

| Expanded Molded-Fiber Inserts |

| E-commerce and Retail |

| Consumer Electronics |

| Cosmetics and Personal Care |

| Books and Media |

| Other End-user Industries |

| Self-Seal |

| Heat-Seal |

| Dual Peel and Seal / Reusable |

| Resealable Zip / Velcro |

| Tamper-Evident Tape Applied |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material | Virgin Kraft Paper Mailers | ||

| Recycled Kraft Paper Mailers | |||

| Honeycomb-Lined Paper Mailers | |||

| Macerated Newsprint Padded Mailers | |||

| Hybrid Paper-Poly Mailers | |||

| By Cushioning Technology | Macerated Paper Padding | ||

| Honeycomb Paper Core | |||

| Corrugated Flute Padding | |||

| Bubble-Paper Laminate | |||

| Expanded Molded-Fiber Inserts | |||

| By End-user Industry | E-commerce and Retail | ||

| Consumer Electronics | |||

| Cosmetics and Personal Care | |||

| Books and Media | |||

| Other End-user Industries | |||

| By Closure Type | Self-Seal | ||

| Heat-Seal | |||

| Dual Peel and Seal / Reusable | |||

| Resealable Zip / Velcro | |||

| Tamper-Evident Tape Applied | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the paper padded and cushioned mailers market in 2025?

It is valued at USD 1.78 billion and is projected to reach USD 2.85 billion by 2030.

Which region leads the current demand for paper-padded and cushioned mailers?

North America accounts for 36.45% of global revenue, driven by mature parcel networks and dimensional-weight shipping policies.

What is the fastest-growing end-user segment for these mailers?

Consumer electronics shipments show the highest 11.16% CAGR thanks to direct-to-consumer sales requiring premium cushioning.

Why are honeycomb-lined mailers gaining share?

Honeycomb cores deliver superior shock absorption with 30% less fiber, enabling an 11.27% CAGR within the segment.

How do dimensional weight rules benefit paper mailers?

Lightweight mailers reduce billed shipping weight under carrier formulas, saving 30-40% versus rigid cartons while meeting protection standards.

What impact do plastic-reduction regulations have on adoption?

Binding targets in the European Union and U.S. states raise compliance costs for plastic mailers, making recyclable paper alternatives more economical.

Page last updated on: