India Software Services Export Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

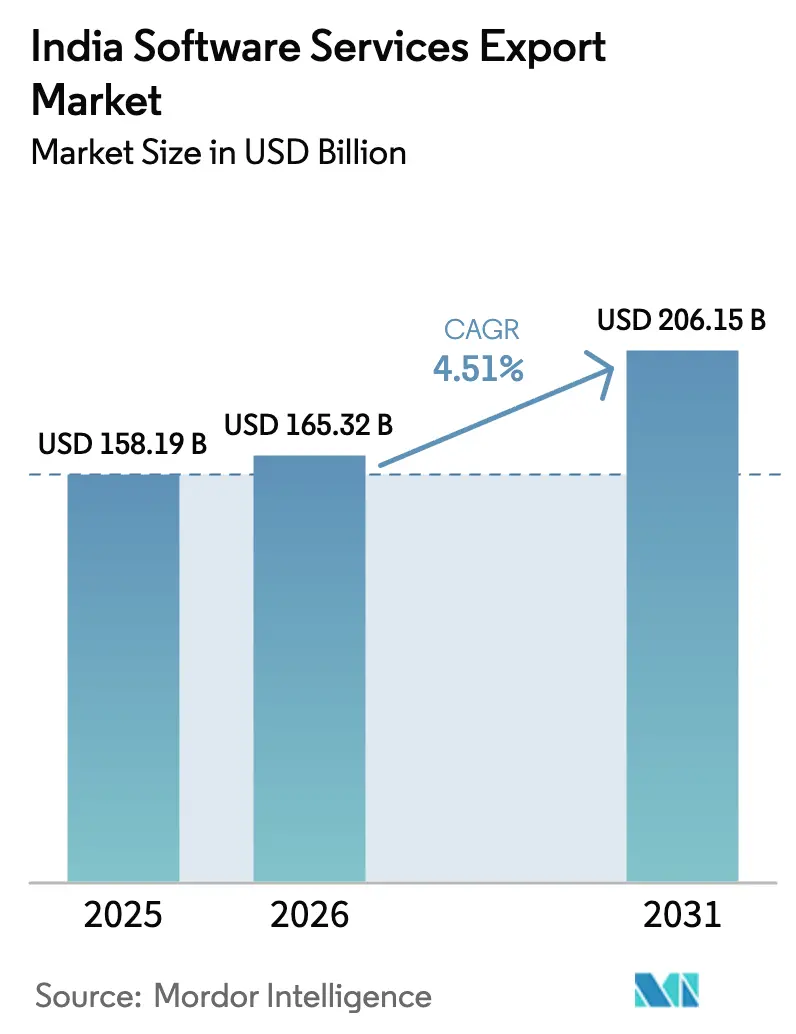

| Base Year Market Size (2025) | USD 158.19 Billion |

| Market Size (2026) | USD 165.32 Billion |

| Market Size (2031) | USD 206.15 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Software Services Export Market Analysis by Mordor Intelligence

The India software services export market size is expected to grow from USD 158.19 billion in 2025 to USD 165.32 billion in 2026 and is forecast to reach USD 206.15 billion by 2031 at 4.51% CAGR over 2026-2031. Its growth rests on a structural shift from pure cost-arbitrage contracts toward value-driven innovation partnerships that embed Indian teams inside clients’ product roadmaps and governance frameworks. Demand is amplified by India’s 55% share of global IT outsourcing, a workforce of more than 5 million professionals, and 1,650 global capability centers (GCCs) employing 1.6 million people. Macro forces including accelerated AI and machine-learning adoption in banking and insurance, government production-linked incentives, and a persistently weak rupee reinforce the competitive edge that Indian vendors hold in multi-year digital-transformation deals. Simultaneously, Japan’s mid-tier firms are pivoting toward near-shore partnerships with India because bilingual staffing and quality governance increasingly outweigh pure wage considerations.

Key Report Takeaways

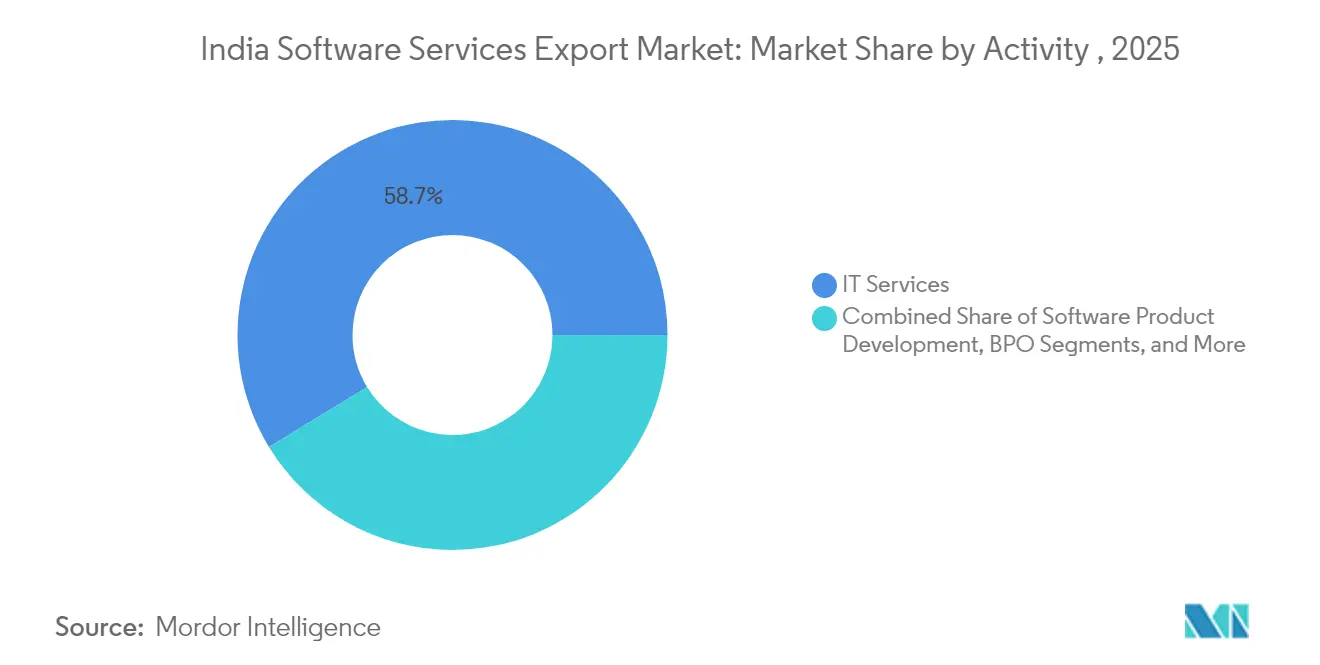

- By activity, IT services commanded 58.72% of the India software services export market share in 2025, while software product development is projected to expand at a 5.71% CAGR through 2031.

- By service-delivery model, offshore held 63.78% of the India software services export market size in 2025; GCCs are forecast to grow at a 6.03% CAGR to 2031.

- By client industry, BFSI led with 32.85% revenue share in 2025, whereas healthcare and life sciences is expected to grow at 5.15% CAGR.

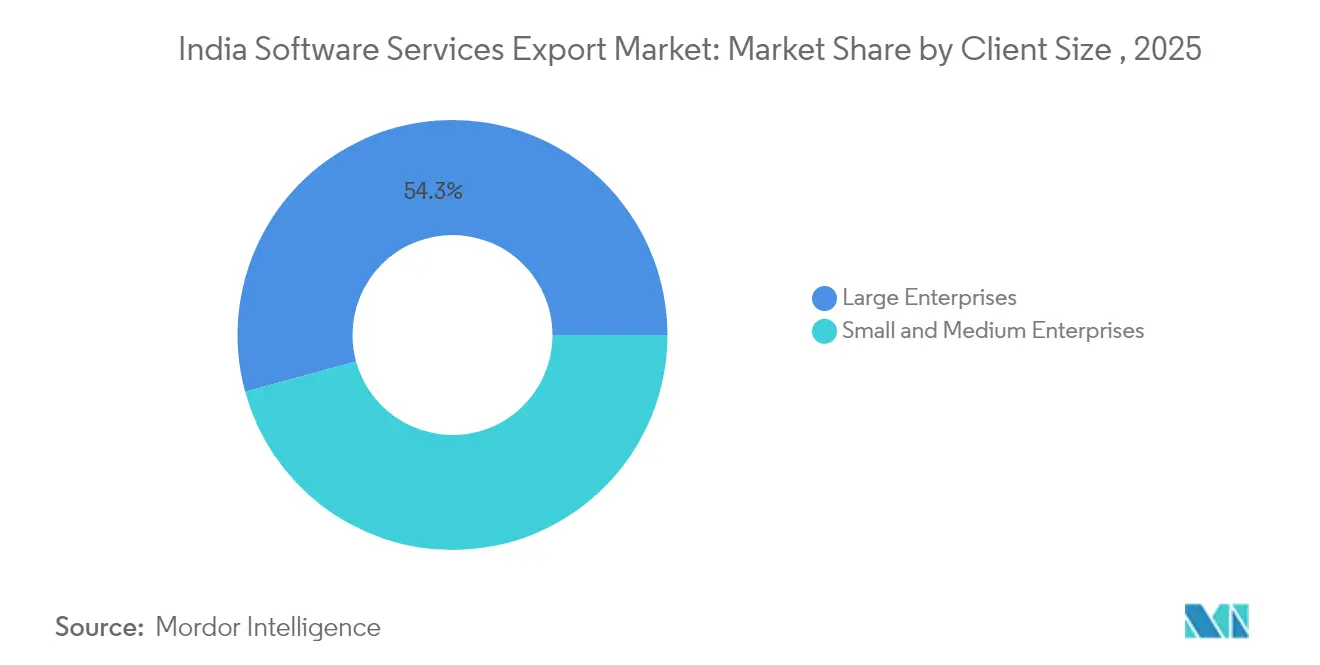

- By client size, large enterprises represented 54.25% of overall revenues in 2025; SMEs exhibit the strongest outlook with a 6.82% CAGR.

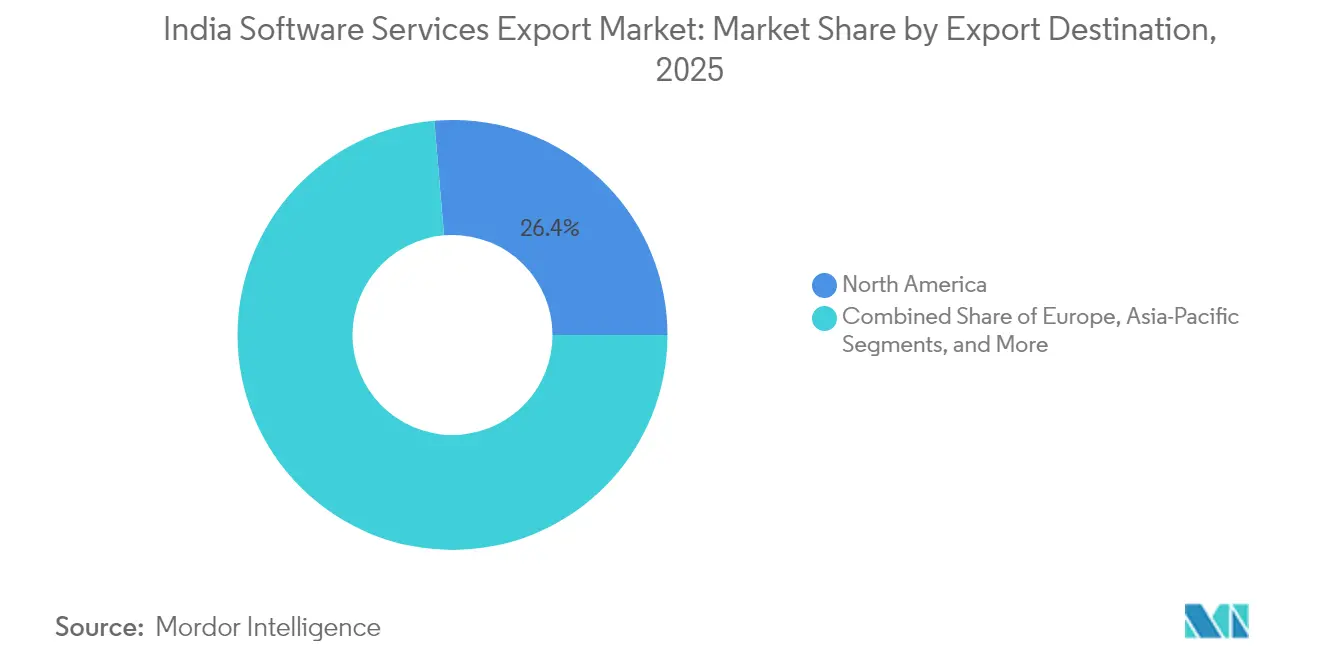

- By export destination, North America retained 26.35% of 2025 revenue, but the Middle East is the fastest-growing region at 5.44% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Software Services Export Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global demand for cost-efficient digital transformation services | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of cloud migration and managed services contracts | +0.9% | North America and Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Government incentives (SEZ, tax holidays, PLI) bolstering IT exports | +0.7% | National, with early gains in Bengaluru, Hyderabad, Chennai | Long term (≥ 4 years) |

| Accelerated AI/ML adoption by BFSI and retail clients | +0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Japan mid-tier firms' near-shore preference for India | +0.3% | Asia-Pacific core, specific to Japan-India corridor | Medium term (2-4 years) |

| ESG-linked "green software engineering" outsourcing surge | +0.4% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Demand for Cost-Efficient Digital-Transformation Services

Enterprise technology spending is rising 11.2% to almost USD 160 billion in 2025, and Indian vendors deliver complex transformations at 40–60% lower cost than on-shore teams. Buyers now seek strategic capability building rather than simple cost-cutting, which lets Indian firms price premium specialty work such as cybersecurity and data analytics. Multi-year engagements improve revenue visibility, while measured ROI proofs Tata CLiQ lifted conversions by 11.3% after implementing personalization, encouraging repeat outsourcing. [1]Ministry of Electronics and Information Technology, "Indian eCommerce site combines customer and product intelligence to deploy personalization suite for customers" indiaai.gov.in Mid-tier suppliers benefit most because they combine domain depth with leaner overheads that global consultancies cannot easily match. Altogether, this driver adds an estimated 1.2 percentage-points to the forecast CAGR of the India software services export market.

Expansion of Cloud-Migration and Managed-Services Contracts

Strategic alliances with AWS, Azure, and Google Cloud let Indian providers capture migration fees plus 3-to-5-year managed-services annuities. HCLTech’s exclusive global services pact for Nuance customers underpins this shift toward cloud-native recurring revenue.[2]HCLTech, “HCLTech collaborates with Microsoft to re-imagine contact centers,” hcltech.com Skills in containerization, micro-services, and DevOps accelerate, and certification pipelines scale across tier-II cities, broadening the talent base. The operational-expenditure model resonates with mid-market buyers, expanding the total addressable pool for Indian exporters.

Government Incentives Bolstering IT Exports

The production-linked-incentive program, enhanced SEZ benefits, and revived RoDTEP credits reduce compliance friction and offshore P&L stress. The USD 5 billion allocation to local electronics aims to reinforce the upstream supply chain that undergirds software exports. BharatNet expansion and national payment-system upgrades lower digital-infrastructure bottlenecks in tier-II cities, giving new entrants cost advantages without quality compromise.

Accelerated AI/ML Adoption by BFSI and Retail Clients

TCS’s AI frameworks for BFSI clarify regulatory-compliant automation paths, while India’s 87% fintech adoption rate compounds demand for fraud analytics, robo-advisory, and risk evaluation tools. Retail personal-ization use cases have moved from pilots to enterprise roll-outs; AI adoption scores now show India at 2.47 on a 4-point maturity scale NASSCOM.[3]NASSCOM, “Enterprise AI Adoption Index 2025,” nasscom.in This driver sustains higher-margin service lines and justifies talent up-skilling budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from Vietnam, Philippines and CEE | -0.8% | Global, particularly Asia-Pacific and Europe | Short term (≤ 2 years) |

| Talent attrition and wage inflation in Tier-I Indian cities | -0.6% | National, concentrated in Bengaluru, Hyderabad, Chennai | Medium term (2-4 years) |

| Cross-border data-residency and localisation mandates | -0.4% | Europe and select Asia-Pacific markets | Long term (≥ 4 years) |

| INR volatility-driven currency-hedging costs | -0.3% | Global impact on Indian exporters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from Vietnam, Philippines and CEE

Vietnamese hourly rates of USD 1,000–3,500 undercut India’s USD 800–4,200 brackets, while attrition stays near 10–15% versus higher churn in Bengaluru and Hyderabad. Central and Eastern Europe lure EU clients needing cultural proximity, eroding India’s hold on commoditized services. To protect share, Indian vendors must double-down on IP creation and high-complexity consulting, or risk margin squeeze.

Talent Attrition and Wage Inflation in Tier-I Indian Cities

Salary pressure persists even after select firms deferred hikes, because AI, cybersecurity, and cloud skills remain scarce. Attrition jeopardizes delivery continuity and inflates hiring costs, especially for mid-tiers that cannot match global-product-company packages. Retention incentives and dispersed workforce strategies become essential to temper this 0.6 percentage-point drag on CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Activity: Software Product Development Drives Innovation Premium

IT services accounted for 58.72% of the India software services export market in 2025, reflecting historical reliance on application management and infrastructure support. However, software product development is growing fastest at 5.71% CAGR, signaling a turn toward IP-led revenue models. Product studios in Bengaluru and Hyderabad now prototype fintech, health-tech, and ed-tech platforms that compete globally. Product teams now integrate design thinking, domain SMEs, and agile governance, creating sticky client relationships that transcend typical T&M billing.

By Service Delivery Model: GCCs Reshape Value Creation

Offshore centers still deliver 63.78% of the India software services export market size, underscoring India’s deep labor pool and resilient digital infrastructure. Yet GCCs are expanding at 6.03% CAGR as multinationals set up captive hubs for R&D, data science, and product engineering. India hosts 1,580 GCCs today and may reach 2,400 by 2030, representing over USD 100 billion in service throughput.

This evolution blurs outsourcing boundaries: service providers now co-innovate with in-house teams or compete head-to-head for AI architects, cloud engineers, and product managers. The India software services export market benefits from ecosystem spillovers start-ups, academia, and government labs collaborate inside smart-city tech parks that accelerate time-to-solution.

By Client Industry: Healthcare Digitization Accelerates Growth

BFSI maintained 32.85% of 2025 revenue through regulatory-driven modernization and seamless payment ecosystems. Conversely, healthcare and life sciences is poised for a 5.15% CAGR as telehealth, electronic health records, and AI diagnostics gain traction. The India software services export market size for healthcare is small today but scaling briskly as 10,088 digital-health start-ups demand integration talent.

Government schemes such as Ayushman Bharat Digital Mission create unified patient-ID frameworks, requiring interoperability expertise that Indian vendors already offer. Partnerships between pharma giants and local IT firms also amplify life-sciences analytics exports to the United States and Europe.

By Client Size: SME Segment Democratizes Technology Access

Large enterprises generated 54.25% of 2025 revenue, yet SMEs will grow at 6.82% CAGR through 2031. Rising MSME exports from INR 3.95 lakh crore (USD 4.6 Billion) in 2020-21 to INR 12.39 lakh crore (USD 14 Billion) in 2024-25 signal broader digital uptake. Cloud SaaS subscriptions, low-code platforms, and pay-as-you-go cybersecurity make enterprise-grade tech affordable.

Budget FY26 set aside INR 5 billion (USD 58 Million) for grants and low-interest loans that fund IT modernization. Consequently, the India software services export market benefits from diverse contract sizes and reduces concentration risk on Fortune 500 clients.

By Export Destination: Middle East Emerges as Growth Frontier

North America delivered 26.35% of 2025 export revenue, keeping the India software services export market anchored to US tech budgets despite economic swings. Yet the Middle East is clocking 5.44% CAGR, powered by USD 75 billion UAE infrastructure outlays and Saudi Arabia’s Vision 2030 digital agenda.

The India-Middle East-Europe Economic Corridor promises smoother logistics for data centers and subsea cables, creating fertile ground for cloud-consulting and smart-city deployments AGDA. Indian vendors also leverage NASSCOM InnoTrek cohorts to match deep-tech start-ups with Gulf investors, accelerating deal flow.

Geography Analysis

North America’s 26.35% slice of India's software services export market reflects entrenched client relationships, though Moody’s sovereign-rating downgrade last year briefly cooled discretionary US tech spend. A weak rupee offsets part of that risk because dollar billing converts to higher domestic margins for giants like TCS and Infosys Mint. Heightened demand for AI governance, cloud security, and data privacy keeps the pipeline healthy even amid macro uncertainty.

Europe offers steady but compliance-heavy growth as GDPR enforcement and ESG mandates reshape project scopes. Penalties of up to 4% of global turnover for data-privacy lapses push Indian vendors to fortify localization, sovereign-cloud, and green-software capabilities. Tech Mahindra’s commitment to carbon neutrality by 2030 resonates with EU buyers, aligning procurement with sustainability targets.

APAC, the Middle East, Africa, and South America together provide diversification. Saudi Arabia’s AI-talent hiring now ranks third worldwide, bolstering Indian exporters who supply cloud-native skill sets. The World Bank projects India’s economy to grow 7% in FY24/25, underpinning outbound investments in these frontier regions as domestic firms chase the USD 1 trillion merchandise-export goal by 2030.

Europe represents a strategic market for Indian international software services exports, demonstrating robust growth of approximately 25% during the period 2019-2024. The region's digital transformation journey has created significant opportunities for Indian IT service providers, particularly in areas such as cloud migration and IT infrastructure modernization. European businesses are increasingly recognizing India's expertise in delivering cost-effective, high-quality software solutions, leading to deeper strategic partnerships. The market is characterized by strong demand across various sectors, including banking, manufacturing, and healthcare, with particular emphasis on cybersecurity and data protection compliance. The region's focus on sustainable and innovative technology solutions has created new opportunities for Indian service providers to showcase their capabilities in emerging technologies. European organizations are increasingly partnering with Indian IT firms to leverage their extensive talent pool and technological expertise while maintaining compliance with stringent regional regulations. The growing adoption of cloud services and digital transformation initiatives continues to drive the demand for specialized IT services from India.

The Asia-Pacific region presents a dynamic growth opportunity for Indian offshore software services exports, with a projected growth rate of approximately 13.4% during the period 2025-2030. The region's accelerating digital transformation initiatives, particularly in countries like Singapore, Australia, and Japan, are creating new avenues for Indian IT service providers. The market is characterized by increasing investments in cloud computing, artificial intelligence, and digital infrastructure modernization across various industries. Countries in the region are actively pursuing smart city initiatives and digital economy transformations, creating substantial opportunities for Indian software service providers. The presence of mature technology markets alongside emerging digital economies provides a diverse range of opportunities for Indian IT companies to showcase their expertise. The region's focus on developing digital infrastructure and adopting advanced technologies has led to increased demand for specialized IT services, particularly in areas such as cloud migration, cybersecurity, and digital transformation consulting. The growing emphasis on innovation and technology adoption across various sectors continues to drive the demand for Indian IT expertise.

The Rest of the World region, encompassing Latin America and the Middle East & Africa, represents an emerging frontier for Indian international software services exports. These markets are characterized by increasing digital adoption and transformation initiatives, particularly in the Gulf Cooperation Council (GCC) countries. The region's focus on modernizing government services and developing smart cities has created new opportunities for Indian IT service providers. Countries in these regions are actively pursuing digital transformation initiatives across various sectors, including banking, retail, and public services. The growing emphasis on cloud adoption and cybersecurity has led to increased demand for specialized IT services. Indian IT companies are well-positioned to capitalize on these opportunities due to their extensive experience in digital transformation and cost-effective service delivery models. The region's diverse market dynamics and varying levels of digital maturity present unique opportunities for Indian software service providers to establish long-term partnerships and contribute to the digital evolution of these economies.

Competitive Landscape

The India software services export market exhibits moderate fragmentation. Tier-I players—TCS, Infosys, Wipro, HCLTech—enjoy scale economics, global-delivery footprints, and balance-sheet strength that secure multi-billion-dollar deals. Yet margin pressures surface as talent inflation and hedging costs eat into operating leverage. Mid-tiers contest by specializing in vertical-specific IP, agile sprints, and outcome-based contracts that attract mid-market buyers.

Strategic moves emphasize platform-centric business models, hyperscaler alliances, and tuck-in acquisitions. Emerging disruptors include deep-tech start-ups building generative-AI code-assist tools and domain-rich boutique consultancies. GCCs likewise compete for scarce architects. Consequently, incumbents double-down on learning academies, patent filings, and campus-to-corporate hiring from tier-II cities to widen talent funnels.

India Software Services Export Industry Leaders

-

Tata Consultancy Services Limited

-

Infosys Limited

-

Wipro Limited

-

HCL Technologies

-

Tech Mahindra Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: HCLTech expanded its strategic partnership with Microsoft to transform contact centers through generative AI and cloud-based solutions, becoming the exclusive professional-services partner for existing Nuance customers.

- April 2025: Infosys reported an 11.7% decline in consolidated net profit to INR 7,033 crore for Q4 FY25 and guided to 0–3% FY26 revenue growth amid softer demand.

- April 2025: Wipro announced a 26% year-on-year net-profit increase to INR 3,570 crore for Q4 FY25, supported by a 48.5% surge in large-deal bookings.

- May 2025: Renesas Electronics partnered with India’s Ministry of Electronics and IT under the Chips-to-Startup program, targeting more than 10% global revenue from India by 2030

- June 2025: AiVANTA and Slangit Technologies launched an AI-based customer-engagement platform for Arabic markets, leveraging AiVANTA’s Indian client experience.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines India's software services export market as revenue earned from delivering computer services, software product engineering, business process management, and other IT-enabled services to clients located outside India, regardless of delivery mode or invoicing currency. Revenue is counted in USD at the point it leaves India, reflecting actual export earnings captured in balance-of-payments data.

Scope Exclusion: Hardware sales, domestic IT spending, and purely in-country captive consumption are excluded.

Segmentation Overview

-

By Activity

- IT Services

- Software Product Development

- Business Process Services (BPO)

- Others

-

By Service Delivery Model

- On-site

- Near-shore

- Offshore

- Captive / Global Capability Centres (GCCs)

-

By Client Industry

- Banking and Financial Services

- Retail and Consumer

- Healthcare and Life Sciences

- Manufacturing

- Telecom and Media

- Others

-

By Client Size

- Large Enterprises

- Small and Medium Enterprises

-

By Export Destination

- North America

- Europe

- Asia-Pacific

- Middle East

- South America

- Africa

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed senior export managers at tier-1 IT firms, finance heads of mid-sized GCCs, and procurement leaders in North America and Europe. These conversations verified billing-rate movements, bench utilization, and appetite for cloud-native engagements, allowing us to reconcile secondary aggregates with on-ground sentiment across India's main delivery hubs.

Desk Research

We collected baseline statistics from public bodies such as the Reserve Bank of India, the Ministry of Commerce's export databank, and Parliament papers that disclose quarterly service-trade receipts. Industry trade groups, including NASSCOM and the Electronics & Computer Software Export Promotion Council, provide macro totals, segment splits, and region-wise export receipts that help our team spot structural shifts. Macroeconomic indicators, notably IMF projections for global tech spending and USD-INR exchange trends, place the export numbers in context.

To refine growth signals, analysts pull audited revenue lines from listed IT firms' 10-Ks, select unlisted company filings on D&B Hoovers, and offshore head-count additions visible in Dow Jones Factiva coverage. Patent volumes from Questel and contract announcements collated on Tenders Info flag demand for newer service lines such as AI engineering. This list is illustrative; many additional open and paid sources fed into data gathering, validation, and clarification.

Market-Sizing & Forecasting

We apply a top-down reconstruction that begins with RBI software export receipts, which are then split by service line, destination, and client size using penetration ratios derived from NASSCOM, STPI shipment logs, and respondent interviews. Select bottom-up roll-ups, sampled average selling price times billed FTEs at large vendors, cross-check the totals before finalizing. Critical variables include GCC count, tech-staff pool growth, currency outlook, average hourly billing rates, share of fixed-price contracts, and attrition. A multivariate regression model links these drivers to export revenue, producing the baseline value and a forecast CAGR. Gap areas in sub-segments lacking public data are bridged with normalized vendor disclosures and client-side spend benchmarks gathered during primary work.

Data Validation & Update Cycle

Outputs pass three analyst reviews that test coherence against historic series, peer ratios, and currency sensitivity. Variances above preset thresholds trigger source re-checks. Reports refresh every twelve months, with interim updates when policy changes, large M&A, or forex swings materially alter forecasts. An analyst rereads all live inputs before each delivery.

Why Mordor's India Software Services Export Baseline Commands Reliability

Published estimates often diverge because firms mix domestic revenue, hardware, or affiliate sales, and they refresh data at different cadences.

Key gap drivers include wider scope definitions, reliance on cash-flow rather than accrual values, single-source assumptions for billing rates, and infrequent model updates that miss currency or wage shifts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 158.19 B (2025) | Mordor Intelligence | - |

| USD 205.2 B (2024) | Government Dataset A | Includes sales by overseas affiliates and uses cash-receipt accounting, which inflates totals. |

| USD 224 B (2025 E) | Trade Association B | Bundles hardware and domestic project revenue, and applies industry self-reported figures without currency normalization. |

The comparison shows how disciplined scoping, multi-source validation, and annual refreshes let Mordor provide a balanced, transparent baseline that decision-makers can track and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the India software services export market?

It is valued at USD 165.32 billion in 2026 and is projected to reach USD 206.15 billion by 2031.

Which activity segment is growing fastest within the India software services export market?

Software product development is expanding at a 5.71% CAGR as firms pivot to IP-led offerings.

What are the key challenges facing Indian IT exporters?

Rising competition from Vietnam and Central Europe, talent attrition, data-localization rules, and currency volatility are the main braking factors.

How do government policies support the India software services export market?

Production-linked incentives, SEZ tax holidays, and RoDTEP credits lower operating costs and encourage export expansion.

Page last updated on: