Team Collaboration Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

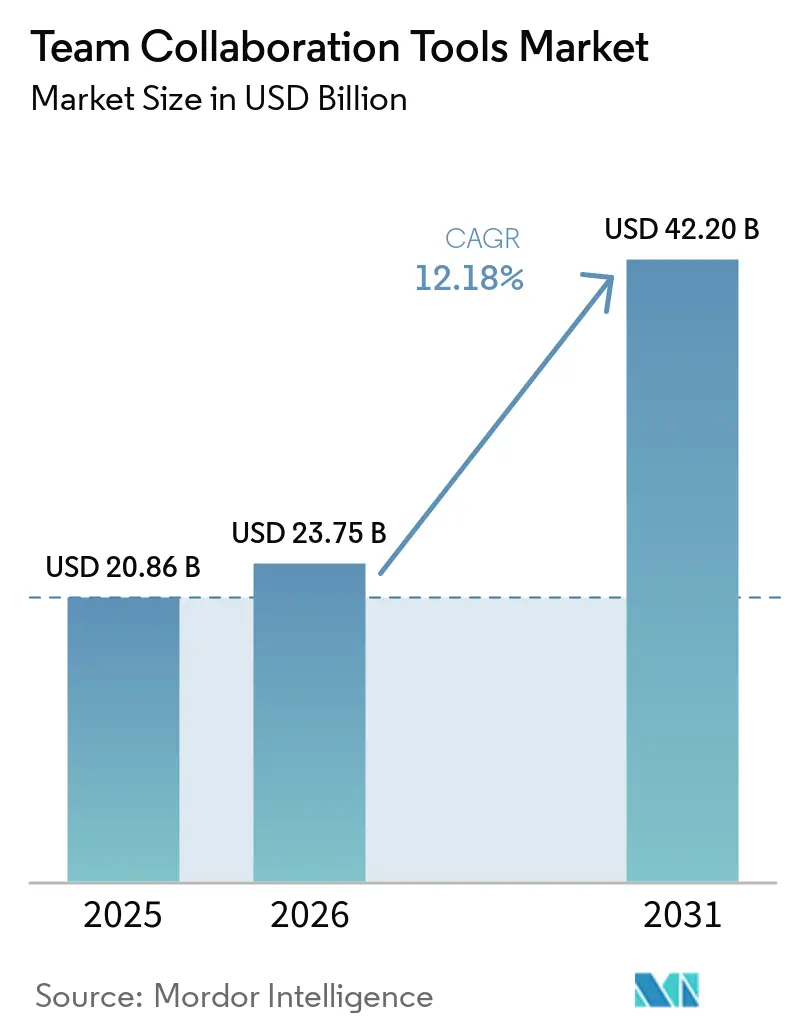

| Market Size (2026) | USD 23.75 Billion |

| Market Size (2031) | USD 42.20 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Team Collaboration Tools Market Analysis by Mordor Intelligence

The Team collaboration tools market size is expected to increase from USD 20.86 billion in 2025 to USD 23.75 billion in 2026 and reach USD 42.2 billion by 2031, growing at a CAGR of 12.18% over 2026-2031. Demand is being propelled by the rapid rollout of generative-AI assistants that summarize conversations, translate content, and automate routine tasks, which lifts knowledge-worker output without expanding headcount. Cost-sensitive small and medium enterprises (SMEs) are scaling adoption faster than large companies because modular, pay-per-seat pricing compresses buying cycles. At the same time, data-sovereignty laws are reshaping procurement, nudging many organizations toward hybrid architectures that keep sensitive information on local servers while tapping cloud AI for productivity gains. Vendors are responding with sovereign-cloud regions, in-product consent workflows, and tighter zero-trust security controls, all of which add services revenue streams. Competitive dynamics center on ecosystem lock-in platforms that bundle chat, meetings, whiteboards, and work management into a single license are displacing point solutions, yet disruptors that integrate more openly continue to win departmental budgets.

Key Report Takeaways

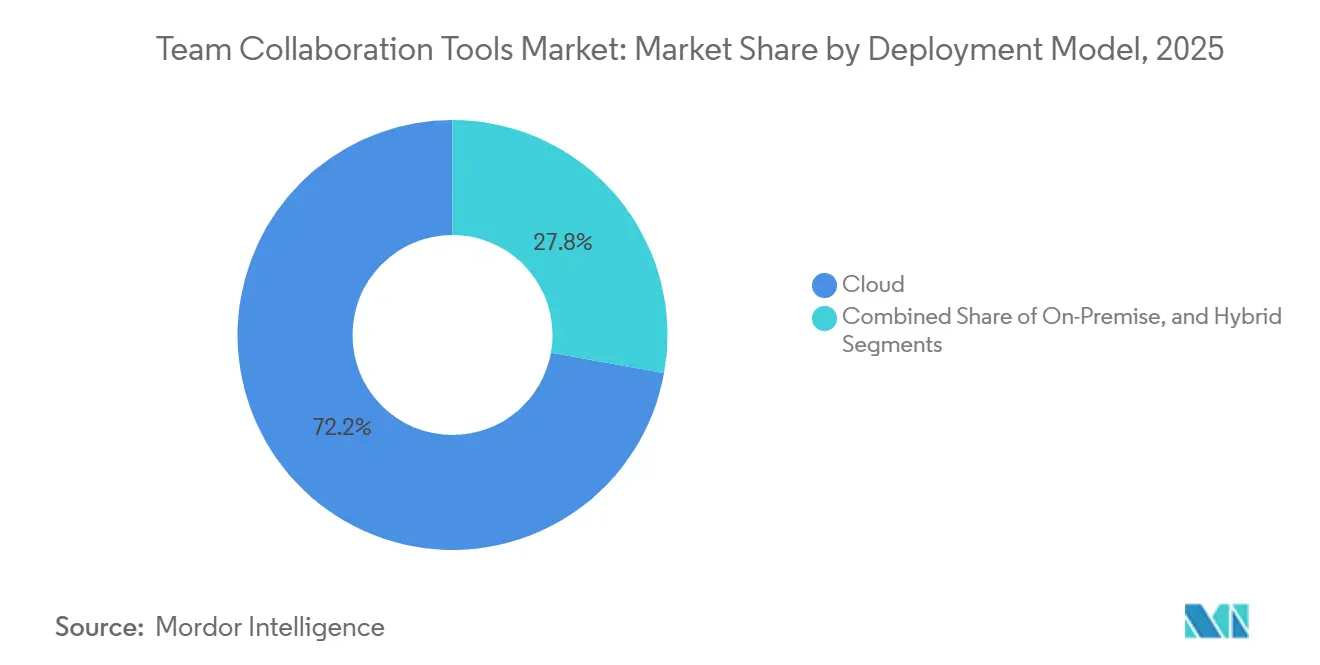

- By deployment model, cloud captured 72.17% of the Team collaboration tools market share in 2025, whereas hybrid configurations are advancing at a 12.86% CAGR through 2031.

- By organization size, SMEs held 58.58% of Team collaboration tools market spending in 2025, and the segment is projected to expand at a 12.96% CAGR to 2031.

- By software type, communication and coordination tools led with a 41.29% share of the Team collaboration tools market size in 2025, while whiteboarding platforms are forecast to post the fastest growth at 12.73% CAGR during 2026-2031.

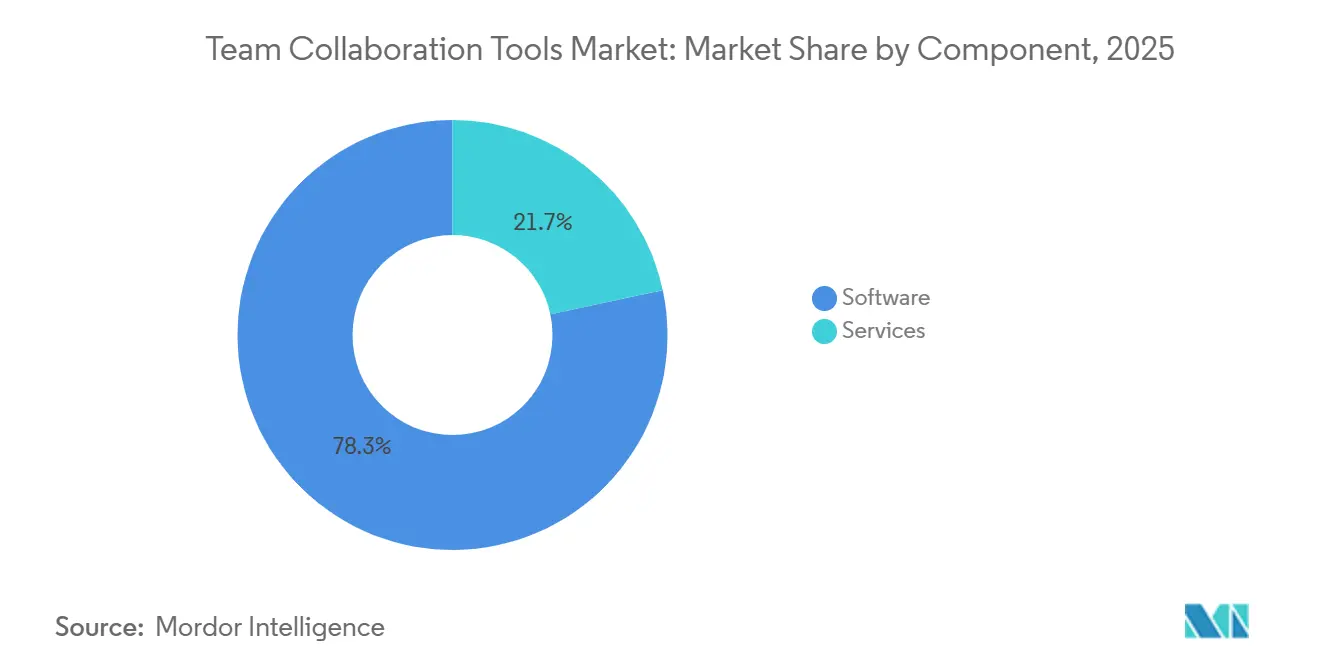

- By component, software accounted for 78.33% of 2025 revenue, yet services are set to climb at a 13.03% CAGR on the back of complex AI-workflow implementations.

- By end-user industry, information technology and telecom commanded 27.01% of Team collaboration tools market size in 2025, whereas healthcare is advancing at a 12.59% CAGR through 2031.

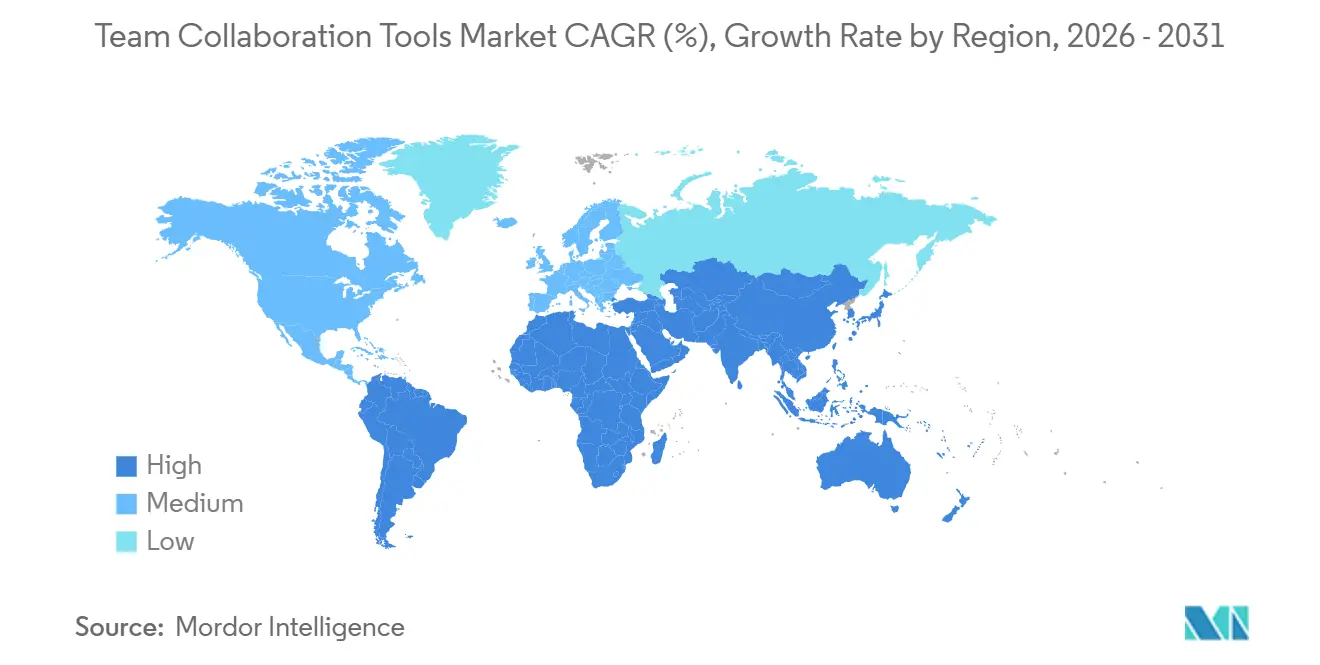

- By geography, North America topped the team collaboration tools market with 39.29% share in 2025, whereas Asia-Pacific is set to expand at a 13.22% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Team Collaboration Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of Hybrid and Asynchronous Work Models | +2.80% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Accelerating SaaS Procurement Cycles Among SMBs | +2.30% | Global, strongest in North America and Asia-Pacific SMB segments | Short term (≤2 years) |

| Generative-AI Plug-ins Boosting Productivity per User | +3.10% | North America and Europe early adopters, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing Focus on Employee-Experience (EX) Platforms | +1.60% | North America and Europe, emerging in Asia-Pacific | Long term (≥4 years) |

| In-App Workflow Automation Reducing Context Switching | +1.90% | Global, with enterprise adoption leading in North America | Medium term (2-4 years) |

| Collaboration Analytics Quantifying Knowledge-Worker ROI | +1.20% | North America and Europe, limited penetration in emerging markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rise Of Hybrid and Asynchronous Work Models

Enterprises are re-architecting digital workplaces so employees scattered across 8-12 time zones can collaborate without endless live meetings. Asynchronous features such as threaded discussions, video clips, and AI-generated summaries have become must-haves, cited by 68% of distributed teams as decisive in platform selection.[1]Slack Technologies, “The State of Work 2025,” slack.com Slack’s Clips usage tripled between Q1 2025 and Q1 2026 as managers replaced daily stand-ups with short video updates that colleagues could watch on demand. Productivity studies show that 81% of workers in asynchronous environments feel more effective versus 52% in meeting-heavy settings. However, shifting to a documentation-centric culture raises training needs, which in turn fuels service revenue growth. Compliance frameworks like ISO 27001 now influence tool choice because asynchronous records must meet audit standards.[2]International Organization for Standardization, “ISO 27001:2022,” iso.org

Accelerating SaaS Procurement Cycles Among SMBs

Modular pricing has shortened buying decisions from nine months to under ninety days for many SMEs, enabling side-by-side trials of multiple collaboration suites.[3]Asana Inc., “Investor Presentation 2025,” asana.com A 2025 McKinsey study found firms that adopted mix-and-match SaaS stacks cut IT costs by 18-22%.[4]McKinsey, “The State of AI 2025,” mckinsey.com Flexibility brings complexity: companies juggling more than ten apps report 30% higher employee frustration, sparking demand for integration hubs like Workato that consolidate notifications. The Team collaboration tools market therefore bifurcates, with SMEs valuing speed while large enterprises focus on governance.

Generative-AI Plug-ins Boosting Productivity Per User

Early adopters documented 27% revenue gains and 21% cost drops within a year of activating AI copilots embedded in collaboration apps. Microsoft research shows Copilot users reclaim 4-6 hours monthly, mostly from auto-generated email drafts and document outlines. Zoom reports that 74% of executives save at least an hour daily via automated meeting recaps. Yet only 38% of enterprises switched AI on for all staff in 2025 because of hallucination worries. Vendors that surface confidence scores and citations are best positioned to convert cautious sectors such as finance and healthcare.

Growing Focus on Employee-Experience Platforms

Tight labour markets push employers to elevate digital engagement, prompting consolidation of chat, learning, and wellness tools under unified experience hubs. Asana’s AI teammates triage tasks autonomously, reframing the platform as an EX-nerve center rather than a project tracker. Atlassian’s Rovo AI cuts information-search time by up to 50%, a boon in knowledge-heavy industries. PwC found that firms with high EX metrics enjoy 22% lower attrition and 18% higher customer satisfaction. Building these hubs requires deep integrations with HR and learning systems, which explains the faster growth of services compared with software.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shadow-IT and Multi-Tool Sprawl Inflating CIO TCO | -1.80% | Global, most acute in North America and Europe enterprises | Short term (≤2 years) |

| Rising Data-Sovereignty and Residency Mandates | -2.10% | Europe (GDPR, DORA), Asia-Pacific (China PIPL, India DPDP), emerging in Middle East | Medium term (2-4 years) |

| Vendor Lock-in Concerns with Hyperscale Ecosystems | -1.30% | Global, particularly affecting large enterprises | Long term (≥4 years) |

| Escalating Privacy Lawsuits over Meeting Transcripts and Recordings | -0.90% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shadow-IT And Multi-Tool Sprawl Inflating CIO TCO

Unauthorized adoption of consumer apps inflates enterprise licensing, integration, and security costs by as much as 40%. On average, organizations run fourteen collaboration products but formally govern only six, leaving eight in a gray zone of inconsistent policy enforcement. Each extra platform consumes budget for API maintenance and user support, diverting funds from innovation. Vendors now offer curated marketplaces where employees can self-install pre-approved integrations, shifting emphasis to governance frameworks rather than outright blockage.

Rising Data-Sovereignty and Residency Mandates

Regulations such as the EU’s DORA and China’s PIPL compel vendors to host data locally, increasing infrastructure spend by 30-50% and fragmenting global feature roadmaps. India’s 2024 DPDP Act adds another jurisdiction requiring in-country storage and deletion rights within 30 days. Regional specialists like Cybozu and Zoho, architected for single-country deployments, are gaining share because they embed compliance at a code level.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Gain Traction

Hybrid solutions expanded at a 12.86% CAGR through 2031, the quickest among deployment types. While cloud still controlled 72.17% of the Team collaboration tools market share in 2025 thanks to low upfront costs, regulatory hurdles prompted banks and governments to keep select workloads on premises. Microsoft reported that hybrid configurations accounted for 34% of new Teams enterprise deals in 2026, up from 22% the year prior. This growing slice of Team collaboration tools market size illustrates how organizations balance sovereign data control with cloud-based AI features.

Demand for true data mobility is pushing vendors to invest in edge appliances and federated identity services that let meeting recordings live on local hardware while transcriptions process in the public cloud. Smaller providers struggle to fund such dual-stack engineering, widening the gap between hyperscale platforms and niche offerings. As more regions adopt data-localization statutes, hybrid will likely shift from exception to default.

By Organisation Size: SMBs Drive Volume Growth

SMEs held 58.58% of spending in 2025 and are projected to outpace large enterprises at a 12.96% CAGR. The Team collaboration tools market size for SMEs rises partly because feature-modular SaaS tiers eliminate capital expenditure barriers. Flexible month-to-month licensing lets small firms test three or four platforms concurrently, often combining Slack messaging with Asana tasks and Miro whiteboards.

Cost savings can be substantial McKinsey pegged IT spend reductions at up to 22% for modular adopters but tool sprawl erodes those gains if integration frameworks lag. Vendors courting SMEs therefore ship turnkey automation templates that require no coding. Large enterprises, by contrast, prioritize consolidation with suitelike products from Microsoft or Atlassian, accepting moderately slower innovation in return for single-vendor governance.

By Software Type: Whiteboarding Platforms Disrupt Traditional Hierarchies

Communication and coordination software led with a 41.29% share in 2025, yet whiteboarding and ideation tools are forecast to rocket at 12.73% CAGR through 2031 as asynchronous brainstorming displaces real-time meetings. The Team collaboration tools market size attached to digital canvases is swelling because product managers, UX designers, and agile coaches prefer infinite boards over static slide decks.

Convergence blurs category borders: Slack added Canvas documents, Notion inserted databases and project boards, while Miro built native video chat. Feature overlap benefits customers by trimming license counts but forces vendors to differentiate on AI-driven insights, semantic search, and pre-built workflow libraries rather than core chat or video functionality.

By Component: Services Revenue Reflects Implementation Complexity

Software commanded 78.33% of revenue in 2025, yet services are climbing at a 13.03% pace as AI workflows, single sign-on, and compliance mapping add deployment complexity. Enterprises implementing Microsoft Copilot spent between USD 150,000 and USD 250,000 on change-management and prompt-engineering curricula, highlighting a shift toward advisory spending.

The Team collaboration tools market share for systems integrators is rising because global consultancies can scale multi-region rollouts more efficiently than vendor-owned professional-services arms. Consequently, platform providers with robust partner networks, such as Microsoft and Salesforce, capture indirect revenue growth as integrators build atop their APIs.

By End-User Industry: Healthcare Emerges as High-Growth Vertical

Information technology and telecom kept the largest allocation at 27.01% in 2025, but healthcare registers the fastest CAGR at 12.59% through 2031. HIPAA-compliant messaging, telehealth workflows, and multi-site clinical-trial coordination underpin adoption. The Team collaboration tools market size within hospitals is expanding as remote patient monitoring and digital front-door initiatives persist beyond the pandemic era.

Banking and insurance also invest heavily due to DORA’s operational-resilience rules, demanding immutable logs and granular access controls. Education, retail, and government exhibit steady but lower growth, constrained by budgets and procurement cycles. Vendors able to embed sector-specific compliance, such as TigerConnect for healthcare, win deals over generic platforms with compliance add-ons.

Geography Analysis

North America accounted for 39.29% of 2025 revenue. Adoption of AI add-ons such as Microsoft Copilot and Slack AI surpassed 40% among Fortune 500 firms, yet overall growth moderates to 11.8% CAGR as user penetration approaches saturation. Vendors focus on boosting average revenue per seat via premium AI and governance modules. Canada and Mexico grow a bit faster than the United States, but together still represent less than one-sixth of regional spend.

Asia-Pacific is the fastest-growing region at 13.22% CAGR. India’s DPDP Act spurs local data-center builds, helping domestic vendor Zoho secure roughly one-fifth of the SME segment. China remains bifurcated between domestic suites like DingTalk and global tools operating in walled-off partitions compliant with PIPL. Japan’s more modest 11.2% CAGR reflects cultural preference for in-person interactions, though low-code workflow builders from Cybozu are nudging older firms toward digital processes. Southeast Asian nations log nearly 14% growth as governments mandate digitalization.

Europe holds 24-26% of the Team collaboration tools market size and grows at 11.5% CAGR, heavily shaped by GDPR and DORA. Germany, the United Kingdom, and France contribute 60% of continental spend, prioritizing data-residency guarantees over price. Eastern European outsourcing hubs adopt collaboration suites quickly to manage cross-border developer teams. The Middle East and Africa combined maintain mid-12% growth, led by United Arab Emirates smart-city programs and South African financial-services digitization. South America trails slightly at near-12% CAGR, with Brazil commanding the lion’s share.

Competitive Landscape

The five largest vendors Microsoft, Salesforce (Slack), Google, Atlassian, and Zoom control an estimated 55-60% of 2026 revenue, giving the Team collaboration tools market a moderate concentration. These incumbents bundle chat, meetings, content, and AI into platform subscriptions that raise switching costs. Microsoft alone filed forty-seven AI collaboration patents in 2025, signalling intent to own the intelligence layer.

Challengers like Notion, ClickUp, and Miro are growing users 15-20% annually by merging disparate workflows into single canvases and pricing aggressively for departments. Open-source or self-hosted options such as Basecamp attract privacy-focused clients unwilling to trust multi-tenant clouds. Vertical specialists, for instance TigerConnect in healthcare or Symphony in finance, secure footholds where regulatory nuance trumps feature breadth.

Strategic pivots increasingly revolve around AI. Vendors that ship generative features inside core workflows enjoy meaningfully higher net-revenue retention than those gating AI behind add-on fees. Compliance baseline is rising, with 78% of 2025 enterprise buyers demanding third-party security attestations like SOC 2 and ISO 27001. As a result, platform roadmaps now weigh security and privacy upgrades on par with new user features.

Team Collaboration Tools Industry Leaders

Microsoft Corporation

Slack Technologies Inc.

Smartsheet Inc.

Asana Inc.

Atlassian Corporation PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Atlassian released Rovo AI, a generative assistant that unifies search across Jira, Confluence, and third-party tools, following a six-month beta with 500 enterprises.

- December 2025: Slack launched Work Objects, a structured data layer that embeds workflow tracking inside chat channels, reducing tool sprawl by one-quarter among early adopters.

- November 2025: Zoom partnered with OpenAI to integrate GPT-4 into AI Companion for real-time summaries and sentiment insights, targeting compliance-minded sectors.

- October 2025: Asana unveiled AI teammates that autonomously triage tasks and escalate blockers, cutting project-manager admin time by up to 30%.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the team collaboration tools market as cloud-based or on-premise software sold on a license or subscription that lets groups exchange messages, hold audio or video meetings, share files, and track tasks inside one digital workspace, regardless of location or device.

Scope Exclusion: stand-alone PBX hardware, dedicated conferencing rigs, and pure file-sync utilities are outside this assessment.

Segmentation Overview

- By Deployment Model

- Cloud

- On-Premise

- Hybrid

- By Organisation Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Software Type

- Communication and Coordination Software

- Conferencing Software

- Project and Task Management Suites

- Whiteboarding and Ideation Platforms

- By Component

- Software

- Services

- By End-User Industry

- Information Technology and Telecom

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life-Sciences

- Education

- Retail and E-Commerce

- Government and Public Sector

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South-East Asia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed product managers at leading platforms, chief information officers in large enterprises, and managed service partners across North America, Europe, and Asia-Pacific. These conversations confirmed churn, feature attach rates, and local price adjustments that documents alone could not reveal.

Desk Research

We first sized the global digital workforce through International Telecommunication Union broadband data, Eurostat ICT usage surveys, and United States Bureau of Labor Statistics remote-work studies. Open papers from the Software and Information Industry Association and the Asia Cloud Computing Association revealed adoption triggers, and company filings plus D&B Hoovers and Dow Jones Factiva showed revenue splits and price bands. The sources listed are illustrative; many additional public and paid datasets informed our evidence base.

A second sweep collected laptop and webcam shipment records that flagged supply pinch points in emerging economies, letting us anchor seat assumptions to real hardware availability.

Market-Sizing and Forecasting

We convert global knowledge workers into an addressable seat pool, apply verified penetration ratios for cloud suites, and test results against selective bottom-up vendor revenue roll-ups. Key variables include average monthly subscription fees, hybrid-work prevalence, mobile broadband reach, AI feature adoption, and SME cloud spending. A multivariate regression model produces five paths, and our analysts, guided by quarterly primary calls, choose the most probable trajectory before reconciling any gaps.

Data Validation and Update Cycle

Outputs move through three analyst reviews where anomalies are re-queried and corrected. Reports refresh each year, and major events such as landmark mergers or price resets trigger interim updates.

Why Mordor's Team Collaboration Tools Baseline Earns Lasting Trust

Published estimates differ because firms frame the market differently, refresh on separate calendars, or lean on untested multipliers. External studies place 2024 values between about USD 18.60 billion and USD 36.11 billion, while Mordor posts USD 23.75 billion for 2025. Our disciplined scope and annual recalibration keep variance low.

Key gap drivers include whether professional services are counted, if unified communication hardware is bundled, and the base year each publisher favors.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.75 B (2025) | Mordor Intelligence | - |

| USD 36.11 B (2024) | Global Consultancy A | Bundles conferencing hardware and enterprise social networks |

| USD 18.60 B (2024) | Research Publisher B | Excludes implementation services and freemium conversions |

| USD 17.15 B (2021) | Regional Firm C | Uses pre-pandemic workforce base without hybrid uplift |

Together, the comparison shows that our carefully bounded scope, primary-validated variables, and disciplined update cadence yield a balanced, transparent baseline that decision-makers can depend on.

Key Questions Answered in the Report

What is the projected value of the team collaboration tools market by 2031?

The market is forecast to reach USD 42.2 billion by 2031.

How fast is the team collaboration tools market expected to grow between 2026 and 2031?

It is projected to register a 12.18% CAGR during that period.

Which deployment model is expanding the quickest?

Hybrid architectures are advancing at a 12.86% CAGR through 2031 as organizations balance cloud AI with data sovereignty.

Why are SMEs adopting collaboration tools faster than large enterprises?

Modular, pay-per-seat pricing compresses procurement cycles, letting SMEs experiment inexpensively and scale solutions rapidly.

Which end-user industry shows the highest growth potential?

Healthcare and life sciences lead with a 12.59% CAGR because HIPAA-ready platforms enable telehealth and multi-site clinical trials.

What regional market is growing the fastest?

Asia-Pacific, propelled by data-residency laws in India and China, is expanding at a 13.22% CAGR through 2031.

Page last updated on: