Information And Communications Technology (ICT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

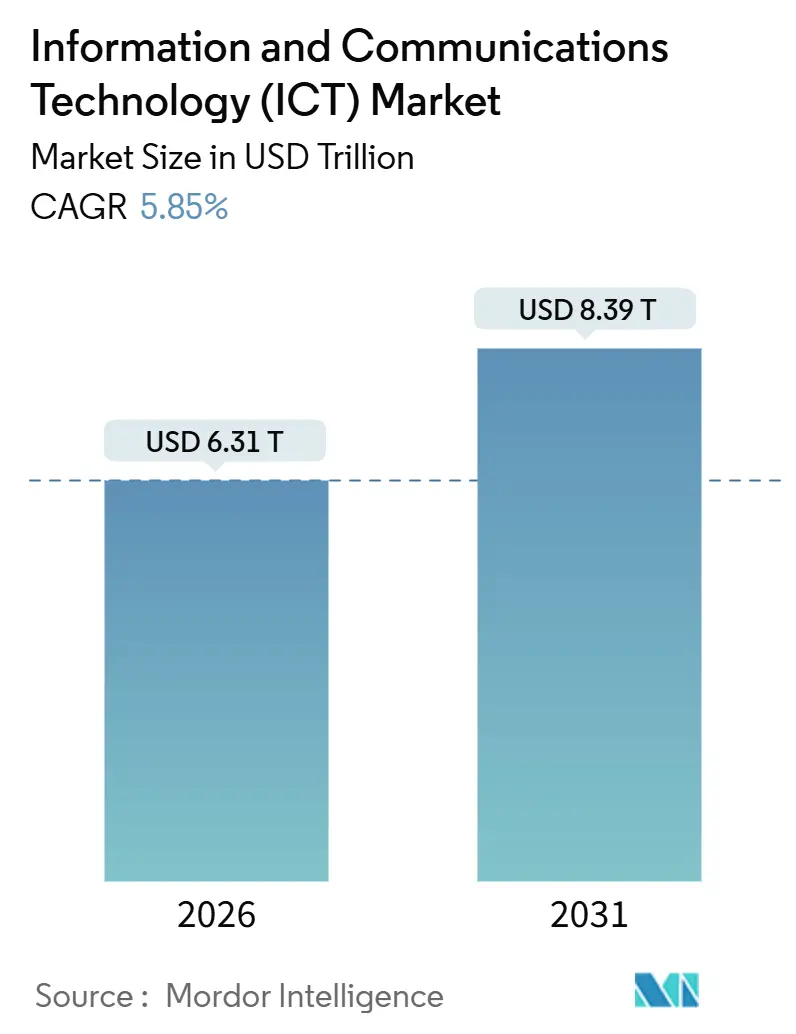

| Market Size (2026) | USD 6.31 Trillion |

| Market Size (2031) | USD 8.39 Trillion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Information And Communications Technology (ICT) Market Analysis by Mordor Intelligence

The Information and Communications Technology (ICT) Market size reached USD 6.31 trillion in 2026 and is projected to climb to USD 8.39 trillion by 2031, reflecting a 5.85% CAGR across the forecast horizon. Enterprises are redirecting funds from episodic hardware refreshes toward sovereign-AI mandates, edge-native workloads, and consumption-based contracts that spread capital needs into quarterly operating budgets. IT Services dominated 2025 revenue at 32.84%, yet IT Software is now accelerating as firms embed generative-AI co-pilots in core systems and decompose legacy monoliths into microservices. Large Enterprises still control the bulk of spending, but Small and Medium Enterprises (SMEs) are adding share quickly because cloud-native tooling removes upfront hardware costs and automates compliance workflows. Hybrid-cloud architectures are gaining favor as digital-sovereignty laws compel regional data residency, while gaming, industrial IoT, and public-sector modernization each widen the total addressable opportunity for vendors willing to certify solutions across heterogeneous chipsets, radio technologies, and regulatory regimes.

Key Report Takeaways

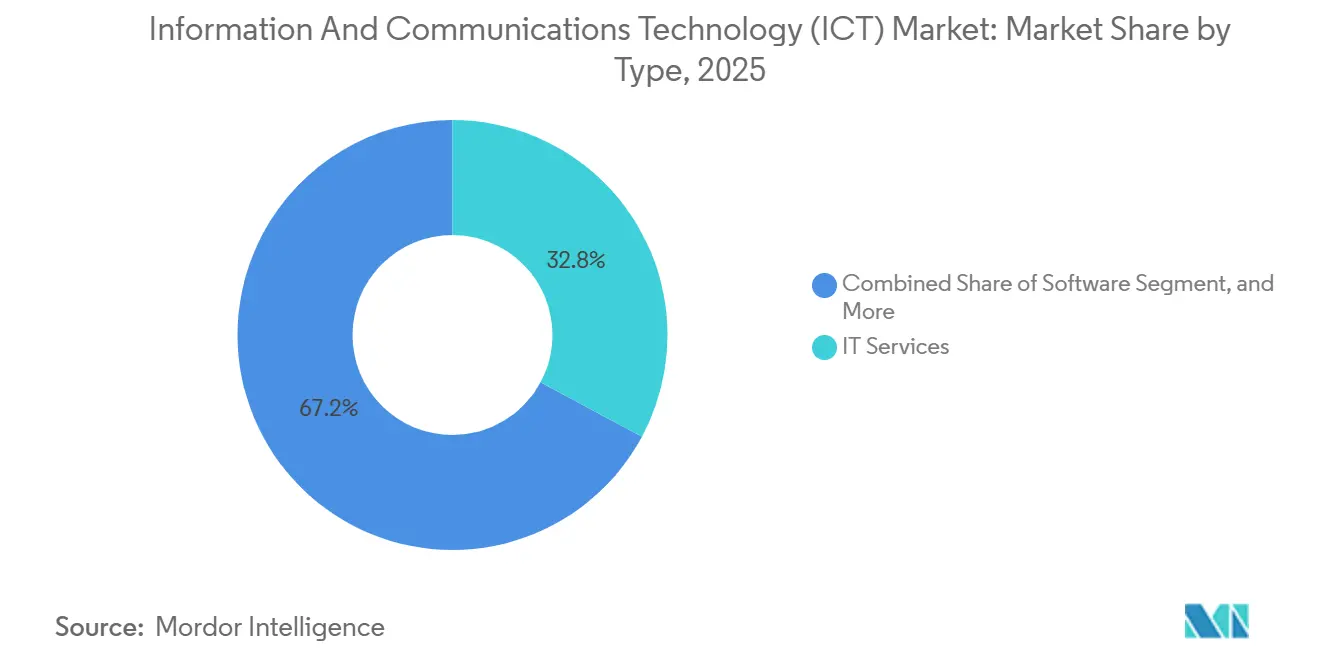

- By type, IT Services held 32.84% revenue share in 2025; IT Software is forecast to advance at a 6.84% CAGR through 2031.

- By enterprise size, Large Enterprises commanded 61.54% of 2025 spending, while SMEs are expanding at a 6.24% CAGR to 2031.

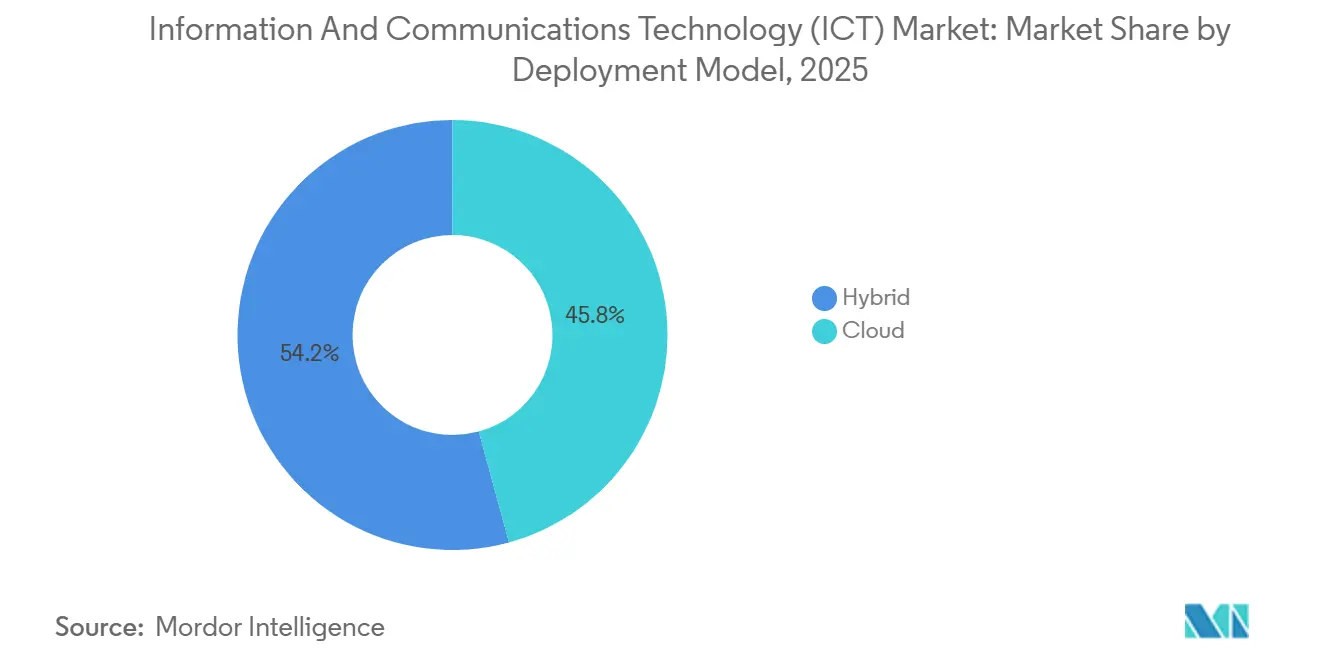

- By deployment model, cloud deployments captured 45.77% of 2025 outlays; hybrid models are rising fastest at a 6.57% CAGR through 2031.

- By end-user vertical, government and public administration represented 18.84% demand in 2025; gaming and esports lead growth with a 7.43% CAGR to 2031.

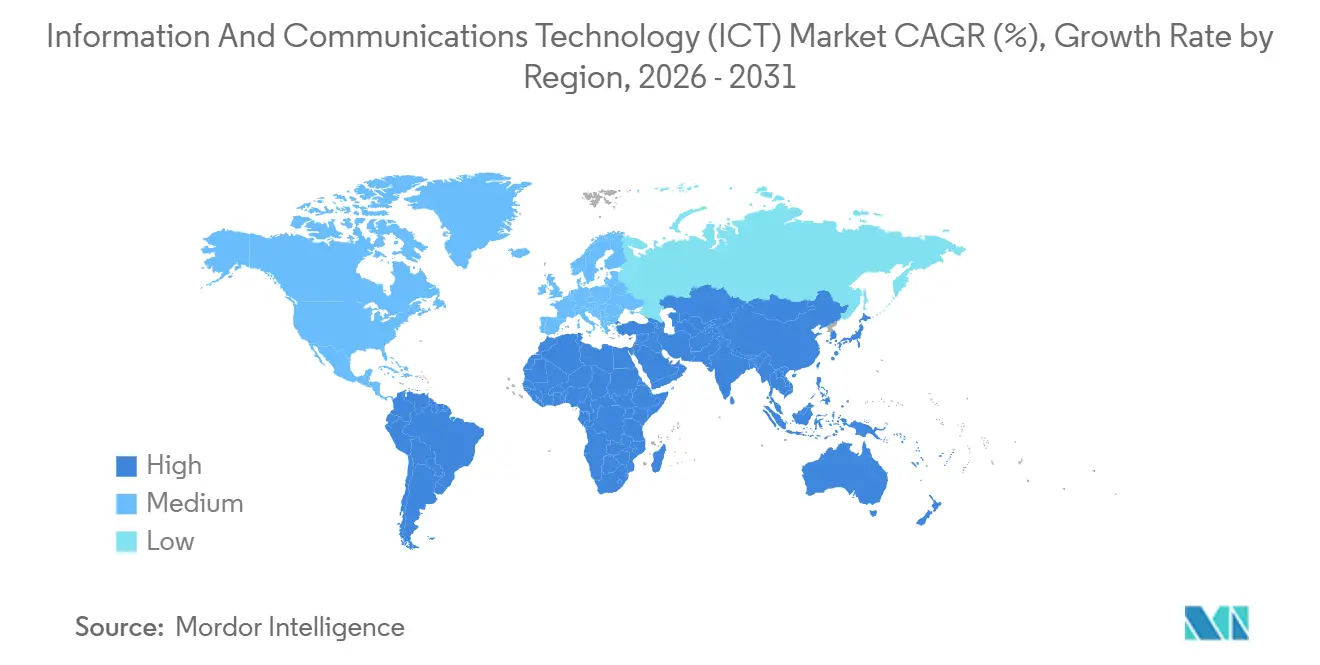

- By geography, North America retained the largest regional footprint at 39.78% of demand in 2025, but Asia-Pacific is pacing the field with a 7.68% CAGR projected to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Information And Communications Technology (ICT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Edge Computing and IoT Data Streams | +1.2% | Global with APAC and North America leading deployments | Medium term (2-4 years) |

| Surge in AI-Optimized Cloud Infrastructure Investments | +1.5% | North America, Europe, China | Short term (≤ 2 years) |

| Rapid 5G Stand-Alone Core Deployments Accelerating Use Cases | +1.0% | APAC core, spill-over to Middle East and South America | Medium term (2-4 years) |

| Regulatory Push for Digital Sovereignty and Secure Cloud Regions | +0.8% | Europe, China, India, Middle East | Long term (≥ 4 years) |

| Growing Preference for Consumption-Based IT Services Models | +0.9% | Global, especially North America and Europe | Short term (≤ 2 years) |

| National Digital Public Infrastructure Programs in Emerging Economies | +1.1% | India, Indonesia, Philippines, Brazil, Nigeria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In AI-Optimized Cloud Infrastructure Investments

Hyperscalers allocated more than USD 200 billion of capital expenditure during 2025 for GPU clusters, liquid-cooled halls, and high-speed interconnects tuned for large-language-model training and inference. Quarterly consumption-based contracts now bundle compute, storage, and model access into unified pricing that displaces multi-year server refreshes.[1]Amazon Web Services, “Trainium Announcement,” AWS.AMAZON.COM Inference already accounts for roughly 60% of AI compute demand, spurring purpose-built chips that deliver higher throughput-per-watt than general GPUs. Financial institutions are aggressive adopters because fraud-detection and conversational banking workloads require sub-100 millisecond latency, achievable only through edge-distributed inference clusters.

Rapid 5G Stand-Alone Core Deployments Accelerating Use Cases

Commercial stand-alone 5G cores were live in 78 countries by the end of 2025, up from 42 a year earlier.[2]GSMA, “Intelligence 5G Tracker,” GSMA.COM Operators monetize network slicing through enterprise contracts for factory automation, remote surgery, and autonomous-vehicle coordination. China Mobile activated 1.2 million 5G base stations supporting industrial IoT across Guangdong and Jiangsu. Private 5G deployments in logistics and mining now bypass public carriers to cut leased-line costs while retaining data sovereignty. Spectrum-sharing regimes such as the FCC’s CBRS further lower entry barriers for non-telecom entities.

Regulatory Push For Digital Sovereignty And Secure Cloud Regions

Europe’s Digital Operational Resilience Act obliges banks to keep operational control when outsourcing to cloud, effectively mandating hybrid topologies. China’s Multi-Level Protection Scheme 2.0 mandates that sensitive workloads remain within sovereign zones, prompting domestic cloud expansion and foreign-provider partnerships. Oracle, for example, partnered with Saudi Telecom Company to open a sovereign region in Riyadh that meets local residency rules.[3]Ericsson, “Mobility Report 2025,” ERICSSON.COM Vendors offering unified control planes across on-premise, sovereign, and public regions are best positioned to capture regulated workloads.

Proliferation Of Edge Computing And IoT Data Streams

Connected devices topped 18 billion in 2025, generating 90 zettabytes of data, yet only 15% traverses wide-area networks to centralized clouds. Manufacturers now deploy edge servers in assembly plants to run computer-vision quality control that cuts scrap rates by 8-12%. Telecom operators monetize multi-access-edge computing by hosting third-party apps within 10 milliseconds of users, a latency ceiling critical for AR navigation and cloud gaming. Data-localization clauses in GDPR and China’s Personal Information Protection Law make edge processing a legal necessity for cross-border operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Semiconductor Supply-Chain Vulnerabilities | -0.7% | Global with acute exposure in regions reliant on Taiwan and South Korea | Short term (≤ 2 years) |

| Mounting Energy Costs of Hyperscale Data Centers | -0.5% | Europe and parts of North America lacking subsidized renewables | Medium term (2-4 years) |

| Skills Gap in Advanced Cybersecurity and AIOps | -0.4% | Global, especially emerging markets | Long term (≥ 4 years) |

| Fragmented Standards for Interoperable Industry 4.0 Solutions | -0.3% | Europe, North America, APAC manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Semiconductor Supply-Chain Vulnerabilities

Advanced packaging for high-bandwidth memory and chiplet integration remains concentrated in Taiwan and South Korea, lifting AI-accelerator lead times to 12-18 months during 2025. The United States CHIPS and Science Act and the European Chips Act earmark USD 52 billion and EUR 43 billion (USD 47.3 billion) respectively for on-shore fabs, yet volume production will not start before 2027. Enterprises over-order parts to hedge shortages, tying up capital that could fund software or talent. Hyperscalers mitigate risk by designing custom silicon, a path unavailable to smaller providers that now face margin compression.

Mounting Energy Costs Of Hyperscale Data Centers

European electricity prices rose sharply in 2025, eroding data-center profit pools where renewable-energy contracts are not subsidized. Operators accelerate adoption of liquid cooling and supply-chain power-purchase agreements to manage rising kilowatt-hour costs. Regions with abundant hydro and wind attract new builds, while locations reliant on thermal generation see delayed projects. Governments respond with incentives for green-data-center zones, yet permitting delays for transmission upgrades remain a hurdle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Lead While Software Races Ahead

The 2025 benchmark showed IT Services at 32.84% revenue, anchoring the Information and Communications Technology market as enterprises outsource modernization, migration, and security operations. The hardware slice continues to decelerate because higher performance-per-watt elongates server life cycles. Conversely, subscription-based software unlocked a 6.84% CAGR through 2031 as vendors convert upfront licenses into recurring revenue and deploy real-time feature upgrades. This trend redirects procurement toward operating expenditure, smoothing budget approvals for AI-infused productivity suites. Edge hardware finds new life where computer-vision quality control and latency-sensitive analytics need local compute. Continuous regulatory pressure for zero-trust adoption also channels funds into endpoint detection, identity, and data-loss-prevention suites. As a result, the Information and Communications Technology market size attached to IT Software is projected to advance rapidly relative to on-premise hardware.

Subscription momentum signals a durable mix shift. API-first ERP and CRM platforms fold machine-translated chat, automated code generation, and intelligent forecasting into base offerings without site visits. Managed-service providers increasingly resell these capabilities as part of outcome-based contracts, bundling consulting, DevOps, and compliance. Meanwhile, vendors monetize software consumption through tiered options that include reserved price breaks for sustained workloads and burst premiums for episodic use. The Information and Communications Technology market share landscape within software will therefore favor suppliers that embed verticalized AI models directly into business workflows.

By Enterprise Size: Large Budgets Dominate, SMEs Accelerate

Large Enterprises controlled 61.54% of 2025 spending, reflecting expansive digital-transformation roadmaps, multilayer security baselines, and preference for guaranteed service-level agreements. These customers centralize procurement under strategic vendor frameworks, often co-designing road maps that stretch five years. Yet SMEs deliver the faster 6.24% CAGR forecast as consumption-based pricing and turnkey cloud platforms shrink the expertise hurdle. Low-code interfaces and pre-packaged compliance accelerate launch timelines for fintech, retail, and health-tech start-ups.

SME adoption also benefits from regulatory sandboxes that waive certain capital requirements during product testing, enabling quick iteration cycles. Community banks and mid-market manufacturers now access the same data-lake and analytics backbones once reserved for enterprise budgets. This democratization intensifies competitive pressure on incumbents that postpone modernization, thereby expanding total demand captured under the Information and Communications Technology market umbrella.

By Deployment Model: Hybrid Becomes Default Architecture

Public-cloud services captured 45.77% spend in 2025, but hybrid models now post a 6.57% CAGR through 2031 as digital-sovereignty laws and low-latency use cases shift strategies. Financial-services regulators in Europe direct banks to maintain operational control over critical workloads hosted in cloud, driving dual-region architectures blending sovereign zones with hyperscaler burst capacity. Similar mandates in China reinforce domestic data processing. The Information and Communications Technology market size attached to hybrid solutions aligns with enterprises seeking cost elasticity without surrendering data governance.

On-premise footprints shrink overall, yet specialized sectors continue refreshing private clouds for intellectual property and classified workloads. Vendors answer with unified control planes, enabling policy, identity, and observability to span public cloud, private cloud, and edge. For disaster recovery, asynchronous replication to object storage in hyperscale regions replaces secondary data-center leases, optimizing total cost of ownership. Competitive positioning hinges on cross-domain consistency, which will determine the Information and Communications Technology market share secured by each platform provider.

By End-User Industry Vertical: Government Anchors, Gaming Surges

Government and public administration delivered 18.84% of 2025 demand, driven by multi-year projects replacing mainframes with containerized microservices and embedding AI chatbots in citizen portals. Compliance with FedRAMP High and IL5 tiers funnels contracts to providers meeting strict security baselines. Meanwhile, gaming and esports unlock the fastest 7.43% CAGR as real-time rendering, anti-cheat inference, and in-game ad exchanges increase compute intensity per active user.

Financial services maintain robust outlays for anti-money-laundering and stress-testing platforms, while energy utilities expand IoT and edge analytics to balance renewables. Manufacturing firms deploy digital twins to reduce downtime and accelerate line re-tooling. Retail and logistics invest in computer-vision checkout and route optimization. Healthcare embraces AI for drug discovery and remote monitoring, encouraged by regulators approving new AI-enabled devices. These diverse growth vectors confirm that the Information and Communications Technology market remains a foundational enabler across every value chain.

Geography Analysis

North America sustained the largest regional outlay at 39.78% in 2025, underpinned by the concentration of hyperscalers, deep venture-capital pools, and federal procurement favoring domestic cloud for classified workloads. The United States alone represented roughly 70% of regional spending, with Canada and Mexico contributing through cross-border interconnection and near-shore development centers. Growth is moderating as large-enterprise cloud penetration nears saturation, steering vendors toward mid-market and public-sector accounts. Canada’s Digital Charter Implementation Act stimulates investment in privacy-enhancing technologies, while Mexico’s data-center corridors attract capacity for Latin American coverage.

Asia-Pacific posts the highest 7.68% CAGR through 2031, fueled by national digital public-infrastructure rollouts in India, Indonesia, and the Philippines. These programs harmonize identity and payments platforms across fragmented provincial systems, creating a scalable base for e-commerce, telemedicine, and ed-tech. China remains the single largest market inside the region, propelling indigenous cloud and semiconductor ecosystems. India’s production-linked incentive scheme attracted USD 28 billion in electronics commitments, positioning the country as an alternate server-assembly hub. Japan and South Korea invest in 6G research and quantum test beds, while Australia and New Zealand harden cybersecurity frameworks for critical infrastructure.

Europe grows more slowly due to stringent data-protection rules and high energy costs, yet leads in digital-sovereignty policies that generate demand for in-region cloud and edge facilities. Germany, the United Kingdom, France, and Spain account for more than 60% of regional spending, with Germany’s automotive sector driving private 5G adoption. The European Chips Act sparks fabrication commitments such as Intel’s EUR 33 billion (USD 36.3 billion) pledge. South America progresses through cloud-based financial services, exemplified by Brazil’s Pix and Argentina’s digital-ID push.

The Middle East and Africa emerge as strategic hubs, with the United Arab Emirates and Saudi Arabia offering renewable power and tax incentives to attract hyperscaler facilities. Saudi Arabia’s NEOM plans a carbon-neutral cluster targeting AI training. South Africa mandates broadband for 90% of citizens by 2030, while Nigeria funds rural connectivity to extend mobile money.

Competitive Landscape

The Information and Communications Technology market exhibits moderate concentration, with the top 10 vendors capturing roughly 35-40% revenue in 2025. Hyperscalers move upstream into managed security and AIOps, threatening systems integrators. Microsoft expanded via multiple cybersecurity acquisitions, and Oracle forged sovereign-cloud alliances with national telecom operators. Open-source foundations gain momentum in edge orchestration and federated learning, giving rise to interoperability niches. Patent filings in AI accelerators and quantum-error-correction jumped 34% during 2025, signaling intensifying platform competition.

Indian IT-services leaders opened Latin-American and Eastern-European centers to exploit talent cost advantages and timezone alignment. Niche challengers differentiate through verticalization, such as healthcare-focused clouds pre-integrated with electronic-health-record standards. Hardware vendors pivot toward software subscriptions and managed services as consumption-based pricing compresses device margins. Dell Technologies and Hewlett Packard Enterprise now derive more than half of revenue from subscriptions and services.

Partnership ecosystems also deepen. Telecom operators bundle private 5G, edge compute, and security services. Chip designers collaborate with foundries and cloud providers to co-optimize silicon for AI workloads. As vendors race to lock-in developer mindshare via SDKs and open APIs, long-term differentiation will hinge on cross-domain governance, power efficiency, and sovereign compliance credentials.

Information And Communications Technology (ICT) Industry Leaders

Microsoft Corporation

Cisco Systems, Inc.

International Business Machines (IBM) Corporation

Alphabet Inc.

Amazon Web Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft announced a USD 80 billion expansion plan for AI-optimized data centers across North America and Europe, targeting completion by 2027.

- December 2025: Amazon Web Services unveiled Trainium2, offering 4x training and 3x inference throughput over its predecessor while cutting power use 40%; reserved-capacity pricing locks multiyear costs.

- November 2025: Tata Consultancy Services signed a USD 1.2 billion, seven-year deal with a European telco to modernize 450 legacy apps on a hybrid-cloud microservices stack.

- October 2025: Oracle and Saudi Telecom Company launched a sovereign-cloud region in Riyadh that meets local data-residency mandates.

Global Information And Communications Technology (ICT) Market Report Scope

ICT stands for Information and Communication Technology, referring to a broad range of technologies, tools, and services used for communication, information processing, and data management.

The Information and Communications Technology Report is Segmented by Type (Hardware including Computer Hardware, Networking Equipment, and Peripherals; IT Software; IT Services including Managed Services, Business Process Services, Business Consulting Services, and Cloud Services; IT Infrastructure; IT Security; Communication Services), Enterprise Size (Small and Medium Enterprises, Large Enterprises), Deployment Model (On-Premise, Cloud, Hybrid), End-User Industry Vertical (Government and Public Administration, BFSI, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Gaming and Esports), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-Premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up/Mid/Down-stream) |

| Gaming and Esports |

| Other Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Type | Hardware | Computer Hardware | |

| Networking Equipment | |||

| Peripherals | |||

| IT Software | |||

| IT Services | Managed Services | ||

| Business Process Services | |||

| Business Consulting Services | |||

| Cloud Services | |||

| IT Infrastructure | |||

| IT Security | |||

| Communication Services | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Deployment Model | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By End-User Industry Vertical | Government and Public Administration | ||

| BFSI | |||

| Energy and Utilities | |||

| Retail, E-commerce and Logistics | |||

| Manufacturing and Industry 4.0 | |||

| Healthcare and Life Sciences | |||

| Oil and Gas (Up/Mid/Down-stream) | |||

| Gaming and Esports | |||

| Other Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Information and Communications Technology market by 2031?

The sector is forecast to reach USD 8.39 trillion by 2031, expanding at a 5.85% CAGR from its 2026 baseline.

Which deployment model is expected to grow fastest through 2031?

Hybrid-cloud architectures lead growth with a 6.57% CAGR as enterprises balance data sovereignty with scalable capacity.

Why are SMEs increasing their share of ICT spending?

Consumption-based pricing and turnkey cloud platforms eliminate large capital outlays, allowing SMEs to adopt advanced capabilities quickly.

Which end-user segment shows the highest growth momentum?

Gaming and esports post the fastest 7.43% CAGR as real-time rendering and in-game advertising demand low-latency infrastructure.

How are semiconductor supply risks affecting ICT expansion?

Concentrated packaging capacity in Taiwan and South Korea stretches AI-chip lead times to 12-18 months, compelling enterprises to over-order and inflating inventory costs.

What characterizes competition among leading ICT providers?

Hyperscalers vertically integrate security and AIOps, while niche vendors differentiate through industry-specific solutions and open-source interoperability.

Page last updated on: