Market Overview

| Study Period | 2020 - 2031 |

|---|---|

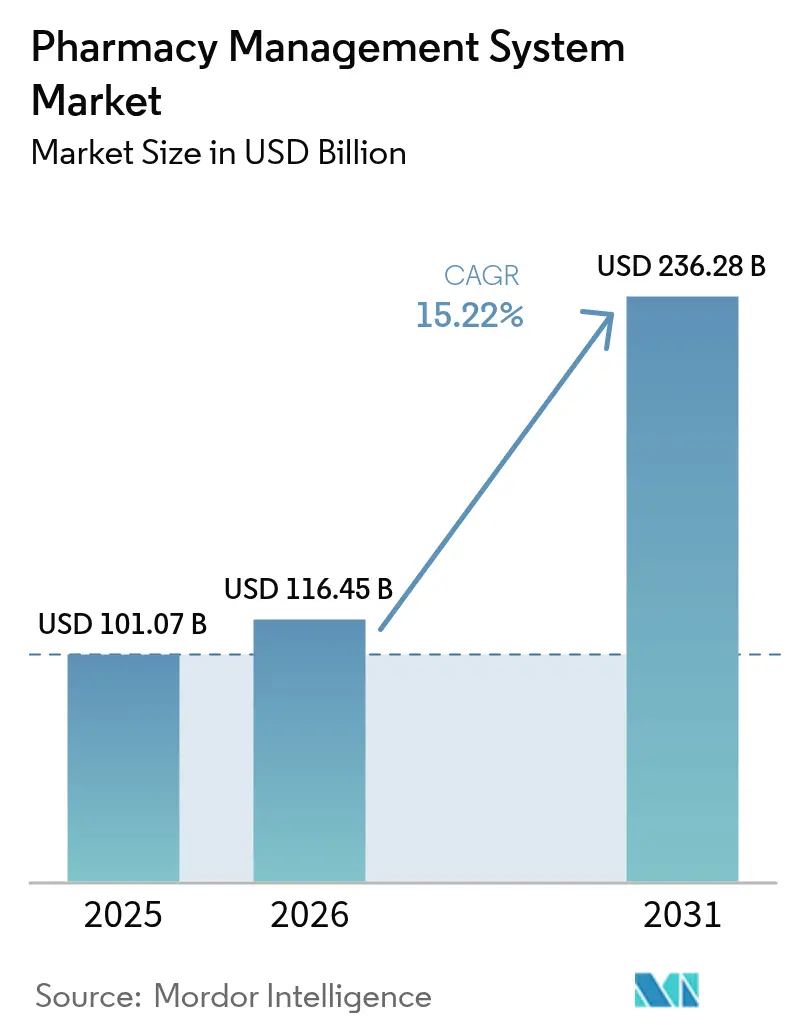

| Market Size (2026) | USD 116.45 Billion |

| Market Size (2031) | USD 236.28 Billion |

| Growth Rate (2026 - 2031) | 15.22% CAGR |

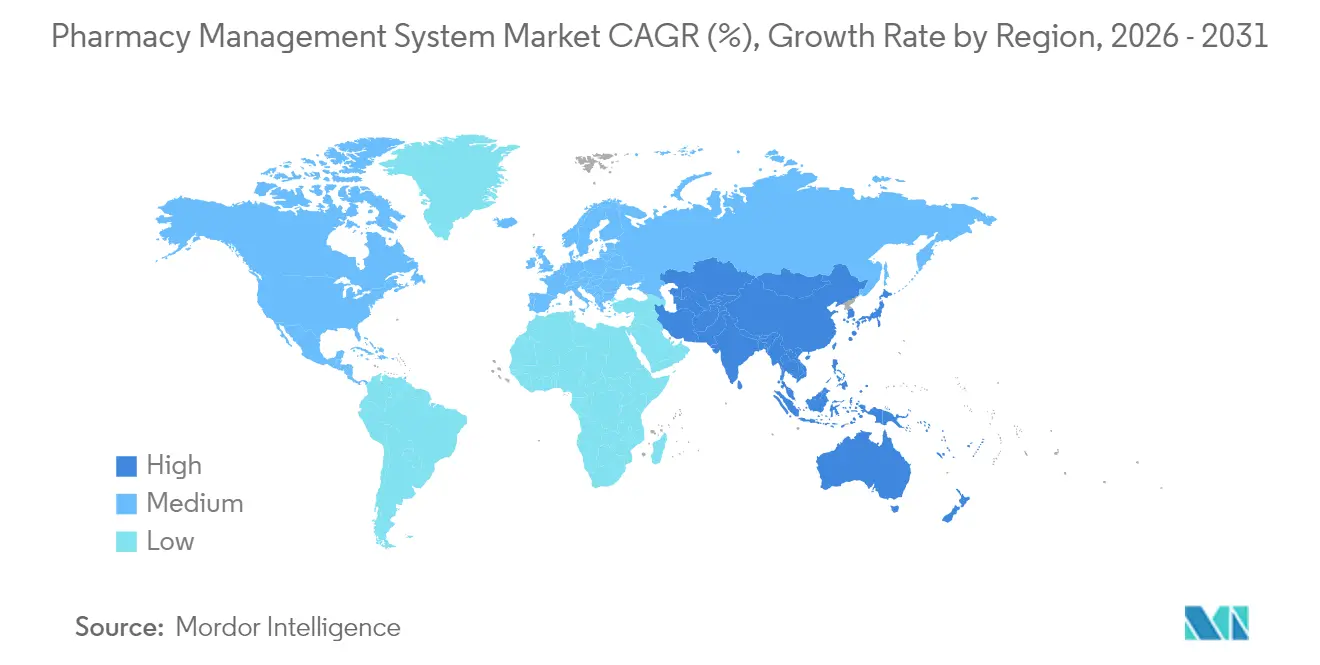

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmacy Management System Market Analysis by Mordor Intelligence

Pharmacy Management System market size in 2026 is estimated at USD 116.45 billion, growing from 2025 value of USD 101.07 billion with 2031 projections showing USD 236.28 billion, growing at 15.22% CAGR over 2026-2031.

The quick rise mirrors a wider transformation in which pharmacies evolve from product-dispensing outlets into digitally connected care hubs. Demand is escalating for cloud platforms that scale easily, for integrated modules that meet tightening safety rules, and for analytics that offset thin margins by lifting operational efficiency. Competition now revolves around technology depth instead of store count, while patient expectations for clinical services push every provider to modernize workflows. North America supplies the largest revenue base, yet Asia-Pacific provides the steepest growth curve as governments fund new digital infrastructure.

Key Report Takeaways

- By cloud deployment held 62.85% of the pharmacy management system market share in 2025 and is on track to expand at a 17.18% CAGR through 2031.

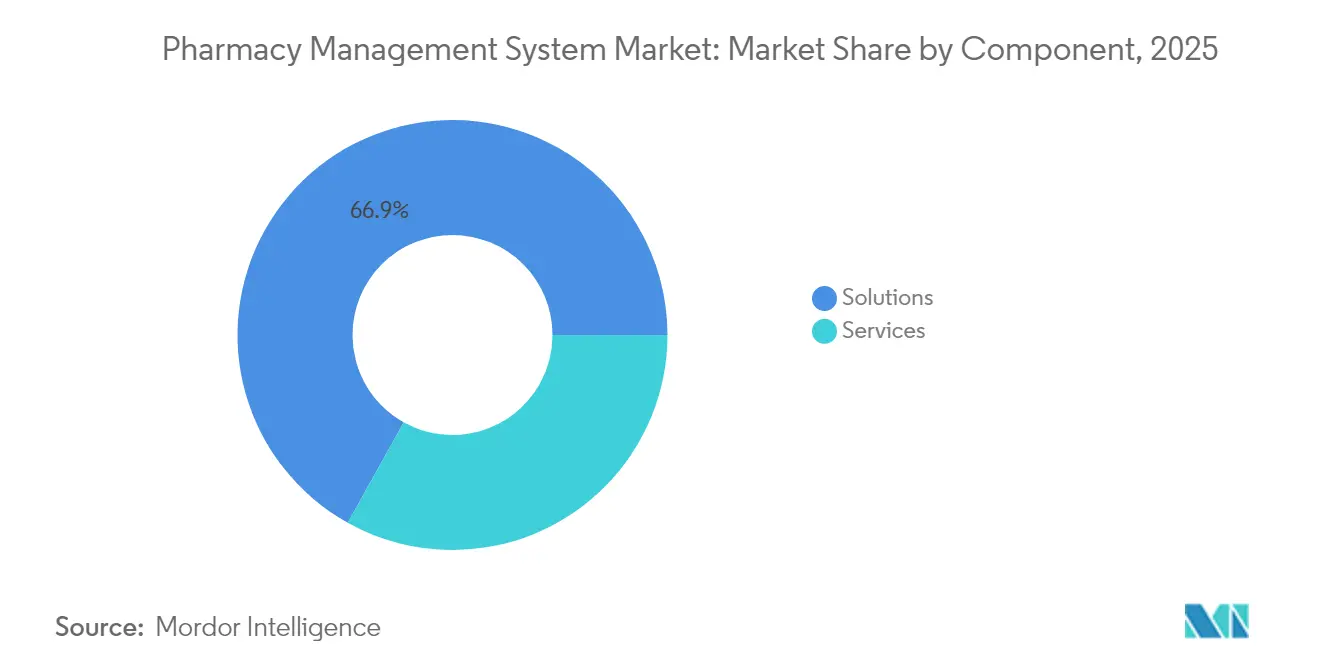

- By solutions captured 66.90% of the pharmacy management system market size in 2025, while services will post a 16.05% CAGR between 2026 and 2031.

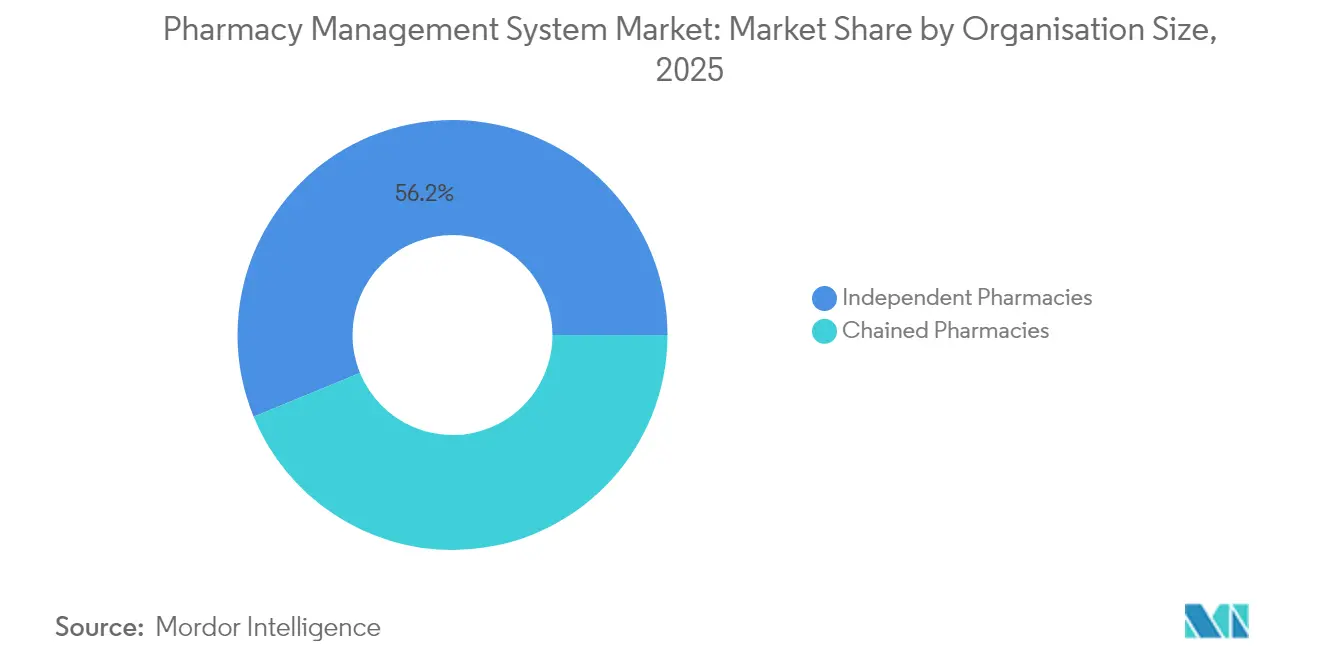

- By independent pharmacies controlled 56.20% of the pharmacy management system market share in 2025; chained pharmacies are poised for 16.84% CAGR to 2031.

- By retail and community locations led with 43.95% revenue share in 2025, whereas long-term-care and specialty outlets will rise at a 14.96% CAGR through 2031.

- By North America accounted for 40.55% of 2025 revenue, but Asia-Pacific is forecast to post the quickest 17.72% CAGR over the period to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmacy Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prescription volumes burdening pharmacists | +2.8% | North America and Europe, spreading globally | Medium term (2-4 years) |

| Rapid shift toward cloud-hosted pharmacy platforms | +3.2% | North America and Asia-Pacific | Short term (≤2 years) |

| Stringent global medication-safety regulations | +2.1% | Global | Long term (≥4 years) |

| Cost-savings from AI-led inventory optimisation | +1.9% | Developed markets first | Medium term (2-4 years) |

| Integration of pharmacogenomics modules | +1.4% | North America and Europe | Long term (≥4 years) |

| Expansion of tele-pharmacy services | +1.8% | Rural and underserved areas | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Prescription Volumes Burdening Pharmacists

Prescription drug spend in the United States rose at 10–12% during 2024, with GLP-1 anti-obesity agents responsible for more than 80% of incremental revenue, intensifying daily dispensing pressure. Surveys show 61% of Americans now consider pharmacies appropriate sites for primary care, stretching pharmacist duties into counseling and vaccination. Independent outlets feel the strain most, with one closing each day in 2023 because reimbursement cuts and manual workflows eroded profits. Automated dispensing and clinical documentation modules inside the pharmacy management system market remove repetitive tasks, letting pharmacists focus on higher-value services. Providers that adopt advanced workflow engines report fewer errors and shorter wait times, improving patient loyalty.

Rapid Shift Toward Cloud-Hosted Pharmacy Platforms

Eighty-three percent of pharmaceutical organizations already keep core workloads in the cloud, and the sector’s cloud spending is forecast to climb to USD 59.37 billion by 2030. Cloud architectures support real-time data synchronization across chains with thousands of branches, a feat that on-premise servers struggle to match. Demand intensified during the COVID-19 pandemic when remote log-ons and elastic capacity became operational necessities, not optional perks. Modern cloud vendors also certify against regional privacy frameworks, lowering concerns over data sovereignty that once delayed adoption. As subscription pricing aligns IT cost with prescription volume, even single-site independents enter the pharmacy management system market to access enterprise-grade analytics without capital outlays.

Stringent Global Medication-Safety Regulations

The U.S. Drug Enforcement Administration warns that hackers now steal DEA numbers and fabricate thousands of orders, forcing pharmacies to tighten controlled-substance oversight.The Office of the National Coordinator formed a Pharmacy Interoperability Task Force to make audit trails and data-exchange standards mandatory for every dispensing system. Parallel moves by the European Medicines Agency and Japan’s PMDA favor platforms that harmonize safeguards across borders. These aligned mandates accelerate spending on secure e-prescription, barcode verification, and real-time diversion monitoring inside the pharmacy management system market. Specialty and long-term-care operators adopt compliance dashboards because their high-alert medication mix exposes them to heavier penalties.

Cost-Savings from AI-Led Inventory Optimisation

Artificial-intelligence engines help pharmacies cut inventory holdings by 20% through smarter demand forecasts and optimal reorder triggers. By illuminating rebate flows and contract tiers, AI tools also deflate the USD 356 billion spread between list and net drug prices reported for 2024. Walgreens now routes 40% of its prescriptions through automated micro-fulfillment hubs, trimming labor cost while raising accuracy. Early adopters gain a hedge against technician shortages and reimbursement pressure, prompting rivals to embed predictive modules quickly. As AI matures, performance gaps widen between pharmacies that mine data and those stuck on batch-based reporting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vendor lock-in with legacy vendors | -2.4% | Global, entrenched installations | Medium term (2-4 years) |

| Escalating cyber-security and privacy concerns | -1.9% | Highly regulated markets | Short term (≤2 years) |

| High upfront automation capital cost | -1.6% | Emerging economies and independents | Short term (≤2 years) |

| FHIR interoperability gaps with next-gen EHRs | -1.3% | Developed multi-system regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Vendor Lock-in with Legacy Vendors

Large health systems often rely on bespoke builds that weave dispensing, billing, and formulary data into proprietary formats; switching vendors can cost millions and demand months of retraining [1]NEXTDC, “When Sustaining Growth is the Highest Business Priority,” nextdc.com . Independent outlets face different barriers, such as limited IT staff and fear of downtime that threaten fragile cash flows. Consolidation can deepen lock-in when an acquirer phases out open APIs, as observers noted after BD paid USD 1.548 billion for Parata Systems in 2024. Cloud newcomers gradually erode these obstacles by offering migration utilities and pay-as-you-grow terms, yet full transition remains protracted while legacy contracts run their course.

Escalating Cyber-Security and Privacy Concerns

Pharmaceutical firms endured some of the world’s most expensive data breaches in 2024, and every compromise raises legal exposure for dispensing sites that transmit protected health information. Independent pharmacies hesitate to pool data in the cloud because they doubt they can oversee vendor security. HIPAA rules oblige owners to document every AI inference tied to patient care, adding governance layers that slow rollouts. Vendors respond with on-shore data centers, zero-trust frameworks, and continual penetration tests, but many buyers still opt for hybrid deployments that trade efficiency for perceived control.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component – Solutions Anchor Core Operations

Solutions products generated 66.90% of the pharmacy management system market size in 2025, reflecting the non-negotiable need for e-prescription processing, inventory control, and compliance tracking. The segment’s built-in clinical checks and automated financial reconciliation guard against errors that can spark regulatory fines. Hospitals and chains deploy multi-module suites so pharmacists practice at the top of license while systems handle repetitive inputs. Growth in services, expected at 16.05% CAGR to 2031, shows users increasingly seek configuration, staff training, and managed hosting once the base software is live.

The services wave signals a maturing marketplace in which optimization extends long after go-live. Pharmacies demand analytics tuning, security patching, and workflow redesign as new reimbursement rules arrive. Consultants embed benchmark dashboards that compare fill rates, wait times, and payer mix across branches, helping operators defend margin. Vendors that blend software and advisory support position themselves for stickier revenue streams, deepening share within the pharmacy management system market.

By Deployment – Cloud Leads Modern Infrastructure

Cloud installations owned 62.85% share in 2025 and will post the fastest 17.18% CAGR through 2031, underscoring how elasticity, lower upfront cost, and seamless updates outweigh the comfort of on-premise hardware. Chains favor cloud to standardize data across hundreds of outlets, while independents welcome subscription models that convert capital expenditure into operating cost.

On-premise footprints shrink as cyber-risk mitigation, redundancy, and maintenance demand skills that small IT teams cannot supply. Compliance auditors now rate cloud systems higher because vendors maintain hardened environments certified under multiple frameworks. The pivot enhances real-time collaboration among prescribers, payers, and pharmacists, deepening adoption of the pharmacy management system market across geographies.

By Organisation Size – Independents Retain Scale but Chains Outpace Growth

Independents commanded 56.20% of 2025 revenue, yet consolidation is unavoidable while payer reimbursement lags cost inflation and manual tasks drain margin. One proprietor shuttered daily in 2023, revealing fragile economics. Chains counter the headwinds through bulk purchasing and shared services, helping them register a 16.84% CAGR to 2031.

Co-operatives and buying groups equip single-site owners with shared cloud instances, lowering entry barriers to the pharmacy management system market. Chain operators meanwhile pour capital into robotics, predictive staffing, and preventive care programs that elevate brand perception. The divide pressures software vendors to craft tiered offerings—lightweight for small shops and enterprise-grade for multi-state networks.

By End-User Industries – Retail Still Rules, Specialty Surges

Retail and community locations produced 43.95% of 2025 turnover, confirming that corner stores remain the first touchpoint for everyday ailments . They require point-of-sale, OTC catalog, and vaccination modules in a single interface so staff can pivot swiftly between tasks. Long-term-care and specialty providers, advancing at a 14.96% CAGR, demand regimented dosing schedules, cold-chain monitoring, and payer-specific adherence reports.

Higher-acuity therapies invite tighter oversight and clinical note capture inside the pharmacy management system market. Vendors now integrate medication administration records with patient education and courier routing to ensure temperature control. Hospital pharmacies focus on closed-loop medication administration that mates with electronic health records, cutting adverse events and shortening stays .

Geography Analysis

North America’s dominance rests on mature insurance markets, sizable chain footprints, and regulators that mandate electronic checks at every dispense. U.S. initiatives to combat opioid misuse spur uptake of real-time prescription monitoring, while Canada’s universal coverage highlights the need for cost-efficient refill coordination. Recent DEA alerts about EHR fraud accelerate investments in audit trails and multifactor authentication. Venture funding also flows into AI start-ups that promise workflow relief, widening the technology gap between modern and legacy stores.

Asia-Pacific records the fastest trajectory as China, India, and Indonesia upgrade primary-care delivery and digitize supply chains. National e-health blueprints channel subsidies into cloud-ready software so rural clinics share records with urban hospitals. Japan’s rapidly aging population sharpens focus on medication adherence apps that integrate with dispensing platforms. Multinational chains entering Southeast Asia insist on enterprise systems that mirror their Western operations, fueling demand within the pharmacy management system market.

Europe sits between these extremes. Harmonized EMA guidelines push pharmacies to track serial numbers and report adverse events uniformly across borders. Brexit introduces extra customs documentation, encouraging British outlets to automate replenishment and regulatory filings. Scandinavian markets, long early adopters of e-prescription, now upgrade to AI-enabled forecasting that offsets higher labor costs. Throughout the continent, privacy regulations such as GDPR favor vendors that offer fine-grained consent management.

Competitive Landscape

Competition remains moderately fragmented. Large healthcare IT players McKesson, Omnicell, and Oracle Health bundle dispensing, supply chain, and analytics features to hold enterprise contracts. Mid-tier specialists such as ScriptPro focus on robotics, while RedSail Technologies courts independents with cloud POS and adherence modules. Technology edge now outweighs storefront count; buyers prioritize AI decision support, open APIs, and cybersecurity credentials when selecting platforms.

Consolidation is quickening as incumbents grab niche innovators. BD’s USD 1.548 billion take-over of Parata Systems brought robotic fulfillment under its medication management umbrella [4]Becton, Dickinson and Company, “10-K 2024,” bd.com. Innovaccer’s purchase of Pharmacy Quality Solutions delivered performance metrics covering 95% of community outlets, expanding value-based care analytics. Private-equity group Sycamore Partners agreed to acquire Walgreens Boots Alliance for USD 23.7 billion, a move expected to pump capital into automation across thousands of stores.

AI and cloud newcomers challenge long-standing brands. Asepha drew USD 4 million in July 2025 to refine machine-learning models that cut verification time by 40%. PQS launched EQUIPP Copilot to surface performance gaps in real time, giving community pharmacies insights typically reserved for larger chains. Vendors able to interoperate with payer portals, telehealth apps, and smart-device sensors win share as healthcare delivery converges.

Pharmacy Management System Industry Leaders

McKesson Corporation

Cerner Corporation

Becton Dickinson and Co.

GE Healthcare Inc.

Omnicell, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Asepha raised USD 4 million in seed funding to accelerate AI tools that streamline pharmacy operations.

- May 2025: PQS released EQUIPP Copilot, an AI workflow optimizer for pharmacies.

- March 2025: Sycamore Partners moved to buy Walgreens Boots Alliance in a USD 23.7 billion deal.

- February 2025: McKesson agreed to purchase PRISM Vision Holdings for roughly USD 850 million, expanding its specialty retina services

- January 2025: LifeMD opened a 22,500 sq ft affiliated pharmacy capable of filling 5,000 prescriptions daily and saving USD 5 million in annual expenses.

Global Pharmacy Management System Market Report Scope

A pharmacy management software system enables pharmacists to provide efficient, professional, and personalized care based on a patient's needs and requirements and streamlines their workflow.

The pharmacy management software systems market is segmented by component (solutions (inventory management, purchase orders management, supply chain management, regulatory, and compliance information, clinical and administrative performance, and other solutions) and services), deployment (cloud-based and on-premise), size of organization (independent pharmacies and chained pharmacies), and geography (North America, Europe, Asia-Pacific, and Rest of the World).

The market sizes and forecasts are provided in value (USD) for all the above segments.

By Component

| Solutions | Inventory Management |

| Purchase Order Management | |

| Supply-Chain Management | |

| Regulatory and Compliance Information | |

| Clinical and Administrative Performance | |

| Other Solutions | |

| Services |

By Deployment

| Cloud-based |

| On-premise |

By Organisation Size

| Independent Pharmacies |

| Chained Pharmacies |

By End-User Industries

| Hospital Pharmacies |

| Retail/Community Pharmacies |

| Long-term-care and Specialty Pharmacies |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Solutions | Inventory Management |

| Purchase Order Management | ||

| Supply-Chain Management | ||

| Regulatory and Compliance Information | ||

| Clinical and Administrative Performance | ||

| Other Solutions | ||

| Services | ||

| By Deployment | Cloud-based | |

| On-premise | ||

| By Organisation Size | Independent Pharmacies | |

| Chained Pharmacies | ||

| By End-User Industries | Hospital Pharmacies | |

| Retail/Community Pharmacies | ||

| Long-term-care and Specialty Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current pharmacy management system market size and its expected growth?

The pharmacy management system market size is USD 116.45 billion in 2026 and is forecast to reach USD 236.28 billion by 2031 at a 15.22% CAGR.

Which deployment model leads the market?

Cloud platforms lead with 62.85% share in 2025 and are expanding fastest at a 17.18% CAGR thanks to scalability and lower upfront cost.

Why are independent pharmacies investing in management systems despite tight margins?

They need automation to counter reimbursement cuts and workload spikes; without technology, independents risk closure as seen in the 2023 shutdown rate of one store per day in the United States.

What role does AI play in pharmacy operations?

AI cuts inventory investment by around 20%, automates fulfillment hubs, and surfaces adherence risks, producing measurable cost savings and service improvements.

Page last updated on: