Outplacement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

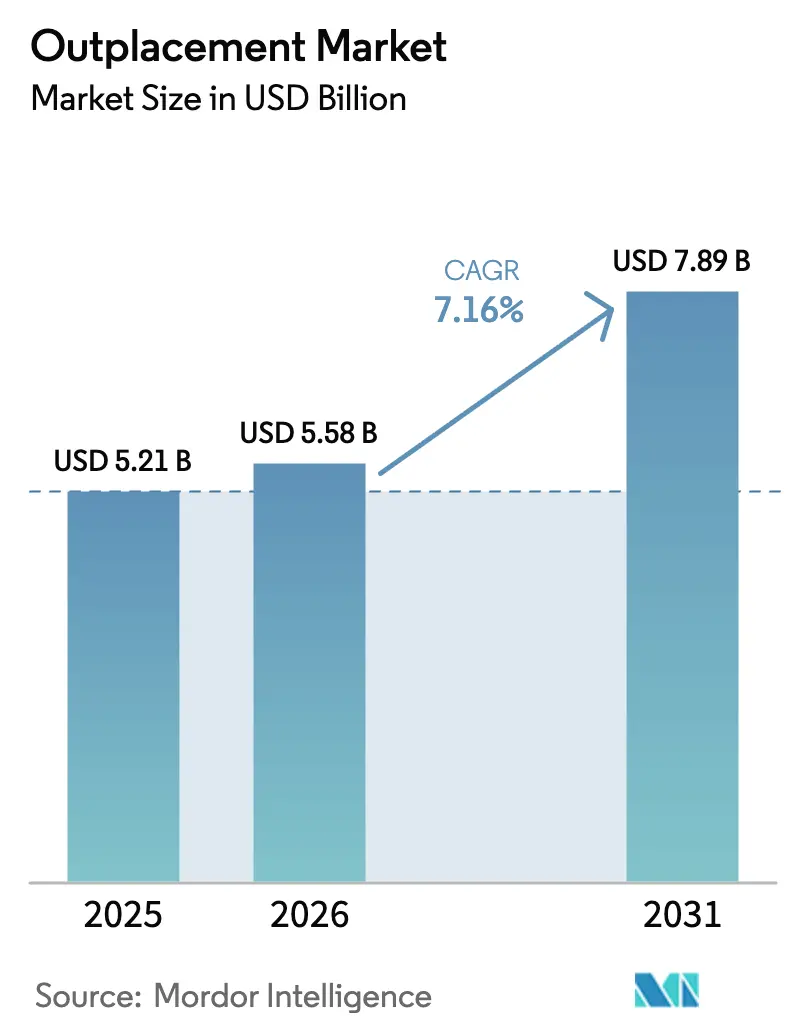

| Market Size (2026) | USD 5.58 Billion |

| Market Size (2031) | USD 7.89 Billion |

| Growth Rate (2026 - 2031) | 7.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outplacement Market Analysis by Mordor Intelligence

The outplacement services market size is expected to grow from USD 5.21 billion in 2025 to USD 5.58 billion in 2026 and is forecast to reach USD 7.89 billion by 2031 at 7.16% CAGR over 2026-2031. Rising corporate restructuring, rapid AI adoption, and intensifying employer-branding pressures are repositioning outplacement from discretionary cost to strategic workforce tool. Continuous head-count reductions across technology, energy, and retail are fueling steady contract volumes, while digitally native platforms are compressing job-search cycles and broadening geographic reach. Executive churn remains elevated, prompting premium service uptake, and regulatory push in Europe is hard-wiring transition support into dismissal processes. These intertwined forces create a resilient demand curve that firmly underpins the outplacement services market through 2030.

Key Report Takeaways

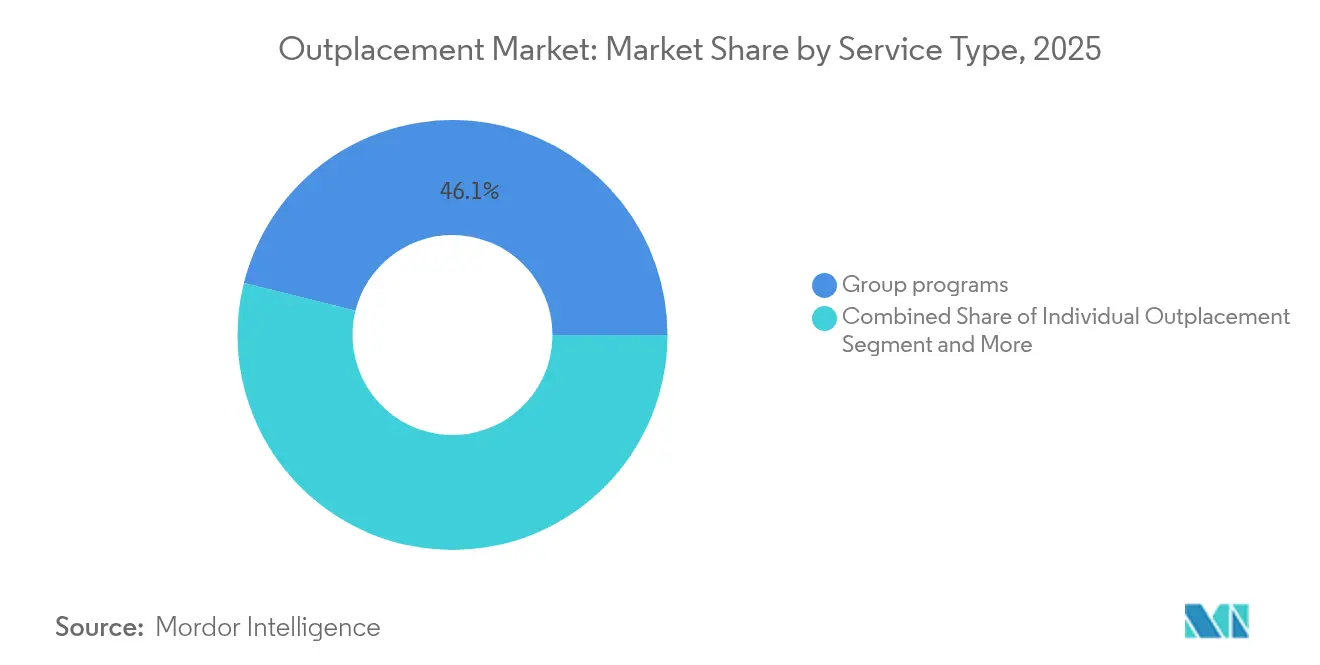

- By service type, group outplacement led with 46.12% of outplacement services market share in 2025; executive outplacement is tracking the fastest 10.12% CAGR to 2031.

- By delivery mode, virtual and online programs captured 61.30% revenue share in 2025, while the same channel is expanding at a 13.65% CAGR.

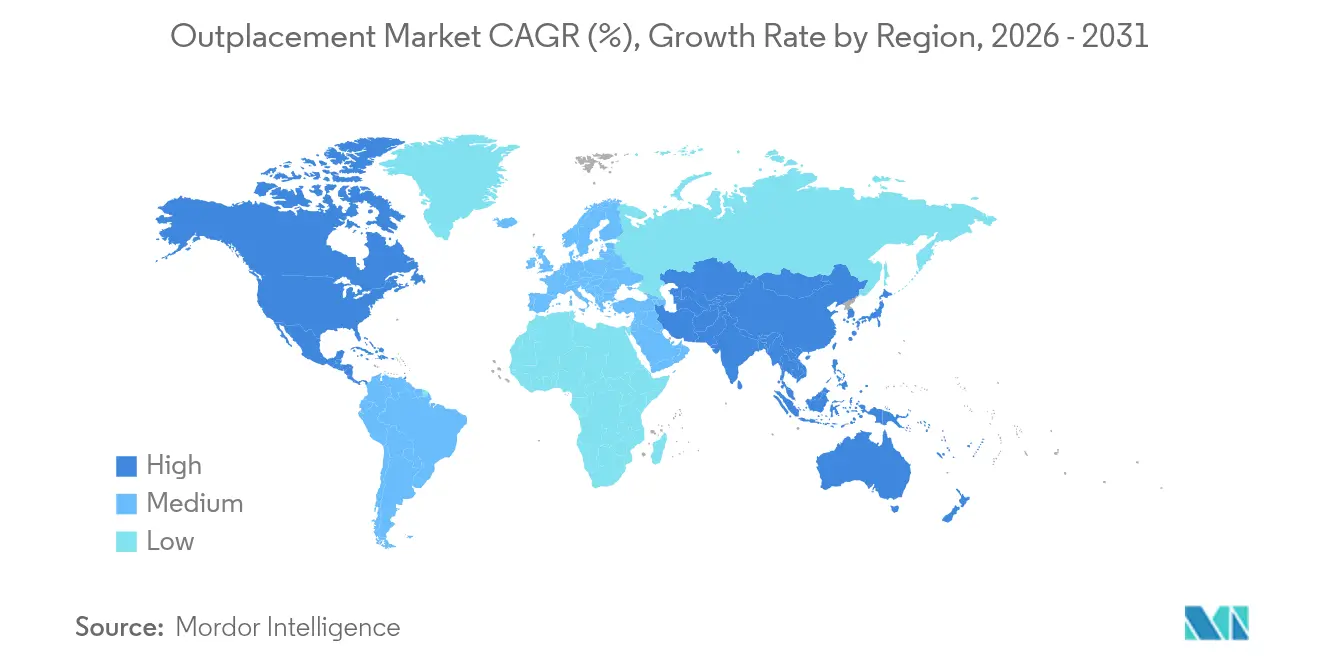

- By geography, North America contributed 41.40% of 2025 revenues; Asia Pacific is projected to record the highest 8.63% CAGR through 2031.

- By end-user, enterprise clients held 69.25% share of the outplacement services market size in 2025; the personal segment is projected to grow at an 8.41% CAGR.

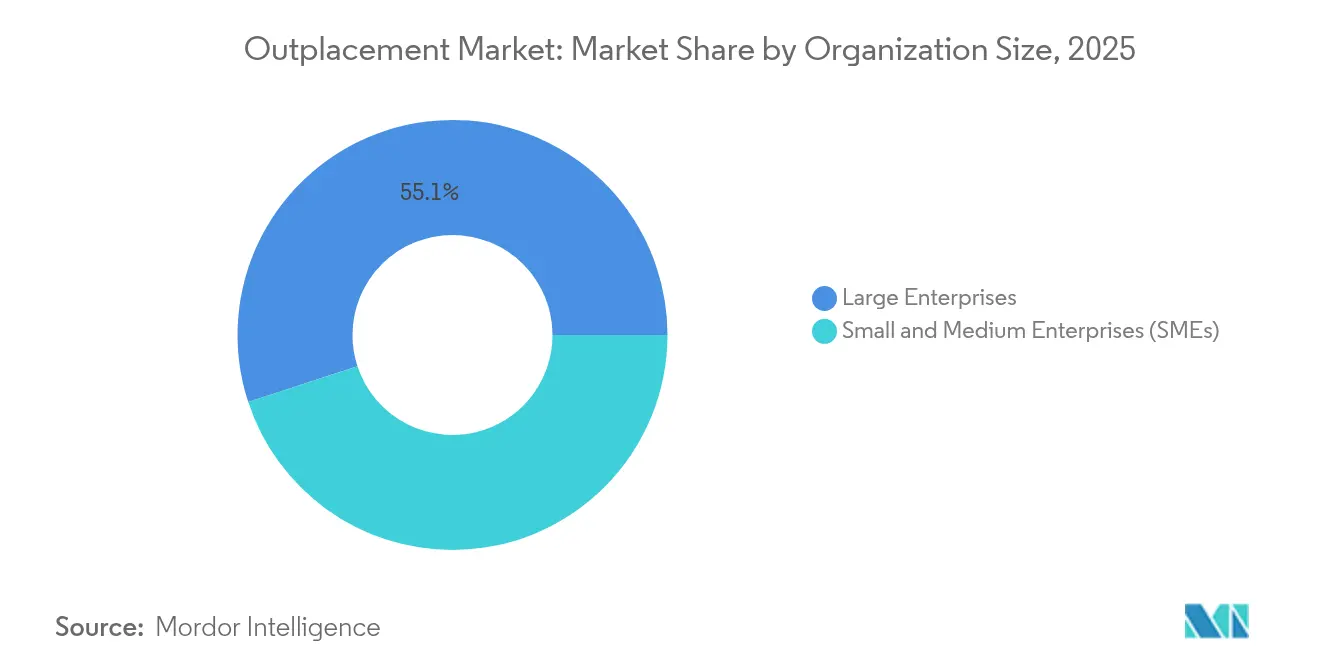

- By organization size, large enterprises accounted for 55.05% share in 2025, whereas SMEs represent the fastest-rising cohort with a 9.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Outplacement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate restructuring and downsizing surge | +2.1% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Employer-branding and CSR imperatives | +1.3% | Global, particularly developed markets | Medium term (2-4 years) |

| Expansion of virtual outplacement platforms | +1.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| EU-style regulations mandating transition support | +0.9% | Europe primarily | Long term (≥ 4 years) |

| AI-driven personalised career-pathing | +1.5% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Tech-sector layoff aftershocks in emerging hubs | +0.7% | Asia-Pacific, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Corporate Restructuring and Downsizing Surge

Tech majors and energy giants cut more than 172,000 roles in February 2025 alone, a 245% jump over January, and the layoffs show little sign of reverting to pre-pandemic norms. ManpowerGroup confirmed that demand for its Talent Solutions outplacement unit continued to climb even as its overall staffing revenue softened in 2024. Such structural reductions—often tied to AI investment rather than cyclical slowdowns—signal persistent opportunity for providers across the outplacement services market.

Employer-Branding and CSR Imperatives

Pressure from investors, recruits, and consumer activists is pushing firms to prove that layoff processes remain humane. Right Management found companies offering transition support cut unemployment-insurance outlays by 26% while reporting stronger engagement scores among remaining staff. Embedding outplacement within ESG roadmaps reframes spend as an investment, a perception shift that is widening contract sizes in mature markets.

Expansion of Virtual Outplacement Platforms

Digital programs now deliver career landings twice as fast as legacy models, according to Sherpact’s 2025 user analytics. Cloud portals scale globally at marginal cost, integrate AI résumé parsing, and keep displaced staff connected to far broader job pools. As a result, virtual workflows command the largest slice of the outplacement services market and continue to outpace every other channel.

AI-Driven Personalised Career-Pathing

Neural-network engines can ingest behavioral profiles, market data, and vacancy feeds to surface precise job matches in real time. Talview’s algorithmic interview coach now offers adaptive feedback based on live candidate responses. LHH’s Career Studio blends human mentors with predictive analytics to craft hyper-personal transition plans, raising placement rates and compressing program costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low awareness among SMEs | -1.2% | Global, notably emerging markets | Medium term (2-4 years) |

| Premium-service cost perceptions | -0.8% | Price-sensitive regions | Short term (≤ 2 years) |

| Data-privacy and confidentiality concerns | -0.6% | Europe, North America | Medium term (2-4 years) |

| Rise of gig/freelancing alternatives | -0.9% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Awareness Among SMEs

OECD surveys show small firms still struggle to quantify ROI on transition programs and lack HR bandwidth to vet vendors. While these businesses form the bulk of employers in emerging economies, many perceive outplacement as a luxury for multinationals. The rise of modular online packages priced per seat is beginning to chip away at this barrier, suggesting latent upside once education gaps narrow.

Data-Privacy and Confidentiality Concerns

GDPR positions both employer and provider as data controllers, meaning missteps can expose both parties to stiff penalties. Financial services and healthcare clients are particularly cautious about pushing sensitive career data into external clouds. Providers able to certify zero-trust architectures and granular consent flows gain an edge, but compliance overhead raises costs and slows onboarding in the outplacement services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Executive Outplacement Drives Premium Uptake

Group programs delivered 46.12% revenue in 2025, keeping cost efficiency front and center for mass layoffs in the outplacement services market. C-suite churn, however, is propelling executive packages at a 10.12% CAGR, a pace more than 40% above the overall outplacement services market size for the period 2026-2031. Challenger, Gray and Christmas logged 177 chief-executive exits in March 2025, evidence of the leadership volatility supporting premium demand.

Executive offerings carry bespoke networking access, discreet branding, and complex remuneration consulting. Providers able to marshal board-level mentors and private-equity contacts command fees often 4-6 times higher per participant. The segment’s momentum reinforces a two-tier structure inside the outplacement services market where mass solutions coexist with high-touch advisory lines.

By End-User: Personal Purchases Accelerate

Enterprises still purchase 69.25% of total packages, using umbrella contracts to buffer brand equity and reduce litigation risk. Nevertheless, individually funded subscriptions are expanding at an 8.41% CAGR as professionals shoulder greater career-management responsibility. Gig-economy contractors and mid-career technologists increasingly buy self-serve access to coaching portals.

This shift enlarges the addressable outplacement services market and pushes providers to adopt consumer-grade onboarding, flexible pricing, and always-on support. Peer-rating systems and community forums add social proof that was absent from traditional B2B engagements, nudging reputational dynamics closer to mainstream e-commerce.

By Organization Size: SME Adoption Gains Momentum

Large enterprises made up 55.05% of 2025 billings, buoyed by mandatory programs in certain jurisdictions and robust HR budgets. Even so, SMEs are moving fastest at 9.95% CAGR as stripped-down SaaS products erase historical entry barriers. Thrive’s pay-as-you-go platform lets firms onboard employees in minutes rather than weeks.

Wider SME uptake broadens geographic penetration and reduces revenue seasonality for providers tied to big-ticket corporate events. It also enlarges data pools feeding AI models, further sharpening personalization across the outplacement services market.

By Delivery Mode: Virtual Platforms Secure Dominance

Virtual channels captured 61.30% share in 2025 and remain on a 13.65% growth trajectory. Always-on dashboards, asynchronous video coaching, and global mentor marketplaces underpin that expansion. Careerminds credits its cloud framework with enabling 24/7 access and stronger candidate adherence.

Hybrid designs persist for senior executives or markets valuing face-to-face etiquette, yet pure-play virtual suites now show equal or superior placement metrics in most demographics. As AI conversational agents and holographic meeting rooms mature, the digital modality is positioned to deepen its hold on the outplacement services market share.

Geography Analysis

North America anchored 41.40% of 2025 revenue, benefiting from long-entrenched severance norms and a culture of external career services. Layoff notices often bundle transition help by default, and corporate governance bodies routinely audit employer-brand fallout. QVC, Hudson’s Bay, and Chevron all partnered with top-tier vendors during 2024-2025 restructurings, keeping contract volume elevated. Healthy venture funding in HR tech has also birthed API-driven matching tools that broaden client menus without inflating costs.

Europe’s trajectory is steadier but equally durable, buoyed by statutory backstops. Belgium obliges employers to pay EUR 1,800 (USD 1,926) toward a Return-to-Work fund when dismissing staff for medical incapacity. The European Commission proposed in 2025 to extend the European Globalisation Fund into pre-emptive reskilling grants, effectively underwriting partial program costs for providers. GDPR frameworks elevate provider selection criteria and confer advantage on vendors boasting ISO-27001 data centers, adding defensible moats inside the outplacement services market.

Asia Pacific is the growth engine at an 8.63% CAGR. Japan continues to liberalize redundancy rules, raising outplacement adoption, while Australia’s tech layoffs ripple into fresh contract wins. Randstad RiseSmart appointed a dedicated APAC managing director in 2025 as part of a region-first innovation hub, signaling strategic priority. Cultural stigma around job hopping is gradually receding, aided by platform features that anonymize early engagement between job seekers and employers. This shift primes the outplacement services market size in APAC for sustained upside through 2031.

Competitive Landscape

The competitive field is moderately fragmented: the top five vendors hold less than 40% combined revenue, giving mid-tier specialists room to carve niches. Randstad RiseSmart, Lee Hecht Harrison, and Right Management leverage multinational footprints to win global master agreements, yet local champions thrive by tailoring playbooks to cultural norms and language nuance.

Technology is a decisive differentiator. Careerminds’ October 2024 buyout of AI framework start-up Progression expanded its skills-taxonomy engine, letting the firm export competency libraries across industry clients. Keystone Partners’ acquisition of The Ayers Group bolstered executive coaching depth on the U.S. East Coast. Patent filings like US20200394539A1 around AI-assisted employment matching illustrate sustained IP investment that elevates entry barriers.

White-space remains in SME-centric bundles, sector-specific analytics, and emerging-market localization. Disruptors deploying low-code tooling can integrate with HRIS stacks rapidly, challenging incumbents reliant on legacy portals. Meanwhile, vendor due diligence matrices are widening to include data sovereignty certifications, sustainability disclosures, and AI-bias audits, reshaping RFP scoring in the outplacement services market.

Outplacement Industry Leaders

Randstad RiseSmart, Inc.

Lee Hecht Harrison LLC

Mercer (US) LLC

Career Partners International, LLC

Right Management Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sherpact launched enhanced digital outplacement tools featuring AI-driven career-transition capabilities that deliver placements twice as fast as conventional programs.

- March 2025: Allygatr purchased a minority stake in HR-tech start-up Senior Connect, broadening its workforce-transition technology suite.

- December 2024: LHH introduced Career Studio, a hybrid platform that marries human coaching with AI matching to streamline executive transitions.

- October 2024: Careerminds acquired Progression, a SaaS specialist in AI-based career frameworks, deepening its analytics stack.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the outplacement market as the fee-based programs that organizations buy to guide laid-off or redeployed employees into new roles, spanning career coaching, résumé optimization, interview preparation, networking tools, and digital job-search platforms. According to Mordor Intelligence, all delivery modes, onsite, virtual, and hybrid, plus individual, group, and executive packages are included.

Scope exclusion: Stand-alone recruiting, staffing, and unemployment insurance services sit outside this study.

Segmentation Overview

- By Service Type

- Individual Outplacement

- Group Outplacement

- Executive Outplacement

- By End-User

- Personal

- Enterprise

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Delivery Mode

- In-Person (Traditional)

- Virtual / Online

- Hybrid

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed HR leaders, career transition coaches, and platform providers across North America, Europe, and Asia Pacific. These discussions tested our desk findings, uncovered region-specific price spreads, and benchmarked digital platform uptake. Follow-up surveys with recently displaced professionals supplied conversion rate and average support duration metrics that desk sources lacked.

Desk Research

Our analysts first mapped the universe of demand using freely available labor statistics, such as U.S. BLS mass layoff filings, Eurostat dismissal data, and OECD unemployment duration series. Trade bodies, SHRM, CIPD, and the International Outplacement Alliance, helped us gauge program penetration and median contract fees. Regulatory texts, notably the EU Collective Redundancies Directive and state-level WARN notices, clarified compliance-driven adoption. Company filings, investor decks, and reputable press reports were mined to size vendor revenues, while D&B Hoovers and Dow Jones Factiva verified financial snapshots. This list is illustrative; many other public sources were tapped for validation and context.

Market-Sizing & Forecasting

A top-down model began with global layoff announcements, severance budget norms, and employer outplacement penetration to create the addressable spend pool, which was then cross-checked with sampled vendor revenues for a selective bottom-up sense check. Key variables like average contract fee per employee, share of virtual delivery, large enterprise downsizing cycles, unemployment duration, and HR outsourcing penetration drove annual values. Multivariate regression with scenario analysis projected 2025-2030 totals; anomalous outputs were iterated until expert consensus aligned.

Data Validation & Update Cycle

Outputs pass variance checks against independent labor indicators before senior review. Reports refresh yearly, and analysts trigger interim updates when major layoffs, regulatory shifts, or disruptive M&A materially alter assumptions.

Why Mordor's Outplacement Baseline Commands Confidence

Published figures differ because each publisher picks its own scope, base year, and data proxies.

Mordor's disciplined inclusion criteria, fresher refresh cadence, and mixed method cross-checks reduce blind spots that inflate or deflate peer numbers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.21 B (2025) | Mordor Intelligence | - |

| USD 4.89 B (2023) | Global Consultancy A | combines career transition fees with wider HR outsourcing and uses an older base year |

| USD 2.10 B (2023) | Trade Journal B | omits virtual only programs and most SME contracts |

| USD 5.00 B (2025) | Industry Analysis Firm C | extrapolates from per employee severance budgets in five countries only |

The comparison shows that scope drift, dated baselines, and narrow geographies shift totals noticeably, whereas Mordor's balanced model, anchored to global layoff data and validated revenue samples, gives decision makers a dependable starting point.

Key Questions Answered in the Report

What is the current size of the outplacement services market?

The outplacement services market is valued at USD 5.58 billion in 2026 and is set to reach USD 7.89 billion by 2031.

Which delivery mode is growing fastest within outplacement?

Virtual and online programs are scaling at a 13.65% CAGR, already holding 61.30% revenue share in 2025.

Why are executive outplacement services expanding so quickly?

Record C-suite turnover, confidentiality needs, and premium networking requirements are driving a 10.12% CAGR for executive packages.

How big is the opportunity in Asia Pacific?

Asia Pacific is the fastest-growing region, posting an 8.63% CAGR as Western-style workforce practices spread and layoffs rise in tech hubs.

What role does AI play in modern outplacement?

- AI-powered matching, résumé optimization, and adaptive coaching cut placement times by up to 50% and allow providers to serve global audiences at scale.

Are small and medium enterprises adopting outplacement services?

Yes. SME uptake is growing at 9.95% CAGR thanks to modular, cloud-based packages that lower cost and administrative overhead.

Page last updated on: