Commercial Vehicle Rental And Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

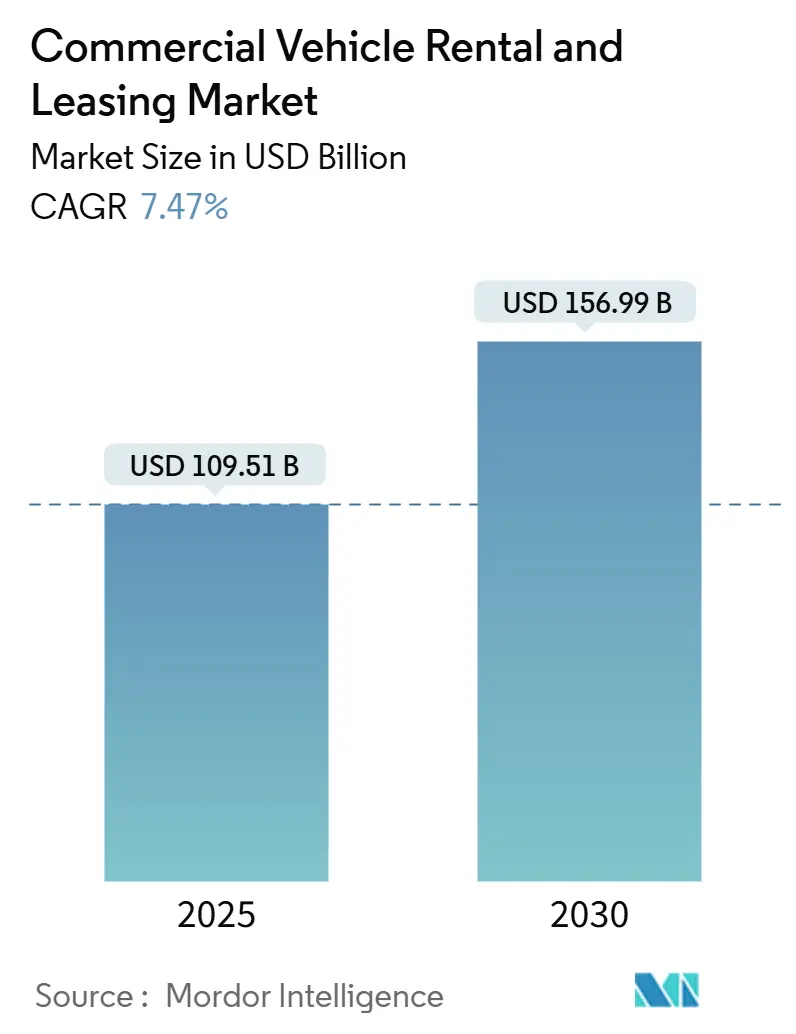

| Market Size (2025) | USD 109.51 Billion |

| Market Size (2030) | USD 156.99 Billion |

| Growth Rate (2025 - 2030) | 7.47% CAGR |

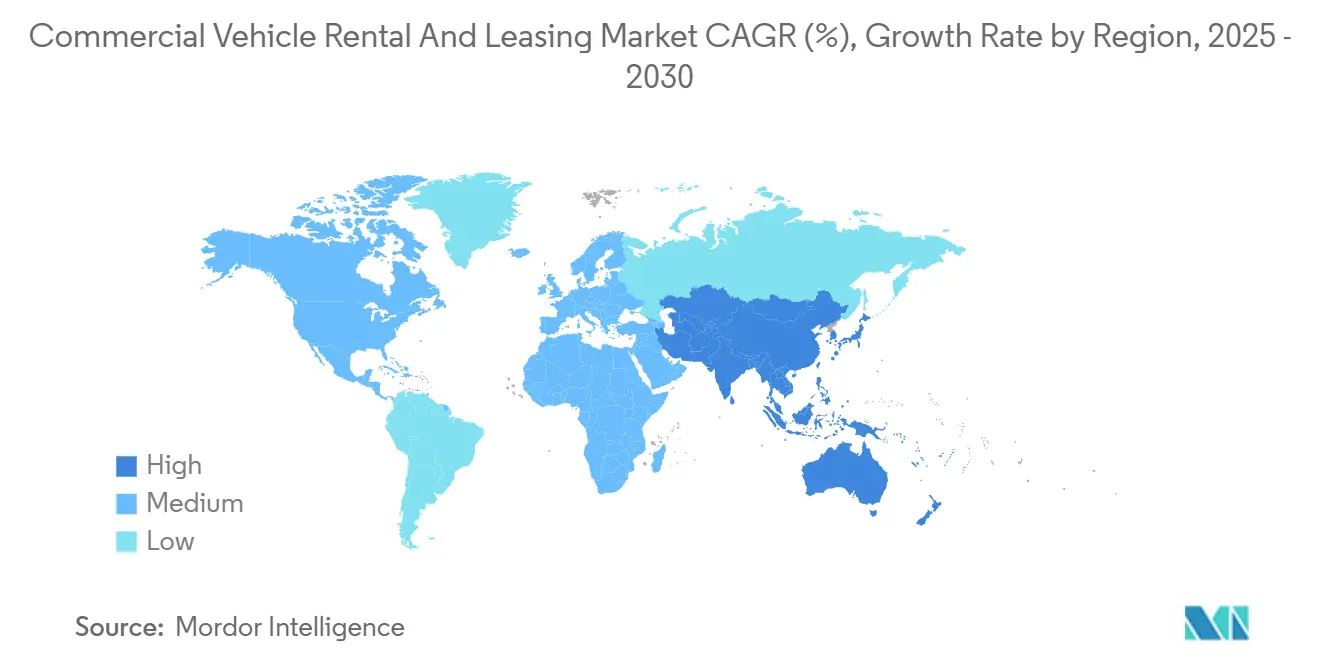

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

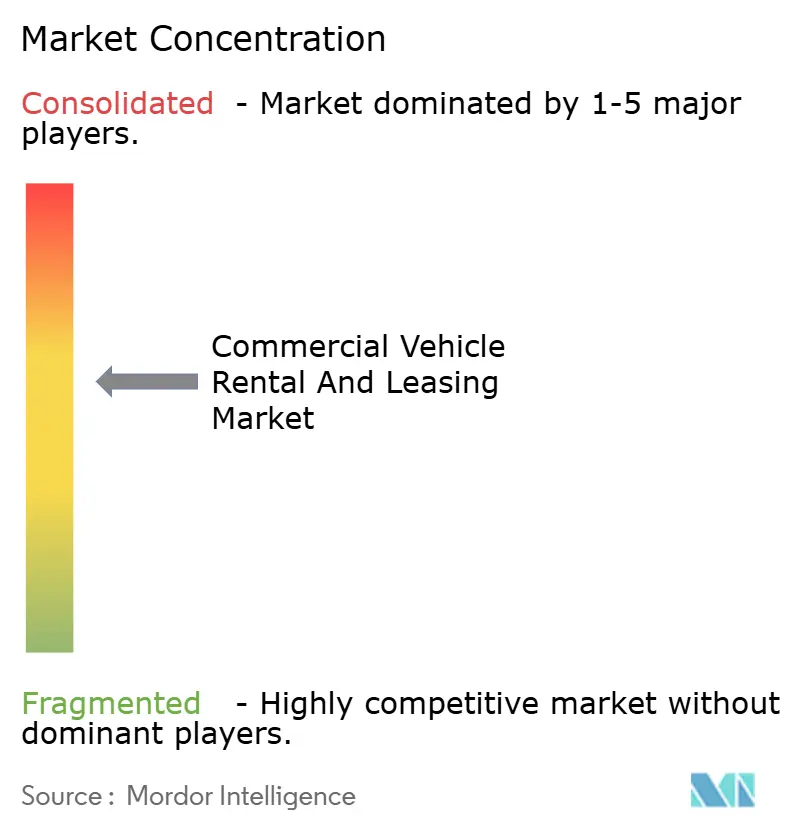

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Commercial Vehicle Rental And Leasing Market Analysis by Mordor Intelligence

The Commercial Vehicle Rental And Leasing Market size is estimated at USD 109.51 billion in 2025, and is expected to reach USD 156.99 billion by 2030, at a CAGR of 7.47% during the forecast period (2025-2030). Rising e-commerce volumes, tightening emission rules and the need to conserve cash in a high-interest-rate environment are accelerating the shift from outright ownership to flexible access models. Light commercial vehicles (LCVs) continue to anchor demand, while battery electric alternatives gain traction as regulators mandate lower fleet emissions. Incumbent lessors leverage nationwide workshop networks and telematics to optimize uptime, whereas emerging digital platforms compete on user-centric subscription experiences. Together, these factors reinforce a solid demand outlook for the commercial vehicle rental and leasing market through 2030.

Key Report Takeaways

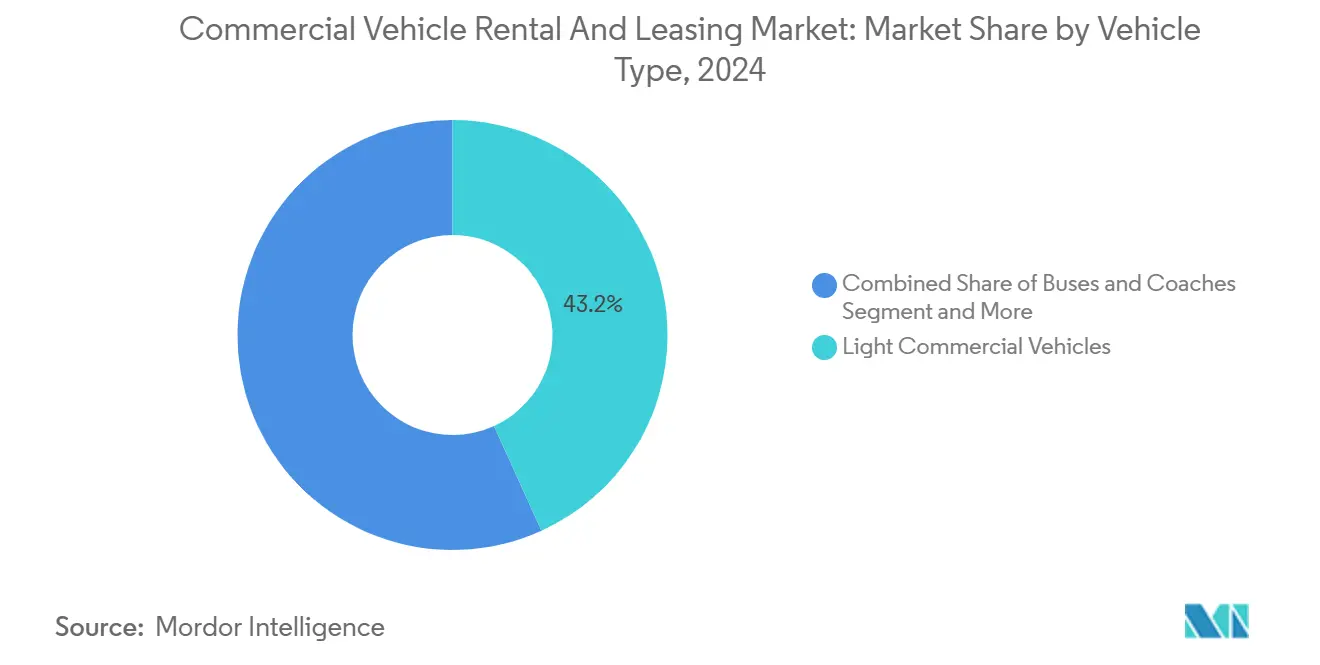

- By vehicle type, LCVs led with 43.18% commercial vehicle rental and leasing market share in 2024, and the segment is expanding at a 7.49% CAGR through 2030.

- By service type, long-term leasing held 54.31% of the commercial vehicle rental and leasing market in 2024, while short-term rental is advancing at a 7.53% CAGR through 2030.

- By application type, enterprise customers accounted for 67.83% of 2024 demand, yet personal leasing is forecast to grow at a 7.58% CAGR to 2030.

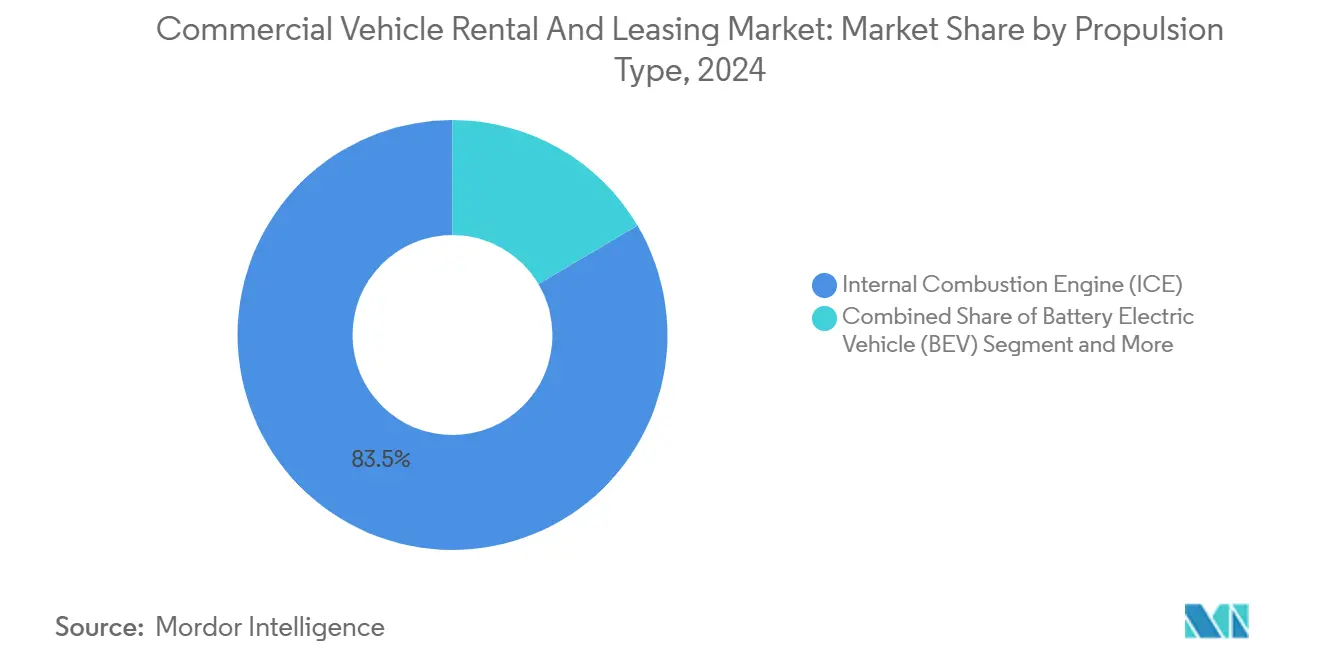

- By propulsion, internal combustion engines commanded 83.45% of 2024 revenue, but battery electric models are rising at a 7.52% CAGR on tightening emission standards.

- By end-use, logistics led with 38.91% share in 2024; e-commerce deliveries are the fastest-growing use case at a 7.57% CAGR.

- By geography, North America captured 38.77% of 2024 revenue; Asia-Pacific is the fastest-expanding region at a 7.55% CAGR on infrastructure upgrades and surging online retail.

Global Commercial Vehicle Rental And Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce-Fuelled Last-Mile Delivery Boom | +2.1% | Global, with concentration in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Cost-Efficiency Versus Ownership | +1.8% | North America and Europe primarily, spreading to emerging markets | Short term (≤ 2 years) |

| Emission-Compliance | +1.5% | Europe and California leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Logistics Outsourcing | +1.2% | Asia-Pacific core, spill-over to Latin America and MEA | Medium term (2-4 years) |

| Truck-As-A-Service Subscriptions | +0.9% | North America and Europe leading, expanding globally | Medium term (2-4 years) |

| Heavy E-Truck Battery-Swapping Ecosystems | +0.7% | China primarily, with potential expansion to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Fuelled Last-Mile Delivery Boom

In 2024, US online retail sales grew rapidly and accounted for nearly one-fifth of total retail spending. Surging parcel volumes push fleet utilization rates close to 88%, leaving operators short of peak-season capacity and reinforcing the appeal of on-demand rentals located near consumption centers. Same-day service expectations require geographically distributed pools of LCVs, and rental branches embedded in city fringes have seen double-digit rate increases as availability tightens. Flexible contracts enable logistics firms to right-size fleets without tying up capital for assets used only a fraction of the year. Consequently, the commercial vehicle rental and leasing market continues to benefit from the structural migration of retail sales to e-commerce ecosystems.

Cost-Efficiency Versus Ownership Under a High-Interest-Rate Cycle

Benchmark lending costs in the United States and Europe rose by more than 300 basis points between 2022 and 2024, lifting the effective rate on five-year truck loans to about 10% in early 2025[2]Federal Reserve Board, “Statistical Release: H.15 Selected Interest Rates,” federalreserve.gov. Higher debt service erodes the total-cost-of-ownership equation, nudging fleets toward leasing structures that roll maintenance, registration and tire expenses into predictable monthly fees. Repair bills rose nearly one-tenth over 2023–24, averaging USD 0.20 per mile, and operators increasingly shift maintenance risk to lessors through full-service agreements. Rental day rates also act as a real-time gauge of freight demand: Ryder's rental utilization historically leads broader freight indices by roughly three months, giving fleets a tactical hedge during demand inflections.

Emission-Compliance Mandates Driving Fleet Modernization

California’s Advanced Clean Fleets Rule requires 100% zero-emission drayage truck purchases by 2028, while revised European Union CO₂ standards mandate a one-tenth reduction in heavy-duty fleet emissions versus 2021 levels by 2025[3]European Commission, “Heavy-Duty Vehicles CO₂ Standards,” europa.eu . Compliance windows shorten traditional amortization timelines, making five-year ownership cycles risky for operators uncertain about future resale values. Leasing mitigates that exposure by shifting residual-value risk to specialized financiers who manage remarketing. Upfront incentives, charging grants and favorable depreciation schedules further narrow the cost gap between electric and diesel, especially in high-mileage urban delivery use cases where regenerative braking lowers per-mile energy spend. As a result, leasing firms accelerate bulk orders of battery electric trucks to satisfy impending customer demand.

Logistics Outsourcing in Emerging Markets

Developing economies embrace asset-light third-party logistics (3PL) models to fill infrastructure gaps and standardize service quality. India’s commercial vehicle market is forecast to climb exponentially by 2030, with leasing penetration rising in lockstep as local 3PLs eschew debt-funded purchases. International lessors provide capital, maintenance expertise and lifecycle management unavailable through fragmented banking channels. The resulting scale economies lower per-kilometer costs and enable emerging-market fleets to deploy newer, cleaner vehicles faster than under conventional ownership structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Residual-Value Risk | -1.4% | Global, particularly acute in EV segments | Long term (≥ 4 years) |

| Technician Shortages | -1.1% | North America and Europe primarily, spreading globally | Short term (≤ 2 years) |

| Battery-Value Uncertainty | -0.9% | Europe and North America leading EV adoption | Medium term (2-4 years) |

| Tighter Regulation Of Lease-Purchase Programmes | -0.7% | North America primarily, with regulatory spillover effects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Residual-Value Risk & Front-Loaded Capex

Used electric vans depreciated by about 60% between 2022 and mid-2025, prompting several European leasing groups to record impairment charges. Traditional residual algorithms built on diesel aging curves fail to capture technology step-changes, compelling lessors to shorten contract tenors or hike monthly rates. Upfront list prices for medium electric trucks often sit USD 100,000 above diesel equivalents, binding more capital and elevating balance-sheet leverage. The twin pressure of higher capex and uncertain resale proceeds is encouraging consolidation, joint-venture battery residual pools and usage-based contracts that share risk between lessor and lessee.

Battery-Value Uncertainty Dampening EV-Lease Economics

Telematics datasets indicate traction-battery modules typically retain four-fifth of capacity after 200,000 miles, yet market perception lags the evidence, depressing estimated resale values and elevating lease payments. Replacement packs for light-duty electric vans still cost USD 10,000–20,000, a figure that anchors risk adjusters’ worst-case scenarios. Pilot programs separating battery and chassis leases, alongside transparent battery health certificates, aim to narrow the information gap and improve bankability. However, standardized state-of-health protocols remain in draft form, delaying widespread adoption and tempering growth in the electric slice of the commercial vehicle rental and leasing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Light Commercial Vehicles Drive Urban Logistics Revolution

LCVs represented 43.18% of the commercial vehicle rental and leasing market in 2024 and are expanding at a 7.49% CAGR as package density inside metropolitan areas climbs. This segment’s commercial vehicle rental and leasing market size for LCVs is forecast to widen its lead through 2030, buoyed by e-grocery and quick-commerce demand surges. Leasing appeals because LCVs endure high stop-start cycles that accelerate wear and tear, making fixed-rate maintenance attractive. Meanwhile, the heavier truck category grows more slowly as long-haul carriers often retain ownership for tax depreciation.

Europe illustrates the LCV pivot: more than a million units were sold in 2024, with electric penetration reaching almost one-tenth as low-emission zones proliferated. Lessors pre-order battery electric vans to secure favorable allocation, allowing clients to trial zero-emission deliveries without balance-sheet strain. Over time, the share of electric in the commercial vehicle rental and leasing market size for LCVs could surpass three-fifth by 2032 if component costs continue to fall.

By Service Type: Short-Term Flexibility Gains Momentum

Long-term leases still account for 54.31% of 2024 revenue, cementing predictable fleet budgets for multiyear contracts. Yet short-term rental, growing at a 7.53% CAGR, captures incremental volume during holiday peaks, new-product launches and infrastructure projects. Enterprises increasingly mix modalities: a core long-term fleet covers baseline needs while on-demand rentals absorb volatility.

Subscription bundles further blur the line between rental and lease. Penske’s FlexFleet program combines daily or weekly access with telematics-based invoicing, lowering idle-time costs. Such pay-as-you-go structures particularly serve startups and 3PLs negotiating volatile freight rates. As inflation and interest-rate uncertainty persist, the commercial vehicle rental and leasing market will continue leaning toward shorter commitments aligned with revenue cycles.

By Application Type: Enterprise Dominance Faces Personal Market Disruption

Corporate accounts captured 67.83% of demand in 2024 due to scale purchasing, but the gig-economy wave is pushing personal leasing up at a 7.58% CAGR. Food-delivery drivers, event organizers and seasonal entrepreneurs value instant booking via mobile apps and the ability to return vehicles without penalties.

Shared-use platforms lower utilization friction by bundling insurance, maintenance and digital key handover. For lessors, the personal slice diversifies revenue and raises fleet turn rates, though it introduces credit-risk management challenges. Continual refinement of driver-scoring algorithms and over-the-air software locks help mitigate misuse and ensure asset security.

By Propulsion Type: Electric Transition Accelerates Despite ICE Dominance

Internal combustion powertrains still hold an 83.45% share because fueling infrastructure is universal and residual-value benchmarks mature. However, battery electric entries are growing at 7.52% CAGR, aided by urban noise limits and lower kilowatt-hour pricing. The United Kingdom’s congestion-charge exemptions illustrate how operating-cost math favors electric vans on high-density routes, tipping total-cost-of-ownership equations toward zero-emission units.

Plug-in hybrids and hydrogen fuel-cell trucks serve niche bridges where daily range exceeds 250 miles or payloads breach 15 tons. China’s battery-swap model decouples battery ownership, allowing 3-minute exchanges and stabilizing residual risk. If replicated elsewhere, this ecosystem could further expand the commercial vehicle rental and leasing market size for alternative powertrains.

By End-Use Industry: Logistics Leadership Faces E-Commerce Disruption

Traditional logistics controlled 38.91% of 2024 revenue, leveraging leasing to balance asset turns against stringent service-level agreements. Yet the e-commerce cohort, expanding at a 7.57% CAGR, is closing the gap as omnichannel retailers outsource last-mile execution. Micro-fulfillment centers situated inside city limits demand compact, maneuverable e-LCVs that can charge overnight on-site.

Construction, mining and utilities adopt rental to cover project-based spikes, limiting idle capital during downturns. Tourism operators favor seasonal buses and coaches, mitigating winter under-utilization. Emerging verticals—mobile healthcare, pop-up retail and cold-chain meal kits—represent small yet high-margin niches, underscoring the versatility of the commercial vehicle rental and leasing market.

Geography Analysis

North America held 38.77% of global revenue in 2024, underpinned by mature maintenance infrastructure and a robust e-commerce backbone. The United States accounts for more than four-fifths of regional demand; Ryder's dedicated contract revenue climbed one-tenth year-over-year in Q1 2025 as shippers opted for asset-light capacity[4]Ryder System Inc., "Q1 2025 Earnings Release," ryder.com . Canada complements with resource-sector heavy-haul rentals and cross-border trade corridors.

Asia-Pacific is the fastest-growing territory at a 7.55% CAGR. India's burgeoning 3PL sector and China's technology-enabled battery-swap depots exemplify the leapfrogging effect, where emerging markets bypass legacy ownership paradigms. Southeast Asian countries adopt subscription trucks to serve expanding grocery-delivery apps, underscoring the region's digital penchant.

Europe advances steadily on emissions regulation and consolidation. The European vehicle leasing market is expected to grow, supported by emissions regulation and consolidation. Germany's mature logistics networks and the United Kingdom's omnichannel retail pivot sustain branch-level rental demand. The integration of ALD Automotive and LeasePlan into Ayvens Group signals ongoing scale plays aimed at funding the electric transition.

Competitive Landscape

The commercial vehicle rental and leasing market exhibits moderate concentration. Top players—Ryder System, Penske Truck Leasing and Enterprise Holdings—capitalize on national service centers, proprietary telematics and bulk procurement to maintain pricing power. Middle-tier challengers focus on specialized niches such as refrigerated vans, electric minibuses or cross-border paperwork facilitation.

Technology integration underscores competitive strategy. Predictive maintenance algorithms flag faults before roadside failures, boosting uptime and customer satisfaction. Block-hour telematics packages allow customers to optimize dispatch planning, reducing fuel burn. Penske’s collaboration with REE Automotive brings drive-by-wire electric trucks into its rental pool, offering clients early access to disruptive technologies.

Acquisition‐led growth persists: Ryder’s purchase of Cardinal Logistics extended its e-commerce fulfillment footprint and deepened dedicated contract carriage capabilities. Private-equity investors increasingly accumulate regional independents, betting on back-office synergies and digitization to lift margins. Meanwhile, digital natives deploy app-only interfaces, dynamic pricing and cashless key handover to court micro-businesses and individual entrepreneurs, gradually expanding addressable volume.

Commercial Vehicle Rental And Leasing Industry Leaders

-

Ryder System, Inc.

-

Penske Truck Leasing

-

LeasePlan Corporation N.V.

-

Sixt SE

-

Enterprise Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Ryder acquired a 35% stake in Pit Stop Fleet Service to enhance in-house maintenance capacity.

- May 2024: Penske Truck Leasing partnered with REE Automotive to offer P7-C electric trucks for North American demonstrations and customer pilots.

- February 2024: Ryder purchased Cardinal Logistics for USD 302 million, adding middle-mile and e-commerce fulfillment assets.

Global Commercial Vehicle Rental And Leasing Market Report Scope

| Light Commercial Vehicles (LCVs) |

| Medium & Heavy-Duty Trucks |

| Buses & Coaches |

| Short-Term Rental |

| Long-Term Leasing |

| Enterprise Leasing |

| Personal Leasing |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Logistics |

| Construction |

| Mining |

| Tourism |

| E-Commerce |

| Event Management |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Light Commercial Vehicles (LCVs) | |

| Medium & Heavy-Duty Trucks | ||

| Buses & Coaches | ||

| By Service Type | Short-Term Rental | |

| Long-Term Leasing | ||

| By Application Type | Enterprise Leasing | |

| Personal Leasing | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By End-Use Industry | Logistics | |

| Construction | ||

| Mining | ||

| Tourism | ||

| E-Commerce | ||

| Event Management | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the commercial vehicle rental and leasing market by 2030?

The market is forecast to reach USD 156.99 billion by 2030, reflecting a 7.47% CAGR from its 2025 base.

Which vehicle type will generate the most incremental revenue through 2030?

Light commercial vehicles, already leading in 2024, are growing at 7.49% CAGR as last-mile demand accelerates.

How fast is the Asia-Pacific region expanding?

Asia-Pacific is advancing at a 7.55% CAGR, the highest regional pace, on infrastructure upgrades and online retail growth.

Why are short-term rentals gaining ground versus long-term leases?

Elevated interest rates and seasonal demand volatility prompt fleets to favor flexible, pay-as-you-go rental contracts.

What drives electric vehicle adoption in commercial fleets?

Tightening emission mandates, urban low-emission zones and falling battery costs push fleets toward battery electric models.

Which recent deal illustrates market consolidation?

Ryder’s USD 302 million acquisition of Cardinal Logistics in Feb 2024 expanded its e-commerce fulfillment capabilities.

Page last updated on: