Truck Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 108.65 Billion |

| Market Size (2030) | USD 140.13 Billion |

| Growth Rate (2025 - 2030) | 5.22% CAGR |

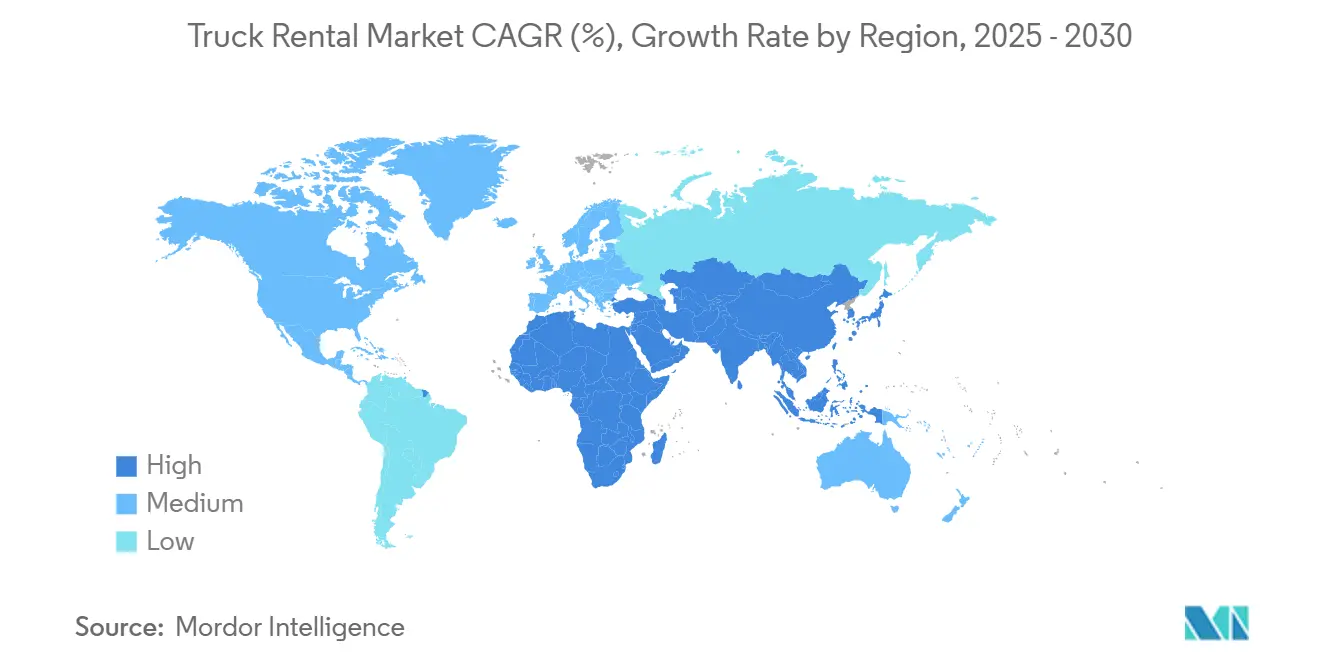

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Truck Rental Market Analysis by Mordor Intelligence

The truck rental market size stands at USD 108.65 billion in 2025 and is forecast to reach USD 140.13 billion by 2030, advancing at a 5.22% CAGR. Sustained e-commerce growth, public-sector infrastructure spending, and flexible fleet management preferences keep demand resilient despite macroeconomic uncertainty. Ongoing digital platform penetration lowers transaction friction, expands customer reach, and lifts fleet-utilization levels. Meanwhile, tighter borrowing conditions reinforce the appeal of rental over ownership by stabilizing operating costs and preserving capital. Intensifying corporate sustainability mandates also push operators to pilot zero-emission trucks, opening a fresh revenue stream even as internal-combustion vehicles remain dominant.

Key Report Takeaways

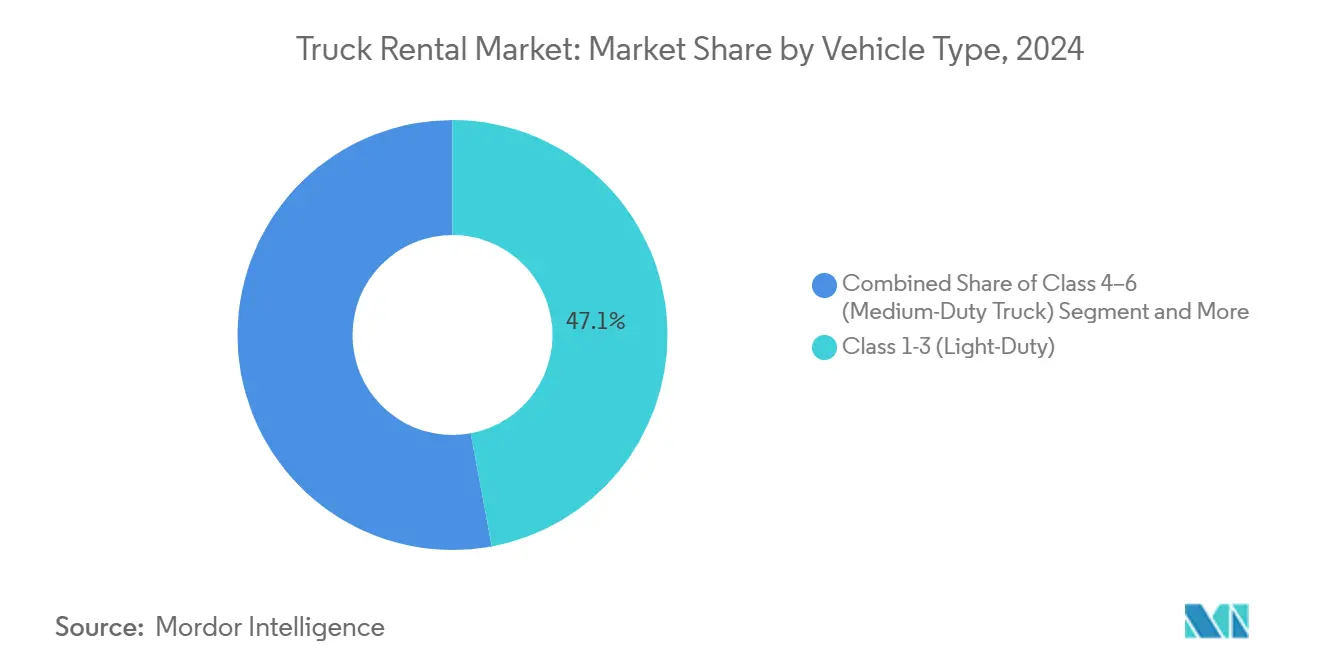

- By vehicle type, Class 1–3 light-duty trucks held 47.08% of the truck rental market share in 2024, and are projected to post the fastest 9.79% CAGR to 2030.

- By propulsion type, internal-combustion units captured 98.25% of the truck rental market size in 2024, while electric trucks are poised for the highest 17.01% CAGR through 2030.

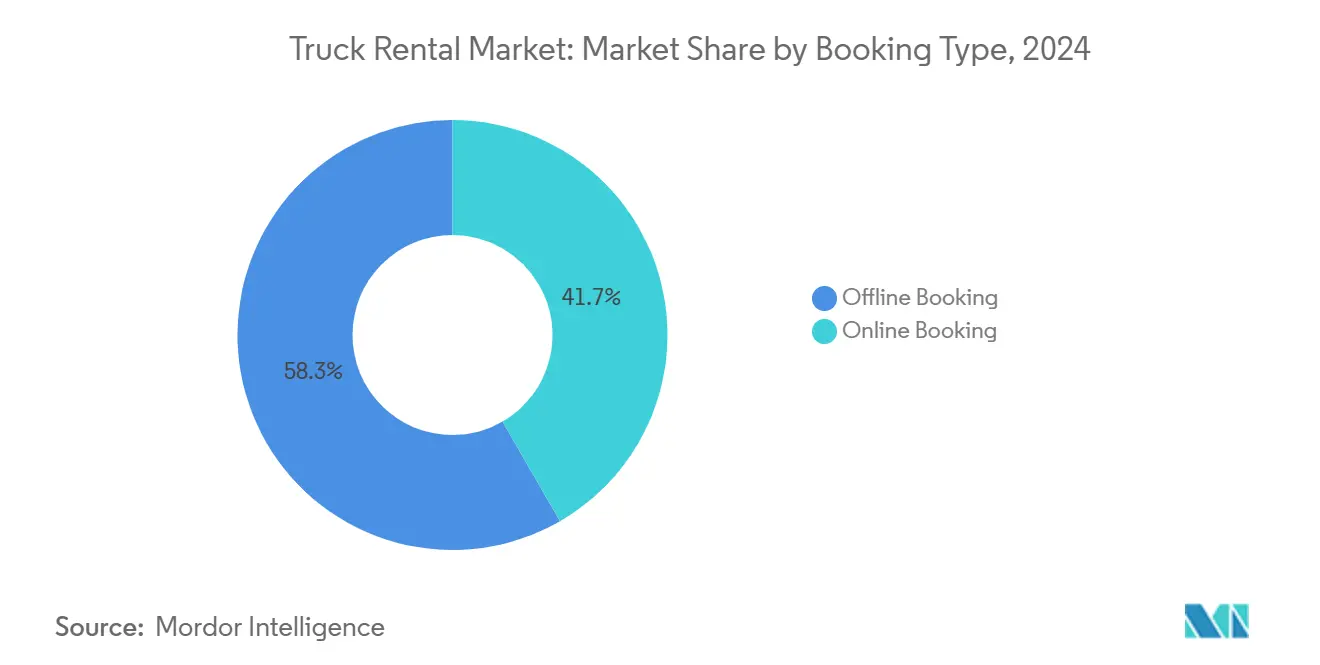

- By booking type, offline channels commanded 58.33% of the truck rental market size in 2024; Online channels are expanding at a 10.78% CAGR through 2030.

- By rental type, short-term leasing accounted for 65.50% of the truck rental market share in 2024, while long-term leasing is expected to rise at an 8.39% CAGR between 2025 and 2030.

- By geography, North America held 41.96% of the truck rental market share in 2024; Asia-Pacific is projected to be the fastest-growing region at a 7.57% CAGR by 2030.

Market Trends and Insights

Drivers Impact Analysis of Truck Rental Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Parcel Volumes | +0.8% | Global, concentrated in North America & APAC | Short term (≤ 2 years) |

| Construction Boom | +0.6% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Volatile Interest Rates | +0.5% | Global, particularly North America & Europe | Short term (≤ 2 years) |

| Digital Truck-Rental Platforms | +0.4% | Global, early adoption in North America | Medium term (2-4 years) |

| ESG-Driven Zero-Emission Trials | +0.3% | North America & EU regulatory zones | Long term (≥ 4 years) |

| Free-Trade-Zone Trailer-Swap | +0.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive E-Commerce Parcel Volumes

Surging digital commerce replaces bulk consignments with high-frequency small-parcel flows that strain fixed fleets. During peak seasons, fulfillment centers see rental demand exceed permanent capacity significantly, driving short-term contracts that boost the truck rental market[1] Amazon, “Annual Report 2024,” AMAZON.COM. Rental pricing engines now track parcel-volume indices in real time and shift assets into hot spots before capacity bottlenecks form. Small businesses enjoy the same agility, tapping rentals to satisfy flash sales without draining working capital. As a result, holiday surcharges and surge-pricing windows are becoming a larger share of annual revenue, helping operators offset rising labor and maintenance expenses.

Infrastructure-Led Construction Boom

Massive public spending programs schedule multi-year work that contractors prefer to service with rented trucks rather than owned fleets. Heavy civil, renewable-energy, and urban-revitalization projects create localized spikes that well-positioned fleets convert into near-full utilization. Rental contracts avoid idle-equipment costs once a job ends, preserving contractor liquidity for the next bid cycle. Operators, meanwhile, sharpen project-based pricing models to capture premium margins on specialty units such as dump trucks and concrete agitators. These mutually reinforcing dynamics steadily widen the addressable base for the truck rental market over the forecast horizon.

Volatile Interest Rates Favor Rental

Commercial-vehicle loan rates between 6% and 12% leave many small enterprises unable to forecast total ownership cost confidently [2]Board of Governors of the Federal Reserve System (US), "Finance Rate on Consumer Installment Loans at Commercial Banks, New Autos 48 Month Loan", fred.stlouisfed.org. Rentals fix cash outflows into predictable operating expenses and eliminate balloon payments that can breach bank covenants when borrowing costs spike. Accounting treatment keeps rentals off the balance sheet, protecting debt-to-equity ratios and freeing credit lines for core investments. Operators exploit this environment by rolling out subscription plans that bundle maintenance, insurance, and telematics for a single monthly fee. The wider adoption of such plans cements rentals as a hedge against monetary-policy uncertainty.

Expansion of Digital Truck-Rental Platforms

Marketplace apps such as Fluid Truck and TruckSmarter are turning fragmented truck supply into a searchable, on-demand network. Instant ID verification, integrated insurance and automated billing shrink booking time from hours to minutes, attracting digitally native merchants and gig-economy drivers. Telematics feeds give customers live location, fuel and safety data, raising transparency and trust levels seldom matched by legacy counter-based models. As platform density grows, network effects lower customer-acquisition cost and lift asset-utilization rates, reinforcing competitive moats for early movers. Established rental brands respond by white-labeling their fleets on these portals, signaling that platform participation is evolving from optional to mandatory for market relevance.

Restraints Impact Analysis of Truck Rental Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Driver Shortages | -0.5% | Global, severe in North America | Short term (≤ 2 years) |

| Financing & Insurance Costs | -0.4% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Urban Grid Limits | -0.3% | North America & EU urban centers | Long term (≥ 4 years) |

| Accident-Litigation Expenses | -0.2% | North America regulatory environment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Driver Shortages

High annual turnover, often above 85%, forces rental firms to pour money into sign-on bonuses, training programs, and retention incentives. Capacity shortages are especially acute for Class 8 rentals, where a commercial driver’s license and stricter safety rules limit the labor pool. Some operators partner with staffing agencies or bundle driver services within rental contracts, but these solutions inflate operating complexity and cost. Persistent demographic headwinds, therefore, cap fleet-deployment potential even when physical trucks are available.

Elevated Financing & Insurance Costs

“Nuclear verdicts” increase liability premiums by around 35–40% annually for small fleets, eroding rental-operator margins. Rising interest rates pile on extra pressure, lifting equipment-loan coupons 200–400 basis points above pre-pandemic norms. Insurers and lenders tighten underwriting standards, demanding stronger safety records and higher down payments that many new entrants cannot meet. Capital-rich incumbents leverage their balance-sheet strength to secure bulk-purchase discounts and lower insurance deductibles, widening the moat against smaller rivals. Collectively, expensive risk capital slows fleet expansion and keeps rental rates elevated, dampening demand among price-sensitive customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Truck Rental Market Segment Analysis

By Vehicle Type:

Light-Duty Trucks Sustain MomentumClass 1–3 models accounted for 47.08% of the truck rental market size in 2024, with a 9.79% CAGR through 2030. Urban delivery patterns favor their maneuverability and lower licensing thresholds, allowing retailers and gig drivers to cover dense routes efficiently. Digital platforms route same-day orders across dispersed micro-fleet operators, boosting short-duration rentals that keep utilization high. Medium-duty trucks maintain relevance for food, utility, and mid-haul distribution, offering balanced payload and fuel economy. Heavy-duty segments experience episodic demand from infrastructure projects but wrestle with stricter licensing and safety compliance, dampening growth relative to lighter classes.

Broader adoption of telematics and predictive maintenance extends service intervals for light units, reducing downtime and maximizing availability. Lower upfront cost and fuel savings make light trucks attractive entry points for emerging markets chasing e-commerce. Medium-duty fleets embrace alternative fuel retrofits but face route-planning challenges. Heavy-duty operators pursue specialized vocational applications to mitigate driver scarcity. As a result, light-duty dominance is expected to widen, reinforcing value creation in the truck rental market.

By Propulsion Type:

Electric Adoption AcceleratesInternal-combustion vehicles represented 98.25% of the truck rental market share in 2024, yet electric trucks are projected to advance at a 17.01% CAGR to 2030. Battery electric vans already prove viable in last-mile routes under 150 miles, aligning with corporate ESG goals. Federal incentives narrow the total-cost-of-ownership gap, while declining battery prices enhance asset residual values. Operators pilot depot-charging hubs in urban corridors, bundling charging services with rental contracts to lock in recurring revenue.

Nevertheless, range limitations and grid bottlenecks slow adoption in heavier classes. Fleet managers hedge by integrating electric units alongside diesel to match route profiles, tempering the pace of displacement. Innovations in solid-state batteries may broaden viable duty cycles post-2030, but interim momentum remains concentrated in light-duty fleets. The dual-track strategy allows the truck rental market to capture emerging demand without jeopardizing utilization of core combustion fleets.

By Booking Type:

Digital Channels Gain ScaleOffline arrangements still generated 58.33% of the truck rental market size in 2024 as enterprise customers value personalized account management and complex contract structuring. Yet online bookings are growing at 10.78% CAGR, propelled by intuitive mobile apps and instant insurance verification. Self-service interfaces resonate with younger decision-makers tasked with fast procurement, driving higher conversion rates for short-term rentals and small-volume corporate accounts.

Marketplace algorithms enhance price transparency and route matching, reducing idle time for fleets and simplifying pick-up logistics. Established operators revamp legacy systems with cloud APIs to integrate with third-party logistics platforms. While paper-based processes linger for specialized vehicles that need custom up-fits, digitization is expected to surpass parity with offline bookings during the forecast period, further professionalizing the truck rental market.

By Rental Type:

Short-Term Flexibility PrevailsIn 2024, short-term leasing dominates the truck rental market with a 65.50% share, driven by businesses prioritizing flexibility and capital efficiency. This model is especially attractive to companies with seasonal operations, project-based needs, or uncertain growth paths, where long-term commitments may pose financial risks. Improved fleet availability and competitive pricing have made short-term leasing a viable alternative to ownership, offering access without asset management burden. As a result, many businesses are opting for short-term arrangements to stay agile in a rapidly evolving market.

Meanwhile, long-term leasing is gaining traction, growing at a steady 8.39% CAGR through 2030, as companies seek predictable costs and guaranteed vehicle access. This shift reflects a broader move toward service-based fleet management, where maintenance, insurance, and depreciation risks are transferred to rental providers. Industries like logistics and professional services often prefer long-term leases for their stability and bundled service offerings. Digital platforms are playing a key role in streamlining both short- and long-term rentals, though long-term agreements typically involve more customization and negotiation. Together, these trends highlight a maturing market that caters to diverse business needs through flexible leasing models.

Geography Analysis

North America Truck Rental Market

North America controlled 41.96% of the truck rental market in 2024 and is projected to post a 5.65% CAGR to 2030. The United States benefits from dense interstate networks, mature e-commerce ecosystems, and a rental-friendly business culture that values off-balance-sheet mobility solutions. Canada adds energy-sector and cross-border trade demand, and regulatory harmonization simplifies fleet redeployment across provincial lines. Digital integration between dispatch, fuel, and telematics providers raises utilization for major operators, while driver supply constraints and rising insurance premiums weigh on capacity.

APAC Truck Rental Market

Asia-Pacific is forecast to achieve the fastest 7.57% CAGR through 2030. China’s Belt and Road infrastructure projects and vibrant domestic e-commerce drive heavy light-duty uptake, while India’s highway upgrades and organized retail growth broaden the addressable base. Fragmented regulations across Southeast Asia complicate cross-border fleet pooling, yet lifting trade volumes and free-trade-zone expansions underpin demand for trailer swaps. South Korea and Japan contribute stable manufacturing and port logistics volumes, deepening the region’s strategic importance for the truck rental market.

Europe Truck Rental Market

Europe will progress at a 5.51% CAGR to 2030 on the back of environmental policy harmonization and resilient cross-border goods flows. Germany anchors demand with automotive supply chains and logistics hubs, whereas the United Kingdom adapts to post-Brexit route realignment and domestic delivery reconfiguration. Stringent emissions targets accelerate electrification pilots, prompting rental operators to diversify fleets. Meanwhile, varied national tax regimes and urban access regulations require operators to tailor offerings by country, adding complexity yet opening localized niches within the truck rental market. Overall, the continent balances mature infrastructure with shifting regulatory landscapes that reward agile, technology-driven rental strategies.

Competitive Landscape

The truck rental market exhibits moderate concentration with fragmented characteristics, as top-5 players control less than half the combined market share, while numerous regional and specialized operators serve local markets and niche applications. Fragmentation fosters acquisition prospects, especially in trailer leasing, where economies of scale magnify purchasing power and residual-value management. Leading firms differentiate through national coverage, asset diversity, and integrated logistics services that extend beyond core vehicle rental.

Strategic themes include geographic infill, fleet electrification, and digital customer engagement. Operators invest in data analytics to optimize dispatch and predictive maintenance, boosting uptime and cutting total operating cost. Technology partnerships with telematics, fuel, and payment providers deepen client stickiness. Fleet electrification strategies emphasize light-duty units in urban settings, limiting range risk while capturing ESG-oriented demand.

Private-equity interest intensifies as recurring revenue, tangible asset backing, and consolidation headroom align with buy-and-build playbooks. Mid-tier operators seek scale through mergers to negotiate better fleet-procurement pricing and harmonize back-office systems. Competitive intensity remains moderate: barriers include capital requirements, geographic network effects and regulatory complexity. Over the forecast horizon, sustained digital adoption and rising compliance costs are expected to lift the competitive bar, spurring further consolidation but also nurturing tech-enabled newcomers that focus on niche segments within the truck rental market.

Truck Rental Industry Leaders

-

Ryder System Inc.

-

Penske Truck Leasing

-

Enterprise Truck Rental

-

U-Haul International

-

Sixt SE (Sixt Rent a Truck)

- *Disclaimer: Major Players sorted in no particular order

Truck Rental Market Companies Covered in this Report

- Ryder System Inc.

- Penske Truck Leasing

- Enterprise Truck Rental

- U-Haul International

- Budget Truck Rental (Avis Budget Group)

- Sixt SE (Sixt Rent a Truck)

- Europcar Mobility Group

- Fraikin Group

- TIP Trailer Services

- PACLease (PACCAR Leasing)

- Idealease Inc.

- Rush Enterprises (Rush Truck Leasing)

- LeasePlan Corporation N.V.

- TR Group

- Hertz Truck Rental

- Home Depot Rental

- Velocity Truck Rental & Leasing

- Hylane

- United Rentals (truck segment)

- Ashtead Group (Sunbelt Rentals)

- COOP by Ryder

Recent Industry Developments in Truck Rental Market

- June 2025: German mobility provider Hylane GmbH established a Dutch subsidiary to offer usage-based rentals of battery and hydrogen trucks in the Netherlands.

- April 2025: Penske Truck Leasing opened a full-service facility in Ocala, Florida, providing consumer and commercial rental, long-term leasing, and maintenance services.

- September 2024: Velocity Truck Rental & Leasing and energy advisory firm Trio deployed 47 high-power charging stations across Southern California to support electric truck rentals.

Global Truck Rental Market Report Scope

Segmentation Overview

| Class 1–3 (Light-Duty Trucks) |

| Class 4–6 (Medium-Duty Trucks) |

| Class 7–8 (Heavy-Duty Trucks) |

| Internal Combustion Engine (ICE) |

| Electric |

| Offline Booking |

| Online Booking |

| Short-term Leasing |

| Long-term Leasing |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Class 1–3 (Light-Duty Trucks) | |

| Class 4–6 (Medium-Duty Trucks) | ||

| Class 7–8 (Heavy-Duty Trucks) | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Electric | ||

| By Booking Type | Offline Booking | |

| Online Booking | ||

| By Rental Type | Short-term Leasing | |

| Long-term Leasing | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the truck rental market in 2025?

The truck rental market size is USD 108.65 billion in 2025.

How fast is the truck rental market expected to grow?

It is forecast to expand at a 5.22% CAGR from 2025 to 2030, reaching USD 140.13 billion.

Which vehicle class leads demand in truck rentals?

Class 1–3 light-duty trucks lead with 47.08% share and the highest 9.79% CAGR.

Why are businesses favoring rentals over ownership?

High interest rates, flexible contracts and off-balance-sheet treatment make rentals more attractive than financing purchases.

Which region is growing the fastest?

Asia-Pacific shows the fastest growth at a 7.57% CAGR, driven by infrastructure expansion and e-commerce.

What role do digital platforms play in the sector?

Online marketplaces streamline booking, boost fleet utilization and are growing at a 10.78% CAGR, reshaping customer acquisition.

Page last updated on: