Electric Vehicle Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

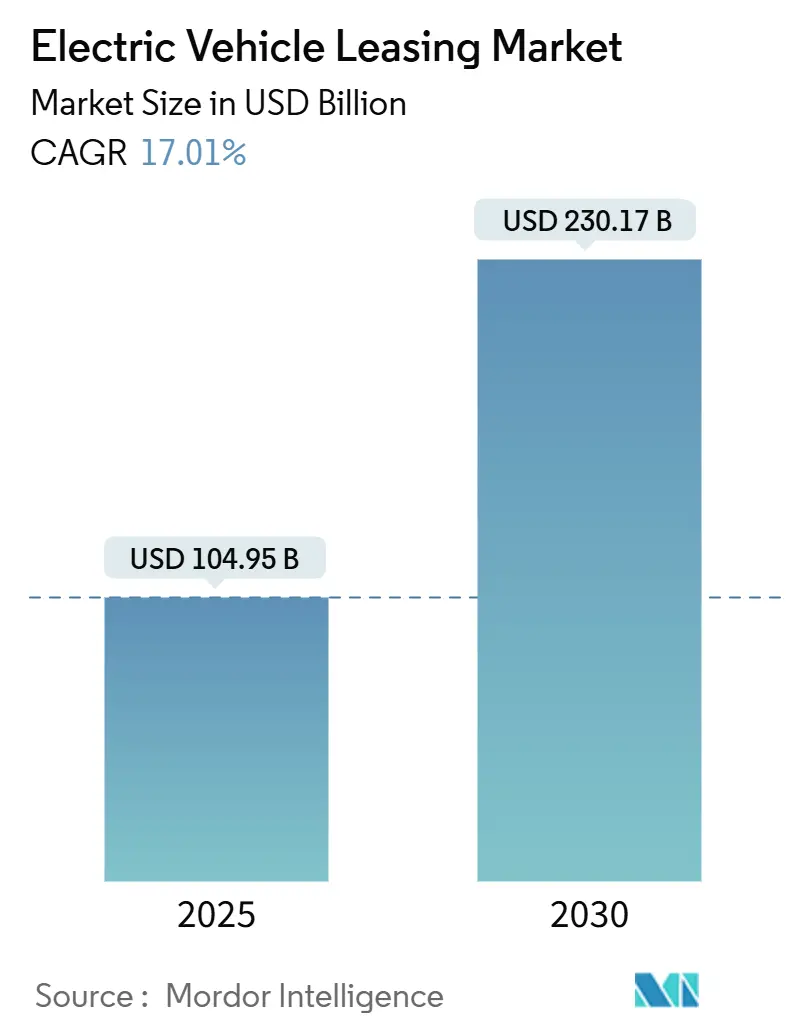

| Market Size (2025) | USD 104.95 Billion |

| Market Size (2030) | USD 230.17 Billion |

| Growth Rate (2025 - 2030) | 17.01% CAGR |

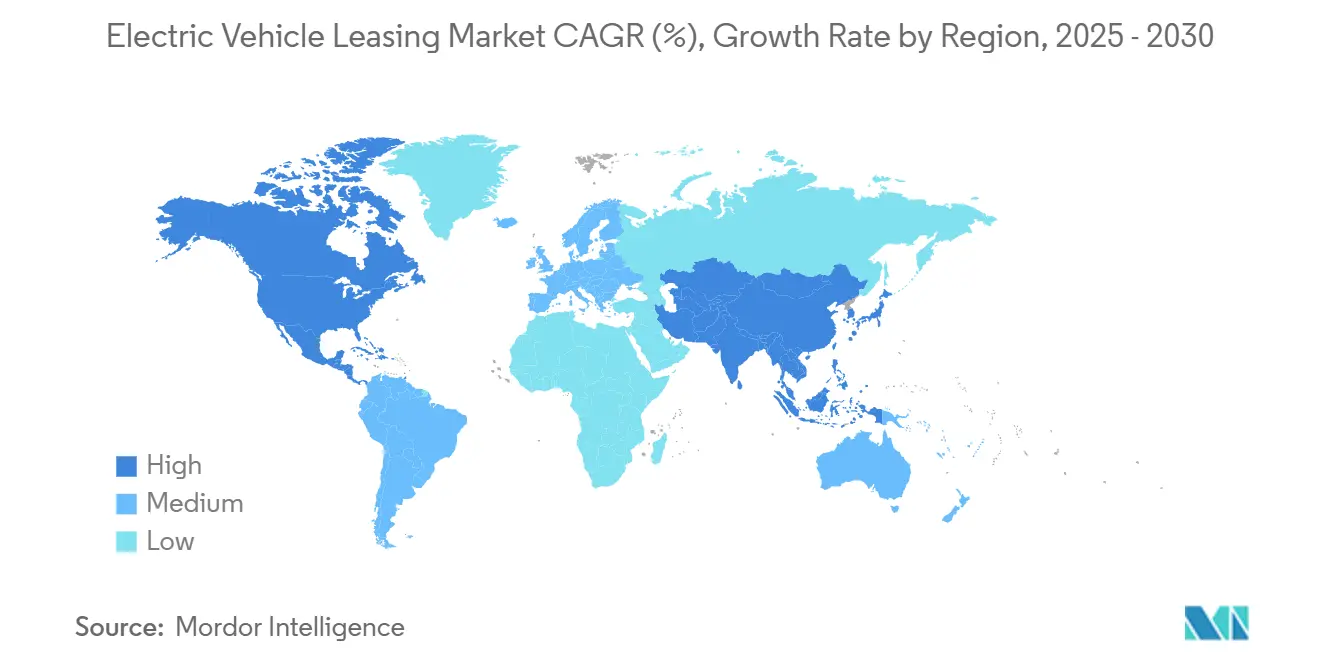

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

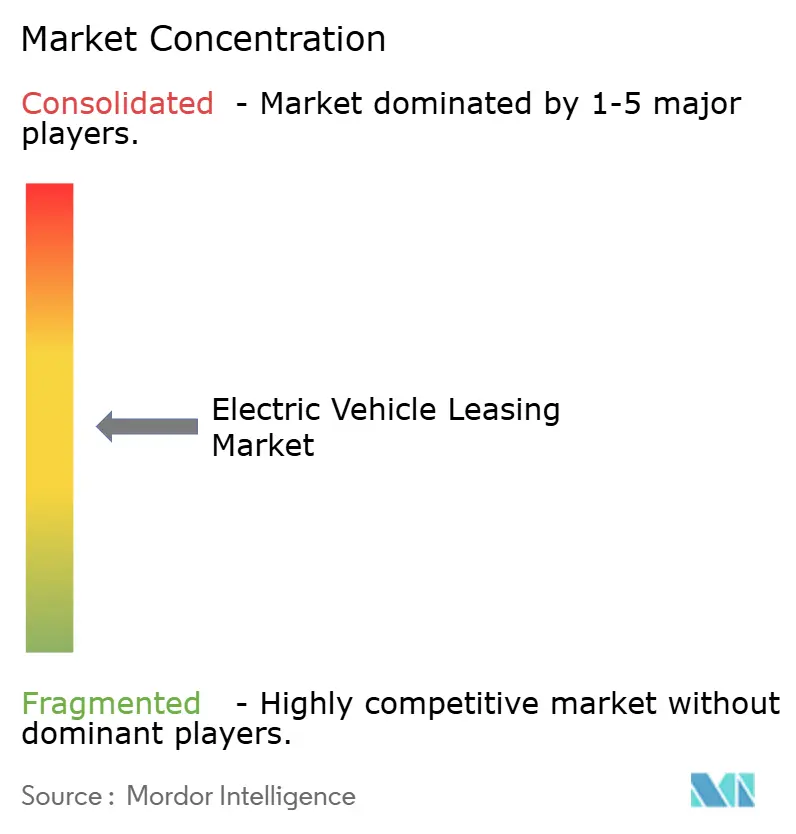

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Leasing Market Analysis by Mordor Intelligence

The electric vehicle leasing market size stood at USD 104.95 billion in 2025 and is forecast to expand to USD 230.17 billion by 2030, delivering a 17.01% CAGR over the period. Government tax credits, tightening emissions regulations, and battery-technology gains give leasing a clear cost and flexibility edge over outright purchase, pushing lease penetration above 50% of new EV transactions in 2025. Corporate fleet electrification, led by mandatory zero-emission procurement rules, is enlarging bulk-lease volumes and pressuring lessors to integrate charging and analytics services. Model-line proliferation, especially from Chinese manufacturers, is widening price bands so that lease offers now range from entry-level urban hatchbacks to USD 999-per-month electric pickups, amplifying consumer reach. Rising central-bank rates channel more buyers toward leases because monthly payments absorb less of the interest-rate spike than conventional loans, while AI-enabled battery health tools protect residual values and let lessors quote more competitive terms.

Key Report Takeaways

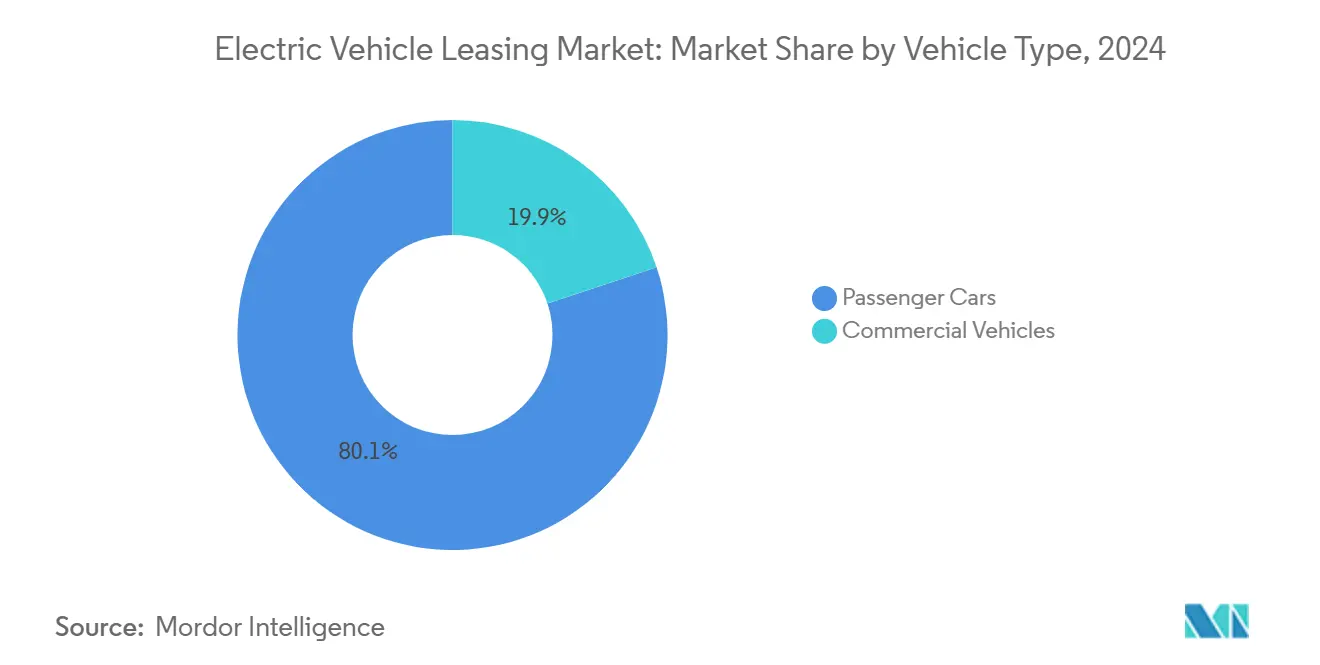

- By vehicle type, passenger cars accounted for 80.13% share of the electric vehicle leasing market size in 2024, while commercial vehicles are projected to grow at a 18.24% CAGR through 2030.

- By propulsion, battery electric vehicles accounted for 72.56% share of the electric vehicle leasing market size in 2024 and are advancing at a 19.66% CAGR through 2030.

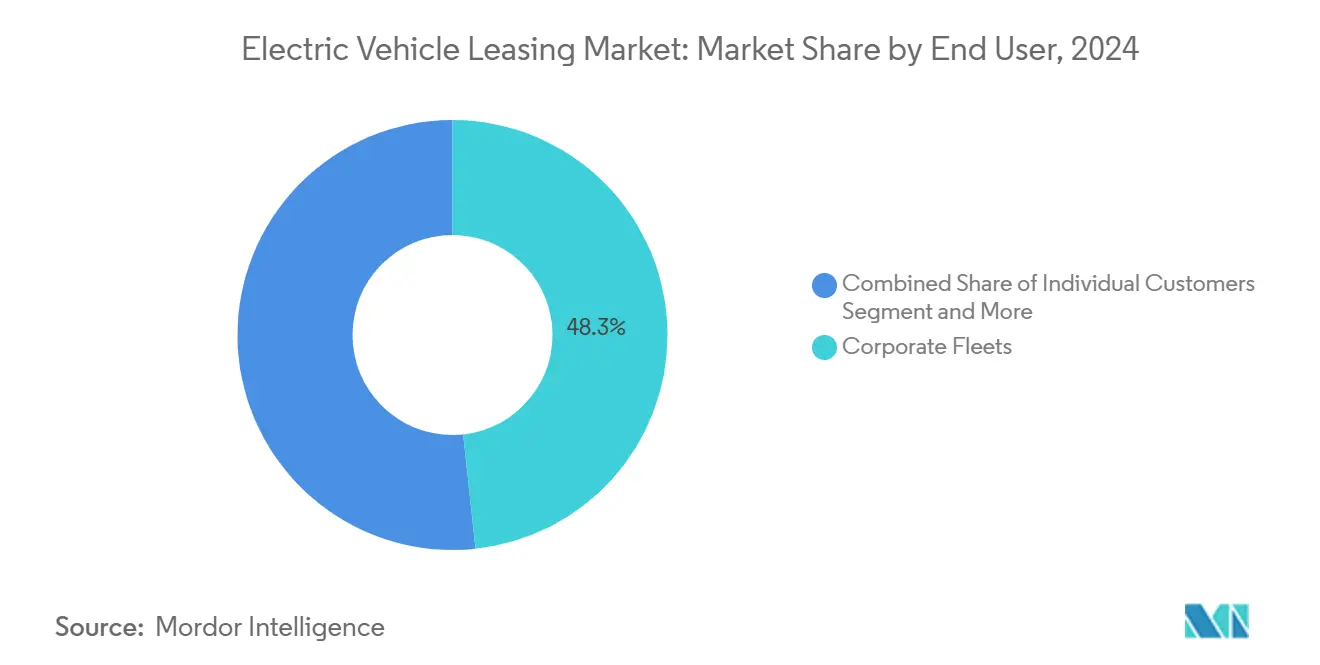

- By end user, corporate fleets commanded 48.25% of the electric vehicle leasing market size in 2024, while ride-sharing and delivery platforms recorded the highest 19.14% CAGR to 2030.

- By duration, mid-term contracts (1-3 years) held 56.81% share in 2024; short-term leases (less than 12 months) are forecast to expand at an 18.76% CAGR.

- By geography, Europe retained 43.66% electric vehicle leasing market share in 2024, whereas Asia-Pacific is set to grow at a 17.85% CAGR through 2030.

Global Electric Vehicle Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability Drives Fleet Electrification | +4.1% | North America and EU | Medium term (2-4 years) |

| Government Incentives Favor EV Leasing | +3.2% | North America and EU | Short term (≤ 2 years) |

| Declining Battery Costs Improving Residual Values | +2.9% | Global, supply-chain strength in China | Long term (≥ 4 years) |

| EV Variety Reduces Entry Barrier | +2.8% | Global, faster in Asia Pacific | Medium term (2-4 years) |

| Micro-Lease Platforms Expand EV Access | +1.7% | Urban centers worldwide, early adoption in North America | Short term (≤ 2 years) |

| AI Battery Analytics Lowers Residual-value Risk | +1.4% | North America and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate Sustainability Mandates Electrify Fleets

Executive-branch orders require U.S. federal agencies to shift 100% of new light-duty acquisitions to zero-emission vehicles by 2027, translating into roughly 650,000 incremental lease opportunities [1]U.S. White House, “Federal Sustainability Plan Targets Zero-Emission Vehicle Acquisitions,” whitehouse.gov. Private-sector firms mirror the push: Amazon remains on track for 100,000 Rivian electric vans by 2030, using operating leases to preserve capital and hedge residual values. Public companies increasingly report scope-1 fleet emissions under ESG frameworks, and leasing offers a rapid compliance route because vehicles can be rotated every two years to meet newer regulatory thresholds. Leasing firms respond by bundling charging management, telematics, and carbon-report dashboards so that fleet managers secure full-service packages under one contract. As mandates tighten globally, fleet electrification keeps injecting multi-thousand-unit tranches into the electric vehicle leasing market every quarter.

Government Incentives and Tax Credits Favor Leasing

Federal legislation classifies leased EVs as commercial vehicles, allowing lessors to capture the full USD 7,500 credit and flow the savings into lower monthly payments regardless of buyer income or vehicle origin. The rule shift raised EVs to nearly 20% of all new U.S. leases in Q4 2024 and will pull thousands of additional government-fleet orders forward because federal agencies must meet zero-emission targets beginning in 2027. Parallel programs in Germany subsidize “social leases” for low- and middle-income households, demonstrating how policy supports broad demographic reach. As these measures spread, the electric vehicle leasing market attracts price-sensitive buyers who previously leaned toward used internal-combustion models. The immediate boost to demand is reinforcing lessor appetite for larger multiyear procurement deals with automakers.

Declining Battery Costs Improve Residual Values

Spot-lithium prices fell more than 40% between 2023 and 2025, helping drive battery-pack costs down toward USD 86 per kWh in the U.S. and even lower in China [2]Argonne National Laboratory, “Battery Cost Projections Under the IRA,” anl.gov. Lessors translate those savings into stronger residual assumptions because batteries now account for a smaller share of vehicle replacement cost than five years ago. Solid-state pilot lines coming online after 2027 will further cut cell weight and raise energy density, extending vehicle lifetimes beyond 300,000 miles. Robust residuals unlock longer-term lease offerings without punitive monthly rates, broadening eligibility to mid-income households. Together, cost deflation and durability gains amplify the electric vehicle leasing market’s value proposition while reducing financial-reserve requirements for captives and independents alike.

Rising EV Model Variety Lowers Entry Cost via Leasing

More than 350 battery electric and plug-in variants were on sale globally in 2025, quadruple the 2020 count, giving consumers unprecedented choice at multiple price points [3]International Energy Agency, “Global EV Outlook 2025,” iea.org. Tesla trimmed Model 3 leases to USD 299 per month while premium brands such as BMW introduced the i5 line with starting MSRPs above USD 67,000, yet both are moving through lease channels at similar velocity because customers perceive an ability to upgrade every 24–36 months. China’s BYD and SAIC expand aggressively in Europe through bulk-lease partnerships, bringing city-car sticker prices below USD 18,000 and accelerating entry-level uptake. Continuous model refresh cycles ease technology-obsolescence fears because lessees know they can transition to next-generation batteries without carrying disposal risk. The resulting diversity of configurations—from compact sedans to long-range vans—cements leasing as the preferred on-ramp to electric mobility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 2026–27 Off-lease EV Glut | -2.3% | North America core, spillover to EU | Medium term (2-4 years) |

| Residual Uncertainty Amid Tech Change | -2.1% | Global premium segments | Medium term (2-4 years) |

| Limited Public Charging Dampens Confidence | -1.8% | Rural and suburban areas | Short term (≤ 2 years) |

| Interest rates Increase Lease Payments | -1.4% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

2026–27 Off-lease EV Glut May Depress Prices

Lease maturities peak in 2026 as the wave of contracts signed during the 2023–24 incentive surge returns to market, adding more than 200,000 used EVs in the U.S. alone. Concentrated model-year clustering risks pushing wholesale prices lower, forcing lessors to absorb heavier depreciation hits or delay remarketing to avoid inventory pile-ups. Any reduction or phase-out of federal incentives for new purchases during the same window could magnify price pressure by shifting bargain hunters toward discounted used units. Leasing companies are already testing drip-feed remarketing and flexible extension offers, but analysts warn these measures may only smooth, not eliminate, the underlying oversupply. The potential residual-value shock poses a medium-term drag on profit margins and could tighten credit terms for new leases originating in 2025–26.

Uncertain Residual Values Amid Rapid Tech Change

Fierce price competition led by Tesla’s 2024 list-price cuts triggered sharper-than-expected used-EV depreciation, with several models losing 15–20% more value than guidebooks had penciled in. Software-defined vehicles complicate matters because an over-the-air update can instantly increase range or autonomy, making earlier builds feel obsolete. Academic tracking shows five-year EV depreciation near 49.1%, higher than internal-combustion peers, forcing lessors to add risk buffers or shorten lease terms. Premium brands weather volatility better, yet overall uncertainty narrows profit margins. Higher risk premia, in turn, nudge some consumers back toward traditional loans, limiting short-term lease growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Electrification

Passenger-car leasing remains dominant with an 80.13% share in 2024, powered by affordable sub-USD 300 monthly offers that undercut comparable gasoline vehicles on running costs. However, commercial demand is where lessors extract stronger margins through bundled telematics, maintenance, and energy-management add-ons. As fleet managers swap diesel for electricity, the electric vehicle leasing market draws incremental revenue streams from managed-services fees that cushion residual-value risk.

Commercial vehicles are forecast to grow at 18.24% CAGR, outpacing the larger passenger-car base and signaling fresh momentum in the electric vehicle leasing market size for high-utilization assets. California’s Advanced Clean Fleets regulation makes zero-emission procurement compulsory for priority operators, attracting long-term master-lease agreements from last-mile giants. Lease pricing favors commercial adopters because high annual mileage compresses the total cost of ownership faster than for private users, while guaranteed buy-back clauses reduce capital-budget strain.

By Propulsion Type: Battery Electric Dominance Accelerates

Battery electric vehicles represented 72.56% of 2024 lease signings and are projected to hold that leadership while logging a 19.66% CAGR, ensuring the electric vehicle leasing market share for BEVs widens over the decade. Falling cell prices and higher pack durability cut estimated depreciation curves, enabling lessors to quote aggressively without eroding margins. Fast-charging rollouts along logistics routes make BEVs viable for medium-duty freight, stealing volume from plug-in hybrids.

Fuel-cell models stay niche, restricted to fleet pilots in regions with a hydrogen supply. Plug-in hybrids retain a foothold among range-conscious buyers but face declining relevance once nationwide 350 kW charging targets materialize. In turn, the electric vehicle leasing industry sees a gradual portfolio reweighting toward pure battery platforms, aligning residual-value modeling with one propulsion architecture instead of three.

By End User: Corporate Leadership Drives Market Evolution

Corporate accounts controlled 48.25% of 2024 contracts, translating to the single largest client block within the electric vehicle leasing market size. Bulk procurement aggregates charging services, accident-management cover, and carbon-reporting tools under multiyear umbrella deals. ESG reporting rules add urgency, compelling listed firms to turn over a portion of their light-duty fleet every 24 months to hit interim emission milestones.

Ride-sharing and delivery platforms grow the fastest at a 19.14% CAGR as operators outsource entire vehicle pools to specialist lessors who guarantee uptime and battery health. Individual households still chase promotional rates but represent a thinner margin segment because mileage is low and ancillary revenue opportunities are limited. Government agencies, bound by statutory zero-emission targets, provide a predictable demand floor even during economic downturns.

By Duration: Short-term Flexibility Gains Momentum

Mid-term leases of 1–3 years commanded 56.81% of 2024 signings because they balance monthly affordability against technology refresh cadence, anchoring the electric vehicle leasing market. Corporate fleets favor the cycle because depreciation aligns neatly with accounting schedules and residual-value risk stays manageable.

Short-term leases under 12 months clock an 18.76% CAGR as subscription platforms court urban millennials who view cars as on-demand utilities. Three-month trials convert skeptics into committed EV drivers without tethering them to long contracts, raising future retention. Long-term leases beyond 36 months lose appeal given rapid drivetrain advances that could leave lessees locked into outdated chemistries.

Geography Analysis

Europe held 43.66% of the electric vehicle leasing market share in 2024, supported by CO₂ fleet penalties and social-leasing programs that subsidize lower-income drivers. Company-car tax breaks, extended to 2035 in Germany, spur corporate renewals every two years. Yet subsidy roll-backs, such as Germany’s Umweltbonus halt, introduce demand swings that lessors must factor into residual assumptions.

Asia-Pacific, led by China, registers the fastest 17.85% CAGR as production scale slashes sticker prices and domestic demand tops 50% of new sales. Thailand’s EV 3.5 roadmap funnels battery-electric incentives toward both buyers and manufacturers, making Southeast Asia a rising export hub. North America leverages Inflation Reduction Act provisions that channel purchase credits into lease structures, but charging-network gaps outside metro areas temper volume growth.

North America benefits from a commercial-vehicle credit that overrides origin rules, making imported models finance-eligible. Federal and state fleet mandates provide a demand baseline, yet the patchwork nature of fast-charging corridors holds back rural adoption. South America and the Middle East remain early-stage but show promise where ride-hail operators form anchor tenants for leasing volumes centered on metropolitan hubs.

Mordor Intelligence provides coverage of the electric vehicle leasing market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Japan, India, United States, and South Korea incorporating local coverage and market participation, as required.

Competitive Landscape

Traditional heavyweights such as Arval, Sixt, and Enterprise Holdings deploy scale economies to secure six- and seven-figure procurement deals with automakers, locking in discounted unit costs that translate into lower monthly rates for customers. Arval’s memorandum with BYD underscores a pivot toward Chinese supply chains that deliver faster and cheaper than legacy European plants, while Sixt’s multi-brand strategy diversifies residual-value exposure.

Captive finance arms like Tesla Finance wield price-setting power by adjusting lease factors instead of headline vehicle prices, positioning USD 299 Model 3 leases to sustain showroom traffic even when cash buyers hesitate. Start-ups such as Autonomy exploit subscription demand with bundled insurance, charging, and maintenance, creating an asset-light pathway that skirts the high capital intensity of classical fleet ownership.

Market entrants increasingly differentiate through data analytics—NETSOL and Element Fleet integrate battery-health AI to predict residuals with sub-5% error margins, shaving reserve requirements and enabling sharper quotes. As platforms converge hardware, software, and finance, the electric vehicle leasing market rewards players that couple multi-brand supply with end-to-end digital servicing.

Electric Vehicle Leasing Industry Leaders

Ayvens

Arval (BNP Paribas)

Sixt SE

Hertz Global Holdings

Volkswagen Financial Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Leasys announced plans to double its European low-emission fleet by 2026, aligning with region-wide sustainability mandates

- May 2025: Tata Motors partnered with Vertelo to launch leasing programs for its electric commercial vehicles in India, easing fleet-owner capital constraints.

- November 2024: Tesla began Cybertruck leases priced from USD 999 per month on 36-month terms, capitalizing on full federal credits while keeping list prices intact

- February 2024: Arval signed a memorandum with BYD to expand telematics-enabled EV lease packages across Europe, combining procurement scale with Chinese manufacturing depth.

Global Electric Vehicle Leasing Market Report Scope

| Passenger Cars |

| Commercial Vehicles |

| Battery Electric Vehicles |

| Plug-in Hybrid Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| Individual Customers |

| Corporate Fleets |

| Government Agencies |

| Ride-Sharing and Delivery Platforms |

| Short-Term (Less than 12 months) |

| Mid-Term (1–3 years) |

| Long-Term (More than 3 years) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Propulsion Type | Battery Electric Vehicles | |

| Plug-in Hybrid Electric Vehicles | ||

| Fuel-Cell Electric Vehicles | ||

| By End User | Individual Customers | |

| Corporate Fleets | ||

| Government Agencies | ||

| Ride-Sharing and Delivery Platforms | ||

| By Duration | Short-Term (Less than 12 months) | |

| Mid-Term (1–3 years) | ||

| Long-Term (More than 3 years) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What was the global electric vehicle leasing market size in 2025?

It reached USD 104.95 billion in 2025 and is projected to more than double to USD 230.17 billion by 2030.

How fast is the sector expected to grow?

The market is forecast to register a 17.01% CAGR between 2025 and 2030, outpacing most traditional auto-finance segments.

Which region leads in market share today?

Europe holds the largest share at 43.66%, supported by strict emissions rules and social-leasing initiatives.

What propulsion type dominates current contracts?

Battery electric vehicles command 72.56% of leases, benefiting from falling battery costs and expanding fast-charge networks.

Page last updated on: