Commercial Airport Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 312.64 Billion |

| Market Size (2030) | USD 442.39 Billion |

| Growth Rate (2025 - 2030) | 7.19% CAGR |

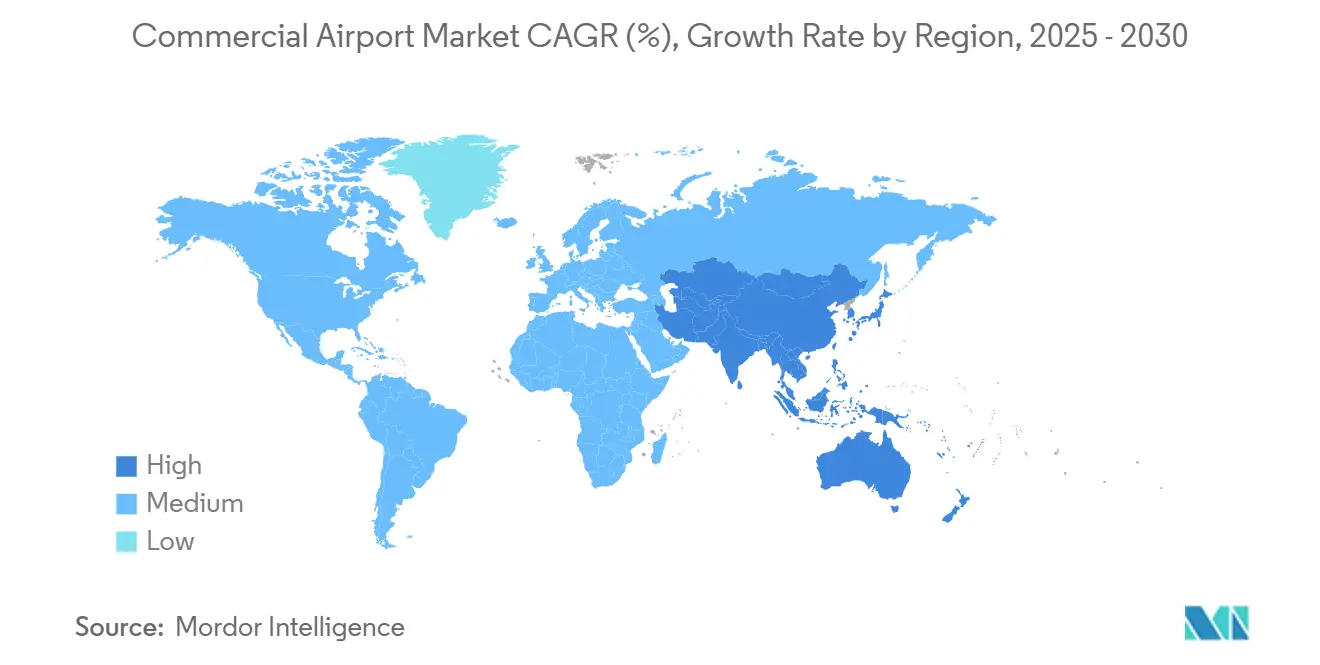

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

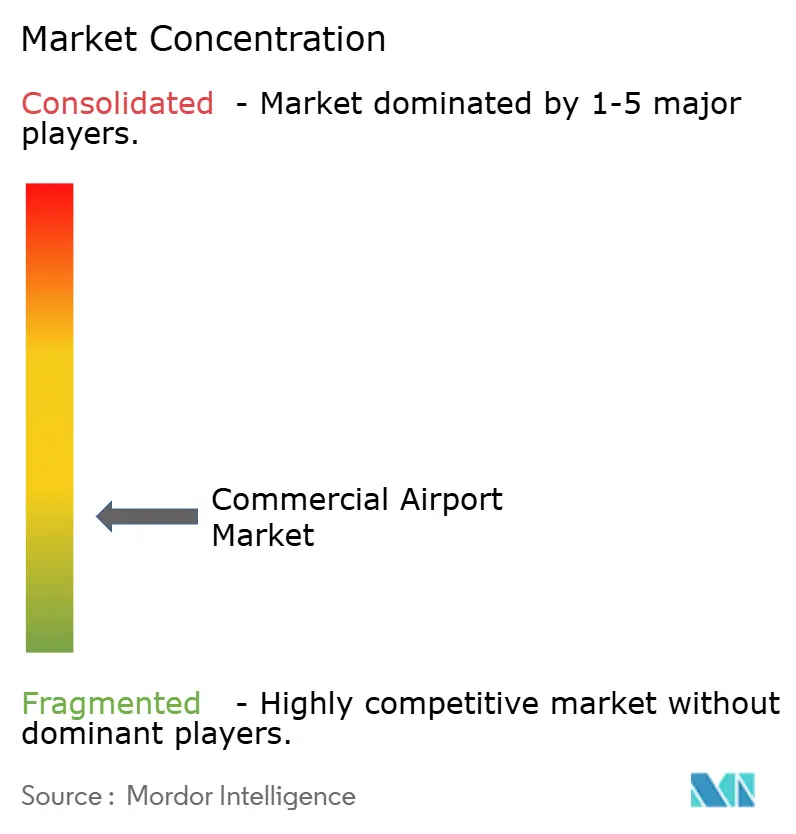

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Airport Market Analysis by Mordor Intelligence

The commercial airport market size is valued at USD 312.64 billion in 2025 and is projected to reach USD 442.39 billion by 2030, advancing at a 7.19% CAGR during the forecast period. The industry’s full traffic recovery underpins growth, global passenger volumes surpassing 9.5 billion in 2024, and sustained infrastructure outlays prioritizing capacity expansion and technology upgrades. Accelerated privatization programs in emerging economies, wider adoption of public-private partnership models, and the strategic pivot toward non-aeronautical revenue streams that contribute up to 60% of total airport income collectively reinforce the commercial airport market’s momentum. Airside modernization, especially taxiway and runway projects, addresses capacity bottlenecks created by the surge in wide-body deployments and secondary-hub traffic redistribution. Meanwhile, AI-enabled airport operations centers (APOCs) improve throughput and resilience by integrating real-time datasets across airside and landside touchpoints. These structural drivers provide an enduring platform for network airlines, low-cost carriers, and cargo operators to absorb demand while meeting tightening sustainability and service benchmarks.

Key Report Takeaways

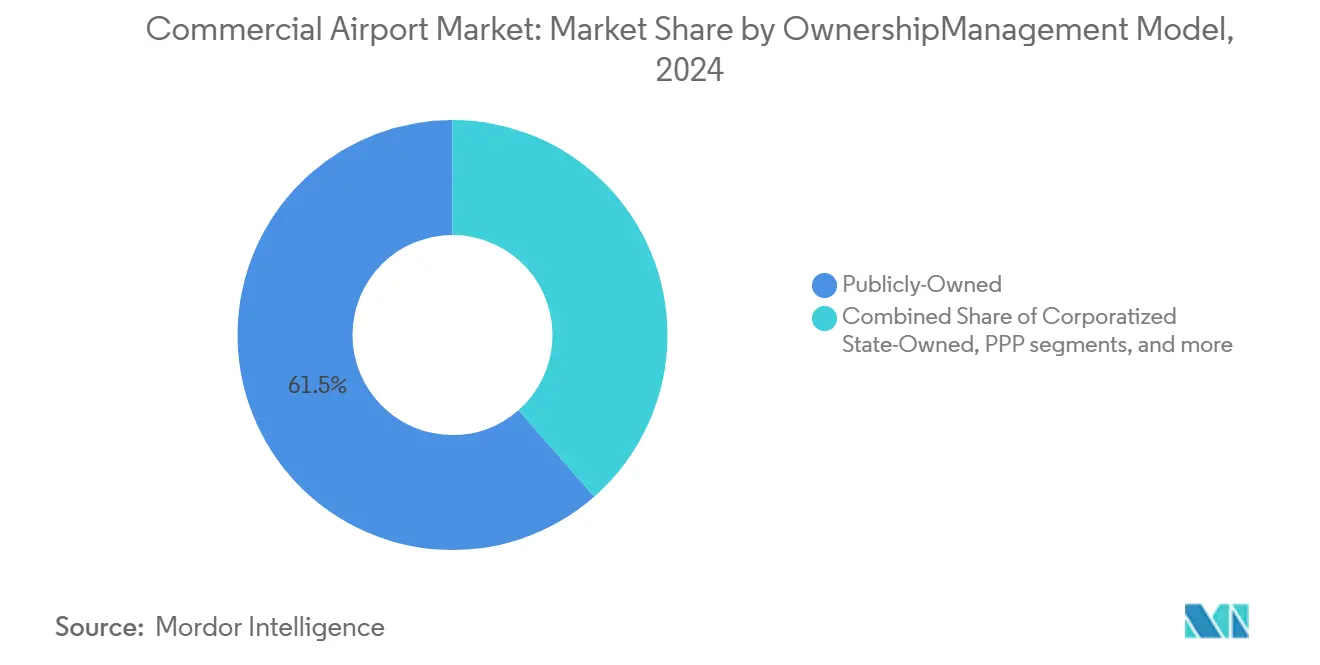

- By ownership/management model, publicly-owned airports held 61.45% of the commercial airport market share in 2024; public-private partnerships are forecasted to register the fastest 6.45% CAGR through 2030.

- By airport size class, large hubs commanded 41.34% of the commercial airport market size in 2024, while medium hubs are expected to advance at a 7.12% CAGR through 2030.

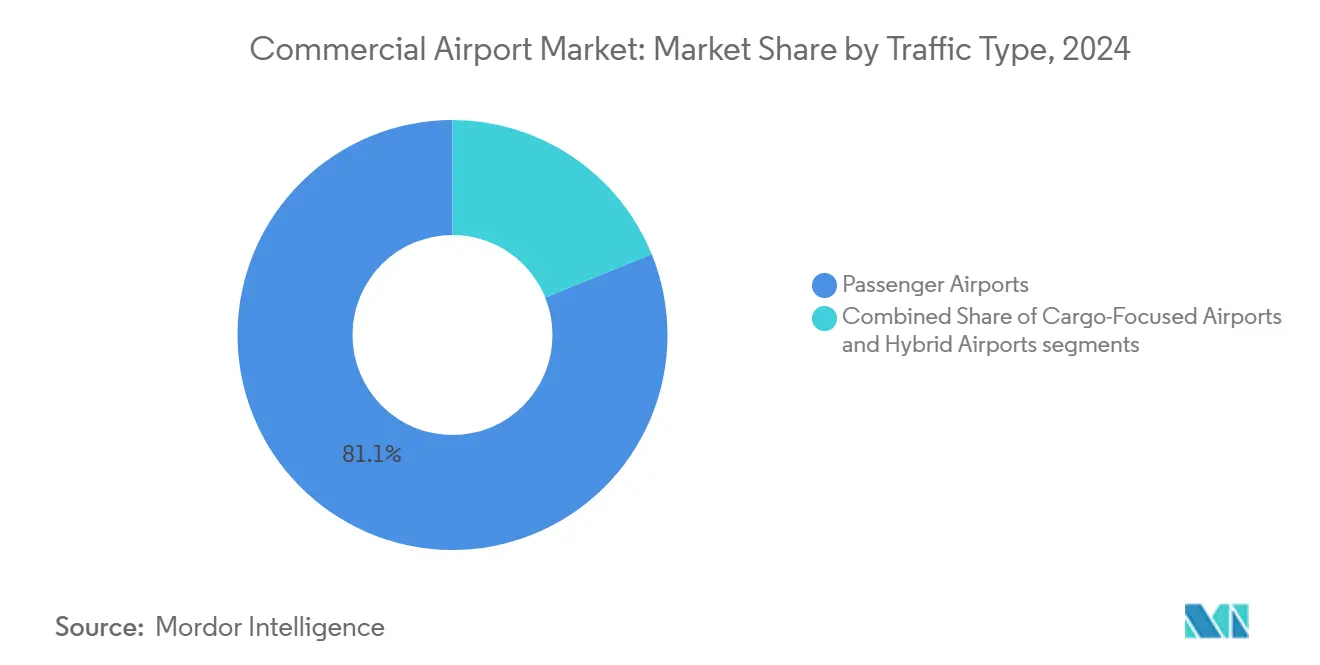

- By traffic type, passenger-focused facilities accounted for 81.12% share of the commercial airport market size in 2024, whereas hybrid airports integrating cargo and passenger flows expand at a 6.87% CAGR to 2030.

- By infrastructure type, terminal projects led with 42.67% revenue share in 2024; taxiway and runway upgrades exhibit the highest 7.87% CAGR over the outlook period.

- By geography, North America contributed 46.87% of the commercial airport market size in 2024, while the Asia-Pacific region recorded the fastest growth of 8.56% CAGR through 2030.

Global Commercial Airport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global passenger demand post-pandemic recovery | +1.2% | Global; strongest in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Rapid expansion of airport privatization and public-private partnership (PPP) investments | +0.8% | Global; concentrated in emerging markets | Long term (≥ 4 years) |

| Diversification into non-aeronautical revenue streams | +1.1% | Global; advanced in Europe and North America | Medium term (2-4 years) |

| AI-enabled airport operations centers (APOCs) boosting throughput | +0.9% | Asia-Pacific core; spill-over to Europe and North America | Long term (≥ 4 years) |

| Rise of secondary-hub low-cost carrier (LCC) networks stimulating regional traffic | +1.3% | Europe, Asia-Pacific, Latin America | Medium term (2-4 years) |

| Space-based ADS-B unlocking additional airspace and slot capacity | +0.7% | Global; early adoption in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Global Passenger Demand Post-pandemic Recovery

Passenger traffic reached 9.5 billion in 2024 and exceeded pre-crisis peaks, putting immediate pressure on terminal and gate capacities at primary hubs.[1]Airports Council International, “Global Passenger Traffic Reaches 9.5 Billion in 2024,” aci.aero Medium hubs benefit as airlines redirect flows to bypass congestion, prompting incremental gate expansions that accommodate widebody aircraft rotations. The robust demand profile supports route reinstatement and new city-pair launches, fostering healthy aeronautical revenue growth for airports even as competition intensifies. Airports leverage this volume surge to negotiate favorable concession terms with retailers and hospitality providers, reinforcing landside revenue diversification. The resiliency of discretionary travel spending, barring major geopolitical shocks, positions the commercial airport market for multi-year demand tailwinds.

Rapid Expansion of Airport Privatization and PPP Investments

Governments from Manila to New Delhi turned to private capital to accelerate large-scale airport upgrades, exemplified by the USD 3 billion NAIA concession and India’s ongoing privatization pipeline.[2]Department of Transportation Philippines, “NAIA Concession Award Announcement 2024,” dotr.gov.ph Private operators inject operational know-how, modern commercial practices, and faster decision cycles than traditional public-sector governance. Improved service-level agreements and performance-based concession models safeguard public interests while ensuring investor returns, prompting replication across Latin America and parts of Africa. The pipeline of brownfield concessions and greenfield build-operate-transfer projects enables capital-starved jurisdictions to meet surging passenger and cargo requirements without straining public balance sheets. Stable regulatory frameworks further de-risk long-dated infrastructure assets and widen the pool of international bidders.

Diversification into Non-aeronautical Revenue Streams

Retail, car-parking, advertising, and real-estate ventures now contribute up to 60% of revenue at leading hubs, protecting cash flows from cyclicality in air traffic.[3]Airports Council International, “Global Passenger Traffic Reaches 9.5 Billion in 2024,” aci.aero Mixed-use developments such as logistics parks and data centers amplify land-side monetization, while destination-style retail precincts increase passenger dwell time and spend. Digital marketplaces embedded in airport apps extend the commercial footprint beyond the terminal, enabling click-and-collect and loyalty integrations that lift yield per passenger. In regions with high slot constraints, non-aeronautical growth is often the only avenue to expand revenue faster than traffic. Airports that master omni-channel engagement and curate compelling tenant mixes secure superior EBITDA margins and healthier balance sheets.

AI-enabled Airport Operations Centers Boosting Throughput

Hyderabad's AI-driven APOC improved on-time performance by 15% and cut ground delays by 20%, demonstrating tangible efficiency gains.[4]GMR Group, “Hyderabad Airport Operations Center Performance Report 2024,” gmrgroup.in Machine-learning algorithms synthesize weather, flight plan, and gate allocation data to produce predictive decision support, curbing disruption cascades. Asset uptime improves through condition-based maintenance scheduling, reducing repair costs and service disruptions. As labor shortages intensify in key aviation markets, AI tools compensate by automating repetitive coordination tasks and enhancing controllers' situational awareness. Implementation costs are offset by higher throughput within existing footprints, postponing expensive brick-and-mortar expansions. Early adopters gain reputational benefits that attract carriers seeking slot reliability, reinforcing competitive positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex requirements and financing cost volatility | -0.9% | Global; acute in emerging markets | Short term (≤ 2 years) |

| Regulatory slot and environmental constraints | -0.6% | Europe and North America | Long term (≥ 4 years) |

| Aircraft delivery/engine shortages capping seat growth | -0.4% | Global | Medium term (2-4 years) |

| Escalating cybersecurity threats causing operational outages | -0.5% | Global; higher in digitally advanced airports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex Requirements and Financing Cost Volatility

Interest-rate hikes added 200-300 basis points to long-term project debt, pushing greenfield terminals above pro-forma hurdle rates in markets already coping with currency risk. Rising construction-material prices strain budget contingencies and compel scope reductions or timeline extensions. Private investors demand revenue-share guarantees or tariff-indexation clauses that sometimes stall concession negotiations, particularly where political transitions create policy uncertainty. Multilateral lenders step in with blended-finance structures, yet due diligence cycles prolong project gestation periods. Airports that secure investment-grade ratings and diversify funding across bonds, sustainability-linked loans, and export-credit agency support mitigate volatility and keep shovel-ready projects moving forward.

Regulatory Slot and Environmental Constraints

European eco-mandates target net-zero operations by 2050, compelling airports to budget for on-site renewable energy, SAF infrastructure, and carbon-neutral building standards. Simultaneously, community noise curfews and slot caps at capacity-constrained hubs limit peak-period growth potential. North American regulators explore tighter particulate-matter thresholds, raising compliance costs for older air-side equipment. Without harmonized regional rules, airports juggling multiple jurisdictional frameworks face incremental administrative burdens and higher legal risk. Long-term planning must account for carbon-pricing schemes that could alter route economics and suppress transfer traffic through specific hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership/Management Model: Private partnerships drive efficiency gains

Publicly-owned airports retained a 61.45% share of the commercial airport market size in 2024, yet public-private partnerships exhibit the fastest 6.45% CAGR to 2030. Corporatized state-owned entities strike a middle ground, modernizing governance while preserving public equity, whereas fully-private concessions, though smaller in number, often lead service-quality rankings. The growth of PPPs reflects fiscal constraints and the proven ability of global operators to compress construction schedules and lift retail yields. Standardized concession templates promoted by ICAO shorten tender durations, increasing deal flow and cross-border investor participation.

Operationally, performance-based key performance indicators (KPIs) such as passenger satisfaction scores, baggage-delivery times, and on-time departure ratios align incentives between public authorities and concessionaires. Successful contracts in Brazil and India demonstrate that transparent regulatory oversight and tariff predictability underpin investor confidence. Over the forecast horizon, more midsize airports are expected to corporatize before seeking private equity injections, widening the talent pool and creating benchmarking pressure on purely public peers.

By Airport Size Class: Medium hubs capitalize on network evolution

Large hubs captured 41.34% of the market share in 2024, yet congestion and slot scarcity temper their expansion headroom. Medium hubs, handling 10-40 million passengers annually, post the strongest 7.12% CAGR as airlines favor point-to-point connections and cost-efficient operations. Secondary hubs often benefit from shorter taxi times, lower charges, and regional traffic stimulation measures, positioning them to attract full-service carriers (FSCs) using narrowbodies and LCCs with quick turnarounds.

Investment priorities at medium hubs concentrate on flexible swing gates, modular terminals, and self-service technologies that adapt to seasonality without compromising passenger experience. Federal initiatives like the US Federal Aviation Administration's (FAA's) NextGen program further boost medium-hub competitiveness by reducing arrival spacing and improving ground-movement predictability. As network planners diversify risk away from mega-hubs, medium hubs evolve into regional connection centers, capturing spill-over demand and reinforcing their viability for further capital upgrades.

By Traffic Type: Hybrid models optimize revenue diversification

Passenger-only facilities led with 81.12% share of the commercial airport market size in 2024, but hybrid airports that integrate cargo grow at a 6.87% CAGR. The hybrid approach mitigates seasonality; cargo peaks often counterbalance passenger troughs, stabilizing cash flows and asset-utilization ratios. E-commerce growth elevates the importance of express freight, prompting passenger hubs to add dedicated sort facilities and airside truck docks.

Operationally, segmentation between freight and traveler flows demands sophisticated apron management and security zoning, yet the capital outlay pays back through higher stand occupancy rates and diversified tariff structures. As global trade agreements, including the WTO Trade Facilitation Agreement, smooth cross-border goods movement, hybrid airports positioned near manufacturing clusters or free-trade zones stand to capture incremental tonnage. The model’s resilience during passenger downturns observed during the 2020-2022 period reinforces stakeholder support for hybrid expansions.

By Infrastructure Type: Airside capacity drives investment priorities

Terminal projects maintained a 42.67% share in 2024, reflecting the high visibility of passenger experience enhancements, while taxiway and runway works grow at a 7.87% CAGR as airports confront hard airside limits. Runway-end safety areas, rapid-exit taxiways, and high-speed turnoffs feature prominently, enabling throughput gains without new runways. LED ground-lighting, advanced surface-movement radars, and pavement health sensors extend asset life and support eco-targets.

Control-tower modernization incorporates remote digital tower solutions, reducing staffing costs for low-traffic periods and enhancing situational awareness during adverse weather. Hangar and MRO capacity escalates to accommodate aircraft life-extension programs triggered by delivery delays, with many airports partnering with OEMs for on-airport heavy-maintenance bases. Complementary utility projects such as renewable-energy microgrids and stormwater recycling integrate sustainability goals mandated by regulators and concession covenants.

Geography Analysis

North America held 46.87% of the commercial airport market size in 2024, anchored by mature network carriers and steady modernization funding. Capital injection focuses on terminal upgrades, biometric boarding deployments, and NextGen air-traffic integration rather than greenfield runway builds. Canada prioritizes carbon-neutral operations, adding on-site solar arrays and electric ground-service fleets that reduce Scope 1 emissions. Mexico’s surging tourism and nearshoring trends spur runway extensions and cargo apron expansions in Pacific and Gulf corridors.

Asia-Pacific charts the fastest 8.56% CAGR, propelled by large-scale airport infrastructure development schemes across China, India, and Southeast Asia. China’s Belt and Road Initiative co-finances regional gateways that knit together secondary cities, while India’s USD 4.14 billion Jewar project exemplifies megahub ambitions. Governments integrate smart-terminal blueprints and SAF logistics at the design phase, sidestepping retrofit costs that burden legacy hubs elsewhere. Passenger demographic tailwinds alongside e-commerce cargo demand provide a dual engine for sustained cap-ex justification.

Europe emphasizes efficiency and sustainability over capacity additions, constrained by strict environmental statutes and community noise curbs. Slot auctions and performance criteria reshape airline schedules, incentivizing larger-gauge aircraft and off-peak movements. Middle Eastern hubs leverage geographic positioning for intercontinental transfer traffic, yet growth normalizes as previous double-digit expansions moderate. Although sovereign-risk premiums persist, Africa’s nascent modernization builds momentum in Kenya, South Africa, and Nigeria, buoyed by multilateral funding and regional open-skies agreements.

Competitive Landscape

Competition is fragmented, with international construction conglomerates, specialized airport operators, and regional builders vying for concession and EPC contracts. VINCI Airports, Ferrovial, and Bechtel routinely pre-qualify for megaproject tenders, bringing integrated financing and operational capabilities that streamline lifecycle delivery. Domestic players such as China State Construction Engineering and India’s Larsen & Toubro capture projects, leveraging local supply chains and regulatory familiarity. Technology partners like SITA and Siemens Digital Industries embed smart-infrastructure layers that differentiate bids through operational efficiency guarantees.

Strategic moves increasingly marry capital strength with digital prowess. In January 2025, VINCI Airports commissioned a USD 2.1 billion Santiago expansion featuring terminal-wide biometrics and green-energy systems, raising the bar for Latin American projects. In November 2024, Ferrovial acquired a 25% stake in Jewar Airport, bringing European service standards to Asia’s most extensive greenfield development and signaling continued cross-border equity participation. Contractors form consortia with cybersecurity firms to meet tightened selection criteria that weigh operational resilience alongside cost.

Barriers to entry remain significant: concession tender complexity, multiyear cash-flow ramp-up, and the need for deep working-capital reserves deter smaller firms. Nonetheless, midsize regional contractors find opportunities in phased runway rehabilitations and modular terminal builds championed by national stimulus programs. Partnerships among builders, OEMs, and institutional investors further consolidate market share around players able to furnish turnkey solutions encompassing design, build, finance, and operate phases.

Commercial Airport Industry Leaders

Aéroports de Paris SA

VINCI Airports

Bechtel Corporation

HOCHTIEF AG

Ferrovial SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Centralny Port Komunikacyjny (CPK) issued a tender to select a general contractor to construct the new passenger terminal of the new CPK Airport, planned to be built between Warsaw and Łódź in Poland. With an estimated value exceeding USD 1.3 billion, this contract is the largest procurement under the CPK program.

- May 2025: Bechtel signed an agreement with the King Salman International Airport Development Company to act as the delivery partner for developing three new terminals at King Salman International Airport (KSIA) in Riyadh.

- February 2025: Saudi-based Matarat Holding, in partnership with the National Center for Privatization & PPP, announced that leading global players in the airport construction sector, including Korea's Samsung C&T, French major Bouygues Batiment, UK's Manchester Airport Group, Germany's Munich Airport International, Corporación América, France's Egis, and India's GMR Airports, are competing for the development of Taif International Airport in Saudi Arabia.

Global Commercial Airport Market Report Scope

| Publicly-Owned |

| Corporatized State-Owned |

| Public-Private Partnership (PPP) |

| Fully-Private Concession |

| Large Hub (Greater than 40 million) |

| Medium Hub (10 to 40 million) |

| Small/Regional (Less than10 million) |

| Passenger Airports |

| Cargo-Focused Airports |

| Hybrid Airports |

| Terminal |

| Control Tower |

| Taxiway and Runway |

| Apron |

| Hangar |

| Other Infrastructure Types |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Ownership/Management Model | Publicly-Owned | ||

| Corporatized State-Owned | |||

| Public-Private Partnership (PPP) | |||

| Fully-Private Concession | |||

| By Airport Size Class (Annual Pax) | Large Hub (Greater than 40 million) | ||

| Medium Hub (10 to 40 million) | |||

| Small/Regional (Less than10 million) | |||

| By Traffic Type | Passenger Airports | ||

| Cargo-Focused Airports | |||

| Hybrid Airports | |||

| By Infrastructure Type | Terminal | ||

| Control Tower | |||

| Taxiway and Runway | |||

| Apron | |||

| Hangar | |||

| Other Infrastructure Types | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Commercial Airport Market in 2025?

The commercial airport market size stands at USD 312.64 billion in 2025.

What CAGR is expected for global airport revenues through 2030?

Revenues are projected to expand at a 7.19% CAGR, reaching USD 442.39 billion by 2030.

Which ownership model is growing fastest in commercial airports?

Public-private partnerships (PPPs) lead growth at a 6.45% CAGR, outpacing other ownership structures.

Why are medium hub airports attracting more airline routes?

Network carriers target medium hubs for lower charges and available slots, driving a 7.12% CAGR for this size class.

What is the main restraint holding back airport expansion plans?

High capital-expenditure needs combined with financing-cost volatility reduce near-term project viability.

Page last updated on: