Aviation Asset Management Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

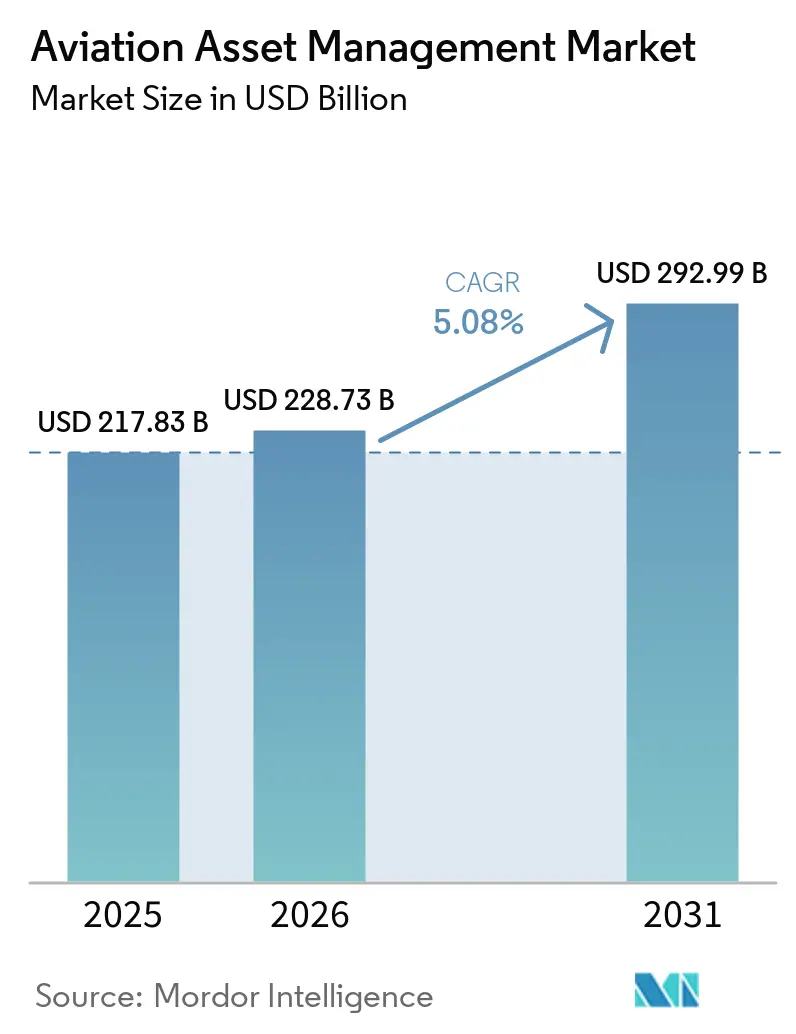

| Market Size (2026) | USD 228.73 Billion |

| Market Size (2031) | USD 292.99 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Asset Management Market Analysis by Mordor Intelligence

The aviation asset management market size was valued at USD 217.83 billion in 2025 and USD 228.73 billion in 2026 and is forecast to reach USD 292.99 billion by 2031 at a CAGR of 5.08% during 2026-2031. The aviation asset management market covers leasing, technical oversight, financial and portfolio management, and end-of-life solutions, which keep it closely linked to capital deployment, fleet planning, and aircraft lifecycle control. Leasing remains central because lessors controlled 50% of the global commercial aircraft fleet by unit count in 2025, up from 48% in 2020, underscoring the continued shift in asset ownership away from airlines and toward specialist platforms.[1]BOC Aviation, “2025 Final Results Review,” BOC Aviation, bocaviation.com Supply remains tight because Airbus and Boeing backlogs now extend beyond 11 years, which supports lease rates, lengthens placements, and keeps vacancy risk low across major aircraft classes. The aviation asset management market is also being shaped by a funding environment that remains firmer than pre-2022 levels, even after policy easing, meaning balance-sheet strength and access to long-duration capital matter more than before. At the same time, compliance rules such as the EU ReFuelEU Aviation Regulation are starting to create a divide between newer and older aircraft, which creates wider pricing gaps across portfolios and opens room for active managers to reposition, upgrade, or exit assets at the right point in the cycle.

Key Report Takeaways

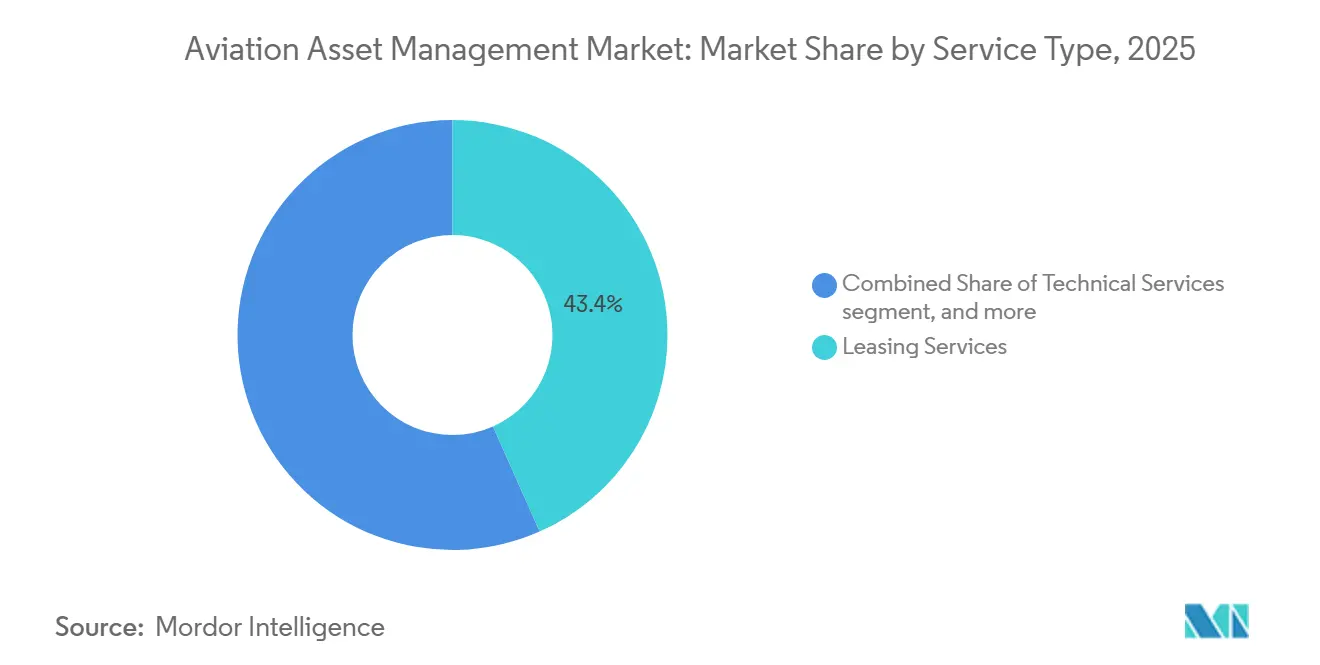

- By service type, leasing services accounted for 43.36% of the aviation asset management market size in 2025, while financial and portfolio management is forecast to expand at a 6.98% CAGR through 2031.

- By aircraft type, general aviation accounted for a 39.87% share of the aviation asset management market in 2025, while commercial aviation is projected to grow at a 7.81% CAGR through 2031.

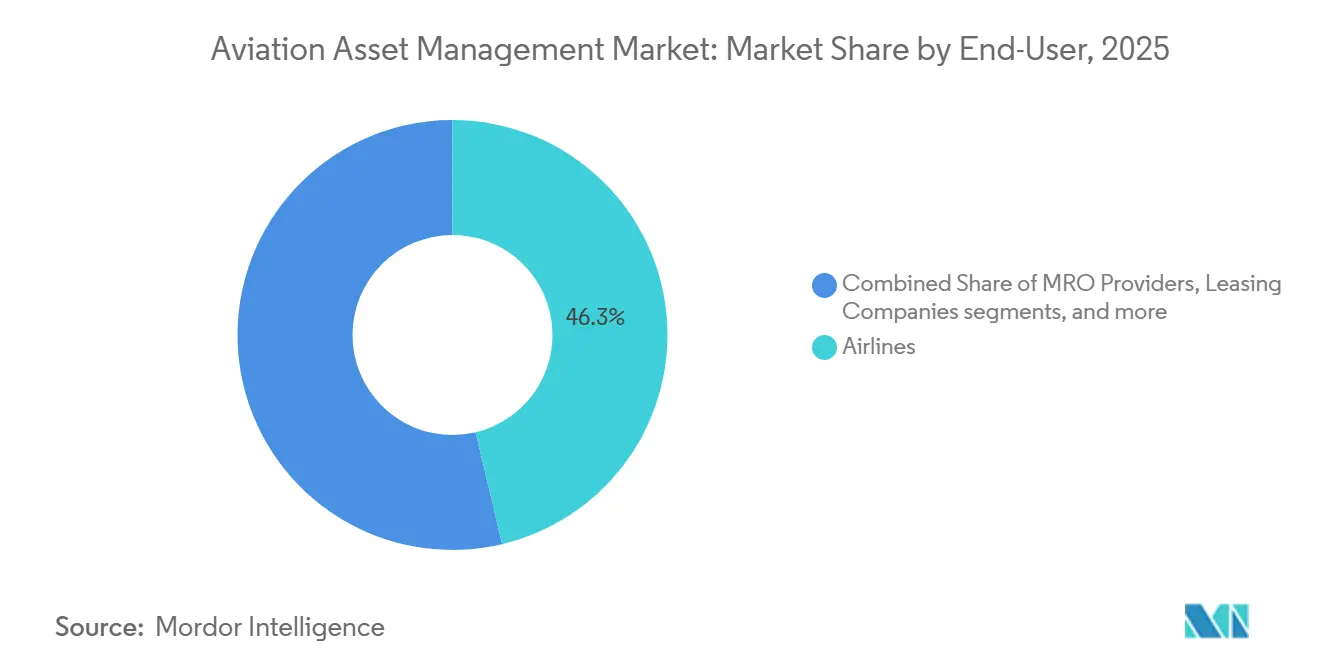

- By end user, airlines held a 46.29% share of the aviation asset management market in 2025, while financial institutions and investors are expected to grow at a 6.77% CAGR through 2031.

- By asset ownership, leased aircraft accounted for 42.59% of the aviation asset management market in 2025, while owned aircraft portfolios are forecast to grow at a 7.21% CAGR through 2031.

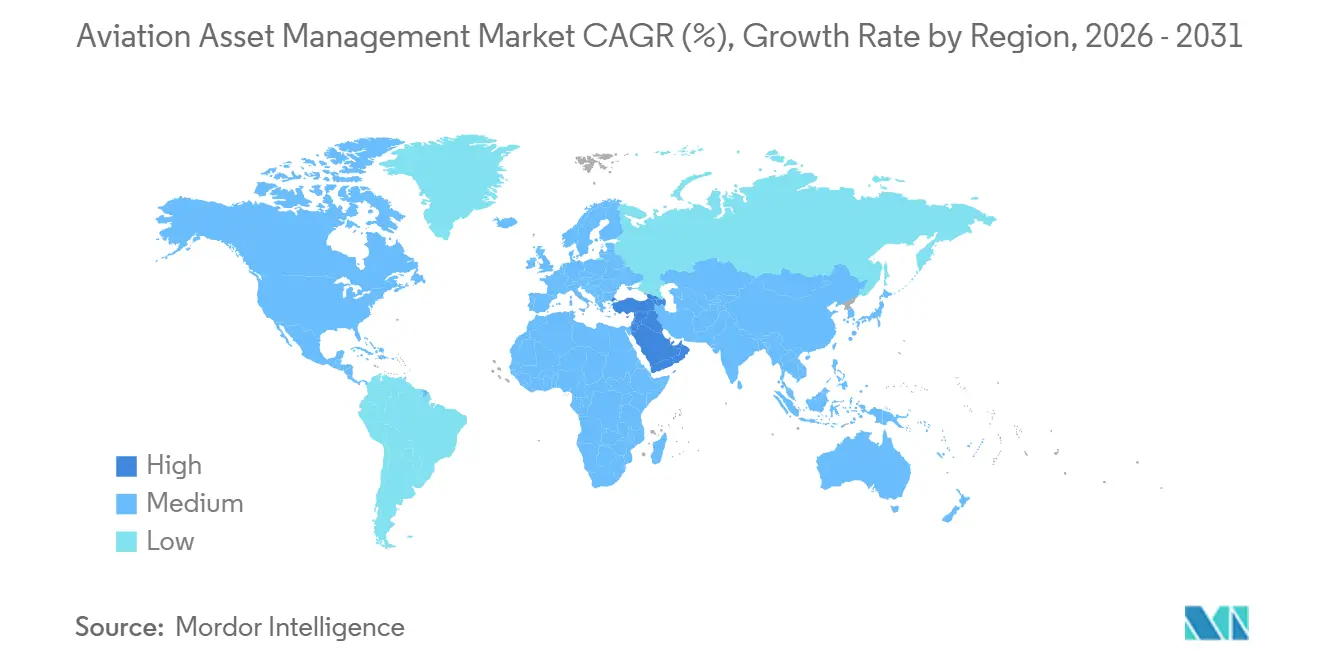

- By geography, North America held 40.67% of the aviation asset management market share in 2025, while the Middle East is projected to expand at an 8.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aviation Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Sale-and-Leaseback (SLB) demand post-pandemic | +1.2% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Growth of LCCs in emerging markets | +0.8% | Asia-Pacific core, spill-over to Middle East and Latin America | Medium term (2-4 years) |

| Rising adoption of predictive maintenance analytics | +0.7% | Global, led by North America, Europe, and Middle East | Medium term (2-4 years) |

| Liquidity-driven demand from alternative asset investors | +0.6% | North America and EU, expanding to Middle East and Japan | Medium term (2-4 years) |

| Emergence of leasing platforms for new eVTOL fleets | +0.3% | Asia-Pacific, North America, and Europe | Long term (≥ 4 years) |

| Regulatory push for fuel-efficient fleet renewals | +0.5% | EU-led, with global relevance through ICAO CORSIA and SAF mandates | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Sale-and-Leaseback (SLB) Demand Creates a Self-Reinforcing Liquidity Cycle

SLB activity has become one of the clearest sources of demand support for the aviation asset management market. SMBC Aviation Capital stated that 750 aircraft were transacted with leases attached in 2025, which was double the volume recorded in 2021. Airlines continue to use these deals to release capital while preserving fleet access, and lessors benefit because the structure limits pre-delivery exposure and secures long-term rent streams. The aviation asset management market gains further support as aircraft scarcity lifts residual values and improves the economics of allocating scarce delivery positions to strong operators. That effect is becoming more important because jets with more than 150 seats are effectively sold out until 2035, which gives delivery slots an added strategic premium for owners who can control them.[2]Avolon, “India, UAE, and Saudi Arabia Set to Lead Global Aviation Growth,” Avolon, avolon.aero ESG-linked structures are also becoming more visible, meaning SLB contracts are increasingly reflecting fleet carbon intensity and the share of new-generation aircraft in use.

Growth of LCCs in Emerging Markets Widens the Lessee Base

The aviation asset management market is also benefiting from the continued expansion of LCCs in emerging regions, as these operators usually favor operating leases over full ownership when adding capacity quickly and reshaping route networks to match demand. The Middle East alone is expected to require 1,430 new single-aisle deliveries through 2044, which supports a long runway for lessors holding narrowbody positions and able to place aircraft at scale.[3]Boeing, “Middle East Airlines Enter New Era of Growth as Region’s Fleet Will More Than Double by 2044,” Boeing, boeing.com Avolon also pointed to India, the UAE, and Saudi Arabia as major growth centers, with combined aircraft backlogs above 3,000 units and 900 deliveries expected between 2026 and 2028. That delivery pipeline expands the future lessee base for the aviation asset management market and deepens demand for technical oversight, remarketing, and portfolio planning. It also shifts more negotiating leverage toward platforms that can secure aircraft early and place them across multiple airline business models.

Rising Adoption of Predictive Maintenance Analytics Transforms Technical Asset Management Value

Predictive maintenance is becoming a practical revenue protection tool in the aviation asset management market. NBAA reported that aircraft equipped with comprehensive predictive monitoring improved dispatch reliability from 97.5% to 99.2% and reduced unscheduled maintenance events by 35% to 40%.[4]National Business Aviation Association, “How Trend Analysis Informs Predictive Aircraft Maintenance,” NBAA, nbaa.org That matters for asset managers because fewer unscheduled events mean fewer revenue interruptions and tighter control over lease performance. GE Aerospace and Scandinavian Airlines also showed in 2025 that targeted predictive monitoring on the Embraer E190 fleet reduced exposure to specific technical failures and lowered unscheduled out-of-service time. As the average global fleet age reached 15.1 years by the end of 2025, these tools became more valuable for older portfolios, where maintenance timing and redelivery conditions can materially affect asset outcomes. The aviation asset management market, therefore, gains not only from better aircraft uptime but also from better maintenance reserve calibration, stronger redelivery planning, and more disciplined residual value management.

Liquidity-Driven Demand from Alternative Asset Investors Restructures the Capital Stack

Institutional capital is becoming more important in the aviation asset management market. FTAI Aviation completed fundraising for its inaugural Strategic Capital Vehicle in October 2025, reaching an upsized hard cap of USD 2.0 billion in equity commitments, with full deployment expected by mid-2026. In January 2026, KKR increased its ownership stake in Altavair, extending a relationship through which KKR-managed funds had already committed more than USD 5 billion to aircraft transactions since 2018. In the same month, Mercuria Investment and Airborne Capital launched MACH OE, the first open-ended aircraft fund from a Japan-based asset manager, broadening the range of structures available to investors entering the sector. These moves show that the aviation asset management market is attracting capital from investors seeking long-duration contracted cash flows without having to build a full airline or lessor operating platform. They also reinforce the role of specialist asset managers that can originate, service, value, and exit aircraft on behalf of third-party capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM production delays tightening supply | -0.8% | Global | Short term (≤ 2 years) to Medium term (2-4 years) |

| Interest-rate volatility raising financing costs | -0.6% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| ESG scrutiny on aircraft lifecycle carbon footprint | -0.4% | EU-led, increasingly global through ICAO CORSIA | Medium term (2-4 years) to Long term (≥ 4 years) |

| Secondary-market uncertainty for aging widebodies | -0.3% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interest-Rate Volatility Compresses Lessor Margins and Reshapes Lease Structures

Interest-rate conditions remain a clear constraint on the aviation asset management market. SMBC Aviation Capital noted that long-dated funding costs have not fallen in line with multiple Federal Reserve rate cuts, because the 10-year swap rate has remained stable while refinancing needs have remained large. The same analysis showed that the 10 largest investment-grade rated lessors faced refinancing needs of USD 14.4 billion in 2026, which limits how aggressively some platforms can grow even when operating conditions are strong. The pressure is uneven because larger investment-grade platforms can still access tighter spreads, while smaller and private vehicles face a harder hurdle to new acquisitions. That gap is pushing the aviation asset management market toward more structured partnerships, co-investment vehicles, and lease documentation that offers stronger protection against funding mismatches. It also keeps returns sensitive to capital structure quality, not only to lease rates and aircraft placement performance.

OEM Production Shortfalls Constrain Asset Turnover and Amplify Residual Value Uncertainty

OEM production disruption continues to shape the aviation asset management market by keeping new aircraft scarce. Avolon stated that Airbus and Boeing backlogs now extend back more than 11 years, reflecting the scale of the delivery bottleneck facing airlines and lessors. When new aircraft arrive later than planned, lessors hold existing assets longer, airlines extend leases, and planned portfolio turnover slows. This environment supports near-term lease income, but it makes residual-value forecasting harder because older aircraft stay in service longer than expected, while newer models remain constrained. The aviation asset management market, therefore, faces a trade-off: scarcity improves placement conditions today but reduces visibility into replacement timing, redelivery planning, and secondary-market price discovery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Leasing Anchors Revenue as Portfolio Management Accelerates

Leasing services held 43.36% of the aviation asset management market share in 2025, which confirms that operating leases remain the core revenue engine of the aviation asset management market. Airlines continue to rely on leased capacity because access to new aircraft remains tight and balance-sheet flexibility still matters. SMBC Aviation Capital noted that narrowbody lease rates rose 27% to 35% from 2021 in constant-age terms, while the A330neo is expected to see lease rate growth above 15% because it remains the only available new widebody before 2032. That pricing backdrop makes leasing more valuable not only as a financing tool, but also as a way to secure scarce lift without waiting for long production slots. Technical asset management continues to matter across the rest of the mix because active oversight protects maintenance timing, contract compliance, and value retention through the lease term.

Financial and portfolio management is forecast to grow at a 6.98% CAGR through 2031, making it the fastest-expanding service line in the aviation asset management market. Growth in this area reflects the rising use of managed vehicles, co-investment structures, and specialist portfolio mandates rather than simple balance-sheet leasing alone. FTAI Aviation’s USD 2.0 billion Strategic Capital Vehicle is one clear example of how outside capital is being directed into aircraft assets through manager-led structures. End-of-life solutions remain the smallest service category, but their importance is rising as older fleets face increasingly stringent fuel-efficiency and documentation requirements. DLR and NLR published life-cycle assessment guidance in October 2025 that set a clearer framework for dismantling, parts recovery, and recycling decisions. That shift gives the aviation asset management industry a more formal basis for asset retirement planning. It lifts the strategic value of companies that can manage teardown economics and traceable circularity outcomes.

By Aircraft Type: General Aviation Leads as Commercial Segment Builds Momentum

General aviation accounted for 39.87% of the aviation asset management market in 2025, making it the largest aircraft type segment. This position reflects the wide base of business jets, rotorcraft, turboprops, and other aircraft that sit under professional management arrangements. The segment is broad and fragmented, so asset managers often create value through technical oversight, placement expertise, and pooling rather than sheer fleet scale. These portfolios also tend to offer varied lease structures and operating profiles, which makes careful monitoring more important than standardized execution alone. In practice, that gives general aviation a stable role in the aviation asset management market even when commercial fleet cycles become more volatile.

Commercial aviation is projected to grow at a 7.81% CAGR through 2031, making it the fastest-growing aircraft segment. That growth is tied to narrowbody demand, delayed fleet renewal, and the premium placed on newer aircraft that offer lower fuel burn and stronger residual values. Lessors remain focused on these assets because scarcity and airline demand support pricing discipline over long periods. Military aviation and UAV fleet management are smaller in terms of share, but they remain strategically relevant because they expand the scope of services beyond airline-focused leasing. The aviation asset management industry is also starting to prepare for next-generation aircraft classes, where value assessment, maintenance standards, and bankable residual assumptions are not yet fully settled, keeping commercial aircraft at the center of near-term expansion while leaving room for adjacent asset classes to become more material later in the forecast period.

By End-User: Airlines Drive Volume While Investors Expand Reach

Airlines held a 46.29% share in 2025, making them the largest end-user group in the aviation asset management market. Their lead reflects recurring demand for operating leases, lease extensions, technical monitoring, and fleet transition support across mainline, regional, and low-cost operations, making airlines the volume anchor of the aviation asset management market, as their fleets require sourcing, placement, maintenance oversight, and remarketing support. It also reinforces the role of asset managers in balancing airline credit quality with aircraft liquidity and re-leasing flexibility.

Financial institutions and investors are projected to grow at a 6.77% CAGR through 2031, which makes them the fastest-expanding end-user cohort. Their growth reflects a wider shift toward structured participation in aircraft ownership through funds, joint ventures, and specialist management mandates. SMBC Aviation Capital closed GAEL II in August 2025 with 14 Japanese investors and a portfolio of 8 aircraft, while SKY Leasing raised more than USD 1.35 billion for SKY Fund VI in April 2025 with support from insurers, sovereign investors, pension funds, and family offices. These structures let capital providers enter the aviation asset management market without building a full operating platform. MRO providers and leasing companies complete the end-user mix, and their participation is deepening because technical management is increasingly tied to asset performance rather than handled as a separate afterthought.

By Asset Ownership: Leased Aircraft Dominate, Owned Fleet Returns Gaining Ground

Leased aircraft accounted for 42.59% of the aviation asset management market in 2025, making them the largest ownership class. This position aligns with the long-running shift toward operational flexibility and away from full airline ownership. It also reflects how lessors can spread aircraft across multiple operators and preserve placement options when route economics change. BOC Aviation reported full utilization of its owned portfolio in 2025, underscoring the limited idle capacity in the market. Tight supply and strong demand, therefore, continue to support the economic case for leased fleets, especially for airlines that need access to aircraft more than they need permanent ownership.

Owned aircraft portfolios are forecast to grow at a 7.21% CAGR through 2031, which means they are set to outpace the overall aviation asset management market. This growth is tied to lessors and investors securing direct-order positions to capture delivery slot value and reduce dependence on the secondary market. Managed aircraft pools are also becoming more visible as a distinct ownership model, providing outside capital access to the aviation asset management industry through specialist managers. FTAI Aviation’s strategic capital initiative and SMBC Aviation Capital’s third-party management activity both demonstrate how the lines between lessor, fund manager, and asset servicer are becoming less rigid. That shift matters because return expectations now depend not only on lease yield, but also on management fees, portfolio strategy, and exit timing. As a result, ownership structures in the aviation asset management market are becoming more varied, even as leased aircraft remain the largest single category.

Geography Analysis

North America accounted for 40.67% of the aviation asset management market share in 2025, making it the largest regional contributor. The region benefits from deep capital markets, a high concentration of lessors and servicers, and extensive experience in sale-and-leaseback transactions, positioning North America as a strong player in aircraft placement, fleet refinancing, and transaction structuring across a wide range of credits and asset ages. It also supports a large installed base of technical and portfolio management expertise, which keeps the region central to global asset decisions. As a result, North America remains the primary benchmark for pricing discipline and institutional execution across the aviation asset management market.

The Middle East is projected to expand at a 8.58% CAGR through 2031, making it the fastest-growing regional segment. Growth is supported by sovereign-backed platform-building and national aviation strategies that link aircraft ownership, airline expansion, and capital formation. In September 2025, Hassana Investment Company and AviLease formed a dedicated aircraft leasing joint venture in Saudi Arabia, with an initial portfolio of 10 new-technology aircraft. Boeing also expects the Middle East passenger fleet to more than double by 2044, with 2,950 new commercial aircraft required and USD 455 billion in related commercial aviation services. That demand outlook gives the aviation asset management market in the region a long investment runway across leasing, technical support, and portfolio management.

Asia-Pacific remains a major growth engine for the aviation asset management market because traffic growth, airline expansion, and fleet replacement needs remain high across several large economies. The region’s growth profile is especially important for narrowbody demand, which directly supports lessor placement opportunities and long-horizon portfolio planning. Europe remains a mature center of the aviation asset management market, with Dublin and Luxembourg continuing to act as major hubs for operating lease structures, capital raising, and portfolio administration. South America is smaller in scale, yet it highlights how credit-cycle risk can quickly change aircraft values and lease strategies when airline balance sheets weaken. Together, these regions show that the aviation asset management market is being pulled in two directions at once: mature centers are driving structuring depth, while emerging regions are driving fleet growth. That balance favors managers who can move across jurisdictions, credit profiles, and aircraft vintages without losing remarketing flexibility. It also explains why global scale is valuable, but regional execution remains just as important.

Competitive Landscape

The aviation asset management market is moderately concentrated at the top and much more fragmented through the middle tier. The largest global lessors still hold strong positions in new-technology aircraft, funding access, and OEM relationships. At the same time, a much wider group of smaller platforms compete in specific asset classes, geographies, and capital structures. ISTAT noted in 2026 that scale, consolidation, and capital were reshaping the aircraft leasing landscape, which matches the broader direction of the aviation asset management market. That scale gives leading players stronger market presence, better funding terms, and greater flexibility in balancing fleet age, lease duration, and customer exposure.

Consolidation is continuing, which is narrowing the field of large independent platforms and raising the strategic value of scale. One example occurred in March 2026, when Crestone Air Partners acquired Arena Aviation Capital, creating a combined aviation asset manager with more than USD 4 billion in assets under management across 124 aircraft and 17 engines. Another example came in January 2026, when KKR increased its ownership stake in Altavair and deepened a long-running investment relationship in aircraft leasing and lending. A third example came from Saudi Arabia in September 2025, when Hassana and AviLease launched a dedicated leasing joint venture to support domestic and international fleet growth. These moves show that competitive advantage in the aviation asset management market no longer rests solely on fleet count. It increasingly depends on how well a platform can combine capital access, technical capability, and portfolio specialization.

A second layer of competition is developing around asset intelligence, maintenance control, and specialty portfolios. Predictive maintenance tools, tighter lease monitoring, and data-backed residual value work are becoming more important as portfolios age and compliance obligations rise. FTAI Aviation’s USD 2.0 billion strategic vehicle also points to a market where specialist managers can scale by pairing technical asset skills with outside capital rather than relying only on their own balance sheet. The aviation asset management market, therefore, rewards two very different strengths at the same time: one is large-platform funding power, and the other is focused expertise in engines, mid-life aircraft, regional fleets, or end-of-life solutions. That mix keeps the top-tier influential, but it also leaves meaningful room for niche operators that can manage complex assets better than broad-based fleets can. In practical terms, competition is intensifying, but it is doing so through specialization as much as through simple scale.

Aviation Asset Management Industry Leaders

AerCap Holdings N.V.

Avolon Aerospace Leasing Limited

Air Lease Corporation

BOC Aviation Limited

SMBC Aviation Capital Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Crestone Air Partners, a global aviation asset management platform majority owned by Air T, Inc., entered into a definitive agreement to acquire Arena Aviation Capital, an established aviation asset manager with a diversified portfolio and strong airline relationships.

- May 2025: ACIA Aero Leasing delivered the first of two ATR 72-600 aircraft to Emerald Airlines, marking the establishment of a new leasing partnership. The 72-seat aircraft will join Emerald's Dublin-based fleet as part of the airline's expansion strategy.

- March 2025: Singapore-based aircraft leasing firm BOC Aviation ordered 120 narrowbody aircraft from Airbus and Boeing. The company will acquire 70 A320neo family aircraft and 50 B737 MAX 8 aircraft.

- January 2025: Southwest Airlines executed a new sale-and-leaseback package with BBAM, monetizing mature B737-700 assets.

Global Aviation Asset Management Market Report Scope

The aviation asset management market is witnessing growth driven by rising aircraft leasing activity, a growing preference for sale-and-leaseback transactions, and the adoption of predictive maintenance and digital fleet management solutions. Airlines and operators are prioritizing capital optimization and operational flexibility, which is driving demand for professional asset management services across the commercial, military, and general aviation sectors. Additionally, the market is supported by the expansion of aircraft fleets, growing investments from financial institutions, and a heightened focus on sustainable aviation and lifecycle management solutions.

The aviation asset management market is segmented by service type, aircraft type, end user, asset ownership, and geography. By service type, the market encompasses leasing services, technical services, financial and portfolio management, and end-of-life solutions. By aircraft type, the market is divided into commercial aviation, military aviation, general aviation, and unmanned aerial vehicles (UAVs). By end-user, the market covers airlines, leasing companies, MRO providers, and financial institutions and investors. By asset ownership, the market is segmented into owned aircraft, leased aircraft, and managed aircraft pools. The report also covers the market sizes and forecasts for the aviation asset management market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Leasing Services |

| Technical Services |

| Financial and Portfolio Management |

| End-of-Life Solutions |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Fighter Jets |

| Transport Aircraft | |

| Rotorcraft | |

| General Aviation | |

| Unmanned Aerial Vehicles (UAVs) |

| Airlines |

| Leasing Companies |

| MRO Providers |

| Financial Institutions and Investors |

| Owned Aircraft |

| Leased Aircraft |

| Managed Aircraft Pools |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Service Type | Leasing Services | ||

| Technical Services | |||

| Financial and Portfolio Management | |||

| End-of-Life Solutions | |||

| By Aircraft Type | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Fighter Jets | ||

| Transport Aircraft | |||

| Rotorcraft | |||

| General Aviation | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By End-User | Airlines | ||

| Leasing Companies | |||

| MRO Providers | |||

| Financial Institutions and Investors | |||

| By Asset Ownership | Owned Aircraft | ||

| Leased Aircraft | |||

| Managed Aircraft Pools | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current outlook for aviation asset management?

The aviation asset management market was valued at USD 217.83 billion in 2025 and is forecast to reach USD 292.99 billion by 2031, growing at a 5.08% CAGR over 2026-2031.

Which service category leads revenue generation?

Leasing services lead the aviation asset management market with a 43.36% revenue share in 2025, reflecting the importance of operating leases in a supply-constrained fleet environment.

Which aircraft type is growing the fastest through 2031?

Commercial aviation is the fastest-growing aircraft type with a forecast CAGR of 7.81%, supported by strong narrowbody demand and the premium on newer aircraft.

Why are sale-and-leaseback deals so important now?

Airlines are using sale-and-leaseback deals to release capital while keeping aircraft access, and lessors are benefiting from long-term lease income and scarce delivery positions.

Which region offers the strongest growth potential?

The Middle East shows the fastest regional growth with an 8.58% CAGR through 2031, supported by sovereign-backed leasing platforms and long-term fleet expansion plans.

What are the main risks affecting asset values?

The main risks are persistent OEM delivery delays, a firmer funding environment than before 2022, and rising ESG-related pressure on older, less fuel-efficient aircraft.

Page last updated on: