Aviation Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

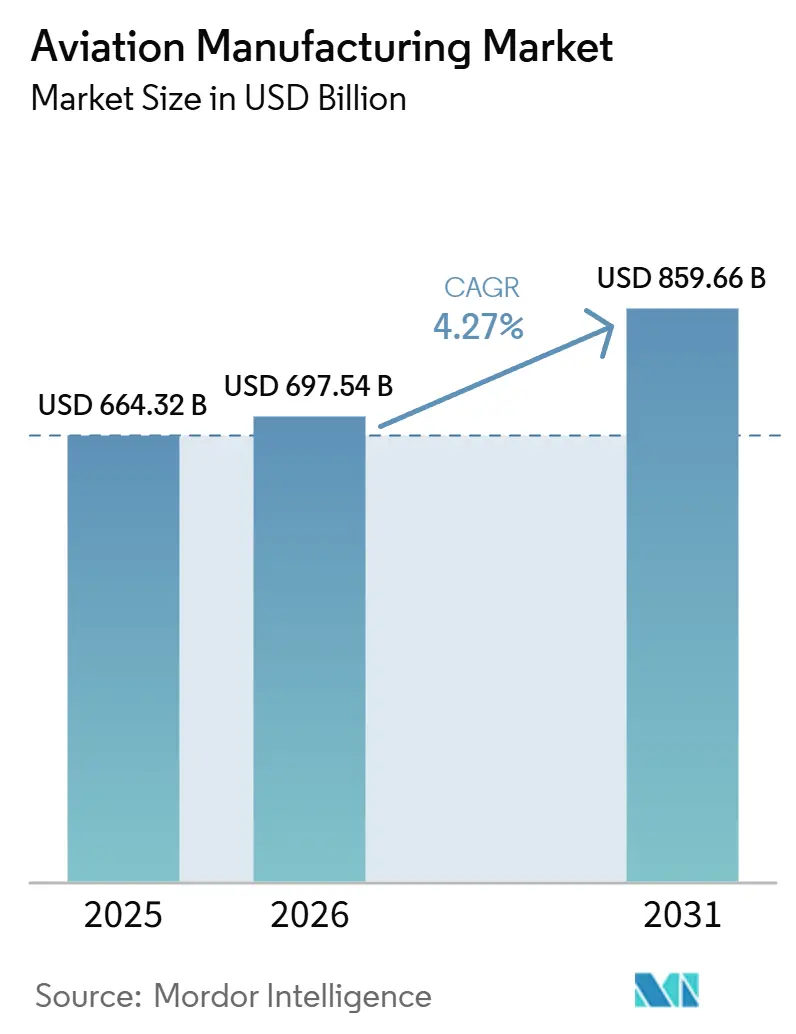

| Market Size (2026) | USD 697.54 Billion |

| Market Size (2031) | USD 859.66 Billion |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Manufacturing Market Analysis by Mordor Intelligence

The aviation manufacturing market size is expected to grow from USD 664.32 billion in 2025 to USD 697.54 billion in 2026 and is forecast to reach USD 859.66 billion by 2031 at a 4.27% CAGR over 2026-2031. Commercial fleet renewal, defense modernization, and wide-ranging digitalization initiatives anchor the near- to mid-term outlook, while additive manufacturing and composite adoption position the sector for longer-run efficiency gains. Airline preference for fuel-efficient narrowbody models sustains high order backlogs and stabilizes production planning despite lingering supply-chain friction. At the same time, North American and European reshoring incentives spur localized component ecosystems that reduce exposure to logistics shocks and geopolitical risk. Intensifying defense spending across NATO and the Indo-Pacific complements civil demand, allowing the aviation manufacturing market to balance cyclical passenger trends with multi-year military procurement cycles.

Key Report Takeaways

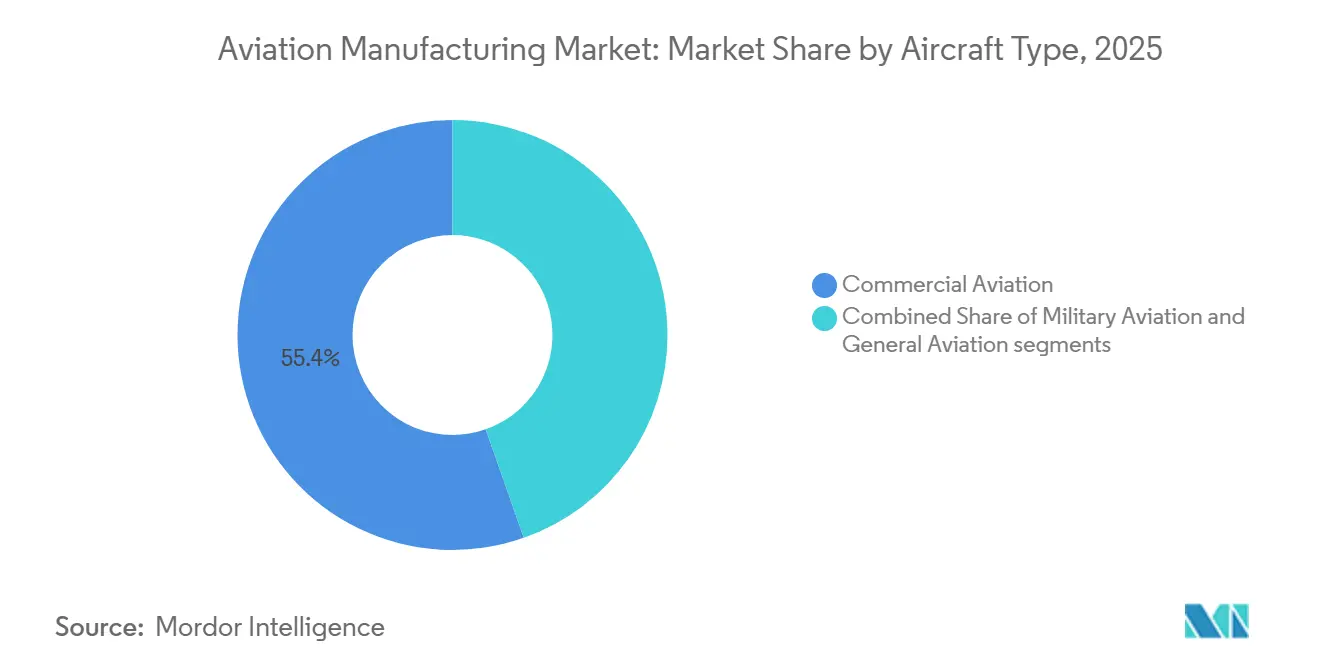

- By aircraft type, commercial aviation platforms captured 55.38% of the aviation manufacturing market share in 2025, while military aviation is advancing at a 6.79% CAGR through 2031.

- By component, airframe structures accounted for 43.58% of the aviation manufacturing market in 2025, and avionics and flight control systems are expanding at a 6.28% CAGR through 2031.

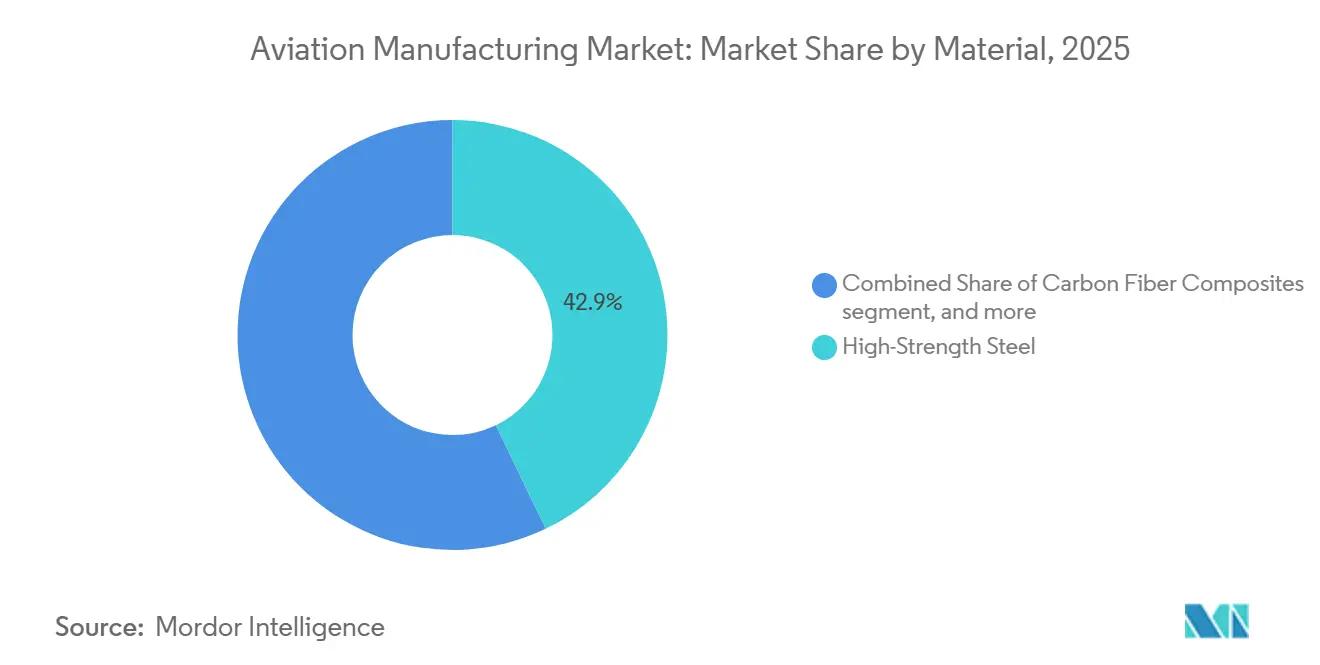

- By material, high-strength steels held 42.87% of the aviation manufacturing market share in 2025; carbon fiber composites are projected to grow at a 7.38% CAGR through 2031.

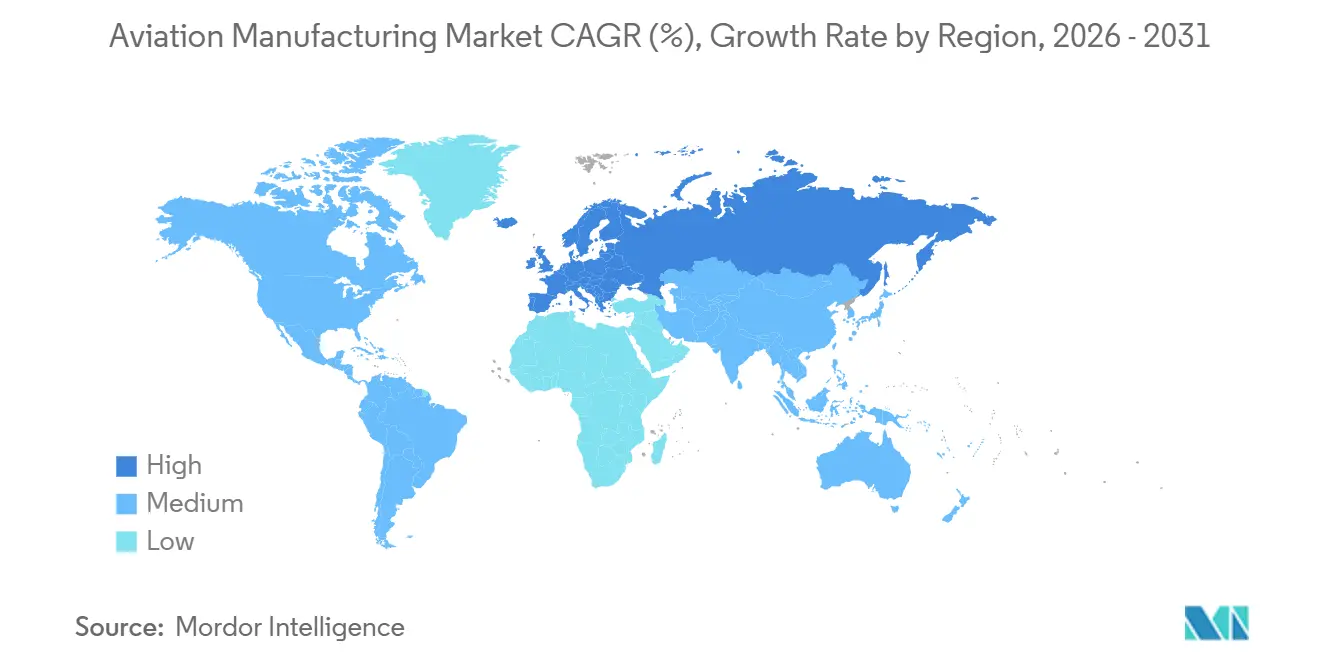

- By geography, North America commanded 40.99% of the aviation manufacturing market size in 2025, whereas Europe is forecasted to post the fastest 5.92% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aviation Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial air travel rebound and fleet expansion | +1.20% | Global, strongest in APAC and North America | Short term (≤ 2 years) |

| Sustained demand for fuel-efficient, next-gen aircraft | +0.80% | Global, led by North America and Europe | Medium term (2–4 years) |

| Defense sector fleet-modernization programs | +1.10% | North America, Europe, Indo-Pacific | Long term (≥ 4 years) |

| Emerging market airline fleet growth | +0.90% | APAC core, spill-over to MEA and Latin America | Medium term (2–4 years) |

| Additive manufacturing adoption for structural parts | +1.40% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| Supply-chain re-shoring incentives in the US/EU | +0.60% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Commercial Air Travel Rebound and Fleet Expansion

Global passenger traffic recovered to 94.10% of 2019 levels by December 2024, prompting carriers to accelerate fleet replacement with newer fuel-efficient jets that cut energy cost exposure while meeting stricter emissions caps.[1]International Air Transport Association, “Air Passenger Market Analysis December 2024,” IATA, iata.org Airlines favor narrowbody families such as the B737 MAX and A320neo, using high-frequency point-to-point networks that boost aircraft utilization and compress unit costs. Low-cost carriers (LCCs) continue to extend service into secondary cities, raising incremental demand for 100–220-seat platforms well-suited to thin routes. Delivery slots remain scarce through the decade, preserving pricing power for prime contractors. These dynamics collectively reinforce the aviation manufacturing market’s short-term growth trajectory.

Defense Sector Fleet-Modernization Programs

Fiscal 2024 US appropriations allocated USD 61.4 billion to aircraft procurement, a 12% uptick that underscores sustained bipartisan support for air-power readiness.[2]U.S. Department of Defense, “Fiscal Year 2024 Budget Request,” comptroller.defense.gov European initiatives such as the Future Combat Air System (FCAS) channel EUR 8 billion (USD 9.36 billion) into collaborative R&D, advancing stealth, sensor fusion, and unmanned teaming capabilities that elevate platform complexity and aftermarket value. Asia-Pacific allies accelerate purchases of multi-role fighters and maritime patrol aircraft to counter evolving security threats. Modernization extends beyond new frames to mid-life avionics, electronic warfare (EW), and propulsion upgrades that lengthen service life and diversify revenue for tier-1 and tier-2 suppliers. The defense contribution provides a strategic buffer, stabilizing the aviation manufacturing market during civil down-cycles.

Additive-Manufacturing Adoption for Structural Parts

General Electric’s LEAP fuel-nozzle success story, reducing 20 subassemblies into a single printed unit, demonstrates additive manufacturing’s cost and weight advantages.[3]GE Aerospace, “Additive Manufacturing Milestone Achievement,” geaerospace.com Prime contractors now pilot 3D-printed brackets, ducts, and control surfaces, trimming raw-material waste and compressing lead times. Regulatory pathways for printed parts have matured, with the FAA and EASA releasing guidance that shortens certification for qualified geometries, which hastens broader deployment. Suppliers can localize production as powder-bed and directed-energy deposition systems scale, mitigating logistics risk and supporting reshoring goals. Over the long term, additive adoption will lift the aviation manufacturing market’s productivity baseline.

Emerging Market Airline Fleet Growth

India’s domestic traffic surged 13.20% in 2024, pushing carriers such as IndiGo to order more than 1,000 jets for delivery through 2030.[4]Directorate General of Civil Aviation India, “Air Transport Statistics 2024,” dgca.gov.in China’s carriers focus on domestic expansion under the dual-circulation strategy, procuring single-aisle aircraft that fit constrained airport slots yet offer high throughput. Middle Eastern hubs exploit geographic neutrality to capture connecting traffic, driving dual demand for narrowbody and widebody fleets that feed sixth-freedom networks. These regions favor simplified cabin layouts and robust on-time performance, encouraging OEMs to refine high-utilization designs. Rising purchasing power in secondary cities extends aviation’s addressable base, enhancing the long-term scale of the aviation manufacturing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile aerospace-grade raw-material prices | -0.70% | Global, highest in North America and Europe | Short term (≤ 2 years) |

| Lengthy certification and regulatory compliance cycles | -0.50% | Global, particularly affecting new entrants | Long term (≥ 4 years) |

| Skilled labor shortages in advanced machining | -0.40% | Global, with notable pressure in North America and Europe | Medium term (2–4 years) |

| Rising cybersecurity compliance costs across digitalized production lines | -0.30% | Global, acute in North American and European tier-2 supplier bases | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Aerospace-Grade Raw-Material Prices

Aluminum spot prices climbed 23% in 2024 amid energy-driven smelting constraints, while titanium supply tightened after sanctions disrupted Russian exports. Prime contractors wield long-term hedges, yet smaller tier-2 vendors face margin compression that forces consolidation or exit. OEMs respond with dual-sourcing, scrap-recycling loops, and design substitutions that cut costly metals by integrating composites where structurally feasible. Dynamic contract escalation clauses have become standard, yet persistent volatility still subtracts near-term growth from the aviation manufacturing market.

Lengthy Certification and Regulatory Compliance Cycles

The 20-month B737 MAX return-to-service review illustrated the rigorous test regimes required for flight-critical systems. Novel propulsion or autonomy solutions confront additional uncertainty because harmonized frameworks remain incomplete across the FAA, EASA, and CAAC. Duplicate documentation, simulator sessions, and flight-test campaigns extend time-to-market by three to five years relative to consumer-product cycles, delaying revenue capture. Emerging entrants with limited capital find these hurdles particularly daunting, damping competitive dynamism inside the aviation manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Commercial Scale Meets Military Momentum

Commercial aviation retained 55.38% of the aviation manufacturing market share in 2025, underscoring its dominance despite lingering international-travel headwinds. Airlines favor narrowbody families such as the B737 MAX and A320neo, which deliver high utilization on point-to-point networks, while cargo conversions add resilience as e-commerce elevates freight yields. Supply-chain tightness around engines and aerostructures continues to cap monthly output, prompting Boeing to integrate Spirit AeroSystems to boost quality control and reduce schedule risk. Widebody demand remains muted because carriers prize capacity flexibility, yet scope-clause relaxations allow larger regional jets to penetrate mainline routes, broadening production runs for secondary OEMs. Heightened regulatory scrutiny after the B737 MAX recertification extends development timelines and strengthens operator confidence through more rigorous validation protocols.

Military aviation is projected to expand at a 6.79% CAGR through 2031 as geopolitical flashpoints in Eastern Europe, the Indo-Pacific, and the Middle East spur fleet-modernization drives that emphasize multi-role versatility Programs such as the F-35, with a lifetime value topping USD 400 billion, channel composite structures, digital flight controls, and fuel-efficient engines from civil platforms into stealth and electronic-warfare applications that redefine air-power doctrine. International cooperation, exemplified by the Future Combat Air System (FCAS), spreads R&D burdens and embeds domestic industrial participation across partner nations. Non-combat assets, including tankers and transports, see steady procurement as logistics resilience becomes a strategic priority. At the same time, export credit support helps prime contractors convert domestic success into foreign military sales. The civil volume of commercial jets and the accelerating defense backlog position the aircraft-type segment as a dual-engine for the aviation manufacturing market growth through the decade.

By Component: Avionics Systems Anchor Digital Migration

Avionics and flight control systems are set to expand at a 6.28% CAGR, outpacing other components as airlines digitize operations and regulators mandate equipment upgrades for air-traffic modernization. Airframe structures accounted for 43.58% of the aviation manufacturing market share in 2025, thanks to continued fuselage and wing demand that scales directly with delivery volume. Engine OEMs navigate a structural shift toward power-by-the-hour agreements, converting upfront sales into recurring service revenue that locks operators into long-term maintenance frameworks.

Cabin interior suppliers redesign galleys and lavatories to minimize touchpoints while preserving density. Environmental control and auxiliary power units (APUs) migrate from pneumatic bleed systems to electrically driven architectures that cut fuel burn. Landing-gear manufacturers harness sensor suites and predictive analytics to optimize overhaul intervals. As operators modernize cockpits with real-time data links and enhanced autopilot functions, avionics revenues climb, deepening the digital transformation sweeping the aviation manufacturing market.

By Material: Composite Uptake Challenges Legacy Alloys

Carbon fiber composites are forecasted to register a 7.38% CAGR as OEMs chase weight savings that translate directly into fuel cost reductions and range extensions. Conventional high-strength steels and allied alloys still represented 42.87% of the aviation manufacturing market share in 2025, a testament to entrenched supply chains, proven machinability, and favorable cost positions for non-primary structures. Aluminum remains the fuselage mainstay due to mature repair ecosystems, while titanium occupies engine hot-section and high-load landing gear niches thanks to superior heat tolerance.

Robotic fiber-placement cells and out-of-autoclave curing processes lower composite part costs, broadening viable use cases beyond wing skins and vertical tails. However, inspection complexity and reparability concerns persist, particularly for lower-tier airlines in emerging regions with limited MRO infrastructure. Recycling solutions such as pyrolysis and chemical depolymerization are advancing in response to growing end-of-life mandates. Material trade-offs will continue to shape design choices, reinforcing the multi-material character of the aviation manufacturing market.

Geography Analysis

North America commanded 40.82% of the aviation manufacturing market share in 2025, sustained by Boeing’s scale, an expansive defense contractor network, and robust MRO capacity. Federal export-credit facilities and foreign-military-sales pipelines elevate international reach, while domestic reshoring incentives support component localization. Canada contributes niche strength in regional aircraft and business jets, led by Bombardier programs that retain loyal customer bases despite competitive stress.

Europe is forecasted to post a 5.92% CAGR through 2031 as Airbus expands single-aisle assembly lines and EU strategic autonomy policies channel R&D funding to indigenous suppliers.[5]European Defence Agency, “Future Combat Air System Programme Milestone,” eda.europa.eu Collaborative defense platforms like the FCAS drive cross-border technology exchange and deepen industrial integration. Germany’s engine competencies, France’s avionics expertise, and Italy’s aerostructures specialization collectively reinforce regional self-sufficiency. The UK leverages global supply links while navigating post-Brexit regulatory divergence.

Asia-Pacific registers the most dynamic absolute demand growth, driven by rising disposable incomes, airport capacity additions, and pro-aviation government policies. China’s domestic network expansion underpins large narrowbody orders, while India’s carriers commit to sizable backlogs, positioning the subcontinent as a future assembly hub. Japan and South Korea sustain high-value subsystem exports, and Singapore consolidates regional MRO leadership. Concurrently, Gulf carriers in the Middle East exploit geographic crossroads positioning, purchasing long-range widebodies and investing in local overhaul centers that feed into the broader aviation manufacturing market ecosystem.

Mordor Intelligence provides coverage of the aviation manufacturing market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Commercial aircraft manufacturing remains a duopoly, with Boeing and Airbus controlling a major share of global large-jet orders. This concentration affords economies of scale and negotiation leverage, yet leaves OEMs vulnerable to certification setbacks or program-specific quality issues. Defense markets are more fragmented: Lockheed Martin, Northrop Grumman, and BAE Systems lead fighter programs, while Embraer, Saab, and Korea Aerospace Industries supply light-attack and trainer niches.

Strategic alliances proliferate as suppliers share R&D risk. Examples include GE and Safran’s CFM partnership for the RISE open-fan demonstrator and Rolls-Royce’s tie-ups with start-ups on hybrid-electric propulsion. Digital twin platforms and predictive maintenance analytics differentiate service offerings, tipping operator preference toward OEMs that guarantee high dispatch reliability. Additive manufacturing, composite mastery, and avionics cybersecurity expertise emerge as competitive vectors shaping procurement decisions. Over time, technology convergence is likely to redraw traditional value-chain boundaries inside the aviation manufacturing market.

Aviation Manufacturing Industry Leaders

Airbus SE

The Boeing Company

Lockheed Martin Corporation

RTX Corporation

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Honeywell expanded its collaboration with PT Garuda Maintenance Facility Aero Asia Tbk (GMF), Indonesia's primary aircraft maintenance, repair, and overhaul (MRO) provider. The expanded partnership includes a three-year APU 131-9A/B and 331-350-part supply program and a three-year flat-rate repair program for the 331-350 APU line-replaceable units (LRUs), provided exclusively to GMF.

- August 2025: RTX's Pratt & Whitney unit received a USD 2.8 billion modified contract for F135 engine production. The contract supports the manufacturing of engines for Lockheed Martin's F-35 jets, serving both the US Joint Strike Fighter (JSF) program and international customers.

- August 2025: LOT Polish Airlines selected Honeywell's advanced avionics systems for its 13 new B737 MAX aircraft. The aircraft will enter service in 2026 and feature Honeywell's technologies to enhance pilot situational awareness and support flight operations.

Global Aviation Manufacturing Market Report Scope

The aviation manufacturing market includes the production of commercial, military, and general aviation aircraft, along with their components and systems. The market benefits from a geographically diversified demand in Europe and the Asia-Pacific.

The aviation manufacturing market is segmented by aircraft type, component, material, and geography. By aircraft type, the market is segmented into commercial aviation, military aviation, and general aviation. By component, the market is segmented into airframe structures, propulsion systems, avionics and flight control systems, cabin and interior modules, landing gear and actuation, and other components. By material, the market is segmented into aluminum alloys, carbon fiber composites, titanium alloys, high-strength steel, and other materials. The report also covers the market sizes and forecasts for the aviation manufacturing market in major countries across different regions. For each segment, the market size and forecast are provided in terms of value (USD).

| Commercial Aviation | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| Military Aviation | Combat Aircraft |

| Non-Combat Aircraft | |

| Helicopters | |

| General Aviation | Business Jets |

| Turboprop Aircraft | |

| Piston Aircraft | |

| Helicopters |

| Airframe Structures |

| Propulsion Systems |

| Avionics and Flight Control Systems |

| Cabin and Interior Modules |

| Landing Gear and Actuation |

| Other Components |

| Aluminum Alloys |

| Carbon Fiber Composites |

| Titanium Alloys |

| High-Strength Steels |

| Other Materials |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Commercial Aviation | Narrowbody Aircraft | |

| Widebody Aircraft | |||

| Regional Jets | |||

| Military Aviation | Combat Aircraft | ||

| Non-Combat Aircraft | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Turboprop Aircraft | |||

| Piston Aircraft | |||

| Helicopters | |||

| By Component | Airframe Structures | ||

| Propulsion Systems | |||

| Avionics and Flight Control Systems | |||

| Cabin and Interior Modules | |||

| Landing Gear and Actuation | |||

| Other Components | |||

| By Material | Aluminum Alloys | ||

| Carbon Fiber Composites | |||

| Titanium Alloys | |||

| High-Strength Steels | |||

| Other Materials | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current valuation of the aviation manufacturing market?

The aviation manufacturing market size is expected to grow from USD 664.32 billion in 2025 to USD 697.54 billion in 2026 and is forecast to reach USD 859.66 billion by 2031 at a 4.27% CAGR over 2026-2031.

Which aircraft category dominates current production?

Commercial aviation jets hold 55.38% market share due to high-frequency, fuel-efficient route structures favored by airlines.

Which segment shows the fastest growth potential through 2031?

Military aviation is projected to expand at a 6.79% CAGR on the back of heightened defense spending.

How fast are avionics and flight control systems expected to grow?

They are set to rise at a 6.28% CAGR, supported by mandatory digital upgrades and autonomous flight initiatives.

Which region is increasing its market weight most rapidly?

Europe is projected to post the fastest 5.92% CAGR as Airbus expands capacity and EU funding drives aerospace autonomy.

What strategic trend is reshaping component sourcing?

US and EU reshoring incentives are encouraging suppliers to localize production, reducing logistics risk and improving responsiveness.

Page last updated on: