Green Airport Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.87 Billion |

| Market Size (2030) | USD 10.13 Billion |

| Growth Rate (2025 - 2030) | 11.54% CAGR |

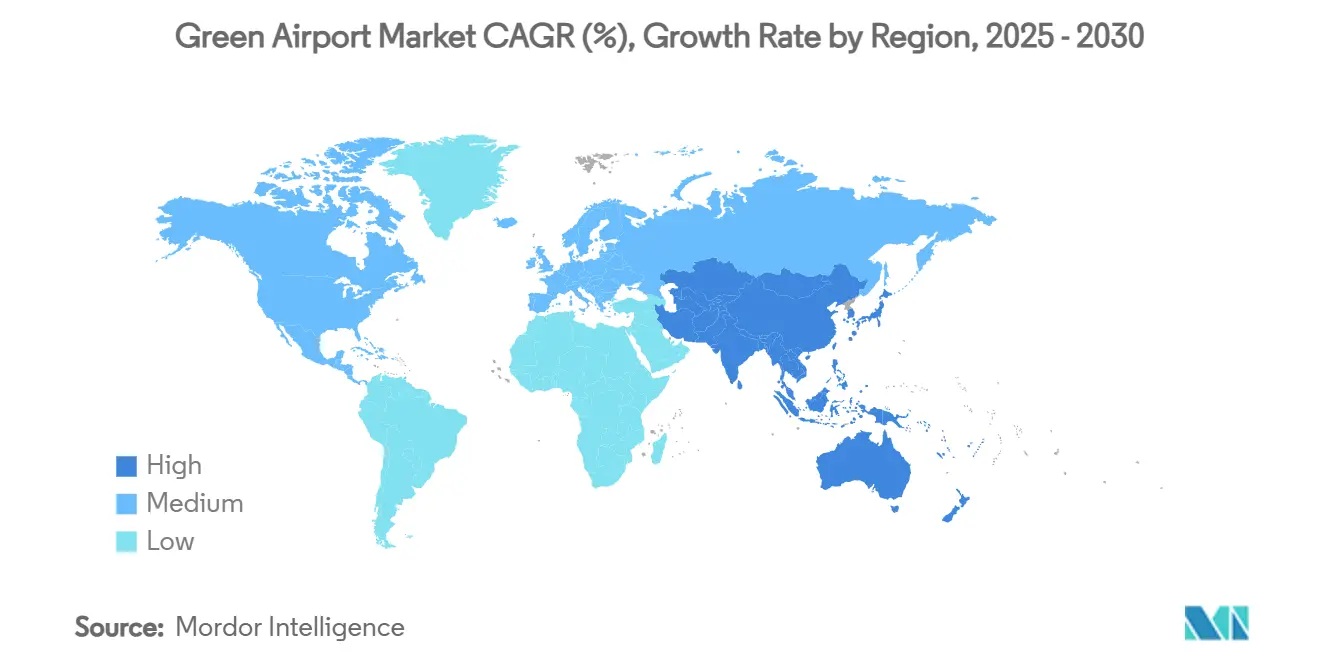

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

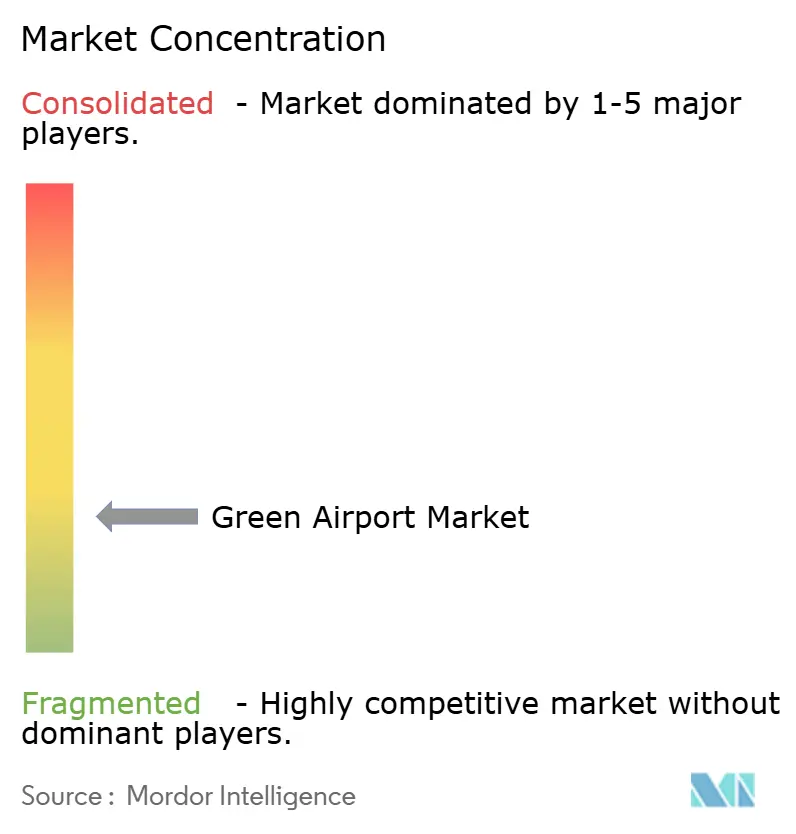

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green Airport Market Analysis by Mordor Intelligence

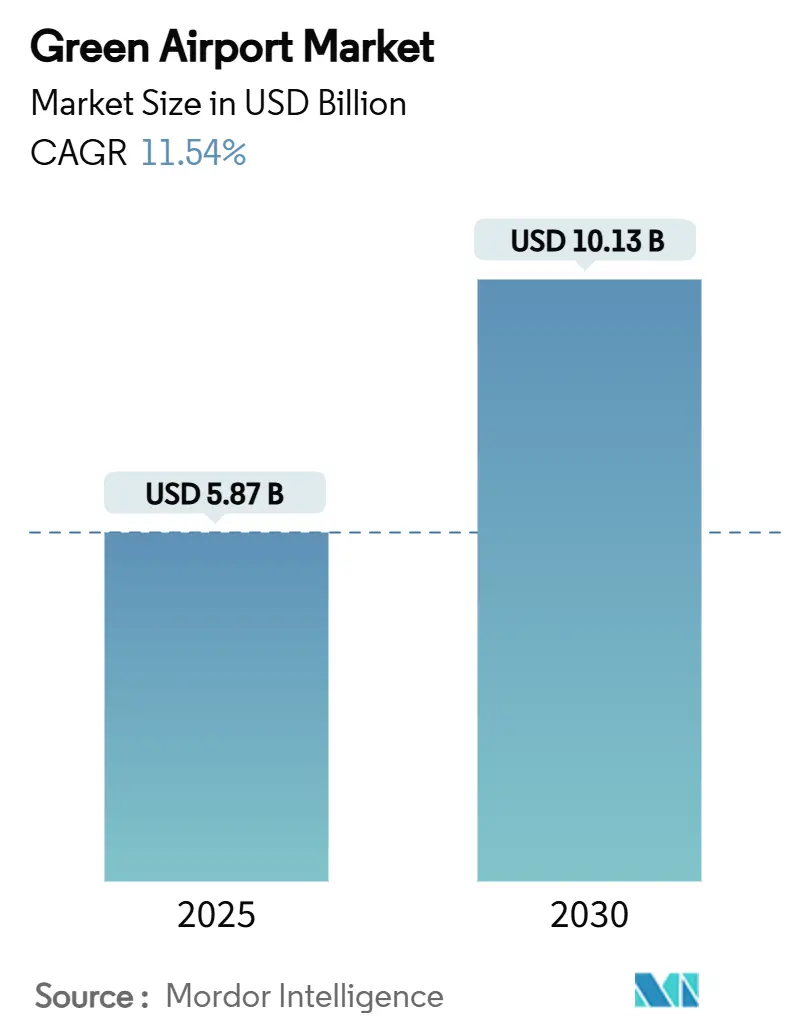

The green airport market size stands at USD 5.87 billion in 2025 and is forecasted to reach USD 10.13 billion in 2030, translating into an 11.54% CAGR. Growth stems from airports’ accelerated push toward net-zero operations, tighter global emissions rules, and expanding capital flows into on-site renewable energy projects. Large-scale redevelopment programs—such as the USD 19 billion upgrade at John F. Kennedy International Airport incorporating a 12 MW microgrid—signal how infrastructure spending is redirected toward clean-energy assets. Solar photovoltaic installations dominate present deployments, yet investment is quickly widening to storage, hydrogen, and advanced energy-management platforms that improve resiliency and reduce operating costs. Airport operators increasingly treat electricity generation as a new revenue line, selling excess power to local grids and hedging against volatile utility prices. Suppliers offering modular, rapidly deployable technologies now enjoy a first-mover advantage because mid-sized and regional airports need cost-effective retrofits that minimise service disruption.

Key Report Takeaways

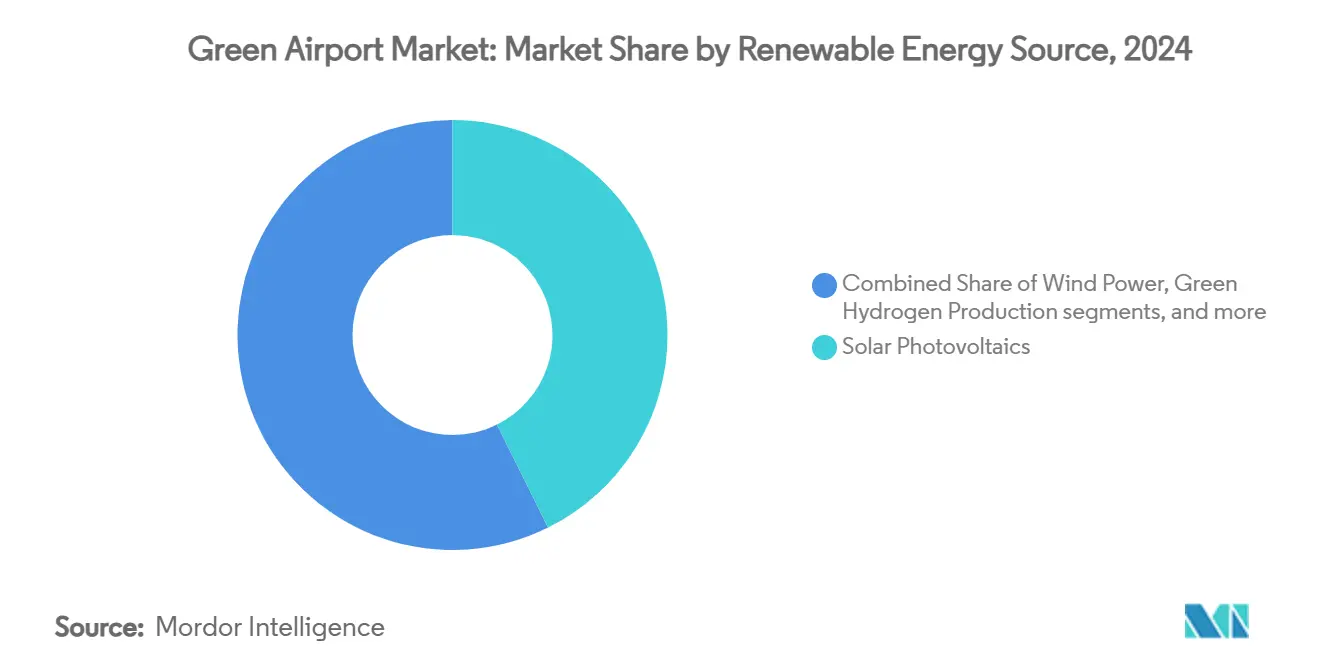

- By renewable energy source, solar photovoltaics (PV) led with 42.67% of the green airport market share in 2024, while green hydrogen production is projected to expand at an 18.95% CAGR through 2030.

- By infrastructure, solar-plus-storage systems commanded 29.78% share of the green airport market size in 2024; hydrogen refuelling and cryogenic storage infrastructure is advancing at an 18.26% CAGR to 2030.

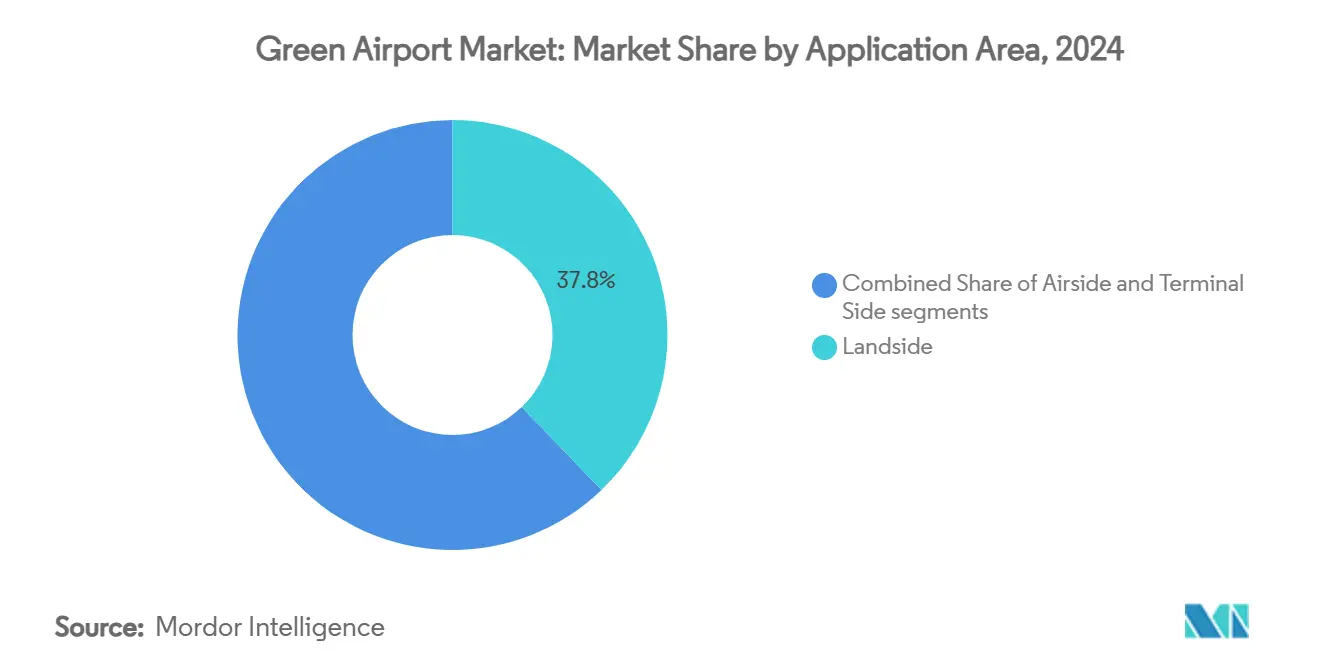

- By application area, landside facilities accounted for 37.81% of the green airport market size in 2024, whereas airside solutions are rising fastest at a 14.12% CAGR through 2030.

- By airport size, large hubs held 51.20% of the green airport market share in 2024, yet small airports recorded the strongest 13.01% CAGR due to incentive-backed modular packages.

- By geography, North America controlled 31.54% of the green airport market size in 2024; Asia-Pacific is anticipated to progress at a 15.22% CAGR to 2030 on the back of 575 ongoing airport projects.

Global Green Airport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening international emissions standards for aviation infrastructure | +2.2% | Global; early adoption in EU and North America | Medium term (2-4 years) |

| Increasing capital allocation toward renewable energy projects at airports | +1.8% | North America and EU leading; APAC accelerating | Long term (≥ 4 years) |

| Accelerated deployment of electric ground support equipment (eGSE) | +1.5% | Global; strongest in mature markets | Short term (≤ 2 years) |

| Expansion of sustainable aviation fuel (SAF) production and distribution networks | +1.2% | North America and EU core; spill-over to APAC | Medium term (2-4 years) |

| Development of on-site green hydrogen production and refueling facilities | +0.9% | APAC and Middle East leading; EU following | Long term (≥ 4 years) |

| Integration of AI-driven energy-management systems across airport operations | +0.7% | Global; early use in smart-city hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening International Emissions Standards for Aviation Infrastructure

The Second Edition of Annex 16 Volume IV, effective January 2024, obliges airports to implement emissions-cutting upgrades that cannot be met by operational tweaks alone. European ReFuelEU rules that mandate 2% sustainable aviation fuel from 2025 trigger comprehensive overhauls of fuel-handling, storage, and power systems. Operators find compliance more economical when folded into integrated sustainability plans rather than ad-hoc retrofits, spurring larger bundled contracts. Because the standards cover all international gateways, airports in emerging economies must modernise to preserve route rights, creating fairly uniform demand for scalable solutions. Technology vendors that offer turnkey packages and proven payback profiles now see shorter sales cycles as regulatory certainty rises.

Increasing Capital Allocation to Renewable Energy Projects at Airports

Airport boards increasingly view on-site renewables as profit centres. In sunny regions, airport solar farms often reach internal rates of return above 50% even without subsidies. VINCI Airports has already hit 75% renewable electricity across its portfolio and sells surplus power to local utilities, proving that clean-energy assets can bolster non-aeronautical revenue streams.[1]VINCI Concessions, “2023-2024 Activity Report,” vinci-concessions.com Updated Federal Aviation Administration land-use rules, effective May 2024, remove lengthy approval hurdles, cutting project lead times and lowering soft costs. With clearer permitting pathways and rising investor appetite for green infrastructure notes, the pool of available capital has broadened, making multi-megawatt projects viable at secondary and tertiary airports.

Accelerated Deployment of Electric Ground Support Equipment (eGSE)

Electric baggage tractors and belt loaders now post total ownership costs 40–60% lower than diesel versions, which shifts the primary adoption driver from compliance to pure economics. Service firms such as Swissport have mandated electric-only purchases from 2025, underscoring an industry consensus that performance thresholds have been met. Once a limiting factor, range has improved with next-generation lithium-iron-phosphate batteries, while standardised charging interfaces simplify fleet integration. Early adopters like Long Beach Airport have crossed 80% eGSE penetration and reported lower maintenance downtime. Autonomous electric dollies now piloted in Cincinnati demonstrate how electrification creates a platform for further operational innovation.

Expansion of Sustainable Aviation Fuel (SAF) Production and Distribution Networks

The global SAF capacity was announced to hit 17.3 million tons, which aligns with the projected demand of 16.1 million tons driven by regulatory mandates. Due to federal incentives, the United States expects daily output to climb from 2,000 to nearly 30,000 barrels by the end of 2024. Airports must therefore invest in specialised storage, blending, and quality-assurance systems so that multiple feedstock pathways can coexist safely. Long-term offtake agreements, such as Air France-KLM’s 1.5 million-ton supply deal, provide bankers with revenue certainty, unlocking project finance for integrated SAF terminals. Regional production hubs reduce transport costs and bolster supply-chain resilience, adding another tailwind for infrastructure roll-outs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Significant capital requirements for retrofitting existing airport infrastructure | −1.4% | Global; highest in mature markets | Short term (≤ 2 years) |

| Grid capacity constraints and limited on-site energy storage capabilities | −1.1% | Primarily APAC and developing markets | Medium term (2-4 years) |

| Supply-chain vulnerabilities in critical minerals for clean-energy tech | −0.8% | Global; risk concentrated in China-dependent chains | Long term (≥ 4 years) |

| Limited land availability for large-scale solar and hydrogen deployments | −0.6% | Dense urban hubs in developed nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Significant Capital Requirements for Retrofitting Existing Airport Infrastructure

Comprehensive decarbonization can entail hundreds of millions of dollars per hub. Dallas–Fort Worth’s USD 10 million outlay on electric central-plant equipment is a fraction of its wider net-zero roadmap, highlighting the sheer sums involved. Maintaining continuous operations during construction often necessitates temporary systems that boost project budgets by up to 30%. Small and mid-sized airports, which lack bond-market access, must rely on public-private partnerships and energy-as-a-service contracts that require sophisticated risk-allocation clauses. The complexity of structuring these deals slows the pace of upgrades and can leave airports dependent on ageing carbon-intensive assets for longer than planned.

Grid Capacity Constraints and Limited On-Site Energy Storage Capabilities

Airport electrification could nearly double peak power draw by 2030, putting pressure on local utilities and interconnection queues. Long-duration storage remains costly; studies in California show 100-hour systems still need sizable price drops before they become cost-effective. Approval backlogs frequently delay projects by more than a year, compelling airports to oversize on-site generation as a hedge, which pushes capex higher. Advanced energy-management platforms that juggle solar, storage, and grid imports are gaining traction, but they add another layer of integration expense that can strain already tight budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Renewable Energy Source: Solar PV Dominance Drives Infrastructure Evolution

Solar photovoltaic installations captured 42.67% of the green airport market share in 2024, securing their position as the baseline technology for airport sustainability programs. Rapid cost declines and predictable performance outputs make PV arrays the first choice for sites with ample roof or land availability. Hydrogen is currently a niche and is projected to expand at an 18.95% CAGR by 2030 as airports prepare for hydrogen-powered aircraft and zero-emission ground fleets.

The green airport market is shifting from single-source projects to hybrid systems where PV provides daytime power, batteries manage peak shaving, and electrolyzers convert surplus into hydrogen for mobility. Pittsburgh International Airport’s USD 1.5 billion integrated hydrogen and SAF complex highlights how hubs can evolve into regional energy anchors. Wind remains limited by height and wake-vortex constraints, whereas waste-heat recovery and bio-energy thrive at mega-hubs with large organic waste streams. Airports without sufficient land sign power-purchase agreements for off-site renewables as an interim compliance measure until on-site technology matures.

By Infrastructure: Storage Systems Enable Grid Independence

Solar-plus-storage solutions accounted for 29.78% of the green airport market size in 2024, underscoring how batteries have become centrepieces of resiliency planning. Electrochemical storage flattens load curves, buffers grid fluctuations, and offers black-start capability critical for safety-of-life operations. Hydrogen refuelling and cryogenic storage infrastructure shows the fastest 18.26% CAGR because airports want to future-proof for hydrogen aircraft while immediately serving fuel-cell buses and logistics vehicles.

Airports are layering innovative building systems, LED retrofits, and advanced HVAC automation on top of foundational energy assets to capture quick wins. JFK’s 12 MW microgrid demonstrates the integrated approach: solar on rooftops, batteries in basements, and fuel-cell support for redundancy. Electric ground-power units and taxi-assist systems are emerging categories that promise further peak-load reductions once commercialised at scale, giving airports additional levers to curtail grid dependence.

By Application Area: Airside Electrification Accelerates Operations Transformation

Landside facilities represented 37.81% of the green airport market size in 2024, covering passenger EV charging, terminal lighting, and parking-garage PV canopies. However, airside projects—electric baggage tugs, eGPUs, and charging pads—are growing fastest at 14.12% CAGR because they cut emissions directly where aircraft operate.

Terminal-side investments in AI-enabled energy management can trim HVAC consumption by up to 25%, as validated by BrainBox AI deployments now integrated into Trane’s portfolio. Copenhagen Airport’s Total Airport Management platform illustrates how digital twins and predictive analytics stretch efficiency gains across stand allocation, gate turnaround, and building systems. As autonomous eGSE matures, airside electrification will compound emissions savings and tighten turnaround times.

By Airport Size: Small Airports Drive Modular Solution Adoption

Large hubs held 51.20% of the green airport market share in 2024, benefitting from scale economies and diversified revenue streams that fund multi-year decarbonization journeys. Yet small airports clock the highest 13.01% CAGR because modular solar, containerised battery units, and prefabricated hydrogen stations drastically lower entry barriers.

Government grants and feed-in tariffs tilt project economics in favour of regional airports, allowing them to leapfrog older hub architectures. Vendors are shipping plug-and-play microgrids that can be installed in months without extensive civil works. This democratisation has started rebalancing supplier focus: product catalogues now feature smaller capacity brackets, service contracts scaled to limited staff, and financing bundles that match lower aeronautical fee bases.

Geography Analysis

North America led with 31.54% of the green airport market size in 2024, buoyed by USD 297 million in Inflation Reduction Act grants and the FAA CLEEN program’s emissions-reduction incentives.[2]ICAO Environment Regional Seminar, “Decarbonization Investments,” icao.int Mature infrastructure simplifies retrofits, while established public-private finance vehicles accelerate project execution. Milestones include JFK’s rooftop solar array and Dallas–Fort Worth’s net-zero central-utility plant, which serve as demonstration sites for other regions.

Asia-Pacific posts the quickest 15.22% CAGR, spurred by 575 active airport developments worth USD 488 billion that embed sustainability features from the blueprint phase. Singapore’s Changi T5, budgeted at USD 10 billion, integrates district cooling, onsite renewables, and SAF logistics to handle a forecast surge in passenger traffic. China’s study of 239 airports identified 2.5 GW photovoltaic potential, while India commissioned the world’s first airport green hydrogen plant at Cochin, showcasing regional innovation appetite.

The Green Deal and Airport Carbon Accreditation framework make Europe an influential player. More than 90 airports have pledged net-zero targets by 2030, and new Level 4/4+ criteria mandate detailed decarbonization roadmaps. VINCI Airports already sources 75% renewable electricity for its European network, and mandates such as ReFuelEU Aviation push demand for SAF pipelines, blending stations, and quality labs.

South America and the Middle East and Africa regions are nascent but show growing intent. Brazil’s concession model lets private operators recoup renewable investments through longer lease tenures, while Gulf airports explore large-scale solar canopy systems that double as shade structures for passenger parking.

Competitive Landscape

The green airport industry features a moderately fragmented field where industrial automation giants, energy specialists, and operators converge. Siemens, Honeywell International Inc., and ABB bundle IoT sensors, control software, and power hardware into holistic platforms that balance on-site generation, storage, and building loads.[3]Siemens, “Energy Efficiency Retrofit for UAE Government Buildings,” siemens.com Airport operators like VINCI and Fraport move upstream by owning solar farms and energy-storage assets, thereby internalising margins and locking supply security.

Smaller innovators target niche pain points. BrainBox AI’s autonomous HVAC algorithms earned a 25% energy-savings record, prompting acquisition by Trane to enrich its portfolio. Hardware start-ups offering autonomous electric dollies, high-power airside chargers, or modular electrolyzers attract venture funding as airports look for turnkey modules. Traditional utilities enter the space via microgrid EPC contracts, seeking to monetise redundant capacity and grid-services revenue.

Strategic partnerships dominate recent deal flow. Honeywell’s methanol-to-jet agreement with Power2X signals a pivot toward eFuels infrastructure in major maritime and aviation hubs. ABB’s alliance with Charbone Hydrogen points to a systematic rollout of modular green hydrogen plants across North America, linking airports with trucking corridors and industrial parks. As regulations tighten and technology converges, the next competitive battleground will likely focus on integrated energy-as-a-service offerings that transfer capex risk away from airport balance sheets.

Green Airport Industry Leaders

Siemens AG

Honeywell International Inc.

VINCI Airports

ABB Group

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: The Port Authority of New York and New Jersey began constructing JFK Airport’s 12 MW microgrid, which features 13,000 rooftop panels and is the most extensive US airport solar array.

- August 2024: King Salman International Airport Development Company appointed Jacobs to deliver design services for Riyadh's new airport project. The 57-square-kilometer master plan includes six parallel runways, terminal facilities, and surrounding real estate developments. The project emphasizes sustainable operations through low-carbon design and renewable energy integration and targets LEED Platinum certification.

Global Green Airport Market Report Scope

| Solar Photovoltaics |

| Wind Power |

| Bio-energy and Waste-Heat Recovery |

| Green Hydrogen Production |

| Grid-Supplied Renewable Electricity |

| Airport Solar Generation and Storage Systems |

| Electric Ground-Support Equipment |

| Smart Building and LED-Lighting Systems |

| Sustainable Aviation-Fuel Supply Infrastructure |

| Hydrogen Refueling and Cryogenic Storage |

| Electric Taxiing and eGPU Systems |

| Landside |

| Airside |

| Terminal Side |

| Large |

| Medium |

| Small |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Switzerland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Renewable Energy Source | Solar Photovoltaics | ||

| Wind Power | |||

| Bio-energy and Waste-Heat Recovery | |||

| Green Hydrogen Production | |||

| Grid-Supplied Renewable Electricity | |||

| By Infrastructure | Airport Solar Generation and Storage Systems | ||

| Electric Ground-Support Equipment | |||

| Smart Building and LED-Lighting Systems | |||

| Sustainable Aviation-Fuel Supply Infrastructure | |||

| Hydrogen Refueling and Cryogenic Storage | |||

| Electric Taxiing and eGPU Systems | |||

| By Application Area | Landside | ||

| Airside | |||

| Terminal Side | |||

| By Airport Size | Large | ||

| Medium | |||

| Small | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Switzerland | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the green airport market?

The green airport market size is USD 5.87 billion in 2025 and is projected to reach USD 10.13 billion by 2030, translating to an 11.54% CAGR.

Which region leads the green airport market today?

North America leads with 31.54% market share thanks to supportive federal funding and mature retrofit frameworks.

Which renewable technology holds the highest share in airport deployments?

Solar photovoltaic systems accounted for 42.67% of installations and serve as the core platform for many airport energy programs.

Why are small airports growing faster than larger hubs?

Modular microgrids, simplified financing packages, and targeted government incentives allow small airports to adopt green technologies quickly, delivering a 13.01% CAGR.

How fast is hydrogen infrastructure growing at airports?

Hydrogen refuelling and cryogenic storage infrastructure is expanding at an 18.26% CAGR due to preparations for hydrogen-powered aircraft and fuel-cell ground fleets.

What is the most significant restraint on green airport development?

High upfront capital for retrofitting existing terminals slows progress, especially at mid-sized airports without easy access to bond financing.

Page last updated on: