Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

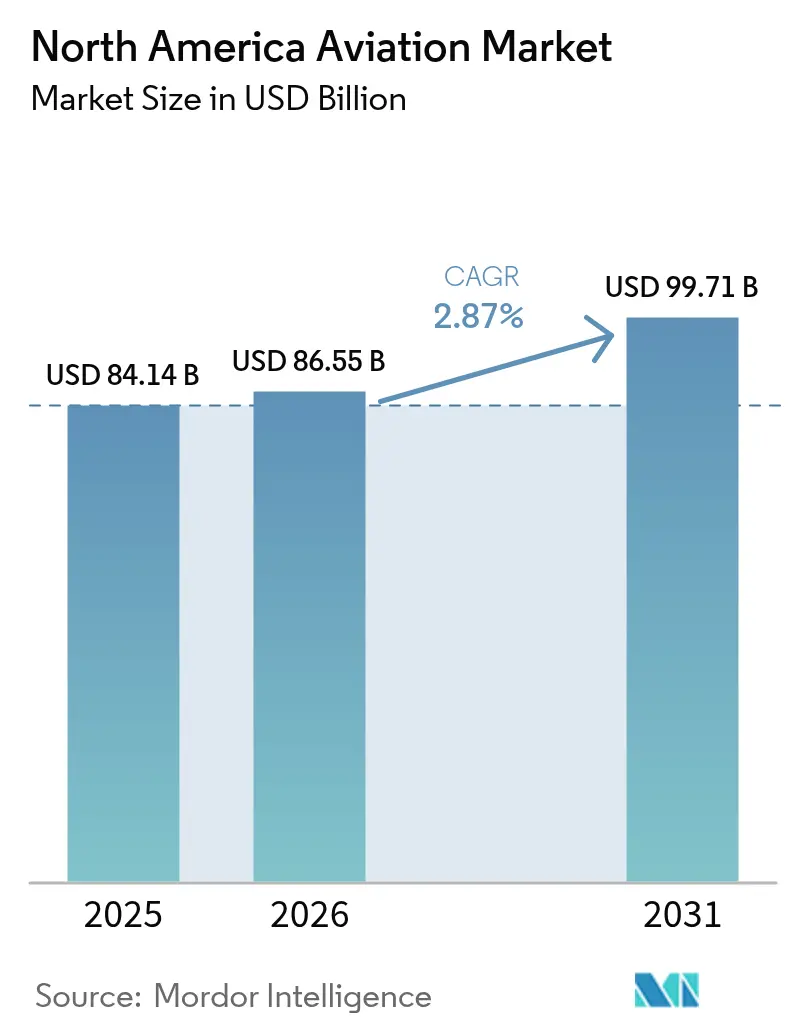

| Base Year Market Size (2025) | USD 84.14 Billion |

| Market Size (2026) | USD 86.55 Billion |

| Market Size (2031) | USD 99.71 Billion |

| Growth Rate (2026 - 2031) | 2.87% CAGR |

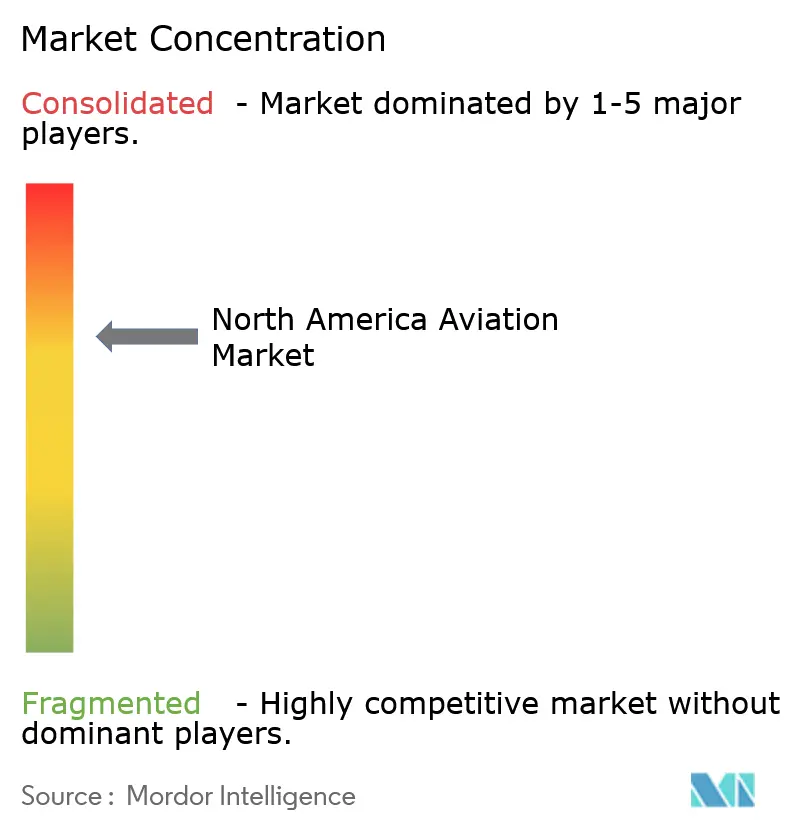

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Aviation Market Analysis by Mordor Intelligence

The North America Aviation Market size is expected to grow from USD 84.14 billion in 2025 to USD 86.55 billion in 2026 and is forecast to reach USD 99.71 billion by 2031 at 2.87% CAGR over 2026-2031.

The North America aviation landscape is experiencing a significant transformation with the rise of low-cost carriers (LCCs) and ultra-low-cost carriers (ULCCs), which are fundamentally reshaping traditional airline business models. These carriers have successfully democratized air travel by offering competitive fares and expanding accessibility to a broader customer base. However, the industry faces operational challenges as fuel costs continue to impact profitability, with fuel surcharges adding between USD 600 to over USD 1,000 per hour depending on aircraft types and fuel price fluctuations. This cost pressure has forced companies to either transfer expenses to consumers through increased trip costs or accept reduced profit margins, creating a delicate balance between market growth and operational sustainability.

The region's aviation infrastructure is undergoing substantial modernization, particularly evident in major hub airports across the United States and Canada. Airports such as Los Angeles International Airport, Chicago's O'Hare Airport, and John F. Kennedy International Airport are at the forefront of infrastructure investments, focusing on increasing passenger handling capacity and implementing smart airport solutions. These modernization efforts are addressing operational inefficiencies, passenger congestion, and access challenges that have historically impacted the passenger experience in several North American airports.

The industry is witnessing a significant shift toward innovative aviation technology and manufacturing processes, with aircraft OEMs heavily investing in research and development. The focus has intensified on developing advanced materials, implementing additive manufacturing techniques, and exploring electric architecture solutions. This technological evolution extends to the integration of Big Data analytics and advanced maintenance techniques, aimed at reducing operational costs and improving efficiency. The industry's commitment to innovation is particularly evident in the urban air mobility sector, where major airlines are investing in electric vertical takeoff and landing (eVTOL) vehicles and related infrastructure.

The North American aviation sector is increasingly prioritizing sustainability initiatives and environmental responsibility. Aircraft manufacturers are exploring alternative fuel solutions and developing more fuel-efficient aircraft designs to reduce environmental impact. The industry is also witnessing a growing emphasis on electric and hybrid propulsion systems, particularly in the general aviation segment. This sustainability focus is complemented by the modernization of aviation infrastructure, with many facilities implementing green building practices and renewable energy solutions in their expansion projects. These environmental considerations are becoming central to strategic planning across the industry, influencing everything from aircraft design to operational procedures.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Aviation Market Trends and Insights

Growth in the Defense Expenditures of the Countries in the Region

The robust defense aviation spending in North America, particularly by the United States, continues to be a major driver for the military aviation market. The United States has maintained its position as the world's largest defense spender, with military expenditure reaching USD 916 billion in 2023, representing approximately 37% of global defense spending. This substantial investment has enabled the country to pursue ambitious aircraft procurement and fleet modernization programs across its military branches. The US Marine Corps' comprehensive fleet renewal initiative, which includes plans to acquire approximately 340 F-35B and 80 F-35C models to replace aging AV-8B Harrier II and F/A-18 Hornet jets, demonstrates the significant impact of defense spending on aviation demand.

The commitment to military aviation advancement is further evidenced by recent strategic acquisitions and modernization efforts. In April 2024, the United States made a significant purchase of 81 Soviet-era fighter and bomber planes from Kazakhstan, including MiG-31 interceptors, MiG-27 fighter bombers, MiG-29 fighters, and Su-24 bombers. This acquisition, part of a larger auction of 117 military aircraft, reflects the ongoing investment in expanding and diversifying the military aircraft fleet. The sustained high levels of defense expenditure enable the procurement of sophisticated military aircraft and support continuous research and development in advanced aviation technologies, ensuring the region maintains its technological edge in military aviation.

Understand The Key Trends Shaping This Market

Download PDF

Airline Fleet Expansion Plans Will Drive the Market in the Coming Years

The ambitious fleet expansion and modernization plans of major North American airlines are serving as a significant catalyst for market growth. As of August 2023, the region's airlines had placed substantial orders with major manufacturers, with expectations of 1,474 Boeing and 986 Airbus aircraft deliveries. These large-scale orders reflect the airlines' commitment to fleet renewal and expansion, driven by the need for more fuel-efficient aircraft and increased capacity to meet growing travel demands. The trend is exemplified by recent developments such as Delta Air Lines' January 2024 order for 20 A350-1000 planes, adding to their existing fleet of over 450 Airbus aircraft and more than 200 pending orders.

The expansion plans extend beyond passenger airlines to include cargo operators, demonstrating the broad-based nature of fleet modernization efforts. United Parcel Service's announcement in June 2023 to expand its fleet by 55 aircraft within two years, including eight B777F aircraft between 2023 and 2025, highlights the comprehensive nature of aviation market growth. These expansion initiatives are driven by multiple factors, including the need for fuel-efficient aircraft, fleet modernization requirements, and the industry's commitment to achieving zero emissions by 2050. The substantial backlog of aircraft orders and ongoing fleet renewal programs indicate a sustained demand for new aircraft, supporting long-term market growth.

Growth in HNWI and UHNWIs in the Region

The significant presence and continued growth of High-Net-Worth Individuals (HNWIs) and Ultra-High-Net-Worth Individuals (UHNWIs) in North America is driving substantial demand in the aerospace market, particularly in the business aviation sector. North America maintains its position as the region with the largest concentration of UHNWIs, hosting over 230,000 such individuals who frequently utilize private aviation services for both business and personal travel. This wealthy demographic's preference for private aviation is driven by factors such as time efficiency, schedule flexibility, and access to a broader network of destinations, contributing to sustained demand for business jets and related aviation services.

The influence of HNWIs and UHNWIs extends beyond direct aircraft ownership to include various forms of aviation service utilization, such as fractional ownership programs and charter services. These individuals' global lifestyle requirements and business interests necessitate extensive air travel capabilities, making them active participants in the aviation market. Their demand for sophisticated, technologically advanced aircraft with superior comfort and performance capabilities continues to drive innovation and development in the business aviation sector. The presence of this wealthy customer base has encouraged manufacturers to develop new aircraft models and enhance existing ones with advanced features and capabilities, further stimulating market growth.

Segment Analysis

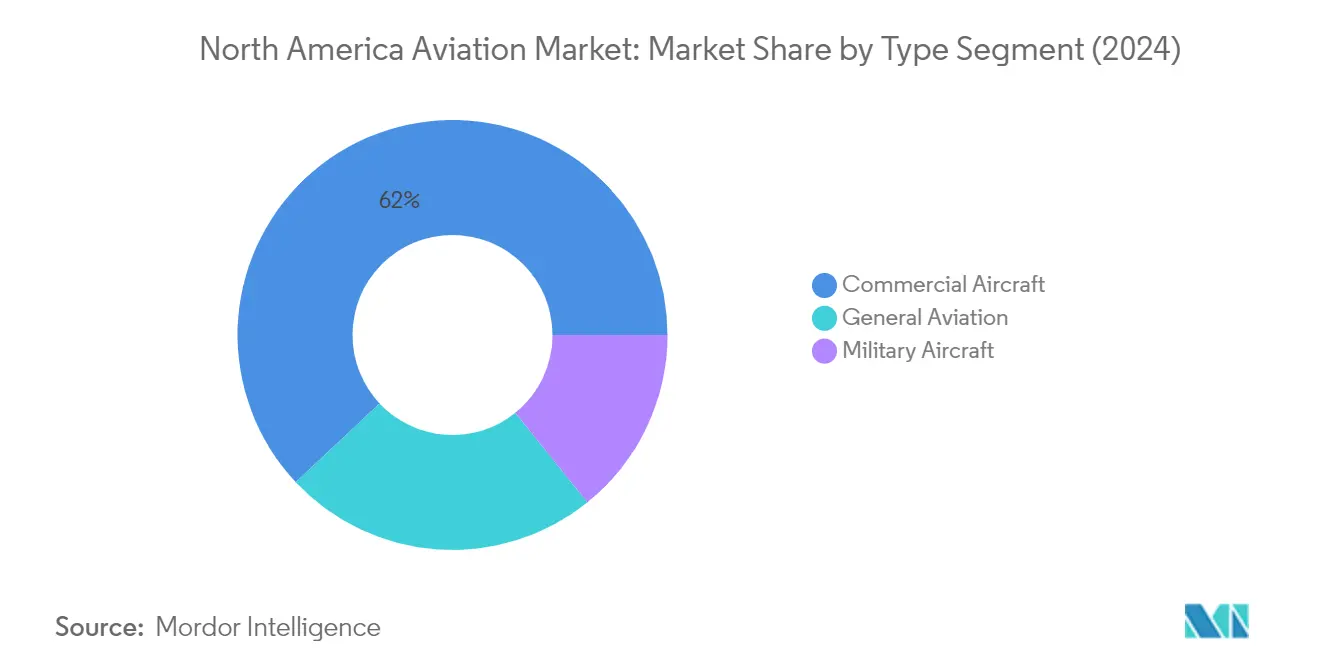

Commercial Aircraft Segment in North America Aviation Market

The commercial aviation segment continues to dominate the North America aviation market, holding approximately 61.35% market share in 2025. This significant market position is primarily driven by the robust demand from major airlines in the United States and Canada for fleet modernization and expansion. The segment's growth is further supported by the increasing recovery of passenger traffic in the region, with airlines actively expanding their networks and introducing new routes. Major carriers like United Airlines, American Airlines, Delta Air Lines, and Air Canada are placing substantial orders for new-generation aircraft, particularly focusing on narrow-body aircraft to enhance operational efficiency and reduce environmental impact. The segment's strength is also reinforced by the large-scale backlog with aircraft OEMs and the airlines' post-pandemic growth strategies that emphasize fleet renewal and capacity expansion.

Military Aircraft Segment in North America Aviation Market

The military aviation segment is projected to exhibit the highest growth rate in the North America aviation market during 2025-2031, driven by substantial defense spending and modernization initiatives. The United States Department of Defense's continued focus on replacing aging aircraft fleets and incorporating advanced technologies is propelling this growth. The segment's expansion is supported by major procurement programs, including the F-35 fighter variants, F-15EX fighters, KC-46A tankers, and various transport aircraft. Additionally, the development of next-generation aircraft under programs like the Next Generation Air Dominance (NGAD) and the increasing emphasis on enhancing aerial combat capabilities are contributing to the segment's growth trajectory. Canada's plans to modernize its military aviation fleet and reduce dependency on the US Air Force for certain aerial missions are also supporting this growth momentum.

Remaining Segments in North America Aviation Market

The general aviation segment represents a significant portion of the North America aviation market, encompassing business aviation jets, helicopters, turboprops, and piston fixed-wing aircraft. This segment is particularly driven by the strong presence of high-net-worth individuals and corporate customers in the region, especially in the United States. The segment has shown remarkable resilience with increasing demand for business aviation services, particularly in the charter operations sector. The growth in this segment is supported by the expanding network of private aviation infrastructure, the introduction of new aircraft models with enhanced capabilities, and the increasing preference for private aviation solutions. The segment continues to evolve with emerging trends in urban air mobility and the development of more sustainable aviation solutions.

Geography Analysis

The United States dominates the North American aviation landscape, commanding approximately 92.65% of the market share in 2025, while also demonstrating the strongest growth trajectory with a projected CAGR of around 1.93% from 2025 to 2031. The country's aviation sector benefits from hosting the world's four largest airlines and maintaining the largest military aviation fleet globally. The robust domestic market is driven by extensive aviation infrastructure modernization projects across major hubs like Los Angeles International Airport, Chicago's O'Hare Airport, and John F. Kennedy International Airport. The United States maintains its position as a significant hub for aerospace innovation, with manufacturers heavily investing in research and development of advanced technologies, including electric aircraft architecture and urban air mobility solutions. The presence of major aircraft manufacturers, coupled with substantial defense spending and a thriving commercial aviation sector, continues to reinforce the country's market leadership. The aviation industry's growth is further supported by increasing demand for both commercial aviation and military aircraft, with particular emphasis on narrow-body aircraft for domestic routes and next-generation military aircraft for defense capabilities.

Canada represents a vital component of the North American aviation ecosystem, with its market characterized by a strong focus on aerospace innovation and manufacturing capabilities. The country's aviation sector is undergoing significant transformation through substantial investments in airport infrastructure modernization, including expansions at facilities like Red Deer Regional Airport and Waterloo International Airport. The government's commitment to aviation development is evident through initiatives like the Airport Critical Infrastructure Program (ACIP) and the Airport Relief Fund (ARF), which provide crucial funding for infrastructure improvements and operational support. Canada's commercial aviation landscape is dominated by major carriers like Air Canada and WestJet, who are actively modernizing their fleets with next-generation aircraft. The country's aerospace industry benefits from a robust manufacturing base and significant research and development activities, particularly in Montreal's aerospace cluster. The military aviation sector is experiencing notable growth through various procurement programs, including the Future Fighter Capability Project and the Fixed-Wing Search and Rescue Aircraft Replacement project, demonstrating the country's commitment to maintaining advanced aerial capabilities.

The broader North American aviation market encompasses various territories and dependencies beyond the United States and Canada, though their contribution to the overall market remains relatively modest. These regions benefit from connectivity to major aviation hubs in the United States and Canada, primarily serving regional and tourism-related air travel needs. The regional aviation infrastructure in these areas typically focuses on supporting domestic connectivity and tourism, with varying levels of development and modernization initiatives. While these markets may not match the scale of the US and Canadian aviation sectors, they play important roles in regional connectivity and economic development. The aviation activities in these regions are often characterized by regional aircraft operations, general aviation services, and specialized air transport services catering to local needs. These markets also benefit from the technological advancements and regulatory frameworks established by the larger aviation markets in the region, though often at a smaller scale and with adaptations to local conditions and requirements.

Competitive Landscape

Top Companies in North America Aviation Market

The North America aviation market is dominated by established manufacturers who have demonstrated consistent innovation and market adaptability. Companies are heavily investing in research and development of advanced materials, additive manufacturing technologies, and electric propulsion systems to develop next-generation aircraft. Operational strategies focus on streamlining production processes, optimizing supply chains, and enhancing aftermarket services to maintain competitive advantages. Strategic partnerships and collaborations with technology providers are becoming increasingly common to accelerate innovation in areas such as urban air mobility and autonomous systems. Market leaders are expanding their product portfolios through both organic growth and strategic acquisitions, while simultaneously focusing on sustainability initiatives and reducing environmental impact through improved aircraft efficiency and alternative fuel technologies.

Consolidated Market Led By Global Players

The North America aviation market exhibits a highly consolidated structure dominated by large multinational corporations with diverse product portfolios spanning commercial, military, and general aviation segments. These established players leverage their extensive manufacturing capabilities, robust research and development infrastructure, and well-established distribution networks to maintain their market positions. The high barriers to entry, including substantial capital requirements, complex regulatory frameworks, and the need for specialized technological expertise, have resulted in limited new entrant penetration.

The market demonstrates active merger and acquisition activity, primarily driven by the need to acquire new technologies, expand geographic presence, and strengthen vertical integration capabilities. Major players are increasingly focusing on strategic partnerships with specialized technology firms to enhance their competitive positioning in emerging segments such as electric aircraft and advanced avionics. The industry structure is characterized by long-term relationships between manufacturers and suppliers, creating a complex ecosystem of interdependent stakeholders throughout the value chain.

Innovation and Adaptability Drive Market Success

Success in the North America aviation market increasingly depends on companies' ability to innovate while maintaining operational efficiency. Incumbent manufacturers must focus on developing advanced aviation manufacturing capabilities, investing in digital technologies, and building robust aftermarket service networks to maintain their market positions. The ability to adapt to changing customer preferences, particularly regarding sustainability and operational efficiency, while managing complex supply chains and regulatory requirements, has become crucial for maintaining competitive advantage. Companies must also develop strong relationships with key customers and maintain flexibility in their production systems to respond to market fluctuations.

For new entrants and smaller players, success lies in identifying and exploiting niche market segments, particularly in emerging areas such as urban air mobility and specialized military applications. The ability to offer innovative solutions while maintaining cost competitiveness is crucial, as is the development of strategic partnerships with established players. Companies must navigate complex regulatory environments while maintaining sufficient capital reserves to support long-term development programs. The increasing focus on environmental regulations and sustainability requirements presents both challenges and opportunities for market participants, while the concentration of major customers in both commercial and military segments necessitates strong relationship management capabilities.

North America Aviation Industry Leaders

The Boeing Company

Airbus SE

Lockheed Martin Corporation

General Dynamics Corporation

Textron Inc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Airspace modernization and airport infrastructure programs are creating near-term demand for avionics, surveillance, communications, and software platforms across North America. In 2026, the FAA highlighted a USD 12.5 billion National Airspace System overhaul via its Modern Skies tracker, including large-scale refresh of radios and radar systems. The agency also awarded a 12-year, USD 875 million contract to Air Space Intelligence for AI-enabled air traffic management platforms (including the SMART system). At the same time, in July 2026 the U.S. Department of Transportation announced USD 1.776 billion in FAA airport grants, which supports opportunities for airport-side systems integration, digital operations, and capacity upgrades.

Defense-driven demand is also widening the opportunity set for mission systems, autonomous capabilities, and North American industrial participation, especially where programs emphasize rapid capability insertion and resilient supply chains. In July 2026, the U.S. Air Force conducted a live-fire event involving Anduril’s YFQ-44A Collaborative Combat Aircraft firing an AMRAAM at a digital target, highlighting momentum behind uncrewed combat aircraft ecosystems and related sensors, datalinks, training, and sustainment. Canada also advanced Arctic domain awareness through agreements for the CAD 1.75 billion Arctic Over-The-Horizon Radar partnership with Australia (June 2026), reinforcing demand for long-range surveillance, integration, and support services aligned with NORAD-focused modernization.

Recent Industry Developments

- July 2026: The FAA awarded a 12-year, USD 875 million contract to Air Space Intelligence for AI-enabled air traffic management platforms, including the SMART system for strategic management of airspace, routes, and trajectories. The award places software and data-driven decision support at the center of National Airspace System modernization and is creating demand for integration, cybersecurity, and sustainment services.

- May 2026: The FAA launched the Modern Skies website to track the USD 12.5 billion National Airspace System overhaul, including plans for 27,000 new radios and 612 new radar systems. Public program tracking improves visibility into upgrade timelines and component needs, helping suppliers align communications, surveillance, and installation efforts.

- April 2024: The United States purchased 81 Soviet-era fighter and bomber aircraft from Kazakhstan as part of an auction of 117 military aircraft. The acquisition points to continued work to broaden aircraft access for training, testing, or exploitation activities, which sustains demand for associated maintenance, spares, and support across defense aviation ecosystems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the North America aviation market is defined as the revenue generated from aircraft and rotorcraft demand across commercial, military, and general aviation activities within North America, measured in current US dollars.

Scope exclusions: We exclude airport infrastructure construction, air traffic management systems sold as standalone software, and pure airline ticketing revenues that do not reflect aircraft demand and fleet activity.

Segmentation Overview

- Type

- Commercial Aircraft

- Passenger Aircraft

- Freighter Aircraft

- Military Aircraft

- Combat Aircraft

- Non-combat Aircraft

- General Aviation

- Helicopter

- Piston Fixed-wing Aircraft

- Turboprop Aircraft

- Business Jet

- Commercial Aircraft

- Geography

- United States

- Canada

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to lock the market boundary and build a simple fact base before modeling begins. We referenced public sources such as FAA aircraft registry and operations statistics, Bureau of Transportation Statistics air traffic series, Transport Canada civil aviation updates, and US Department of Defense budget documents for procurement signals. For trade and cross-border movement signals that affect fleet planning, we also reviewed data releases such as US International Trade Administration travel and tourism metrics and customs summaries where relevant.

On the industry side, we used company annual reports and regulatory filings, investor presentations, airport and airline press releases, and peer-reviewed aerospace and transportation journals to validate demand direction and timing. Select paid subscriptions were used only as support for company financials and intelligence, news and financials, aircraft level and engine level aviation databases for fleet tracking, and defense related market information where public detail was limited. These examples are not exhaustive, and many other public and paid sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys across airlines and operators, MRO and leasing participants, airport and service ecosystem stakeholders, and defense-facing respondents. We used these conversations to re-check delivery timing assumptions, utilization shifts, and pricing direction, and then we aligned the model to North America conditions across the United States and Canada.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | |

| Mid tier: 55% | Functional/Unit leaders: 29% | |

| Smaller Players: 20% | Managers: 56% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up approach where air passenger traffic, fleet size changes, and defense spending signals are used to reconstruct the addressable demand pool for aircraft activity in the region, and then revenue is derived using realistic price and mix assumptions. The totals are corroborated with selective bottom-up approximations, including sampled delivery roll-ups by aircraft category and a price times volume check for representative platforms, which are then used to adjust totals when there is a mismatch.

Inputs that matter for this market include aircraft orders and deliveries, backlog and production rate guidance, passenger traffic trends (domestic and cross-border), utilization and retirement patterns for major aircraft classes, and procurement intensity for military aviation programs. Where the model gets finalized, it happens only after the variable series are normalized to a consistent currency timing and then re-tested against recent route and capacity announcements. Forecasting is done using scenario analysis, supported by expert views on capacity additions, delivery schedules, and supply chain constraints, followed by sensitivity checks around price progression and retirement pace. When bottom-up coverage is incomplete for smaller platforms, we apply conservative fill factors based on observed mix and recent delivery patterns, and we keep the assumption visible for later updates.

Data Validation & Update Cycle

Validation is handled through triangulation across independent signals, followed by variance checks at the country and aircraft-type level to confirm outputs align with what traffic, fleet, and procurement series imply. Anomalies are flagged and reviewed in a second analyst pass, and re-contact is triggered when interview feedback suggests a meaningful shift in deliveries, retirements, utilization, or pricing behavior.

Reports are refreshed annually, and interim updates are made when material events occur such as major order swings, production rate changes, or defense budget revisions. Before delivery, we run a final pass on the latest public releases and recent industry announcements so clients receive an updated view instead of a dated model output.

Mordor Intelligence's North America Aviation Market Size Versus Other Published Estimates

Published market sizes for North America aviation can vary because the counting rules are not always aligned, even when the same region name is used. Differences often come from what is included in aviation revenue, the year selected as the anchor, and how pricing and delivery timing are converted into a single USD value.

The table shows a wide spread between the two 2024 figures and the 2025 figure, and under Mordor Intelligence's scope the total is tied to aircraft and rotorcraft demand across commercial, military, and general aviation in North America, instead of including airport infrastructure builds or broader aerospace manufacturing revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 84.14 B (2025) | |

| Trade Journal A | USD 80.98 B (2024) | Uses an earlier anchor year and a longer forecast window, and the public summary does not clearly state how delivery timing, retirements, and currency timing are normalized, which can shift the starting value. |

| Global Consultancy B | USD 233.80 B (2024) | Appears to apply a wider revenue scope that can fold in systems and manufacturing-related revenues beyond aircraft demand activity, which typically raises the market total versus an aircraft activity linked definition. |

Across the three figures, most of the difference is explained by scope and by how demand signals are translated into revenue, especially when adjacent categories are bundled into the total. By tying assumptions to observable indicators and re-checking them through interviews and public series, the final number stays easier to repeat and update as conditions change.

Key Questions Answered in the Report

How big is the North America Aviation Market?

The North America Aviation Market size is expected to reach USD 86.55 billion in 2026 and grow at a CAGR of 2.87% to reach USD 99.71 billion by 2031.

What is the current North America Aviation Market size?

In 2026, the North America Aviation Market size is expected to reach USD 86.55 billion.

Who are the key players in North America Aviation Market?

The Boeing Company, Airbus SE, Lockheed Martin Corporation, General Dynamics Corporation and Textron Inc are the major companies operating in the North America Aviation Market.

What years does this North America Aviation Market cover, and what was the market size in 2025?

In 2025, the North America Aviation Market size was estimated at USD 84.14 billion. The report covers the North America Aviation Market historical market size for years: 2025. The report also forecasts the North America Aviation Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: