Aerospace & Defense

8th MayFeasibility Analysis for FBO Services in East Africa

3 Min Read

The Aviation Market Report is Segmented by Type (Commercial Aviation, Military Aviation, General Aviation, Unmanned Aerial Systems, and Advanced Air Mobility), Propulsion Technology (Turboprop, Turbofan, Piston Engine, and More), Power Source (Conventional Fuel, Fuel Cell, and More), Fit (Line Fit, and Retrofit), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

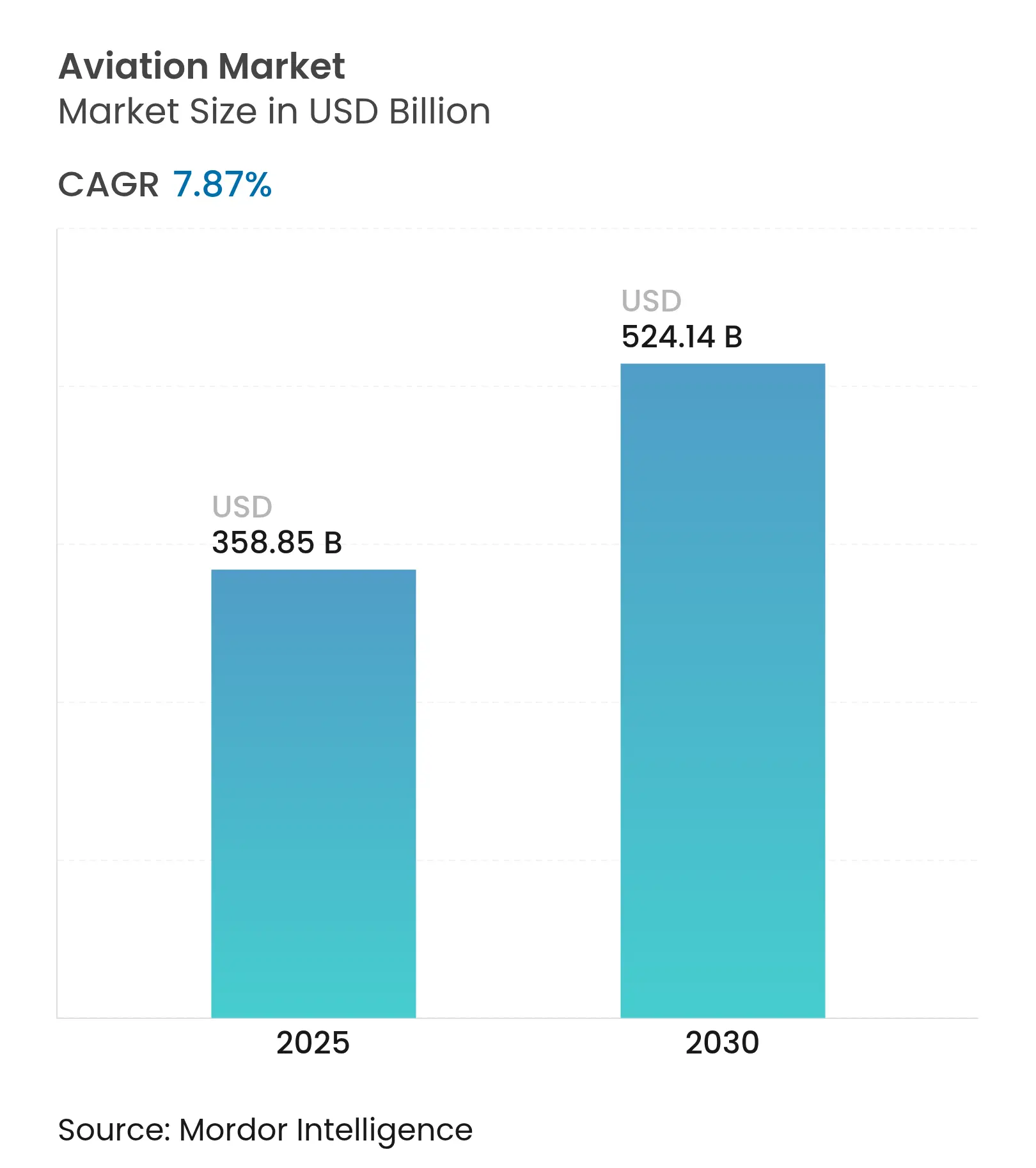

| Market Size (2025) | USD 358.85 Billion |

| Market Size (2030) | USD 524.14 Billion |

| Growth Rate (2025 - 2030) | 7.87 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The aviation market is valued at USD 358.85 billion in 2025 and will expand to a market size of USD 524.14 billion by 2030, reflecting a 7.87% CAGR. The aviation market benefits from renewed passenger demand, accelerated fleet modernization, and record public- and private-sector investment in sustainable propulsion. Airlines and manufacturers are pivoting from sheer capacity growth to value optimization by prioritizing fuel-efficient aircraft, advanced digital maintenance, and alternative power sources that cut emissions and lower unit costs. The aviation market is also shaped by surging e-commerce volumes that lift dedicated cargo traffic, governmental net-zero mandates that spur sustainable aviation fuel (SAF) uptake, and intensified competition from new electric-aircraft entrants. Technology convergence with the automotive and energy sectors, particularly around batteries and hydrogen, further widens the opportunity set for stakeholders that can manage complex certification pathways and supply-chain risk.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Fleet modernization driven by fuel efficiency and cost optimization Fleet modernization driven by fuel efficiency and cost optimization | +2.1% | North America and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:North America and Europe | Impact Timeline:Medium term (2-4 years) |

Rising passenger traffic across emerging and mature aviation markets Rising passenger traffic across emerging and mature aviation markets | +1.8% | Asia-Pacific, MEA, South America | Long term (≥ 4 years) | |||

Growth in e-commerce catalyzing demand for air cargo and freighter conversions Growth in e-commerce catalyzing demand for air cargo and freighter conversions | +1.2% | Global, led by North America, China, India | Medium term (2-4 years) | |||

Rebound in business travel fueling commercial aviation recovery Rebound in business travel fueling commercial aviation recovery | +0.9% | North America and Europe, selective Asia-Pacific markets | Short term (≤ 2 years) | |||

Integration of drone–aircraft teaming concepts in military aviation programs Integration of drone–aircraft teaming concepts in military aviation programs | +0.7% | North America and Europe | Long term (≥ 4 years) | |||

Corporate sustainability targets accelerating adoption of SAF-compatible aircraft Corporate sustainability targets accelerating adoption of SAF-compatible aircraft | +0.6% | Europe and North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Fleet Modernization Driven by Fuel Efficiency and Cost Optimization

Airlines are replacing legacy fleets earlier than planned to lock in 20-30% fuel-burn savings promised by next-generation narrow-body families.[1]Airbus, “Fuel-Efficient Single-Aisle Program,” airbus.com The aviation market now prices fuel efficiency as a strategic hedge against volatile jet fuel, which can equal 30% of total airline costs. Predictive maintenance suites in new aircraft reduce unplanned downtime, while cabin upgrades lift ancillary revenue per seat. Low-cost carriers and legacy flag carriers alike face rising competitive pressure as newer fleets enable profitable thin routes at lower load factors, reshaping global network design.

Rising Passenger Traffic Across Emerging and Mature Aviation Markets

IATA’s 2025 outlook indicates aggregate passenger traffic growing 4.7% annually through 2043, yet APAC drives more than half that increment alone.[2]Boeing, “World Air Cargo Forecast,” boeing.com Chinese carriers will double their fleets by 2043, and India’s domestic market is now the world’s third-largest. Africa’s annual growth rate of 6.4% underpins demand for 1,170 new aircraft even as infrastructure constraints channel investment toward smaller, fuel-efficient types. Mature regions regain pre-pandemic premium-cabin demand, with corporate travel spend rebounding to USD 1.5 trillion in 2024.

Growth in E-commerce Catalyzing Demand for Air Cargo and Freighter Conversions

Cross-border e-commerce volumes and near-shoring trends push dedicated freighter capacity higher, with Boeing projecting the global freighter fleet to expand by two-thirds by 2043. Operators favor converted twin-aisle freighters that meet express-delivery time windows while serving secondary hubs. Economics improve as conversion costs run 40-60% lower than a new-build freight aircraft, providing a compelling bridge amid wide-body production slots that remain tight through mid-decade.

Rebound in Business Travel Fueling Commercial Aviation Recovery

Global business-travel budgets are nearing full pre-2020 levels as firms recognize the sales lift from face-to-face interaction. Long-haul corporate itineraries outpace domestic commuter trips, rewarding airlines that invest in premium-service cabins, Wi-Fi-enabled productivity, and flexible fare structures. Higher-yield mix boosts airline break-even load factors and supports the aviation market’s return to sustainable profit margins.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Persistent supply chain disruptions delaying aircraft deliveries Persistent supply chain disruptions delaying aircraft deliveries | -1.4% | North America and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:North America and Europe | Impact Timeline:Medium term (2-4 years) |

Volatile jet fuel prices putting pressure on operator margins Volatile jet fuel prices putting pressure on operator margins | -0.8% | Global, with higher impact on emerging market carriers | Short term (≤ 2 years) | |||

Limited availability of sustainable aviation fuel constraining adoption Limited availability of sustainable aviation fuel constraining adoption | -0.6% | Europe and North America, expanding to APAC | Medium term (2-4 years) | |||

Air traffic congestion and slot scarcity impacting operational efficiency Air traffic congestion and slot scarcity impacting operational efficiency | -0.5% | Global, concentrated in major hub airports | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Persistent Supply Chain Disruptions Delaying Aircraft Deliveries

Airframe and engine OEMs still wrestle with shortages in castings, forgings, and avionics chips, extending delivery schedules by 6-18 months. Boeing’s USD 4.7 billion purchase of Spirit AeroSystems is emblematic of vertical integration used to regain control over critical fuselage sections. Airlines respond by keeping older aircraft longer, inflating maintenance spend, and dampening capacity growth—a drag on the aviation market’s near-term trajectory.

Volatile Jet Fuel Prices Putting Pressure on Operator Margins

Spot jet-fuel prices have swung 35% within twelve-month windows, testing airline hedging programs. While modern fleets are 25% more fuel-efficient, price instability compels carriers to levy dynamic surcharges, which risk demand erosion in price-sensitive leisure segments. Fuel volatility accelerates interest in SAF offtake agreements that secure multi-year supply at predictable prices, even at a 1.4-2.0x premium to conventional fuel.

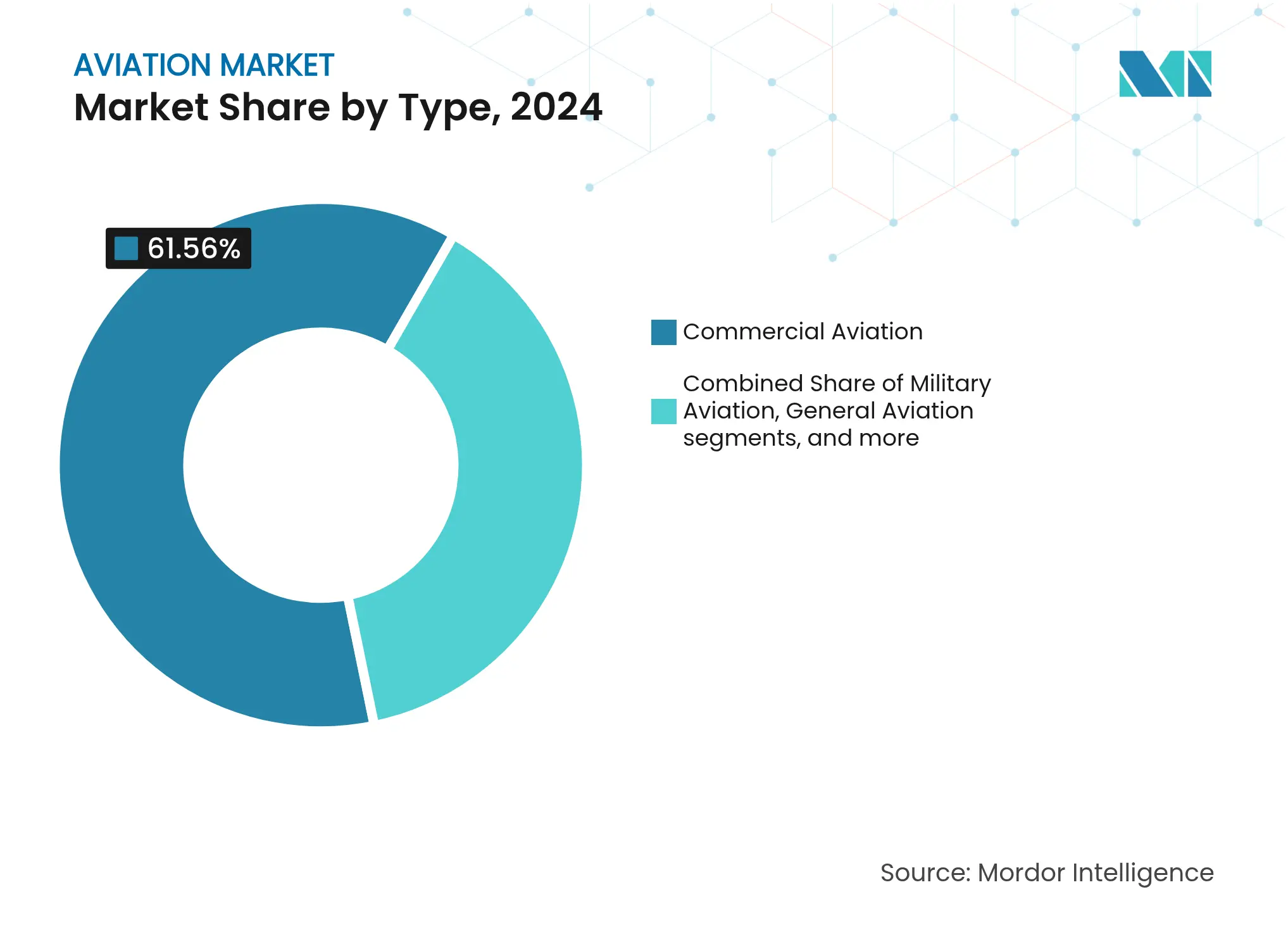

By Type: Commercial Aviation Leads While Advanced Air Mobility Disrupts

Commercial aviation retained a 61.56% share of the aviation market in 2024, supported by global passenger traffic normalization and targeted capacity discipline that restores pricing power. The aviation market size for commercial aviation is projected to grow from USD 221.0 billion in 2025 to USD 308.9 billion in 2030 at a 6.90% CAGR. Network carriers pivot toward more efficient narrow-bodies, while low-cost carriers steadily raise average stage length to tap cross-border leisure demand.

Advanced air mobility (AAM) represents the industry’s most disruptive vector, clearing 18.90% CAGR through 2030 as municipalities approve vertiport frameworks and first-generation eVTOL prototypes log meaningful flight hours. Dubai’s plan to launch Joby services by 2026 illustrates the push to integrate urban air taxis into multimodal transport grids. Although current AAM revenue is minimal, its high growth rate compels incumbents to invest in minority stakes or joint ventures to preserve future relevance.

By Propulsion Technology: Electric Systems Challenge Turbofan Dominance

Turbofan engines held 52.67% of the aviation market size in 2024, buoyed by the prolific A320neo and B737 MAX programs. LEAP and GTF engine families drive double-digit order books as airlines prize double-digit fuel savings. Yet, electric propulsion is scaling at 15.76% CAGR, focusing first on sub-200 nm regional segments where battery mass trade-offs are feasible.

NASA’s Electric Propulsion Flight Demonstration program with industry partners targets commercial-service entry by 2030. GE Aerospace allocates USD 1 billion in 2025 to additive manufacturing lines that will produce next-generation electrical machines.[3]GE Aerospace, “2025 U.S. Manufacturing Investment,” geaerospace.com Hybrid-electric systems bridge today’s range limitations, combining turbogenerator sets with battery packs to cut fuel burn 30% on 400 nm sectors—a pathway sustains turbofan supply chains while advancing electrification.

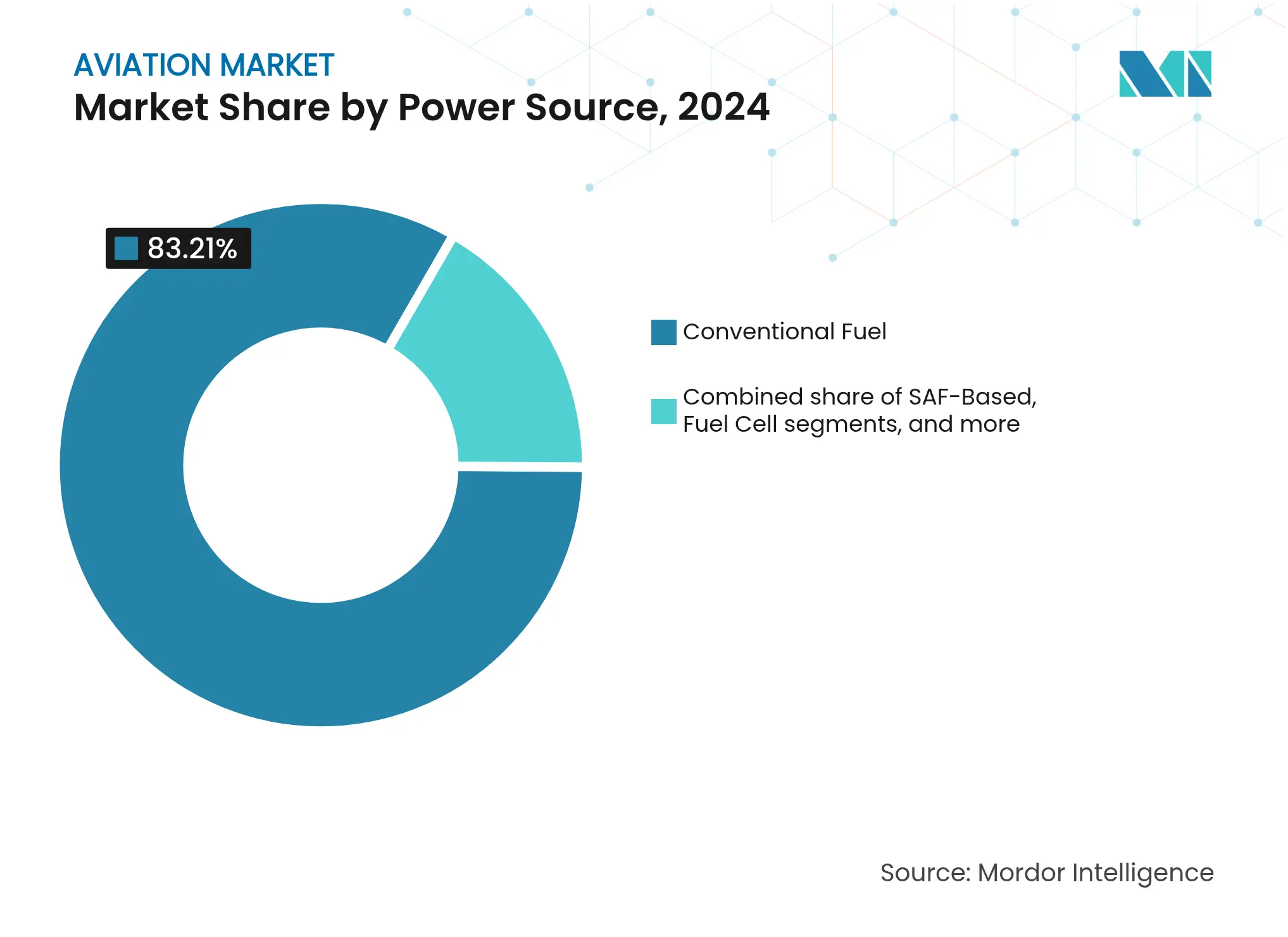

By Power Source: Fuel Cell Innovation Accelerates Despite Conventional Fuel Dominance

Conventional fuel still accounts for 83.21% of the aviation market in 2024, but long-term decarbonization agendas shift capital toward hydrogen and SAF pathways. Fuel-cell propulsion posts the strongest 19.43% CAGR, championed by ZeroAvia’s 2025 flight-test campaign of a 19-seat Dornier 228 retrofitted with a 600 kW hydrogen-electric drivetrain.[4]ZeroAvia, “Hydrogen Hubs Agreement with Airbus,” zeroavia.com Major airports in Canada, Germany, and the United Kingdom are now evaluating hydrogen-production hubs that will co-locate electrolysers with airside distribution, signaling regulatory momentum for mid-2030s entry of 100-seat hydrogen aircraft.

Battery-electric options target 9- to 30-seat regional aircraft that fly under 200 nm, segments accounting for 17% of global departures yet only 4% of fuel burn, offering a credible early decarbonization win. Combining liquid-fuel turbines with battery packs, hybrid systems secure certification credibility by relying on existing infrastructure while delivering double-digit fuel savings.

By Fit: Retrofit Market Gains Momentum Amid Line-Fit Dominance

Line-fit installations held an 82.76% share in 2024, and their share remains high because integrated avionics and powerplant packages confer performance guarantees and finance-lease advantages. The aviation market size for retrofit solutions will nevertheless climb from USD 54.3 billion in 2025 to USD 85.1 billion in 2030, a 9.45% CAGR, as operators pursue cabin densification, in-flight connectivity, and winglet retrofits that pay back in under five years.

Delayed narrow-body deliveries make retrofit necessary, with airlines extending leases on 10-15-year-old aircraft. Engine OEMs capitalize by selling performance upgrade kits that cut fuel burn by 2-3%, and interiors specialists see rising demand for slimline seats that free an additional row in older cabins. Regulators support retrofit pathways by streamlining Supplemental Type Certificates, lowering downtime, and cost barriers.

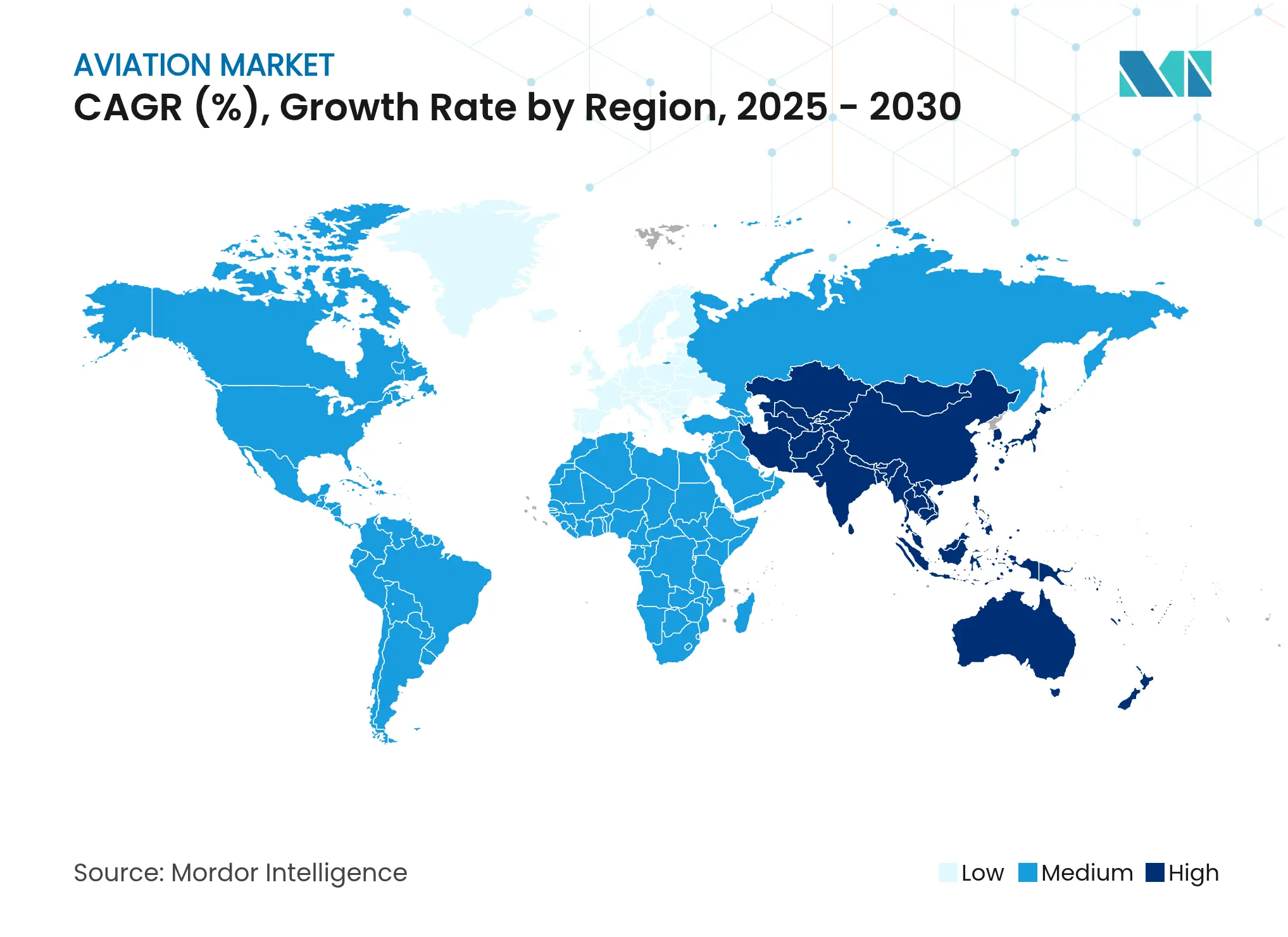

North America’s aviation market size was USD 134.8 billion in 2025 and will advance to USD 175.3 billion by 2030 at a 5.4% CAGR. The United States drives most of this value, leveraging B737 MAX recovery, an expanding defense backlog for the T-7A trainer, and aftermarket revenue from a fleet of 9,600 registered commercial jets. Canada’s aerospace hubs in Quebec and Ontario diversify regional propulsion research, especially in hydrogen storage and fuel-cell testing. Mexico’s free-trade zones attract tier-2 suppliers for wiring harnesses and interiors, improving supply-chain resilience.

Asia-Pacific adds USD 88.5 billion of incremental value between 2025 and 2030, reflecting the fastest growth among major blocs. China’s Civil Aviation Administration simplifies type-certificate validation for the C919, while India’s Airports Authority earmarks USD 11.8 billion in green-field developments to alleviate metro congestion. Japan’s electrified regional-aircraft venture and Australia’s SAF hub in Queensland further enlarge the aviation market footprint. ASEAN regionals such as Thailand and Vietnam pivot to cargo-focused models amid e-commerce booms, employing passenger-to-freighter conversions of A321s to serve intra-Asia logistics corridors.

Europe maintains a balanced growth trajectory at 6.1% CAGR, underpinned by Airbus’s Hamburg and Toulouse production ramp that supports widebody A350 slate extensions. The continent is also the first to propose a binding 2% SAF mandate in 2025, rising to 70% by 2050, pressuring regional airlines to sign long-term offtake deals. Eastern European low-cost carriers enlarge their fleets, encouraging second-line airports to invest in new aprons and maintenance bays. South America rebounds as low-cost penetration exceeds 40% of passenger volumes, with airports from Bogotá to Lima advancing USD 24.4 billion in modernization projects that unlock additional slots for narrowbody aircraft.

The Middle East and Africa contributed a combined aviation market size of USD 47.6 billion in 2025, climbing to USD 70.2 billion by 2030. Gulf carriers reinvest pandemic-era windfalls into A350 and B777X orders, while African carriers benefit from the Single African Air Transport Market, which harmonizes bilateral agreements. Airbus projects the African commercial fleet to surge from 1,250 aircraft in 2025 to 2,650 by 2043, enabling connectivity growth on the continent’s 20 busiest intra-regional routes.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

The aviation market is moderately consolidated: Boeing and Airbus command over 85% of the large commercial aircraft backlog. However, their duopoly is challenged by COMAC’s single-aisle C919 and Irkut’s MC-21. Electric-aircraft start-ups attract venture funding yet rely on partnerships with legacy OEMs for certification know-how and mass-production scale. Turboprop resurgence invites rivalry from Embraer with its conceptual 19- and 30-seat hybrid aircraft that promises 50% emissions cuts, potentially reshaping regional routes.

Strategic moves dominate 2024-2025: Honeywell’s spin-off of its automation unit isolates a USD 15 billion-revenue aerospace pure-play ready to deepen software analytics capability for predictive maintenance. Boeing consolidates its supply base through the Spirit AeroSystems acquisition to stabilize fuselage section flow, whereas Airbus’s bid for select Spirit assets secures composite nacelle capacity. Engine makers GE and Safran extend their CFM partnership through the RISE open-fan demonstrator, targeting 20% fuel-burn savings by the early 2030s.

Urban air-mobility players forge airline alliances—United inks conditional deals for up to 200 JetZero blended-wing-body jets that promise 50% fuel savings on transcontinental missions. The Federal Aviation Administration issues powered-lift criteria enabling eVTOLs in scheduled service, lowering regulatory hurdles for market entry. Fuel producers Neste and World Energy lock multi-decade SAF supply contracts with major airlines, reinforcing vertical integration between energy and aviation.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The aviation industry encompasses the sales of fixed-wing and rotary-wing aircraft across the commercial, military, and general aviation segments. The market report offers an overview of air passenger traffic, aircraft orders and deliveries, variation in defense spending, the introduction of new routes, and investments by major countries into the aviation sector.

The aviation industry report is segmented by type into commercial aviation, military aviation , and general aviation. Commercial aviation is further segmented by passenger aircraft and freighter. Military aviation is further segmented by combat aircraft and non-combat aircraft. General aviation is further segmented by helicopter, piston fixed-wing aircraft, turboprop aircraft, and business jet. The report also covers the market sizes and forecasts for the aviation market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

Feasibility Analysis for FBO Services in East Africa

3 Min Read

Unlocking Market Potential for Solid-State Transformers

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.