Cloud Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

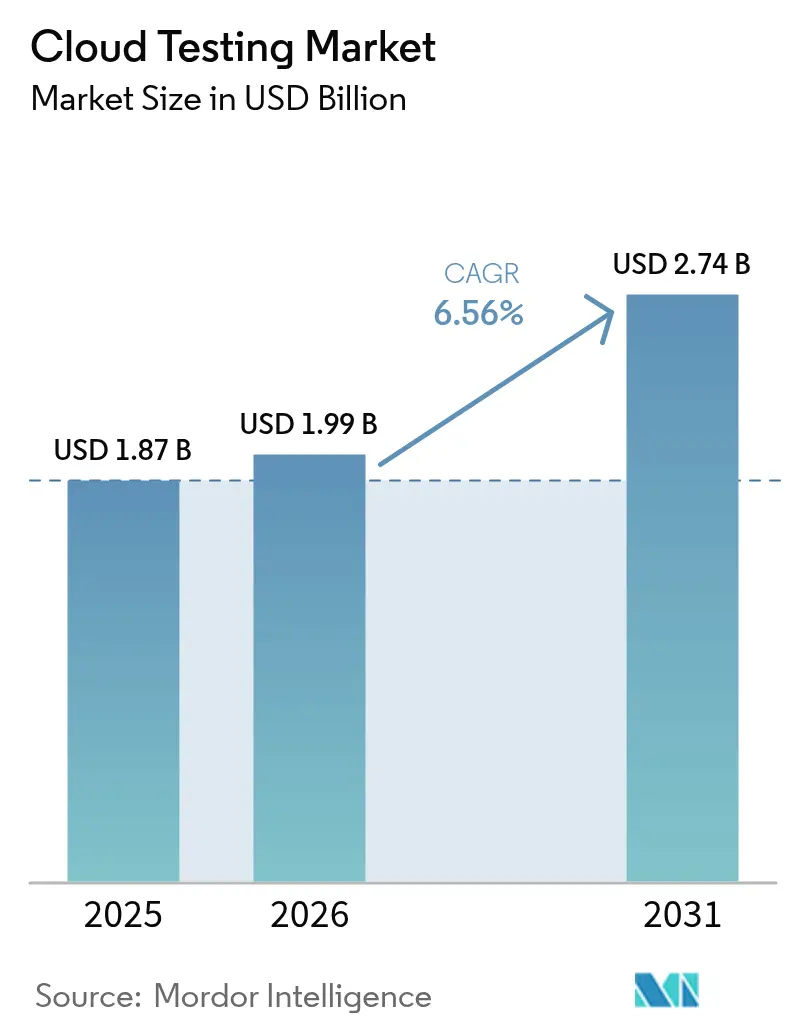

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 2.74 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

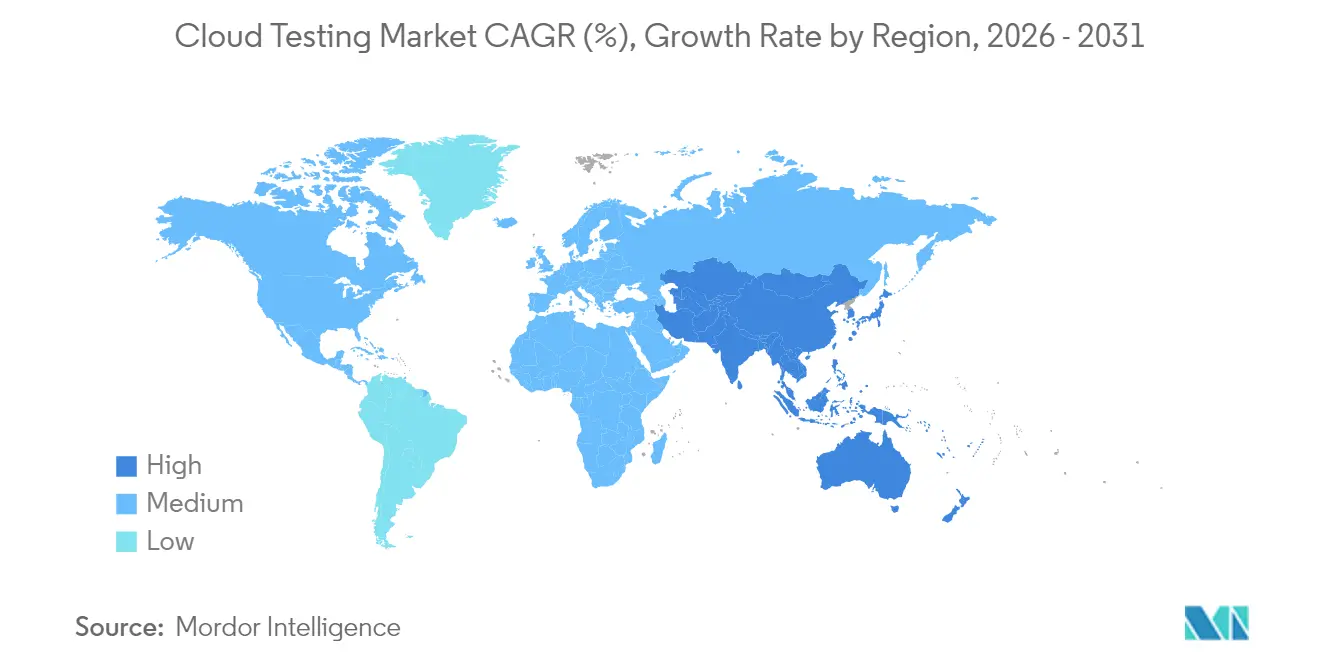

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

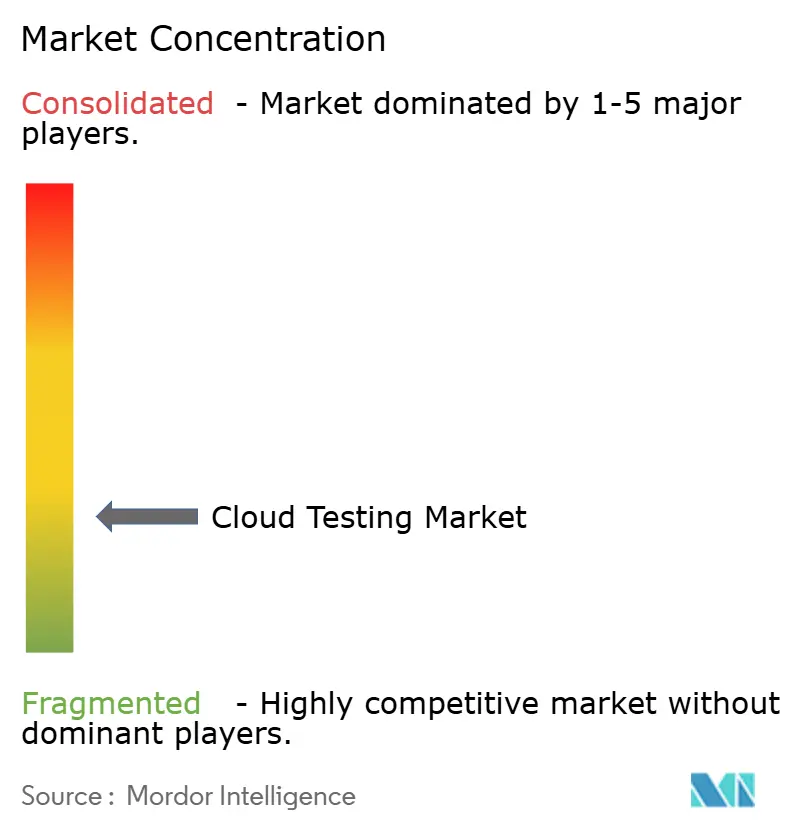

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Testing Market Analysis by Mordor Intelligence

The cloud testing market size was valued at USD 1.87 billion in 2025 and estimated to grow from USD 1.99 billion in 2026 to reach USD 2.74 billion by 2031, at a CAGR of 6.56% during the forecast period (2026-2031). This steady rise reflects the wholesale shift of quality-assurance workloads into cloud-native continuous-integration and continuous-deployment pipelines, a transition that lets teams launch short-lived test environments on demand. Enterprises value elastic infrastructure that absorbs unpredictable peak loads, while usage-based pricing eliminates capital barriers that once limited small firms. Artificial-intelligence test generation, autonomous script healing and tight links to observability platforms now rank among the most requested capabilities, encouraging tool vendors and hyperscale cloud providers to embed them natively. Geopolitical data-sovereignty rules and egress-fee sticker shock temper enthusiasm, yet organizations continue to migrate because on-premise environments cannot match the speed, coverage and economics of cloud-hosted testing.

Key Report Takeaways

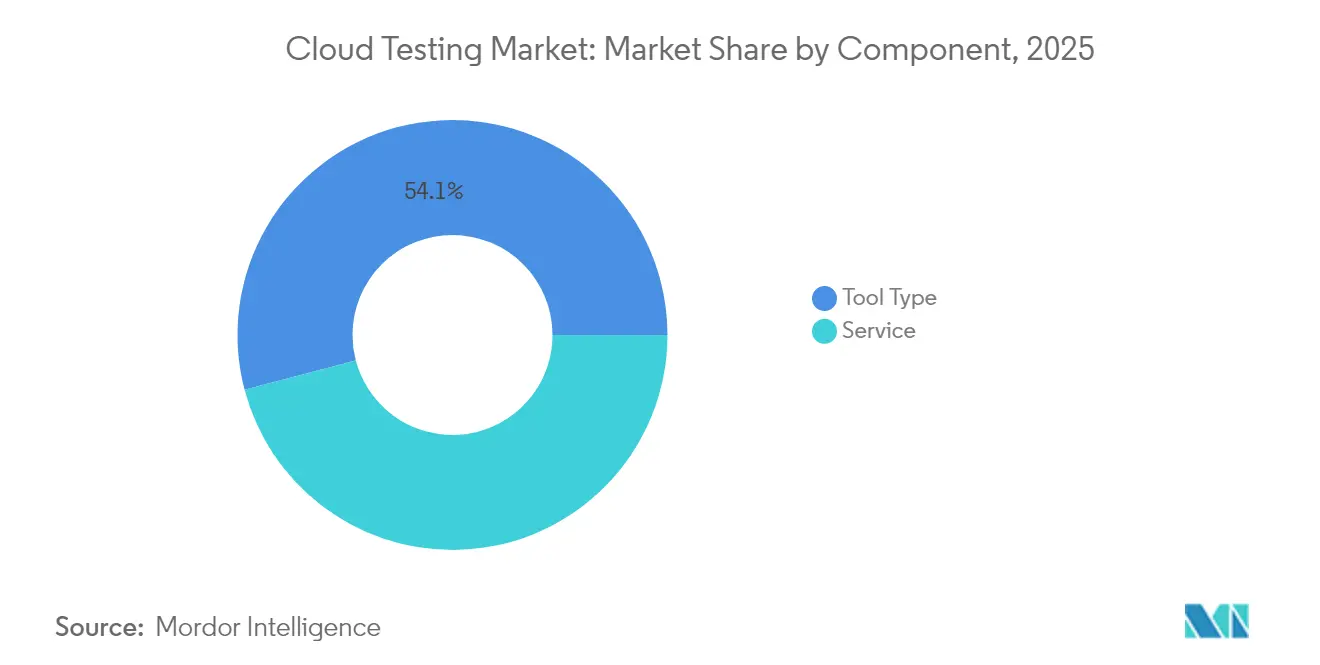

- By component, tool type offerings captured 54.10% of the cloud testing market share in 2025 and are expected to expand at an 8.35% CAGR through 2031.

- By enterprise size, large enterprises accounted for 63.10% of 2025 revenue of the cloud testing market, while small and medium enterprises are forecast to grow at a 8.74% CAGR to 2031.

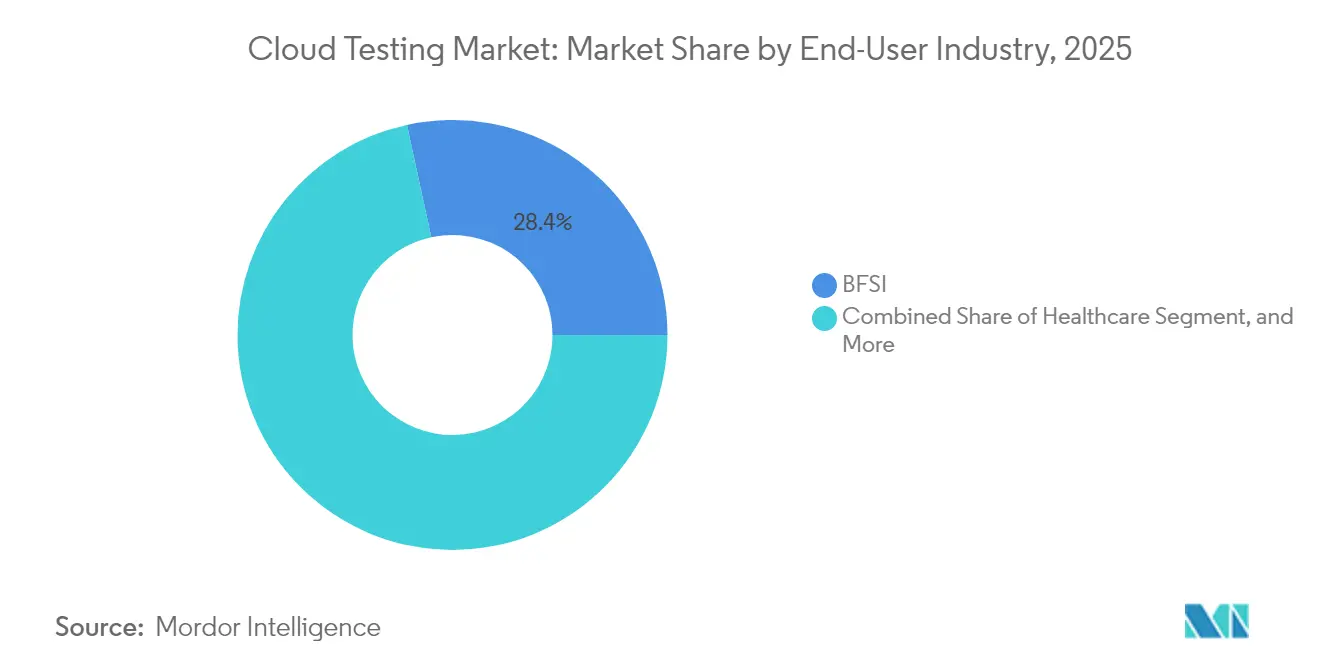

- By end-user industry, BFSI led with a 28.40% revenue share in 2025 of the cloud testing market; healthcare is projected to advance at a 7.62% CAGR through 2031.

- By geography, North America held 43.20% of 2025 revenue of the cloud testing market, whereas Asia-Pacific is projected to record the fastest regional CAGR at 8.12% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated shift to DevOps and CI/CD demanding continuous testing | +1.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Growing complexity of multi-cloud architectures requiring end-to-end validation | +1.5% | Global, particularly North America, Europe, and Asia-Pacific financial hubs | Long term (≥ 4 years) |

| Cost and scalability benefits of cloud-based testing tools vs on-premise | +1.3% | Global, with strongest uptake in Asia-Pacific and South America | Short term (≤ 2 years) |

| Explosion of mobile and IoT applications needing higher test coverage | +1.2% | Asia-Pacific core, spill-over to MEA and South America | Medium term (2-4 years) |

| Usage-based pricing models democratizing access for SMBs | +0.9% | Global, with accelerated adoption in India, Southeast Asia, and Brazil | Short term (≤ 2 years) |

| Integration of AI-powered autonomous testing within cloud platforms | +1.0% | North America and Europe early adopters, Asia-Pacific fast followers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to DevOps and CI/CD Demanding Continuous Testing

Organizations that adopt DevOps release code significantly more frequently than traditional teams, and this cadence necessitates automated validation at every pipeline stage. The Continuous Delivery Foundation recorded deployment frequencies 208 times higher among mature practitioners, a gap that hinges on cloud-hosted suites able to spin up and tear down resources in minutes. Docker’s 2024 survey confirmed that testing and debugging remain time sinks even in cloud environments, reinforcing demand for integrated tooling.[1]Docker, “State of Application Development Report 2024,” docker.com Perforce found that 75% of practitioners view AI-driven testing as pivotal, and 57% already run workloads in the cloud. Financial services and SaaS providers, where release velocity shapes competitiveness, adopt these platforms earliest. Global service-management frameworks such as ISO/IEC 20000 now recommend continuous testing, embedding it into compliance roadmaps.

Growing Complexity of Multi-Cloud Architectures Requiring End-to-End Validation

Most of enterprises operate in multi-cloud settings, exposing them to misconfigurations that waste spend and heighten risk. Banking supervisors warn that vendor lock-in threats prompt institutions to adopt dual- or triple-provider strategies, but this approach requires rigorous cross-platform testing of failover mechanisms and API gateways. Supervisory agencies in Europe now require threat-led penetration tests for systemically important institutions, driving adoption of unified dashboards that consolidate security, performance, and compliance results.[2]European Central Bank, “Cloud Outsourcing Guide,” bankingsupervision.europa.eu Tool vendors that visualize estate-wide results while minimizing license sprawl gain a competitive advantage. The cloud testing market thus rewards platforms that stay neutral yet integrate natively with AWS, Azure, and Google Cloud.

Cost and Scalability Benefits of Cloud-Based Testing Tools vs On-Premise

Capital-intensive labs struggle to keep pace with bursty modern workloads, whereas cloud testing converts fixed costs into variable expenses and allows teams to pay only for what they use. Indian SME studies show that half of the respondents prioritize cloud services because they can scale their infrastructure during peak release cycles without purchasing additional servers. The OECD likewise found that usage-based pricing levels the playing field for smaller firms. Yet 59% of enterprises reported higher overall spending, with egress fees for large datasets a frequent surprise. Effective data-management policies that limit cross-region transfers become essential to preserving savings. As firms mature, they mix spot instances, reserved capacity, and intelligent scheduling to optimize spend.

Explosion of Mobile and IoT Applications Needing Higher Test Coverage

Mobile banking, streaming, and connected-device rollouts intensify the need for performance, security, and interoperability validation. Tricentis’ 2024 survey ranked mobile quality among top enterprise concerns, reflecting customer intolerance for latency or downtime. ETSI’s updated EN 303 645 standard establishes a baseline security for consumer IoT, prompting device makers to verify cryptographic agility, secure updates, and responsible vulnerability disclosure. The adoption of edge computing in the Asia–Pacific region further complicates latency tests, as workloads now reside closer to users. Tool vendors that provide geographically distributed load generators and protocol support for MQTT, CoAP, and 5G-SA stand to win share in the cloud testing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and compliance concerns restricting test-data movement | -1.1% | Europe (GDPR), North America (HIPAA), Asia-Pacific financial centers | Medium term (2-4 years) |

| Legacy infrastructure inertia in highly regulated sectors | -0.8% | Global, particularly North America and Europe banking, healthcare | Long term (≥ 4 years) |

| Escalating cloud egress costs for large test datasets | -0.6% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Tool sprawl and skill gaps causing orchestration complexity | -0.7% | Global, with higher impact in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Security and Compliance Concerns Restricting Test-Data Movement

European Central Bank guidance obliges financial institutions to retain audit rights and maintain exit strategies when outsourcing to the cloud. The Digital Operational Resilience Act layers on penetration-testing mandates and third-party registries, making some firms wary of moving production-like datasets into shared environments. HIPAA and GDPR heighten risks for providers that handle personal health information or data of EU citizens. Vendors respond with encrypted storage, single-tenant regions and synthetic-data tooling, yet adoption still slows when privacy officers demand extra reviews. Consequently, data-masking and sub-setting technologies are rising in tandem with the cloud testing market, ensuring teams can validate functionality without exposing sensitive records.

Legacy Infrastructure Inertia in Highly Regulated Sectors

Most banks continue to run mainframe-based core systems whose interfaces resist modern automation. Federal agencies recount similar challenges: undocumented interfaces, hard-coded business logic and outdated security controls impede cloud-native testing adoption. While tool vendors offer connectors and emulators, the investment needed to refactor applications and retrain staff deters rapid change. Supervisors nonetheless signal impatience, underscoring that extended reliance on legacy stacks heightens operational-resilience risks. The cloud testing market, therefore, bifurcates, with digital-native challengers adopting fully hosted suites while incumbents pursue hybrid strategies that bridge on-premise simulators and cloud-based harnesses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Self-Service Tools Outpace Managed Services

Tool Type platforms generated the largest slice of the cloud testing market in 2025, accounting for 54.10% of revenue and positioning the segment to grow at 8.35% CAGR through 2031. Demand concentrates on performance, load and security modules that plug directly into CI/CD pipelines and spin up infrastructure only when needed, minimizing idle spend. Enterprises also gravitate toward interoperability testing that validates microservices across multi-cloud estates and toward resilience tests that prove failover under chaotic conditions. Usage-based pricing lowers entry barriers, encouraging broader experimentation and making the cloud testing market size for tools swell faster than services. AI additions now generate test cases and heal scripts, trimming repetitive labor and letting senior engineers focus on edge conditions.

Service offerings, which combine managed and professional services, retained 45.90% in 2025 but trail in growth. Clients that lack internal expertise still rely on integrators such as Cognizant, Wipro and Qualitest for outcome-based contracts, particularly when regulatory compliance frameworks require formal attestations. Vendor portfolios increasingly emphasize advisory on AI-bias validation, IoT device hardening and data-residency architectures. Even so, as platform usability improves and internal DevOps maturity rises, many enterprises shift routine regression runs back in-house, a trend that restrains service revenue expansion within the broader cloud testing market.

By Enterprise Size: SMEs Accelerate Adoption via Usage-Based Pricing

Large enterprises held 63.10% of 2025 spending, reflecting their complex global estates, layered compliance obligations, and appetite for advanced automation. These organizations often deploy several overlapping suites, for example, pairing vendor-specific security scanners with open-source load-generators, to cover every workload. They also negotiate enterprise agreements with hyperscalers that bundle compute credits and native testing features, reinforcing their weight within the cloud testing market size category.

Small and medium-sized enterprises, however, represent the fastest-growing cohort, with a 8.74% CAGR through 2031. Their appeal stems from pay-as-you-go tiers that let a two-person startup run the same browser matrix once limited to Fortune 500 budgets. Community forums and low-code interfaces reduce learning curves, while marketplace extensions add niche functions, such as accessibility or localization checks, on demand. As these firms scale, they rarely revert to on-premise setups, making them lifelong contributors to cloud testing market expansion.

By End-User Industry: BFSI Leads, Healthcare Accelerates

BFSI contributed the greatest slice to the cloud testing market in 2025, delivering 28.40% of revenue. Regulators now expect always-on penetration testing, zero-downtime resilience drills and immutable audit trails, forcing banks to adopt sophisticated testing orchestration. Fintech challengers compound the urgency by releasing multiple times per day, prompting incumbents to modernize pipelines or risk customer churn. Core banking migrations to dual-provider estates add further complexity that fuels demand for end-to-end validation.

Healthcare applications, from telemedicine portals to software as a medical device, are projected to rise at a 7.62% CAGR to 2031. FDA guidance on AI transparency obliges makers to track datasets, reference models, and test outcomes for every release. Interoperability rules, such as FHIR and TEFCA, create additional checkpoints to ensure seamless data exchange across electronic health record systems. Vendors that offer traceable, role-based access to protected health information test beds differentiate themselves in this compliance-centric arena of the cloud testing market.

Geography Analysis

North America generated 43.20% of the 2025 revenue, reflecting mature DevOps practices and a dense concentration of software firms that treat fast release cycles as a competitive advantage. U.S. financial institutions, large SaaS providers, and the federal sector all emphasize resilience, driving continual investment in automated testing. Canada’s technology ecosystem reflects these priorities, with provincial digital government programs adopting cloud-native QA frameworks. Mexico’s near-shore development centers further boost regional consumption as they supply code to North American clients.

The Asia-Pacific region is expected to be the fastest-growing geography, with a 8.12% CAGR through 2031, driven by sovereign-cloud buildouts, mobile-centric consumer habits, and large public-sector digitalization mandates. China’s push to localize software stacks sparks demand for domestic toolchains, while India’s 25% annual growth in public cloud fuels uptake among both startups and state agencies. Southeast Asia’s USD 263 billion digital economy expansion adds transactional workloads that must be performance-tested across fragmented network conditions. Japan and South Korea focus on private-cloud migrations of mission-critical SAP landscapes, which require regression suites to validate converted business logic.

Europe balances high adoption with rigorous oversight. The Digital Operational Resilience Act, effective January 2025, forces banks to document cloud testing procedures, retain threat-led-penetration partners and maintain exit strategies. Germany, France and the United Kingdom lead spending, leveraging multi-tenant regions that comply with GDPR data-sovereignty rules. The Netherlands' dense data-center footprint attracts hyperscalers and independent testing vendors, forming a regional hub. Elsewhere, Brazil’s fintech boom, Saudi Arabia’s sovereign-cloud mandates and South Africa’s mobile-banking surge collectively widen the customer base, ensuring that the cloud testing market remains globally contested.

Regulatory Landscape

Cloud testing adoption is shaped by security, resilience, and sovereignty requirements that influence where test data can be processed and how third-party cloud providers are assured. In the European Union, the Digital Operational Resilience Act (DORA) has been effective since January 2025, raising the bar for continuous testing evidence, third-party ICT registers, and threat-led security validation in financial services. This, in turn, increases demand for audit-ready cloud test environments and traceable test artifacts.

In June 2026, the European Commission advanced a proposed Cloud and AI Development Act (CADA), introducing a cloud sovereignty framework with Union assurance levels and recognition pathways via national competent authorities for providers serving the public sector. Alongside regulation, widely adopted standards continue to function as practical compliance anchors in cloud test programs, including ISO/IEC 27017:2025 for cloud-specific security controls and NIST SP 800-171 Revision 3 as a benchmark for protecting controlled unclassified information in nonfederal systems. These standards influence procurement checklists and control mapping for both testing platforms and managed services.

Value Chain Analysis

The value chain starts with cloud infrastructure and platform enablers (compute, storage, identity, networking, observability) from hyperscalers, which provide the elastic environments and native services used to spin up ephemeral test beds. Above this layer sit cloud testing tool vendors delivering performance and load testing, security testing, compatibility testing, and CI/CD-integrated automation, along with agentic capabilities that generate tests and repair scripts.

Data foundations (synthetic data creation, masking, and sub-setting) and security and compliance tooling act as key intermediaries, particularly for regulated customers that need production-like coverage without moving sensitive data across regions or tenants. System integrators and managed service providers then operationalize these platforms into enterprise DevSecOps workflows, managing pipeline integration, governance, and cross-cloud orchestration for complex estates in BFSI, healthcare, and telecom. Distribution and commercialization increasingly run through cloud marketplaces and enterprise agreements, reducing onboarding time while concentrating spend into fewer procurement channels. Downstream, end users (large enterprises and fast-growing SMEs) execute continuous testing in CI/CD, using telemetry to improve test prioritization and remediation, with multi-cloud and regional resilience requirements pushing higher use of distributed test execution and standardized reporting.

Competitive Landscape

Competition spans global integrators, pure-play test-automation specialists, and hyperscale cloud platforms. IBM, Cognizant, Wipro, and Capgemini leverage enterprise relationships to bundle testing into digital-transformation engagements. AWS, Google Cloud, and Microsoft Azure embed native frameworks, capturing workloads early and pressuring independent vendors to integrate through extensible APIs. Specialized providers such as Tricentis, SmartBear, Sauce Labs, and Micro Focus compete on depth, offering model-based automation, self-healing scripts, and compliance templates that outstrip generic platform offerings.

M&A activity underscores consolidation momentum. GTCR’s USD 1.33 billion investment in Tricentis at a USD 4.5 billion valuation provides capital to expand AI features and enter new geographies. SmartBear’s acquisition of QMetry integrates requirements management and risk-based testing into its suite, enhancing its appeal to regulated verticals. Accenture’s 27 acquisitions, including Navisite and OpenStream, scale its managed testing capacity and demonstrate the service provider's appetite for end-to-end DevSecOps portfolios.[3]Accenture, “Accenture Completes Acquisition of Navisite,” accenture.com Vendors also invest in synthetic-data engines, IoT protocol libraries, and agent-testing sandboxes to differentiate in niches underserved by hyperscalers.

Strategic focus now blends AI-augmented test generation with production telemetry. Vendors integrate with observability tools so that post-release incidents feed model retraining loops, reducing future escape defects. Partnerships emerge between testing suites and security-information-event-management platforms, acknowledging that functional and security validations converge in zero-trust architectures. Open-source projects such as Testcontainers and k6 keep pressure on commercial pricing, ensuring the cloud testing market remains competitive despite consolidation.

Cloud Testing Industry Leaders

Oracle Corporation

IBM Corporation

Cognizant Technologies

Akamai Technologies Inc.

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace is the shift from isolated test automation toward agentic, governance-aware quality engineering that can operate across hybrid estates while preserving an auditable trail. Product activity in 2026 points in this direction: Tricentis introduced an end-to-end agentic quality engineering platform (March 2026), SmartBear rolled out AI enhancements across its testing lifecycle (March 2026), Leapwork launched its Continuous Validation Platform for cloud and on-premises use cases (April 2026), and Inflectra released Rapise 9.0 with AI-driven self-healing for web tests (March 2026). These launches show active investment in autonomous test creation, self-healing maintenance, and orchestration across UI, API, and performance domains, supporting enterprises as they address tool sprawl and pipeline friction.

Regulated and infrastructure-heavy environments also create opportunity for platforms that pair continuous testing with compliance mapping and standardized process controls. International testing process standards such as ISO/IEC/IEEE 29119 provide a framework for risk-based testing governance, while ITU-T Recommendation Q.4045 formalizes automated testing considerations for virtualized network functions. Together, these requirements reinforce demand for repeatable assurance in telecom and cloud-native network deployments. In parallel, data-sovereignty and privacy constraints raise the need for synthetic-data pipelines and controlled test-data movement, including Oracle capabilities for realistic synthetic data creation for development and testing workflows that support production-like coverage without exposing sensitive datasets.

Recent Industry Developments

- April 2026: Oracle released Oracle Communications Solution Test Automation Platform (STAP) 1.26.1.0.0, adding an Intelligent Search capability in the dashboard to surface test recommendations and speed up creation of new test jobs from existing artifacts. The release supports faster regression cycles for cloud-based communications stacks and strengthens Oracle-aligned automation workflows for enterprises standardizing on packaged test assets.

- June 2025: Tricentis acquired Testim, adding low-code UI automation and generative test-data capabilities to its platform for SaaS and mobile-first testing programs. The deal broadened Tricentis coverage for teams seeking faster authoring and lower maintenance, while reinforcing consolidation among cloud testing and quality engineering suite providers.

- September 2024: Oracle announced Generative Development (GenDev) for enterprise application development, including Autonomous Database Select AI Synthetic Data Creation to generate realistic test data from production database clones. This capability directly addresses a core bottleneck in cloud testing, producing compliant, production-like datasets for validation without exposing sensitive source data.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cloud testing market covers software testing activities delivered through cloud-based environments, tools, and services that help teams validate application quality, performance, and security without owning all test infrastructure.

Scope exclusions: We exclude general on-premise-only testing work that does not use cloud infrastructure or cloud-delivered testing services.

Segmentation Overview

- By Component

- Tool Type

- Performance and Load Testing

- Interoperability and Compatibility Testing

- Stress and Recovery Testing

- Security Testing

- System Integration and User Acceptance Testing

- Other Tool Types

- Service

- Managed Service

- Professional Service

- Tool Type

- By Enterprise Size

- Small and Medium Enterprise

- Large Enterprise

- By End-user Industry

- BFSI

- Healthcare

- IT and Telecom

- Media and Entertainment

- Retail

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on cloud adoption and software delivery patterns, since these are the practical demand drivers for cloud testing. We refer to public sources such as NIST guidance on cloud computing, ISO/IEC software testing and quality standards, and peer-reviewed journals that track test automation and DevOps practices.

To anchor regional context, we also use official statistics and public datasets such as the US Bureau of Labor Statistics for software occupations, the OECD for ICT indicators, and ITU for telecom and broadband penetration trends that influence digital application usage. On the supply side, we review company filings, earnings materials, product documentation, and reputable press coverage to understand how offerings are packaged as tools versus services. When needed, we also use paid subscriptions for company financials and intelligence, patent databases, and news and financials to cross-check business mix and product focus. The specific desk sources listed here are only illustrative, and other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary validation is done through expert interviews and structured surveys with cloud QA leaders, test managers, DevOps owners, and service delivery teams, so assumptions from desk research can be corrected and filled in with how vendors and buyers describe cloud testing spend. Since this is a global market, we spread outreach across APAC, EMEA, and the Americas to reflect differences in cloud maturity, enterprise compliance needs, and buying behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 15% | APAC: 45% |

| Mid tier: 54% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 15% | Managers: 54% | Americas: 23% |

Market-Sizing & Forecasting

Market sizing uses top-down and bottom-up logic. The top-down build starts from the addressable pool of cloud-based application development and testing activity, then reconstructs it using adoption of cloud test environments and the mix of tool subscriptions versus testing services. Once that demand pool is formed, we corroborate it with selective bottom-up approximations such as sampled supplier revenue splits, channel checks on common packaging models, and an ASP times usage estimate for typical test execution and environment consumption.

Inputs used in the model include the pace of DevOps and CI/CD adoption, cloud migration levels by enterprise size, the tool versus services share treated as a real buying split, the intensity of test automation, and region-wise cloud maturity signals. Where direct revenue attribution is unclear, we apply gap-handling rules that avoid double counting between tool licenses and service-led delivery, and we only count spend tied to cloud-based testing execution or management.

For forecasting, scenario analysis is used to reflect different rates of cloud modernization and regulatory friction, and then scenario weights are adjusted using what practitioners expect for budgets, automation rollout, and vendor pricing changes across the next few years.

Data Validation & Update Cycle

Validation is done by comparing model outputs with independent indicators that move with this market, including enterprise cloud spending direction, software release frequency trends, and reported tool adoption patterns from engineering teams. Outliers are reviewed in steps, first through internal analyst checks on arithmetic and definitions, and then through re-contact triggers when a key assumption shifts or a regional result looks inconsistent with known demand signals.

Reports refresh annually, and interim updates are made when material events occur, such as major pricing changes, large platform shifts, or regulation-led changes in cloud usage. Before delivery, a final review pass is completed so clients receive the most current view based on the latest available public data and refreshed primary inputs.

Mordor Intelligence's Cloud Testing Market Sizing Compared With Other Published Estimates

Published market sizes for cloud testing can appear far apart, and the differences usually trace back to how each publisher defines cloud testing spend, which adjacent spend pools get bundled, and how assumptions like adoption and pricing are carried forward.

The table shows a wide spread across numbers. In Mordor Intelligence's model, the value is limited to cloud testing tools and related services used for software testing delivery, rather than including broader software testing budgets that remain on-premise or sit in adjacent cloud infrastructure testing spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.87 B (2025) | |

| Industry Publisher A | USD 7.80 B (2025) | Typically expands the counted spend by bundling wider testing types and deployment modes, and it may attribute a larger share of enterprise QA budgets to cloud even when execution is mixed across cloud and on-premise environments. |

| Industry Publisher B | USD 14.01 B (2025) | Often uses a broader definition that blends tools, services, and cloud platform-related testing activities, which can lift totals when cloud adoption rates are applied across a larger software testing addressable pool. |

Looking across the table, the main takeaway is that scope and attribution explain most of the difference, especially around whether mixed-delivery testing and adjacent infrastructure testing spend are included. We keep the model repeatable by tying totals back to adoption, tool versus services mix, and region-level demand signals, and then re-checking any outliers before results are signed off.

Key Questions Answered in the Report

How big is the cloud testing market in 2026?

The cloud testing market size is USD 1.99 billion in 2026 and is forecast to reach USD 2.74 billion by 2031.

What is the expected growth rate for cloud-based testing?

Revenue is projected to rise at a 6.56% CAGR between 2026 and 2031 as enterprises shift quality-assurance workloads to the cloud.

Which component segment is growing fastest?

Tool Type platforms are set to expand at an 8.35% CAGR, outpacing service offerings as teams favor self-service automation.

Which region will add the most new spending?

Asia-Pacific is projected to grow at an 8.12% CAGR through 2031, the quickest pace of any region.

Why are SMEs adopting cloud testing rapidly?

Usage-based pricing removes capital expense barriers, letting small teams scale test coverage without owning infrastructure.

Page last updated on: