Size and Share of Wireless Testing Market for Wi-Fi

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

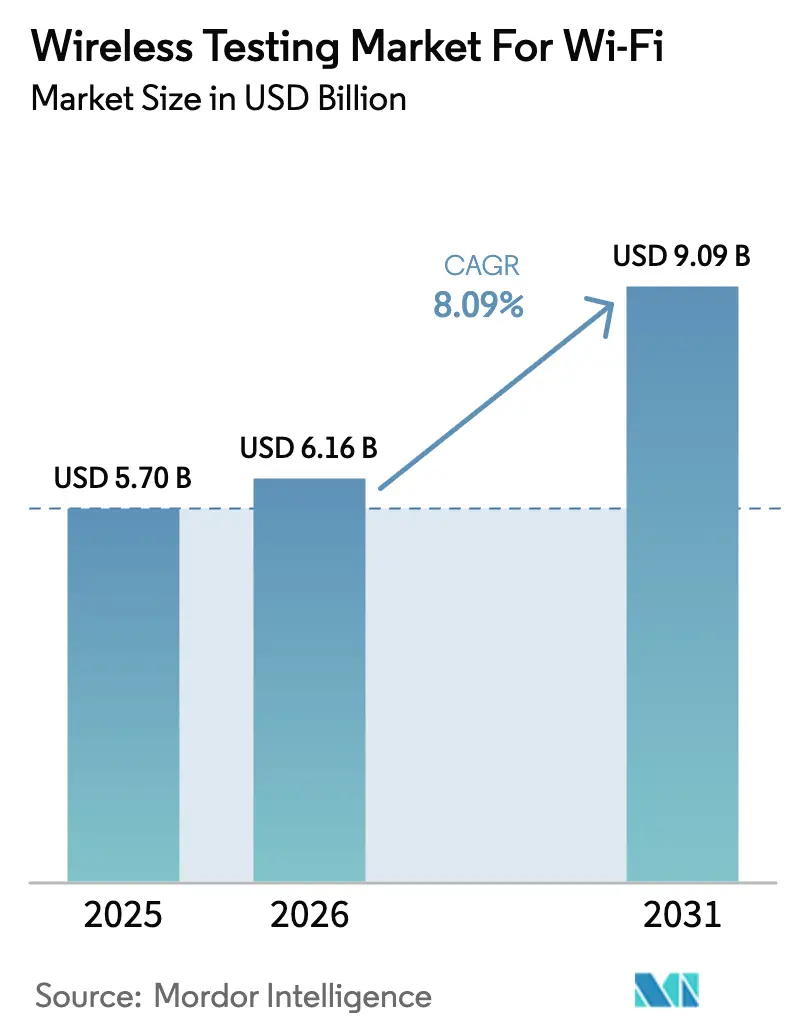

| Market Size (2026) | USD 6.16 Billion |

| Market Size (2031) | USD 9.09 Billion |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

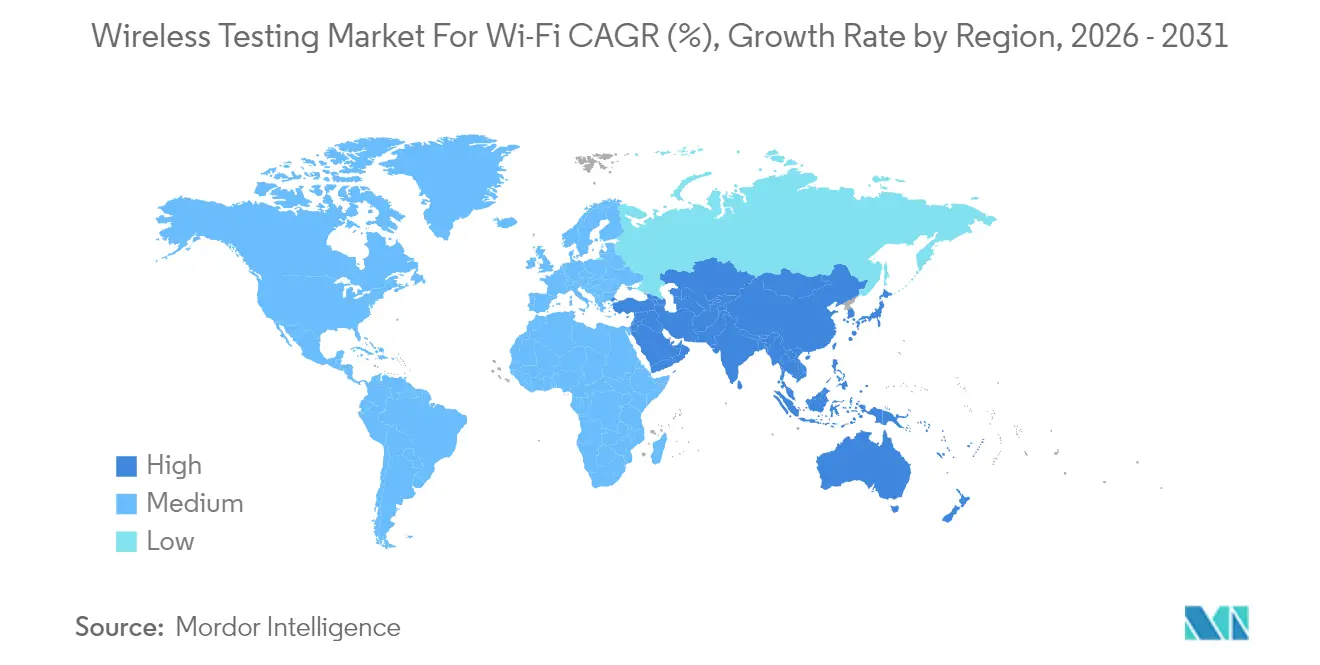

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Wireless Testing Market for Wi-Fi by Mordor Intelligence

The wireless testing market size for Wi-Fi market is expected to grow from USD 5.7 billion in 2025 to USD 6.16 billion in 2026 and is forecast to reach USD 9.09 billion by 2031 at 8.09% CAGR over 2026-2031. Expanding Wi-Fi 7 commercial roll-outs, continuing enterprise Wi-Fi 6E upgrades, and the explosion of Wi-Fi-enabled IoT hardware all push test volumes higher. Growing demand for tri-band validation, multi-link operation checks, and cellular–Wi-Fi convergence scenarios encourages providers to expand chambers, add 320 MHz channel emulation, and certify devices under tighter global rules. Equipment sales still dominate revenue because every major protocol revision triggers fresh capital spend on signal generators, shielded enclosures, and over-the-air MIMO arrays. Yet the fastest incremental value now sits in specialised services, where deep RF know-how, multi-protocol scripting, and cybersecurity verification shorten product launches. Risk factors include gallium supply shocks that may delay new vector network analyser shipments and an acute shortage of Wi-Fi RF engineers, especially as automotive regulations mandate formal penetration tests of in-vehicle Wi-Fi modules.

Key Report Takeaways

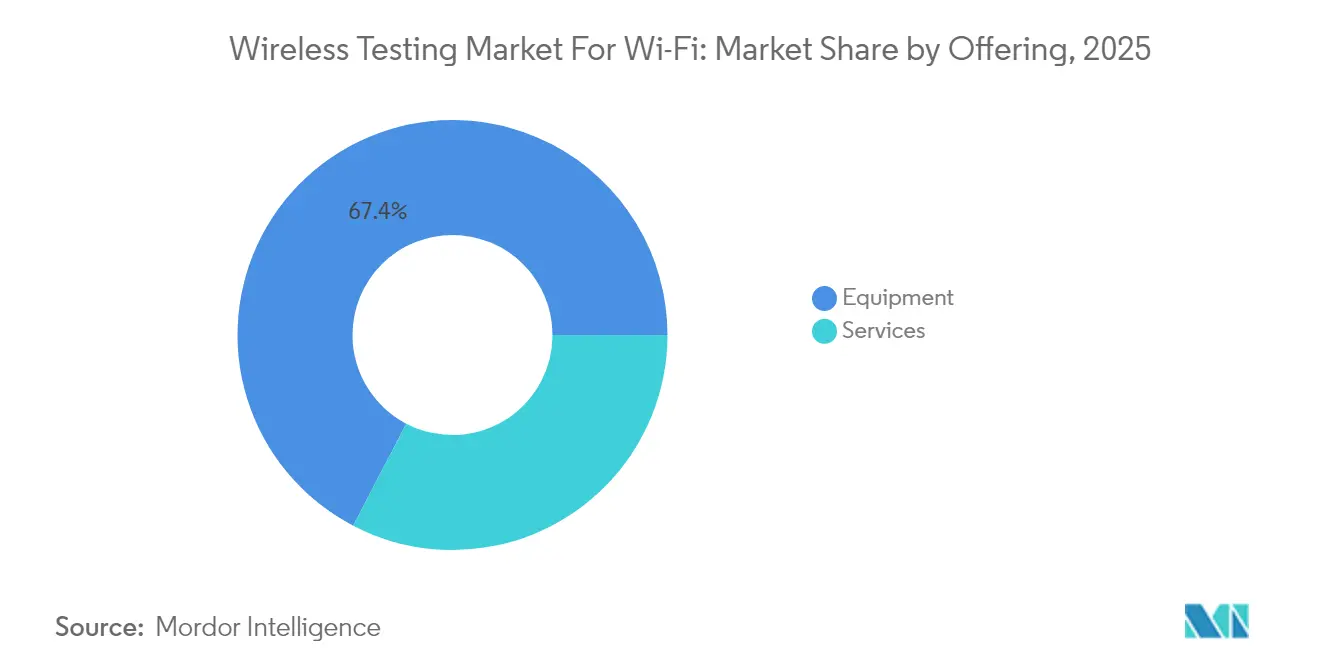

- By offering, equipment held 67.35% of the wireless testing market for Wi-Fi share in 2025, while services are projected to expand at a 11.58% CAGR to 2031.

- By connectivity technology, legacy 4G/LTE maintained 32.10% share of the wireless testing market for Wi-Fi size in 2025, whereas 5G/5.5G test demand is forecast to climb 17.2% each year to 2031.

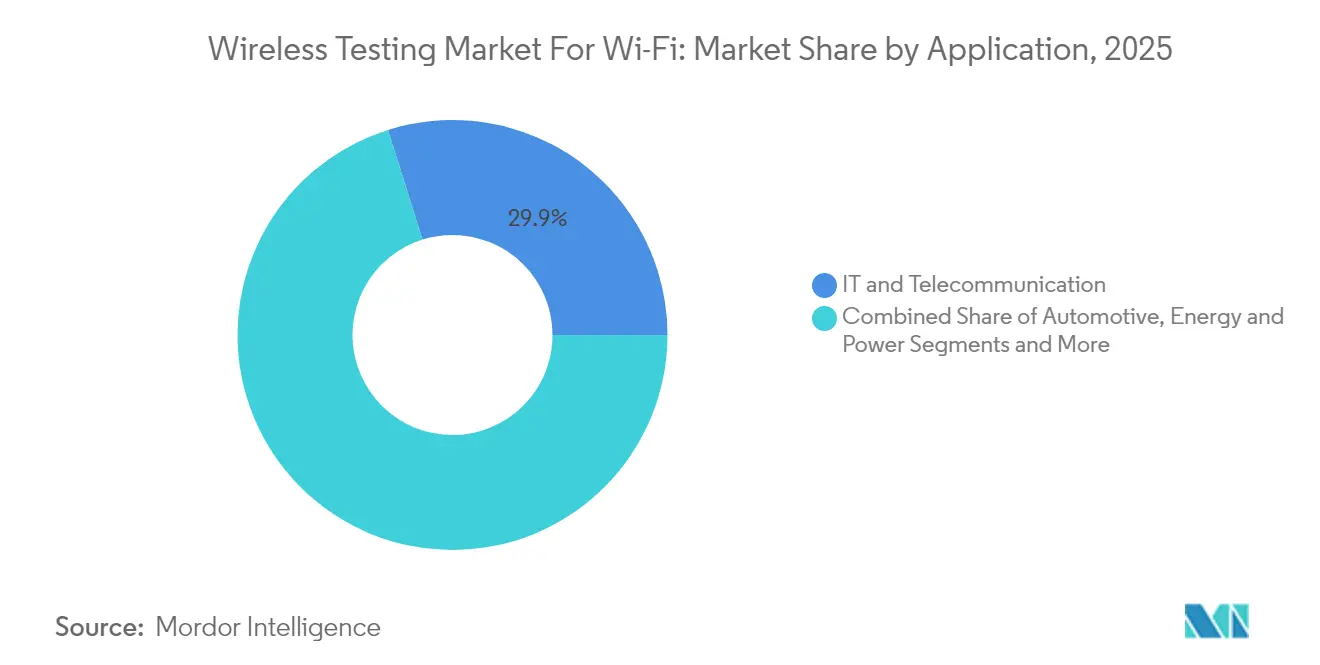

- By application, IT and telecommunications led with 29.85% revenue share in 2025; automotive is set to grow fastest at 14.62% CAGR through 2031.

- By end-use phase, production/manufacturing commanded 56.20% of the wireless testing market for Wi-Fi size in 2025 and R&D/lab testing is advancing at a 11.93% CAGR through 2031.

- By geography, North America accounted for 34.95% of the wireless testing market for Wi-Fi share in 2025, while Asia-Pacific is projected to post the strongest 9.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Wireless Testing Market for Wi-Fi

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Connected devices proliferation | +2.1% | Global | Medium term (2-4 years) |

| Advances in Wi-Fi 6/6E/7 and 5G/5.5G | +2.8% | North America, EU, APAC | Short term (≤ 2 years) |

| IoT expansion across verticals | +1.9% | Global | Long term (≥ 4 years) |

| Stricter certification mandates | +1.4% | Global | Medium term (2-4 years) |

| OTA testing for connected vehicles | +0.7% | North America, EU | Medium term (2-4 years) |

| Direct-to-device satellite links | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of connected devices

Wi-Fi Alliance began certifying Wi-Fi 7 hardware in early 2024, adding 46 Gbps peak throughput and multi-link operation that compounds interoperability scenarios. Manufacturers now blend Wi-Fi, Bluetooth, UWB, and 5G radios on single chipsets, so test houses must script roaming verification across three bands while measuring latency in edge-computing topologies. Consumer, industrial, and medical IoT nodes all demand battery-life profiling under real-world airtime duty cycles, driving service revenues as OEMs outsource power-consumption sweeps.

Advances in Wi-Fi 6/6E/7 and 5G/5.5G standards

Labs need to emulate 320 MHz channels, millimetre-wave coexistence, and Release 18 network slicing. DEKRA’s authorised Wi-Fi lab in Stuttgart opened in 2024 to serve vehicle OEMs that must prove 5G–Wi-Fi handover stability.[1]DEKRA SE, “DEKRA opens first Wi-Fi Alliance Authorized Test Lab in Stuttgart,” dekra.com Providers invest in phased-array over-the-air test rigs that cover 6 GHz indoor concessions and 24 GHz vehicular radome mounts simultaneously.

IoT expansion across verticals

The FDA cleared the TipTraQ wearable for sleep-apnoea screening in February 2025, signalling the pathway for Wi-Fi-certified medical devices.[2]U.S. Food & Drug Administration, “PranaQ TipTraQ 510(k) Clearance,” fda.gov Agricultural drones, smart-grid meters, and factory sensors push qualification beyond consumer form factors, so labs build mixed-fading chambers to mimic dust, vibration, and EMI found on shopfloors or in rural deployments.

Stricter global certification mandates

The FCC’s wireless E911 rules add z-axis accuracy, forcing indoor-location validation that leans on Wi-Fi round-trip-time methods.[3]Federal Communications Commission, “DA-24-1193 Gen2 Starlink Order,” fcc.gov China’s MIIT will enforce new ultra-wideband provisions from August 2025, altering coexistence test limits in the 7.1-8.8 GHz span. Japan’s updated MIC fee schedule raises compliance costs, nudging more OEMs to outsource certification audits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented standards and set-ups | -1.8% | Global | Short term (≤ 2 years) |

| RF testing talent shortage | -1.2% | North America, EU | Medium term (2-4 years) |

| RF-grade component bottlenecks | -0.9% | Global | Short term (≤ 2 years) |

| Higher cyber-compliance burden | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented standards and complex test setups

Parallel support for 802.11n through Wi-Fi 7 multiplies chamber permutations and calibration routines. China retains separate SRRC filings alongside global marks, so a handset shipping worldwide may run six discrete Wi-Fi suites before market entry. The rise of 5G non-terrestrial networking adds orbital Doppler to what were once static indoor scripts, lengthening cycle times.

Shortage of RF testing talent

The European Chips Skills Academy warns of a 75,000-person deficit in semiconductor-related skills by 2030, with graduate output trailing demand. Millimetre-wave beamforming, satellite link emulation, and automotive cybersecurity audits all require niche expertise that takes years to develop, inflating labour costs and delaying commercial releases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate Despite Equipment Dominance

Equipment revenue accounted for 67.35% of the wireless testing market for Wi-Fi in 2025, as every Wi-Fi generation demands fresh vector signal analysers and reverberation chambers. Nevertheless, service revenue is forecast to rise 11.58% annually to 2031, reflecting a pivot toward knowledge-intensive validation. The divergence highlights the value of seasoned engineers who can script multi-standard regression tests faster than in-house teams. TTM Technologies’ 6.4-7.2 GHz RF front-ends illustrate hardware upgrades that keep the equipment segment solid.

Providers increasingly bundle consultancy with hardware access. Clients gain scheduled chamber time, protocol-stack debugging, and regulatory paperwork in a single engagement, cutting launch cycles by weeks. As a result, the services slice of the wireless testing market for Wi-Fi should steadily climb even while absolute hardware spend remains high.

By Connectivity Technology: 5G/5.5G Disrupts Legacy Dominance

Although 4G/LTE still represents 32.10% of the wireless testing market for Wi-Fi size in 2025, 5G/5.5G workstreams will grow 17.2% per year to 2031. Skylo Technologies and Rohde & Schwarz joined forces to close test gaps around non-terrestrial networks, blending Release 17 NB-IoT and Wi-Fi coexistence metrics in orbital scenarios.

Higher-frequency operation and network-slicing complexity mean every new device variant generates a larger battery of tests than its 4G predecessor. Even Wi-Fi 6E gear must now be assessed for fair coexistence with 5G millimetre-wave back-haul. This technical lift, not pure shipment volume, explains why 5G-centric work already absorbs disproportionate lab hours inside the wireless testing market for Wi-Fi.

By Application: Automotive Transformation Accelerates Wi-Fi Testing Demand

IT & telecommunications contributed 29.85% of 2025 revenue, but automotive requests are slated to rise at a 14.62% CAGR. Keysight supplies Deutsche Telekom’s satellite NB-IoT early-adopter program, which underpins emergency call features in connected cars that must still verify Wi-Fi hotspot reliability.

Automotive projects typically span RF, functional safety, and penetration testing. UN Regulation 155 pushes OEMs to prove secure over-the-air updates over Wi-Fi, driving multi-layer assessments that smaller consumer-electronics vendors rarely need. As vehicles integrate tri-band Wi-Fi, Bluetooth, UWB, and 5G, the wireless testing market for Wi-Fi will see automotive vertical revenue nearly triple by 2030.

By End-use Phase: R&D Investment Signals Wi-Fi Innovation Acceleration

Production testing absorbed 56.20% of revenue in 2025 thanks to high device throughput, yet R&D lab work is projected to rise 11.93% annually. VIAVI Solutions and Rohde & Schwarz built a digital-twin testbed for SKY Perfect JSAT that simulates satellite and terrestrial chains, letting R&D teams tune designs months before first silicon.

Earlier engagement reduces costly redesigns later in the cycle, so OEMs are funnelling budget into prototype-stage compliance. As Wi-Fi 7 finalises and satellite links proliferate, up-front simulation will account for a growing slice of the wireless testing market for Wi-Fi.

Geography Analysis

North America generated 34.95% of global revenue in 2025 under the FCC’s tight equipment-authorisation regime. Lockheed Martin’s 5G.MIL payload program reflects the region’s investment in space-based backhaul that must integrate smoothly with terrestrial Wi-Fi 6E ground stations. Frequent rule changes such as very-low-power 6 GHz allowances, sustain steady test demand as networking firms scramble to certify refreshed radios.

Asia-Pacific is on track for a 9.48% CAGR to 2031, propelled by 1.8 billion mobile subscribers and governments fast-tracking spectrum decisions. China’s upcoming UWB rules will force coexistence checks in the upper 7 GHz band, while ASEAN regulators harmonise 6 GHz allocations, boosting cross-border Wi-Fi device roll-outs. Domestic labs in China, Japan, and India are expanding capacity, gradually reducing export-house dependence, and reshaping trade flows within the wireless testing market for Wi-Fi.

Europe holds a meaningful slice of revenue through strong automotive penetration. DEKRA’s authorised lab in Germany gives local OEMs a high-speed path to Wi-Fi 7 certification without shipping prototypes overseas. Meanwhile, Middle Eastern and African nations budget for smart-city infrastructure that embeds Wi-Fi, and South America upgrades national broadband footprints, together creating long-tail growth pockets for lab operators.

Competitive Landscape

Competition is moderate, with global TIC conglomerates vying against RF-centric specialists. SGS, Bureau Veritas, and Intertek wield multinational footprints and regulatory liaisons, allowing one-stop filing across continents. Conversely, Keysight, Rohde & Schwarz, and Anritsu build proprietary signal-analysis suites that perform protocol-layer introspection beyond general-purpose scopes.

Alliances are multiplying. Rohde & Schwarz and VIAVI share satellite emulation infrastructure, splitting capital risk while capturing early revenues from non-terrestrial projects. Skylo and Anritsu similarly align to close measurement gaps around Release 17 NTN handsets. Such moves illustrate how no single vendor can cover every frequency band, antenna topology, and cybersecurity script alone.

White-space remains in AI-driven workflow automation. Start-ups feed neural networks with channel-state logs to predict failures, trimming test cycles without compromising coverage. Established firms are quietly acquiring these analytics teams to integrate dashboards into existing bench analysers, signalling that future differentiation in the wireless testing market for Wi-Fiwill lean as much on software intelligence as on hardware horsepower.

Leaders of Wireless Testing Market for Wi-Fi

SGS Group

Bureau Veritas

Intertek Group PLC

Dekra SE

Anritsun Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Rohde & Schwarz presented live 5G satellite back-haul at World Expo 2025, aided by a VIAVI digital-twin testbed.

- March 2025: Ericsson, Qualcomm, and Thales completed the first 5G NTN voice call using a simulated low-earth-orbit satellite with Wi-Fi coexistence measures

- February 2025: The FDA cleared PranaQ’s TipTraQ Wi-Fi-enabled wearable for sleep-apnoea diagnosis, underscoring medical Wi-Fi compliance hurdles

- January 2025: China’s MIIT updated ultra-wideband regulations, effective Aug 2025, raising minimum 500 MHz signal bandwidth and altering coexistence criteria

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the worldwide wireless testing market for Wi-Fi as every dollar earned from instruments and associated services that measure, validate, or certify the performance, compliance, and safety of Wi-Fi chipsets, modules, access points, and finished devices across R&D labs, production lines, and field environments.

Scope Exclusions: Hardware and audits aimed solely at cellular, GNSS, Bluetooth, or full TIC portfolios lie outside this scope.

Segmentation Overview

- By Offering

- Equipment

- Wireless Device Testing

- Wireless Network Testing

- Services

- Equipment

- By Connectivity Technology

- 5G / 5.5G

- Wi-Fi 6/6E/7

- Bluetooth and UWB

- GNSS / GPS

- Legacy Cellular (2G-4G/LTE)

- By Application

- Consumer Electronics

- Smartphones and Wearables

- Smart Home Devices

- Automotive

- ADAS and V2X

- Infotainment and Telematics

- IT and Telecommunication

- Energy and Power

- Aerospace and Defense

- Healthcare and Medical Devices

- Consumer Electronics

- By End-use Phase

- RandD / Lab

- Production / Manufacturing

- Field Service / Maintenance

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with test-instrument product managers, contract-manufacturing engineers, certification auditors, and Wi-Fi silicon architects in North America, Europe, and Asia-Pacific. They clarified typical test hours, service attach rates, and upgrade cycles that secondary data could not fully explain.

Desk Research

We began by mining open datasets from the FCC, ETSI, and the Wi-Fi Alliance, trade statistics from UN Comtrade, and peer-reviewed IEEE papers, building an initial demand map. Company filings, investor decks, and reputable news wires accessed through Dow Jones Factiva and D&B Hoovers filled gaps on vendor revenues and price moves. Procurement notices on Tenders Info and global customs records cross-checked unit flows. This list is illustrative; many additional public and subscription sources informed our desk work.

Market-Sizing & Forecasting

Our top-down model starts with annual shipments of Wi-Fi enabled devices reconstructed from production and trade data. It multiplies them by average test spend per unit and then corroborates results with sampled ASP × volume roll-ups from key suppliers. Variables such as Wi-Fi 6E and Wi-Fi 7 chipset volumes, R&D intensity of telecom OEMs, regional certification cadence, and average test time per device feed multivariate regression and scenario analysis to 2030. Bottom-up checks for large vendors reconcile anomalies before finalization.

Data Validation & Update Cycle

Before sign-off, our team performs variance checks against historical signals, resolves outliers, and secures peer review. Models refresh each year, with interim updates triggered by material events like spectrum reallocations. An analyst revalidates all figures prior to release.

Why Mordor's Wireless Testing Market For Wi-Fi Size & Share Analysis Baseline Commands Reliability

Published estimates often diverge because different firms mix protocols, apply distinct price curves, and refresh at uneven intervals.

Key gap drivers include the broader technology baskets many studies use (5G, Bluetooth, and GNSS together), aggressive ASP escalation, and update cycles that overlook rapid Wi-Fi 7 rollouts. In contrast, Mordor's figures isolate Wi-Fi spending, use current exchange rates, and undergo yearly review.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.70 B (2025) | Mordor Intelligence | - |

| USD 22.64 B (2024) | Global Consultancy A | Bundles all wireless protocols and counts only equipment |

| USD 23.12 B (2024) | Industry Publisher B | Adds service revenues across cellular plus Wi-Fi and inflates ASPs uniformly |

The comparison shows that, by focusing on pure Wi-Fi testing spend and validating both price and volume drivers every year, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current size of the wireless testing market?

The market generated USD 6.16 billion in revenue during 2026 and is projected to reach USD 9.09 billion by 2031.

Which segment grows fastest through 2031?

Services, fuelled by demand for specialised Wi-Fi 7 and automotive cybersecurity expertise, is forecast to expand at a 11.58% CAGR.

How quickly will 5G/5.5G testing expand?

The connectivity-technology segment covering 5G/5.5G is expected to rise at an 17.2% CAGR as devices integrate cellular–Wi-Fi convergence features.

Why is Asia-Pacific the high-growth region?

Regional spectrum harmonisation and large-scale Wi-Fi 6E deployments drive a 9.48% CAGR, making Asia-Pacific the fastest-expanding geography.

What risk could slow market expansion?

A shortage of qualified RF test engineers and potential gallium supply constraints for high-frequency components threaten to bottleneck capacity.

Which application will add the most new revenue?

Automotive testing, driven by UN Regulation 155 security mandates and advanced infotainment use cases, is expected to deliver the highest incremental growth at a 14.62% CAGR.

Page last updated on: