Accessibility Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

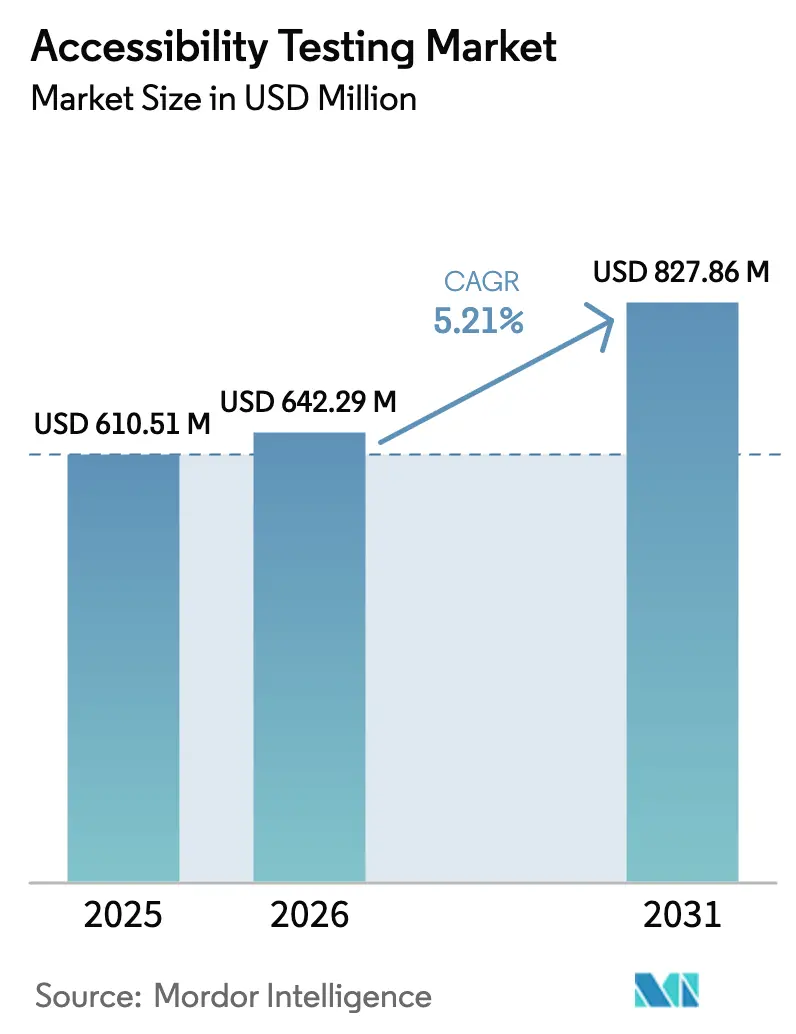

| Market Size (2026) | USD 642.29 Million |

| Market Size (2031) | USD 827.86 Million |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

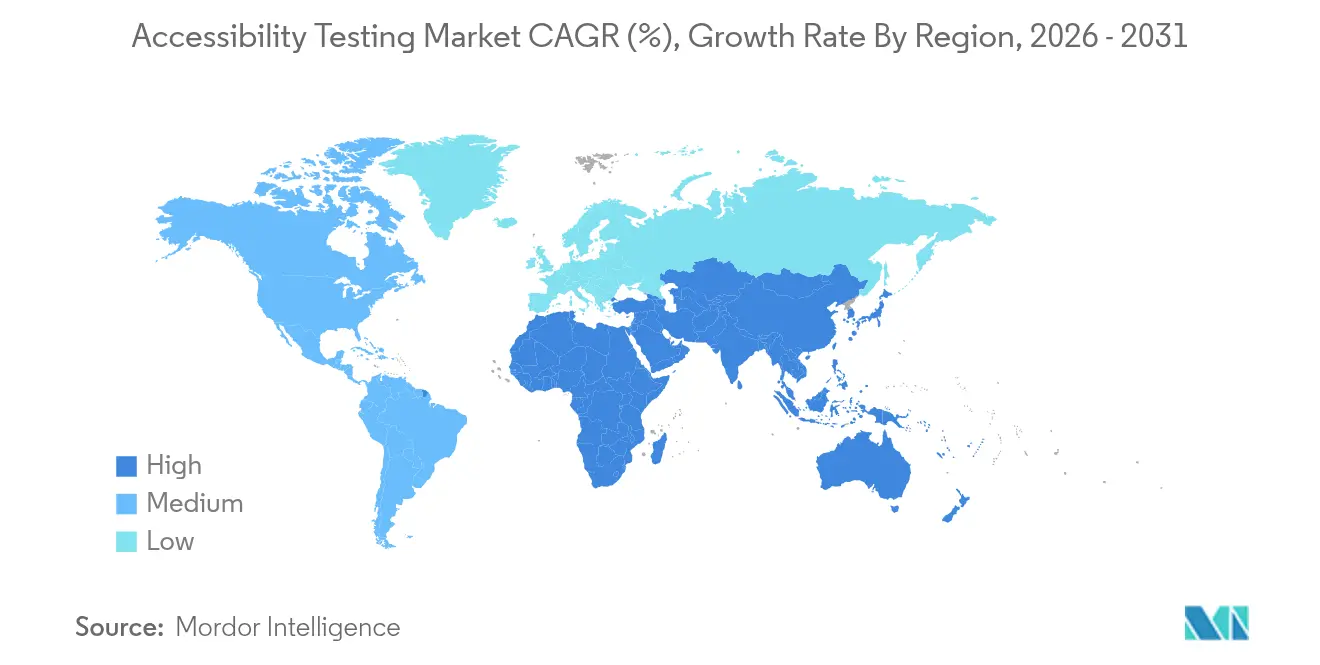

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Accessibility Testing Market Analysis by Mordor Intelligence

Accessibility testing market size in 2026 is estimated at USD 642.29 million, growing from 2025 value of USD 610.51 million with 2031 projections showing USD 827.86 million, growing at 5.21% CAGR over 2026-2031. The expansion reflects three reinforcing forces: stricter global rules that demand digital inclusivity, the brisk tempo of enterprise digital-first initiatives, and the arrival of artificial-intelligence (AI) tools that cut audit expenses and raise compliance accuracy. North America holds sway because mature ADA enforcement makes accessibility a cost-of-doing-business matter, but Asia-Pacific is growing faster as emerging economies legislate inclusive design to spur cross-border trade. Web applications remain the fulcrum of demand, yet voice and conversational interfaces are surging as AI assistants permeate customer touchpoints. Manual methodologies still dominate revenue, though automated and hybrid platforms are closing the gap as organizations embed shift-left DevSecOps practices into development pipelines. Taken together, these factors position the accessibility testing market as a critical component of enterprise risk management and customer-centric product design.

Key Report Takeaways

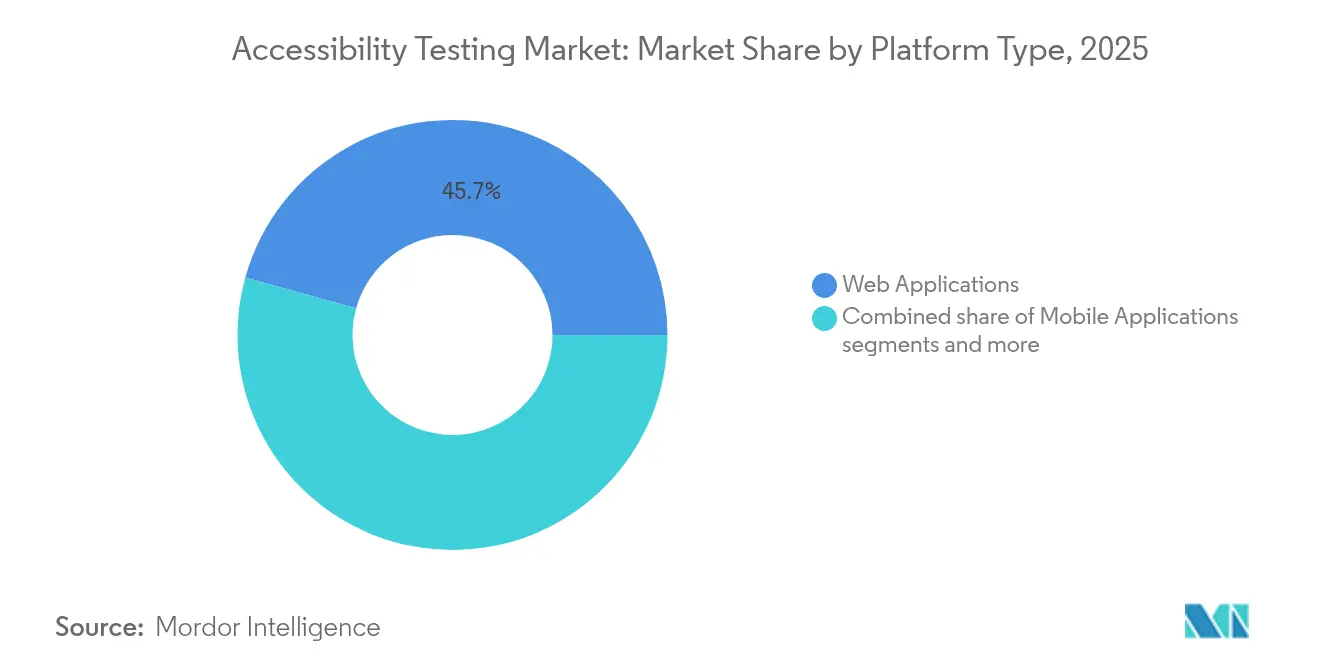

- By platform type, web applications led with 45.70% revenue share in 2025, while voice and conversational interfaces registered the fastest CAGR at 5.86% through 2031.

- By testing approach, manual methods held 53.20% of the accessibility testing market share in 2025, whereas automated solutions are expanding at a 6.54% CAGR to 2031.

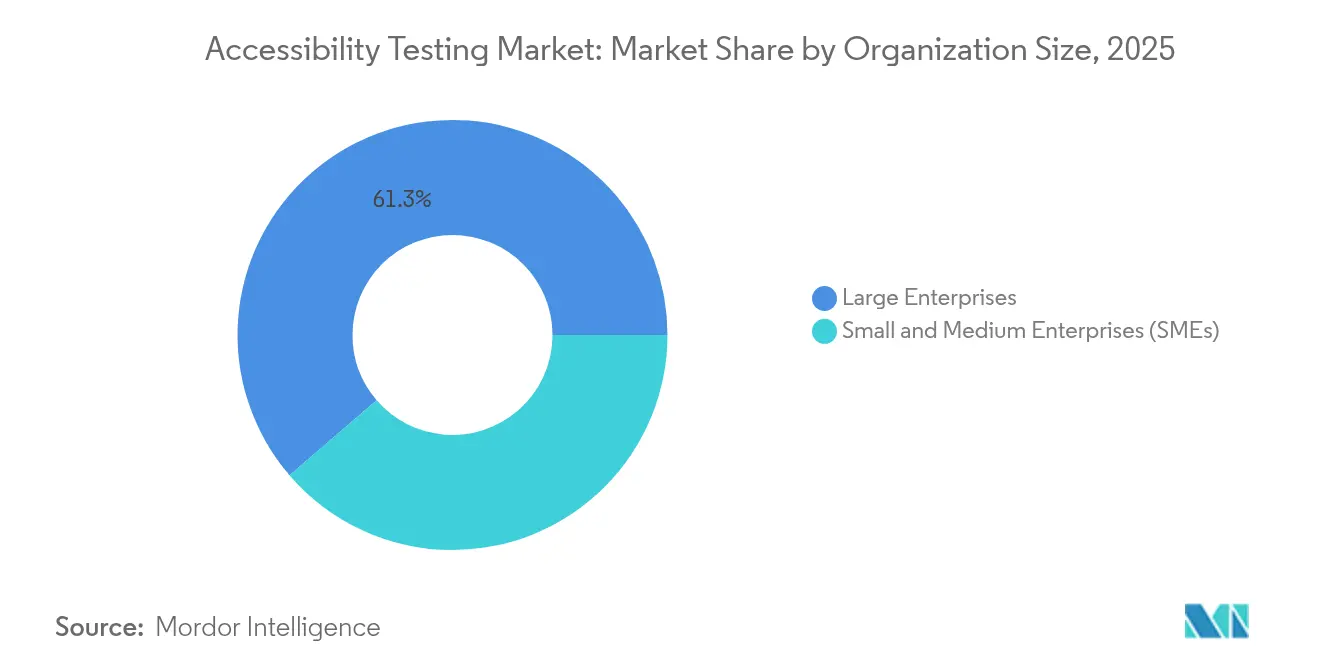

- By organization size, large enterprises commanded 61.30% of the accessibility testing market in 2025, but small and medium enterprises are posting the highest growth at 6.62% CAGR.

- By end-user industry, IT and telecommunications accounted for 23.80% of 2025 revenue; healthcare is set to advance at a 5.62% CAGR to 2031.

- By geography, North America captured 40.60% of the accessibility testing market in 2025; Asia-Pacific is on course for a 6.07% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Accessibility Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter global accessibility mandates | +1.2% | North America, EU, Canada | Medium term (2-4 years) |

| Digital-first initiatives across industries | +0.9% | Global, rapid in Asia-Pacific | Short term (≤ 2 years) |

| Escalating litigation and penalty exposure | +0.8% | Primarily North America, spreading to EU and Asia-Pacific | Short term (≤ 2 years) |

| Shift-left DevSecOps integration | +0.7% | North America and EU leading, Asia-Pacific catching up | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Accessibility Mandates Drive Market Expansion

Canada’s 2024 adoption of EN 301 549 and the European Accessibility Act create a converging rule-set that removes jurisdictional loopholes and compels firms to meet WCAG Level AA across borders. The Accessible Canada Act reinforces compliance by allowing fines, while provincial frameworks like Ontario’s AODA layer additional penalties[1]Bureau of Internet Accessibility, “Canadian Accessibility Laws Update,” boia.org. These converging statutes simplify multinational compliance strategies, generate economies of scale for testing providers, and deepen demand for continuous validation services. Providers able to map test suites to multiple regional mandates win contracts because organizations prefer single-vendor coverage. As a result, mandates elevate accessibility from a discretionary design ideal to an operational requirement that drives sustained market spending.

Digital-First Initiatives Accelerate Testing Demand

COVID-era digitization normalized online transactions, and firms discovered that accessible design broadens reach to the USD 225 billion annual spending power of disabled consumers. Government healthcare systems illustrate the trend: Section 508 rules force accessible patient portals, spurring recurring audits throughout software upgrades[2]Centers for Medicare and Medicaid Services, “Section 508 Compliance,” cms.gov. AI-driven chatbots and voice agents introduce new interaction modes and fresh compliance checkpoints, pulling testing from post-launch audits into product roadmaps. Management teams now measure accessibility dashboards alongside page-load metrics, framing inclusive design as customer-experience upside rather than mere regulatory insurance.

Litigation Risk Escalation Transforms Testing from Optional to Essential

ADA Title III cases topped 10,000 annually, with average settlements near USD 25,000 per demand letter, imposing USD 6.625 billion in yearly legal costs. Plaintiffs favor quick settlements, so even midsize companies face serial claims across multiple properties. Healthcare entities juggle both ADA and HIPAA, raising the stakes for non-compliance and driving premium pricing for nuanced audits that safeguard electronic protected health information. The rise of specialist law firms signals persistent courtroom pressure, turning accessibility from a goodwill initiative into a financial necessity.

Shift-Left DevSecOps Integration Revolutionizes Testing Workflows

Continuous integration pipelines now embed tools such as axe DevTools, allowing developers to catch defects early. Organizations recognize that resolving issues during sprint cycles costs a fraction of post-release remediation. AI scanners flag roughly 30% of WCAG violations instantly, freeing human experts to handle nuanced scenarios. The blend of rapid scans and expert reviews shortens delivery timelines and improves coverage, making shift-left practices a cornerstone of modern accessibility programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of certified accessibility experts | −0.8% | Worldwide, most acute in emerging markets | Medium term (2-4 years) |

| High cost of comprehensive manual audits | −0.6% | Global, pronounced for SMEs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Accessibility Professionals Constrains Market Growth

University curricula seldom cover accessibility testing in depth, causing a pipeline gap just as enterprise demand spikes. Multiplatform ecosystems require practitioners who understand code, assistive tech, and user psychology, skills that develop only through extensive field exposure. Salary inflation follows scarcity, pushing service rates beyond SME budgets and reinforcing a divide in market adoption. Automated scanners ease routine tasks but cannot replace expert judgment in complex, dynamic content or custom controls, keeping top talent in short supply and restraining market expansion.

High Manual Audit Costs Limit SME Market Penetration

Full manual audits for a multi-site environment can exceed USD 50,000, a significant outlay for small businesses. Emerging-market firms feel the strain magnified by currency fluctuations and scarce local expertise. Fragmented device landscapes—from low-cost Android handsets to proprietary enterprise kiosks—multiply test matrices and inflate hours. Although automated platforms trim up-front costs, only 30% of success criteria can be machine-verified, obliging firms to retain specialists for the remaining checkpoints. The resulting cost hurdle delays adoption among budget-constrained organizations until self-service or subscription-based models mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Web Leads While Voice Gains Ground

Web applications generated 45.70% of 2025 revenue, anchoring the accessibility testing market because browsers remain the default gateway for commerce and citizen services. Voice and conversational interfaces are expanding at a 5.86% CAGR, propelled by smart-speaker penetration, AI contact centers, and the need to validate speech recognition for users with impairments. Mobile apps follow close behind, as app-store compliance reviews push publishers to prove inclusive design. Desktop software holds niche relevance in legacy enterprise environments, whereas extended-reality platforms sit at an early-adopter stage marked by standards flux. Convergence on WCAG 2.1 AA reduces duplication by letting providers reuse test scripts across form factors, though voice interfaces still demand bespoke heuristics to account for noisy environments and alternate input modalities.

Second-order dynamics reinforce growth: enterprises migrating to progressive web apps prefer unified audits that cover browser and OS layers simultaneously, while consumer-electronics brands embed voice assistants into appliances, expanding testable endpoints. The accessibility testing market rewards firms that can map test suites to varied device capabilities without inflating project timelines. Specialists who master voice-first heuristics command premium fees, yet cross-training teams in both visual and conversational paradigms reduces overall project cost, making hybrid skill-sets attractive to buyers.

By Testing Approach: Manual Expertise Retains Primacy but Automation Accelerates

Manual evaluation retained 53.20% of the accessibility testing market share in 2025 because human cognition remains irreplaceable for task-flow analysis, cognitive load assessment, and subjective usability checks. Automated scanners, however, are rising at a 6.54% CAGR as DevOps teams incorporate plug-ins that flag violations during code commits. Hybrid workflows—machine scans followed by human confirmation—deliver wider coverage with fewer billable hours, tightening project budgets without sacrificing quality. AI-driven platforms now generate detailed remediation guidance, shortening feedback loops between testers and developers.

Despite progress, tools alone verify only 30% of WCAG checkpoints. Dynamic content, live-region updates, and custom widgets demand manual inspection, ensuring steady demand for specialists. Enterprises, therefore, allocate automation for daily builds and reserve skilled auditors for milestone gates. Over time, AI that simulates diverse disability personas promises to lift automated coverage, but market consensus holds that complete replacement of human review remains distant, preserving a healthy services component in the accessibility testing market.

By Organization Size: Enterprise Spend Dominates, SME Growth Outpaces

Large enterprises contributed 61.30% of revenue in 2025, driven by expansive digital estates, brand-risk concerns, and multi-jurisdictional regulation. Enterprise budgets fund comprehensive testing engagements that blend audits, training, and continuous monitoring. SMEs, however, register the fastest growth at 6.62% CAGR as self-service platforms democratize tooling. Vendors targeting SMEs emphasize subscription pricing, guided remediation dashboards, and integration with popular content-management systems, reducing reliance on scarce consultants.

The accessibility testing market benefits when enterprise programs open-source internal rule libraries, allowing smaller firms to bootstrap compliance. Still, SME awareness gaps persist in emerging regions, where digital transformation itself is in early stages. Government incentives—such as grants for accessible web redesigns—can bridge cost hurdles and accelerate adoption. Over the forecast period, rising procurement clauses that require vendor accessibility attestations will nudge SMEs into action to remain in upstream supply chains.

By End-User Industry: IT and Telecom Remain Anchors, Healthcare Surges

IT and telecommunications maintained 23.80% share in 2025, reflecting their dual role as technology creators and early adopters of inclusive standards. The sector’s rapid release cycles demand continuous testing, fueling stable service contracts. Healthcare is the quickest climber with a 5.62% CAGR, motivated by Section 508 obligations and the clinical benefits of accessible patient portals. Financial services post solid growth as regulators focus on equal access to online banking and as litigation risk looms over inaccessible statements or card apps.

Government and education sectors form a steady channel because funding eligibility often depends on compliance proof. Retail and e-commerce firms, aware that frictionless access lifts conversion rates, increasingly treat accessibility as revenue strategy. Media and entertainment grapple with time-based media requirements—captioning, audio description—that necessitate specialist workflows and elevate per-project fees. Collectively, these patterns ensure that the accessibility testing market serves a broad vertical mix, insulating providers from downturns in any single industry.

Geography Analysis

North America delivered 40.60% of global revenue in 2025, underpinned by the strictest litigation climate and by federal procurement rules that enforce Section 508 compliance across agencies. The region’s buyers view accessibility audits as preventive budgeting against lawsuits that routinely settle for USD 25,000 each. Canada’s alignment with EN 301 549 in 2024 harmonizes requirements with the EU, letting cross-border firms streamline test protocols while broadening the serviceable addressable market for bilingual vendors.

Europe’s steady expansion rests on the European Accessibility Act, which sets common rules and minimizes patchwork compliance. Germany and the United Kingdom top the demand due to e-government ambitions and ecommerce maturity. Brexit-related uncertainty faded as the UK reaffirmed WCAG adherence, letting testing programs proceed without regulatory detours. European buyers prioritize early-stage design reviews over litigation defense, so consultancies offering design-system remediation gain traction.

Asia-Pacific is the fastest-growing region at 6.07% CAGR to 2031. Japan and South Korea drive spending because aging demographics intensify policy focus on digital inclusion. Australia enforces WCAG conformance for public websites, sustaining routine retesting contracts. In emerging economies—India, Indonesia, Vietnam—digital government programs treat accessible portals as levers for social equity and export competitiveness, yet local talent shortages inflate project timelines. China’s huge market beckons, but diverging national standards and data-hosting rules complicate foreign vendor entry. Overall, Asia-Pacific’s rapid digitization ensures the accessibility testing market captures expanding budget lines across both mature and developing digital economies.

Competitive Landscape

The accessibility testing market is moderately fragmented. Deque Systems, Siteimprove, and Level Access hold strong brand recognition, but the collective revenue of the top five players sits below 50%, leaving room for emergent challengers. BrowserStack’s 2025 courtroom victory against Deque opened doors for multifunctional testing suites that bundle accessibility into broader quality-assurance offerings. Vendors are differentiating through AI depth, platform breadth, and seamless CI/CD plug-ins rather than through sheer headcount.

Investment is clustering around automation engines that simulate user personas with varying assistive technologies. Level Access added machine-learning overlays that auto-generate alt-text suggestions. Siteimprove deepened analytics that tie accessibility scores to SEO and customer-experience metrics, repositioning compliance as revenue enablement. Meanwhile, regional specialists in Latin America and Southeast Asia secure contracts by pairing language expertise with local guidelines. Consolidation is likely as well-capitalized firms buy niche providers to fill skill gaps, particularly in voice and extended-reality testing.

White-space opportunities remain plentiful. Voice interface validation lacks uniform standards, leaving a gap for experts who can craft protocol libraries. SMEs worldwide crave cost-effective self-service portals; startups offering freemium scanners plus paid expert consults are scaling rapidly. Market incumbents that pivot to hybrid models—balancing AI efficiency with human insight—are poised to maintain leadership amid intensifying competition.

Accessibility Testing Industry Leaders

Invensis Technologies Pvt Ltd

Planit Testing

Knowbility

TPGi – a Vispero Company

Qualitest Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Expert Adrian Roselli emphasized that automation still covers only 30% of WCAG criteria.

- February 2025: Bureau of Internet Accessibility updated analysis of layered Canadian accessibility mandates and penalties.

- January 2025: A US District Court dismissed Deque Systems’ IP suit against BrowserStack, validating new entrants’ automated testing tools.

- December 2024: AbilityNet’s TechShare Pro spotlighted AI’s rising role while reaffirming the need for human judgment in final auditing.

- November 2024: Ministry of Testing catalogued AI-assisted tools and warned vendors to align with forthcoming WCAG 3.0 changes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the accessibility testing market as all commercial services and software tools that evaluate digital assets, websites, mobile apps, documents, and connected products, against recognized accessibility standards such as WCAG, Section 508, and the European Accessibility Act. The valuation covers revenues earned from manual audits, automated scanners, hybrid platforms, and related remediation add-ons that are sold to end users worldwide.

Scope Exclusions: The assessment does not count broader UX design consultancies that deliver accessibility only as a peripheral add-on.

Segmentation Overview

- By Platform Type

- Web Applications

- Mobile Applications

- Desktop Software

- Voice / Conversational and IoT Interfaces

- Extended Reality (XR) / Immersive Experiences

- By Testing Approach

- Manual Accessibility Testing

- Automated Accessibility Testing

- Hybrid

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-user Industry

- IT and Telecom

- BFSI

- Healthcare

- Retail and E-commerce

- Government and Public Sector

- Education

- Media and Entertainment

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with accessibility auditors, platform vendors, corporate compliance officers, and disability advocates across North America, Europe, and Asia-Pacific. These conversations validated pricing bands, clarified adoption triggers by organization size, and tested usability pain points that cannot be captured through secondary data alone.

Desk Research

We gathered baseline figures from open data sets issued by bodies such as the W3C, the U.S. Access Board, Eurostat, and the International Telecommunication Union, which provide counts of active websites, mobile subscribers, and disability prevalence. Government contract databases, customs records for test software imports, and filings with the SEC and Companies House helped our team benchmark vendor revenues. Additional context came from trade associations like the International Association of Accessibility Professionals and peer-reviewed journals that quantify lawsuit volumes linked to digital barriers. Paid touchpoints, including Dow Jones Factiva for news flow and D&B Hoovers for company financials, supplied trend signals. The sources named above are illustrative; many others were referenced for corroboration and gap filling.

Market-Sizing & Forecasting

A top-down reconstruction starts with the global pool of active public-facing websites and native apps, which are then mapped to estimated penetration rates of paid testing solutions by industry and region. Results are checked through selective bottom-up roll-ups of supplier billings and sampled average selling prices to fine-tune totals. Key variables like annual WCAG lawsuit filings, regulatory deadlines, cloud migration rates, screen reader user growth, and average remediation cost per page drive both the base year and forward view. Multivariate regression explains historical revenue movement, while ARIMA smoothing projects each driver five years ahead. Expert feedback steers scenario weighting when data volatility spikes. Where supplier revenue splits are opaque, proxy metrics such as job postings for accessibility roles bridge gaps.

Data Validation & Update Cycle

Outputs pass a two-level analyst review that flags anomalies against independent benchmarks and year-on-year variance bands. Reports refresh every twelve months, with interim updates triggered by major policy changes or M&A events, and a last-mile sweep is performed just before client delivery.

Why Our Accessibility Testing Baseline Commands Reliability

Published estimates differ because firms choose dissimilar product mixes, assume various average prices, and refresh at uneven intervals.

Key gap drivers include some publishers model testing tools only and miss professional services revenue; others apply static take-up rates that ignore the surge in ADA litigation; a few forecast in local currencies without mid-year FX rebasing, inflating growth.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 610.5 M (2025) | Mordor Intelligence | - |

| USD 589.1 M (2024) | Industry Publication A | Excludes hybrid service platform bundles and uses constant ASPs |

| USD 578.7 M (2024) | Global Consultancy B | Focuses on testing tools segment only, limited primary validation |

The comparison shows that when scope breadth, live currency indexing, and verified adoption triggers are fully integrated, as in Mordor's model, the resulting baseline offers decision-makers a balanced, transparent figure they can track and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the accessibility testing market?

The market stands at USD 642.29 million in 2026 and is forecast to hit USD 827.86 million by 2031 at a 5.21% CAGR.

Why are web applications still the largest segment?

Browsers remain the main gateway for commerce and public services, so companies prioritize web audits, giving this platform 45.70% revenue share in 2025.

How much of the market is in North America?

North America captured 40.60% of the accessibility testing market size in 2025 due to robust ADA enforcement and high litigation costs.

Which industry vertical shows the fastest future growth?

Healthcare leads with a projected 5.62% CAGR to 2031 as Section 508 mandates drive demand for patient-facing accessible interfaces.

Can automated tools fully replace manual accessibility testing?

No. Current AI scanners detect only about 30% of WCAG issues; human experts remain essential for complex scenarios such as dynamic content and voice interfaces.

What factors limit adoption among small and medium enterprises?

Audit costs and scarcity of certified professionals make full compliance expensive, although emerging self-service platforms are lowering entry barriers.

Page last updated on: