North America Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

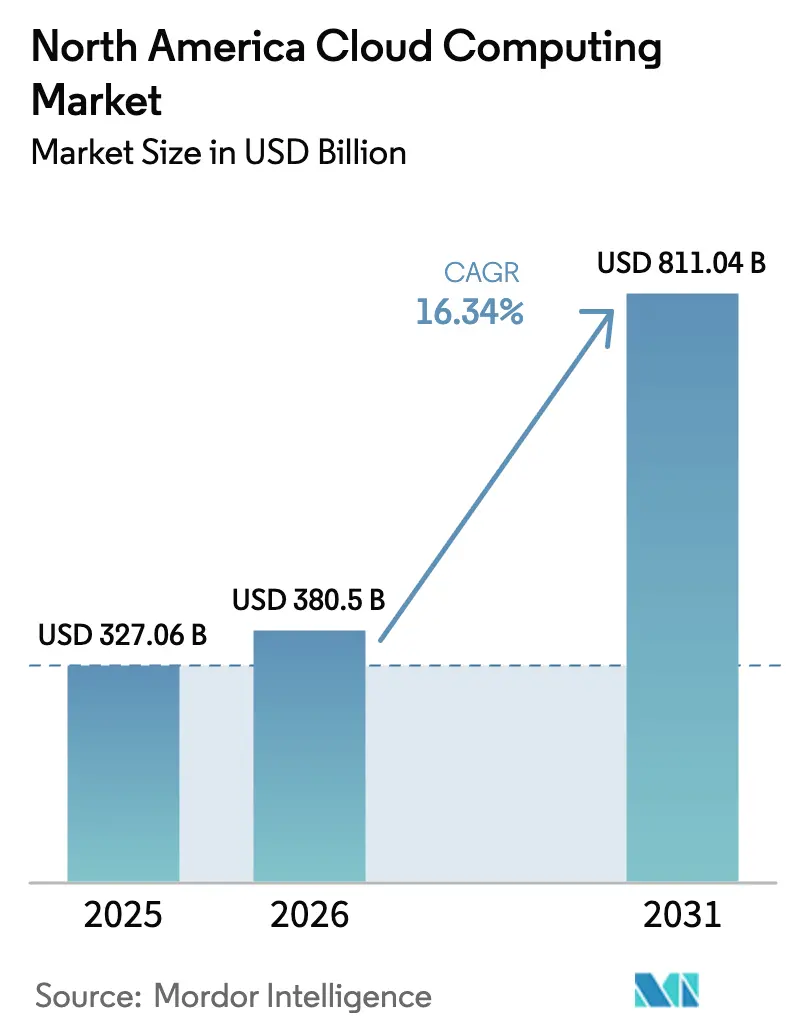

| Base Year Market Size (2025) | USD 327.06 Billion |

| Market Size (2026) | USD 380.5 Billion |

| Market Size (2031) | USD 811.04 Billion |

| Growth Rate (2026 - 2031) | 16.34% CAGR |

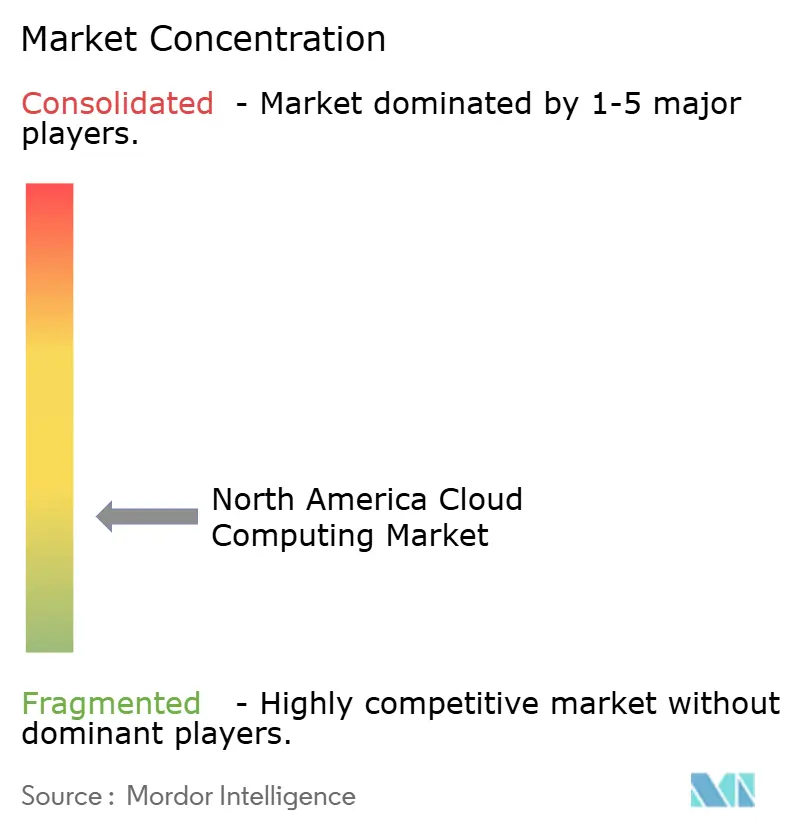

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Cloud Computing Market Analysis by Mordor Intelligence

The North America Cloud Computing Market size in 2026 is estimated at USD 380.5 billion, growing from 2025 value of USD 327.06 billion with 2031 projections showing USD 811.04 billion, growing at 16.34% CAGR over 2026-2031. The region’s enterprises are scaling AI workloads, modernizing legacy stacks, and adopting edge architectures, all of which keep the cloud computing market on a steep growth curve. Hyperscale providers are racing to deploy capital-intensive GPU clusters, renewable-powered campuses, and localized edge zones to secure latency-sensitive customers. Rapid PaaS uptake, vertical SaaS roll-outs, and hybrid strategies are broadening the addressable base, while government incentives for domestic chip-to-cloud supply chains reinforce long-term demand. Although grid congestion and water-usage restrictions slow some projects, regulatory clarity around data-sovereignty agreements and carbon disclosures is gradually improving, preserving investment momentum in the cloud computing market.

Key Report Takeaways

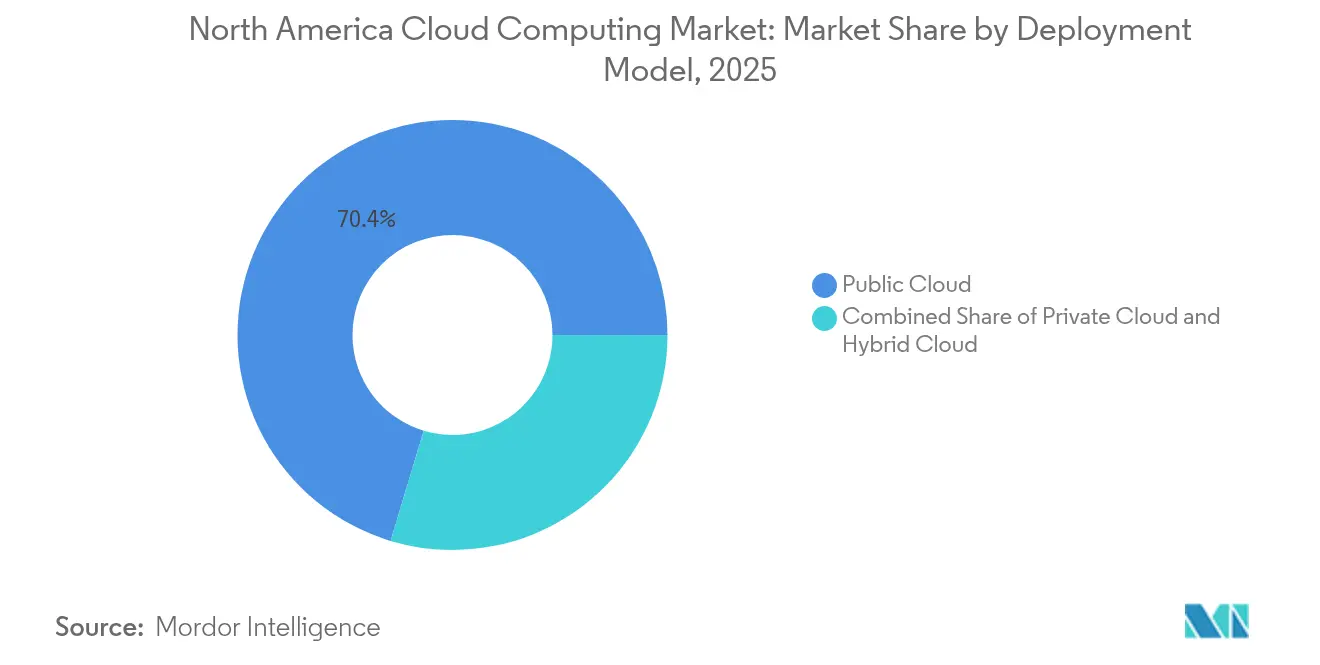

- By deployment model, public cloud captured 70.35% of the cloud computing market share in 2025, while hybrid cloud is advancing at a 22.05% CAGR through 2031.

- By service model, Software-as-a-Service led with 39.85% of the cloud computing market size in 2025; Platform-as-a-Service is set to grow at 25.51% CAGR to 2031.

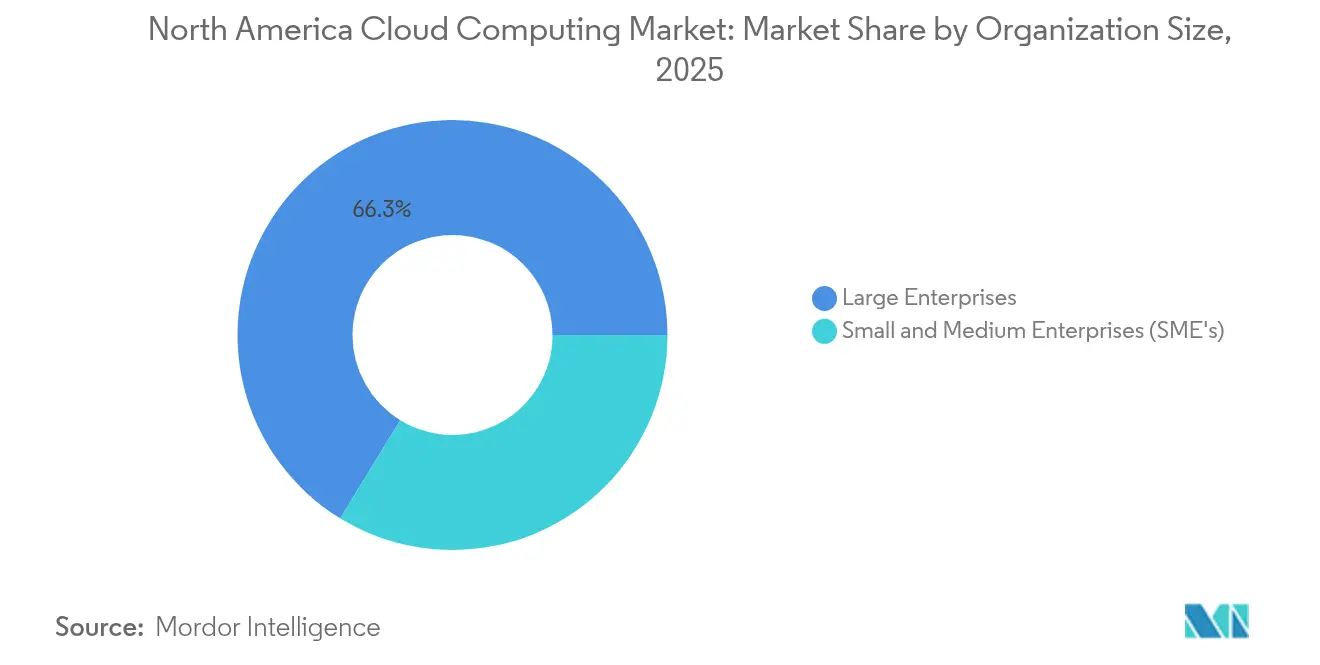

- By organization size, large enterprises held 66.25% revenue share in 2025, whereas SMEs are projected to post a 20.35% CAGR.

- By end-user vertical, BFSI commanded 24.05% of 2025 revenue, but healthcare is on track for an 17.65% CAGR to 2031.

- By geography, the United States controlled 88.62% of regional revenue in 2025; Canada is forecast to progress at a 16.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with North america forming one of the important contributors. Mordor Intelligence's global cloud computing market size report represents that cumulative total.

North America Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating digital-transformation & GenAI workloads | +4.2% | Global, concentrated in US tech hubs | Medium term (2–4 years) |

| Expansion of hyperscale data-center & edge regions | +3.8% | US (Virginia, Oregon), Canada emerging | Long term (≥4 years) |

| AI/ML & big-data analytics proliferation | +3.5% | North America core, spill-over to Mexico | Short term (≤2 years) |

| SMB cloud uptake amid vertical SaaS boom | +2.1% | US & Canada, early gains in Mexico | Medium term (2–4 years) |

| Renewable-energy PPAs enabling carbon-neutral builds | +1.8% | US renewable-rich states, Canada hydro regions | Long term (≥4 years) |

| Government incentives for domestic chip-to-cloud chains | +1.2% | US federal programs, provincial Canada schemes | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital Transformation and GenAI Workloads Drive Infrastructure Demand

Generative AI projects are amplifying compute density requirements and shifting enterprise spending toward GPU-rich instances across the cloud computing market. Major providers deployed tens of thousands of accelerators in 2024, yet average utilization lingered near 8% efficiency, signaling ample headroom for expansion.[1]Tom Claburn, “Big Cloud Deploys Thousands of GPUs for AI – Yet Most Appear Under-Utilized,” The Register, theregister.com Community Health Systems’ adoption of Google Cloud for clinical documentation and Highmark Health’s USD 2.7 million annual savings highlight sector-specific ROI, encouraging broader enterprise migration. Custom silicon programs, low-latency fabrics, and AI-optimized PaaS stacks are now core differentiators as vendors compete for GenAI-driven workloads within the cloud computing market.

Hyperscale Data Center Expansion Accelerates Regional Infrastructure Development

Amazon committed USD 30 billion across Pennsylvania and North Carolina the largest single cloud build in regional history creating 1,750 skilled roles and thousands of ancillary jobs. Microsoft’s USD 1.5 billion San Antonio campus and Google’s USD 1 billion Kansas City facility show a pivot from traditional Virginia-Oregon corridors toward energy-diverse states. Investments emphasize proximity to customers, renewable-energy availability, and diversified risk, pushing the cloud computing market toward a distributed, edge-friendly topology that balances performance with sustainability.

AI/ML and Big Data Analytics Proliferation Transforms Enterprise Computing

ServiceNow’s Workflow Data Fabric slashed service resolution times by 37% and lifted client revenue potential by 20% through real-time analytics, exemplifying how AI drives measurable gains.[2]Kevin Krewell, “ServiceNow Is Poised to Quantify Its Generative AI Revenue,” Forbes, forbes.com Oracle’s disclosure of a USD 30 billion annual cloud contract starting fiscal 2028 underscores the commercial magnitude of data-intensive migrations. State programs such as North Carolina’s Medicaid encounter platform, which processed 250 million transactions in its first year, further validate public-sector readiness for AI-centric workloads. These cases demonstrate that AI integration is no longer experimental; it is a production-scale imperative reshaping the cloud computing market.

SMB Cloud Uptake Accelerates Through Vertical SaaS Solutions

SMEs account for more than 99% of US businesses, and targeted investments now lower legacy barriers in the cloud computing market. Microsoft’s USD 1.3 billion Mexico initiative pairs local data centers with satellite connectivity to reach 30,000 SMEs and 5 million citizens by 2025.[3]Jordan Novet, “Microsoft Expects to Spend $80 Billion on AI-Enabled Data Centers in Fiscal 2025,” CNBC, cnbc.com Industry-specific SaaS bundles reduce customization overhead, letting smaller firms tap the same AI analytics, ERP, and cybersecurity stacks that were once enterprise-exclusive. As cost and complexity fall, SME demand becomes a durable tailwind for regional cloud revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory compliance & data-sovereignty complexity | –2.3% | US–Canada cross-border, Mexico emerging | Medium term (2–4 years) |

| Cloud-native talent shortage & wage inflation | –1.8% | US tech hubs, Canada urban centers | Short term (≤2 years) |

| Power-grid congestion delaying new regions | –1.5% | Virginia, Texas, California hotspots | Long term (≥4 years) |

| Water-usage restrictions for data-center cooling | –0.9% | Western US drought regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance and Data Sovereignty Complexity Challenge Cross-Border Operations

Financial institutions must align with a patchwork of US statutes, the CLOUD Act, and emerging provincial mandates that complicate multi-jurisdictional architectures.[4]ISACA Staff, “Cloud Data Sovereignty: Governance and Risk Implications,” ISACA, isaca.org Legal teams now embed encryption, key-management, and audit-logging requirements directly into contracting frameworks to satisfy regulators without crippling agility. Enterprises with Pan-North American footprints allocate larger budgets to legal-ops and compliance tooling, which slows roll-outs but ultimately fortifies trust in the cloud computing market.

Cloud-Native Talent Shortage and Wage Inflation Constrain Implementation Velocity

Demand for site reliability engineers, FinOps analysts, and AI platform specialists far exceeds supply, inflating wages and lengthening project timelines. Vendors are opening remote hubs, funding scholarships, and building apprenticeship programs Amazon’s data-center technician track is one example—to replenish the talent pool. Until these pipelines mature, skills scarcity remains a brake on the otherwise fast-moving cloud computing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Accelerate Enterprise Adoption

Public cloud accounted for 70.35% of the cloud computing market share in 2025, reflecting enterprises’ preference for instantly scalable resources. Hybrid cloud is forecast to expand at a 22.05% CAGR as organizations blend on-premises control with hyperscale economics, a trajectory that is redefining the cloud computing market. Cisco’s survey showing 82% hybrid adoption confirms that operational flexibility, innovation speed, and data-mobility options outweigh the complexity trade-off.

Hybrid frameworks increasingly anchor digital-core strategies because they avoid single-vendor lock-in and simplify compliance. Broadcom’s VMware Cloud Foundation 9 unifies management planes across public, private, and edge footprints, illustrating how platform advances are unlocking new portions of the cloud computing market. As more workloads migrate to containerized stacks, hybrid governance models will mature, bolstering the overall cloud computing industry.

By Service Model: PaaS Growth Outpaces Traditional Infrastructure Services

Software-as-a-Service held 39.85% of the cloud computing market size in 2025, driven by productivity suites and ERP renewals. Platform-as-a-Service is on track for a 25.51% CAGR, fueled by microservices, DevOps pipelines, and AI model-hosting demands. Developers prefer turnkey PaaS layers that abstract infrastructure chores, accelerating release cycles within the cloud computing market.

ServiceNow’s Workflow Data Fabric shows how modern PaaS solutions integrate data residency controls, event-stream processing, and AI orchestration in a single layer. Meanwhile, GPU-as-a-Service offerings sit at the boundary of IaaS and PaaS, letting customers rent accelerators without managing bare-metal clusters. These hybridized formats blur service-model lines yet expand addressable revenue, sustaining a flywheel that keeps the cloud computing market vibrant.

By Organization Size: SME Adoption Gains Speed Through Accessibility Improvements

Large enterprises retained 66.25% revenue share in 2025 as they migrate complex ERP, SCM, and analytics hubs. However, SMEs are projected to register a 20.35% CAGR, demonstrating how inclusive pricing tiers and vertical SaaS bundles unlock fresh pockets of the cloud computing market. Microsoft’s Mexico program exemplifies how localized regions and satellite backhaul can narrow connectivity gaps for smaller firms.

SME cloud strategies commonly start with accounting, e-commerce, or CRM workloads before extending to AI chatbots and predictive analytics. Pay-as-you-go billing, automated compliance packs, and guided migration playbooks lower adoption friction. As knowledge networks grow, SMEs will influence platform roadmaps, reinforcing a two-sided dynamic where big-ticket enterprise contracts coexist with high-volume SME deals across the cloud computing industry.

By End-User Verticals: Healthcare Growth Outpaces Traditional Leaders

BFSI maintained 24.05% revenue in 2025 by modernizing digital banking stacks, implementing real-time AML engines, and adopting zero-trust architectures. Healthcare, projected at an 17.65% CAGR, is rapidly scaling telemedicine, EHR migrations, and AI-assisted diagnostics, carving out a larger slice of the cloud computing market size. Highmark Health’s Google Cloud integration saved USD 2.7 million annually while improving data access for 7 million members, offering a template for cost-efficient modernization.

Manufacturing, retail, and logistics continue leveraging IoT and predictive supply-chain analytics, while media firms transition to cloud-native content pipelines. Government programs, such as North Carolina’s Medicaid platform, showcase how cloud architectures can process hundreds of millions of transactions at scale. The diversity of use cases across verticals underscores the cloud computing market’s resilience.

Geography Analysis

The United States captured 88.62% of regional revenue in 2025, bolstered by USD 150 billion in long-term Amazon commitments and Microsoft’s USD 80 billion FY 2025 spend that is more than half directed to domestic projects. Traditional hubs in Virginia and Oregon still expand, yet secondary sites in Texas, Kansas, and the Carolinas are catching up thanks to renewable-energy contracts and tax incentives. The Federal-State Modern Grid Deployment Initiative, covering 21 states, aims to raise data-center power availability as electricity demand from cloud facilities could climb from 4% to 9% of total US generation by 2030. These measures reflect the country’s determination to preserve leadership in the cloud computing market.

Canada is advancing at a 16.95% CAGR, supported by CAD 149 million in Ontario digital-health funding for 2023-2024 that is catalyzing EHR migrations and telehealth expansion. Hyperscale entrants position Canadian regions as data-sovereignty-compliant alternatives for multinationals. Ample hydro resources and cooler climates reduce PUE ratios, improving sustainability metrics for the cloud computing market.

Mexico is emerging as a strategic bridge to Latin America. Amazon’s USD 5 billion Querétaro campus and Microsoft’s multi-year program targeting 30,000 SMEs illustrate confidence in local demand. The USMCA framework simplifies cross-border digital trade, yet network latency and skills gaps remain challenges. Continued investment in fiber corridors, edge nodes, and vocational training will determine how quickly Mexico captures a greater portion of the regional cloud computing market.

Coverage of the cloud computing market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, Asia, and South America, alongside detailed country-level intelligence for Canada, United States, United Kingdom, Germany, Italy, and Japan, each shaped by local operating conditions.

Competitive Landscape

North America’s cloud computing market shows moderate concentration, with Amazon Web Services, Microsoft Azure, and Google Cloud surpassing 60% combined revenue in 2024. AWS leverages diversified service breadth and a 15-year, USD 150 billion expansion plan to defend share. Microsoft’s integration of Copilot-infused apps and its USD 1.5 billion San Antonio build signal a deep commitment to AI-optimized infrastructure. Google Cloud differentiates through analytics, machine learning, and carbon-free energy pledges, recently signing a 128 MW Texas solar PPA.

Specialization is growing. Broadcom’s VMware Cloud Foundation 9 targets regulated sectors seeking private-cloud control without abandoning public-cloud agility. IBM’s acquisition of Applications Software Technology LLC widens Oracle Cloud Application expertise for public-sector migrations. Oracle, buoyed by its USD 30 billion annual contract, capitalizes on customers that prefer vertically integrated stacks. Edge services, sustainability dashboards, and AI-tuned PaaS layers are now battlegrounds where newer entrants and niche vendors can chip away at incumbent positions within the cloud computing market.

North America Cloud Computing Industry Leaders

Amazon.com Inc. (AWS)

Google LLC

Microsoft Corporation

Salesforce Inc

Adobe Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Oracle shares rose after revealing a cloud contract projected to surpass USD 30 billion annually beginning fiscal 2028.

- June 2025: Amazon unveiled a USD 10 billion data-center program in North Carolina, creating 500 high-skilled jobs.

- May 2025: ServiceNow introduced Workflow Data Fabric, an integrated platform to streamline AI-driven processes in large enterprises.

- March 2025: Microsoft committed USD 1.5 billion to expand its San Antonio, Texas, campus, adding AI security and resiliency features.

North America Cloud Computing Market Report Scope

Cloud computing provides computing services via the Internet. These services encompass servers, storage, databases, networking, software, analytics, and intelligence. The primary benefits include accelerated innovation, flexible resources, and economies of scale. Typically, customers pay solely for the cloud services they utilize. This model reduces operational costs, enhances infrastructure efficiency, and allows for scaling in response to evolving business needs.

The North American cloud computing market is segmented by type (public cloud [IaaS, PaaS, SaaS], private cloud, and hybrid cloud), by organization size (SMEs, and large enterprises), end-user verticals (manufacturing, education, retail, transportation, and logistics, healthcare, BFSI, telecom, and IT, Government and public sector, others (utilities, media & entertainment, etc.), and geography (United States and Canada). The market size and forecasts regarding value (USD) for all the above segments are provided.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Small and Medium Enterprises (SME's) |

| Large Enterprises |

| Manufacturing |

| Education |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Utilities |

| Media and Entertainment |

| Others |

| United States |

| Canada |

| Mexico |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| By Organization Size | Small and Medium Enterprises (SME's) |

| Large Enterprises | |

| By End-user Verticals | Manufacturing |

| Education | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Utilities | |

| Media and Entertainment | |

| Others | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the size of the North America cloud computing market in 2026?

The cloud computing market in North America is valued at USD 380.5 billion in 2026.

How fast is the market expected to grow by 2031?

The market is projected to reach USD 811.04 billion by 2031, expanding at a 16.34% CAGR during 2026-2031.

Which deployment model holds the largest revenue share?

Public cloud leads with 70.35% of the regional revenue in 2025.

Which segment is growing the fastest?

Hybrid cloud is the fastest-growing deployment model, forecast to post a 22.05% CAGR through 2031.

What is driving small and medium enterprise (SME) adoption?

Vertical SaaS solutions and targeted hyperscale investments are lowering entry barriers, helping SMEs register a 20.35% CAGR.

What are the main constraints facing providers?

Data-sovereignty regulations, talent shortages, and power-grid congestion are the key challenges slowing some new cloud region launches.

Page last updated on: