Cloud Discovery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

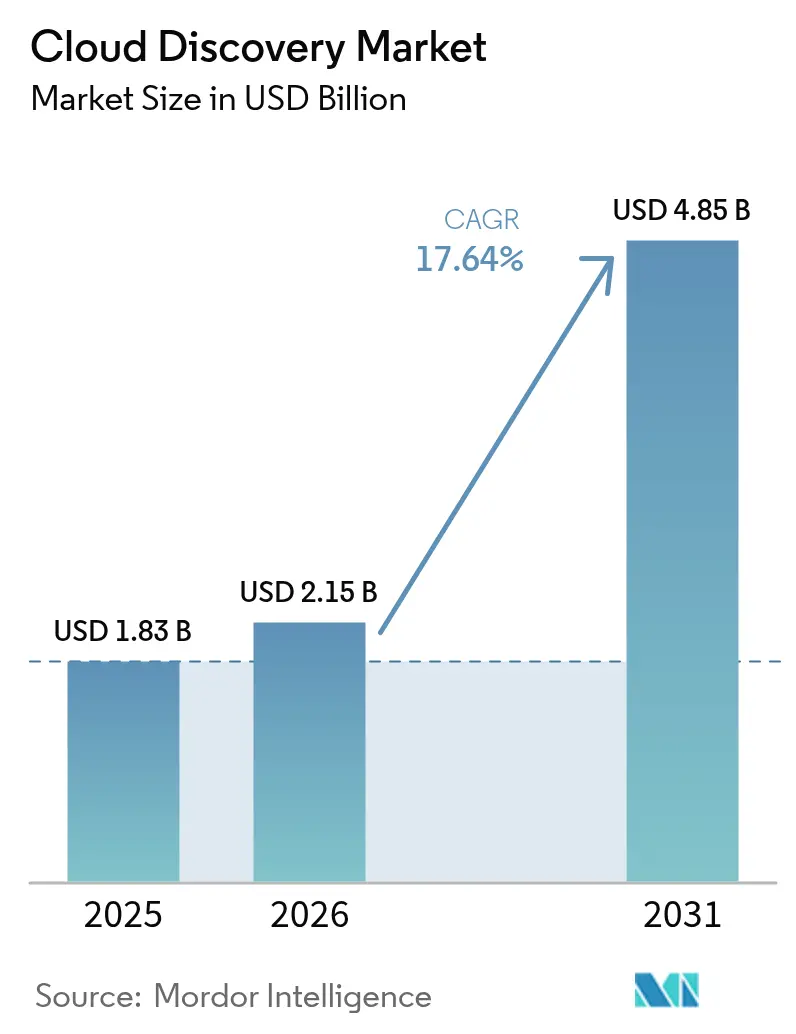

| Market Size (2026) | USD 2.15 Billion |

| Market Size (2031) | USD 4.85 Billion |

| Growth Rate (2026 - 2031) | 17.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Discovery Market Analysis by Mordor Intelligence

The Cloud Discovery market size is expected to grow from USD 1.83 billion in 2025 to USD 2.15 billion in 2026 and is forecast to reach USD 4.85 billion by 2031 at 17.64% CAGR over 2026-2031. Rapid multi-cloud adoption, stricter zero-trust mandates, and sustainability reporting rules are reshaping enterprise security architecture by making continuous asset visibility a board-level priority. Vendors that embed agentless discovery, automated classification, and FinOps-ready analytics into their platforms are gaining share as enterprises shift from one-time audits to real-time monitoring. North American demand remains anchored in federal compliance frameworks, while Asia-Pacific's sovereign-cloud initiatives are accelerating regional uptake. Budget constraints at smaller organizations and persistent credential-access hurdles in segmented networks moderate overall growth, but sustained innovation in AI-driven automation continues to expand total addressable demand.

Key Report Takeaways

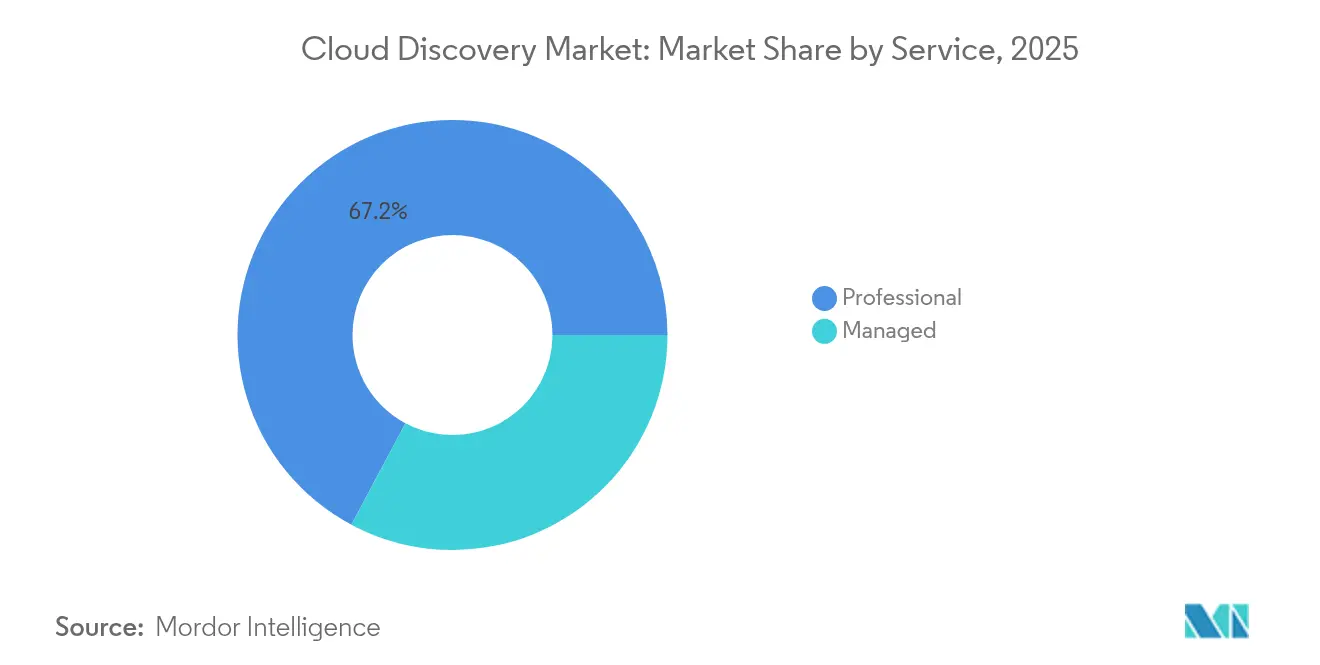

- By service, professional services led with 67.20% revenue share in 2025, while managed services are forecast to advance at a 23.28% CAGR through 2031.

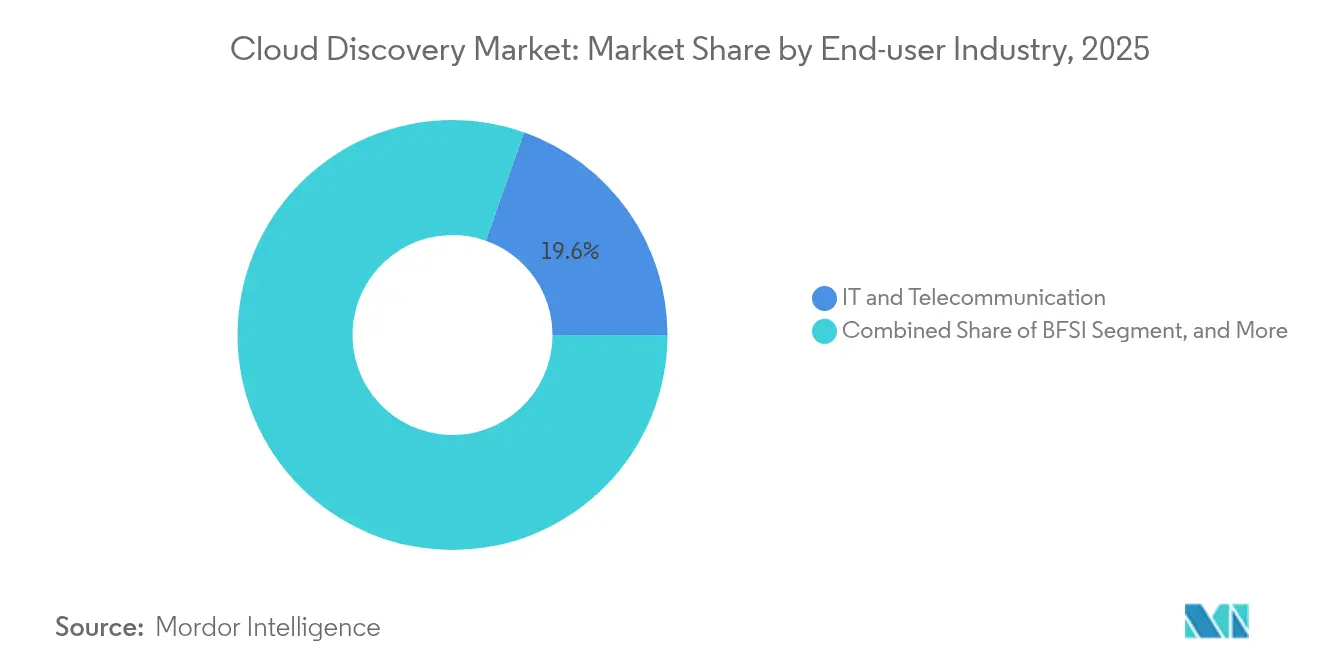

- By end-user industry, IT and Telecommunication held 19.60% share of the cloud discovery market size in 2025; Healthcare is projected to grow at a 22.12% CAGR between 2026-2031.

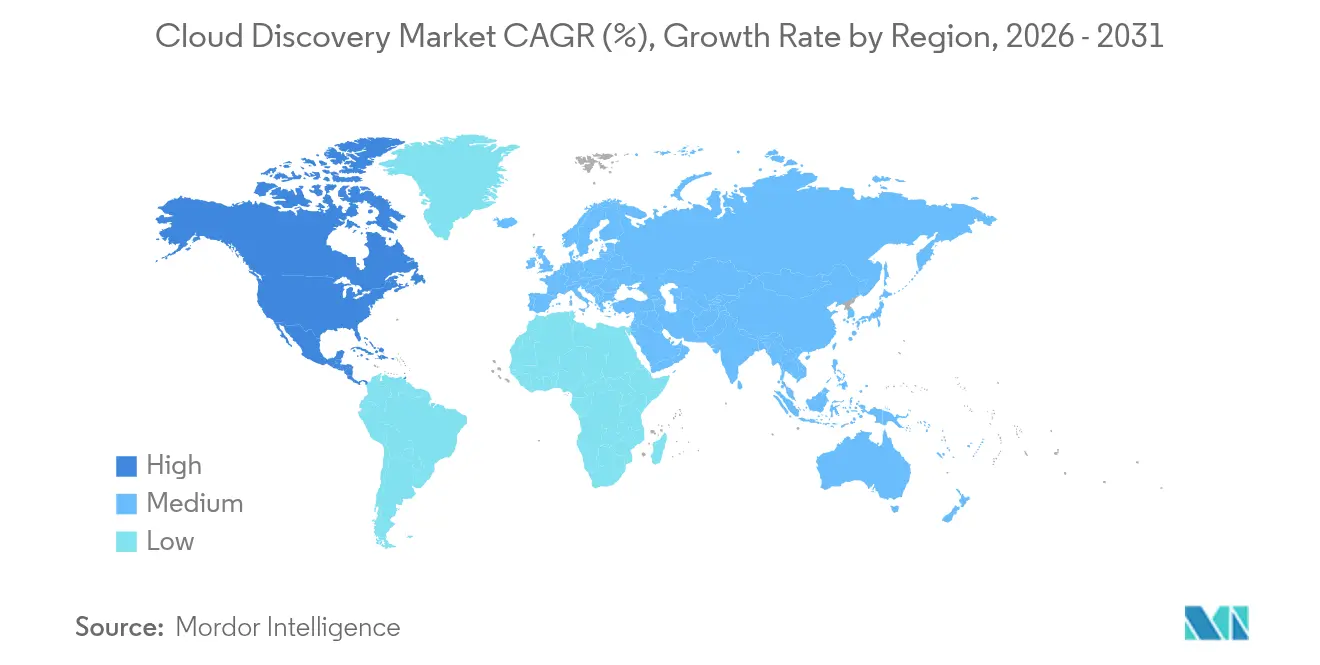

- By geography, North America commanded 37.40% of the cloud discovery market share in 2025, whereas Asia-Pacific is expected to register the fastest 21.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Discovery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing multi-cloud adoption among Global 2000 enterprises | +4.20% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Rising need for real-time configuration visibility to harden cyber-resilience | +3.80% | Global, emphasis on regulated industries | Short term (≤ 2 years) |

| Convergence of FinOps and ITOM driving discovery modules into cost-governance stacks | +2.90% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| GenAI-powered auto-classification reducing CMDB maintenance cost | +2.10% | Global, early adoption in tech-forward firms | Long term (≥ 4 years) |

| Mandatory asset-discovery clauses in new U.S. Federal Zero-Trust contracts | +1.60% | National – United States (Federal and Defense agencies) | Short term (≤ 2 years) |

| Sustainability reporting rules (CSRD, SEC) demanding cloud-asset inventories | +1.80% | Regional – EU (CSRD), U.S. (SEC), spreading globally via supply-chain mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Multi-Cloud Adoption Among Global 2000 Enterprises

Organizations now run production workloads across an average of 3.2 public clouds, a strategy that boosts resilience but fragments visibility. Discovery engines must therefore interface with multiple provider APIs, container orchestration layers, and service meshes in near real time. Early adopters in Asia are compelled to run parallel domestic and international cloud estates due to sovereign cloud directives, reinforcing the demand for platform-agnostic discovery. ServiceNow’s integration with a leading hyperscaler illustrates how workflow automation and discovery are converging to shorten response times across hybrid estates.[1]ServiceNow, “Patent US11184242B2: Automated Discovery Processes,” servicenow.comWithout these capabilities, enterprises report discovery lags of up to 72 hours, exposing security and compliance blind spots that regulators increasingly penalize.

Rising Need for Real-Time Configuration Visibility to Harden Cyber-Resilience

Misconfigurations continue to account for the overwhelming majority of cloud breaches, prompting regulators to enforce continuous monitoring requirements. The U.S. Department of Defense’s updated cloud clause obliges contractors to track data location and remediate drift instantly. Healthcare providers, subject to HIPAA and ransomware threats, are leading investments in real-time discovery tied to data-security-posture management. Vendors integrating discovery with AI-driven threat analytics claim mean-time-to-detect reductions of more than 30%. Manufacturing firms report double-digit improvements in overall equipment effectiveness after embedding continuous asset discovery within industrial IoT environments.

Convergence of FinOps and ITOM Driving Discovery Modules Into Cost-Governance Stacks

Cloud spending now constitutes a top-three operating expense at many enterprises, driving CFOs to demand resource-level attribution. Discovery platforms enriched with tagging automation link consumption data to business units, enabling organizations to achieve savings of 15-25% in year one when adopting FinOps-aligned governance. A large manufacturer utilizing an integrated cost-governance suite reduced its annual cloud expenditures by USD 300,000, primarily by eliminating orphaned resources. In this space, acquisitions underscore the importance of platform collaboration. VMware’s CloudHealth integration embeds discovery functions directly within financial dashboards, thereby widening the total addressable demand.[2]VMware, “CloudHealth FinOps Overview,” vmware.com

GenAI-Powered Auto-Classification Reducing CMDB Maintenance Cost

Large-language-model augmentation now produces asset descriptions, dependency maps, and compliance labels with accuracy rates exceeding 95%. ServiceNow’s patented discovery engine applies GenAI to automate relationship mapping and CMDB enrichment, cutting manual maintenance costs by up to 60% within 18 months. Generated insights free engineers to focus on remediation rather than data curation, while higher data fidelity accelerates audit readiness. Security operations teams also benefit from faster root-cause analysis when every cloud element is continuously classified.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent credential-access hurdles in highly segmented networks | −0.6% | Global – especially in highly regulated industries (BFSI, healthcare, government) | Medium term (2–4 years) |

| SMB budget squeeze for discovery licences and staff | −0.8% | High in emerging economies (India, Southeast Asia, Latin America) | Short term (≤ 2 years) |

| Sovereign-cloud restrictions limiting discovery scope outside region | −0.5% | Regional – strong in EU, GCC, and APAC countries with data-localization laws | Long term (≥ 4 years) |

| Shadow-IT growth outpacing discovery coverage despite tool upgrades | −0.7% | Global – most pronounced in large enterprises with hybrid or multi-cloud setups | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Persistent Credential-Access Hurdles in Highly Segmented Networks

Zero-trust designs intentionally restrict lateral movement, requiring discovery engines to authenticate separately in every micro-segment. Financial services institutions must also segregate business-unit data by jurisdiction, multiplying credential overhead.[3] Microsoft, “Financial-Services Cloud Compliance Framework,” microsoft.com Healthcare providers face comparable challenges when isolating protected health information. Agentless approaches alleviate some friction yet still struggle with depth, forcing trade-offs between breadth and granularity. Enterprises estimate that 40-60% of discovery budgets are consumed by credential management tasks alone.

SMB Budget Squeeze for Discovery Licences and Staff

Comprehensive discovery suites often start above USD 50,000 per year, a price point out of reach for firms with fewer than 500 employees. Implementation further demands cloud-security skill sets that SMBs cannot readily recruit. Although managed discovery services offer pay-as-you-go options, many small firms prefer capital over operating expenditure and hesitate to grant third parties persistent access to sensitive workloads. As a result, approximately one-third of potential market demand remains addressable only through lower-cost, simplified offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Professional Services Lead Market Transformation

Professional services captured 67.20% of the cloud discovery market in 2025, underscoring enterprises’ reliance on specialized architects to integrate discovery engines with complex identity, network, and workflow layers. Engagement scopes typically encompass multi-cloud API mapping, policy tuning, and CMDB population tasks that require deep vendor expertise. Managed services, however, are forecast to accelerate at a 23.28% CAGR through 2031 as enterprises recognize that discovery must run continuously rather than ad hoc.

Growth in managed offerings signals a structural shift in spending from project-based deployments to subscription models anchored in ongoing visibility. ServiceNow’s managed discovery subscriptions contributed materially to its USD 2,866 million Q4 2024 recurring revenue, illustrating the appeal of outcome-based contracts. Manufacturing clients adopting always-on discovery have reported 10-15% boosts in operational effectiveness through faster anomaly detection. The shift also benefits vendors, as automated classification reduces marginal delivery costs and widens adoption among organizations lacking full-time cloud-security staff.

By End-User Industry: Healthcare Accelerates Past Traditional Leaders

The IT and Telecommunication sector remained the leading adopter, holding 19.60% of the cloud discovery market size in 2025, sustained by early cloud penetration and complex, latency-sensitive workloads. Yet Healthcare’s 22.12% forecast CAGR positions it to outpace traditional leaders as regulators tighten safeguards for electronic health records and connected-care platforms. The sector’s reliance on distributed telemedicine and imaging workloads heightens exposure to misconfigurations, reinforcing demand for continuous discovery.

Provider groups implementing always-on asset inventories report that audit preparation times have dropped from weeks to days, while avoiding HIPAA penalties that can exceed USD 10 million per violation. Pharmaceutical manufacturers also extend their discovery to laboratory information systems and edge devices that support clinical trials. BFSI continues to invest steadily for regulatory reasons, whereas Retail, Consumer Goods, and Industrial Manufacturing tie discovery rollouts to omnichannel and supply-chain digitization initiatives that blend OT and IT assets.

Geography Analysis

North America held 37.40% of 2025 revenue thanks to early enterprise cloud adoption, a mature hyperscale ecosystem, and federal mandates that embed discovery clauses in government contracts. Financial institutions, defense contractors, and healthcare networks represent the largest buyer clusters, while Canadian firms increasingly adopt managed discovery to address cross-border data movement. Competition remains intense as established IT-service-management vendors integrate discovery into broader workflow suites, yet market saturation among Fortune 1000 firms tempers incremental growth.

The Asia-Pacific region is projected to post a 21.34% CAGR from 2026 to 2031, the fastest worldwide, driven by sovereign-cloud policies and localization laws that require companies to inventory assets at the regional level. More than one-third of Asia-Pacific governments plan to deploy sovereign clouds by 2026, compelling enterprises to maintain granular records of workload residency. Data-center capacity in the region surpassed 12,000 MW in 2024, with an additional 14,000 MW under construction, underscoring the need for hybrid-cloud visibility. Industries such as financial services and sovereign defense lead adoption, while emerging digital-native enterprises accelerate managed-service uptake.

Europe represents a sizable, compliance-driven market where GDPR and the Corporate Sustainability Reporting Directive make discovery essential for both data protection and emissions accounting. Enterprises leverage discovery engines to map data flows and assign Scope 3 carbon factors, enabling transparent ESG disclosures. Uptake is most pronounced in Germany, France, and the Nordics, where energy-efficient cloud zones intersect stringent data-residency rules. While growth rates are lower than in Asia-Pacific, vendors benefit from long contract tenures due to high switching costs tied to regulatory certification. South America and the Middle East & Africa remain nascent but promising; telco-led cloud rollouts and public-sector digitization programs are laying the groundwork for future demand, provided pricing aligns with constrained IT budgets.

Regulatory Landscape

Cloud discovery deployments are increasingly shaped by security and sovereignty regimes that emphasize continuous visibility and auditable controls across hybrid and multi-cloud estates. In the United States, federal procurement and guidance anchor requirements around zero trust and protection of sensitive data, with NIST updates such as SP 800-228 (March 2026) on API protection for cloud-native systems and SP 800-172 Rev. 3 (finalized May 13, 2026) strengthening enhanced security requirements used to protect Controlled Unclassified Information in nonfederal systems. FedRAMP also moved toward more persistent, automated assessment constructs with its 2026 updates (June 24, 2026), reinforcing the shift from periodic attestations to machine-verifiable monitoring that depends on accurate, near-real-time asset inventories.

In Europe, cloud discovery requirements are influenced by certification and sovereignty initiatives alongside GDPR-driven controls. Germany's BSI updated its Cloud Computing Compliance Controls Catalogue (C5:2026), incorporating requirements aligned with evolving ENISA cloud certification work, which raises the bar for evidence collection, logging, and control mapping across cloud resources. The European Commission Cloud Sovereignty Framework (October 2025) further elevates data residency and operational independence concerns, pushing enterprises and service providers to maintain region-scoped inventories and telemetry that can be demonstrated during audits and customer due diligence.

Value Chain Analysis

The cloud discovery value chain begins with cloud platform and SaaS data sources, where AWS, Microsoft Azure, Google Cloud, VMware-based environments, Kubernetes layers, and enterprise SaaS expose configuration and telemetry through APIs. Discovery vendors and IT operations platforms ingest these signals using agentless API connectors, optional agents, and network interrogation, then normalize, classify, and map relationships to populate CMDBs and service graphs used for ITSM, ITOM, and security workflows. Differentiation concentrates in normalization logic, relationship mapping, auto-classification, and integration breadth across identity, network segmentation, and multi-account structures, since credentialing and permissions are recurring operational bottlenecks.

Downstream, systems integrators and professional services teams implement discovery at scale by aligning identity and access policies, tagging standards, and workflow automation, and by integrating outputs into CMDB-driven processes such as incident response, change governance, and cost allocation. Managed service providers increasingly operate discovery as an always-on service, maintaining connectors, permissions, and coverage for dynamic cloud estates, while hyperscaler marketplaces and platform ecosystems distribute connectors and integrations that accelerate adoption. Feedback loops from security posture management and FinOps teams drive ongoing tuning, as discovery outputs become inputs for compliance evidence, drift detection, and cost attribution across business units.

Competitive Landscape

The cloud discovery market exhibits moderate fragmentation, with the top five vendors accounting for roughly 55% of global revenue. Incumbent IT-service-management providers extend existing CMDB and workflow portals, leveraging deep enterprise relationships to upsell discovery. ServiceNow alone reported 2,109 customers with annual contract value above USD 1 million, highlighting the power of installed-base expansion.

Strategic acquisitions are reshaping competitive dynamics. Fortinet’s acquisition of Lacework added 225 AI and cloud-security patents, broadening its Security Fabric for unified on-premises-to-cloud coverage. Akamai’s purchase of an API-security specialist and Tenable’s entry into cloud-data posture management illustrate horizontal moves into adjacent controls. Patent filings-such as ServiceNow’s auto-discovery configuration patent and IBM’s pattern-based cloud transformation patent-signal a race to automate classification at scale, lowering total cost of ownership for buyers.

Disruptors emphasize agentless deployment and rapid time-to-value. While they lack the depth of lifelong CMDBs, their low-touch models appeal to mid-market customers. Rumors of a multibillion-dollar hyperscaler acquisition of one such specialist underscore strategic interest in turnkey discovery to complement broader security clouds. Competitive advantage increasingly hinges on integrating sustainability metrics and FinOps dashboards, platforms that correlate asset inventories with carbon disclosures and cost allocation stand to win multi-year enterprise commitments.

Cloud Discovery Industry Leaders

ServiceNow Inc.

BMC Software Inc.

Amazon Web Services Inc.

Microsoft Corp.

McAfee LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is vendor-neutral normalization and interchange of asset inventory and topology across heterogeneous environments, reducing lock-in and simplifying multi-vendor governance. Emerging technical efforts such as Open Resource Discovery (ORD) specifications and OSIRIS JSON focus on standardizing how resources and relationships are described, while network inventory standardization work in the IETF (draft-ietf-ivy-network-inventory-yang) supports more consistent reporting across network domains. These initiatives align with enterprise needs to reconcile cloud API inventories, network views, and CMDB records into a single source of truth, particularly as organizations operate multiple public clouds alongside on-premises and sovereign-cloud footprints.

FinOps and governance integration also creates near-term expansion room for discovery platforms that connect real-time inventory to ownership, usage, and policy outcomes. Flexera's 2026 State of the Cloud report notes the operationalization of cloud governance, citing 71% of organizations with a cloud center of excellence and 63% using a FinOps team, which increases demand for reliable tagging, attribution, and detection of orphaned resources. On the services side, programs described by Capgemini (May 2026) emphasize multi-method discovery (agent-based, agentless, network, and API-based) and correlation across CMDBs and cloud platforms, signaling a buying pattern that prioritizes continuous discovery operations over one-time audits and supports managed discovery offerings for organizations constrained by skills and credential-management overhead.

Recent Industry Developments

- July 2026: BMC introduced governed AI agent capabilities for enterprise workflows spanning hybrid cloud and mainframe operations. By extending control and automation across heterogeneous environments, the announcement supports discovery and inventory use cases that rely on unified visibility into where operational agents and related resources are deployed.

- April 2025: Upwind acquired Nyx Security to enhance runtime protection through embedded application insights. The deal strengthened cloud runtime visibility signals that can complement discovery tools by improving context on workloads and dependencies during continuous monitoring.

- December 2024: ServiceNow and AWS expanded their strategic collaboration with new capabilities focused on accelerating AI transformation across enterprise environments. Deeper integration between workflow automation and cloud platform services reinforces the role of discovery-fed service graphs and inventories in operating and governing hybrid estates.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software and related services that help organizations find, inventory, and monitor cloud use and cloud resources, including shadow IT applications, so security and IT teams can improve visibility and control.

Scope exclusions: We exclude general on-premises asset discovery tools that do not materially identify cloud application usage or cloud resource footprints.

Segmentation Overview

- By Service

- Professional

- Managed

- By End-user Industry

- IT and Telecommunication

- BFSI

- Retail and Consumer Goods

- Industrial Manufacturing

- Healthcare

- Other End-user Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting structure of the model and to keep assumptions realistic before we spoke with industry participants. We referred to public sources such as NIST and other cybersecurity guidance, US SEC filings, cloud governance and security publications from agencies like CISA, and standards references such as ISO and SOC reporting guidance where relevant. We also used cloud adoption and digital economy indicators from sources such as the World Bank, OECD, and regional telecom and IT association publications to sense-check demand direction.

To translate the story into numbers, we pulled supporting signals from company annual reports, investor presentations, and product documentation that describes API based discovery workflows, plus reputable press coverage of cloud security and IT operations changes. Where needed, we also checked subscriptions that compile company financials and news, patent databases, and a global contracts and tenders feed to validate vendor activity patterns and buying cycles. These desk sources are not exhaustive, and we used additional public references during the research to collect, validate, and clarify specific data points.

Primary Interviews and Surveys

Primary discussions were run with buyers and practitioners who handle cloud visibility and governance, along with people closer to delivery such as managed service providers and implementation partners. We used these interviews to confirm what is counted as cloud discovery in live deployments, how tools are priced (subscription versus service-led), and which budget drivers are changing across major regions.

The inputs were also used to pressure-test desk assumptions on adoption rates, renewal behavior, and typical coverage in multi-cloud and hybrid environments, before the final totals and forecasts were signed off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 45% |

| Mid tier: 55% | Functional/Unit leaders: 37% | EMEA: 34% |

| Smaller Players: 14% | Managers: 51% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build-up where cloud adoption intensity by region is translated into likely discovery needs, and then filtered through security and IT governance spend patterns to estimate addressable budgets. Once that structure is in place, we corroborate totals with selective bottom-up checks, including sampled vendor revenue relevance, typical subscription price ranges, and channel feedback on deal sizes, and then adjust any obvious over- or under-counts.

Key inputs tracked in the model include multi-cloud and hybrid usage penetration, policy pressure around shadow IT, compliance requirements that force asset visibility, service mix between professional and managed engagements, and the shift toward API based discovery coverage versus manual tracking. For the forecast, we use scenario analysis supported by trend lines in cloud workload growth and expected security governance tightening, then align the slope with what interviewees report in budget planning. Where bottom-up information is thin for smaller suppliers or private firms, we use conservative share ranges anchored to buyer adoption and observed pricing bands, before final numbers are finalized.

Data Validation & Update Cycle

Outputs are checked against independent signals, including cloud security spend direction, disclosed recurring revenue trends from relevant vendors, and regional cloud adoption indicators, so the results do not drift away from observed demand behavior. When large variances show up, we reopen assumptions, test outliers, and trigger follow-up calls with select participants to understand whether the change is scope-related, timing-related, or driven by pricing.

Before sign-off, the model goes through multi-step internal reviews where calculations are rechecked and key assumptions are challenged, then the narrative is aligned to the final numbers. The dataset is refreshed on an annual cycle, with interim updates when material events occur, such as major policy changes, large cloud security incidents, or sharp macro shifts. Right before delivery, an analyst performs a fresh pass so clients receive the most current view available.

Mordor Intelligence's Cloud Discovery Market Estimate Compared With Other Published Estimates

Published cloud discovery market values can look different because each publisher draws the market line in its own way and also picks different base years, currencies, and growth paths. These differences are most visible when an estimate includes adjacent categories or counts broader cloud security tools that are not strictly discovery.

In this study, the key gap drivers are whether managed services are counted consistently with software, whether shadow IT discovery is treated as a subset or as part of a wider cloud governance bundle, and how pricing is handled as more usage shifts to multi-cloud. If currency conversion timing or base year changes, the current-year value also moves even when the long-term story stays similar, which is why refresh cadence matters for fast-moving software categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.15 B (2026) | |

| Global Consultancy A | USD 1.20 B (2024) | Uses an earlier base year and a component scope that can undercount managed service revenues, and it may treat shadow IT discovery as part of a broader IT operations bundle rather than a dedicated cloud discovery spend line. |

| Industry Publisher B | USD 1.42 B (2025) | Runs a longer forecast window with different inflation and pricing progression assumptions, and the definition can blend discovery with wider cloud security controls, which shifts what is counted in the current-year total. |

The table shows that most of the spread comes from year selection and what gets bundled into the definition, especially around managed services and neighboring cloud security capabilities. By keeping the count tied to API led identification of cloud services and unmanaged cloud application use, and then validating adoption and pricing through buyer conversations, the totals stay closer to what organizations actually purchase, a scope choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the cloud discovery market?

The cloud discovery market reached USD 2,154 million in 2026.

How fast is the cloud discovery market expected to grow?

The market is forecast to expand at an 17.64% CAGR, reaching USD 4,854 million by 2031.

Which service segment is growing the fastes

Managed services are projected to post a 23.28% CAGR between 2026-2031 as enterprises seek continuous monitoring.

Why is Healthcare the fastest-growing end-user segment?

Healthcare faces stringent HIPAA and ransomware risks, driving a 22.12% CAGR for discovery solutions through 2031.

Which region will outpace others in growth?

APAC is expected to record a 21.34% CAGR, fueled by sovereign-cloud mandates and data-localization laws.

What key technology trend is reshaping discovery platforms?

GenAI-powered auto-classification is cutting CMDB maintenance costs by up to 60% while boosting accuracy to 95%.

Page last updated on: