Asia-Pacific Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

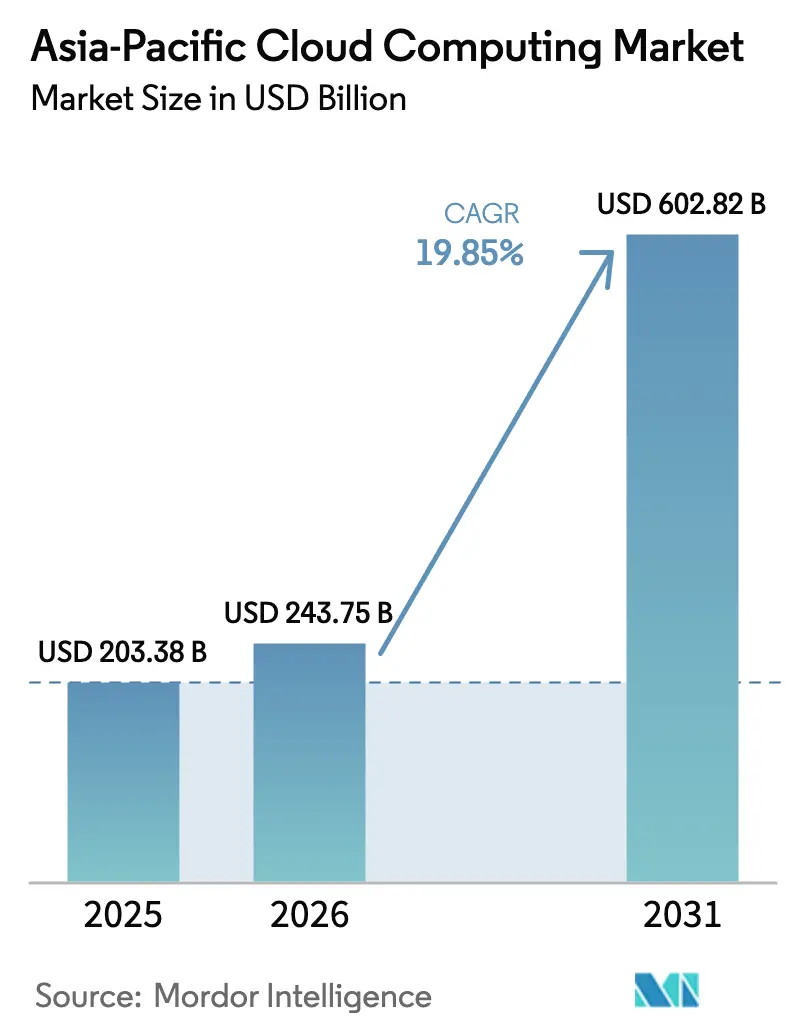

| Base Year Market Size (2025) | USD 203.38 Billion |

| Market Size (2026) | USD 243.75 Billion |

| Market Size (2031) | USD 602.82 Billion |

| Growth Rate (2026 - 2031) | 19.85% CAGR |

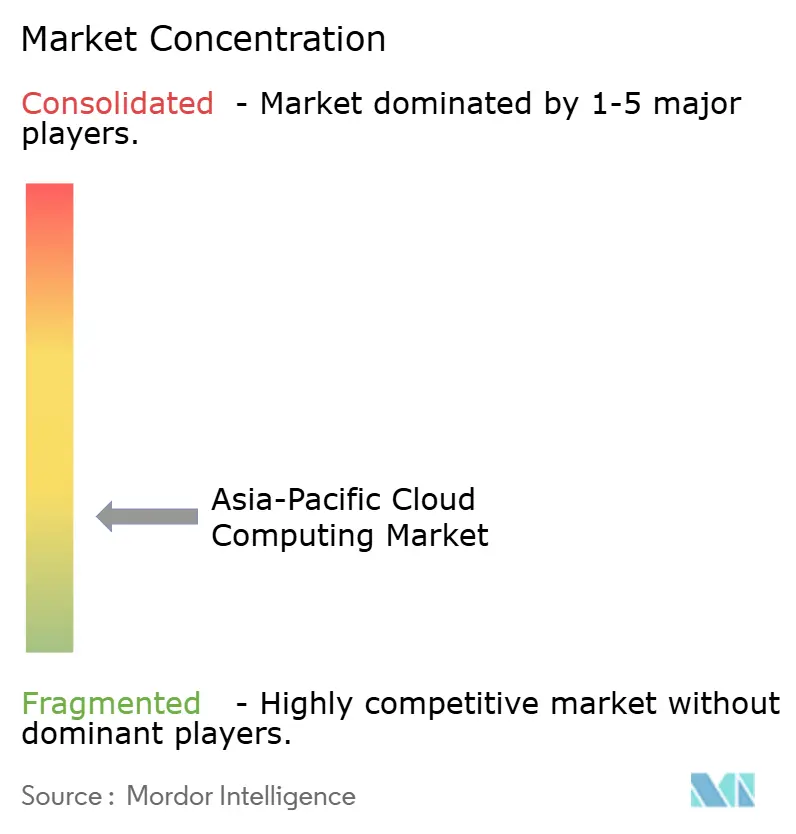

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Cloud Computing Market Analysis by Mordor Intelligence

The Asia-Pacific Cloud Computing Market size was valued at USD 203.38 billion in 2025 and estimated to grow from USD 243.75 billion in 2026 to reach USD 602.82 billion by 2031, at a CAGR of 19.85% during the forecast period (2026-2031). Sovereign-AI policies and government cloud-first mandates are unlocking regulated-sector spending, while hyperscalers deploy new capacity in tier-2 metros to bring workloads closer to users. GPU-rich instances built for generative-AI workloads are reshaping data-center designs, and 5G-edge partnerships between telcos and cloud providers are lowering latency for real-time applications. Public cloud still commands the largest share, yet hybrid architectures record the fastest growth as enterprises balance performance with data-sovereignty and vendor-lock-in considerations. Competitive intensity is rising as global hyperscalers face domestic champions that bundle compliance with localized services, making infrastructure efficiency and regulatory alignment decisive factors.

Key Report Takeaways

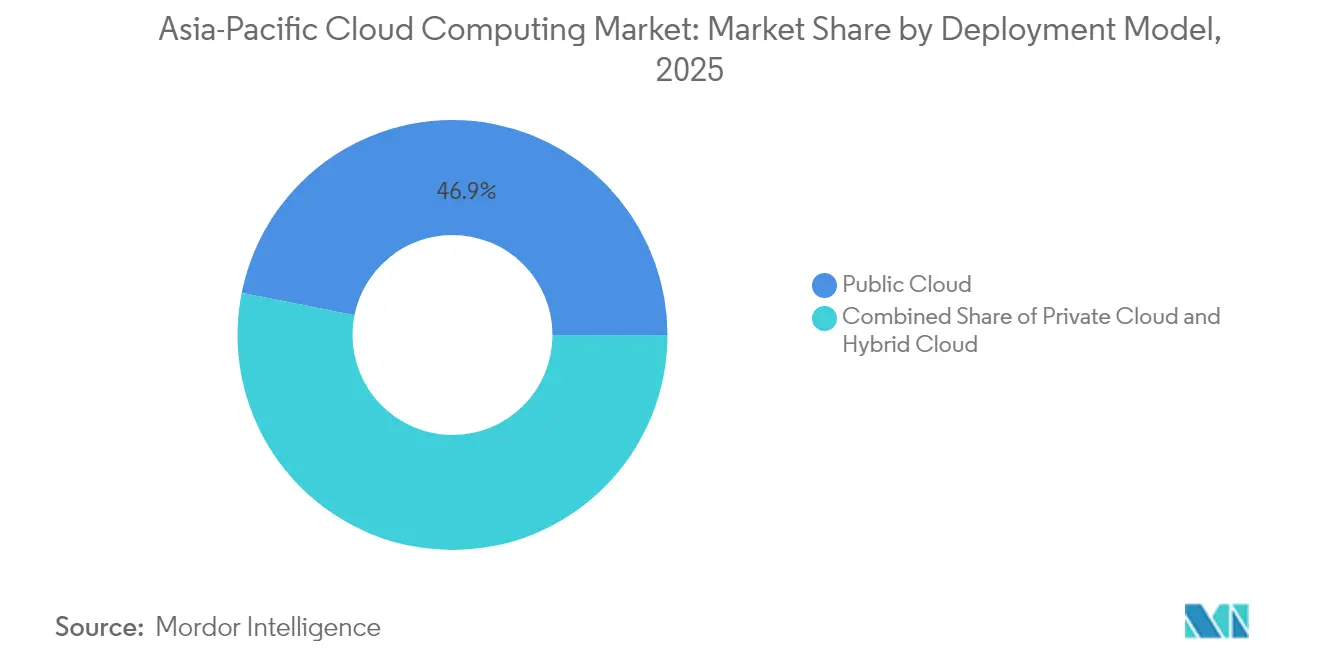

- By deployment model, public cloud led with 46.85% of the Asia-Pacific cloud computing market share in 2025; hybrid cloud is projected to grow at 26.4% CAGR through 2031.

- By service model, Software-as-a-Service accounted for 54.60% of the Asia-Pacific cloud computing market size in 2025, while Platform-as-a-Service is forecast to expand at 27% CAGR to 2031.

- By organization size, large enterprises held 63.10% revenue share of the Asia-Pacific cloud computing market in 2025, whereas SMEs are advancing at 21.6% CAGR to 2031.

- By end-user industry, BFSI captured 19.75% of the Asia-Pacific cloud computing market share in 2025; healthcare and life sciences is growing at 22.9% CAGR to 2031.

- By geography, China led with 38.20% share of the Asia-Pacific cloud computing market in 2025, while India is expanding at 25.1% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Expected changes in Asia many a times form part of a broader pattern of global movement rather than an isolated trend. The report on worldwide cloud computing market outlook by Mordor Intelligence brings these expectations together.

Asia-Pacific Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive AI / Gen-AI workload demand for GPU-rich cloud instances | +4.2% | Global, strongest in China, Japan, South Korea | Medium term (2-4 years) |

| Government “Cloud-First” mandates expanding in emerging APAC economies | +3.8% | India, Malaysia, Singapore, Thailand, Vietnam | Short term (≤ 2 years) |

| Telco-edge 5G partnerships accelerating multi-cloud adoption | +2.9% | APAC core, spill-over to Southeast Asia | Medium term (2-4 years) |

| Sovereign-cloud frameworks unlocking regulated-sector spend | +3.1% | China, India, Australia, Singapore | Long term (≥ 4 years) |

| Hyperscaler expansion into tier-2 metros | +2.7% | India, China, Indonesia, Thailand | Medium term (2-4 years) |

| Enterprise pivot from lift-and-shift to cloud-native modernisation | +2.5% | Global, led by Japan, Australia, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive AI / Gen-AI Workload Demand for GPU-Rich Cloud Instances

Generative-AI use cases are forcing providers to add accelerators at unprecedented scale, with 878,000 GPUs deployed by major clouds in 2023 even as scheduling inefficiencies limit utilization.[1]The Register, “Big Cloud deploys thousands of GPUs for AI,” theregister.com China tops the global generative-AI patent league with 38,210 filings between 2014 and 2023, underscoring demand for specialized infrastructure. Regional telcos are moving upstream: Singtel and Nvidia launched an AI-focused data center in early 2026 to offer GPU-as-a-Service across Southeast Asia. SK Telecom’s AI Infrastructure Superhighway roadmap positions the carrier as an infrastructure provider for AI workloads. Nations are also investing in sovereign-AI systems, driving projected USD 110 billion in regional AI spend by 2026.

Government “Cloud-First” Mandates Expanding in Emerging APAC Economies

Policy initiatives are converting public-sector IT budgets into predictable cloud demand. Malaysia’s MyGovCloud aims for 80% public-sector cloud storage and is expected to attract up to USD 3.4 billion in investments by 2025.[2]Ministry of Finance Malaysia, “Govt introduces cloud computing service MyGovCloud,” mof.gov.my Singapore’s Government on Commercial Cloud has onboarded 3,006 systems and maintains 99.5% uptime. New Zealand mandates public-cloud adoption after risk assessments, citing 60% cost savings at the Land Transport Authority. India’s GI Cloud (MeghRaj) provides a national cloud backbone supporting digital-public-good delivery. Such mandates favor compliance-ready offerings over low-price bids and accelerate time-to-revenue for vendors.

Telco-Edge 5G Partnerships Accelerating Multi-Cloud Adoption

Seventy-seven percent of communication-service providers favor hybrid-cloud strategies and almost one-third plan to revamp operations systems to support them.[3]TMCnet, “Telcos are Heavily Prioritizing the Cloud and 5G,” tmcnet.com Singtel’s GPU-as-a-Service alliance with Bridge Alliance distributes accelerator pools across multiple markets. Aduna and Bridge Alliance are integrating CAMARA network-API access, giving enterprises programmable connectivity that pairs with cloud workloads. Hitachi and Singtel collaborate to marry operational-technology expertise with edge-cloud capacity for industry solutions. These partnerships shrink latency windows, foster real-time analytics and support multi-cloud placement strategies.

Sovereign-Cloud Frameworks Unlocking Regulated-Sector Spend

Nineteen percent of Asia-Pacific organizations intend to increase sovereign-cloud budgets, with 48% of public-sector entities planning adoption within 12 months. Singapore’s Infocomm Media Development Authority released cloud-resilience guidelines in February 2025 that emphasize risk assessments and cybersecurity. China’s tightened data-export rules and Vietnam’s cross-border data clauses complicate multinational operations and encourage domestic hosting. Google Cloud’s compliance mapping for Indonesia’s GR-71 shows how hyperscalers localize controls. Providers able to certify compliance at national level gain privileged access to banking, healthcare and government contracts.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented data-residency laws inflate compliance cost | -2.8% | Global, particularly China, India, Australia | Long term (≥ 4 years) |

| Scarcity of certified cloud talent drives wage inflation | -1.9% | APAC core, acute in Singapore, Japan, Australia | Medium term (2-4 years) |

| Power-grid constraints slowing hyperscale DC build-outs | -1.5% | China, India, Southeast Asia | Medium term (2-4 years) |

| Sovereign-cloud price premiums erode SMB attractiveness | -1.2% | Regional, strongest impact in regulated sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Data-Residency Laws Inflate Compliance Cost

Divergent localization statutes force providers to run multiple compliance frameworks, eroding economies of scale and passing costs to customers.[4]Belfer Center, “Sovereignty and Data Localization,” belfercenter.org Malaysia’s Personal Data Protection Act obliges providers to build granular data-management controls. The extraterritorial U.S. CLOUD Act deepens jurisdictional conflict, adding to legal uncertainty. As a result, SMEs lacking compliance budgets delay migration, dampening overall expansion momentum.

Scarcity of Certified Cloud Talent Drives Wage Inflation

Seventy-one percent of Asia-Pacific enterprises report limited skills as a barrier to digital value realization. Malaysia’s forecast USD 11 billion IT outlay is constrained by skill shortages that slow managed-service uptake. Korea’s cloud-managed-services revenue grew to USD 4.76 billion in 2023 but margins remain thin due to high staffing costs. Singtel’s Nxera Academy aims to expand talent pipelines for AI-dense data centers. Persistent wage inflation increases total-cost-of-ownership, particularly for sovereign-cloud deployments that need scarce compliance specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid adoption narrows the public-cloud lead

Public cloud represented 46.85% of the Asia-Pacific cloud computing market in 2025, validating trust in hyperscaler security and global footprints. Hybrid architectures are projected to expand at 26.4% CAGR through 2031 as enterprises integrate on-premises assets with public-cloud scalability. This preference balances latency, sovereignty and business-continuity requirements. Telco-edge 5G rollouts inject new edge nodes that extend hybrid fabrics for low-latency use cases, reinforcing multi-cloud patterns.

Hybrid-cloud success depends on orchestration tools that unify policy, cost and performance management across environments. Seventy-seven percent of telecom providers plan hybrid setups, indicating strong infrastructure support. Enterprises with legacy core systems view hybrid pathways as risk-mitigation strategies when modernizing. As a result, the Asia-Pacific cloud computing market size for hybrid deployments is forecast to outpace the regional average over the next five years.

By Service Model: Platform services unlock cloud-native value

Software-as-a-Service controlled 54.60% revenue in 2025 by standardizing business applications across verticals. Platform-as-a-Service will grow at 27% CAGR as developers pivot from lift-and-shift to microservices architectures. Infrastructure-as-a-Service remains foundational for bespoke workloads, while Function- and Disaster-Recovery-as-a-Service fill specialized gaps. Sumitomo Mitsui Financial Group’s digital initiative illustrates PaaS benefits by embedding CFO dashboards in supply-chain finance workflows.

Cloud-native demand is particularly strong in fintech and gaming, where iterating quickly on new services is vital. Accelerating PaaS adoption lifts average revenue per user, which enlarges the Asia-Pacific cloud computing market size while deepening provider lock-in around proprietary developer tools.

By Organization Size: SMEs narrow the adoption gap

Large enterprises held 63.10% share in 2025 as they executed complex multi-cloud roadmaps. SMEs, however, will post 21.6% CAGR through 2031, encouraged by affordable SaaS bundles and government digitization subsidies. Studies spanning Pakistan, Indonesia and Mauritius highlight cost, complexity and security as chief SME concerns. Simplified interfaces and pay-as-you-go pricing lower these barriers.

Top-management support and perceived relative advantage drive SME uptake, whereas integration complexity deters investments. Targeted training and marketplace ecosystems designed for micro-businesses will sustain SME momentum, expanding the Asia-Pacific cloud computing market while diversifying user profiles.

By End-User Industry: Healthcare surges on telemedicine and AI diagnostics

BFSI captured 19.75% of Asia-Pacific cloud computing market share in 2025 because digital banking transformation and compliance demand resilient infrastructure. Healthcare and life sciences will register 22.9% CAGR to 2031, propelled by teleconsultation, AI-driven diagnostics and electronic-health-record modernization. Public-health innovations across Japan, South Korea and Singapore highlight cloud’s potential to ease demographic and cost pressures.

Zuellig Pharma’s pivot to cloud logistics safeguarded medical-supply distribution across 13 countries, reinforcing sector confidence. Manufacturing, retail and logistics continue adopting predictive-maintenance and omnichannel solutions, but the healthcare trajectory will contribute disproportionately to incremental Asia-Pacific cloud computing market size gains over the forecast.

Geography Analysis

China commanded 38.20% share of the Asia-Pacific cloud computing market in 2025, with cloud-infrastructure revenue reaching USD 9.7 billion and 449 data centers now consuming 25% of global data-center electricity. The government’s “east data west computing” strategy intends to relocate compute workloads to energy-abundant western provinces, yet tightening data-export rules could temper international workload inflows. Domestic giants hold 39% local share but seek global expansion, illustrated by Alibaba’s plan for new facilities in Malaysia, Thailand and South Korea.

India is the fastest-growing geography at 25.1% CAGR through 2031, catalyzed by the GI Cloud program and hyperscaler investments. AWS’s USD 6 billion Malaysian commitment and NTT’s Bangkok build signal broader sub-regional enthusiasm. Over 370 Southeast-Asian data centers serve underpenetrated markets, with demand projected to grow 20% annually to 2028.

Japan and South Korea remain mature but opportunity-rich. Microsoft pledged USD 2.9 billion for AI and cloud upgrades in Japan. AWS earmarked ¥2 trillion (USD 13.4 billion) to address generative-AI workloads. SK Telecom’s AI-accelerated data centers showcase Korea’s infrastructure sophistication. Australia and New Zealand attract hyperscaler spending, with Amazon allocating AUD 20 billion for data-center capacity from 2025-2029. Singapore functions as the regional hub, maintaining 99.5% uptime on its Government on Commercial Cloud while attracting edge and AI investments.

Mordor Intelligence's coverage of the cloud computing market extends across other regions including North America, Europe, and South America, while country-specific intelligence is also available for Japan, China, India, South Korea, United States, and Spain, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

Global hyperscalers, Chinese champions and sovereign-cloud specialists battle for wallet share, creating a moderately consolidated but fiercely competitive environment. AWS, Microsoft Azure and Google Cloud harness global scale, while Alibaba Cloud, Tencent Cloud and Huawei Cloud localize offerings and compliance. Oracle’s USD 30 billion multiyear cloud deal may raise its global share from 3% to about 4% by 2028, adding new pressure. Strategic partnerships flourish: Singtel and Nvidia deliver AI-ready data centers, and SAP will run its own ERP on Alibaba Cloud to address sovereignty concerns in China.

Telco-cloud collaborations offer differentiation through low-latency edge nodes and network-API exposure, with 77% of carriers adopting hybrid-cloud blueprints. Private-equity appetite is strong: Blackstone led a USD 16 billion acquisition of AirTrunk, signaling investor confidence in data-center assets. Sustainability emerges as a competitive lever; Alibaba Cloud reports PUE of 1.200 and client carbon-reduction equivalents of 988.4 million tons. Talent cultivation programs such as Singtel’s Nxera Academy address labor bottlenecks and reinforce provider ecosystems.

Incumbents respond to regulatory fragmentation by offering sovereign-cloud nodes that embed compliance controls. These nodes command price premiums yet shield customers from data-localization complexity. Over time, successful providers will blend AI-optimized infrastructure, legal compliance and eco-efficiency to preserve margins in the Asia-Pacific cloud computing market.

Asia-Pacific Cloud Computing Industry Leaders

Microsoft Corporation

Alibaba Group Holding Limited

Amazon.com Inc.

Oracle Corporation

Salesforce.com Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SAP partnered with Alibaba to host Cloud ERP workloads in China, with expansion plans to Southeast Asia, Middle East and Africa, while Alibaba will adopt SAP Cloud ERP internally and co-market joint offerings.

- July 2025: Oracle secured a USD 30 billion cloud deal expected to boost annual revenue by 150% from fiscal 2028.

- June 2025: Amazon announced AUD 20 billion (USD 13 billion) investment in Australian data centers for cloud and AI infrastructure.

- May 2025: IBM expanded software availability to 92 countries via AWS Marketplace, giving 18 African nations access to Watson AI and automation tools.

Asia-Pacific Cloud Computing Market Report Scope

Cloud computing delivers a range of services over the internet, encompassing servers, storage, databases, networking, software, analytics, and intelligence. This approach fosters quicker innovation, adaptable resources, and economies of scale. Our study focuses on the Asia-Pacific (APAC) cloud computing market. We gauge the market size by analyzing the revenue generated from cloud computing services by various players in the region. Additionally, we monitor key market metrics and growth influencers, bolstering our market estimates and growth projections for the forecast period. Our analysis draws from insights gathered through both secondary research and primary sources.

The Asia-Pacific cloud computing market is categorized by type (public cloud [IaaS, PaaS, and SaaS], private cloud, hybrid cloud), organization size (SMEs and large enterprises), end-user industries (manufacturing, education, retail, transportation and logistics, healthcare, BFSI, telecom and IT, government and public sector, and others), and country (China, Japan, India, South Korea, and the rest of Asia-Pacific). We present market sizes and forecasts in terms of value (USD) across all segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| Education |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare and Life Sciences |

| Banking, Financial Services and Insurance (BFSI) |

| Telecom and IT |

| Government and Public Sector |

| Others |

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| By Organization Size | Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Industry | Manufacturing |

| Education | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Healthcare and Life Sciences | |

| Banking, Financial Services and Insurance (BFSI) | |

| Telecom and IT | |

| Government and Public Sector | |

| Others | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size of the Asia-Pacific cloud computing market?

The market is valued at USD 243.75 billion in 2026.

How fast is the Asia-Pacific cloud computing market expected to grow?

It is projected to register a 19.85% CAGR and reach USD 602.82 billion by 2031.

Which deployment model is expanding the quickest in the region?

Hybrid cloud shows the fastest growth with a 26.4% CAGR through 2031.

Why is healthcare the fastest-growing vertical for cloud services in Asia-Pacific?

Telemedicine, AI-enabled diagnostics and electronic-health-record modernization are driving a 22.9% CAGR for healthcare and life sciences workloads.

Which country leads in market share and which leads in growth rate?

China holds the largest share at 38.20%, while India records the highest growth rate at 25.1% CAGR.

How are data-sovereignty rules affecting cloud adoption?

Fragmented data-residency laws raise compliance costs, encouraging sovereign-cloud offerings and influencing provider selection across regulated sectors.

Page last updated on: