Clinical Trial Kits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 8.13% CAGR |

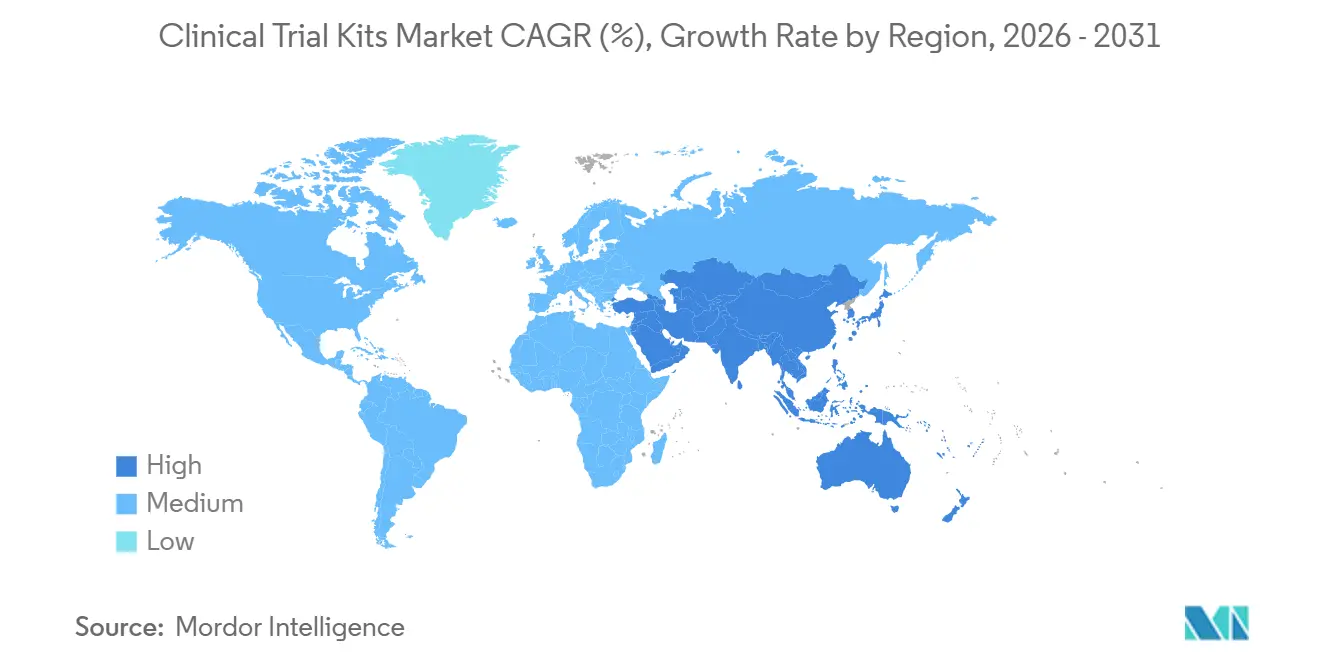

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trial Kits Market Analysis by Mordor Intelligence

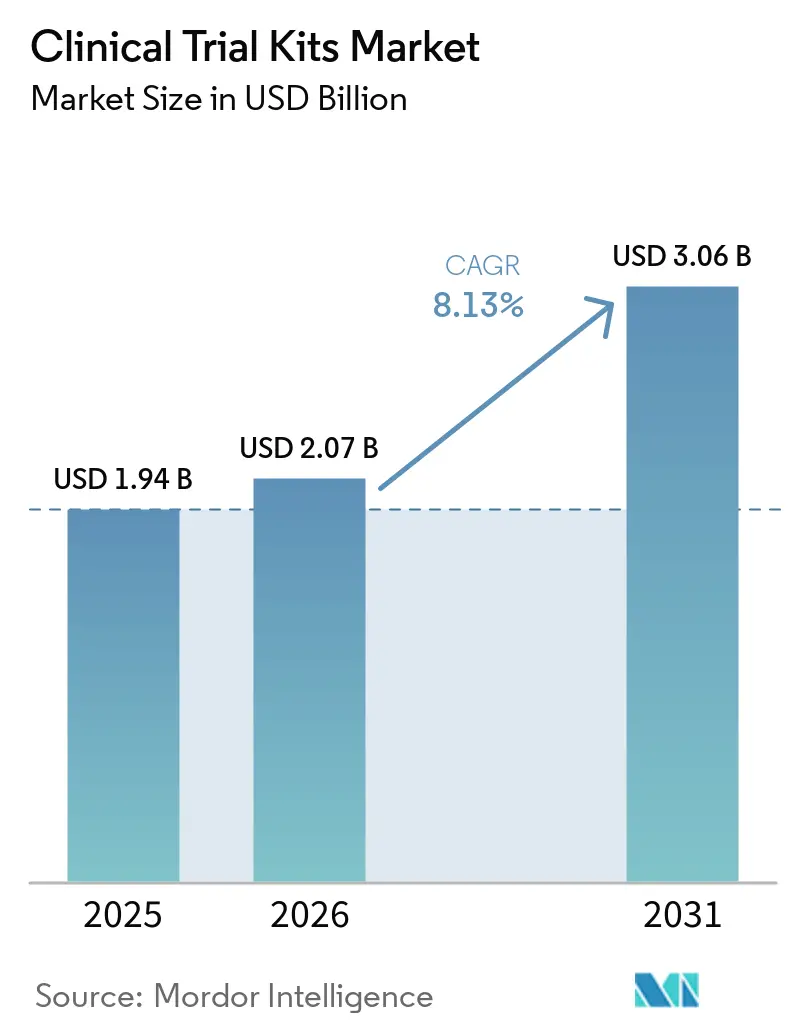

The Clinical Trial Kits Market size is expected to increase from USD 1.94 billion in 2025 to USD 2.07 billion in 2026 and reach USD 3.06 billion by 2031, growing at a CAGR of 8.13% over 2026-2031.

Growth reflects a steady transition toward higher execution quality and resilience, shaped by risk-based good clinical practice standards, digital visibility across depots and sites, and a wider use of direct-to-patient shipping models that reduce participant burden and improve continuity. Regulatory convergence is a major catalyst as the EU Clinical Trials Regulation mandates CTIS workflows across the EU/EEA and ICH E6(R3) codifies proportionate, DCT-ready supply practices that elevate packaging validation and chain-of-custody documentation to core capabilities. Technology adoption is reinforcing supplier differentiation, with RFID and IoT visibility reducing losses in cold chains and sensor-enabled packaging helping sponsors demonstrate audit-ready compliance under R3. Providers that invest in ultra-cold infrastructure, validated dry shipper networks, and rapid kitting turnaround for decentralized studies are positioned to capture premium services as protocols become more complex and site footprints blend physical and virtual elements. The clinical trial kits market continues to reward companies that connect cryogenic custody expertise with integrated eClinical tools, since end-to-end traceability, real-time exception management, and interoperable submissions reduce operational risk and speed cycle times across multi-country programs. Expanding decentralized and hybrid workflows, now explicitly accommodated by U.S. guidance, are further normalizing direct-to-patient supply design and triggering new packaging, labeling, and monitoring requirements at the kit level.

Key Report Takeaways

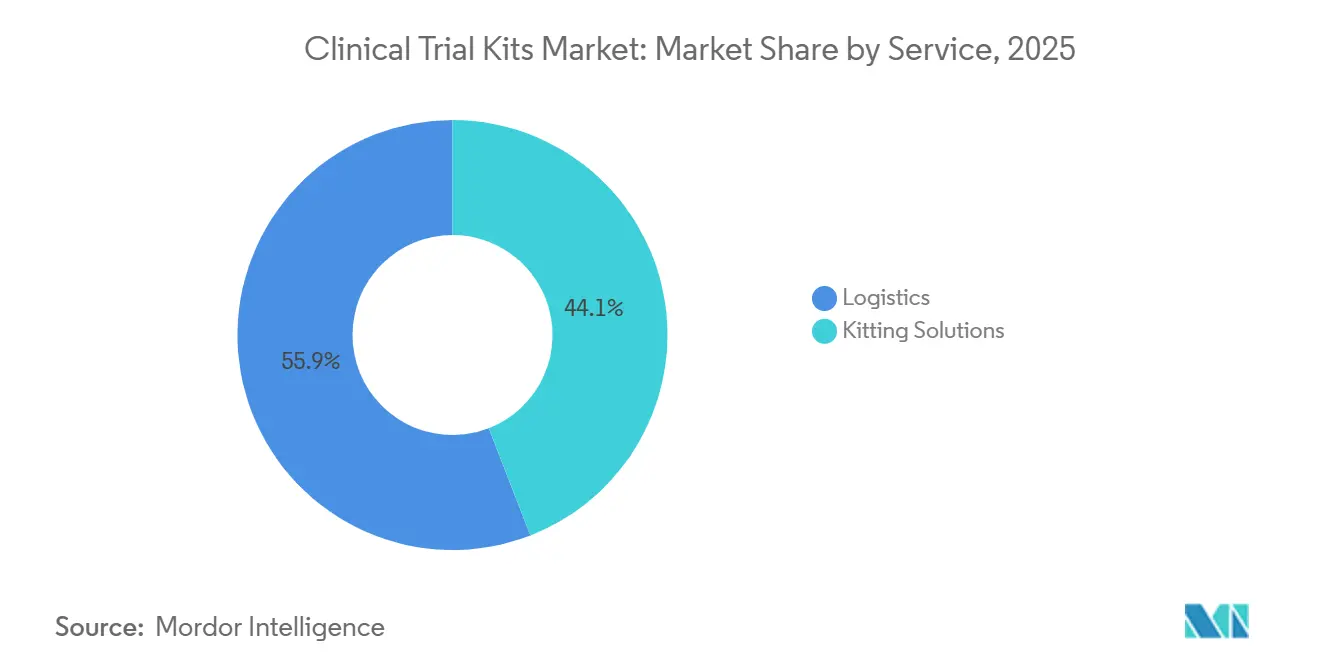

- By service, logistics services led with 55.90% revenue share in 2025 while kitting solutions is projected to grow at an 8.80% CAGR through 2031.

- By phase, Phase III maintained 44.17% of the Clinical trial kits market share in 2025 while Phase I is projected to expand at a 9.65% CAGR through 2031.

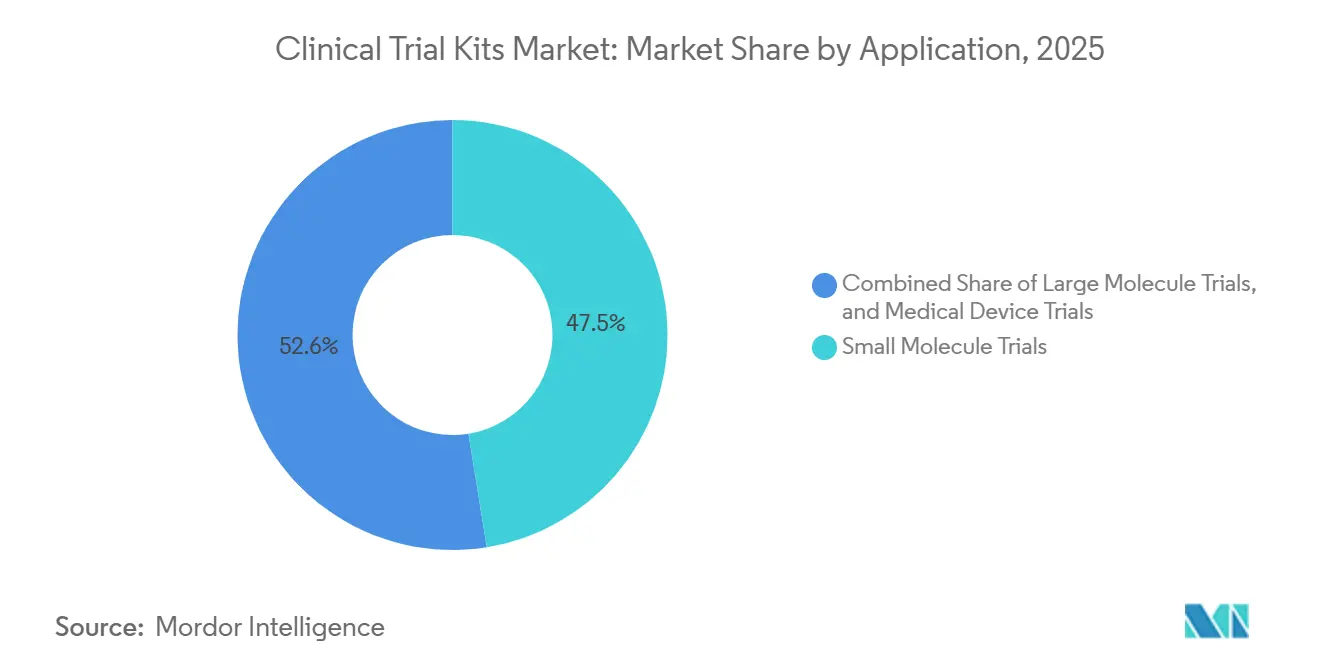

- By application, small molecule trials accounted for 47.45% of the Clinical trial kits market share in 2025 while large molecule trials are forecast to advance at an 8.81% CAGR to 2031.

- By end user, pharmaceutical and biopharmaceutical companies held 57.20% share in 2025 while contract service providers are expected to post an 8.92% CAGR.

- By geography, North America led with 41.39% share in 2025 while Asia-Pacific is expected to record a 9.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Trial Kits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Global Trial Volumes and Protocol Complexity | + 1.8% | Global, with concentration in US, EU, and China | Medium term (2-4 years) |

| Expansion of Biologics, Cell & Gene Therapies Requiring Cold-Chain and Specialized Kitting | + 2.4% | Global core (US, EU, Japan), spillover to APAC emerging markets | Long term (≥ 4 years) |

| Adoption of Decentralized and Hybrid Trial Models (DTP/DFP Workflows) | + 1.6% | North America and EU leading, selective APAC adoption | Medium term (2-4 years) |

| Regulatory Harmonization (EU CTR/CTIS) and ICH E6(R3) Enabling Risk-Based, DCT-Ready Supply | + 1.3% | EU/EEA mandatory, US/Japan voluntary alignment | Long term (≥ 4 years) |

| Microsampling (DBS/PSC) Enabling Ambient, Mail-Back Kits and Site/Patient Burden Reduction | + 0.8% | Global, early gains in Europe (CE-IVD certified), expanding to US/Asia | Medium term (2-4 years) |

| RFID/IoT-Enabled Temperature and Chain-Of-Custody Monitoring Reducing Loss & Waste | + 0.4% | Global, primarily in high-value biologics/CGT shipments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Global Trial Volumes and Protocol Complexity

Rising protocol complexity and broader multinational execution are amplifying the operational premium on rapid kitting turnaround, continuous inventory visibility, and audit-ready chain-of-custody at the kit and shipment level. The shift toward risk-proportionate GCP has made packaging validation for home use and serialized tracking essential, since ICH E6(R3) explicitly references controls for preventing deterioration during storage and transport and enables direct-to-patient shipping when justified. In practice, this places more operational weight on the clinical trial kits market, since a single temperature excursion can void a participant’s visit and disrupt downstream schedules across decentralized studies. Large providers are investing in integrated digital and supply capabilities to meet this bar, such as Almac’s Trial Coordinator platform that links eClinical workflows with clinical supply coordination to shorten cycle times. Sponsors are rewarding vendors that connect comparator sourcing, kitting, and global cold-chain logistics under unified quality oversight, because this reduces handoffs and supports faster, cleaner submissions. As global regulators harmonize in favor of risk-based oversight, operational proof at the packaging and dispatch level has become central to product integrity and data credibility across cross-border trials. [1]ICH Secretariat, “Integrated Addendum to ICH E6(R3) Guideline for Good Clinical Practice,” International Council for Harmonisation, ich.org Almac’s 2025 platform launch underscores how digital enablement is now part of core value delivery in the clinical trial kits market. [2]Almac Group Editorial Team, “Almac Trial Coordinator Launched in $48 Million Investment to Advance Integrated eClinical Technologies,” Almac Group, almacgroup.com

Expansion of Biologics, Cell & Gene Therapies Requiring Cold-Chain and Specialized Kitting

As more cell and gene therapies progress through development and gain expedited pathways, demand for cryogenic custody and patient-specific kitting has intensified. FDA’s guidance suite for cellular and gene therapies clarifies expectations on expedited programs and postapproval data, which raises the importance of validated ultra-cold logistics, traceability of batches and doses, and documentation that supports lot-level analysis. Operational requirements for autologous workflows, including continuous cryogenic control and documented chain of identity, elevate specialized kitting from a delivery function to an integral component of product integrity. Suppliers are expanding regional cryogenic nodes and quality oversight near major air hubs to cut transit times for time-sensitive cell therapies and to reduce customs exposure within the EU/EEA. Cold-chain service and storage providers detail process and infrastructure standards, including validated dry shippers and redundant monitoring, that are now table stakes for high-value biologics and CGT studies. These capabilities are becoming a primary line of differentiation in the clinical trial kits market as sponsors prioritize proven, audited performance on cryogenic custody and turnaround times for vein-to-vein workflows. Technical expectations for ultra-cold handling and secure chain of identity are documented across industry guidance and provider standards, reinforcing specialized kit design and logistics as core levers for risk reduction. [3]Jennifer McGrath, “Cell and Gene Therapy Logistics and Storage,” SciSafe, scisafe.com

Adoption of Decentralized and Hybrid Trial Models (DTP/DFP Workflows)

U.S. regulators have formally recognized decentralized elements, including direct-to-patient shipment of investigational products, telehealth-enabled safety assessments, and use of local facilities for routine tests, which confirms the operating space for DTP and home-health workflows. Industry bodies highlight high adoption of decentralized elements among sponsors and CROs, and site-facing digital tools have advanced to support kit inventory management, sample tracking, and training resources that lower administrative burden for investigators. These changes reframe kit design as a participant experience function because successful home use relies on intuitive formats, clear instructions, and prevalidated packaging that withstands real-world handling. The IATA framework for UN3373 biological substances and dry ice handling has become a design constraint for many DTP supplies, which pushes suppliers to standardize packaging performance and labeling while maintaining patient-friendly configurations. As decentralized workflows expand, the clinical trial kits market is adjusting around home collection devices, mail-back logistics, and local lab integration that together compress timelines and improve participant retention. Institutional guidance and adoption updates show a durable move toward hybrid models, which support sustained growth in kit volumes that are tailored to patient journeys rather than site-only processes. Industry associations and platforms detail uptake momentum and operating considerations that now inform kit assembly and distribution planning across protocols. Site enablement tools introduced in 2024 by central lab providers point to measurable gains in efficiency and error reduction for supplies planning and sample workflows in decentralized settings.

Regulatory Harmonization (EU CTR/CTIS) and ICH E6(R3) Enabling Risk-Based, DCT-Ready Supply

The EU Clinical Trials Regulation set a January 31, 2025 transition deadline for ongoing trials and consolidated multi-country authorizations into the CTIS portal, which shortens approval timelines and streamlines submission consistency across the EU/EEA. CTIS transparency policies updated in 2024 accelerated publication timelines and narrowed deferral options, which means labeling content and patient-facing materials must meet disclosure standards from the outset. In parallel, ICH E6(R3) advanced a risk-based and proportionate standard that explicitly permits shipment of investigational products to participant homes or local pharmacies when justified, making packaging validation and serialized tracking key to compliance. U.S. and EU guidance aligned on R3 in 2025, creating a compressed window for suppliers to update quality systems, define critical-to-quality factors like temperature stability, and implement risk-based monitoring supported by digital tools. These moves reward providers that already invested in interoperable IT for labeling, batch metadata capture, and real-time exception reporting, since they can demonstrate compliance without manual transcription and re-entry. As a result, the clinical trial kits market increasingly differentiates on the maturity of CTIS-ready submissions, packaging validation for decentralized use, and automated audit trails for chain-of-custody and product use at the participant level. The step 4 adoption of ICH E6(R3) and subsequent U.S. guidance provide the formal foundation for these operating models to scale across sponsors and regions. CTIS guidance documents and Q&As detail transparency and submission process expectations that now influence kit labeling workflows and artwork management at the study level.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-Chain & Cross-Border Logistics Complexity and Costs | - 1.2% | Global, acute in Latin America, MEA, and rural APAC regions | Medium term (2-4 years) |

| Regulatory Variability and Documentation Burden Across Countries & Customs | - 0.9% | Latin America, MEA, and multi-country EU trials | Long term (≥ 4 years) |

| PFAS Restrictions Threatening Availability of Fluoropolymer-Based Packaging and Labels | - 0.5% | EU/EEA (April 2026), potential global cascade by 2027-2028 | Long term (≥ 4 years) |

| IATA UN3373/PI650 and Dry Ice Constraints Raising Packaging/Compliance Overhead | - 0.3% | Global air freight corridors, particularly US-EU-Asia routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cold-Chain & Cross-Border Logistics Complexity and Costs

Maintaining temperature integrity across long distances and multiple jurisdictions remains a structural cost and risk for sponsors, especially in regions with persistent high ambient temperatures or limited power redundancy. The operational bar for cell and gene therapy supplies is particularly high since autologous products require continuous cryogenic custody and documented chain of identity that can withstand customs holds and flight disruptions. Provider investments in new ultra-cold capacity and regional secondary packaging are a pragmatic response to reduce exposure to transcontinental delays and to improve delivery times for time-sensitive therapies. Companies with validated dry shipper fleets and redundant monitoring limit losses due to excursions and enable faster recovery from route changes or clearance delays. The clinical trial kits market favors networks that can sustain performance under variable transit times while maintaining audit-ready documentation and telemetry for temperature and location. Practical packaging and compliance demand for shipping biological substances and dry ice under IATA rules further add costs that must be built into kit design and logistics planning. The IATA framework for UN3373 and dry ice handling is a non-negotiable specification that shapes packaging, labeling, and ventilation design for many temperature-sensitive kits.

Regulatory Variability and Documentation Burden Across Countries & Customs

Despite harmonization in the EU and convergence under ICH E6(R3), multinational programs still face documentation variability, procurement differences across hospital systems, and data disclosure requirements that elevate administrative work. CTIS requires standardized data structures and continuous submission handling rather than one-time filings, which favors sponsors and vendors with mature digital infrastructure and clear procedures for redaction and anonymization. Outside the EU, regional regulatory updates can ease certain bottlenecks, but local lab availability, import authorizations, and post-trial access obligations can still complicate feasibility and budgeting. Diversified depot footprints and in-country packaging capabilities are often required to balance import documentation requirements and temperature control needs within expected lead times. The clinical trial kits market therefore values partners that can navigate country-specific labeling rules, customs classifications, and cold-chain permits while maintaining serialized traceability across returns and destruction workflows. Public portals and association reports offer visibility into country-level timelines and policy shifts that affect kit logistics planning and investigator site readiness. Regional health organization resources for the Americas and other blocs provide additional context for routing, lab availability, and approval timelines that impact supply execution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Kitting Outpaces Logistics on Biologics Premium

Logistics services held the largest portion of 2025 revenue at 55.90% as sponsors prioritized on-time delivery, temperature integrity, and assured chain of custody at study and participant levels across decentralized and multi-country operations. Within logistics, transportation accounted for 50.45% in 2025 as shipment velocity rose with cold-chain, frozen, and cryogenic movements that scale with enrollment cycles and dosing schedules rather than fixed depot footprints. The clinical trial kits market reflects this shift because decentralized programs and cross-border trials require more frequent resupply, active returns, and exception-driven re-shipments that keep transportation intensity high. Providers with GPS-enabled tracking and exception alerts are differentiating through proactive loss prevention and faster deviation closure for temperature fluctuations or customs holds. Risk-based GCP and DTP workflows align with logistics partners that can deliver rapid, compliant shipments to homes or local facilities with serialized tracking and automated documentation of lot, expiry, and quantities. This favors vendors with integrated labeling and data capture to support CTIS submissions and site audits without manual re-entry. As an operational anchor, logistics functions remain critical to the clinical trial kits market even as kit assembly grows more specialized under biologics and CGT workflows. Providers improving telemetry and packaging performance within regulated constraints are best placed to protect temperature-sensitive products under real-world conditions.

Kitting solutions posted the fastest growth at an 8.80% CAGR as customization rose with biologics, device-enabled administration, and decentralized kits designed for home use. Within kitting, cell therapy–specific kits showed the strongest momentum at a 10.79% CAGR as autologous and allogeneic programs expanded and as expedited pathways increased the volume of temperature-critical study visits. This segment depends on validated cryogenic components, chain-of-identity elements, and compressed assembly windows that raise value per kit and require tight integration with clinical operations. Vendors that combine patient-ready packaging, clear instructions, and serialized components help reduce protocol deviations while supporting DTP and hybrid scheduling. The clinical trial kits industry is therefore tilting toward suppliers that blend GMP-grade materials, cryogenic know-how, and eClinical interoperability to ensure traceability and rapid release for shipment. Investments in cold-chain packaging and controls show how leaders are scaling capacity where biologics and CGT protocols concentrate, while using digital coordination to align kitting throughput with recruitment and dosing cadence. Almac’s ongoing infrastructure and platform expansion further illustrates how integrated eClinical capabilities are being used to coordinate complex kitting alongside temperature-controlled logistics in the clinical trial kits market.

By Phase: Early-Stage Velocity Meets Late-Stage Volume

Phase I posted the fastest segment growth at a 9.65% CAGR, reflecting sponsors’ emphasis on early human data and the growing availability of high-throughput units in key geographies that can support first-in-human timelines with consistent quality controls. In this environment, flexible kitting and next-day packaging changes are valuable since dose-escalation cohorts and safety-triggered amendments can alter kit contents with little notice. The clinical trial kits market benefits from early-phase designs that emphasize speed, clear instructions, and strict temperature control to protect data integrity at low patient volumes. For Phase I to function at scale across countries, suppliers need unified labeling and documentation that adjust quickly to updated investigator brochures and consent-linked changes. This places a premium on eClinical coordination where kit availability aligns with cohort openings and telemetry confirms receipt and storage conditions at sites. Strong vendor alignment with risk-based GCP and DCT readiness supports the use of home-health elements in early safety studies where appropriate and prevalidated. The clinical trial kits industry is adapting to this early-stage emphasis with modular designs and serialized components that can be combined or swapped as dose changes and visit windows evolve.

Phase III maintained the largest absolute base with 44.17% share in 2025, driven by larger patient populations, longer study durations, and the breadth of geographies needed to meet recruitment goals. At this scale, comparator sourcing, depot coverage, and standardized kit formats create efficiencies that make late stage work a significant revenue anchor for the clinical trial kits market. However, growth can be slower in mature categories where ambient storage dominates and where competing vendors can deliver similar performance at lower cost. Adaptive designs, still common in pivotal work, underscore the importance of inventory visibility and fast reallocation to avoid stockouts during mid-course adjustments. Late-phase decentralized elements are increasing for patient convenience in chronic and rare disease programs, reinforcing the value of DTP-ready packaging and compliant returns handling. The clinical trial kits industry is therefore balancing cost discipline at volume with selective premium services where temperature sensitivity, device integration, or home use requirements justify higher pricing. Vendors that combine standardized late-stage kits with DTP and cold-chain options can serve a wide spectrum of Phase III protocols without fragmenting supply networks.

By Application: Large Molecules Eclipse Small on Cold-Chain Premium

Small molecule trials accounted for 47.45% of 2025 revenue as oral and parenteral formats-maintained relevance in cardiovascular, metabolic, infectious disease, and CNS indications. The clinical trial kits market continues to support these programs with standardized site kits, ambient storage where applicable, and streamlined comparator integration that sustain volume even as novel modalities expand. In emerging geographies, the relative simplicity of ambient shipments and faster site activation supports broader trial footprints for small molecules. Sponsors also extend lifecycles through reformulations and fixed-dose combinations, which keep study activity levels steady. Operational predictability makes ambient kits a competitive area where cost and service reliability dominate supplier selection. Even so, decentralized elements and home-friendly packaging remain important to reduce travel burden in chronic indications, especially where mail-back samples and local lab testing are feasible under country rules. Site-facing digital tools are adding value by reducing kit waste and improving readiness, especially for multi-visit dosing schedules in which inventory misalignment can trigger delays.

Large molecule programs are projected to expand at an 8.81% CAGR through 2031 as their cold-chain intensity and patient-specific workflows command premium pricing for specialized kits. The clinical trial kits market size associated with temperature-sensitive biologics aligns with R3’s validation of DTP workflows, since prevalidated packaging and serialized tracking help mitigate risk in home administration or local pharmacy dispensing. The steep technical bar for cryogenic shipments and monitoring reinforces the need for validated shippers, continuous telemetry, and proven exception management for excursions and delays. Suppliers are also adopting RFID and other sensor technologies to automate documentation of delivery, inventory, and returns, which reduces manual errors and strengthens inspection readiness. Device integration for combination products and patient training materials further differentiate complex biologic kits in decentralized or hybrid designs. As expedited pathways progress for advanced therapies, traceability from manufacturing to patient becomes a central quality signal, and vendors with integrated cold-chain networks and qualified personnel in the EU/EEA gain an execution advantage. Advances in RFID hardware designed for low-temperature, high-humidity environments are improving tag survivability and data integrity for biologics shipments in the clinical trial kits market.

By End User: CROs Capture Outsourcing Surge

Pharmaceutical and biopharmaceutical companies retained 57.20% share of 2025 revenue as lead sponsors continued to drive procurement decisions across large pivotal programs and assets advancing toward registration. Yet the clinical trial kits market shows faster growth among contract service providers, where bundled offerings combine supply management, monitoring, data, and regulatory support under one operating model. End-to-end offerings reduce handoffs and simplify issue resolution on temperature excursions, customs inquiries, or labeling changes that would otherwise multiply across separate vendors. CROs are also leveraging digital tools and AI-driven optimization to shorten cycle times, improve forecasting, and reduce waste, creating measurable savings on kit inventory and logistics. As CTIS and R3 increase documentation expectations, sponsors benefit from providers that can natively capture lot, expiry, and quantities within interoperable systems. The clinical trial kits industry is therefore pivoting toward vertically integrated players that can meet both DTP readiness and ultra-cold custody while sustaining late-stage volume at competitive service levels. CRO investment in cold-chain packaging and device assembly is strengthening the link between kit performance, real-world handling, and site experience.

Contract service providers are projected to grow at an 8.92% CAGR as sponsors seek variable-cost models and specialized expertise in cryogenics, decentralized workflows, and cross-border compliance. Integrated platforms allow CROs to harmonize labeling, serials capture, and CTIS-ready metadata across studies, which reduces startup friction and accelerates submission cycles in the EU/EEA. Providers that combine QP oversight in Europe with global depot coverage and next-day kitting capacity are securing premium engagements tied to CGT and complex biologic protocols. Successful programs in decentralized settings also depend on clear patient instructions, intuitive packaging, and reverse logistics that reduce errors and protect data continuity. CROs that quantify their improvements in delivery timeliness, temperature compliance, and inventory turns offer compelling value to sponsors consolidating vendors. As a result, the clinical trial kits market is moving toward fewer, deeper partnerships centered on digital visibility, regulated content management, and proven performance under inspection. Evidence from central lab platforms and site enablement tools suggests further gains as sponsors integrate supply data with sample workflows and participant communications.

Geography Analysis

North America led with a 41.39% share in 2025 as sponsors invested in digital visibility, cold-chain integrity, and DTP readiness within a mature regulatory framework. U.S. guidance has recognized decentralized elements, which supports direct-to-patient shipping, telehealth check-ins, and local facilities for routine assessments when justified, creating a clear pathway for patient-centric kit design. Providers in the region are deploying integrated platforms and AI-enabled forecasting for supply planning, which lowers waste and shortens cycle times across complex studies. With many temperature-sensitive protocols in oncology and immunology, the clinical trial kits market remains oriented toward validated packaging, telemetry, and rapid exceptions handling that meet inspection expectations. Platform investments by central lab and supply vendors in 2024 and 2025 emphasize end-to-end data capture, on-demand training for sites, and tools that improve supply readiness down to the kit level. [4]Association of Clinical Research Professionals, “Decentralized Clinical Trials Back in the Spotlight Thanks to New FDA Guidance,” ACRP, acrpnet.org Large integrated service providers are highlighting AI-enabled acceleration in clinical operations and supply coordination, which aligns with demand for faster, more resilient execution in the clinical trial kits market.

Europe sustained a significant share in 2025 under a unified regulatory framework that relies on CTIS for multi-country approvals and ongoing transparency. The standardized 104-day target and electronic submissions are improving predictability, though procurement variability and hospital contracting can still affect timelines in some member states. Regional investments near major hubs are adding ultra-cold capacity, QP oversight, and secondary packaging close to air corridors to cut transit times for time-sensitive autologous therapies. EU transparency rules that accelerated publication timelines in 2024 are shaping label and artwork processes at the study outset, which increases the value of template libraries and pre-cleared designs. The clinical trial kits market in Europe, therefore, emphasizes interoperable labeling, serialized tracking, and automated batch data capture to minimize manual handling and re-entry across CTIS workflows. Providers that integrate DTP-ready packaging with clear patient instructions and country-compliant labeling are well-positioned as hybrid designs extend in chronic and rare disease programs. CTIS resources and Q&As further support sponsors seeking efficient submission handling and clarity on transparency obligations for clinical documents.

Asia-Pacific is expected to register the fastest regional expansion, with a 9.50% CAGR through 2031, as sponsors scale oncology, vaccine, and biologic programs across diverse patient populations. Streamlined clinical trial governance in leading countries and alignment with international GCP elements are improving predictability, while import documentation, customs clearances, and labeling rules continue to require local expertise. The clinical trial kits market is benefiting from urban adoption of decentralized elements that support local lab use and home-based participation where national guidelines allow. Adding in-country packaging and local depots is a practical response to temperature-control needs and customs checkpoints that could otherwise stretch lead times beyond acceptable windows. Regional health authorities are publishing direction-of-travel documents and frameworks that signal support for efficient trial conduct under robust quality expectations. These signals are drawing investment in kitting, labeling, and cold-chain capability tailored to country rules and site readiness in major APAC hubs. Industry resources and public portals in the Americas and other regions provide complementary context on cross-border routing and trial setup that sponsors often apply when planning APAC supply operations, especially for multicenter designs that span hemispheres.

Competitive Landscape

The clinical trial kits market remains fragmented but is consolidating where vertically integrated offerings connect comparator sourcing, kitting, and cold-chain logistics under unified quality and digital oversight. Platform launches that integrate eClinical tools with supply coordination illustrate how providers are hardwiring risk-based practices into daily operations to accelerate cycle times and protect temperature-sensitive therapies. Investments in cryogenic capacity, device assembly, and sterile packaging are expanding the scope of services that can be delivered under single agreements, which reduces sponsor handoffs and accelerates deviation closure. Vendors with qualified person networks in the EU/EEA and CTIS-ready submissions can better navigate artwork, labeling, and transparency requirements for multicountry studies. AI-driven optimization initiatives are also entering the mainstream of clinical operations, which supports demand forecasting, shipment planning, and inventory turns that protect budget and schedules. These moves lift the execution bar for late-stage programs where the cost of failure is high and for decentralized designs where patient experience and delivery reliability drive retention. Integration narratives from large providers emphasize digital and operational control as the path to resilience and premium services in the clinical trial kits market.

Strategic transactions are redefining optionality for sponsors, including acquisitions that move sterile fill-finish and packaging resources under ownership structures designed to secure capacity for marquee therapies. Such moves can concentrate comparator sourcing and kitting capacity and spark pricing changes in categories that were once more competitive on unit cost alone. Service expansions by CROs and CDMOs demonstrate a push to capture growth at the intersection of decentralized workflows and advanced modalities. Providers are also rolling out device indicators and RFID tags tuned for extreme temperatures, high humidity, and condensation to preserve traceability through demanding cold chains. These hardware and packaging innovations reduce loss and waste while simplifying audit readouts with time-temperature histories and serialized data capture. As these capabilities scale, sponsors can compare vendors using more granular performance data on delivery punctuality, excursion avoidance, and documentation completeness. The clinical trial kits market is thus moving toward more data-rich vendor selection, especially in biologics and CGT programs where risk-transfer and measurable performance lift matter most. New RFID designs purpose-built for low-temperature corridors show growing maturity of components that support automated, inspection-ready records.

Leaders are seeking advantage by co-locating critical functions near major air corridors to shorten transit for time-sensitive therapies and by launching regional capacity upgrades to meet rising demand. Investments in secondary packaging, expanded -20°C storage, and enhanced temperature-controlled services in Asia are intended to reduce exposure to cross-hemisphere customs and routing variability. Central labs and sample logistics partners are introducing dashboards and site tools to align sample collection, kit inventory, and requisitions, which cut errors and delays. Clinical trial supply businesses within large life-sciences groups are also publicizing operational acceleration programs that include AI for demand planning, which supports more accurate kit production and dispatch timing. Across the clinical trial kits market, the operational thread ties back to risk-based compliance and DTP readiness under R3 and CTIS, since demonstrated control is now a commercial differentiator. Providers with interoperable submissions, standardized artwork libraries, and prevalidated packaging can alleviate delays linked to transparency and labeling reviews. As a result, the competitive field is rewarding those who can quantify improvement in temperature integrity, on-time performance, and documentation accuracy under inspection. Integrated platforms and hardware that automate traceability complete the picture by simplifying audits and accelerating issue resolution in the clinical trial kits market.

Clinical Trial Kits Industry Leaders

Almac Group

Azenta US Inc.

Charles River Laboratories

Labcorp

Patheon (Thermo Fisher Scientific Inc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Almac Group announced a multi-million-pound investment in Singapore to expand warehouse capacity, quadruple dedicated −20°C storage and enhance secondary cold-chain packaging and temperature-controlled services. The upgrade strengthens localized infrastructure for rising trial volumes in Asia and reduces transcontinental transit exposure.

- July 2025: Almac Clinical Services completed a multi-million-pound investment at its Craigavon headquarters, adding new ultra-low-temperature capacity and tripling secondary packaging at −15°C to −25°C while doubling storage at −60°C to −80°C.

- December 2024: Novo Holdings completed the acquisition of Catalent in an all-cash transaction valued at approximately USD 16.5 billion, consolidating fill-finish capacity and associated clinical supply capabilities under the broader Novo ecosystem.

- June 2024: Labcorp launched Global Trial Connect, a digital suite that improves site workflows, reduces data delays, and supports supply readiness with tools for kit inventory and sample management.

Global Clinical Trial Kits Market Report Scope

Clinical trial kits are pre-assembled, protocol-specific packages used to support the conduct of clinical trials at investigational sites or patient locations. They typically include investigational products, sample collection materials, ancillary consumables, and patient instructions. These kits are designed to ensure regulatory compliance, dosing accuracy, and standardized trial execution. The Clinical Trial Kits Market Report is Segmented by Service (Kitting Solutions, and Logistics), Phase (Phase I, Phase II, Phase III, and Phase IV), Application (Small Molecule, Large Molecule, and Medical Devices), End User (Pharmaceutical & Biopharmaceutical Companies, Contract Service Providers, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Size and Forecasts are Provided in Terms of Value (USD) for all the above segments.

| Kitting Solutions | Drug Kits |

| Sample Collection Kits | |

| Self-Therapy Kits | |

| Medical Device Trial Kits | |

| Cell Therapy-Specific Kits | |

| Other Solutions | |

| Logistics | Transportation |

| Warehousing & Storage | |

| Other Logistics |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Small Molecule Trials |

| Large Molecule Trials |

| Medical Device Trials |

| Pharmaceutical & Biopharmaceutical Companies |

| Contract Service Providers (CRO/CDMO) |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Kitting Solutions | Drug Kits |

| Sample Collection Kits | ||

| Self-Therapy Kits | ||

| Medical Device Trial Kits | ||

| Cell Therapy-Specific Kits | ||

| Other Solutions | ||

| Logistics | Transportation | |

| Warehousing & Storage | ||

| Other Logistics | ||

| By Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By Application | Small Molecule Trials | |

| Large Molecule Trials | ||

| Medical Device Trials | ||

| By End User | Pharmaceutical & Biopharmaceutical Companies | |

| Contract Service Providers (CRO/CDMO) | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the long-range outlook for the clinical trial kits market through 2031?

The clinical trial kits market size is projected to rise from USD 1,944.63 million in 2025 to USD 3,060.47 million by 2031 at an 8.13% CAGR, supported by risk-based GCP adoption, DTP workflows, and expanding biologics and CGT pipelines.

Which services are growing fastest within clinical trial kits?

Kitting solutions are the fastest-growing at an 8.80% CAGR, while logistics services remain the largest by revenue due to higher shipment velocity and temperature-control needs across decentralized and cross-border trials.

How are regulations like ICH E6(R3) and the EU CTR shaping kit design and logistics?

ICH E6(R3) enables risk-based, DCT-ready supply and permits direct-to-patient shipping when justified, while the EU CTR’s CTIS portal standardizes submissions and transparency, pushing suppliers to validate packaging and automate labeling and batch data capture.

What application areas are driving premium demand?

Large molecule and CGT programs are driving premium kit demand due to cryogenic custody, serialized chain-of-identity, and device integration, with large molecule trials forecast to grow at an 8.81% CAGR through 2031.

Which regions represent the largest and fastest-growing opportunities?

North America led with 41.39% share in 2025 due to mature infrastructure and advanced digital coordination, while Asia-Pacific is expected to grow at a 9.50% CAGR due to scaled oncology, vaccine, and biologic programs.

How is decentralization changing kit requirements?

Decentralized and hybrid models are increasing direct-to-patient shipments, mail-back kits, and local lab use, which elevates demand for validated home-use packaging, clear instructions, serialized tracking, and automated temperature monitoring.

Page last updated on: