Market Overview

| Study Period | 2020 - 2031 |

|---|---|

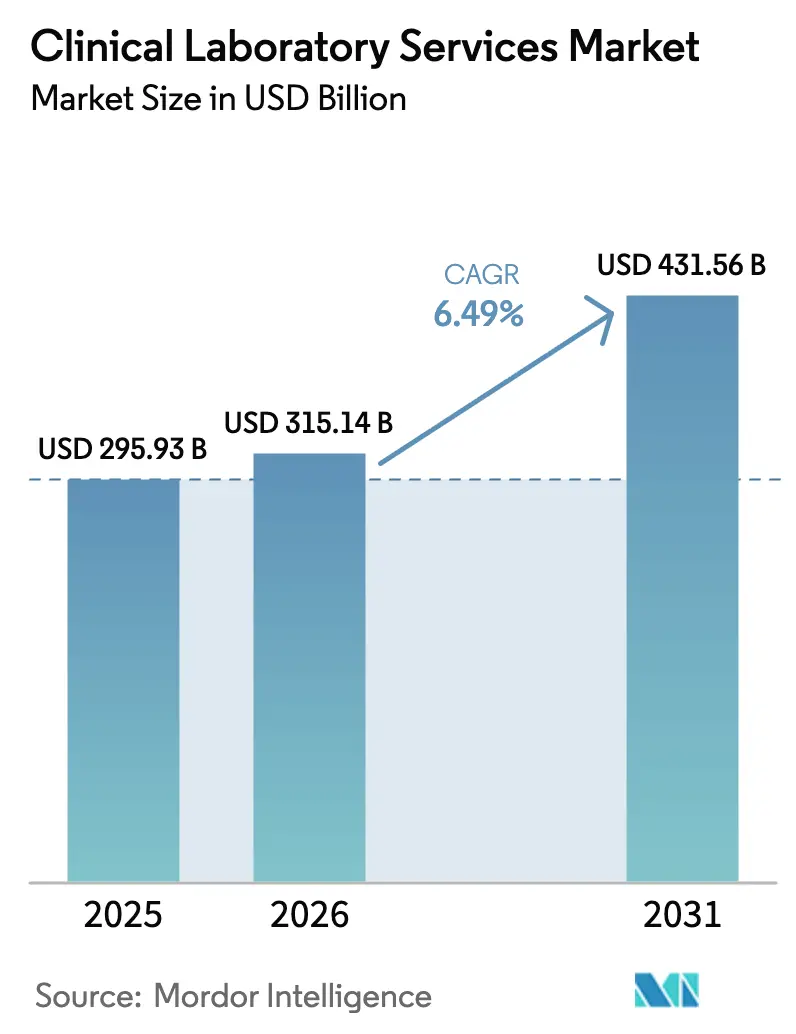

| Market Size (2026) | USD 315.14 Billion |

| Market Size (2031) | USD 431.56 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

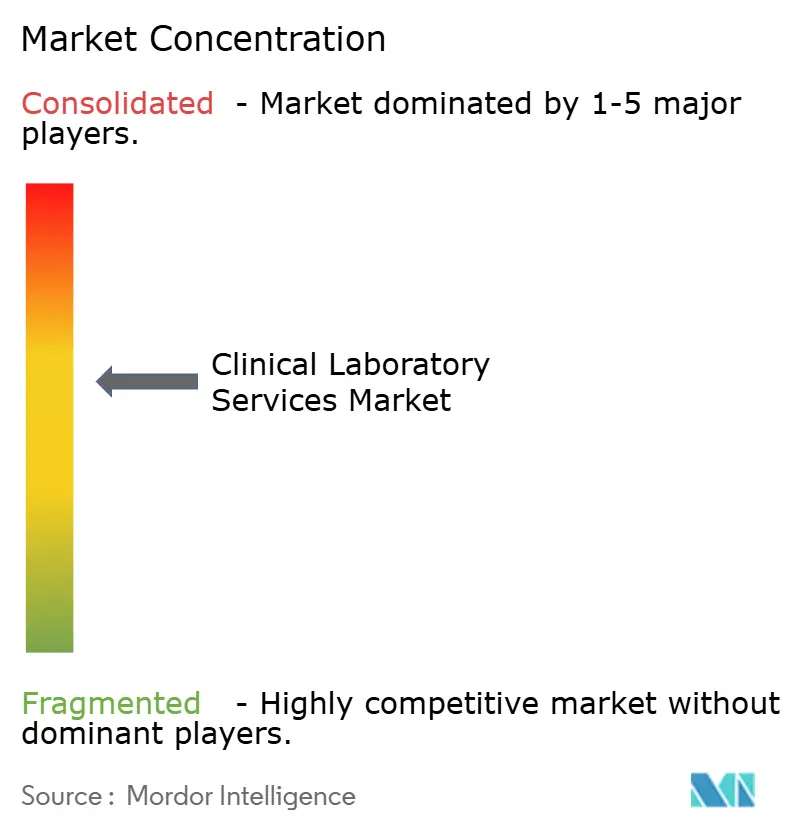

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Laboratory Services Market Analysis by Mordor Intelligence

The clinical laboratory services market size is projected to expand from USD 295.93 billion in 2025 and USD 315.14 billion in 2026 to USD 431.56 billion by 2031, registering a CAGR of 6.49% between 2026 to 2031. This growth highlights the sector's transition from a fee-for-volume model to a value-based diagnostics framework, where decision-support algorithms embedded in electronic health records increasingly guide the selection of tests. The market's expansion is driven by three key structural factors: the increasing prevalence of non-communicable diseases that require continuous monitoring, regulatory mandates replacing legacy laboratory-developed tests with cleared assays, and the integration of real-time data to automate reflex testing. Laboratories that adopt high-throughput automation, liquid biopsy platforms, and mobile phlebotomy services are well-positioned to mitigate reimbursement pressures while capitalizing on the growing demand for preventive screenings and chronic care programs. Meanwhile, competitive dynamics are intensifying as reference laboratories focus on vertical integration, acquisition of specialty test assets, and scaling mobile collection networks to offset declining margins in routine chemistry.

Key Report Takeaways

- By test type, clinical chemistry led with a 56.60% share of the clinical laboratory services market in 2025, while genetics and molecular diagnostics are expected to advance at a 9.50% CAGR through 2031.

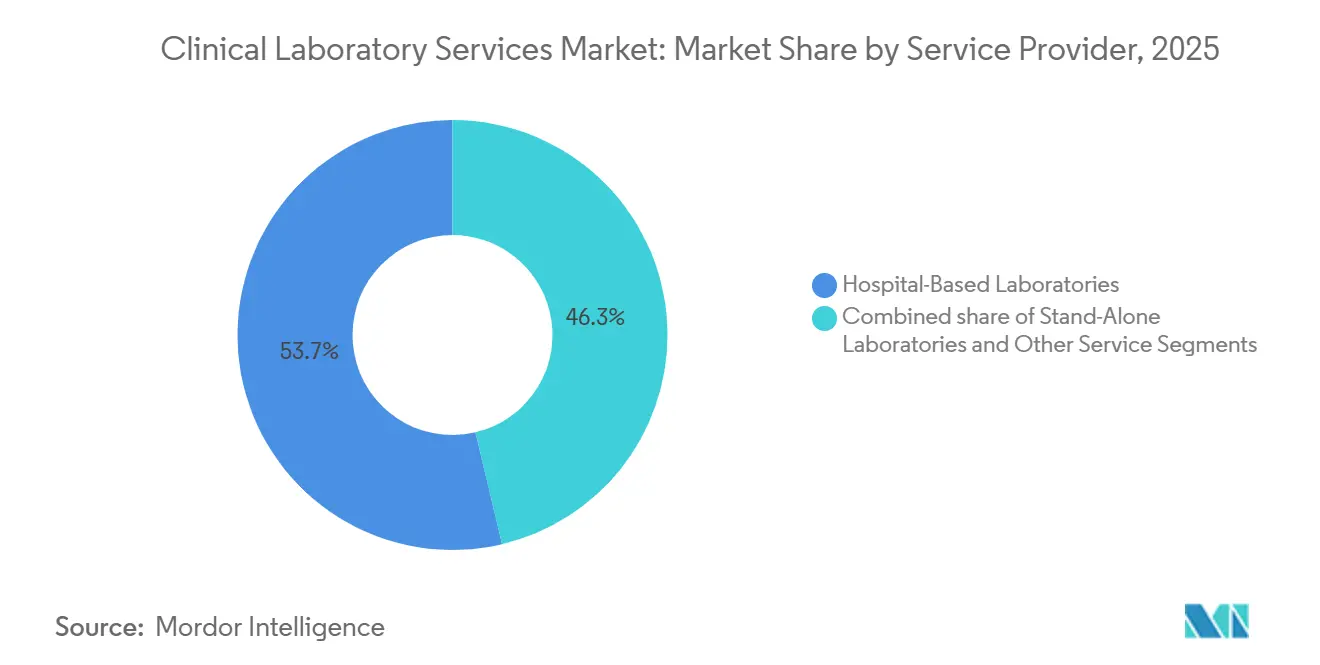

- By service provider, hospital-based laboratories held 53.70% of the clinical laboratory services market size in 2025; stand-alone and independent laboratories are growing at an 8.20% CAGR during the same period.

- By application, infectious disease testing accounted for 31.40% of the clinical laboratory services market size in 2025, and oncology testing is projected to rise at a 10.70% CAGR through 2031.

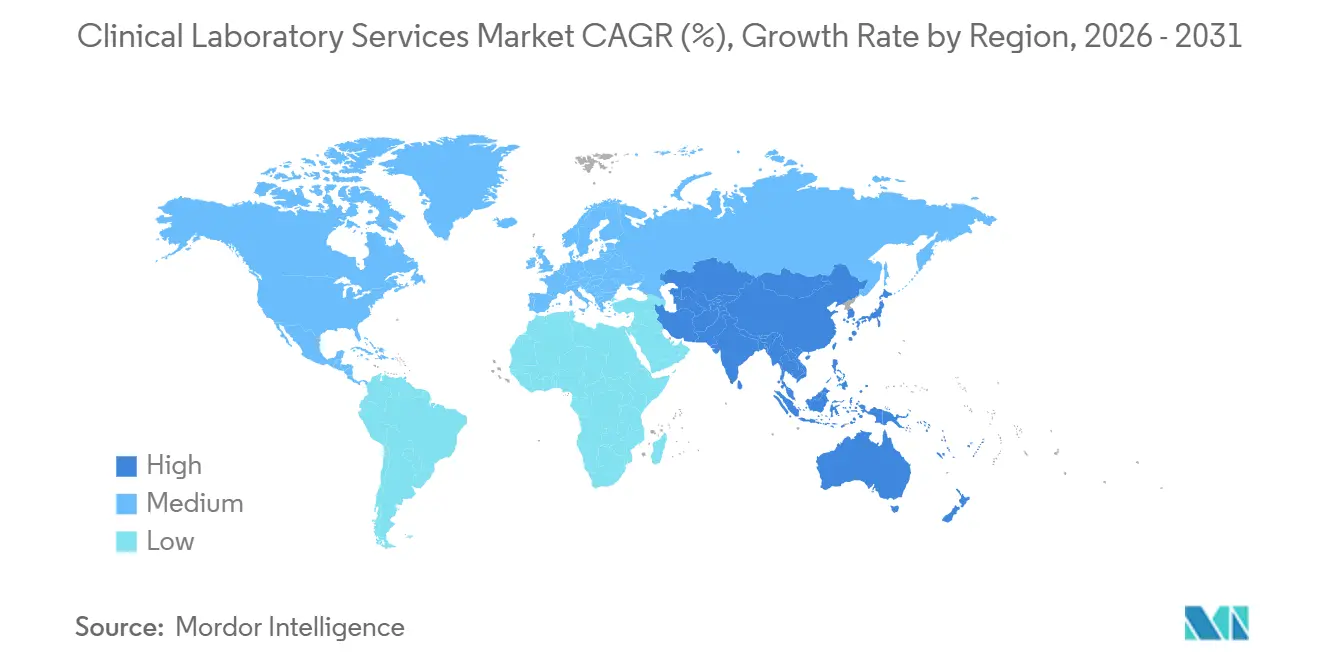

- By geography, North America captured a 41.30% revenue share in 2025, whereas the Asia-Pacific region is set to expand at a 7.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Laboratory Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Burden of Chronic and Infectious Diseases | +1.8% | Global, highest intensity in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Aging Population and Expansion of Preventive Health Screening Programs | +1.5% | North America, Europe, Japan; spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Technological Advancements in Molecular and High-Throughput Diagnostics | +1.3% | North America and Europe early adoption; Asia-Pacific scaling phase | Medium term (2-4 years) |

| Expansion of Health Insurance and Universal Healthcare Coverage in Emerging Markets | +1.2% | Asia-Pacific (India, China, Southeast Asia), Middle East & Africa | Long term (≥ 4 years) |

| Rise of Decentralized Specimen Collection and At-Home Phlebotomy Services Enabling Higher Test Volumes | +0.4% | North America and select European urban centers | Short term (≤ 2 years) |

| Integration of Real-Time Laboratory Data with AI-Driven Clinical Decision Support Systems Driving Test Utilization | +0.5% | North America and Western Europe; pilot programs in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Burden of Chronic and Infectious Diseases

Non-communicable diseases caused 41 million deaths in 2024, equivalent to 71% of global mortality, while diabetes prevalence climbed to 830 million cases. Such epidemiology drives serial testing for glycemic control, lipid management, and renal surveillance, thereby increasing the frequency of tests per patient. Concurrently, PCR confirmation of mpox outbreaks and mandatory tuberculosis screening in visa and employment protocols sustain elevated infectious disease volumes[1]Centers for Disease Control and Prevention, “Mpox 2024 Response Update,” cdc.gov. Laboratories equipped with high-throughput analyzers and data analytics capture recurring revenue, whereas those relying on manual batch processing encounter margin pressure as payers’ lower reimbursement on routine panels. In the Asia-Pacific and sub-Saharan Africa regions, the dual burden of communicable and chronic illnesses requires laboratories to maintain both molecular and chemical capacity, stretching capital budgets and staffing plans. The clinical laboratory services market responds with consolidated testing hubs that automate central workflows yet retain rapid reflex capabilities for acute pathogens.

Aging Population and Expansion of Preventive Health Screening Programs

The global population aged 65 and older reached 1.6 billion in 2024 and is expected to surpass 2.1 billion by 2050[2]United Nations Population Division, “World Population Prospects 2024,” un.org. Individuals in this cohort order 3.2 times more laboratory tests than those under 50, reflecting the need for monitoring for osteoporosis, cognitive decline, and complex medication regimens. Preventive programs now bundle cardiovascular panels, pre-diabetes screenings, and germline risk assessments into annual wellness visits, which employers and insurers subsidize. CMS broadened its cognitive-assessment benefit in 2024 to include homocysteine and B12, bolstering specialty chemistry demand. In Japan, biennial metabolic syndrome screening generates over 50 million tests annually, demonstrating how national mandates embed laboratory utilization into public health infrastructure. Laboratories that integrate data reporting with primary-care portals gain preferred-provider status, while those lacking interoperability risk exclusion from pay-for-performance contracts.

Technological Advancements in Molecular and High-Throughput Diagnostics

The FDA cleared Illumina’s TruSight Oncology Comprehensive assay in August 2024, allowing a single sample to guide 15 targeted therapies. Exact Sciences won approval for Cologuard Plus in May 2024, a multi-target stool DNA test with heightened adenoma sensitivity. Reference laboratories now automate more than 10,000 daily specimens using track-based systems that shorten routine chemistry turnaround from 48 hours to under 12 hours. Artificial-intelligence modules detect instrument drift in real-time and trigger automatic reflex tests, reducing verification labor and error rates to as low as 0.02%. Capital investments exceeding USD 5 million per site are offset by labor savings and higher reimbursement on companion diagnostics, strengthening the clinical laboratory services market.

Expansion of Health Insurance and Universal Healthcare Coverage in Emerging Markets

India’s Ayushman Bharat scheme now safeguards 500 million residents with INR 500,000 (approximately USD 6,000) of family coverage, formalizing diagnostic utilization among previously uninsured groups. China’s 14th Five-Year Plan has earmarked CNY 1.2 trillion (approximately USD 165 billion) for health infrastructure, targeting county-level laboratory networks that funnel specimens to provincial hubs. Southeast Asian nations are piloting social-insurance packages that bundle basic laboratory services into primary care, providing laboratories with predictable cash flows while capping prices below North American benchmarks. To preserve margins, operators scale centralized processing centers, deploy lean staffing models, and prioritize high-throughput analyzers that lower per-test costs by as much as 35%. The clinical laboratory services market thus expands on volume even when unit pricing is moderated.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement Cuts and Pricing Pressures Amid Value-Based Care Models | −0.9% | North America (Medicare/Medicaid), Europe | Short term (≤ 2 years) |

| Stringent and Evolving Regulatory Requirements for High-Complexity Testing | −0.5% | Global, highest compliance burden in North America and Europe | Medium term (2-4 years) |

| Cybersecurity and Data Privacy Risks Constraining Adoption of Cloud-Based Lab Information Systems | −0.3% | North America and Europe; emerging concern in Asia-Pacific | Short term (≤ 2 years) |

| Intensifying Competition from Point-of-Care Testing Curtailing Central Lab Volumes | −0.6% | North America and Europe; selective impact in urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Cuts and Pricing Pressure within Value-Based Care Models

CMS proposed a 3.4% reduction to the 2026 Clinical Laboratory Fee Schedule, following its previous reversal of a 15% cut in 2025, underscoring persistent budget pressure. Private payers echo Medicare by reimbursing at 120–150% of Medicare rates instead of accepting billed charges, while imposing prior-authorization hurdles on genetic panels. Value-based contracts bundle diagnostics into capitated payments, shifting utilization risk to laboratories, which must manage test ordering with data analytics and physician education. In Europe, national health systems cap payments for molecular assays, restricting revenue growth through mix enrichment. Laboratories that diversify into direct-to-consumer channels and specialty oncology testing partially offset declines, yet routine chemistry margins remain compressed across the clinical laboratory services market.

Stringent and Evolving Regulatory Requirements for High-Complexity Testing

The FDA’s April 2024 rule phases out the laboratory-developed test exemption, requiring premarket review for assays that were previously governed only by CLIA, with compliance staggered through 2030. Validation costs, ranging from USD 500,000 to USD 5 million per assay, threaten niche laboratories lacking capital or regulatory expertise, thereby accelerating market consolidation. Europe’s In Vitro Diagnostic Regulation similarly tightens conformity assessment, prompting some reagent suppliers to exit low-volume product lines and forcing laboratories to re-validate methods under ISO 15189. Annual quality-system maintenance adds USD 100,000–300,000 for mid-size labs, disproportionately affecting emerging-market operators. These factors temper the overall clinical laboratory services market CAGR despite volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Assays Become Revenue Catalysts

Clinical chemistry contributed 56.60% to the clinical laboratory services market in 2025, primarily driven by metabolic panel and lipid testing, which are central to chronic disease management. Genetics and molecular diagnostics are expected to expand at a 9.50% CAGR, outpacing all other modalities, as companion diagnostics gain payer coverage and liquid biopsy platforms enable minimal residual disease surveillance. Immunology and serology remain steady in demand for autoimmune profiling, while microbiology and cytology volumes shift toward rapid molecular platforms that deliver identification within hours. Hematology maintains relevance through automated differential counts, yet faces pricing pressure from the Clinical Laboratory Fee Schedule. Laboratories investing in next-generation sequencing and bioinformatics can grow revenue without proportional volume gains, albeit at capital costs surpassing USD 10 million per site.

Liquid biopsy adoption highlights this shift. Guardant Health’s minimal residual disease assay tracks tumor DNA in blood months before imaging reveals recurrence, offering new recurring-revenue streams from oncology follow-up. Exact Sciences’ Cologuard Plus further illustrates how non-invasive molecular screening can reach patients who refuse colonoscopy, though reimbursement negotiations continue. Mass spectrometry adoption within clinical chemistry labs defends routine territory by delivering higher specificity in vitamin D and therapeutic-drug assays, where point-of-care devices lack accuracy. Balancing high-margin, low-volume molecular tests with price-pressured routine assays is central to sustaining profitability across the clinical laboratory services market.

By Service Provider: Independent Labs Accelerate via Outreach Models

Hospital-based laboratories controlled 53.70% of the clinical laboratory services market size in 2025, propelled by inpatient acuity and stat testing. Stand-alone and independent laboratories, growing at an 8.20% CAGR, leverage centralized processing hubs, direct employer contracts, and mobile phlebotomy fleets to undercut hospital facility fees. Quest Diagnostics’ CAD 1.35 billion acquisition of LifeLabs added 11 million patient encounters and cross-border infrastructure, demonstrating how scale delivers cost advantages that hospitals struggle to match. Labcorp’s USD 237.5 million purchase of BioReference Health assets reinforced its pivot toward specialty women’s health and oncology, where reimbursement is richer, and contract terms extend beyond five years.

Independent operators centralize volumes in high-throughput hubs that reduce per-test costs by 30–40% compared to hospital labs, while offering at-home collection that lowers patient no-show rates to under 5%. Hospitals defend their share in emergency-driven settings but lose outpatient specimens as physicians opt for independent labs for convenience and cost. Retail health clinics and physician-office labs offer niche point-of-care services, yet they remain constrained by the complexity of CLIA regulations. The clinical laboratory services market thus experiences a two-track evolution: consolidation among reference laboratories and the gradual outsourcing of non-critical in-hospital testing to efficient external partners.

By Application: Oncology Testing Delivers Premium Economics

Infectious disease testing generated 31.40% of revenue in 2025, supported by respiratory panels and mandated tuberculosis screens. Oncology and tumor marker testing are forecast to grow at a 10.70% CAGR, reflecting the rising adoption of liquid biopsy, comprehensive genomic profiling, and early-detection assays. Laboratories that supply oncology tests receive reimbursement 10–20 times higher than routine infectious-disease screens, which lifts gross margins even at modest volumes. Endocrinology and metabolic panels remain staple revenue contributors, while cardiovascular testing seeks differentiation through advanced lipoprotein particle analysis as standard lipid panel pricing declines.

Drug discovery and clinical-trial support laboratories report double-digit revenue lifts as sponsors adopt decentralized protocols, requiring central labs to coordinate remote specimen collection and near-real-time data feeds. Guardant360 CDx gained multiple companion diagnostic approvals in 2024, showing how single assays can replace multiple gene tests, improve payer acceptance, and streamline sample logistics. Laboratories unable to integrate bioinformatics pipelines or secure oncology practice partnerships risk marginalization. Consequently, the clinical laboratory services market rewards operators that pair specialized oncology, genetics, and trial services with scalable routine capacity.

Geography Analysis

North America commanded 41.3% of the clinical laboratory services market in 2025, owing to advanced molecular infrastructure, high electronic health record penetration, and Medicare fee-for-service volumes. The Protecting Access to Medicare Act dampens growth, as reimbursement cuts lowered payments for high-volume chemistry tests by up to 30%, alongside commercial payer reference-based pricing that narrows margins[3]Centers for Medicare & Medicaid Services, “Clinical Laboratory Fee Schedule Updates,” cms.gov. Quest Diagnostics and Labcorp processed more than 500 million requisitions combined, leveraging their scale to absorb pricing pressure while investing in mobile phlebotomy and artificial intelligence-driven quality control. Canada’s government-funded model channels volumes to provincial labs, with LifeLabs integration into Quest setting a precedent for cross-border service models. Operators aim to offset slower routine growth by expanding their support for liquid biopsy and decentralized clinical trials.

Europe’s clinical laboratory services market growth is constrained by national reference pricing, which caps reimbursement for high-complexity assays, and by ongoing compliance with the In Vitro Diagnostic Regulation, which strains reagent supply chains. SYNLAB and Eurofins deploy centralized hubs across multiple countries to amortize accreditation costs and harmonize quality systems. Germany and the United Kingdom restrict reimbursement for molecular testing unless strict clinical criteria are met, thereby curbing revenue expansion driven by the mix. Nevertheless, niche opportunities persist in pan-European clinical-trial laboratories and in integrated radiology-laboratory offerings, exemplified by Sonic Healthcare’s acquisition of Canberra Imaging Group, which aligns pathology and imaging under unified contracts.

The Asia-Pacific region is expected to post a 7.84% CAGR through 2031, driven by expansions in universal health coverage in India and China, as well as mandatory infectious disease screening for visa and employment processes. India’s Ayushman Bharat and China’s infrastructure stimulus inject large volumes into the clinical laboratory services market, yet pay 40–60% below North American rates. Laboratories thus focus on economies of scale, outsourcing reagent leasing, and adopting automation to sustain profitability. Japan’s aging demographic and mandatory metabolic screening program create a steady demand for routine chemistry, while private laboratories experiment with genomic screening packages aimed at affluent consumers. Southeast Asian pilots of social insurance bundles further expand the user base, making the Asia-Pacific region the fastest-growing contributor to global volumes.

The Middle East and Africa are experiencing greenfield investments tied to public-private partnerships that aim to shorten specimen transit times in remote areas, while Gulf Cooperation Council states are funding advanced molecular labs to support medical tourism. South America’s progress hinges on Brazil and Argentina digitizing requisition workflows to enable batch processing and centralized quality oversight. Taken together, geographic dispersion of reimbursement models, patient demographics, and infrastructure readiness shape a diversified growth matrix across the clinical laboratory services market.

Competitive Landscape

The top five participants - Quest Diagnostics, Labcorp, Sonic Healthcare, Eurofins Scientific, and SYNLAB - capture roughly 35–40% of global revenue, indicating moderate concentration across the clinical laboratory services market. Larger players offset shrinking routine chemistry margins by acquiring specialty test portfolios, hospital outreach contracts, and central laboratory services. Quest’s CAD 1.35 billion LifeLabs acquisition added 11 million encounters and reinforced its data-sharing backbone for multinational clinical trials. Labcorp’s USD 237.5 million purchase of BioReference women’s health and oncology assets positioned it further into high-margin genetics panels.

Technology investment is the new competitive fulcrum. Laboratories deploy artificial intelligence quality-control modules that reduce manual verification tasks by up to 60% and automate specimen triage. Mobile phlebotomy fleets, such as QuestDirect and Pixel by Labcorp, reduce no-show rates below 5% and enable payers to capture adherence gains in chronic disease monitoring. Liquid biopsy remains a contested white space: Guardant Health and Natera claim early footholds, but reference laboratories are licensing assays or pursuing bolt-on acquisitions to secure capabilities.

Point-of-care molecular devices from Abbott and Cepheid siphon respiratory and sexually transmitted infection volumes from central labs. In response, reference labs promote hybrid models combining on-site rapid tests with centralized next-generation sequencing to preserve share. Small specialty labs emphasize rare-disease and pharmacogenomic panels but face existential risk from the FDA’s laboratory-developed-test rule that raises entry costs for high-complexity assays. Scale, automation, and specialty diversification remain decisive in sustaining profitability across the clinical laboratory services market.

Clinical Laboratory Services Industry Leaders

Sonic Healthcare Limited

Eurofins Scientific SE

SYNLAB International GmbH

Labcorp

Quest Diagnostics Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Corewell Health and Quest Diagnostics announced the completion of their joint venture agreement. The partnership aims to expand access to innovative, high-quality, and affordable laboratory services in Michigan. This collaboration is part of their effort to improve healthcare services in the region.

- August 2025: Quest Diagnostics completed its acquisition of select clinical testing assets from Spectra Laboratories, a division of Fresenius Medical Care. This move enhances Quest's ability to offer dialysis-related testing services to independent dialysis clinics.

- May 2025: Bayer launched its new Imaging Core Lab, Centafore, leveraging over 25 years of clinical trial support. The company now offers tailored imaging services for external clients across various therapeutic areas and development stages.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the clinical laboratory services market as patient-oriented diagnostic tests on blood, tissue, or other specimens that inform screening, diagnosis, or monitoring across inpatient and outpatient care. The scope covers routine chemistry, hematology, immunology, microbiology, cytology, and molecular or genetic assays delivered by hospital, independent, and public-health laboratories for the 2019-2030 period.

Central laboratories that only process research or clinical-trial samples without reporting back to treating clinicians are not counted.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immunology / Serology

- Microbiology & Cytology

- Genetics / Molecular Diagnostics

- Hematology

- Other Test Types

- By Service Provider

- Hospital-Based Laboratories (In-Patient & Out-Patient)

- Stand-Alone / Independent Laboratories

- Other Service Providers

- By Application

- Infectious Disease Testing

- Oncology & Tumor Marker Testing

- Endocrinology & Metabolic Disorder Panels

- Cardiovascular & Lipid Testing

- Drug Discovery & Clinical Trial Support

- Other Applications

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview laboratory directors, reference-lab managers, pathologists, and payer medical officers across North America, Europe, Asia-Pacific, and Latin America to confirm reimbursement shifts, margin pressure, and molecular-test uptake that desktop work alone cannot surface.

Desk Research

Mordor analysts begin by mining the WHO Global Health Observatory, CDC National Center for Health Statistics, CMS Medicare fee schedules, ECDC dashboards, and OECD Health Data. They then weave in annual reports, regulator filings, and peer-reviewed articles. Paid assets such as D&B Hoovers and Dow Jones Factiva supply verified revenue splits and expansion news. The sources named illustrate, not exhaust, the reference stack.

Market-Sizing & Forecasting

A top-down model pairs national health spending with processed test counts, adjusting for test mix, reimbursement schedules, and screening intensity. Targeted bottom-up checks, sampled average selling price multiplied by test numbers, anchor totals. Key drivers include chronic-disease prevalence, molecular-diagnostics penetration, payer revisions, automation spend, and physician-visit density. Multivariate regression, stress-tested under three macro scenarios, projects values to 2030.

Data Validation & Update Cycle

Outputs pass anomaly flags, variance checks, and peer review. Models refresh each year, with mid-cycle updates after material policy shifts, and a final sweep precedes client release.

Why Mordor's Clinical Laboratory Services Baseline Stands Firm

Published estimates differ because firms pick unmatched service mixes, currencies, and cut-off years. Yet when the main clause finally arrives, our disciplined scope keeps numbers grounded and current.

These comparisons show that Mordor Intelligence, through yearly refreshes, scenario-tested drivers, and clear service boundaries, provides a balanced baseline trusted by decision makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 295.90 B | Mordor Intelligence | |

| USD 237.76 B | Regional Consultancy A | Excludes genetic panels; relies on 2023 utilization ratios |

| USD 291.01 B | Trade Journal B | Blends central trial labs; applies flat ASP growth |

| USD 274.21 B (2024) | Industry Association C | Uses pre-COVID volumes and conservative CAGR carry-forward |

Key Questions Answered in the Report

How fast is the clinical laboratory services market expected to grow through 2031?

The market is projected to advance at a 6.49% CAGR, expanding from USD 315.14 billion in 2026 to USD 431.56 billion by 2031.

Which test modality is expanding the quickest?

Genetics and molecular diagnostics is forecast to post a 9.50% CAGR, propelled by FDA-approved companion diagnostics and rising payer coverage.

Why are independent laboratories gaining ground on hospital-based labs?

Independent laboratories centralize processing, use mobile phlebotomy, and contract directly with employers, enabling 30-40% lower per-test costs than most hospital labs.

What regions present the highest growth potential?

Asia-Pacific leads with a projected 7.84% CAGR, fueled by universal health-coverage expansions in India and China and mandatory infectious-disease screening programs.

How will new FDA regulations affect laboratory-developed tests?

The 2024 FDA rule requires premarket review for high-complexity assays, adding USD 500,000 to USD 5 million in validation costs per test and likely accelerating industry consolidation.

Which recent technology approvals are reshaping oncology diagnostics?

FDA clearance of Illumina's TruSight Oncology Comprehensive assay and approval of Exact Sciences-Cologuard Plus are expanding access to comprehensive genomic profiling and non-invasive cancer screening.

Page last updated on: