Clinical Trial Technology and Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 31.24 Billion |

| Market Size (2031) | USD 63.91 Billion |

| Growth Rate (2026 - 2031) | 15.39% CAGR |

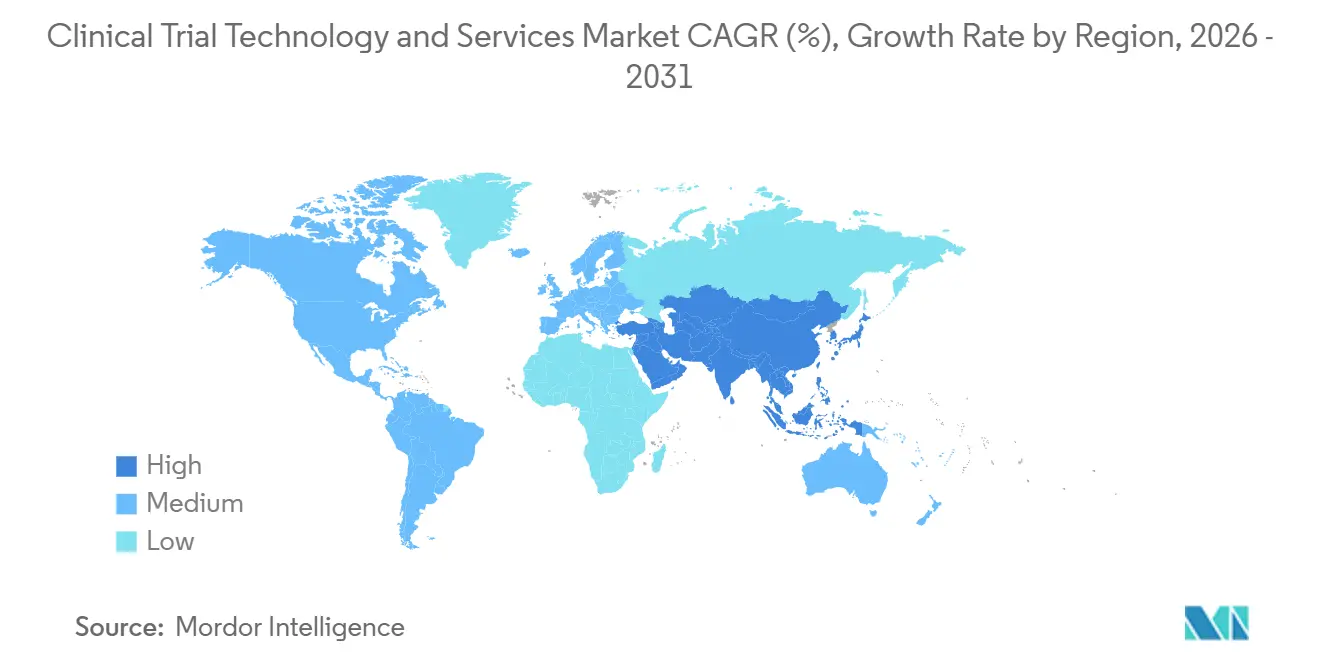

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trial Technology and Services Market Analysis by Mordor Intelligence

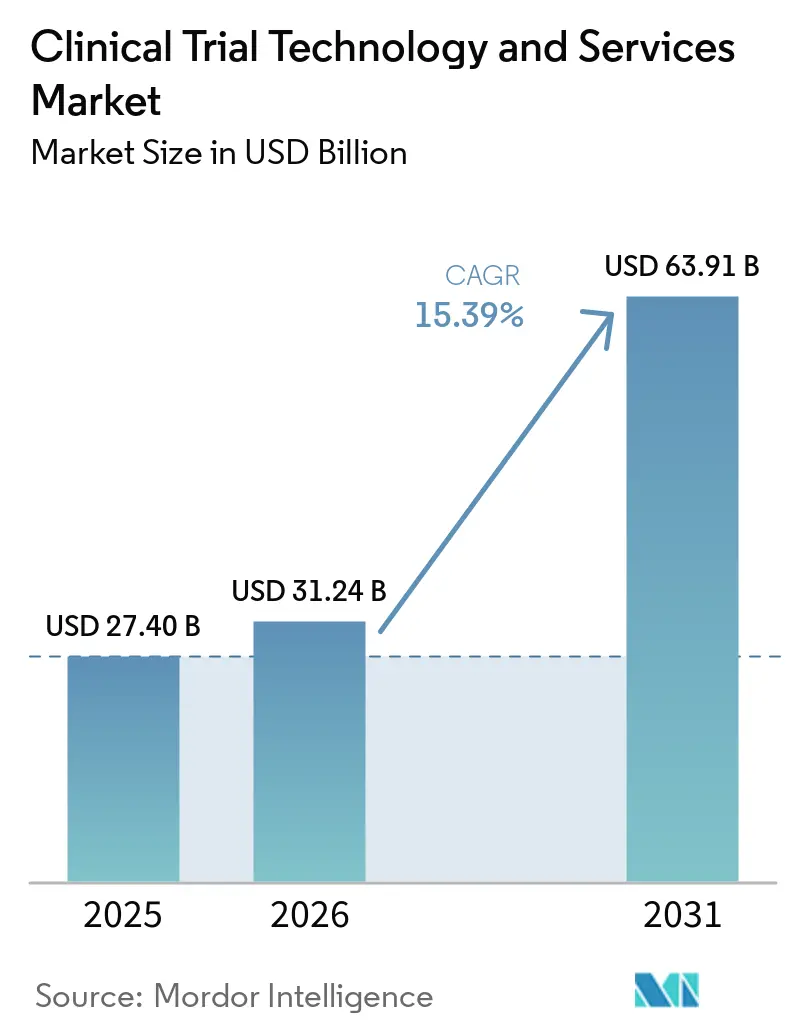

The Clinical Trial Technology And Services Market size is expected to increase from USD 27.40 billion in 2025 to USD 31.24 billion in 2026 and reach USD 63.91 billion by 2031, growing at a CAGR of 15.39% over 2026-2031.

The market is expanding because sponsors and CROs are putting more money into connected platforms that can handle more complex protocols, stronger data controls, and broader digital trial workflows. The clinical trial technology and services market is also moving past simple software replacement, since buyers now want unified environments that connect data capture, trial management, analytics, patient engagement, and compliance functions in one operating model. Growth is also being supported by broader use of decentralized and hybrid trials, rising AI deployment in feasibility and monitoring, and a heavier reliance on specialist service partners for implementation and integration. Competition remains active across both technology and services, with platform vendors trying to widen suite coverage while CROs and service providers use therapeutic depth, site reach, and digital execution capability to protect accounts. The market also faces pressure from integration difficulty, validation costs, and cybersecurity exposure, which means buyers are favoring vendors that can reduce deployment friction while meeting audit and traceability expectations.

Key Report Takeaways

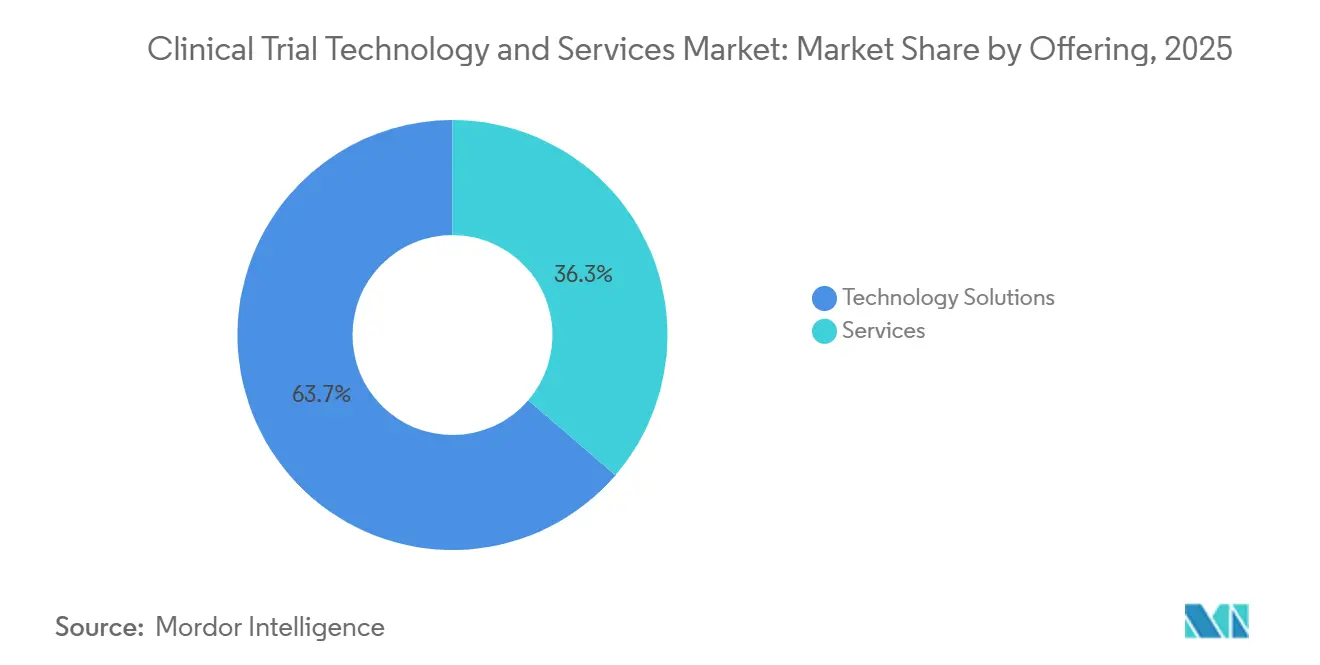

- By offering technology solutions, the company held 63.72% share of the clinical trial technology and services market size in 2025, while services are forecast to grow at a 16.49% CAGR through 2031.

- By deployment model, cloud-based held 49.77% of revenue in 2025, while hybrid is projected to expand at an 18.22% CAGR through 2031.

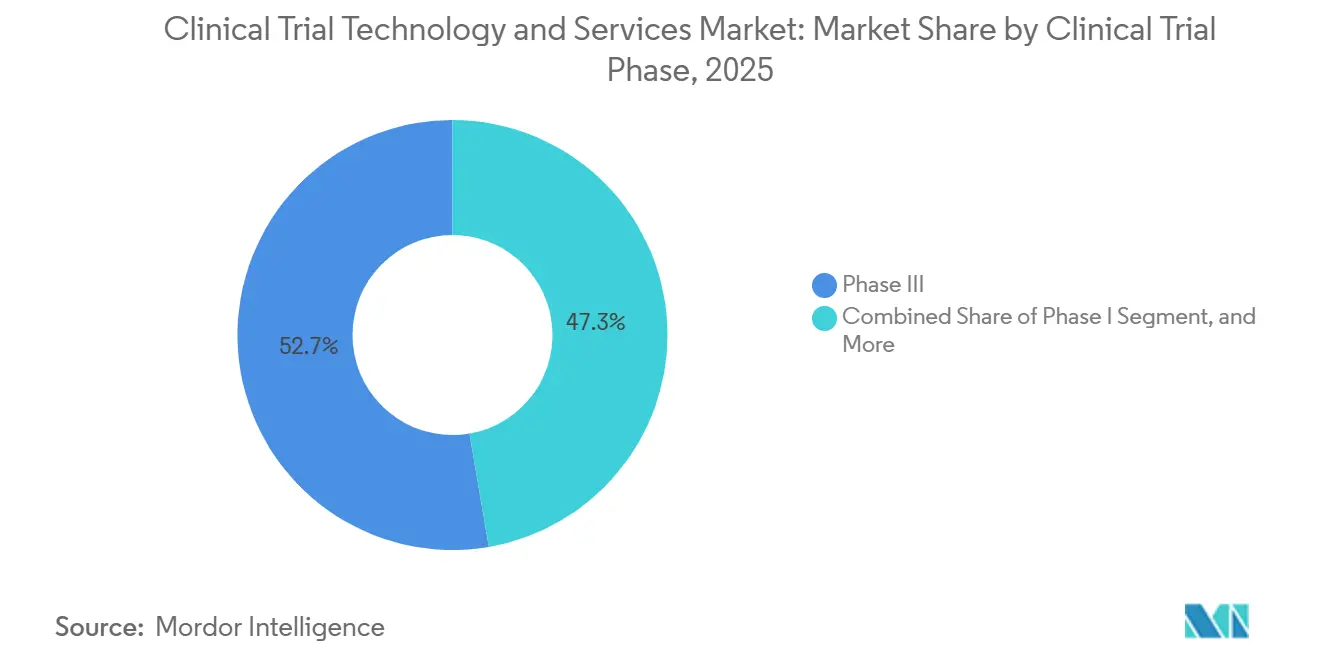

- By clinical trial phase, phase III accounted for 52.68% share in 2025, while phase I is expected to advance at a 17.74% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 43.82% of revenue in 2025, while CROs recorded the highest projected CAGR at 16.86% through 2031.

- By geography, North America held 41.64% of revenue in 2025, while Asia-Pacific is forecast to grow at an 18.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Trial Technology and Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Clinical Trial Complexity and Protocol Burden | +3.0% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Rapid Adoption of Decentralized and Hybrid Trial Operations | +2.8% | Global, early adoption in North America, spillover to Europe and Asia-Pacific | Medium term (2-4 years) |

| Expansion of AI-Enabled Feasibility, Monitoring, and Analytics | +2.5% | Global, concentrated in North America and Europe, growing in Asia-Pacific | Medium term (2-4 years) |

| Rising Outsourcing by Sponsors Seeking Flexible Trial Execution | +2.2% | Global, strongest in North America, Asia-Pacific gaining rapidly | Short term (≤ 2 years) |

| More Stringent Data Integrity, Traceability, and Audit Expectations | +1.8% | Global, particularly Europe and North America | Short term (≤ 2 years) |

| Site Burden Reduction Through Unified Clinical Operating Platforms | +1.5% | Global, strongest uptake in North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Clinical Trial Complexity and Protocol Burden

Protocol complexity has become a direct spending trigger in the clinical trial technology and services market because it raises the cost of running studies and increases the need for structured digital oversight. In 2025, 76% of Phase I to Phase IV trials required at least 1 protocol amendment, up from 57% in 2015, and the average protocol accumulated 3.3 amendments across its life cycle. Oncology remained the clearest stress point, where 90% of protocols needed at least 1 substantial amendment, and 45% of substantial amendments were avoidable. A 2025 journal analysis also showed that total data volume per Phase III protocol has been rising by 10.8% a year since 2020, which explains why sponsors are leaning on stronger data collection, workflow, and analytics tools in the clinical trial technology and services market.[1]Scott Bui et al., “Insights Informing Strategies for Optimizing the Collection of Clinical Trial Data,” Therapeutic Innovation & Regulatory Science, link.springer.com Site pressure is also increasing because 38% of sites identified trial complexity as their top operating challenge in 2024, which supports demand for unified workflows that cut duplication and manual effort in the clinical trial technology and services market. That same pressure also reinforces stricter data integrity and audit expectations, since more complex studies create more records, more amendments, and more points of inspection across the trial process.

Rapid Adoption of Decentralized and Hybrid Trial Operations

The clinical trial technology and services market is benefiting from decentralized and hybrid trial adoption because regulators now treat these approaches as part of normal trial planning rather than as limited experiments. The FDA final guidance on trials with decentralized elements gives sponsors clearer operating expectations for telehealth visits, direct-to-patient product movement, digital health technology use, and remote oversight.[2]Food and Drug Administration, “Conducting Clinical Trials With Decentralized Elements,” FDA, fda.gov A 2025 peer-reviewed paper on the Trials@Home RADIAL proof of concept also showed that conventional, hybrid, and fully decentralized designs can be run across multiple countries with technology packages that support onboarding, validation, and post-go-live governance. This is why the clinical trial technology and services market is not moving toward a single end state, because hybrid delivery has become a durable model for studies that still need physical site visits and remote data capture in the same protocol. The same shift also raises the importance of data traceability, since vendors must prove they can manage site and remote data streams together without weakening control. It also strengthens demand for site burden reduction tools, because hybrid operations work better when clinical teams use connected platforms instead of separate point systems.

Expansion of AI-Enabled Feasibility, Monitoring, and Analytics

AI use in the clinical trial technology and services market is moving from isolated pilots into broader platform deployment, and regulatory support is now making that transition more credible. In April 2026, the FDA launched a real-time clinical trial pilot with AstraZeneca and Amgen on Paradigm Health's Study Conduct platform, and at the same time announced an AI-enabled optimization pilot for early phase trials. The NIH TrialGPT tool reached 87.3% accuracy in eligibility screening and reduced screening workload by 42.6%, which speaks directly to one of the most persistent operating bottlenecks in early trials.[3]National Institutes of Health and National Library of Medicine, “TrialGPT – An AI Powered Tool for Matching Patients to Clinical Trials,” NIH, ncbi.nlm.nih.gov Medidata stated in 2026 that its unified clinical AI has been trained across 38,000 validated studies and more than 12 million patients, showing how scale is becoming a commercial advantage in the clinical trial technology and services market. This shift is important because buyers now want AI that works across enrollment, risk management, and monitoring tasks instead of tools that solve only 1 step. It also supports the larger move toward unified operating platforms, since AI performs better when it can draw from broader and better-governed data environments inside the clinical trial technology and services market.

Rising Outsourcing by Sponsors Seeking Flexible Trial Execution

The clinical trial technology and services market is also being pushed higher by rising sponsor outsourcing, especially among smaller and mid-sized biotechnology companies that depend on external trial execution capacity. The SMid biotech companies outsource 71% of clinical trial work to CROs, while the broader outsourcing rate stands at 50.6%, and large pharma outsourcing has eased to 40.8%. This matters because the CRO is no longer only a delivery partner, since it increasingly influences platform choice, workflow design, and service integration across the full clinical operating stack. The clinical trial technology and services market, therefore, gains from a multiplier effect, where each new outsourced program can also pull through software, implementation, and support demand across sponsor and CRO environments. The August 2025 IQVIA and Veeva partnership reflected this reality by linking platform interoperability with service capability, allowing sponsors to use Veeva's clinical suite alongside IQVIA data management, programming, and AI capabilities. The same pattern also rewards vendors that lower validation, training, and change management effort, because outsourced delivery works best when partner ecosystems can deploy technology without heavy rework.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity Across EDC, CTMS, eTMF, and Finance Systems | -2.5% | Global, most acute in North America and Europe where legacy stacks are deepest | Medium term (2-4 years) |

| High Validation, Training, and Change-Management Costs | -1.8% | Global, intensified in regulated markets in Europe and the United States | Short term (≤ 2 years) |

| Cybersecurity, Privacy, and Cross-Border Data Governance Risk | -1.5% | Global, particularly cross-border Europe to Asia-Pacific and United States to Asia-Pacific data corridors | Short term (≤ 2 years) |

| Uneven Digital Readiness Across Sites and Emerging Markets | -1.2% | Asia-Pacific core, with spillover to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across EDC, CTMS, eTMF, and Finance Systems

Integration difficulty remains a major drag on the clinical trial technology and services market because large sponsors still run deep legacy environments that are hard to consolidate. Veeva reported in 2025 that a top 20 biopharma customer removed more than 100 legacy integrations during a unified cloud CTMS move, which required the migration of more than 9 million records and training for more than 4,500 users. A separate Veeva customer story on GSK described a 3-year CTMS modernization program that migrated more than 6 million records from 1,500 active studies and onboarded 4,500 users before go-live. These examples show why the clinical trial technology and services market is not limited by software demand alone, because the cost of connecting EDC, CTMS, eTMF, finance, and legacy systems often shapes vendor choice more than license fees do. The same burden grows when buyers also need validation, training, and change management across large teams and regulated workflows. It also favors service vendors and hybrid deployment models, since many enterprises need staged modernization rather than a single cutover.

Cybersecurity, Privacy, and Cross-Border Data Governance Risk

Cybersecurity and data governance remain active restraints on the clinical trial technology and services market because broader digital trial architectures create larger and more distributed exposure points. The market increasingly depends on federated environments that connect sponsor systems, CRO platforms, site workflows, and remote patient data streams, and that structure expands oversight demands even when tools are technically interoperable. Privacy obligations also vary across regions, which makes cross-border data movement more difficult for global studies and slows adoption in the clinical trial technology and services market when buyers are uncertain about residency, traceability, and access control. This issue is also linked to uneven site readiness, because the value of advanced digital systems falls when local infrastructure, training depth, or operating discipline is inconsistent across study locations. Buyers are therefore placing more weight on security architecture and governance controls during vendor qualification, even when the underlying feature set is strong. As a result, the clinical trial technology and services market continues to reward vendors that combine platform breadth with practical controls that can hold up across remote, hybrid, and cross-border trial environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Momentum Reveals the Hidden Cost of Platform Complexity

Technology solutions held 63.72% of the clinical trial technology and services market share in 2025, showing that core platform demand still leads spending across EDC, CTMS, eTMF, patient engagement, and analytics environments. The clinical trial technology and services market continues to rely on these systems because every sponsor type needs secure data capture, workflow control, and trial oversight across multiple geographies and phases. Within Technology Solutions, AI integration tools are expanding quickly because sponsors want intelligence layers that work across existing systems rather than full platform replacement. Trial management and data collection remain central within this segment, and the pressure on these tools is rising as protocol data volume keeps growing across late stage studies. The same pattern supports the wider clinical trial technology and services industry, where buyers are shifting toward tools that can unify operational data and reduce manual handoffs.

Services is the fastest-growing top-level segment, with a 16.49% CAGR through 2031, which shows that deployment effort is becoming as important as software ownership in the clinical trial technology and services market. This growth reflects a structural gap between the pace of platform complexity and the ability of many sponsor teams to manage integration, validation, and training internally. The August 2025 IQVIA and Veeva partnership made that commercial logic clear because it combined technology interoperability with service delivery capability across data management, EDC programming, and AI support. Recruitment and retention services are also benefiting because more complex protocols increase participant burden and raise dropout risk, especially in oncology and remote enabled studies. Patient engagement tools are therefore rising in parallel with service demand, since the clinical trial technology and services market now values both digital functionality and the operating support needed to make it work consistently at scale.

By Deployment Model: Hybrid Architecture Emerges as a Permanent Enterprise Operating Model

Cloud-Based deployment accounted for 49.77% share of the clinical trial technology and services market size in 2025, reflecting broad use among CROs, mid-sized sponsors, and vendors built around cloud native delivery. The appeal of this model remains straightforward in the clinical trial technology and services market because it supports multi-site scale, faster data access, lower infrastructure burden, and easier connection to decentralized trial tools. Hybrid is the fastest-growing2 deployment model, with an 18.22% CAGR through 2031, which shows that many enterprises are not making full cloud migrations in a single step. Large sponsors often keep validated on-premises record systems in place because full replacement can trigger major revalidation work under regulated compliance frameworks. That keeps the clinical trial technology and services market centered on mixed environments where older record systems and newer cloud analytics or patient tools need to work together reliably.

On-Premise deployment, therefore, remains relevant even as its share faces longer-term pressure in the clinical trial technology and services market. It still matters in settings where data residency rules or internal validation history make local control more attractive than rapid migration. Veeva's January 2026 eSource launch showed how even site level data origination is being pulled into connected workflows through EDC integration and EHR to EDC transfer. As eSource, eConsent, and eCOA tools spread further, deployment decisions will increasingly depend on how well vendors support complex transitions rather than on whether they promote only 1 architecture. That is why the clinical trial technology and services market still gives an advantage to vendors that can manage cloud growth while preserving compatibility with regulated and deeply embedded legacy estates.

By Clinical Trial Phase: Phase I Gains Technology Investment as Regulators Prioritize Early-Stage Efficiency

Phase III represented 52.68% of revenue in 2025, making it the largest phase level spending pool in the clinical trial technology and services market. This concentration is logical because pivotal trials carry larger patient volumes, broader site footprints, and heavier documentation demands than earlier stages. The burden in these studies is also rising because protocol data volume per Phase III study has increased by 10.8% annually since 2020, which raises the need for stronger data collection, coordination, and audit controls. Phase II remains important in absolute spending because sponsors need adaptive design support and continuity as programs move toward later stages. Phase IV is also becoming more relevant in the clinical trial technology and services market because post-market surveillance and real-world data capture require more integrated operating tools.

Phase I is the fastest-growing phase, at a 17.74% CAGR through 2031, and that shift reflects both regulatory focus and pipeline mix. The FDA stated in April 2026 that it would launch an AI-enabled optimization pilot for early phase trials, directly identifying uncertainty, limited patient pools, and inefficient decision-making as problems that deserve new methods. The NIH TrialGPT result also matters here because an 87.3% screening accuracy rate and a 42.6% workload reduction can materially improve patient matching in small and tightly defined populations. The clinical trial technology and services market is therefore seeing stronger early phase demand for platforms that support safety monitoring, dose escalation decisions, and precise enrollment workflows. This effect is reinforced by growth in oncology first-in-human studies and cell and gene therapy programs, where early execution quality has a larger effect on the full development path.

By End User: CRO Technology Spend Accelerates as Platform Choice Becomes a Competitive Differentiator

Pharmaceutical and biotechnology companies held 43.82% share in 2025 and remained the anchor demand group in the clinical trial technology and services market. Their position is sustained by direct ownership of global development pipelines and by a stronger push toward suite consolidation across clinical systems. Many of these companies are moving away from isolated point purchases because they need unified records, stronger traceability, and better cost control across study operations. Medical Device Manufacturers also remain relevant because expanding software as a medical device and regulated device study requirements are drawing more device programs into validated digital workflows. Healthcare Providers and Research Centers are critical to recruitment and study execution, but adoption in this layer is still influenced by hospital integration limits and budget constraints.

CROs are the fastest-growing end-user segment, with a 16.86% CAGR through 2031, which highlights how service partners are shaping technology demand inside the clinical trial technology and services market. The draft states that SMid biotechnology companies outsource 71% of clinical work to CROs, which gives these providers growing influence over the tools used by sponsors. That change alters buying power because the platform chosen by a CRO can become the practical standard for the sponsor program that sits on top of it. IQVIA's 2026 IQVIA.ai launch and Veeva's May 2026 Falcon announcement both reflect this shift toward broader platform control through AI-enabled workflow automation. In practical terms, the clinical trial technology and services market is rewarding CROs that can combine therapeutic expertise, execution scale, and digital operating depth in a single client offer.

Geography Analysis

North America held 41.64% of the clinical trial technology and services market share in 2025, which kept it as the leading regional revenue base. The region benefits from a deep installed base of enterprise EDC, CTMS, and eTMF systems, along with dense sponsor and CRO activity across later-stage studies. The FDA strengthened this position in April 2026 when it launched a real-time clinical trial pilot with AstraZeneca and Amgen using Paradigm Health's cloud-based platform and paired that move with a broader early phase AI initiative. This step matters because it signals a shift toward continuous oversight models that require stronger digital infrastructure throughout the clinical trial technology and services market. Canada adds support through academic research depth and coordinated site networks, while Mexico remains relevant as a cost-effective enrollment location for North American Phase II and Phase III work.

Asia-Pacific is the fastest-growing region, with an 18.92% CAGR through 2031, which gives it a rising strategic role in the clinical trial technology and services market. The region is benefiting from broader sponsor interest, expanding trial activity, and a stronger need for scalable platforms that can operate across mixed site conditions. The clinical trial technology and services market also sees Asia-Pacific as a testing ground for flexible deployment because site maturity varies more widely than it does in North America or Western Europe. That creates room for vendors that can deliver low-friction implementations, practical training, and systems that work in both advanced and less uniform operating environments. The same regional mix also supports hybrid deployment, since buyers often need cloud-connected coordination without assuming that every site can absorb the same level of digital change at the same pace.

Europe remains a significant revenue region in the clinical trial technology and services market, with Germany, the United Kingdom, and France forming core demand centers. The EU Clinical Trials Regulation and CTIS are reshaping sponsor workflows, and the ACT EU monitoring report showed that 3,325 substantial modification applications affecting 2,465 trials were submitted in the first quarter of 2026, from a cumulative 28,070 applications since CTIS started in January 2022. This burden is lifting demand for submission management, eTMF, and data traceability tools across the clinical trial technology and services market. Italy, Spain, and other European countries add meaningful Phase II and Phase III activity, while the Middle East and Africa and South America offer smaller but strategically relevant growth pools for vendors willing to invest early in training and implementation capacity.

Competitive Landscape

The clinical trial technology and services market is moderately concentrated in enterprise platforms and fragmented in specialized solutions and services. Veeva Systems, IQVIA, and Medidata Solutions remain the most visible platform leaders because they compete on suite breadth, AI roadmaps, and the ability to support governed workflows across sponsor and CRO environments. The clinical trial technology and services market is also seeing consolidation pressure because buyers want fewer system handoffs and more accountable delivery across technology and service layers. The August 2025 IQVIA and Veeva agreement was a major strategic move because it ended legal disputes and established bidirectional interoperability between 2 major ecosystems. That change lowered switching friction for sponsors and increased pressure on vendors that rely on narrower or less connected product offers.

Full-service CROs such as ICON, Parexel, Syneos Health, Thermo Fisher PPD, and Medpace compete by linking domain expertise, site reach, and delivery capacity to their digital operating models. In the clinical trial technology and services market, this means service providers are no longer judged only on execution quality, because clients also expect them to help shape usable and compliant technology environments. Veeva's April 2025 SiteVault CTMS release for research sites and its January 2026 eSource launch are good examples of this shift because both moves aimed at site workflows that were still more fragmented and paper-dependent than sponsor systems. These moves show that the clinical trial technology and services market is opening new competitive space at the site layer, where adoption can improve data flow on both sides of the sponsor site relationship.

AI is becoming the next clear line of competition in the clinical trial technology and services market because vendors are trying to automate work instead of only displaying information. Veeva Falcon, announced in May 2026, targets trial master file intake, quality control, safety case triage, and regulatory correspondence across Veeva Development Cloud. IQVIA.ai is positioned in a similar direction, with a unified agentic model spanning clinical, commercial, and real-world use cases. Medidata is also reinforcing scale as a differentiator by highlighting AI capabilities trained across a very large validated study base. Together, these moves suggest that the clinical trial technology and services market will reward vendors that can combine proven compliance depth with practical automation that reduces workload in real study operations.

Clinical Trial Technology and Services Industry Leaders

ICON plc

IQVIA Inc.

Oracle Corporation

Syneos Health

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Veeva Systems announced Veeva Falcon, an agentic AI platform integrating with Veeva Development Cloud across clinical, regulatory, and safety applications, targeting trial master file document intake and quality control, health authority correspondence, and safety case triage. Planned for early adopter availability in November 2026, Falcon marks the first multi-agent AI deployment across all core drug development functions within a single GxP-governed environment and serves Veeva's base of over 1,500 life sciences customers.

- April 2026: The US FDA launched a real-time clinical trial (RTCT) pilot program with AstraZeneca (Phase 2 TRAVERSE mantle cell lymphoma trial) and Amgen (Phase 1b STREAM-SCLC trial) using Paradigm Health's Study Conduct platform to deliver continuous cloud-based data feeds to FDA reviewers. A broader AI-enabled optimization pilot for early-phase trials was announced simultaneously, with selection criteria due in July and pilot participants to be selected in August 2026. This is the first formal US regulatory architecture for continuous clinical trial oversight.

- January 2026: Veeva Systems announced Veeva eSource, a direct data capture application for research sites designed to eliminate paper through EDC integration and EHR-to-EDC transfer, with early adopter availability planned for H2 2026. The product extends Veeva's clinical platform from sponsor-side systems into site-level data origination workflows, targeting a layer of the eClinical stack that has remained largely paper-dependent across most global research networks.

- August 2025: IQVIA Holdings and Veeva Systems announced a long-term global clinical and commercial partnership and the resolution of all pending legal disputes. The agreement enables sponsors to combine Veeva EDC and clinical suite with IQVIA's clinical data management, AI services, and real-world data under a unified interoperability arrangement, ending a multi-year competitive standoff that had imposed platform choice constraints on enterprise sponsors.

Global Clinical Trial Technology and Services Market Report Scope

The Clinical Trial Technology and Services Market is defined as the global industry providing digital solutions, platforms, and specialized services that enhance the efficiency, accuracy, compliance, and patient engagement in clinical trials. It covers technology solutions such as electronic data capture (EDC), decentralized trial platforms, AI-driven analytics, and services including patient recruitment, site monitoring, data management, and regulatory support.

The Clinical Trial Technology and Services Market is segmented by offering, deployment model, clinical trial phase, end user, and geography. By offering, it includes Technology Solutions such as Trial Launch Solutions, Trial Management Solutions, Data Collection and Analytics Solutions, Patient Engagement Solutions, and AI Integration Solutions, along with Services including Consulting Services, Training and Support Services, Recruitment and Retention Services, and Implementation and Integration Services. By deployment model, the market is segmented into Cloud-Based, On-Premise, and Hybrid. By clinical trial phase, it covers Phase I, Phase II, Phase III, and Phase IV. By end user, the market serves Pharmaceutical and Biotechnology Companies, Medical Device Manufacturers, Contract Research Organizations, and Healthcare Providers and Research Centers.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia‑Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of MEA), and South America (Brazil, Argentina, Rest of South America).

| Technology Solutions | Trial Launch Solutions |

| Trial Management Solutions | |

| Data Collection and Analytics Solutions | |

| Patient Engagement Solutions | |

| AI Integration Solutions | |

| Services | Consulting Services |

| Training and Support Services | |

| Recruitment and Retention Services | |

| Implementation and Integration Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Pharmaceutical and Biotechnology Companies |

| Medical Device Manufacturers |

| Contract Research Organizations |

| Healthcare Providers and Research Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Technology Solutions | Trial Launch Solutions |

| Trial Management Solutions | ||

| Data Collection and Analytics Solutions | ||

| Patient Engagement Solutions | ||

| AI Integration Solutions | ||

| Services | Consulting Services | |

| Training and Support Services | ||

| Recruitment and Retention Services | ||

| Implementation and Integration Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Clinical Trial Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Medical Device Manufacturers | ||

| Contract Research Organizations | ||

| Healthcare Providers and Research Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and forecast outlook for clinical trial technology and services?

The clinical trial technology and services market size was USD 27.40 billion in 2025, reached USD 31.24 billion in 2026, and is forecast to reach USD 63.91 billion by 2031 at a 15.39% CAGR.

Which offering leads revenue and which one is growing faster?

Technology solutions led with 63.72% revenue share in 2025, while services is growing faster with a projected 16.49% CAGR through 2031.

Why are hybrid trial operating models gaining ground?

Hybrid models are expanding because sponsors need both site based visits and remote data capture, and regulators now expect stronger controls across both settings. Hybrid deployment is projected to grow at an 18.22% CAGR through 2031.

Which trial phase is creating the strongest new demand for digital tools?

Phase III remained the largest spending phase with 52.68% share in 2025, but Phase I is growing fastest at 17.74% CAGR as regulators and sponsors focus more on early-stage efficiency, AI support, and tighter patient matching.

Which end users are shaping vendor choice most strongly?

Pharmaceutical and biotechnology companies remained the largest end users with 43.82% share in 2025, while CROs are growing fastest at 16.86% CAGR and increasingly influence platform selection for outsourced programs.

Which region offers the strongest growth opportunity through 2031?

North America remained the largest region with 41.64% share in 2025, while Asia-Pacific offers the fastest growth outlook with an 18.92% CAGR through 2031.

Page last updated on: