Preterm Birth Diagnostic Test Kits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 192.84 Million |

| Market Size (2031) | USD 287.57 Million |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

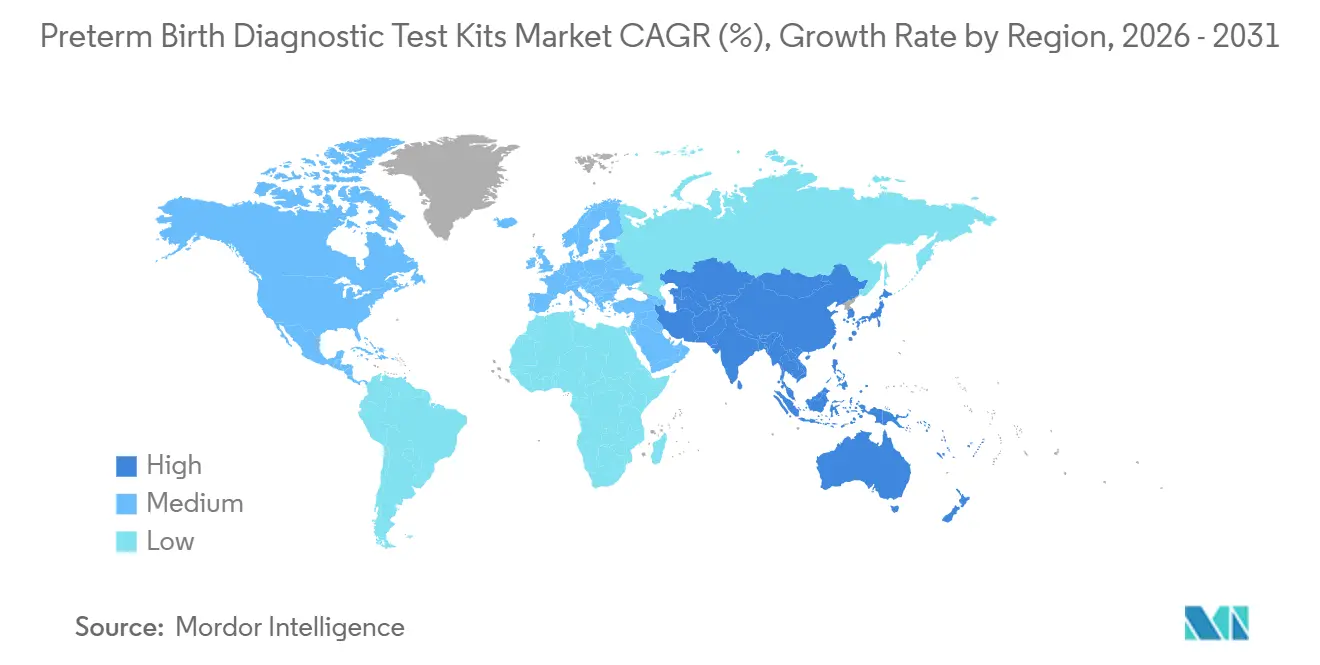

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

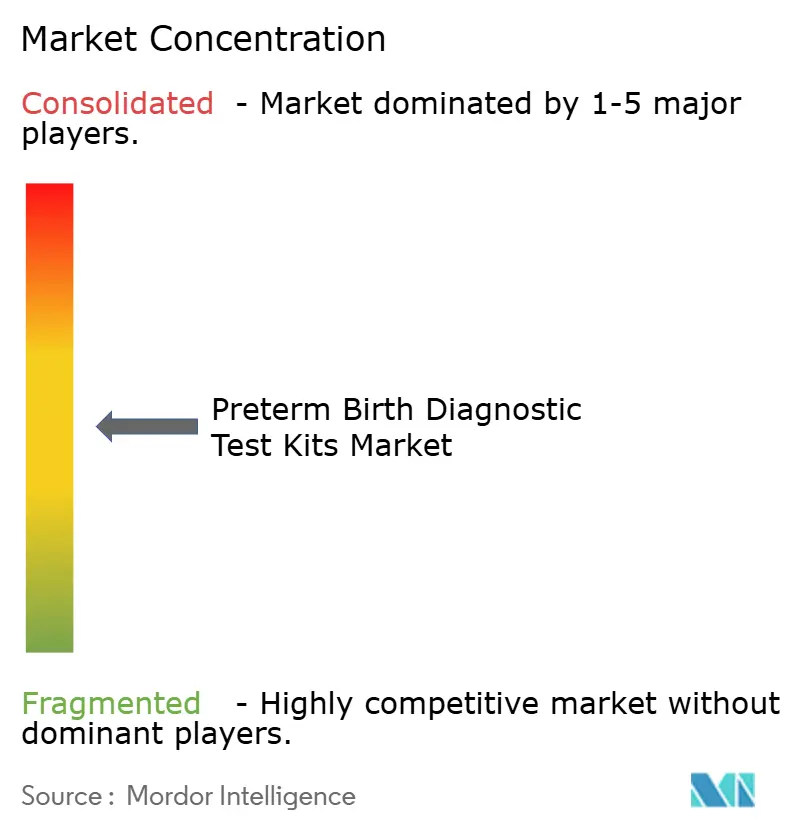

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Preterm Birth Diagnostic Test Kits Market Analysis by Mordor Intelligence

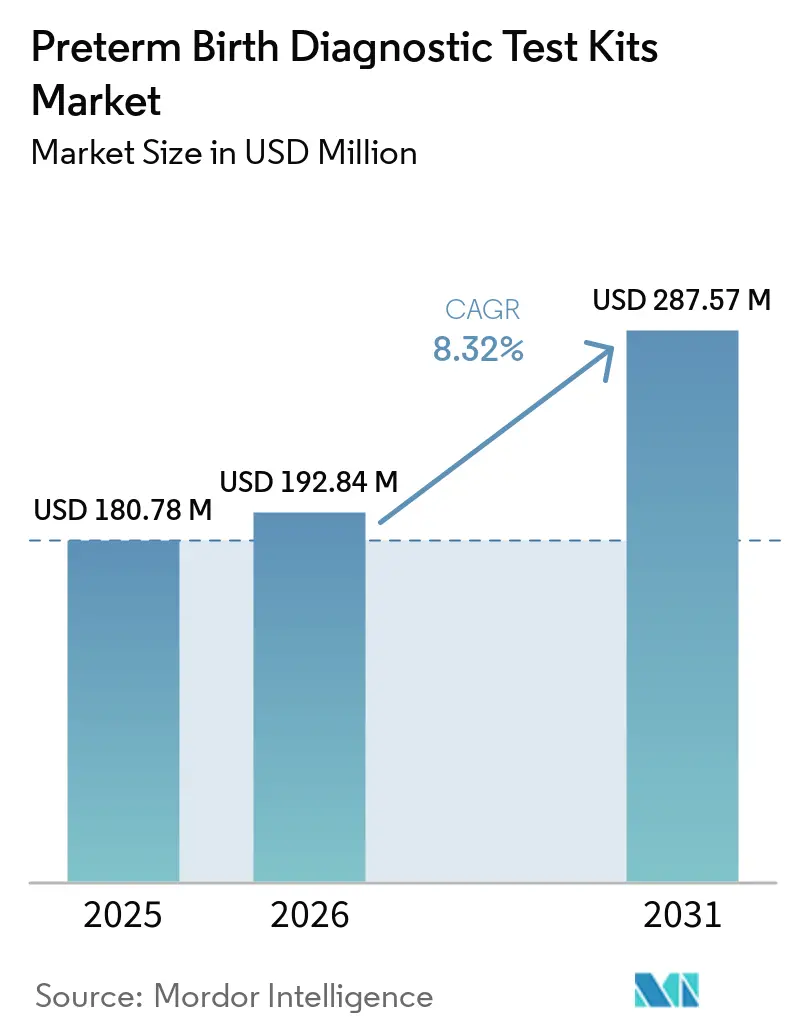

The Preterm Birth Diagnostic Test Kits Market size is projected to be USD 180.78 million in 2025, USD 192.84 million in 2026, and reach USD 287.57 million by 2031, growing at a CAGR of 8.32% from 2026 to 2031.

Growth reflects a shift from symptomatic triage to earlier risk stratification as clinical teams combine biomarker testing with cervical-length ultrasound to lower avoidable admissions and interventions. The discontinuation of quantitative fetal fibronectin cassettes disrupted entrenched hospital routines and redirected procurement to alternative biomarkers and binary rule-out platforms. PAMG-1 and IGFBP-1 swab-based tests, along with ROM diagnostics, continue to anchor rapid decisions inside labor units where minutes matter for discharge or transfer. Evidence from 2026 reinforced the value of blood-based proteomic screening, with a large randomized study showing improved outcomes when a PreTRM-based prevention strategy was applied in low-risk pregnancies. Regional dynamics favor scale and payer engagement, with North America retaining leadership by share while Asia-Pacific expands faster through laboratory buildouts and reimbursement pilots.

Key Report Takeaways

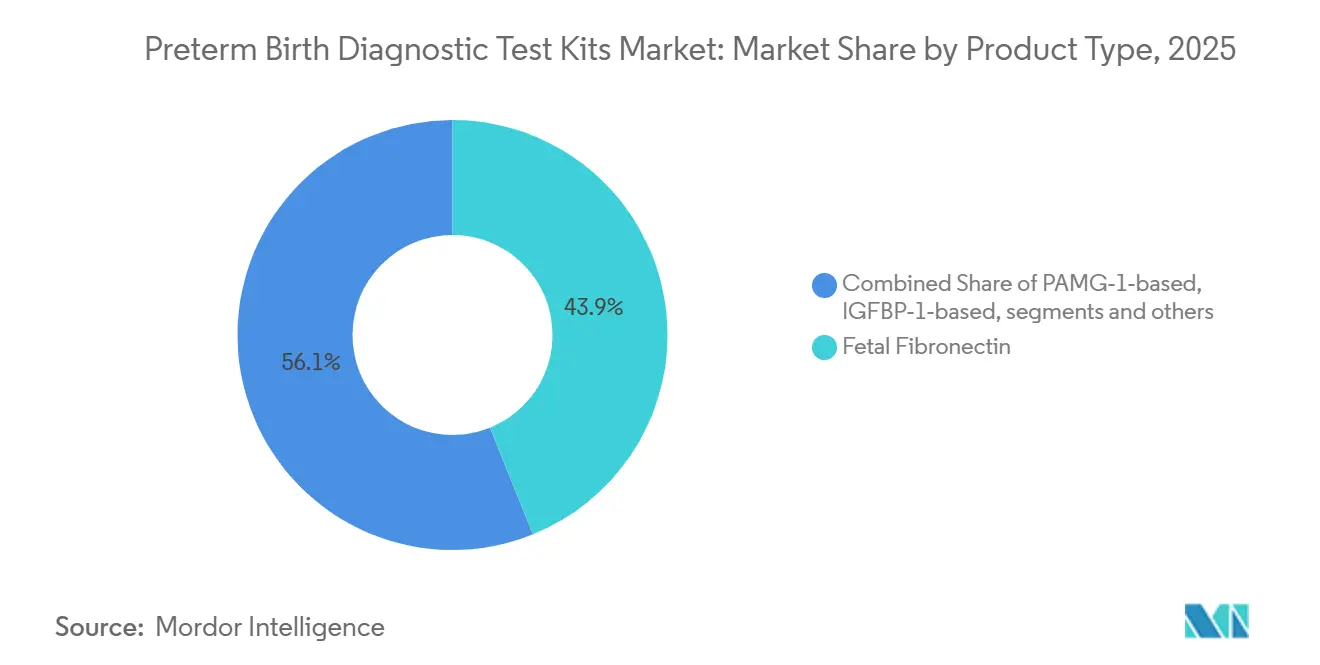

- By product type, fetal fibronectin led with 43.89% revenue share in 2025, while PAMG-1 platforms are projected to record the fastest growth at a 9.67% CAGR through 2031.

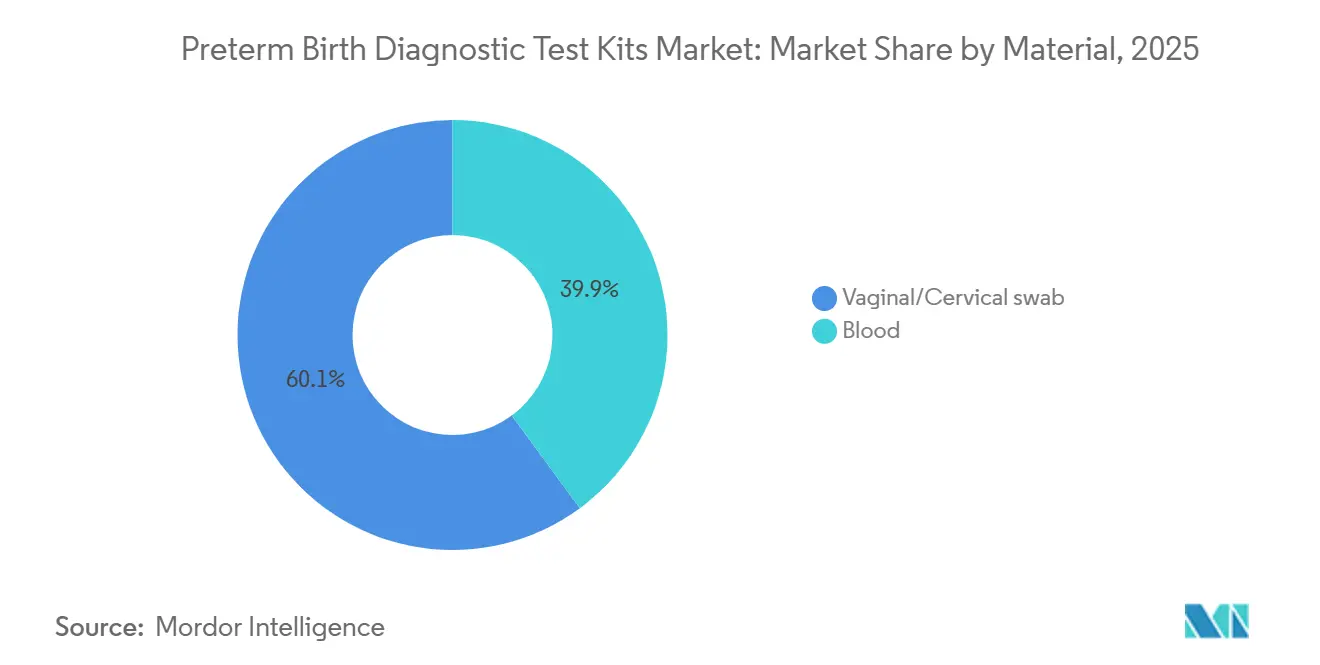

- By material, vaginal-cervical swabs accounted for 60.10% of 2025 revenue and blood-based proteomic assays are advancing at a 9.01% CAGR through 2031.

- By end user, hospitals and maternity centers held 58.56% of 2025 demand and diagnostic laboratories posted the highest projected growth at a 10.34% CAGR.

- By region, North America contributed 43.64% of 2025 revenue and Asia-Pacific is set to grow at a 9.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Preterm Birth Diagnostic Test Kits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global incidence and burden of preterm births | +2.3% | Global, with acute pressure in Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Integration of biomarker-based triage in clinical pathways (fFN, PAMG-1, IGFBP-1) | +2.8% | North America & EU core, spill-over to APAC urban hubs | Medium term (2-4 years) |

| Rapid, point-of-care lateral-flow kits enabling fast rule-out decisions in maternity triage | +1.6% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Hospital-protocol and reimbursement support for targeted testing in high-risk/symptomatic cases | +1.1% | National, with early gains in U.S. commercial & Medicaid plans, European public systems | Medium term (2-4 years) |

| Expansion of blood-based proteomic risk tests informing earlier care pathways | +0.9% | U.S. focus, pilot programs in select European markets | Long term (≥ 4 years) |

| Digital decision tools combining quantitative biomarkers with cervical length | +0.5% | APAC core (China, India, South Korea), emerging in Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Incidence and Burden of Preterm Births

Preterm birth remains a leading cause of neonatal morbidity and mortality worldwide, which sustains clinical demand for earlier and more accurate risk assessment. Hospitals seek to standardize triage to limit unnecessary transfers and to support timely corticosteroid use only when risk is credible and near term. Persistent burden in low-resource settings exposes a gap between need and access, which sustains use of simpler tests and delays adoption of advanced biomarker assays. Health systems weigh the operational value of tests that can quickly rule out imminent delivery, preventing avoidable hospital stays and reducing strain on tertiary units. These dynamics keep the preterm birth diagnostic test kits market focused on speed and clarity of result to strengthen frontline decisions.

Integration of Biomarker-Based Triage in Clinical Pathways (fFN, PAMG-1, IGFBP-1)

Many institutions in North America and Europe have integrated biomarker-based triage into standardized protocols for patients with symptoms between 24 and 34 weeks, reducing unwarranted admissions when a clear negative result is returned. The discontinuation of quantitative fetal fibronectin cassettes prompted national guidance in 2024 to transition to alternative platforms, which reshaped procurement and encouraged broader evaluation of IGFBP-1 and PAMG-1 options[1]NHS England, “Discontinuation of Hologic fetal fibronectin testing,” NHS England, england.nhs.uk. The role of ROM diagnostics persists as part of the care pathway, since membrane status directly influences near-term labor risk and clinical surveillance choices. Protocol-driven triage limits variation among clinicians and channels resources to cases with measurable risk rather than precautionary observation. Professional guidance and institutional committees continue to shape uptake, anchoring the preterm birth diagnostic test kits market to tests that deliver binary or near-binary clarity within minutes.

Rapid, Point-of-Care Lateral-Flow Kits Enabling Fast Rule-Out Decisions in Maternity Triage

Point-of-care immunoassays provide results during the same encounter, which allows teams to discharge with confidence after a negative test or escalate care when a positive result signals near-term risk. Time to result drives operational value since emergency units must often decide on transfer or steroid timing within short windows. Shelf-stable formats and straightforward workflows make lateral-flow kits a practical tool for busy labor units and for smaller centers seeking consistent practice. Where ROM testing is relevant, lateral-flow options support rapid confirmation of membrane status and reduce reliance on less precise legacy methods. Payer policies and local formularies still influence which kits are routinely used, which is why protocols and purchasing standards remain central to scaling access. The preterm birth diagnostic test kits market benefits when test menus integrate into point-of-care workflows that settle triage decisions in minutes.

Hospital-Protocol and Reimbursement Support for Targeted Testing in High-Risk/Symptomatic Cases

Coverage and internal protocols together determine how consistently tests are used in front-line obstetric care. When hospital committees codify testing ladders for symptomatic women, clinical variation falls and outcomes become easier to manage and measure. In the United Kingdom, national guidance after the fFN discontinuation illustrated how public systems can steer product selection and stabilize practice across sites. In the United States, centralized laboratory models for blood-based proteomic tests operate under CLIA and CAP oversight, which enables consistent quality at scale as payers review outcome data for broad coverage. Companies have reported payer engagement and active discussions regarding reimbursement for prevention strategies informed by proteomic risk results, which reflects momentum toward value-based arrangements. These patterns reinforce the preterm birth diagnostic test kits market focus on tests tied to clear clinical actions and measurable cost offsets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mixed/conditional guideline endorsements for some biomarkers and uses | -0.7% | Global, variability highest in Middle East, Latin America | Medium term (2-4 years) |

| Modest PPV/false positives necessitating confirmatory assessment | -0.4% | Global, operational burden concentrated in low-resource settings | Short term (≤ 2 years) |

| Operational sampling constraints (timing, co-interference) limit universal deployment | -0.3% | Sub-Saharan Africa, rural South Asia, remote Australia | Medium term (2-4 years) |

| EU IVDR elevates clinical evidence, cost, and time-to-market for IVDs | -0.8% | EU27, spill-over to countries recognizing CE mark | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mixed/Conditional Guideline Endorsements for Some Biomarkers and Uses

Guideline variability across regions slows standardized adoption and sustains a patchwork of testing practices within and across countries. Professional documents often reference biomarker classes rather than specific brands, which leaves procurement teams to decide based on price, availability, and local familiarity. Inconsistent endorsement for use cases such as asymptomatic screening contributes to uneven uptake outside tertiary centers. Clinicians also face divergent payer rules on which tests are reimbursed in specific scenarios, which adds friction to routine ordering. These factors temper the pace at which the preterm birth diagnostic test kits market can move from pilot usage to stable, protocol-driven deployment.

EU IVDR Elevates Clinical Evidence, Cost, and Time-to-Market for IVDs

European regulatory requirements have expanded evidence and post-market obligations, which raises the cost and complexity of bringing obstetric diagnostics to market. Notified body capacity and documentation demands extend timelines for updates and new claims, which can delay transitions from pilot use to wide availability. Companies with mature quality systems and earlier submissions tend to navigate reviews more predictably, while newcomers face steeper resource needs. The result is a higher bar for performance data and ongoing surveillance that can consolidate share with incumbents over time. This environment encourages vendors to prioritize test claims that align closely with clinical utility and payer value so that compliance investments translate into adoption traction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Blood Proteomics Narrows the Triage Gap

Fetal fibronectin accounted for 43.89% share of the preterm birth diagnostic test kits market size in 2025, reflecting legacy entrenchment before a supply shift changed ordering behavior. The discontinuation of quantitative fFN cassettes in 2024 replaced the quantitative standard with qualitative and alternative biomarkers within many hospital pathways. PAMG-1 platforms are projected to grow at a 9.67% CAGR through 2031 as hospitals adopt binary rule-out formats that streamline triage decisions for symptomatic women. ROM diagnostics remain a complementary pillar in the pathway because confirming membrane status substantially influences near-term risk management. The preterm birth diagnostic test kits market is also redefining timing as proteomic blood tests, led by PreTRM, focus on risk at 18 to 20 weeks with a prevention strategy built around progesterone, aspirin, and intensified care navigation[2]Sera Prognostics, “The Science Behind the PreTRM Test,” PreTRM, pretrm.com. Randomized evidence reported in 2026 showed a reduction in very early preterm births and fewer newborn complications when PreTRM screening was paired with targeted interventions. These shifts move the center of gravity upstream from crisis management at 24 to 34 weeks to earlier risk stratification that may avert high-cost episodes. Hospitals still value actionable negative predictive value to avoid transfers, while laboratories emphasize centralized workflows for complex assays. Together, these product dynamics sustain a two-speed market in which rapid swab kits support acute triage and blood proteomics expands into preventive care.

The product mix reflects clear operational trade-offs that shape buyer preferences. Point-of-care swabs that return results within minutes fit emergency and observation units that need immediate clarity for rule-out decisions. PAMG-1 and IGFBP-1 options compete on price, availability, and local guideline familiarity as procurement teams seek reliable supply after fFN disruptions. Blood-based proteomic assays require centralized processing but open a new prevention play that targets the many spontaneous preterm births that lack traditional risk flags. The preterm birth diagnostic test kits market, therefore, aligns products to clinical timing, with symptomatic triage anchored by lateral-flow kits and asymptomatic risk addressed by proteomic tests that influence care plans weeks before symptoms appear. This complementary positioning helps vendors defend against price-only competition by linking tests to outcomes and budget impact.

By Material: Vaginal Swabs Anchor Volume, Blood Assays Capture Value

Vaginal-cervical swab tests represented 60.10% of the preterm birth diagnostic test kits market share in 2025, reflecting established hospital workflows and the speed of result that these formats deliver. Swab collection aligns with protocols that prioritize patient comfort and immediate decision support for symptomatic cases. Operational realities such as sample timing and potential interference still require discipline, which underscores the importance of standardized triage pathways. Blood-based platforms are projected to expand at a 9.01% CAGR through 2031 as centralized labs use batched processing and quality controls to scale access for preventive screening windows. Sera Prognostics has highlighted ambient whole-blood logistics and centralized CLIA operations as core enablers of consistent proteomic testing at a national scale. Independent research has also reported promising second-trimester plasma protein panels for the prediction of spontaneous preterm birth, which signals further potential for blood-test innovation. These material differences map to distinct care moments and create a balanced path for growth across acute and preventive settings.

Material choice also affects throughput and data flow into care teams. Lateral-flow swabs deliver point-of-care results and support real-time discharge decisions in emergency rooms and labor triage units. Blood proteomics favor scheduled prenatal visits and centralized interpretation that returns individualized risk in days rather than minutes. As health systems combine biomarkers with cervical-length ultrasound, both materials contribute to clearer rule-in and rule-out algorithms that optimize resource use. The preterm birth diagnostic test kits market therefore accommodates a durable role for swabs while expanding the value of blood testing for earlier intervention planning.

By End User: Laboratories Outpace Hospitals on High-Complexity Workflows

Hospitals and maternity centers accounted for 58.56% of the preterm birth diagnostic test kits market share in 2025, driven by consistent use of point-of-care swabs in triage settings where speed is central. Negative results support same-day discharge and limit observation stays that are not clinically necessary. Diagnostic laboratories recorded a 10.34% CAGR to 2031 by absorbing send-out panels and blood proteomics that require centralized workflows and specialized instruments. Sera Prognostics operates a single CLIA-certified and CAP-accredited laboratory to process all PreTRM samples nationally, which allows tight performance oversight at scale. This division of labor aligns with how care is delivered, with hospitals prioritizing immediacy and labs advancing prevention and risk management.

Momentum is building for integrated models that unify point-of-care decisions with centralized analytics. Hospitals retain a strong role in symptomatic triage, while labs expand the upstream screening footprint with proteomic assessments that can trigger targeted interventions. Payers evaluating outcome data may encourage models that combine immediate triage tests with preventive strategies that lower NICU days and costs. The preterm birth diagnostic test kits market therefore reflects end-user strengths on both immediacy and longitudinal care benefits.

Geography Analysis

North America held 43.64% of 2025 revenue and anchors the preterm birth diagnostic test kits market with protocols that embed biomarker use in labor and delivery units. The 2024 discontinuation of quantitative fFN drove expedited transitions to alternative biomarkers and reinforced the weight of national guidance in shaping practice. Canada and Mexico trail U.S. adoption as procurement and coverage rules vary across provinces and payer mixes. U.S. growth now includes asymptomatic screening pilots under commercial plans and Medicaid, which nudges adoption beyond crisis triage toward prevention. The preterm birth diagnostic test kits market in North America continues to balance rapid swab usage with emerging proteomic workflows that can demonstrate measurable outcomes.

Asia-Pacific is projected to grow at a 9.45% CAGR through 2031 as laboratories scale in China, India, and South Korea and as public pilots examine coverage for newer assays. Domestic manufacturing and price-sensitive tenders influence swab adoption in public networks, while private hospital chains concentrate on PAMG-1 and IGFBP-1 in urban centers. Japan’s declining birth rate and a constrained obstetric workforce temper demand growth, yet targeted adoption persists in tertiary centers. In Australia, clinical groups monitored implications of fFN supply changes on rural transfer practices and sought consistent alternatives to preserve triage confidence. Across Southeast Asia, limited cold-chain and fragmented regulatory pathways slow uptake of novel biomarkers, which keeps the preterm birth diagnostic test kits market anchored to affordable and robust options.

Europe maintained share as institutions navigated evolving regulatory expectations and deadlines for IVD compliance. Germany, France, and the United Kingdom embed biomarker testing in maternity pathways, though budget evaluations can slow inclusion on national reimbursement schedules. The 2024 shift in the United Kingdom toward alternative triage tests after the fFN discontinuation highlighted public-sector cost sensitivity and the central role of national guidance. Southern and Eastern Europe exhibit uneven adoption due to regionalized health administration and lower per-capita spend, which sustains reliance on clinical judgment and older tests in some settings. The preterm birth diagnostic test kits market in Europe increasingly rewards vendors that can meet documentation and post-market needs without interrupting supply.

The Middle East and Africa show nascent growth with private hospitals in the Gulf importing Western biomarker platforms and tertiary centers in South Africa using diagnostics selectively. Sub-Saharan Africa bears a high preterm burden but faces infrastructure constraints that limit test usage to urban hubs. Programmatic efforts continue to target related complications such as preeclampsia, where new rapid tests under development seek to broaden access in lower-resource settings. South America’s private sectors in Brazil and Argentina support adoption in urban clinics, while public systems face budget pressures that moderate scale. These regional factors keep the preterm birth diagnostic test kits market growth tied to procurement sophistication, laboratory capacity, and payer willingness to link tests to measurable outcomes.

Competitive Landscape

The preterm birth diagnostic test kits market remains fragmented, and the 2024 fFN discontinuation redistributed share opportunities to multiple biomarker suppliers. QIAGEN leverages a ROM and preterm-labor portfolio to cross-sell within women’s health programs, which enables bundled contracting across hospital networks. Sera Prognostics advances a centralized lab model focused on preventive screening windows and payer outcomes, reinforced by 2026 randomized evidence that supports reductions in very early preterm birth and newborn complications. These strategies differentiate along timing and care setting, which lets vendors defend value despite price competition in commodity swab categories.

Strategic moves underscore evidence generation and coverage as core differentiators. Sera reported payer engagements and expansion of its commercial field presence to accelerate adoption among integrated delivery networks. In hypertensive disorders of pregnancy, Roche secured U.S. 510(k) clearance for a ratio test that informs surveillance intensity and delivery timing, which indirectly expands the addressable problem set linked to preterm birth. Such regulatory advances and clinical data help companies articulate outcome benefits beyond predictive accuracy, which matters for value-based contracts and budget-based procurement.

Cost and compliance pressures shape consolidation incentives without eliminating room for specialists. Firms with robust quality systems and multi-region regulatory experience are better positioned to navigate evolving evidence and post-market obligations, which stabilizes supply and supports price discipline. New entrants that rely on single products compete by emphasizing affordability, shelf stability, or discrete workflow advantages that solve pain points in resource-limited settings. The preterm birth diagnostic test kits market, therefore, centers on speed, regulatory agility, and outcome-linked value that together drive durable adoption.

Preterm Birth Diagnostic Test Kits Industry Leaders

BIOSYNEX S.A.

Laborie Medical Technologies (Clinical Innovations)

Medix Biochemica (Actim)

QIAGEN N.V.

Hologic, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sera Prognostics published the PRIME study in PREGNANCY, demonstrating that PreTRM blood-test screening paired with daily vaginal progesterone, low-dose aspirin, and nurse care management reduced births before 32 weeks by 56% and NICU admissions by 20% across 5,018 women enrolled at 19 U.S. sites. The randomized controlled trial met both primary outcomes and saved one NICU day for every 4.2 patients screened, providing evidence that upstream biomarker screening combined with targeted interventions improves neonatal outcomes and reduces healthcare costs.

- March 2026: Sera Prognostics reported full-year 2025 financial results and noted European commentary in The Journal of Maternal-Fetal & Neonatal Medicine supported the PreTRM test-and-treat approach as scalable for publicly funded systems. The company disclosed active payer discussions with commercial and Medicaid plans and expanded its U.S. commercial organization to target broader adoption among integrated delivery networks.

- February 2025: Roche Diagnostics received FDA 510(k) clearance for the Elecsys sFlt-1/PlGF ratio test to stratify hospitalized pregnant women with hypertensive disorders by short-term risk of developing severe preeclampsia, which may inform surveillance or earlier delivery decisions that intersect with preterm birth risk.

Global Preterm Birth Diagnostic Test Kits Market Report Scope

As per the report’s scope, pre-term birth diagnostic test kits are rapid assays, either point-of-care or laboratory-based, designed to evaluate the risk of premature delivery in pregnant women. These kits function by detecting specific biomarkers in cervicovaginal fluid or blood, enabling healthcare providers to determine if a symptomatic woman is likely to deliver within the next 7–14 days.

The pre-term birth diagnostic test kits market is segmented into product type, material, end user, and geography. By product type, the market is segmented into fetal fibronectin, PAMG‑1‑based, IGFBP‑1‑based , dual‑marker ROM tests, and blood‑based proteomic risk tests. By material, the market is segmented into vaginal/cervical swab and blood. By end user, the market is segmented into hospitals & maternity centers, diagnostic laboratories, birthing centers / outpatient OB‑GYN clinics, and others. By geography, the market is segmented as North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Fetal Fibronectin |

| PAMG‑1‑based |

| IGFBP‑1‑based |

| Dual‑marker ROM tests |

| Blood‑based proteomic risk tests |

| Vaginal/Cervical swab |

| Blood |

| Hospitals & Maternity Centers |

| Diagnostic Laboratories |

| Birthing Centers / Outpatient OB‑GYN Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Fetal Fibronectin | |

| PAMG‑1‑based | ||

| IGFBP‑1‑based | ||

| Dual‑marker ROM tests | ||

| Blood‑based proteomic risk tests | ||

| By Material | Vaginal/Cervical swab | |

| Blood | ||

| By End User | Hospitals & Maternity Centers | |

| Diagnostic Laboratories | ||

| Birthing Centers / Outpatient OB‑GYN Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the preterm birth diagnostic test kits market?

The preterm birth diagnostic test kits market size is USD 180.78 million in 2025 and is projected to reach USD 287.57 million by 2031 at an 8.32% CAGR over 2026-2031.

Which segment is growing fastest within the preterm birth diagnostic test kits market?

PAMG-1 platforms and blood-based proteomic assays are the fastest growing, with projected 9.67% and 9.01% CAGRs through 2031 respectively.

How did the fFN discontinuation affect the preterm birth diagnostic test kits market?

The 2024 discontinuation of quantitative fFN cassettes shifted procurement to alternative biomarkers and reinforced the role of hospital protocols and national guidance in product selection.

What evidence supports earlier, asymptomatic screening in this space?

In 2026, a large randomized study reported fewer very early preterm births and fewer newborn complications when a PreTRM-based prevention strategy was used in low-risk pregnancies.

Which regions lead and which are accelerating in the preterm birth diagnostic test kits market?

North America leads by revenue share in 2025, while Asia-Pacific is projected to expand fastest through 2031 as labs scale and pilots broaden access.

How does the end-user mix influence adoption patterns for preterm testing?

Hospitals dominate urgent triage with rapid swabs, while diagnostic laboratories are growing faster by scaling centralized proteomic testing and send-out panels that require specialized workflows.

Page last updated on: