United States Clinical Trials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 30.84 Billion |

| Market Size (2026) | USD 32.29 Billion |

| Market Size (2031) | USD 41.47 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Clinical Trials Market Analysis by Mordor Intelligence

The United States Clinical Trials Market size is projected to expand from USD 30.84 billion in 2025 and USD 32.29 billion in 2026 to USD 41.47 billion by 2031, registering a CAGR of 5.13% between 2026 to 2031.

Growth continues to reflect a clear shift in how sponsors run development programs, with pharmaceutical and biotechnology companies moving more execution work to external partners instead of building larger internal trial teams. That change keeps the United States clinical trials market closely tied to the strengths of the domestic system, including large patient pools, strong FDA connectivity, deep site networks, and broad late-stage trial capacity. The market is also being shaped by wider use of AI tools in study planning and patient identification, along with hybrid and decentralized trial models that help sponsors reach patients outside traditional academic centers. At the same time, the forecast still depends on how well sponsors and service providers manage recruitment delays, retention shortfalls, and rising protocol complexity, which continue to raise delivery costs and stretch study timelines. Competition remains moderate, with large integrated CROs defending scale advantages while specialized firms expand in areas such as oncology, rare disease, early-phase work, and technology-enabled execution.

Key Report Takeaways

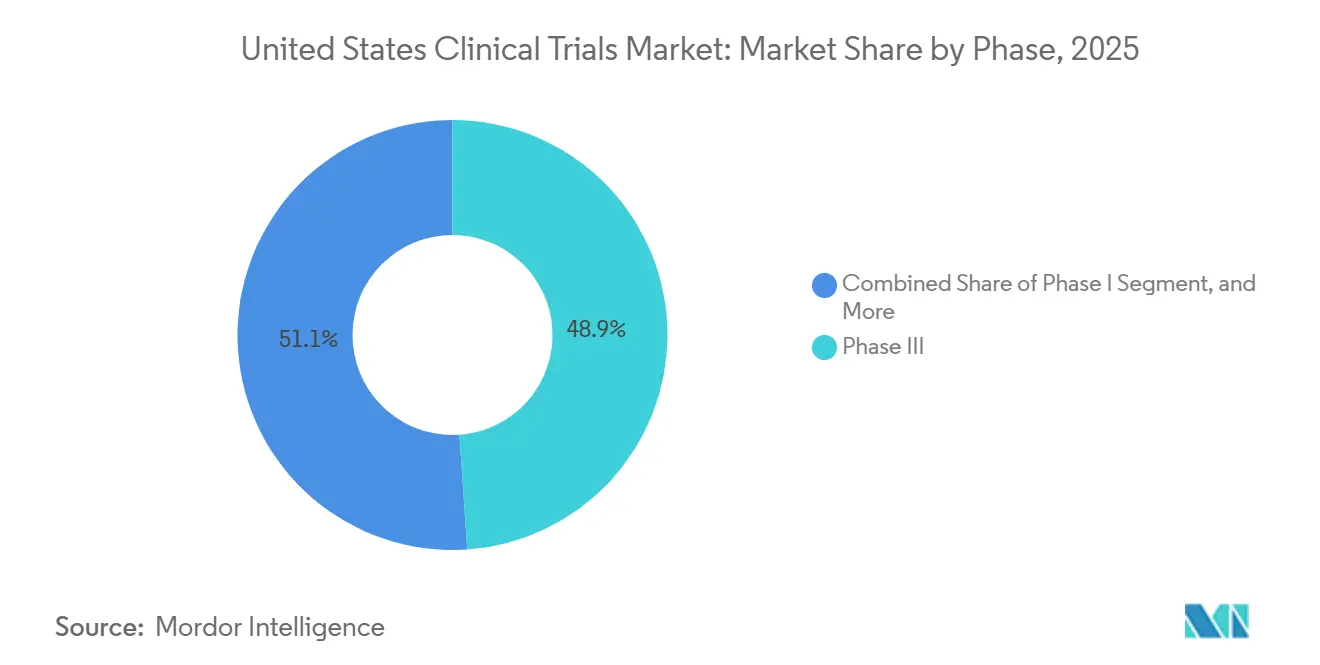

- By phase, Phase III held 48.87% of revenue in 2025, while Phase I is projected to expand at 7.36% CAGR through 2031.

- By study design, interventional studies accounted for 69.83% of the United States clinical trials market size in 2025, while expanded access is projected to grow at 7.87% CAGR through 2031.

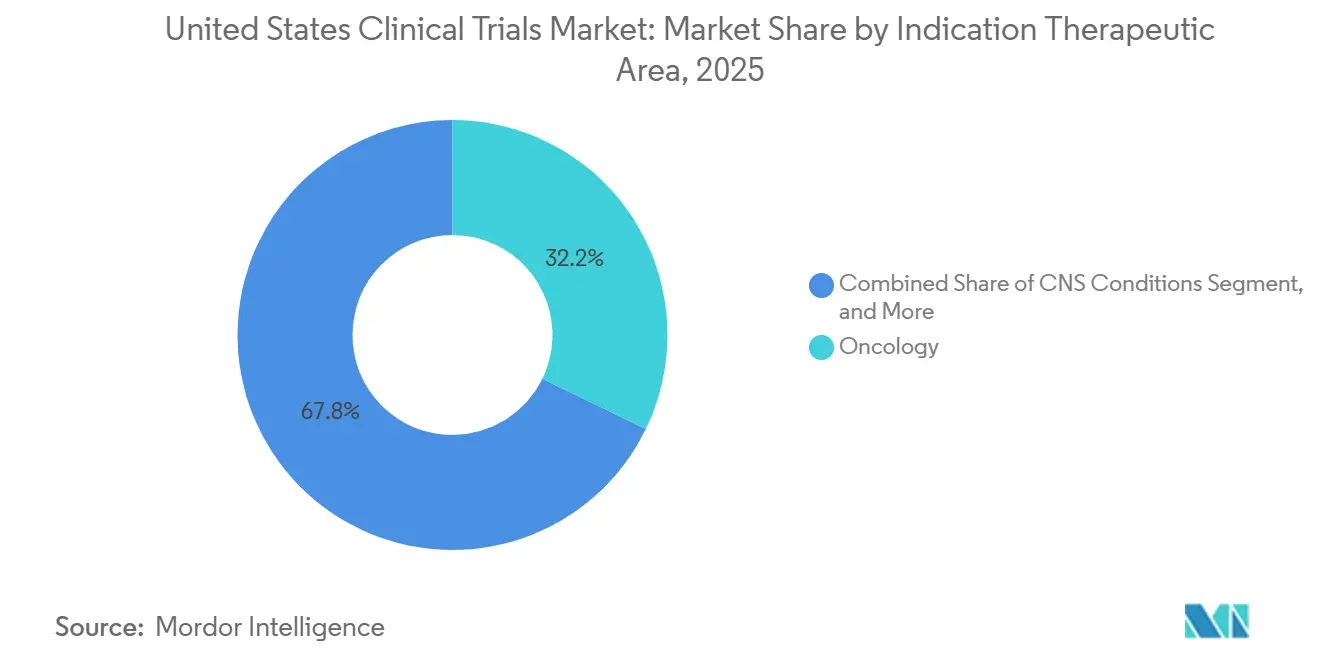

- By indication, oncology led with 32.23% revenue share in 2025, while autoimmune and inflammatory conditions are forecast to expand at 6.97% CAGR through 2031.

- By sponsor, pharmaceutical companies held 63.74% of the United States clinical trials market share in 2025, while biotechnology companies are projected to record the highest CAGR at 7.46% through 2031.

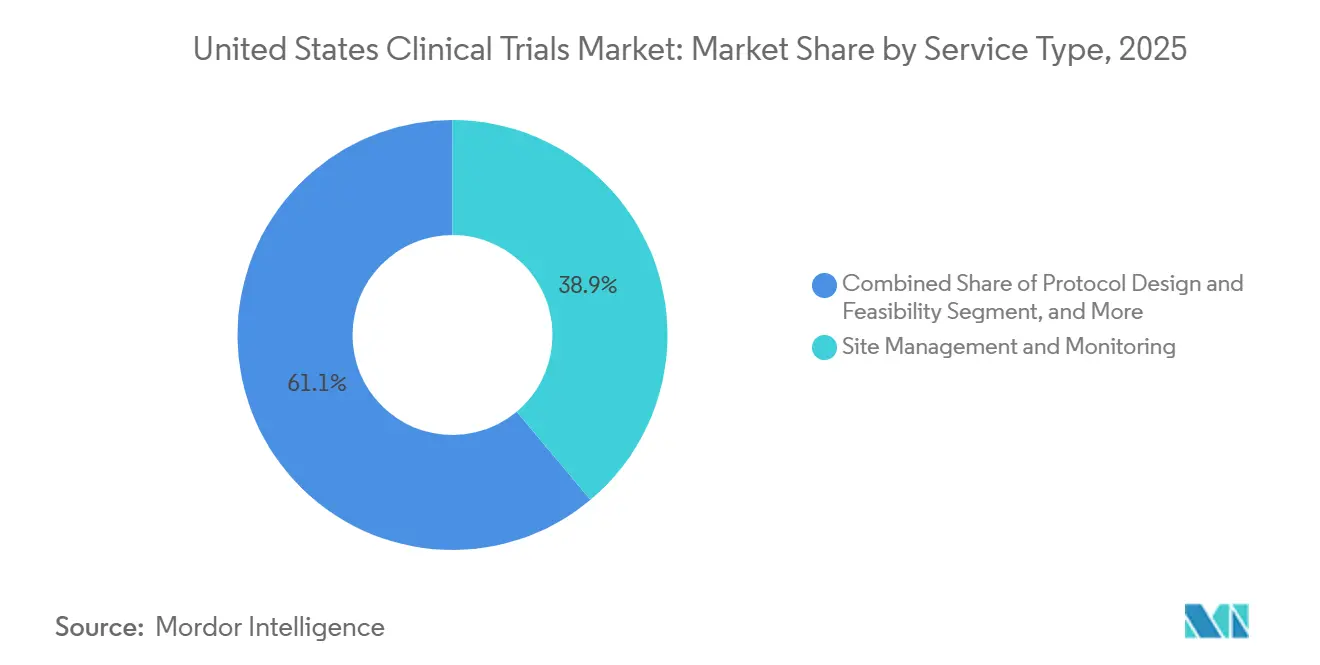

- By service type, site management and monitoring captured 38.86% of revenue in 2025, while patient recruitment and retention is forecast to advance at 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Clinical Trials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing Of Complex R&D Programs | +1.4% | Global, US dominant | Medium term (2-4 years) |

| Oncology And Rare-Disease Pipeline Expansion | +1.2% | Global | Long term (≥ 4 years) |

| AI-Enabled Trial Design And Recruitment | +0.9% | Global | Short term (≤ 2 years) |

| Hybrid And Decentralized Trial Adoption | +0.8% | US, EU spillover | Medium term (2-4 years) |

| FDA Guidance Clarity For Decentralized Elements | +0.5% | US-specific | Short term (≤ 2 years) |

| Diversity Action Plan Operationalization | +0.3% | US-specific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outsourcing Of Complex R&D Programs

The move toward outsourcing remains one of the clearest drivers of the United States clinical trials market. Sponsors are no longer sending only routine activities to outside partners, because they are also shifting regulatory work, safety support, site management, and post-approval obligations into broader service contracts. ACRO reported in March 2026 that member CROs conducted or participated in 7,634 studies involving 1.4 million patients in 2025 and supported 592 sponsor companies, which shows how much program volume is already flowing through external delivery networks.[1]Association of Clinical Research Organizations, “State of the Industry Report 2026,” ACRO, acrohealth.org This matters because a broader outsourcing scope tends to lengthen relationships and raises switching costs once a provider is embedded across several programs. It also favors companies that can combine operational scale with therapeutic depth, which is why the United States clinical trials market increasingly rewards providers that can offer integrated clinical trial services instead of isolated tasks. Smaller generalist firms still compete, but growth is becoming harder where sponsors want fewer vendors and deeper accountability across full development programs.

Oncology And Rare-Disease Pipeline Expansion

Oncology remains the largest engine of study demand in the United States clinical trials market. IQVIA reported that oncology accounted for 38% of all Phase I to III industry-sponsored trial starts in 2025, and one-third of those starts involved novel modalities such as antibody-drug conjugates, radiopharmaceutical therapeutics, chimeric antigen receptor gene therapies, and multi-specific antibodies.[2]IQVIA Institute, “Global R&D Trends 2026 Report, Advancing Innovation in a Changing Landscape,” IQVIA, iqvia.com These programs place heavier demands on site qualification, biomarker screening, cold chain handling, and long follow-up periods, which raises the need for specialized delivery teams. Rare-disease development adds another layer because patient pools are small and widely dispersed, making national outreach and flexible site coverage more important than traditional site-centric recruitment. AACR reported in 2026 that Phase I non-small cell lung cancer activity had consolidated at 223 US sites by 2024, which signals tighter access to high-performing oncology centers and reinforces the value of providers with established site relationships. As a result, the United States clinical trials market continues to favor CRO services that combine oncology scale with strong rare-disease recruitment models.

AI-Enabled Trial Design And Recruitment

AI is moving into everyday use across the United States clinical trials market rather than staying limited to pilot projects. ACRO found that 71% of member CROs used AI for study feasibility and site selection in 2025, while 64% used it for protocol optimization. That shift matters because feasibility, protocol design, and patient matching shape both study speed and study cost before enrollment even starts. A March 2026 paper in Nature Communications showed that AI-powered patient-to-trial matching systems can narrow the gap between eligible patients and enrolled cohorts, especially in orphan conditions where missed identification has been a long-standing problem. When providers combine these tools with operational delivery, they improve their chance of winning preferred-provider positions from sponsors managing broad portfolios of adaptive, basket, and biomarker-led studies. The practical effect is that the United States clinical trials market is starting to reward providers that use AI in both design and execution, not only in last-mile recruitment.

Hybrid And Decentralized Trial Adoption

Hybrid and decentralized models are becoming a normal part of how the United States clinical trials market is organized. The FDA final guidance issued in September 2024 gave sponsors and investigators a clearer framework for decentralized elements, including design, conduct, informed consent, digital health technology use, and investigator responsibilities under established compliance standards.[3]U.S. Food and Drug Administration, “Conducting Clinical Trials With Decentralized Elements, Guidance for Industry, Investigators, and Other Interested Parties,” Federal Register, govinfo.gov That clarity reduced a major compliance barrier and made it easier for sponsors to move remote and community-based elements into routine trial planning. Frontiers in Medicine reported in 2025 that decentralized community-integrated research sites achieved randomization rates comparable with traditional sites in neurodegenerative disease work, which supports the case for broader use outside emergency settings. ICON and Advarra reinforced this direction in March 2026 when they announced a connected site network built to help research-naive sites participate with common technology and oversight. FDA guidance clarity and the long-term push for broader patient representation are both helping this model gain ground, even though execution still depends on site readiness and clean data capture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recruitment And Retention Shortfalls | -0.7% | Global | Medium term (2-4 years) |

| Protocol Complexity And Cost Inflation | -0.6% | Global | Medium term (2-4 years) |

| Site Technology Overload And PI Attrition | -0.5% | US particularly | Medium term (2-4 years) |

| Diversity-Planning Policy Uncertainty | -0.3% | US-specific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Recruitment And Retention Shortfalls

Recruitment still acts as one of the main brakes on the United States clinical trials market. Frontiers in Medicine reported in 2025 that more than 80% of studies missed planned recruitment timelines, and the Association of Clinical Research Professionals reported in 2025 that 28% of sites still identified recruitment and retention as a top operating challenge. IQVIA also reported that median enrollment duration in 2025 exceeded 16 months, which shows how strongly this issue affects study delivery even in a large and mature research system. Retention is part of the same problem because losses after enrollment force sites and sponsors to over-recruit, reopen outreach, and add costs that were not planned at study start. The burden becomes even heavier when site teams are already stretched by multiple systems, staff turnover, and principal investigator shortages. For that reason, providers in the United States clinical trials market are putting more value on retention design, not just patient identification, and that is helping patient support services move closer to the core of clinical trial services.

Protocol Complexity And Cost Inflation

Protocol complexity continues to raise costs across the United States clinical trials market. Tufts Center for the Study of Drug Development data cited in 2024 showed that 76% of Phase I to IV protocols required at least one substantial amendment, and the same body of work placed median implementation cost at USD 141,000 for Phase II and USD 535,000 for Phase III protocols. The direct expense is only part of the issue, because each amendment also adds retraining, document revision, contracting work, and new room for site-level inconsistency. Advarra reported in 2026 that 45% of substantial amendments were avoidable through stronger feasibility and design work before activation, which underlines how much waste still enters studies early. At the same time, ACRP continued to highlight site pressure and investigator shortage as operating concerns in 2025, which means study teams often absorb complex revisions with limited extra capacity. This is why the United States clinical trials market is placing greater value on providers that can reduce avoidable complexity before a study opens, rather than simply managing costly changes after launch.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Phase: Late-Stage Revenue Still Leads While Early-Phase Growth Accelerates

Phase III held 48.87% of phase revenue in 2025, which kept it as the largest phase segment in the United States clinical trials market. Large oncology, cardiovascular, and neurology programs supported that position because they required broad site networks, central lab coordination, and long monitoring cycles. The segment also benefited from resumed late-stage activity that had been deferred earlier, which raised contract value as more studies moved back into active enrollment windows. In practical terms, Phase III remains the part of the United States clinical trials market where sponsor budgets, monitoring effort, and operational complexity come together most clearly. That is why providers with strong site oversight and national delivery footprints still capture much of the largest contract pool.

Phase I is projected to expand at 7.36% CAGR through 2031, making it the fastest-growing phase in the United States clinical trials market. IQVIA reported that emerging biopharma companies generated 68% of all global Phase I starts in 2025, which supports the view that first-in-human activity is rising among sponsors that rely heavily on external partners. This pattern supports demand for CRO services because many of these sponsors do not maintain in-house units for healthy-volunteer work, dose escalation, or intensive safety management. It also supports clinical trial services that combine early-phase unit capacity with flexible outpatient access and tighter data turnaround. ICON reflected this direction in May 2026 by opening a new Clinical Research Unit in San Antonio and adding satellite outpatient clinics in Houston and Lawrence, which expanded early-phase capacity in the United States.

By Study Design: Interventional Studies Dominate While Expanded Access Gains Importance

Interventional studies accounted for 69.83% of study design revenue in 2025 and therefore represented the largest share of the United States clinical trials market size within this segment. Their lead reflects the volume of randomized controlled work across oncology, immunology, and cardiovascular disease, where direct sponsor oversight and service intensity remain high. These studies generate heavier operational needs because they require active treatment assignment, site monitoring, endpoint collection, and protocol compliance across many settings. That structure keeps interventional work central to the United States clinical trials market even as more complementary evidence models develop. Observational programs remain important, but they usually create a different revenue profile because they are more closely linked to post-approval evidence, payer support, and real-world study design.

Expanded access is forecast to grow at 7.87% CAGR through 2031, which makes it the fastest-rising study design category in the United States clinical trials market. FDA guidance published in November 2025 continued to support public access pathways for investigational drugs used outside formal trial enrollment, which helps explain why this category is gaining more attention from sponsors. The segment also creates a more specialized operating need because adverse event reporting and oversight must run alongside the main development program without blurring responsibilities. That requirement opens room for providers that can coordinate safety, medical writing, and regulatory support within the same workflow. As a result, the United States clinical trials market is seeing more value placed on service providers that can handle expanded access execution with the same discipline applied to formal registration programs.

By Indication/Therapeutic Area: Oncology Leads the Revenue Base While Autoimmune Programs Expand Faster

Oncology captured 32.23% of indication revenue in 2025 and remained the largest therapeutic segment in the United States clinical trials market. IQVIA reported that oncology represented 38% of Phase I to III industry-sponsored trial starts in 2025, while ACRO showed that oncology made up 27% of member CRO study mix by count. That scale reflects both the depth of the cancer pipeline and the heavy service intensity attached to biomarker-led studies, novel modalities, and large late-stage programs. BioNTech added to that picture in May 2026 when it highlighted 13 ongoing pivotal trials across solid tumor indications, which points to sustained demand for complex oncology execution. Within the US clinical trials market, oncology remains the segment where provider experience, site access, and logistics depth are most visible to sponsors.

Autoimmune and inflammatory conditions are projected to grow at 6.97% CAGR through 2031, making them the fastest-growing therapeutic cluster in the United States clinical trials market. Growth here reflects a broader wave of targeted biologics and cell-based approaches moving into diseases such as lupus, rheumatoid arthritis, myositis, and multiple sclerosis, where study design and long follow-up remain demanding. Roche reinforced this momentum in April 2026 when its Phase III FENhance 1 and 2 studies met primary endpoints and showed fenebrutinib superiority over teriflunomide in relapsing multiple sclerosis. CNS, cardiovascular, and diabetes studies still provide an important revenue base, especially where confirmatory work and post-approval follow-up continue beyond registration. Even so, autoimmune growth is meaningful because it widens the demand base for providers beyond oncology and brings more specialized clinical trial services into the next phase of portfolio expansion.

By Sponsor: Pharmaceutical Companies Hold the Largest Share While Biotechnology Sponsors Grow Faster

Pharmaceutical companies held 63.74% of sponsor revenue in 2025 and therefore accounted for the largest sponsor base in the US clinical trials market share. Their lead reflects the large contract values attached to multi-regional Phase III programs, confirmatory studies, and long post-approval commitments in areas such as oncology and cardiovascular disease. Large pharmaceutical sponsors also keep an advantage because preferred-provider relationships give them steadier access to site networks, regulatory support, central lab capacity, and specialist delivery teams during busy enrollment periods. This makes the sponsor mix in the United States clinical trials market less about the number of sponsors and more about the size and complexity of the work that each sponsor group places with external providers. Medical device, academic, government, and nonprofit sponsors remain relevant, but they represent smaller and more distinct revenue pools with different timelines and contracting patterns.

Biotechnology companies are projected to expand at 7.46% CAGR through 2031, which makes them the fastest-growing sponsor segment in the US clinical trials market. IQVIA reported that emerging biopharma companies drove 68% of all Phase I trial starts in 2025, and that supports the view that early pipeline activity is shifting toward asset-light companies with limited internal infrastructure. This trend supports both CRO services and flexible clinical trial services because smaller sponsors often need outside partners for design, activation, recruitment, safety, and regulatory work at the same time. The opportunity is strong, but the operating model is different because providers must manage more sponsor relationships with smaller average contract values. That is why the US clinical trials market is increasingly split between large, high-value pharmaceutical programs and a faster-moving biotechnology pipeline that depends heavily on outside execution.

By Service Type: Monitoring Holds the Largest Base While Recruitment Services Expand Faster

Site management and monitoring accounted for 38.86% of service-type revenue in 2025, which made it the largest service segment in the United States clinical trials market. That lead reflects the demands of multi-site oncology and neurology studies, where monitoring intensity, query resolution, site contact, and compliance checks remain core delivery functions. Phase III volume also supports the segment because larger patient populations and broader endpoint structures raise visit frequency and oversight requirements. For many sponsors, this part of the US clinical trials market still defines the baseline value of outsourced execution because it connects protocol requirements to day-to-day study control. The segment remains difficult to displace even as more digital tools enter study management.

Patient recruitment and retention is projected to grow at 7.08% CAGR through 2031 and stands out as the fastest-growing service category in the United States clinical trials market. The growth rate reflects sponsor recognition that enrollment failure and patient loss are among the most common causes of delay, which makes dedicated support less optional than before. Protocol design and feasibility are also becoming more valuable because sponsors want to reduce avoidable amendments before a study opens, and Advarra reported in 2026 that 45% of substantial amendments were avoidable through better early planning. Pharmacovigilance is gaining attention as well, highlighted by Parexel's April 2026 acquisition of Vitrana to strengthen AI-enabled patient safety capabilities across the life cycle. Taken together, these shifts show that the US clinical trials market is slowly moving from a monitoring-heavy mix toward a broader service balance where recruitment, design, data, and safety carry more weight.

Geography Analysis

California leads the United States in active recruiting trial volume in 2026 with 1,246 trials, out of 7,755 active studies nationwide. New York, Massachusetts, Pennsylvania, and Maryland form the second major cluster with 758, 639, 606, and 537 active recruiting trials, which confirms that the United States clinical trials market remains concentrated around established coastal research corridors. This pattern reflects the density of academic hospitals, sponsor offices, FDA proximity in Maryland, and long-developed site networks. It also means patient access remains uneven, which matters as sponsors place more value on broader representation and wider geographic coverage in the US clinical trials market.

Texas and Florida stand out in the South with 818 and 857 active recruiting trials in 2026. Their position is supported by large urban populations, broad hospital systems, and rising interest in early-phase and community-linked site capacity. ICON added to this shift in May 2026 by opening a new San Antonio clinical research unit and launching satellite clinics in Houston and Lawrence. AACR reported in 2026 that Phase I non-small cell lung cancer activity had consolidated at 223 US sites by 2024, which shows why sponsors and providers are investing in new first-in-human access points outside the traditional coastal core. As site access tightens, broader state coverage is becoming a competitive advantage in the United States clinical trials market.

Ohio, Illinois, and Minnesota remain important Midwestern hubs because they combine strong academic infrastructure with more manageable activation timelines for Phase II and investigator-led work. The next shift is the spread of community-integrated research sites around large metro clinical research units, which can widen patient catchment without fully duplicating urban infrastructure. Frontiers in Medicine found in 2025 that decentralized community-integrated sites delivered randomization rates comparable with traditional models in neurodegenerative disease trials, which supports further expansion into suburban and semi-rural settings. States across the Dakotas, Wyoming, and other low-density areas still remain underserved, but FDA-compliant remote visit models are widening the future footprint of the United States clinical trials market.

Competitive Landscape

The United States clinical trials market remains moderately concentrated, with a small group of large full-service CROs setting the pace on scale, data depth, and geographic reach. IQVIA, Thermo Fisher Scientific's PPD clinical research business, Parexel, and ICON compete most directly where sponsors want broad service coverage across development stages. These firms benefit from long-standing sponsor relationships, established site networks, and the ability to combine analytics, operations, and regulatory support in the same account structure. At the same time, specialist operators continue to win work in oncology, rare disease, and early-phase programs where therapeutic focus matters as much as size. This mix keeps the United States clinical trials market competitive and limits the likelihood of one vendor dominating the field.

Leading companies are expanding their role across the development chain rather than protecting only their current service lines. IQVIA agreed in February 2026 to acquire selected Charles River Laboratories drug discovery assets, a move that extends its reach upstream into earlier sponsor decision points. Parexel added Vitrana in April 2026 to strengthen AI-enabled pharmacovigilance and patient safety capabilities across the life cycle. Thermo Fisher's PPD clinical research business also deepened its data offering through a 2026 collaboration with HealthVerity covering claims, EMR, laboratory, and specialty data for feasibility, site selection, and evidence generation.

Mid-sized firms are responding with focused technology and faster delivery rather than trying to match every large-CRO capability. Veristat launched InStat in May 2026 to shorten submission-ready tables, listings, and figures from weeks to days, which shows how automation can narrow execution gaps in specialized work. ICON and Advarra also partnered in March 2026 to build a connected site network that can help research-naive sites enter more complex studies with shared technology and oversight. Governance remains a watchpoint after ICON disclosed in April 2026 that an Audit Committee investigation found overstated revenue in prior reporting periods, a development that may affect sponsor confidence even though the broader United States clinical trials market still shows balanced competition.

United States Clinical Trials Industry Leaders

ICON plc

Celerion

IQVIA

Labcorp Drug Development

Syneos Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ICON plc opened a new, state-of-the-art Clinical Research Unit in San Antonio, Texas, and launched satellite outpatient clinics in Houston, Texas and Lawrence, Kansas, significantly expanding early-phase and Phase I capacity in the south-central United States and broadening geographic access for healthy-volunteer and patient cohort studies.

- May 2026: Veristat launched InStat, the clinical research industry's first fully automated, zero-code biostatistics solution, reducing submission-ready tables, listings, and figures generation from 4–6 weeks to days; the platform was used for the first time in NfL biomarker analyses supporting Clene Nanomedicine's planned 2026 NDA for CNM-Au8.

- April 2026: Parexel acquired Vitrana, a provider of an AI-enabled end-to-end pharmacovigilance technology platform, completing Parexel's AI-enabled service suite from regulatory submissions through trial execution and post-approval safety monitoring; Vitrana will initially operate as "Vitrana – a Parexel Company" during integration.

- April 2026: Thermo Fisher Scientific's PPD clinical research business announced a strategic collaboration with HealthVerity to integrate access to longitudinal claims, EMR, laboratory, and specialty data for trial feasibility, site selection, and real-world evidence generation across PPD's global study portfolio.

United States Clinical Trials Market Report Scope

The clinical trials market encompasses the global industry of outsourced research services used to test, evaluate, and bring new medical interventions (drugs, devices, and therapies) to market. It consists of specialized service providers like Clinical Research Organizations (CROs) that manage study design, patient recruitment, data collection, and regulatory submissions for pharmaceutical, biotechnology, and medical device sponsors.

The United States Clinical Trials Market, valued in USD, is segmented across multiple dimensions to capture its breadth and complexity. By phase, trials are categorized into Phase I through Phase IV, reflecting the progression from early safety testing to post‑marketing studies. In terms of study design, the market encompasses interventional trials, observational studies, and expanded access programs. By indication, clinical activity spans oncology, central nervous system (CNS) disorders, autoimmune diseases, cardiovascular conditions, diabetes, obesity, pain management, infectious diseases, and rare diseases. The sponsor landscape includes pharmaceutical companies, biotechnology firms, medical device manufacturers, academic institutions, and government agencies. Finally, by service type, the market covers protocol design, site management, patient recruitment, central laboratory services, data management, medical writing, and pharmacovigilance.

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Interventional |

| Observational |

| Expanded Access |

| Oncology | Blood Cancers |

| Solid Tumors | |

| CNS Conditions | Epilepsy |

| Parkinson’s Disease | |

| Stroke | |

| Traumatic Brain Injury | |

| Amyotrophic Lateral Sclerosis | |

| Autoimmune / Inflammation | Rheumatoid Arthritis |

| Multiple Sclerosis | |

| Osteoarthritis | |

| Irritable Bowel Syndrome | |

| Cardiovascular Diseases | |

| Diabetes | |

| Obesity | |

| Pain Management | |

| Infectious Diseases | |

| Rare Diseases and Orphan Conditions |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Medical Device Companies |

| Academic Medical Centers |

| Government and Nonprofit Research Organizations |

| Protocol Design and Feasibility |

| Site Identification and Activation |

| Site Management and Monitoring |

| Patient Recruitment and Retention |

| Central Laboratory and Bioanalytical Testing |

| Clinical Data Management and Biostatistics |

| Medical Writing and Regulatory Affairs |

| Pharmacovigilance and Safety |

| By Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By Study Design | Interventional | |

| Observational | ||

| Expanded Access | ||

| By Indication / Therapeutic Area | Oncology | Blood Cancers |

| Solid Tumors | ||

| CNS Conditions | Epilepsy | |

| Parkinson’s Disease | ||

| Stroke | ||

| Traumatic Brain Injury | ||

| Amyotrophic Lateral Sclerosis | ||

| Autoimmune / Inflammation | Rheumatoid Arthritis | |

| Multiple Sclerosis | ||

| Osteoarthritis | ||

| Irritable Bowel Syndrome | ||

| Cardiovascular Diseases | ||

| Diabetes | ||

| Obesity | ||

| Pain Management | ||

| Infectious Diseases | ||

| Rare Diseases and Orphan Conditions | ||

| By Sponsor | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Medical Device Companies | ||

| Academic Medical Centers | ||

| Government and Nonprofit Research Organizations | ||

| By Service Type | Protocol Design and Feasibility | |

| Site Identification and Activation | ||

| Site Management and Monitoring | ||

| Patient Recruitment and Retention | ||

| Central Laboratory and Bioanalytical Testing | ||

| Clinical Data Management and Biostatistics | ||

| Medical Writing and Regulatory Affairs | ||

| Pharmacovigilance and Safety | ||

Key Questions Answered in the Report

How large is the United States clinical trials market in 2026?

The United States clinical trials market is estimated at USD 32.29 billion in 2026 and is forecast to reach USD 41.47 billion by 2031 at a 5.13% CAGR.

Which phase generates the most revenue in United States clinical research services?

Phase III leads with 48.87% of revenue in 2025 because late-stage studies require larger site networks, longer monitoring cycles, and heavier operational oversight.

What is the fastest-growing part of the United States clinical trials market by study design?

Expanded access is the fastest-growing study design segment, with a projected 7.87% CAGR through 2031, supported by FDA guidance and growing sponsor interest in access pathways.

Why does oncology remain the largest therapeutic area for United States clinical trials?

Oncology held 32.23% of indication revenue in 2025, supported by high trial volume, novel treatment modalities, biomarker-led study designs, and large late-stage programs.

How important are biotechnology companies to future trial demand in the United States?

Biotechnology companies are expected to grow at 7.46% CAGR through 2031, and emerging biopharma drove 68% of all Phase I trial starts in 2025, which keeps outside execution demand high.

Page last updated on: