Pediatric Clinical Trials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.03 Billion |

| Market Size (2031) | USD 26.89 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

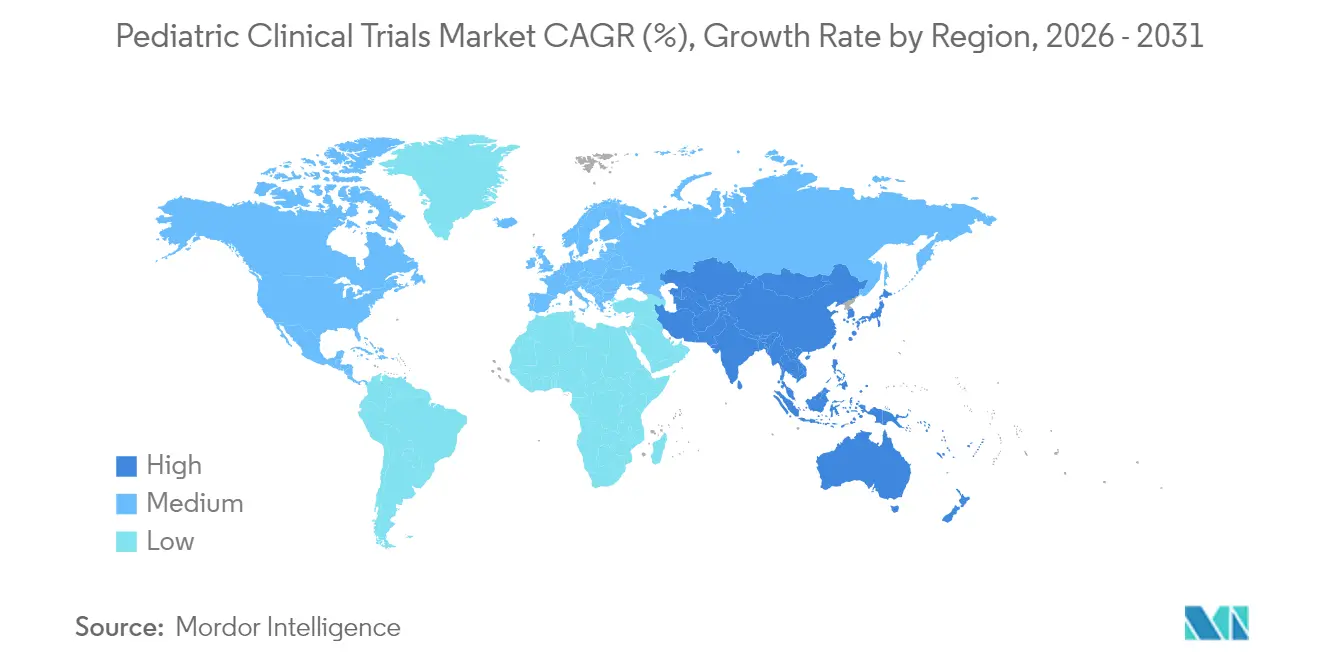

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

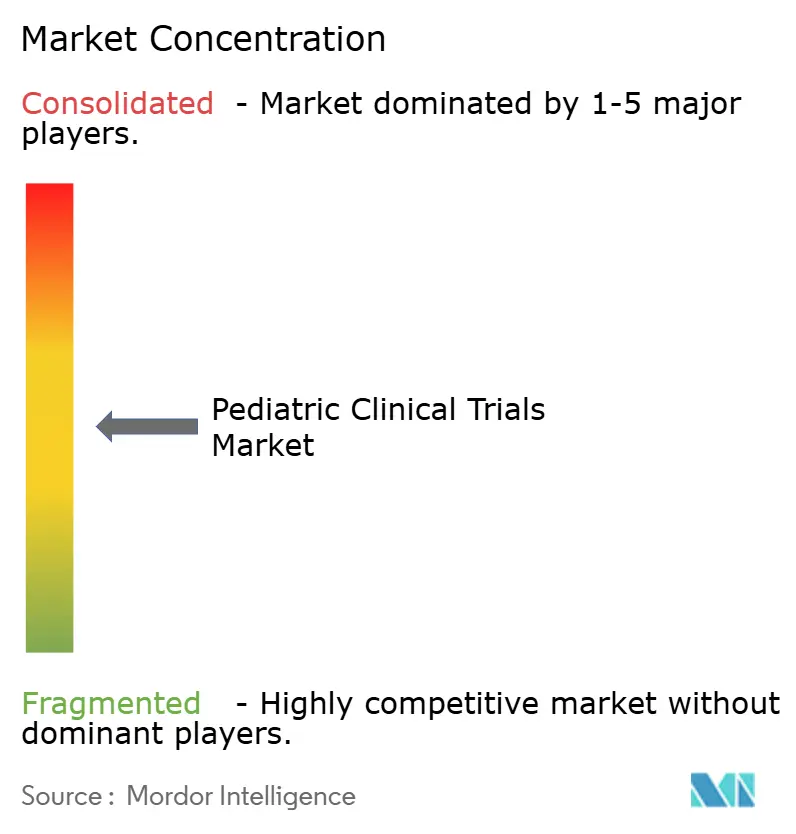

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pediatric Clinical Trials Market Analysis by Mordor Intelligence

The pediatric clinical trials market size was valued at USD 20.02 billion in 2025 and estimated to grow from USD 21.03 billion in 2026 to reach USD 26.89 billion by 2031, at a CAGR of 5.03% during the forecast period (2026-2031). Strong regulatory incentives, notably the US Pediatric Research Equity Act (PREA) and the EU Paediatric Regulation, keep trial volumes rising as every new molecular entity targeting children must present age-appropriate evidence. Mandatory early evaluation of oncology drugs under the RACE for Children Act sustains a high share of cancer-focused protocols. Parallel trends—including rising chronic disease prevalence among children, the shift toward decentralized and AI-enabled study designs, and deeper outsourcing to pediatric-specialist contract research organizations (CROs)—are expanding both the scope and geographic reach of the pediatric clinical trials market. North America remains the largest regional hub, but Asia-Pacific is accelerating fastest as regulators in South Korea, Taiwan, and Australia streamline review pathways and introduce fiscal incentives for sponsors.

Key Report Takeaways

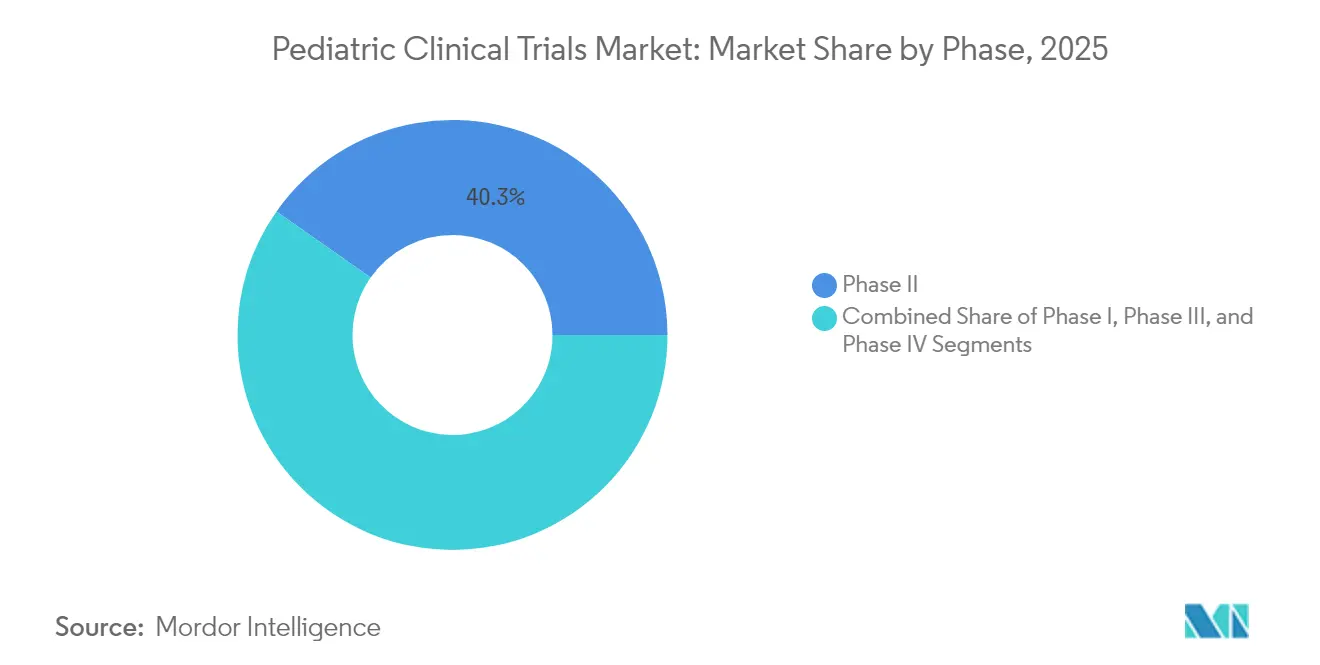

- By phase, Phase II accounted for 40.26% of pediatric clinical trials market share in 2025, while Phase I is projected to expand at a 6.96% CAGR through 2031.

- By study design, interventional drug studies held 64.93% share of the pediatric clinical trials market size in 2025, whereas observational cross-sectional studies will advance at a 7.44% CAGR to 2031.

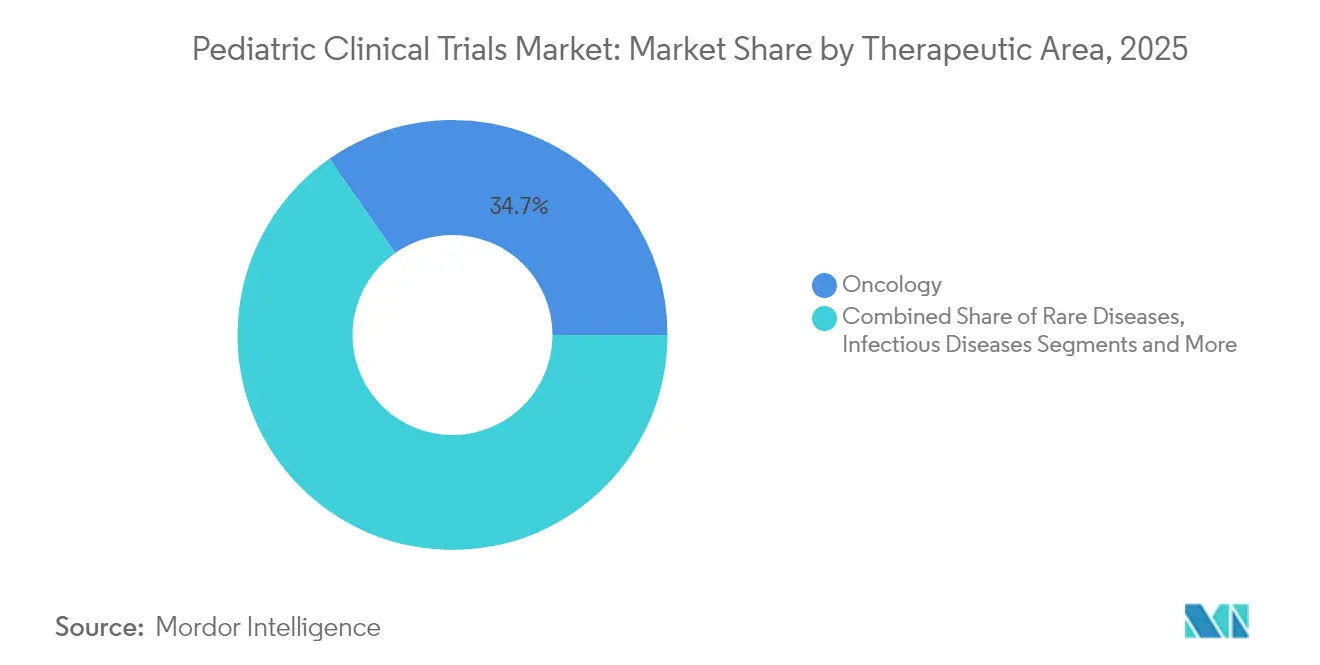

- By therapeutic area, oncology captured 34.71% of pediatric clinical trials market share in 2025, and rare diseases are forecast to grow at an 8.26% CAGR over the same horizon.

- By sponsor type, pharmaceutical and biopharmaceutical companies represented 48.72% of pediatric clinical trials market size in 2025; government and academic institutions show the highest CAGR at 8.15% through 2031.

- By geography, North America led with 39.02% market share in 2025, whereas Asia-Pacific is expected to register a 7.18% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pediatric Clinical Trials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory incentives (US PREA, EU Paediatric Regulation) | +1.8% | Global, strongest in North America & EU | Long term (≥ 4 years) |

| Rising prevalence of chronic pediatric diseases | +1.2% | Global, higher burden in developed markets | Medium term (2-4 years) |

| Outsourcing surge to pediatric-specialist CROs | +0.9% | Global, led by North America, expanding to APAC | Medium term (2-4 years) |

| Decentralized/virtual trial adoption for children | +0.7% | North America & EU early adoption, APAC following | Short term (≤ 2 years) |

| AI-driven adaptive designs cutting sample size | +0.5% | North America & EU leading, selective APAC adoption | Medium term (2-4 years) |

| RACE for Children Act-led oncology trial boom | +0.4% | US-focused with global spillover effects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Incentives (US PREA, EU Paediatric Regulation)

Long-standing mandates have reshaped drug-development economics by requiring Pediatric Investigation Plans in Europe and pediatric study plans under PREA in the United States. Convergence continues with the FDA’s 2024 acceptance of ICH E11A extrapolation guidelines, enabling streamlined dose-finding that leverages adult data where scientifically justified[1]WCG Clinical, “The FDA Accepts ICH E11A on Pediatric Extrapolation,” wcgclinical.com. These policies reduce sequential adult-to-child timelines, lifting demand for specialized pediatric protocols, and the 2025 Innovation in Pediatric Drugs Act proposes stronger enforcement, signaling durable growth.

Rising Prevalence of Chronic Pediatric Diseases

US survey data show persistent increases in asthma and mental-health diagnoses among youth, directly expanding the therapeutic pipeline for pediatric respiratory, endocrine, and neurological agents. Asthma alone continues to impose disparate burdens on non-Hispanic Black children, highlighting equity gaps that prospective studies are beginning to address. The earlier onset and longer treatment windows typical of chronic childhood diseases amplify the requirement for child-friendly formulations and robust long-term safety datasets, prompts that collectively boost the pediatric clinical trials market.

Outsourcing Surge to Pediatric-Specialist CROs

Trial complexity is motivating sponsors to partner with CROs that field board-certified pediatricians and family-centric recruitment teams. IQVIA has already completed 359 pediatric studies across 101 countries, enrolling 221,000 children. ICON manages 399 pediatric trials spanning 117,000 participants and 16,630 sites. Such specialization supports age-appropriate pharmacokinetics, decentralized consent workflows, and innovative dosing strategies—capabilities now recognized as essential in the pediatric clinical trials market.

Decentralized/Virtual Trial Adoption for Children

Hybrid and fully decentralized models are overcoming distance, time, and school-schedule barriers that deter families from participation. The FDA’s 2024 guidance explicitly endorses remote data capture to broaden access for underrepresented pediatric populations. ICON reports a 10% recruitment lift in pediatric studies that incorporate electronic patient-reported outcomes, with 90% of enrolled families preferring travel times under one hour when occasional on-site visits remain necessary.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethical complexities & informed-consent hurdles | -0.8% | Global, stricter in EU & developed markets | Long term (≥ 4 years) |

| Limited recruitable patient pools | -1.1% | Global, pronounced in rare diseases | Medium term (2-4 years) |

| Scarcity of child-friendly drug formulations | -0.6% | Global, variable by region | Medium term (2-4 years) |

| Post-pandemic site staffing shortages | -0.9% | North America & EU, selective APAC impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ethical Complexities & Informed-Consent Hurdles

Dual requirements for parental permission and age-appropriate assent introduce added administrative layers that can delay study start-up and drive costs. A multicenter Canadian survey found wide divergence in feasibility perceptions for obtaining assent within 48 hours of PICU admission. International trials face further institutional review board variation; the PARITY orthopedic oncology study secured approvals from only 46 of 91 interested sites due to resource constraints. Harmonized consent templates and electronic documentation are gradually easing this burden but will remain a headwind for the pediatric clinical trials market.

Limited Recruitable Patient Pools

Systematic reviews show that merely 10% of eligible children enroll in trials, with socioeconomic status, language, and prior therapy heavily influencing participation. Children with rare diseases pose an even greater challenge as prevalence per indication often falls below 2 per 100,000. Efforts such as telehealth-enabled screening and community-based satellite sites are improving reach, yet recruitment remains the most significant brake on pediatric clinical trials market size expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Phase: Early-Stage Trials Drive Innovation Pipeline

Phase II maintained the largest slice of the pediatric clinical trials market size at 40.26% in 2025 as sponsors used proof-of-concept readouts to fine-tune age-appropriate dosing and accrual strategies. Phase I trials, spurred by the RACE Act and ICH E11A framework, are projected to deliver a 6.96% CAGR by 2031 as sponsors move earlier to test mechanism-based therapies in children. Adaptive, model-based escalation designs minimize exposure while accelerating go/no-go decisions—a practice now standard in oncology and rare metabolic disorders.

Phase III programs remain pivotal for labeling, yet heightened reliance on extrapolation data permits smaller randomized cohorts. As a result, Phase III’s proportional pediatric clinical trials market share could erode marginally even though absolute study counts rise. Post-marketing Phase IV surveillance is expanding for chronic therapies where lifetime exposure necessitates pharmacovigilance across developmental stages, leveraging real-world data and registries to capture growth and neurocognitive endpoints.

By Study Design: Drug Interventions Dominate Amid Observational Growth

Interventional drug protocols held 64.93% pediatric clinical trials market share in 2025, reflecting regulatory imperatives for child-specific pharmacokinetic and safety data. Observational cross-sectional studies will contribute the fastest 7.44% CAGR to 2031 as regulators accept real-world evidence to support supplemental labeling, especially in ultra-rare diseases where randomized trials are infeasible.

Device interventions, although smaller in count, are rising steadily in diabetes tech and neuromonitoring, propelled by the need to validate sensor accuracy and alert thresholds in infants. Behavioral and cohort studies complement drug trials by characterizing adherence patterns, school attendance impacts, and psychosocial outcomes critical to holistic benefit-risk assessment in the pediatric clinical trials industry.

By Therapeutic Area: Oncology Leadership Challenged by Rare Disease Innovation

Oncology preserved 34.71% of pediatric clinical trials market share in 2025 on the back of molecularly targeted therapeutics and immunotherapies mandated under the RACE Act. Rare disease programs, however, are set to eclipse all others in growth with an 8.26% CAGR as sponsors pursue Priority Review Voucher incentives and leverage gene-editing platforms to address monogenic disorders.

Infectious-disease trials pivoted after the COVID-19 pandemic toward RSV monoclonal antibodies such as nirsevimab, exemplifying accelerated licensure paths for preventive biologics in neonates. Respiratory, metabolic, and neurologic areas also show steady expansion, fueled by chronic burden trends and breakthroughs in gene-therapy vectors crossing the blood–brain barrier.

By Sponsor Type: Academic Institutions Accelerate Public Health Focus

Pharmaceutical and biopharmaceutical firms retained 48.72% pediatric clinical trials market size in 2025, largely to fulfill mandatory pediatric post-marketing requirements. Government and academic institutions, backed by NIH and EU Horizon grants, will log an 8.15% CAGR to 2031 as they target public-health gaps such as neonatal sepsis and adolescent mental health where commercial incentives are limited.

CROs gain traction as intermediaries, blending industry resources with academic mentorship programs for investigator training. Hybrid sponsor models—pharma supplying investigational product while universities lead protocol design—are flourishing, aligning economic efficiency with scientific rigor and broadening the pediatric clinical trials industry’s collaborative fabric.

Geography Analysis

North America commanded 39.02% of the pediatric clinical trials market in 2025 due to PREA-driven mandates, a dense network of children’s hospitals, and reliable reimbursement for trial-related procedures. Institutional capacity initiatives, such as Lurie Children’s plan to open a specialty pharmacy in 2026, reinforce integrated research-to-care models. Staffing shortages persist but are mitigated by remote-monitoring adoption and site-support alliances.

Asia-Pacific will post a 7.18% CAGR through 2031, buoyed by South Korea’s centralized IRB review, Taiwan’s fast-track approvals, and Australia’s decentralized trial guidelines that slash start-up times by up to three months. China’s expansion of its National Rare Disease List and investment in provincial referral networks further enlarge patient pools. Lower operational costs and rapidly digitizing healthcare records enhance the region’s attractiveness to multinational sponsors aiming to diversify recruitment.

Europe benefits from a harmonized regulatory environment via the Paediatric Committee (PDCO) and maintains robust academic-industry collaboration. Still, post-Brexit regulatory divergence demands duplicate submissions for UK sites, prolonging timelines compared with EU27. Emerging regions such as Latin America and the Middle East show incremental gains as governments upgrade research infrastructure and introduce tax incentives, but limited pediatric specialist density constrains complex trial execution for now.

Regulatory Landscape

In the United States, pediatric trial demand is anchored by the Pediatric Research Equity Act (PREA), which requires sponsors to submit an initial Pediatric Study Plan (iPSP) describing pediatric assessments for new drugs and biologics, and by oncology-specific requirements under the RACE for Children Act that pull pediatric evaluation earlier for relevant molecular targets. The FDA finalized ICH E11A pediatric extrapolation guidance in December 2024, which clarifies how adult data can support pediatric development when scientifically justified, alongside increasing use of modeling and simulation in dose selection and trial design.

In Europe, the Paediatric Regulation (EC) No 1901/2006 mandates an agreed Paediatric Investigation Plan (PIP) and is overseen through the EMA Paediatric Committee (PDCO). EU submissions have also tightened operationally under Clinical Trial Regulation (CTR) 536/2014, with the transition deadline taking full effect for ongoing trials by January 31, 2025, and the EMA requiring use of its IRIS platform for pediatric-related procedures (PIPs, modifications, compliance checks, and deferred-measures reporting). These frameworks help sponsors align global programs, but execution still varies across Member States under CTR assessments, which can affect multi-country pediatric start-up timelines.

Competitive Landscape

The pediatric clinical trials market is moderately fragmented. Top CROs deploy region-specific pediatricians, decentralized sampling logistics, and AI-enabled feasibility platforms to win full-service contracts. IQVIA’s global pediatric database underpins synthetic-control-arm generation, shortening trial durations for rare cancers. ICON expands its AI suite for study-startup forecasting and patient-identification algorithms, translating into quicker first-patient-in milestones.

Strategic alliances intensify: LEO Pharma’s five-year pact with ICON mobilizes 500 dermatology specialists under risk-share terms that link CRO fees to recruitment timelines. Technology disruptors such as Phesi and Pi Health license AI-driven site-selection engines to incumbents, while blockchain pilots from academic consortia test immutable consent tracking for minors. Acquisition activity continues as illustrated by Clario’s 2025 purchase of NeuroRx to bolster pediatric neuroimaging analytics[3]Axios, “Clinical Trials Company Clario Buys Imaging Specialist NeuroRx,” axios.com. Competitive advantage hinges on demonstrating integrated capabilities that compress timelines, respect child-centric ethical standards, and reduce per-patient cost.

White-space opportunities persist in decentralized home-nursing networks, culturally tailored consent tools, and adaptive-design statistical consulting. Companies that integrate these services within a scalable digital backbone are positioned to outpace peers as sponsors increasingly demand end-to-end pediatric solutions.

Pediatric Clinical Trials Industry Leaders

IQVIA

ICON plc

Thermo Fisher Scientific (PPD)

Syneos Health

Labcorp Drug Development (Covance)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Decentralized and family-centric trial operations create practical whitespace in pediatric recruitment and retention, particularly in rare diseases where eligible pools are small and travel burdens are high. Evidence from rare disease trial research published in 2026 indicates strong parent preference for remote visits and digital tools, supporting demand for scalable eConsent, telemedicine, and home-visit models that can be deployed across multiple countries while keeping assent and guardian permission workflows auditable. CROs and technology providers that package these capabilities with pediatric-trained staff can differentiate in sponsor outsourcing decisions as multinational programs expand beyond North America and Europe into Asia-Pacific review pathways.

Methodological innovation is also opening new execution models in pediatric oncology and ultra-rare indications. A 2026 systematic review highlighted increasing use of basket and umbrella designs in early-phase pediatric oncology and rare disease research, which fits the need to study biomarker-defined subgroups when conventional indication-by-indication trials are not feasible. At the same time, reporting and quality expectations are tightening, with the CONSORT-C 2026 extension adding pediatric-specific reporting items for randomized trials, increasing demand for stronger data standards, endpoint definitions, and reproducibility-ready documentation across sponsors, sites, and eClinical stacks.

Recent Industry Developments

- July 2026: Bayer announced a strategic clinical trials alliance with the University of Colorado Anschutz, UCHealth, and Children's Hospital Colorado to expand infrastructure and clinical trial activity, including pediatrics. The collaboration strengthens access to specialized sites and integrated care settings that can support complex pediatric protocols. It also signals continued sponsor investment in regional networks to improve recruitment and operational throughput.

- June 2025: Biogen initiated dosing in the BRAVE Phase 3 study of omaveloxolone in children aged 2 to 15 years with Friedreich ataxia. The program adds late-stage volume in pediatric rare neurology, where enrollment constraints elevate the value of experienced sites and patient-identification workflows. Phase 3 activity also increases downstream needs for pediatric safety monitoring and long-term follow-up infrastructure.

- September 2024: Signant Health joined IQVIA's One Home for Sites program to unify eClinical solutions across decentralized studies, including pediatric protocols. Standardizing site-facing technology reduces friction in hybrid trial execution where consent, ePRO, and remote data capture must be coordinated across families, investigators, and monitors. The move supports broader adoption of virtual elements that can widen geographic reach for pediatric enrollment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the global value of services and spending tied to designing, running, and managing clinical trials where participants are children and adolescents, across the typical trial lifecycle and geographies.

Scope exclusions: We exclude routine pediatric medical care that is not part of a regulated clinical trial and any non-clinical research work that does not generate trial data.

Segmentation Overview

- By Phase

- Phase I

- Phase II

- Phase III

- Phase IV

- By Study Design

- Interventional - Drug

- Interventional - Device

- Behavioral Trials

- Observational - Cohort

- Observational - Case-Control

- Observational - Cross-Sectional

- By Therapeutic Area

- Oncology

- Infectious Diseases

- Respiratory Diseases

- Endocrine & Metabolic (Diabetes)

- Neurology

- Rare Diseases

- By Sponsor Type

- Pharma & Biopharma Companies

- Contract Research Organizations

- Government & Academic Institutions

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public, repeatable references that describe how many pediatric studies are happening and where growth is coming from. We used sources such as ClinicalTrials.gov, the EU Clinical Trials Register, and the World Health Organization trial registry network to understand trial volume, phase mix, and therapy focus by region.

We also relied on supportive public signals like FDA and EMA pediatric regulation pages and guidance updates, peer reviewed publications on pediatric enrollment and trial design, and association websites and reputable press that track R&D and outsourcing trends. For company level grounding, we reviewed filings and investor presentations, and we used an approved paid subscription for company financials and for patent database checks where relevant. These examples are not exhaustive, and many other public sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what desk sources cannot show clearly, like how budgets move by phase, where pediatric recruitment is most constrained, and how outsourcing intensity changes by region. We spoke with a mix of sponsors, CRO delivery leaders, site level operators, and subject experts across major regions so assumptions could be stress tested against how pediatric trials run in practice, then aligned to realistic operating conditions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 17% | APAC: 52% |

| Mid tier: 44% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 19% | Managers: 42% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where trial activity and regulatory driven pediatric study requirements are translated into a spend pool by applying typical cost intensity by phase and study design, and then allocated by region based on observed trial distribution. To keep it practical, we then corroborated the totals with selective bottom-up checks, such as sampled program budgets, CRO revenue exposure to pediatric work, and sanity checks using average cost per patient and expected enrollment ranges.

A few inputs that were treated as core drivers (illustrative) were pediatric trial counts by phase, interventional versus observational split, therapeutic mix shifts (for example oncology and rare diseases), enrollment and retention friction that drives timeline extensions, and outsourcing penetration into CRO led delivery. For forecasting, scenario analysis was used, supported by primary views on cost inflation, currency timing, and expected changes in regulatory enforcement and protocol complexity. Where bottom-up signals were missing in smaller countries, we used proxy ratios from similar markets and adjusted them after interview feedback so gaps did not overstate the total.

Data Validation & Update Cycle

Outputs were cross checked against independent signals, and outliers were reviewed until the reason for variance was clear, such as a sudden phase mix change or a one-time program spike. A second analyst review was done for key assumptions, and follow up outreach was triggered when interview feedback conflicted with desk indicators.

The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or sharp cost inflation shifts. Before delivery, a final pass is completed to capture recent data releases and to ensure the model logic and year labeling remain consistent.

Mordor Intelligence's Pediatric Clinical Trails Market Size Versus Other Published Estimates

Published market sizes for pediatric clinical trials often vary because the counted spend can shift based on timing, currency treatment, and what is considered trial delivery cost versus adjacent research support. Even when the same years are used, different assumptions on cost per patient and trial duration can move the total quickly.

In this market, the biggest gap drivers tend to be how refresh cadence handles recent cost inflation, whether values are reported in a single conversion month versus averaged across the year, and how blended pricing is built across Phase I to Phase IV work. For a refresh-led lens, the tighter alignment comes from re-checking phase level cost intensity and applying consistent currency timing before final sign-off, which is the specific update control used in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.03 B (2026) | |

| Global Research Publisher A | USD 19.90 B (2024) | Uses an earlier base year and can understate the latest cost inflation, and it may blend pediatric trial spend with a broader study design mix that shifts average pricing. |

| Market Analytics Firm B | USD 19.74 B (2024) | Relies on a longer forecast window starting earlier, and differences in currency conversion timing and phase weighting can pull the current value lower than a later-year refresh. |

The spread across sources is directionally consistent with differences in base year selection and how phase level pricing and currency timing are handled. By keeping the model tied to observable trial activity and then re-validating cost assumptions through primary checks, the final number stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current size and growth outlook for the pediatric clinical trials market?

The pediatric clinical trials market is valued at USD 21.03 billion in 2026 and is projected to reach USD 26.89 billion by 2031, advancing at a 5.03% CAGR.

Which clinical trial phase holds the largest share and which is expanding fastest?

Phase II trials account for the largest 40.26% market share in 2025, while Phase I trials are growing quickest with a 6.96% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region for pediatric studies?

Streamlined regulatory reviews in South Korea, Taiwan, and Australia, combined with large patient pools and cost advantages, drive a 7.18% CAGR for Asia-Pacific to 2031.

What primary factors are boosting global pediatric trial volumes?

Mandates such as the US PREA, EU Paediatric Regulation, and RACE for Children Act, plus rising chronic disease prevalence and growth in decentralized trial models, are key growth catalysts.

What recruitment challenges commonly slow pediatric trials?

Small eligible patient pools, complex dual consent-assent requirements, language barriers, and post-pandemic site staffing shortages together constrain enrollment rates to about 10% of eligible children.

Page last updated on: