Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

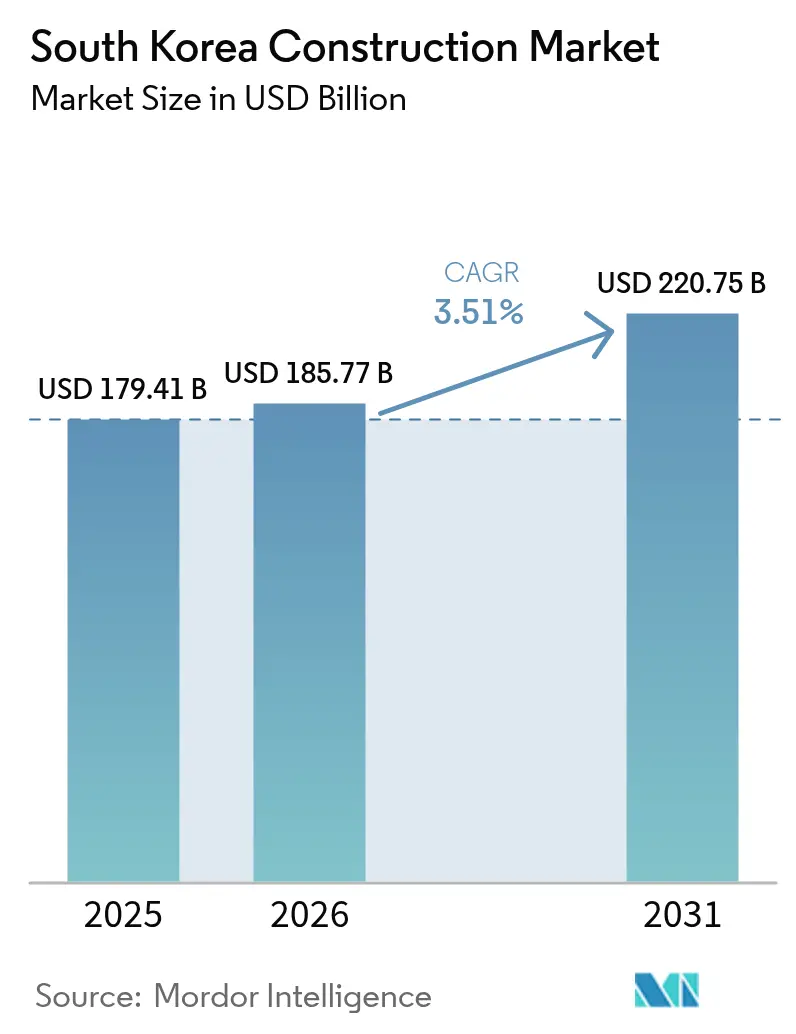

| Base Year Market Size (2025) | USD 179.41 Billion |

| Market Size (2026) | USD 185.77 Billion |

| Market Size (2031) | USD 220.75 Billion |

| Growth Rate (2026 - 2031) | 3.51% CAGR |

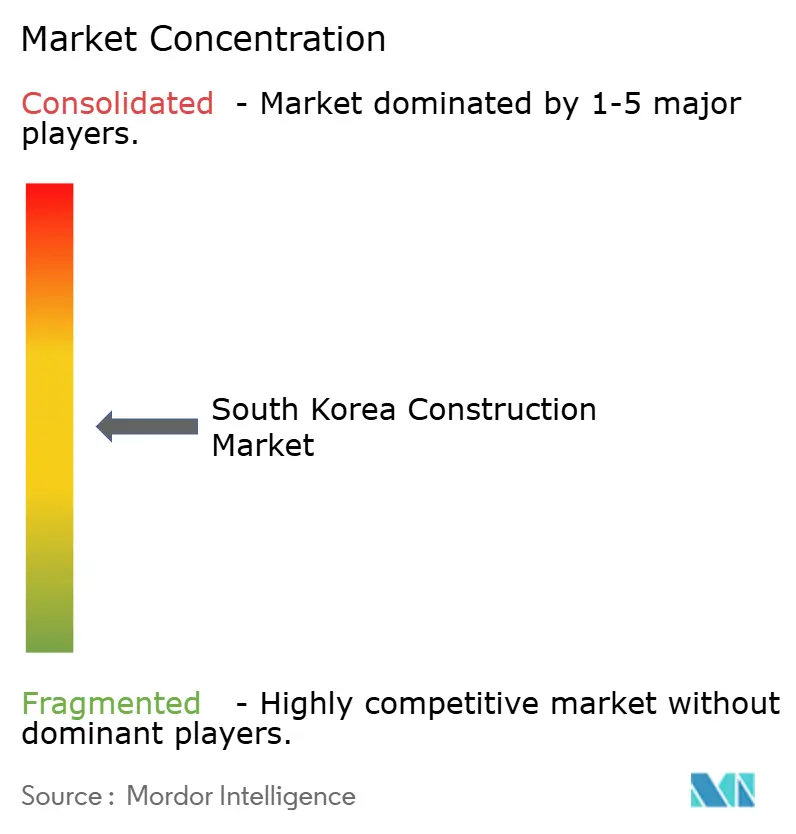

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Construction Market Analysis by Mordor Intelligence

The South Korea construction market size was valued at USD 179.41 billion in 2025 and is estimated to grow from USD 185.77 billion in 2026 to reach USD 220.75 billion by 2031, at a CAGR of 3.51% during the forecast period (2026-2031). A robust pipeline of rail, port and airport schemes, record semiconductor and battery-plant capital expenditure, and Seoul’s mixed-use urban regeneration program together underpin steady demand. Public spending is accelerating on the back of the Korean New Deal 2.0, while private-sector outlays continue to flow into high-tech industrial clusters. Labor shortages and input-cost volatility temper near-term margins yet also speed up the adoption of modular methods. Intensifying competition for trillion-won redevelopment contracts keeps market concentration moderate, even as the top three contractors account for more than two-thirds of large infrastructure orders.

Key Report Takeaways

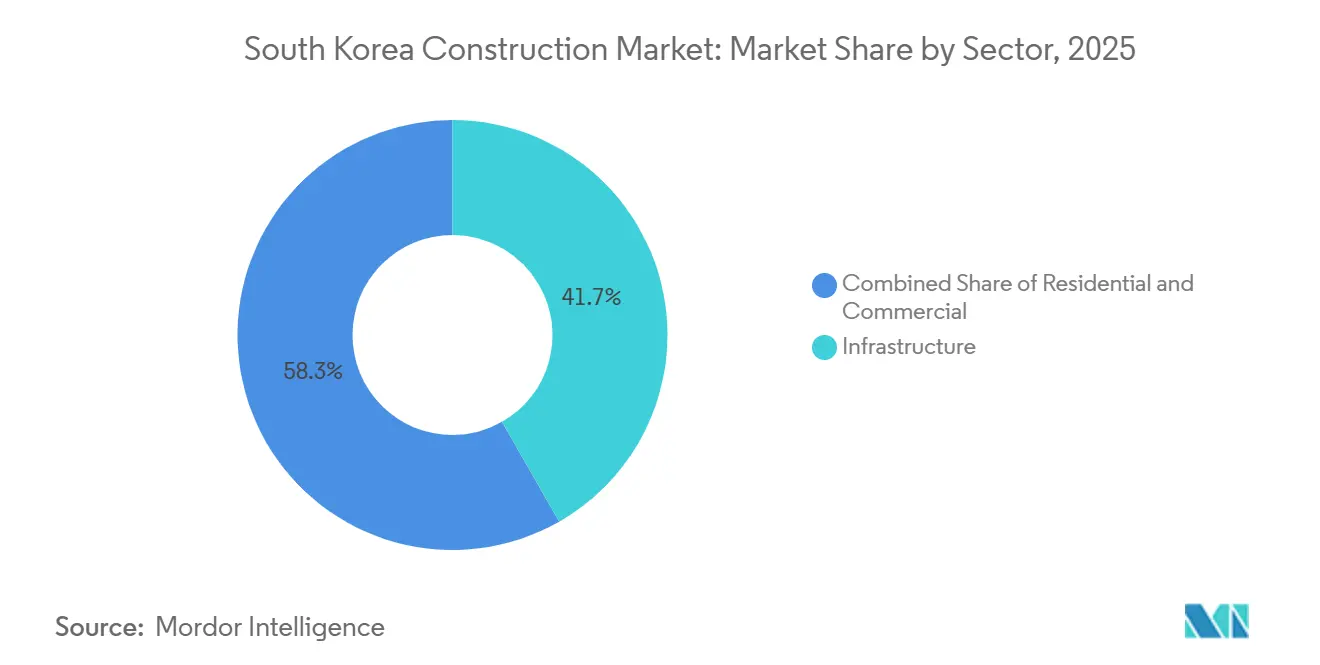

- By sector, Infrastructure led with 41.74% of the South Korea construction market share in 2025, whereas Industrial & Logistics is projected to expand at a 4.11% CAGR through 2031, outpacing overall growth.

- By construction type, New Construction commanded 65.36% of the South Korea construction market size in 2025, while Renovation is advancing at a 4.34% CAGR to 2031.

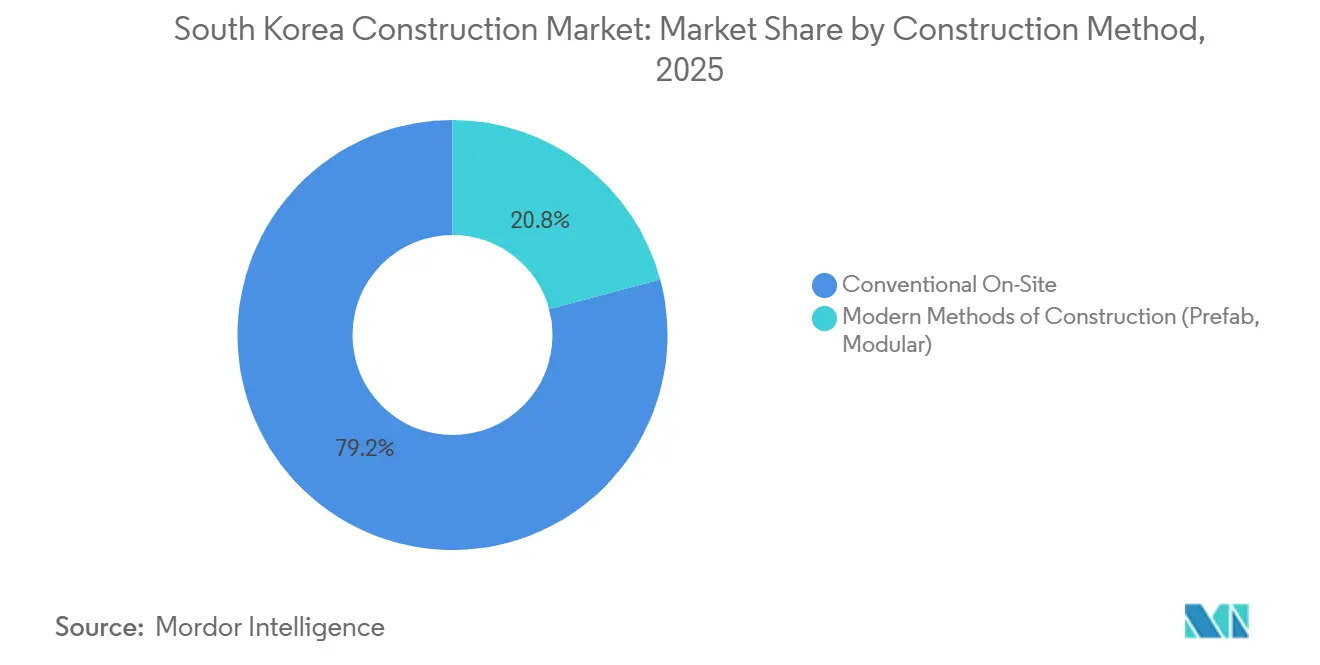

- By construction method, Conventional On-Site held 79.16% of the 2025 market, and modern methods of construction are forecast to grow at 4.55% CAGR through 2031.

- By investment source, the Public segment is set to grow at a 4.65% CAGR through 2031 against Private’s 59.38% share in 2025, reflecting front-loaded infrastructure stimulus.

- By geography, Seoul captured 24.98% of 2025 activity, whereas Daegu is the fastest-growing city with a projected 4.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor and battery-plant CAPEX surge | +1.2% | Gyeonggi, North Jeolla, North Chungcheong | Medium term (2-4 years) |

| Korean New Deal 2.0 infrastructure stimulus | +0.9% | Nationwide | Short term (≤ 2 years) |

| Robust rail, port and airport pipeline | +0.8% | National, notably Busan, Incheon, Seoul | Long term (≥ 4 years) |

| Seoul urban regeneration and mixed-use redevelopment | +0.6% | Seoul metropolitan area | Medium term (2-4 years) |

| Zero-Energy-Building code for ≥1,000 m² floorplate | +0.5% | Nationwide, higher in major CBDs | Medium term (2-4 years) |

| Growth of private REITs and infrastructure funds | +0.4% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor and Battery-Plant CAPEX Surge

High-tech manufacturers are pouring money into new fabs and battery lines, led by SK Hynix’s extra USD 16.6 billion for its Yongin cluster and a USD 4.9 billion battery hub in Saemangeum. Projects need vibration-free slabs, ISO-class cleanrooms and heavy-duty power links, which command premium fees. Contractors with proven chip-plant experience have a clear edge over rivals. The wave of industrial spending also pulls skilled labor away from traditional building sites, tightening labor supply elsewhere.

Korean New Deal 2.0 Infrastructure Stimulus

A record USD 560 billion-equivalent is allocated in the 2026 budget for transport, digital and green retrofits. Front-loaded awards cushion contractors against slower private housing demand, especially on road packages like Daegu’s USD 904 million congestion-relief plan. The big three builders captured most of the early contracts, reinforcing their market position. Although project vetting is tighter, the stimulus provides near-term order visibility through 2027.

Robust Rail, Port and Airport Pipeline

The government is pushing ahead with large transport projects, such as the USD 8.25 billion Gadeok New Airport and the USD 6.68 billion second urban rail network in Incheon. These schemes improve nationwide logistics efficiency and reduce freight bottlenecks between key cities. Large civil-works contractors gain predictable, multi-year revenue from the long build-out schedules. Land-acquisition disputes can delay some packages, yet the program still provides a solid growth floor for the sector.

Seoul Urban Regeneration and Mixed-Use Redevelopment

Seoul is fast-tracking redevelopment along the Yongsan–Gwanghwamun corridor, anchored by the USD 39.2 billion Yongsan International Business District. Redevelopment contracts such as Seongsu 1 and Hannam 4 reward firms that can blend residential, retail and cultural spaces in one footprint. The city’s Rapid Integrated Planning rules shorten permits, but compressed schedules raise execution risk for mid-tier players. Overall, mixed-use schemes keep private investment flowing even when the housing cycle cools.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortages and double-digit wage inflation | -0.7% | National, with acute pressure in Seoul, Busan, Incheon metro areas | Short term (≤ 2 years) |

| High household debt & tighter LTV limits cooling residential starts | -0.6% | Seoul capital region, Busan, Daegu regulated zones | Short term (≤ 2 years) |

| Construction-steel & cement price volatility amid supply-chain realignments | -0.5% | National, with higher exposure in infrastructure and industrial segments | Medium term (2-4 years) |

| Upcoming carbon-pricing & ESG-reporting mandates raising compliance costs | -0.3% | National, with higher impact on KOSPI firms ≥30 trillion KRW assets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-labour shortages and double-digit wage inflation

Average site wages reached 279,988 KRW per day in January 2026, 3.4% higher year on year, while overall construction employment fell by 125,000 workers during 2025[1]Korea JoongAng Daily, “Construction wages hit record…,” JOINS.COM. Government promotion of modular methods aims to offset shortages, yet fabrication capacity is still concentrated among tier-one contractors. Mid-sized firms with limited bargaining power suffer margin compression when wage hikes outpace price-escalation clauses.

High household debt & tighter LTV limits cooling residential starts

An October 2025 policy capped LTV ratios at 40% in regulated areas and limited mortgages above 2.5 billion KRW to 200 million KRW, cutting Seoul groundbreakings to only 6,000 units in the first nine months of 2025. Seoul’s emergency relocation-loan program and rapid-planning initiative offer some relief, but private apartment starts remain subdued.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Dominates as Industrial & Logistics Accelerates

Infrastructure accounted for 41.74% of the South Korea construction market share in 2025, buoyed by megaprojects such as the Gadeok New Airport and Incheon’s second urban rail network. The segment benefits from multi-year public budgets that smooth demand through economic cycles. Industrial & Logistics, while smaller, leads growth at a 4.11% CAGR on the strength of semiconductor fabs, battery plants, and energy-storage facilities.

Capital commitments exceeding 20 trillion KRW for ESS lines and advanced packaging drive specialized demand for vibration-controlled foundations, cleanrooms, and high-voltage substations. Residential starts face lending curbs, but Seoul’s fast-tracked 85,000-unit pipeline underpins steady renovation and infill projects. Commercial developments, exemplified by the Yongsan International Business District, integrate retail and cultural features that meet post-pandemic preferences for mixed-use environments.

By Construction Type: Renovation Gains Speed

New Construction still represented 65.36% of the South Korea construction market size in 2025 as large civil and public-housing schemes dominated order books. Yet Renovation is expanding faster at 4.34% CAGR, reflecting Seoul’s focus on redeveloping aging apartment complexes rather than building on greenfield land.

GS E&C’s 6.3 trillion KRW 2025 redevelopment backlog and Samsung C&T’s Hannam 4 and Sinbanpo 4th projects highlight top-tier appetite for capital-city brownfield sites. The Zero-Energy-Building code further tilts spending toward retrofits as owners upgrade insulation, HVAC and solar arrays to meet efficiency thresholds.

By Construction Method: Modular Adoption Rises

Conventional on-site techniques still accounted for 79.16% of 2025 activity, but Modern Methods of Construction are growing quickest at 4.55% CAGR as labor scarcity pushes fabrication off-site. LH’s Sejong L5, Korea’s largest modular scheme with 450 units completing in 2027, serves as a national proof point.

Off-site production can cut schedules by up to 30% and reduce defect rates, yet structural-complexity limits application to high-rise towers. Mid-tier contractors without prefab yards risk falling behind as public contracts increasingly incorporate modular quotas.

By Investment Source: Public Spending Outpaces Private Growth

Private investors supplied 59.38% of the project's value in 2025, channeling funds into high-tech factories and large-scale urban renewal. Public expenditure, however, is forecast to grow faster at 4.65% CAGR, driven by the New Deal 2.0 and regional transport stimulus.

LH’s 86,000-home capital-region groundbreakings this year and Daegu’s congestion-road network illustrate near-term public-sector heft. At the same time, REIT and fund vehicles attract pension and insurer capital into hybrid public-private models that ease fiscal burdens while ensuring steady yields.

Geography Analysis

Seoul’s 24.98% share in 2025 rests on the 51 trillion KRW Yongsan IBD and an aggressive timeline that moves 85,000 units to groundbreaking by 2028[2]Yonhap News Agency, “Daegu congestion road plan…,” YNA.CO.KR. The Rapid Integrated Planning 2.0 framework collapses sequential approvals into parallel processes, trimming months off schedules. Yet higher land costs and tighter lending standards amplify execution risk for mid-tier builders.

Daegu advances fastest, with a 4.17% CAGR expected through 2031 on the back of a 1.1758 trillion KRW congestion-road package that improves links to its manufacturing belt. Busan captures spillover gains from the 10.72 trillion KRW Gadeok New Airport and complementary tram and station upgrades that transform urban mobility. Incheon pursues seven new rail lines totaling 124 km and backs housing growth with REIT-financed towers near Gulpocheon Station.

Rest-of-nation demand clusters around semiconductor and battery hubs in Gyeonggi, North Jeolla and North Chungcheong. SK Hynix’s multi-decade 600 trillion KRW pledge and a 6.4 trillion KRW Saemangeum battery hub reshape labor flows, prompting wage inflation that spills back into civil works in smaller provinces.

Competitive Landscape

Samsung C&T, Hyundai E&C and Daewoo E&C rank first to third by capability, together winning large infrastructure contracts in 2025[3]Asiae, “Samsung tops capability ranking…,” ASIAE.CO.KR. Redevelopment remains fiercely contested; Samsung clinched Hannam 4 and Sinbanpo 4th, GS E&C secured Seongsu 1, and Daewoo challenges Lotte for Seongsu 4. Vertical integration in steel procurement and equipment pooling gives the top tier cost resilience against volatile inputs.

Strategic alliances are extending beyond South Korea, strengthening the global credentials of domestic engineering and construction firms. For instance, Samsung C&T secured a USD 1.4 billion carbon-capture EPC contract in Qatar and is also delivering the Dukhan solar project, comprising around 2.74 million photovoltaic panels, enhancing its expertise in large-scale sustainable infrastructure that can be leveraged for domestic Zero Energy Building (ZEB) projects. In addition, the merger involving HD Construction Equipment is expected to consolidate construction machinery supply chains, potentially reducing equipment rental costs for contractors operating within aligned industrial networks.

Competitive dynamics are also being influenced by new financing mechanisms. Financial institutions such as KB Financial Group have introduced large infrastructure investment vehicles, including a USD 730 million infrastructure fund, while municipal real estate investment trusts (REITs) are creating additional funding channels for project development. Although these financing innovations may broaden market participation, regulatory factors such as leverage limits and stewardship governance codes are likely to continue favoring large, diversified conglomerates with stronger balance sheets, suggesting that any shift away from incumbent dominance may occur gradually rather than abruptly.

South Korea Construction Industry Leaders

Samsung C&T Corporation

Hyundai E&C

GS E&C

Daewoo E&C

DL E&C (Daelim)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Busan confirmed the Bujeon Station multimodal hub schedule, with construction slated to start in 2030.

- February 2026: Seoul fast-tracked 85,000 housing starts to 2028 and released 50 billion KRW in relocation loans.

- January 2026: HD Construction Equipment completed its Hyundai-Develon merger, posting USD 5.5 billion sales.

- November 2025: Samsung C&T secured a carbon-compression EPC contract in Qatar worth approximately USD 1.4 billion.

South Korea Construction Market Report Scope

Construction is a general term meaning the art and science of forming objects, systems, or organizations. Construction is an industry that includes the erection, maintenance, and repair of buildings and other immobile structures and the building of roads and service facilities that become integral parts of structures and are essential to their use.

The South Korean construction market is segmented by sector (residential construction, commercial construction, industrial construction, infrastructure (transportation) construction, and energy and utilities construction). The report offers market size and forecasts for the South Korean construction market in value (USD billion) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial & Logistics | |

| Others | |

| Infrastructure | Transportation (Road, Rail, Air etc.) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefab, Modular) |

By Investment Source

| Public |

| Private |

By Key Cities

| Seoul |

| Busan |

| Daegu |

| Incheon |

| Rest of South Korea |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial & Logistics | ||

| Others | ||

| Infrastructure | Transportation (Road, Rail, Air etc.) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefab, Modular) | ||

| By Investment Source | Public | |

| Private | ||

| By Key Cities | Seoul | |

| Busan | ||

| Daegu | ||

| Incheon | ||

| Rest of South Korea | ||

Key Questions Answered in the Report

How large is the South Korea construction market in 2026?

The market is estimated at USD 185.77 billion in 2026 with a projected CAGR of 3.51% toward 2031.

Which sector is growing fastest in South Korean construction?

Industrial & Logistics leads with a 4.11% CAGR through 2031, driven by semiconductor and battery-plant investments.

What is driving the uptake of modular construction in South Korea?

Labor shortages and the government’s target of 3,000 modular public housing units per year are prompting faster adoption of off-site fabrication.

Why is Daegu forecast to outpace other key cities?

A USD 0.90 billion road-congestion program improves logistics connectivity, lifting Daegu’s projected CAGR to 4.17% through 2031.

How are builders tackling labor shortages?

By shifting to modular construction and off-site fabrication that cut on-site labor needs.

When do mandatory climate disclosures begin?

Large listed contractors must start ISSB-aligned reporting in 2028, with full Scope 3 data by 2031.

Page last updated on: