Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

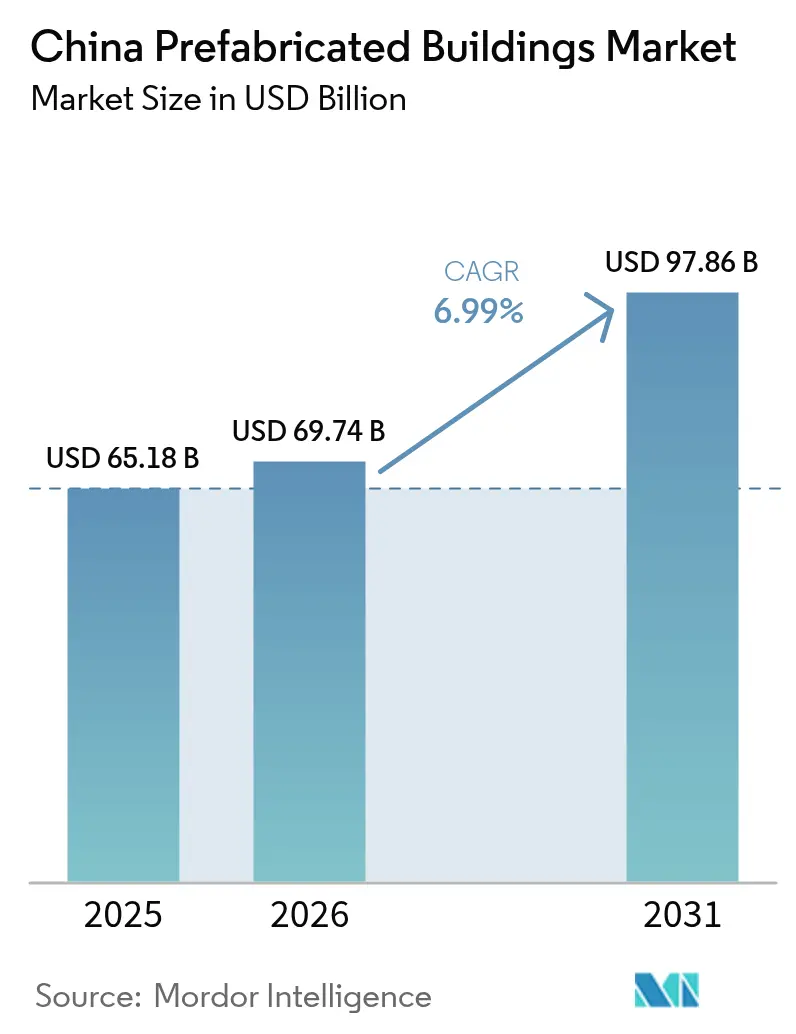

| Base Year Market Size (2025) | USD 65.18 Billion |

| Market Size (2026) | USD 69.74 Billion |

| Market Size (2031) | USD 97.86 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

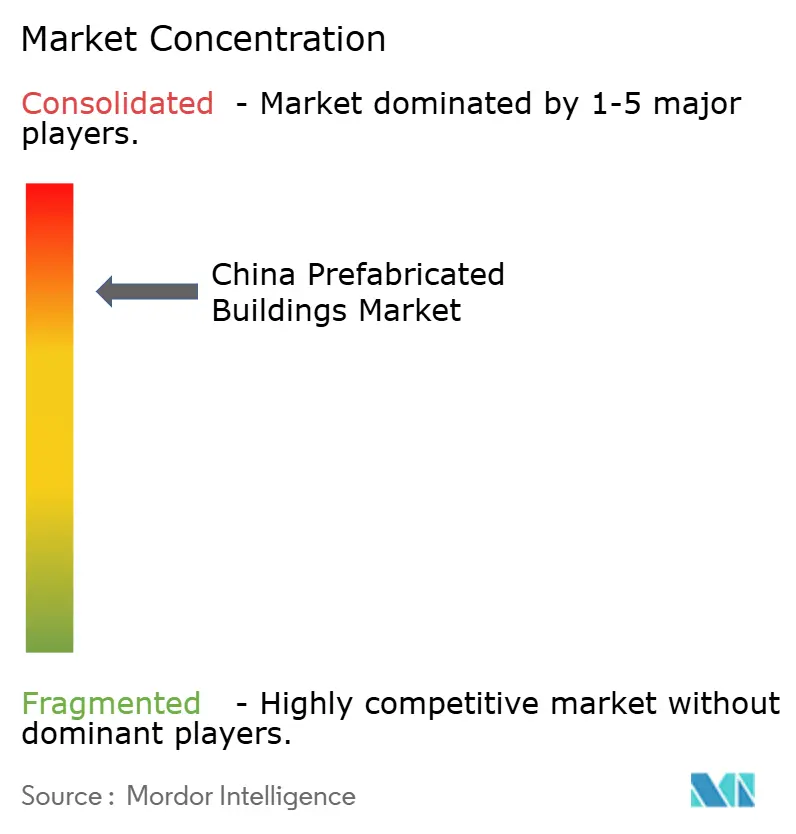

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Prefabricated Buildings Market Analysis by Mordor Intelligence

The China prefabricated buildings market size was valued at USD 65.18 billion in 2025 and estimated to grow from USD 69.74 billion in 2026 to reach USD 97.86 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031). Government quotas that require 30% of new urban construction to be industrialized by 2027, paired with carbon-neutrality commitments, position factory-built methods as the default solution for rapid, low-waste delivery of housing and infrastructure. Post-COVID stimulus, rising labor costs, and stringent site-safety rules further accelerate adoption, while Building-Information-Modeling (BIM) mandates in Shenzhen and other tier-1 cities are pushing digital integration deeper into project workflows. Competitive dynamics remain fragmented because regional specialists retain strong local relationships, yet the liquidity crunch among traditional developers is creating consolidation opportunities for well-capitalized integrated contractors that can design, manufacture, and assemble under one roof.

Key Report Takeaways

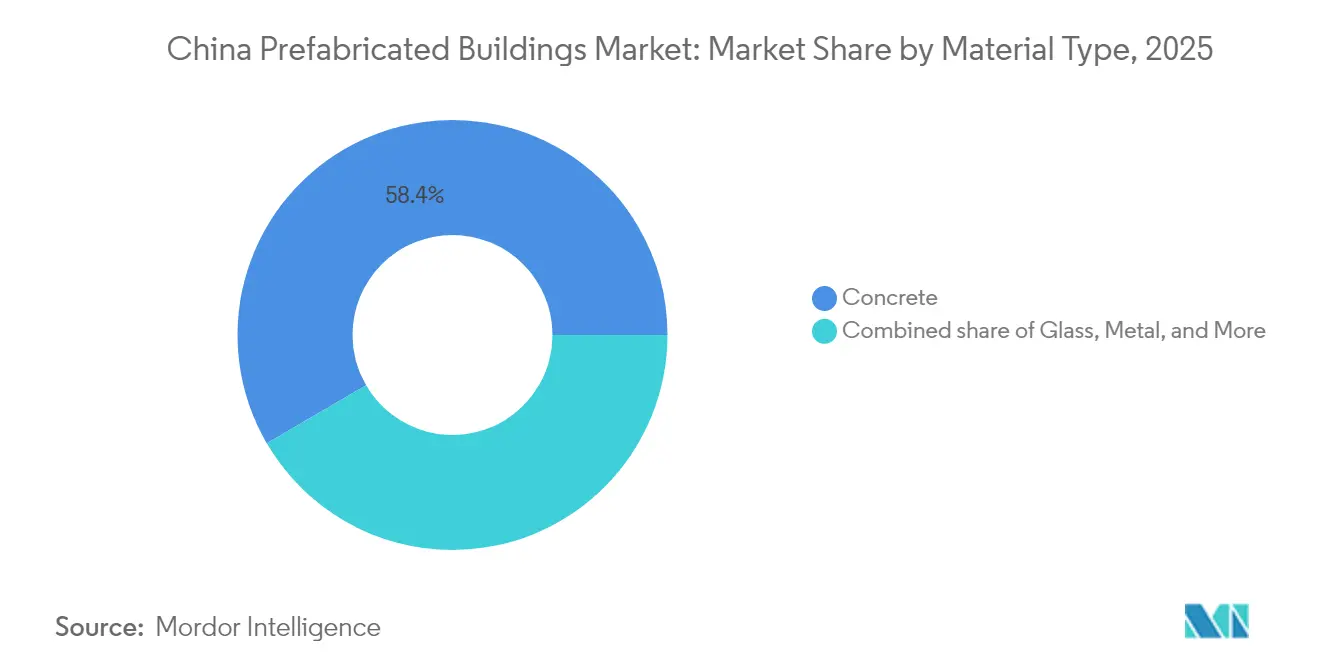

- By material type, concrete led with 58.40% China prefabricated buildings market share in 2025, while timber CLT/LVL is advancing at a 7.45% CAGR between 2026-2031.

- By application, residential construction held 53.65% of the China prefabricated buildings market size in 2025, whereas industrial and infrastructure projects are expanding at a 7.19% CAGR between 2026-2031.

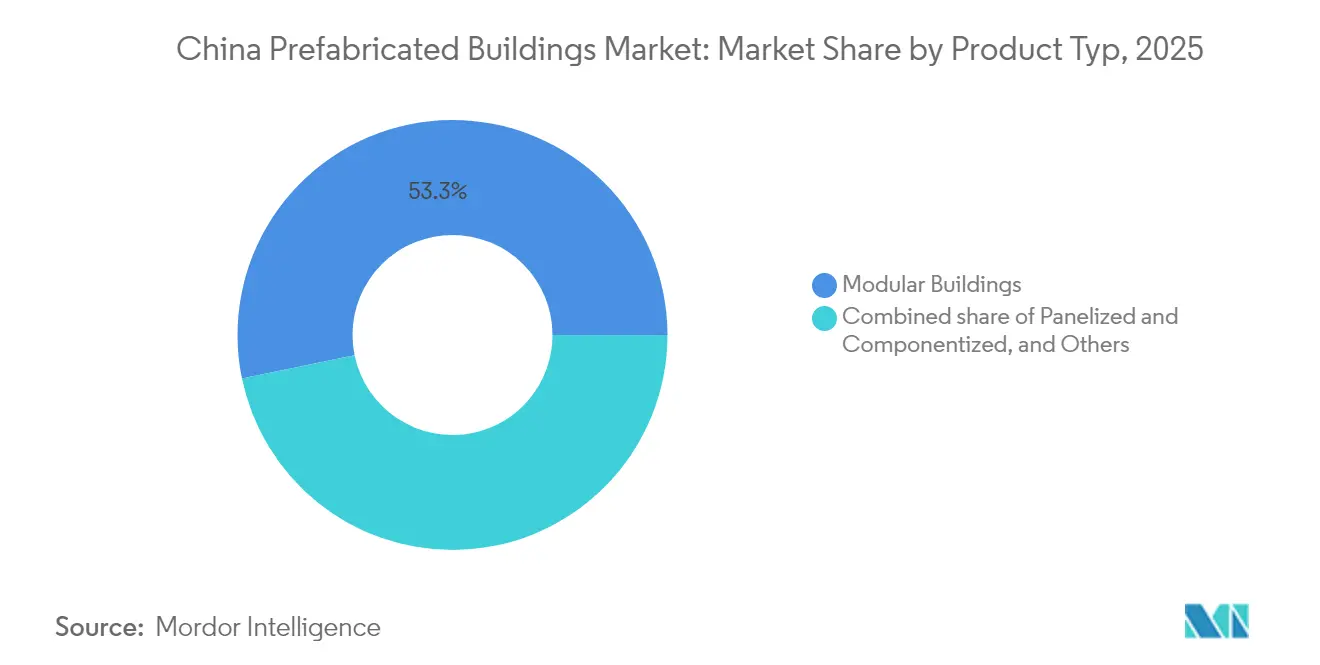

- By product type, modular buildings commanded 53.25% of the China prefabricated buildings market size in 2025, yet panelized and componentized systems are forecast to grow at a 7.32% CAGR.

- By city, Shanghai captured 18.60% of the China prefabricated buildings market share in 2025, with Shenzhen registering the fastest 7.58% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Prefabricated Buildings Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National “Assembly Building” quotas for public projects | +1.8% | Nationwide, early adoption in tier-1 cities | Medium term (2-4 years) |

| Accelerated affordable-housing starts | +1.2% | Urban centers nationwide | Short term (≤ 2 years) |

| Carbon-neutrality mandates | +1.5% | Nationwide, stricter in eastern provinces | Long term (≥ 4 years) |

| Rising labor costs and safety enforcement | +0.9% | Coastal manufacturing hubs | Medium term (2-4 years) |

| Shenzhen BIM-Digital-Twin mandate | +0.4% | Shenzhen and Guangdong spillover | Short term (≤ 2 years) |

| HSR module yards repurposed for micro-apartments | +0.3% | Cities along high-speed rail corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National “Assembly Building” Quota Targets for Public Projects

The Ministry of Housing and Urban-Rural Development (MOHURD) requires 30% of new urban floor area to incorporate prefabricated methods by 2027, guaranteeing a minimum demand floor even during down-cycles. The 14th Five-Year Plan adds 50 million m² of ultra-low-energy buildings that must hit strict performance scores, effectively locking in factory-built envelopes. Multiple provinces have slashed permit processing times for qualifying projects, and Jiangsu has piloted one-stop approvals that cut paperwork by 45%.[1]Jiangsu Provincial Department of Housing and Urban-Rural Development, “Streamlined Approval Measures,” jsszfhcxjst.jiangsu.gov.cn

Accelerated Affordable-Housing Starts amid Post-COVID Stimulus

Special-purpose bonds topping USD 100 billion in 2024 boosted city-level housing starts that favor the 30-60 day delivery cycle achievable with modular components[2]National Development and Reform Commission, “2024 Report on Social and Economic Development,” ndrc.gov.cn. Beijing’s Baiziwan complex used 80% off-site elements across 4,000 units, setting a precedent for tier-2 cities eyeing rapid social-housing rollouts. Subsidies now reimburse up to 15% of component costs once specified assembly rates are verified, enhancing project cash-flow profiles.

Carbon-Neutrality Mandates Favoring Low-Waste Off-Site Methods

Construction accounted for 47.1% of China’s energy-related emissions in 2024, prompting regulators to embed carbon accounting into building codes. Studies show prefabrication cuts site waste and slashes lifecycle emissions by 30-50% compared to cast-in-place builds[3]Springer Nature, “System-based Greenhouse Emission Analysis of Off-Site Prefabrication,” springer.com. Eastern provinces now require carbon-impact statements during tendering, giving prefabricated bids a measurable compliance edge.

Rising Labor Costs & Safety Enforcement Boosting Factory Adoption

Average on-site wages rose 11% YoY in coastal hubs during 2024, while mandatory safety training and monitoring raised overheads for traditional contractors. Prefabricated factories report 30-50% lower accident rates, allowing insurers to cut premiums when modular methods are specified, further tilting the cost equation. Labor demographics amplify the shift because less than 10% of new vocational graduates choose on-site trades.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront CAPEX for <30 k m² projects | -1.1% | Nationwide, acute in tier-3 cities | Short term (≤ 2 years) |

| Non-uniform provincial certification | -0.8% | Nationwide | Medium term (2-4 years) |

| 40-year land-lease cycles for factories | -0.5% | Nationwide, private investors | Long term (≥ 4 years) |

| Developer liquidity crunch | -1.3% | Tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Upfront CAPEX vs. Conventional for <30 k m² Projects

Projects under 30,000 m² rarely achieve economy-of-scale pricing on molds and logistics, leaving a 15–25% component premium despite tax holidays and fee waivers[4]MDPI, “Capital Cost Factors in Prefabrication,” mdpi.com. Break-even shifts nearer 50,000 m², discouraging smaller private developers from adopting industrialized methods. Provincial subsidies mitigate but do not erase the gap because payments arrive only after field inspections certify assembly-rate targets.

Property-Developer Liquidity Crunch Delaying Prefab Factory Payments

Payment cycles lengthened beyond 180 days in 2024 as distressed firms such as Evergrande and Country Garden halted multiple sites, forcing suppliers to tighten credit windows. Smaller prefab plants with thin cash reserves now demand upfront deposits, limiting project starts and elevating bankruptcy risk among tier-3 contractors. Government relending quotas improve cash flow for completions, but confidence in the handover pipeline remains fragile.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Concrete Dominance Faces Timber Innovation

Concrete dominated with 58.40% China prefabricated buildings market share in 2025 due to entrenched supply chains and economical per-m² costs for mass housing. Timber CLT/LVL, however, is on track for a 7.45% CAGR, propelled by embodied-carbon credits and design flexibility valued by eco-conscious developers.

Chinese suppliers are piloting ultra-high-performance concrete (UHPC) that incorporates recycled aggregates and in-plant carbon-capture agents, aiming to protect margins against timber encroachment. Meanwhile, the Ministry’s 2025 guidance promotes structural steel and engineered timber in rural revitalization, signaling policy support for a diversified material mix.

By Application: Industrial Growth Outpaces Residential Base

Residential accounted for 53.65% of the China prefabricated buildings market size in 2025 on the back of large affordable-housing pipelines. Industrial and infrastructure builds are growing faster at a 7.19% CAGR thanks to semiconductor fabs, logistics hubs, and smart-city utility corridors that demand tightly controlled construction environments.

Hospitals and schools are also pivoting toward factory-made units after pandemic-era proof-of-concepts such as the 13-month Jinlong Prefab School in Shenzhen that hit 75% off-site content. Manufacturing projects benefit from reduced dust and vibration on precision lines, reinforcing the economic case for industrialized delivery.

By Product Type: Panelized Systems Challenge Modular Dominance

Modular blocks retained 53.25% market share in 2025, yet panelized and componentized systems will outpace them with 7.32% CAGR to 2031. Contractors seek site flexibility to address variable plot conditions without forfeiting factory productivity.

Broad Group’s 26-story tower erected in 5 days underscores speed advantages, but panelized packages cut transportation weight and crane requirements for mid-rise assets. Digital clone libraries within BIM platforms make late-stage design tweaks feasible, aligning with Shenzhen’s digital-twin verification rules.

Geography Analysis

Shanghai retained the largest China prefabricated buildings market share at 18.60% in 2025, supported by mature EPC ecosystems, deep-water port logistics, and municipal policies that fast-track factory-built high-rises. Its dense supplier base lets developers stage concrete, glass, and MEP modules within 24 hours of call-off, cutting on-site inventory costs and stabilizing project cash flows. Shenzhen’s 7.58% CAGR outlook reflects BIM-Digital-Twin mandates that reward contractors able to feed real-time production data into the city’s planning portal, while Guangzhou and Hangzhou benefit from e-commerce warehousing and tech-park expansions that rely on rapid shell delivery. Collectively, the eastern seaboard accounts for more than half of the China prefabricated buildings market size because integrated rail–road–port networks allow just-in-time component transfers at predictable shipping rates. Rising land prices in these hubs push developers toward taller, slimmer towers that suit modular cores.

In the north, the Beijing-Tianjin-Hebei cluster aligns planning codes so identical wall panels and bathroom pods can be swapped across jurisdictions without fresh certification, reducing re-engineering costs by up to 12%. Beijing’s affordable-housing drive channels high volumes into standardized six-to-nine-story blocks, keeping regional factories running at 80% utilization even during the property down-cycle. Adjacent Hebei cities host new steel-frame module plants that ship large volumetric units to the capital overnight, taking advantage of lower land rents and a direct expressway spine. Central provinces such as Hubei and Hunan are emerging as component export hubs; Broad Group’s Hunan base now supplies stair cores to projects in Shanghai and Chengdu within 48 hours by high-speed freight. These central nodes diversify the risk of coastal bottlenecks and spread economic gains inland.

Western provinces trail on penetration because sparse urban clusters raise per-unit logistics costs, yet Belt-and-Road power-plant and transport packages guarantee anchor orders for new factories, enabling a hub-and-spoke model that can scale over the decade. Local governments in Chongqing, Chengdu, and Xi’an offer discounted land leases and three-year tax holidays to lure investment in light-gauge steel and CLT lines, narrowing the delivered cost differential with the coast. Xinjiang and Qinghai award bonus procurement points to bidders that use at least 40% domestically sourced modular content, stimulating nascent regional supply chains. Nationwide, eastern regulators now require carbon-impact statements and digital-twin submissions during tendering, while several western agencies still rely on manual plan reviews, elongating approval timelines. Over 2026-2031, the alignment of certification rules and the rollout of inland freight-corridor subsidies are expected to spread adoption, anchoring long-term geographic balance in the China prefabricated buildings market.

Competitive Landscape

The competitive landscape in China’s prefabricated buildings arena remains highly fragmented despite the presence of several state-owned conglomerates that dominate conventional construction. Large integrated contractors such as China State Construction Engineering Corporation, China Railway Construction Corporation, and China Communications Construction Group operate national design-to-assembly platforms that give them cost advantages on megaprojects. Alongside these giants, diversified real-estate developers like Vanke and Country Garden have built captive module factories to secure supply and insulate projects from market disruptions. Hundreds of regional engineering, procurement, and construction firms still thrive by focusing on local government relationships, specialized materials, and quick-turn panelized systems that the bigger firms often ignore.

Digital transformation is the defining competitive axis, with leading players embedding BIM, digital-twin, and automated production scheduling into cloud-based workflows that link architects directly to robotic welding and cutting lines. Beijing Guli Technology’s PKPM-BIM suite has become a de-facto standard, and contractors that integrate its automated bill-of-materials feature can cut design iterations by up to 30%. Broad Group continues to differentiate on speed, demonstrating five-day assembly of a 26-story tower by prefabricating complete 12-meter volumetric units with pre-installed MEP systems. Timber innovators such as Dehua TB New Decoration leverage cross-laminated lumber expertise to win low-carbon public tenders, while steel specialists in Jiangsu deploy ultra-high-performance concrete facade panels to meet stringent fire codes. Partnerships with cloud-service providers, green-financing arms of state banks, and carbon-credit exchanges are emerging as pivotal enablers for firms looking to monetize sustainability benefits.

China Prefabricated Buildings Industry Leaders

-

China State Construction Engineering Corp. (CSCEC)

-

Broad Group

-

Vanke Industrialized Building

-

Beijing Urban Construction Group (BUCG)

-

CITIC Construction Prefab Division

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Shenzhen confirmed 4 million m² of prefabricated completions under its 2025 plan, a 35% YoY increase.

- January 2025: Beijing Guli Technology released PKPM-BIM with auto-generated BOM and sequencing simulation, reaching 81% assembly rates in Hunan dormitory pilots.

- November 2024: MOHURD issued digital public-infrastructure standards that embed prefab guidelines into smart-city frameworks.

- August 2024: Jiangsu streamlined fire-safety inspections for small projects, trimming approval times for prefab builds.

China Prefabricated Buildings Market Report Scope

The China Prefabricated Buildings Market covers the growing trends and projects in prefab building markets, like commercial construction, residential construction, industrial construction. The report also covers the industry along the type of material used, like concrete, timber, glass, metal, and other types. Along with the scope of the report also it analyses the key players and the competitive landscape in the China Prefabricated Buildings Market. The impact of COVID'19 has also been incorporated and considered during the study.

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Key Cities

| Shenzhen |

| Beijing |

| Shanghai |

| Hangzhou |

| Guangzhou |

| Other Key Cities |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Key Cities | Shenzhen |

| Beijing | |

| Shanghai | |

| Hangzhou | |

| Guangzhou | |

| Other Key Cities |

Key Questions Answered in the Report

How large is the China prefabricated buildings market in 2026?

The market stands at USD 69.74 billion in 2026 and is projected to reach USD 97.86 billion by 2031 at a 6.99% CAGR.

Which city shows the fastest prefabricated-construction growth?

Shenzhen leads with a forecast 7.58% CAGR through 2031, boosted by BIM-Digital-Twin mandates and aggressive quota targets.

What segment holds the largest share by material?

Concrete dominates with 58.40% market share in 2025, though timber CLT/LVL is the fastest-growing material segment.

How are carbon-neutrality goals affecting adoption?

Carbon-neutral policies favor factory-built methods that cut lifecycle emissions by 30-50%, giving prefabrication a regulatory advantage.

What is the main restraint on smaller projects?

Projects below 30,000 m² face a 15–25% cost premium due to limited scale economies, dampening adoption among small developers.

Who is the largest market player?

China State Construction Engineering Corporation leads the market, recording more than USD 300 billion in 2024 revenue and nationwide prefab capacity.

Page last updated on: