Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

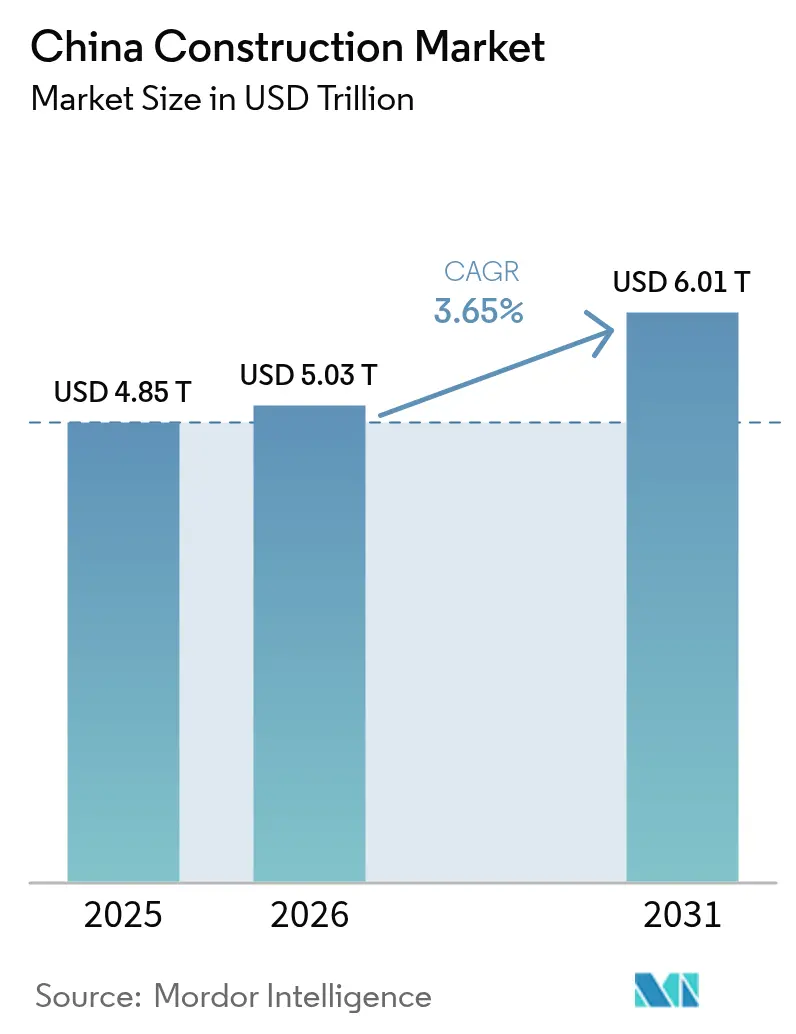

| Base Year Market Size (2025) | USD 4.85 Trillion |

| Market Size (2026) | USD 5.03 Trillion |

| Market Size (2031) | USD 6.01 Trillion |

| Growth Rate (2026 - 2031) | 3.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Construction Market Analysis by Mordor Intelligence

The China Construction Market size is expected to grow from USD 4.85 trillion in 2025 to USD 5.03 trillion in 2026 and is forecast to reach USD 6.01 trillion by 2031 at 3.65% CAGR over 2026-2031.

Robust public spending on underground utilities, sustained urbanization that is pulling millions into city centers, heightened digitalization of approvals, and spill-over demand from domestic Belt and Road Initiative (BRI) corridors are keeping project pipelines active despite property-sector turbulence. Public–private partnership models and infrastructure investment trusts are making it easier for non-state capital to participate in transport, energy, and urban renewal schemes. Technology adoption is quickening: building information modeling (BIM), robotics, and modular manufacturing are compressing schedules and reducing defects. At the same time, cost pressures from an aging workforce and stricter green-finance rules are compelling builders to rethink conventional on-site methods in favor of prefabrication. Regional activity is spreading westward as the government tries to balance growth, while market leaders lean on scale, integrated design-build expertise, and government ties to maintain their edge.

Key Report Takeaways

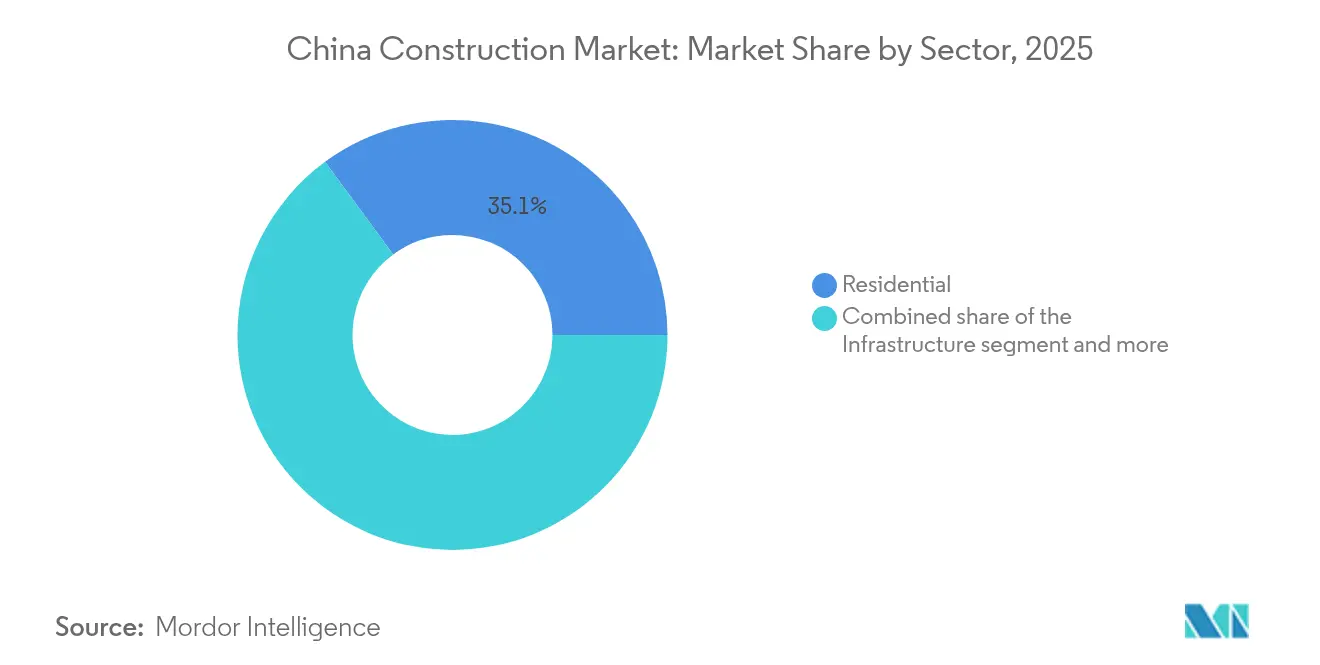

- By sector, residential led with a 35.10% China construction market share in 2025, whereas infrastructure is forecast to expand at a 5.41% CAGR through 2031.

- By construction type, new construction accounted for 77.05% of the China construction market size in 2025, while renovation is progressing at a 5.22% CAGR.

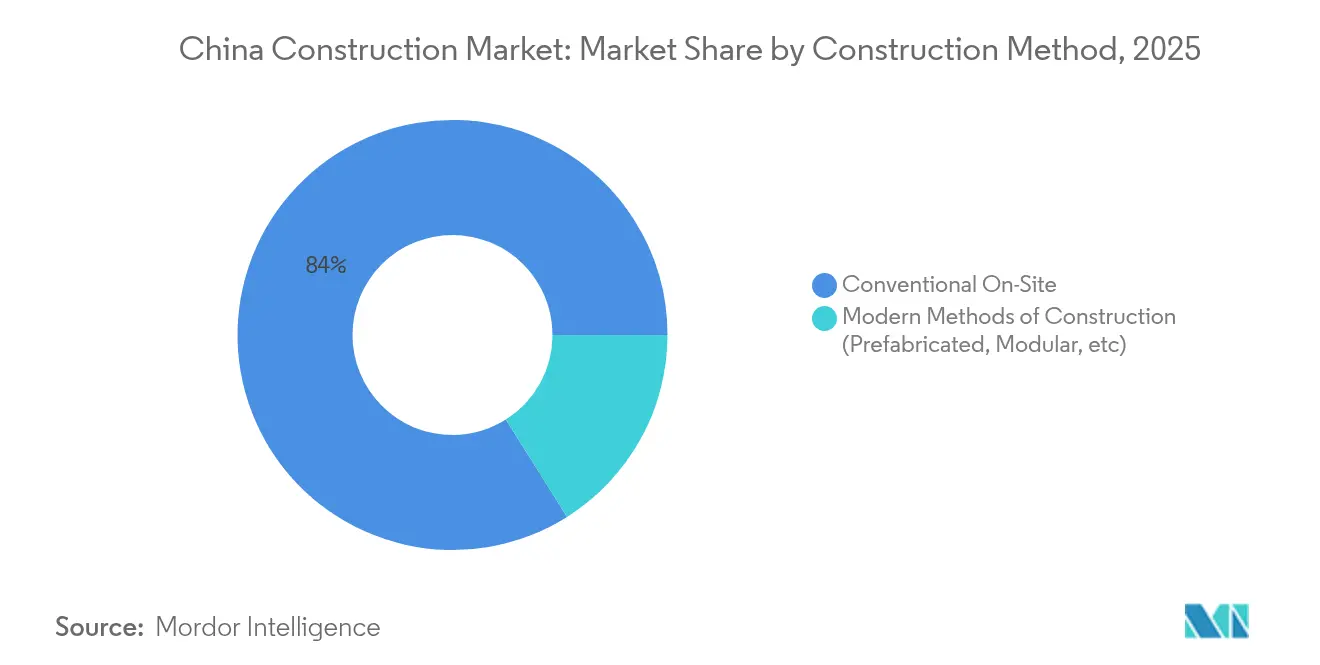

- By construction method, conventional on-site work held 83.95% of the China construction market size in 2025; modern prefabricated approaches are rising at a 6.05% CAGR.

- By investment source, public funding formed 62.05% of spending in 2025, yet private investment is advancing at a 5.45% CAGR.

- By geography, Jiangsu commanded 16.05% of the China construction market share in 2025, whereas the Rest of China grouping is set to climb at a 5.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government infrastructure stimulus packages | +1.2% | National; western and central provinces | Medium term (2-4 years) |

| Urbanization-driven housing demand | +0.8% | Tier-2 and Tier-3 cities; spill-over to county-level areas | Long term (≥ 4 years) |

| Digital project-approval platforms (BIM) | +0.6% | Tier-1 cities expanding to provincial capitals | Short term (≤ 2 years) |

| Domestic BRI corridor spill-over projects | +0.4% | Border provinces; western development zones | Medium term (2-4 years) |

| Mandatory prefabrication quotas | +0.3% | Beijing, Shanghai, Guangzhou, Shenzhen | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Stimulus Packages

China is channeling USD 571.4 billion into “hidden infrastructure” such as underground pipelines, gas grids, and heating networks. The program emphasizes disaster-prevention upgrades and smart-city technologies, which in turn favor contractors with advanced engineering, BIM, and IoT capabilities. Fixed-asset data show 5.6% year-on-year growth in infrastructure outlays during early 2025, with water-conservancy investments leaping 39.1%, underscoring strong near-term momentum. Local authorities must meet green-building codes, linking stimulus funding to energy-efficiency metrics and amplifying demand for high-performance materials[1]Chen Rui, “Press Conference on Infrastructure Investment Trends,” State Council Information Office, scio.gov.cn.

Urbanization-Driven Housing Demand

China’s five-year plan aims for a 70% urbanization rate, granting roughly 300 million migrant workers access to city services through hukou reform. The shift fuels a steady need for affordable apartments plus supporting hospitals, schools, and transit. Central and western provinces are now logging quicker urban growth than the coast, widening geographic demand. Policy directives prioritize inclusive, affordable homes, creating predictable workflows for builders skilled in standardized, low-cost designs[2]Li Wei, “Five-Year Action Plan for New Urbanization,” State Council of the People’s Republic of China, gov.cn.

Digital Project-Approval Platforms (BIM-Powered)

Digitized approval portals embedded with BIM cut review cycles from months to weeks while auto-checking compliance, clashes, and cost targets. Early adopters win bids faster and incur fewer rework penalties. As provincial governments roll out mandates, even mid-tier cities require BIM models, lifting baseline technology standards nationwide. The same datasets feed smart-city dashboards, making BIM a linchpin of broader digital transformation and ensuring sustained state backing.

Domestic BRI Corridor Spill-Over Projects

Rail lines, logistics parks, and energy infrastructure linking China to Southeast Asia and Central Asia demand extensive domestic groundwork. Border provinces are leveraging BRI corridors to justify high-spec highways, inland ports, and power grids, thus drawing construction deeper inland. Contractors meeting elevated technical specs for cross-border assets gain a reputational edge that carries over to public tenders elsewhere.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking local-government land-sale revenue | −0.6% | Tier-3 and Tier-4 cities; northeastern provinces | Medium term (2-4 years) |

| Persistent residential oversupply | −0.5% | Tier-3 and Tier-4 cities, notably in the northeast | Long term (≥ 4 years) |

| ESG-linked lending caps on carbon-heavy work | −0.4% | National; stricter in developed coastal regions | Short term (≤ 2 years) |

| Escalating skilled-labor costs | −0.3% | National; acute in coastal manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shrinking Local-Government Land-Sale Revenues

Land sales finance up to 30% of municipal budgets, but weaker housing demand in smaller cities is shrinking auction receipts and curbing funds available for new projects. Local authorities respond by delaying or downsizing public works pipelines, dampening near-term opportunities for contractors dependent on municipal orders. Fiscal reforms under discussion may diversify revenue streams, yet timelines remain uncertain, adding risk to bid pipelines[3]Gao Lei, “Budget Execution Report 2025,” Ministry of Finance, mof.gov.cn.

Persistent Residential Oversupply in Lower-Tier Cities

Inventory in many Tier-3 and Tier-4 markets exceeds 18 months of sales, making new starts commercially unviable. Developers pivot toward urban-renewal and fit-out work, which offers smaller contract values. Conversion of unsold units into subsidized rentals is underway, but absorbing excess stock will take years, keeping a lid on greenfield housing demand in affected regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Drives Long-Term Growth

Infrastructure captured 5.41% CAGR prospects, outpacing all other sectors as the state prioritizes transport links, water conservancy, and utility upgrades. Within the China construction market, residential retained a 35.10% share in 2025, backed by migrant-friendly housing subsidies. Industrial and logistics facilities are surging on e-commerce and supply-chain localization, while traditional office towers slow amid remote-work adoption.

Government outlays for the 158-km fully automated highway and the USD 571.4 billion hidden-infrastructure program underscore commitment to resilient networks. Renewables-ready grid projects and the Pinglu Canal add multi-year volume. Apartment blocks remain core, yet low-density villas around Tier-2 suburbs are gaining ground as commuters seek larger living spaces. Tight green-building rules steer both public and residential segments toward higher-spec insulation, boosting demand for energy-efficient materials.

By Construction Type: Renovation Gains Momentum

New construction commanded 77.05% of 2025 spend in the China construction market, yet renovations are forecast to climb 5.22% annually to 2031 as urban-renewal campaigns intensify. Multi-family retrofits improve energy performance and seismic safety, aligning with green bond eligibility and special-purpose bond issuance.

Owners favor renovation because prime city plots are limited and demolition carries social costs. Conversion of aging malls into mixed-use community hubs and office-to-apartment reconfigurations are examples of lucrative upgrades. Fiscally, renovations’ lower land-acquisition costs and quicker approvals translate into higher margins for specialist contractors versed in live-environment work. The China construction market size for large-scale retrofits is therefore expanding even faster than ground-up projects in mature metros.

By Construction Method: Prefabrication Transforms Industry

Conventional techniques still dominate China construction market with an 83.95% share, yet modular builds are rising at a 6.05% CAGR, catalyzed by mandatory quotas. Factory production cuts waste and halves on-site labor, which offsets skilled-worker inflation.

The China construction market is witnessing new joint ventures between developers and steel fabricators to secure in-house panel supply. Investment hurdles are high, but once plants reach volume, the cost per square meter drops below conventional builds. Government procurement is starting to score bids on prefabrication usage, effectively embedding the method into public works tenders.

By Investment Source: Private Sector Acceleration

Public capital delivered 62.05% of 2025 value in the China construction market, yet private investment is climbing 5.45% annually, buoyed by tax breaks and guaranteed-return models. Infrastructure investment trusts listed on domestic exchanges enable insurance funds and pension pools to back toll roads, warehouses, and data centers.

Developers previously reliant on presales are turning to equity partnerships with industrials seeking strategic facilities. While foreign direct investment has cooled, domestic private players fill the gap, intensifying competition and fostering innovation in project-finance structures. This ongoing shift is broadening funding diversity within the China construction market and tempering reliance on state budgets.

Geography Analysis

Jiangsu led with 16.05% of 2025 spend in the China Construction Market, reflecting its role in the Yangtze River Delta manufacturing belt. Projects span advanced-manufacturing parks, logistics hubs linked to Shanghai’s ports, and eco-friendly urban renewals in Suzhou and Changzhou. Early adoption of prefabrication plants gives local firms an edge in meeting Tier-1 performance codes.

Guangdong and Zhejiang remain heavyweights but now focus on quality-oriented builds. Guangdong’s Greater Bay Area plan bundles metro extensions, cross-harbor tunnels, and airport expansions that underpin demand through 2030. Zhejiang’s private-enterprise dominance generates steady industrial and warehouse requirements, while heritage-district restorations in Hangzhou showcase high-end renovation skill sets.

The Rest of China grouping is projected for the fastest 5.35% CAGR as central directives push funds toward the west and northeast. High-speed rail spines, provincial highways, and county-level water treatment plants are unlocking latent demand. Remote areas also host BRI-linked inland ports and energy corridors, spreading the footprint of the China construction market well beyond historical coastal centers.

Competitive Landscape

State-owned giants China State Construction Engineering Corporation, China Railway Group, China Railway Construction, Power Construction Corporation of China, and China Communications Construction collectively controlled over 80% of mega-project awards in 2024. Scale provides procurement leverage, captive design institutes, and preferential credit lines, enabling them to underbid smaller rivals on turnkey civil packages.

In the China Construction Market, Technology now shapes differentiation. The 158-km robot-built highway proved that integrated drones, 3D printing, and AI-coordinated plant fleets can deliver 24/7 production with reduced injuries. Firms investing in data-driven site management and carbon-tracking dashboards secure ESG-linked loans at lower spreads.

Private contenders concentrate on niche high-margin arenas such as data-center campuses, electric-vehicle charging corridors, and façade retrofits. Several have partnered with tech start-ups offering digital twins and modular plug-ins, allowing lean teams to compete for smart-city pilot zones. International contractors remain minor players due to stringent localization rules, yet joint ventures in specialized tunneling and deep-sea bridgework persist where local experience is limited.

China Construction Industry Leaders

China State Construction Engineering (CSCEC)

China Railway Group (CREC)

China Railway Construction (CRCC)

China Communications Construction (CCCC)

Power Construction Corporation (PowerChina)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Ministry of Housing and Urban-Rural Development issued stricter national residential standards mandating 3-m ceiling heights and elevators from four stories upward.

- December 2024: Beijing confirmed USD 571.4 billion for hidden-infrastructure upgrades over 2025-2029, focusing on pipelines and urban resilience.

- August 2024: The National Development and Reform Commission launched an urban-renewal and safety-resilience plan centered on disaster-prevention and smart-city tech.

- July 2024: The State Council released a five-year people-centered urbanization roadmap targeting 70% urban residency and hukou reform.

China Construction Market Report Scope

Construction is the installation, maintenance, and repair of buildings and other stationary structures, as well as the construction of roadways and service facilities that form fundamental components of structures and are required for their operation.

The China construction market is segmented by sector (residential, commercial, industrial, infrastructure - transportation, energy, and utilities).

The report provides market size and forecasts in value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Jiangsu |

| Guangdong |

| Zhejiang |

| Beijing |

| Shanghai |

| Rest Of China |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Jiangsu | |

| Guangdong | ||

| Zhejiang | ||

| Beijing | ||

| Shanghai | ||

| Rest Of China | ||

Key Questions Answered in the Report

What is the current value of the China construction market?

The market is valued at USD 5.03 trillion in 2026 with a forecast to reach USD 6.01 trillion by 2031.

Which segment is growing fastest through 2031?

Infrastructure projects are projected to expand at a 5.41% CAGR, outpacing all other segments.

How large is prefabrication within China’s construction activity?

Conventional work still holds 83.95% share, but prefabricated methods are rising at a 6.05% CAGR, helped by Tier-1 city quotas.

Which province contributes most to construction spend?

Jiangsu leads with a 16.05% share owing to its strong manufacturing base and urban-renewal programs.

How is private capital participating in Chinese construction?

Private investment is advancing at a 5.45% CAGR through 2031, supported by infrastructure trusts and favorable tax policies.

Page last updated on: